Abstract

The goal of this study is to assess the industry effects of monetary policy transmission channels in Nigeria within the period 1981-2014. Techniques of analysis employed in the study are the Johansen cointegration and the error correction model (ECM). Our regression estimates reveal that the private sector credit, interest rate, and exchange rate channels have negative effects on real output growth, both in the long run and in the short run. The results further show that, relatively, the degrees of the established effects are higher in the long run than in the short run. We employed the Johansen cointegration approach to determine the nature of relationship that exists between our dependent variable and the independent variables. The results show that, in the Nigerian case, monetary policy transmission channels jointly have a long-run relationship with real output growth of the industrial sector, and disequilibrium in the system is corrected at the speed of 72.2% annually.

Keywords

Introduction

Monetary policy action is the prerogative of the central bank and monetary authorities. It involves the process of controlling the cost, value, and availability of money and credit in other to achieve the desired level of prices, employment, output, and other economic objectives. Monetary policy can be used to influence economic activities and achieve economic objectives of a country. The stance of monetary policy, however, can be either expansionary or contractionary. Expansionary monetary policy stance is a situation whereby the monetary authority increases the supply of money in the economy with the aim of reducing the cost of money (interest rate) and stimulating economic activities. However, a contractionary policy entails the reduction in money supply which potentially increases the cost of money and slows the pace of economic activities.

The choice of any stance to be adopted by the central bank depends on the state of the economy at any time and the policy target of the government. But, finding a trade-off between the attainment of price stability and growth is often difficult. By setting annual monetary growth targets, the central bank intends to assert its commitment to price stability or inflation control. However, in reality, money growth might be consistent with economic growth but not with the stability of prices; in other words, although the economy is stimulated, inflation could at same time escalate. Regarding achieving price stability, Bernanke, Laubach, Mishkin, and Posen (1999) emphasize that an inflation targeting country may not wring inflation out of their economies without laying itself open to costs in lost output and rising unemployment. Moreover, monetary growth target might lead to achieving price stability but might not result in the attainment ofaccelerated growth. It is a herculean task finding a balance or trade-off between set goals (Khan & Jacobson, 1989). Epstein (2007) asserts that limiting monetary policy exclusively to price stabilization cannot guarantee improved economic growth because low inflation does not necessarily give rise to high and steady economic growth.

Over and above, the primary goal of monetary policy is to ensure that money supply is at a level that is consistent with the desired growth rate.

Although no economy is self-sufficient, most economies of the world strive for self-reliance. The successful ones are often those that have a deepened economy with soaring economies of scale, which can take an economy steps farther from economic growth to economic development. Good infrastructural development combined with favorable business and political environment supports the creation of value and increase in the production of goods and services. And, certainly, the monetary authorities are always there to harness the overall mechanism by formulating policies that will promote growth and stability in the economy. Although economic theory and quite a few empirical analyses support the fact that monetary policy influences output, the efficient conduct of monetary policy is crucial (Ćorić, Perović, & Šimić, 2012).

Nigeria is a mono-cultural economy, depending on oil as the mainstay of the economy and foreign exchange earner. Most studies that evaluated monetary policy effects usually equate policy measures against the overall economy. Formulating future policies based on aggregated perspective on the economy might not be entirely misguided but would ultimately hide vital details that could have given a more stable and target-oriented policy designs. Therefore, in a country that chimes mantra for economic diversification, it is necessary to disaggregate the economy and assess the effect of key monetary policy channels on the “preferred” industrial sector. Most of the existing studies have examined transmission effect vis-à-vis the aggregate economy hence creating a gap in the frontiers of knowledge regarding the sectoral effects of monetary policy transmission. There is, however, dearth of literature to explain the real output response, from a disaggregated point of view to monetary policy transmission in Nigeria. To this end, the need to fill such knowledge gaps informed the choice for this study which examines the linkage between monetary policy transmission and industrial sector growth in Nigeria.

Review of Related Literature

According to Toby and Peterside (2014), a monetary policy shift tends to transmit a change for the future in the projected behavior of macroeconomic variables. The traditional economic analysis considers the response of monetary policy makers as exogenous. As explained by this system, money is unbiased in its effects on the economy. Thus, in the classical theory, transmission mechanism reacts directly and indirectly. The direct mechanism is based on the demand for and supply for money, whereas the indirect mechanism has linkage with the banking system and operates through money and interest rate. The Keynesian theory explains that a change in money supply has effects on total expenditure and output level through the changes in interest rate. Hence, the system operates indirectly. The monetarists affirm that although monetary expansions affect output and employment in the short term, interest rate and prices are influenced in the long run (Chaudhry, Qamber, & Farooq, 2012).

Monetary Policy Transition Mechanism

Interest rate channel (INT) and credit channel (CRDT) are considered in some literature as the key propagation and strengthening mechanisms of monetary policy changes. Both types of transmission channels hold the prediction that any variation in bank lending is dependent on monetary policy actions. In other words, a change in bank lending is predicted to be in response to change in monetary policy stance. Because monetary policy hinges chiefly on the supply of money, it will be remiss and abnormal to ignore the role of banks, especially in the money creation process. Hence, the CRDT perspective portends that monetary policy induces movements in bank lending vis-à-vis changes in bank loan supply, whereas shifts in the demand for a bank loan is explained by the INT (Arnold, Kool, & Raabe, 2006). The Nigerian industrial sector faces insurmountable challenges ranging from infrastructural woes to highly unstable business environment. Also, the cyclical nature of industrial output equally intensifies the need for external financing. Bridging the funding gap depends mainly on both availability and cost of fund, which is largely determined by money supply through monetary policy action.

Writing on monetary policy transmission mechanism, Friedman and Schwartz (1963) argue that when the central bank pursues an expansive open market operation, money stock will increase thereby leaving the deposit money banks with fat reserves and enhance their ability to create credit and extend loans and advances, which will increase the money supply. Besides the sale and repurchase of financial instruments like treasury bills to regulate the quantity of money in circulation, the central bank may also decide to use other monetary policy instruments such as rediscount rate or the reserve requirements (liquidity and cash ratio) to achieve the desired economic objectives of output growth, stable price level, and full employment. The industrial sector and other activity sectors stand to benefit from expansionary policy measures (for instance, increase in money supply and reduction of rediscount rate). Although this will promote production through cheaper cost of fund (interest rates), it could turn quite inimical to achieving price stability. On the contrary, a stringent policy, using any appropriate instrument, can help to attain a stable price level but could lead to a recession.

Economists established the general relationship between real output and monetary policy transmissions. From the Keynesian point of view, an unrestricted change in money stock influences real output by bringing down the interest rate, which by efficient utilization of capital will stimulate investment and the real output growth (Athukorala, 1998). Some macroeconomists, however, have a different opinion. They promoted the theory of financial liberalization and argued that if the market forces prompt interest rate to rise, savings would be channeled to the productive investments thus stimulating growth in real output (Mehdi & Reza, 2011). In the overall process, the banking system stands as the key conduit of monetary policy transmission, which draws attention to the CRDT effects of monetary policy in Nigeria. In light of any expansionary policy, therefore, it is expected that it will have indirect positive effects on industrial activities as the cost of borrowing (to finance production or expansion) will fall. Ceteris paribus, the theoretical expectation is that the low cost of fund prompts the makings for an increase in national income via the stimulation in economic activities.

Trend Analysis

A cursory look at the money supply growth and the industrial sector growth in Nigeria from 1981 to 2014 reveals undulating movements over the years, where on average, the money supply growth and the industrial growth rate were 48.08% and 26.67%, respectively. Because the industrial sector is made up of some subsectors, we shall use a few charts to analyze the trends of the money supply, and the characteristics of the industrial sector as well as the various subsectors it comprises.

Figure 1 reveals unstable trends and indicates that money supply, descriptively, does have a significant influence on the pace of industrial advancement. Substantial decreases in money stock have at some years found to have an adverse impact on the growth of the industrial sector, whereas at other points increases in the money supply do not produce a corresponding commensurate increase in the growth of the industrial sector. From the chart above, it can be observed, for instance, that money supply decreased from 10.9% in 1985 to 6.8% in 1986 resulting in a proportionate decline in industrial growth from 22.1% in 1985 to −4.9%. Money growth fell from19.7% in 1989 to 15.2% in 1990 equally lead to negative growth in 1990 from 47.5% in 1989 to −32.4% in 1990. Moreover, such other years (1997, 1998, 2001, 2004, 2009, and 2013) that recorded significant cuts in broad money supply all had corresponding negative growths of the industrial sector except for 2004. In 2004, the growth rate was a paltry 0.44%, which could be attributed to a decline in money growth from 29.7% in 2003 to 9.2% in 2004. The industrial sector had a relative positive response to money growth over the period under study except in 2001, where an increase in money supply from 39.7% in 2000 to 44.5% in 2001 resulted in −19.0% decline in the industrial sector growth in 2001.

Trend analysis of money supply growth and industrial sector growth relationships in Nigeria between 1981 and 2014.

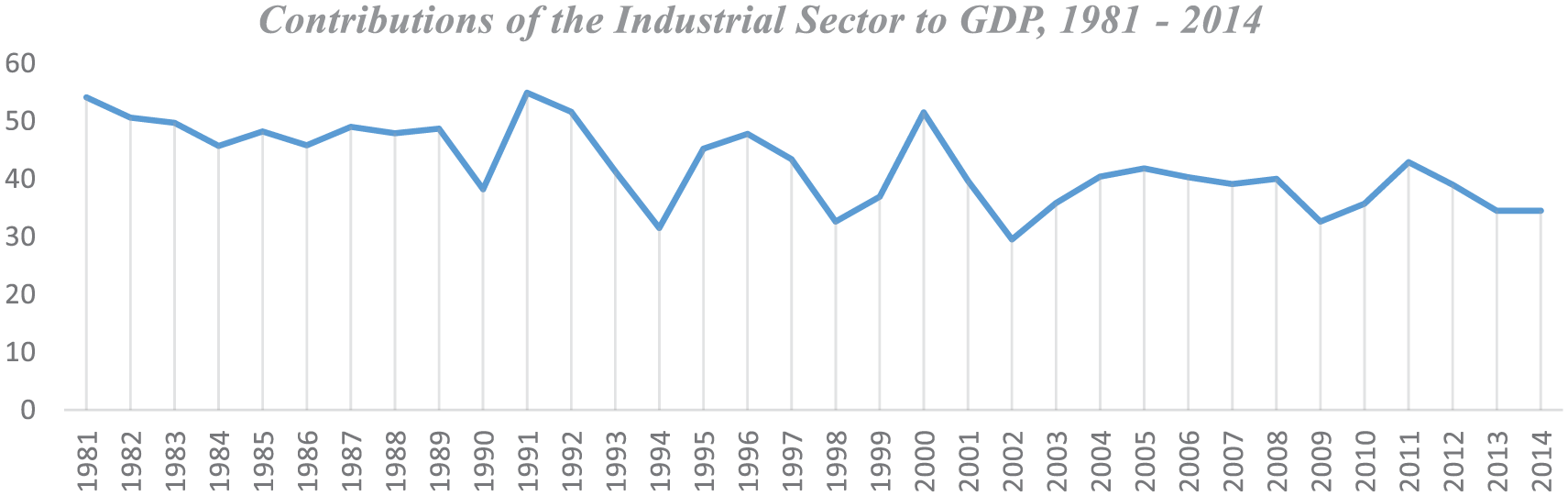

We observe from the Figure 2 that industrial sector contributions to the Nigerian economy was consistently significant and trended with relative stability in the 1980s until it dipped by 10.5% in 1990, from 48.7% in 1989 to 38.2% in 1990. Since rising to an all-time high of 54.9% in 1991, the trend fluctuated visibly but averaged 40.3% between 2004 and 2014.

Trend analysis of the industrial sector contributions to GDP in Nigeria between 1981 and 2014.

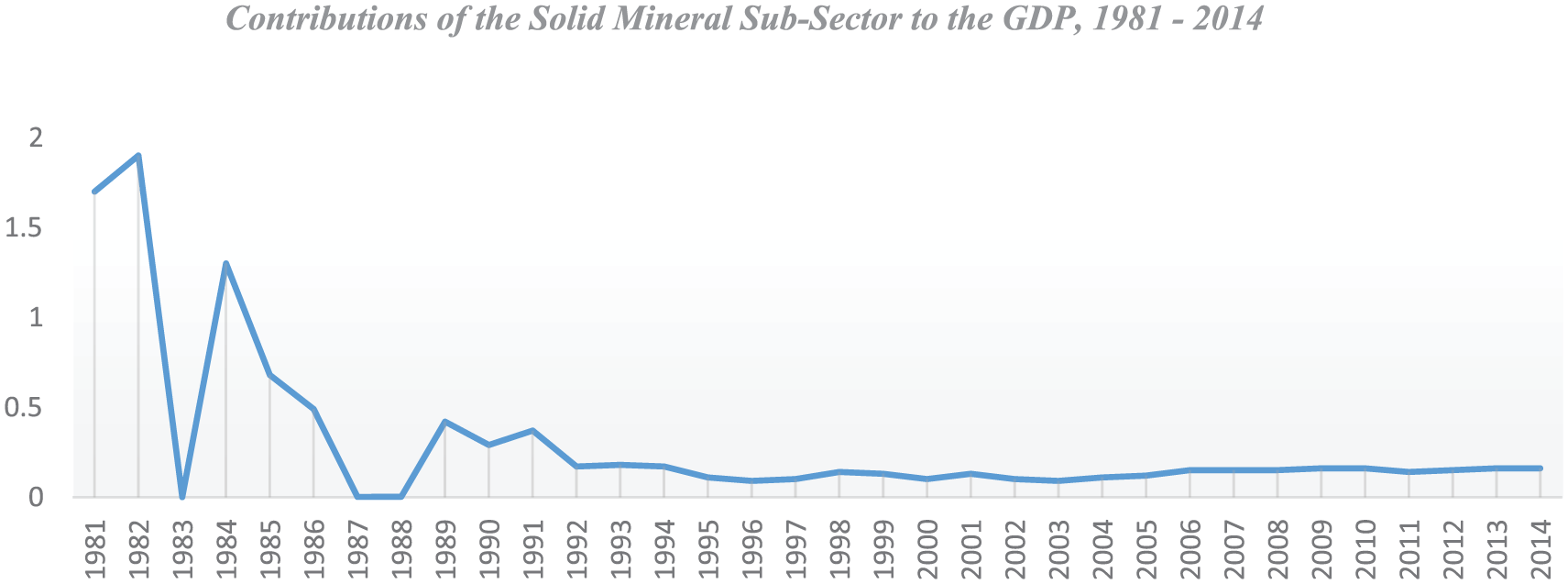

To avoid a general assumption based on the performance of the industrial sector, we have disaggregated this sector into various subsectors that constitute the industrial sector. The sum of the contributions of each of these sectors in any given year equals the input of the industrial sector for that particular year. Therefore, breaking it down further will help us understand what the exact contribution of each subsector to the gross domestic product (GDP) is. These are explained in Figures 3 to 5.

Trend analysis of the manufacturing subsector contributions to GDP in Nigeria from 1981 to 2014.

Trend analysis of the solid mineral subsector contributions to GDP in Nigeria between 1981 and 2014.

Trend analysis of crude petroleum and natural gas contributions to GDP in Nigeria between 1981 and 2014.

Figure 3 reveals that the manufacturing subsector fared well in the 1980s and was the highest contributor to industrial sector performance during this period. It is worthy to emphasize that the subsector recorded 33.6%, 36.4%, 33.0%, and 35.1% in 1981, 1982, 1983, 1984, and 1985, respectively. However, as the economy began to depend on crude oil and natural gas, activity in the manufacturing sector dwindled, and Nigerian economy changed from an export-based economy to an import-dependent economy. As a result, the impact of the manufacturing subsector on the economy fell consistently, without meaningful recovery, from 12.4% in 1990 to 1.9% in 2014.

Figure 4 demonstrates similar trend over the years as Figure 3. However, in absolute terms, as can be observed from the scaling, the solid mineral subsector contributions to GDP have been quite negligible and has never made up for a 2% input to the composite industrial sector contribution and the GDP in any particular year. In fact, its best influence was a 1.9% input in 1982. Between 1989 and 2014, the impact of solid mineral averaged 0.13%. This further explains the neglect of this subsector as oil exploration gained momentum and “oil-money” crowded out the attention given to other subsectors that used to be the mainstay of the Nigerian economy.

Figure 5 depicts that the crude petroleum and the natural gas trend has a reverse characteristic compared with other subsectors analyzed earlier. The lowest contributions were in the 1980s, contrary to the manufacturing and solid mineral subsectors, and trended highly and positively from 1990 to 2014. The reason is not farfetched. As oil revenue trickled in the late 1980s, the nonoil subsectors, which hitherto used to be the highest contributor and foreign exchange earner, were neglected, hence the downward trend observed from the early 1990s to date.

Figure 6 descriptively explains the responsiveness of monetary policy transmission channels to industrial sector size (INDSZE), which is measured as the percentage of industrial sector real output to GDP at current basic prices, where EXR is the exchange rate channel, MPR is the monetary policy rate, LTR is the commercial banks lending rate, TBR is the treasury bill rate, CPSGDP is the ratio of private sector credit to GDP, M2GDP is the ratio of broad money supply to GDP, and INDSZE is the industrial size. From the graph, it appears that a change in industrial sector output (which is real value added [RVA]) is a function of changes in some transmission channels. The relationship between RVA and each of the channels of transmission seems to be relative other than absolute.

Trend analysis of monetary policy transmission channels and industry size in Nigeria, 1981-2014.

Empirical Reviews

A look at existing empirical studies will provide further insights into the dynamics of monetary policy and growth. The effectiveness of the various monetary policy channels in stimulating economic growth remains debatable. Owolabi and Adegbite (2014) used multiple regression to examine the impact of monetary policy on industrial growth in the Nigerian economy, covering the period of 1970-2010. The study found that rediscount rate and deposit have significant positive effect on industrial output, whereas treasury bills do not have a positive impact on industrial output.

Arnold et al. (2006) studied the industry effects of bank lending in Germany. The dynamic panel data models indicated that both bank lending and monetary policy have a strong influence on industrial growth Olorunfemi and Dotun (2008) used simple regression to assess the impact of monetary policy on the economic performance in Nigeria. The results indicate that both interest rate and inflation have a negative relationship with GDP.

Ćorić et al. (2012) explored the effects of a monetary policy shock on output and prices. Results of the structural vector autoregression (VAR) model suggested that economic size and industry size (share of industry in GDP) are among that factors critical for the effects of a monetary policy shock.

Peersman and Smets (2002) estimated the effects of monetary policy change on output growth in seven euro area countries between 1980 and1998. The results revealed that the adverse impact of an interest rate tightening has greater negative and significant effect on output in times of recession than in booms. However, the study underscored the overall impact of cross-industry heterogeneity as well as information asymmetry vis-à-vis overall policy effects.

Yakubu, Barfour, and Shehu (2013) investigated the effectiveness of monetary-fiscal policies on price and output growth in Nigeria. Variance decomposition and impulse response function for Vector Error Correction Model (VECM) captured the correlation among variables. The results suggested that money supply and government revenue have a greater positive influence on prices and output in the long run.

Chaudhry et al. (2012) investigated the relationships between monetary policy, inflation, and economic growth in Pakistan over the period of 1972-2010 using co-integration and causality analysis. The results show that credit to private sector, real exchange rate, and budget deficit are significant variables that influence the real GDP in Pakistan. The pairwise Granger causality results suggest a bidirectional causality between real GDP and real exchange rate, whereas unidirectional causality run from real GDP to money supply, domestic credit, and budget deficit.

Ghosh (2009) used a VAR model to the interlinkage between a monetary policy shock and real industry output in India. The findings indicate that industries show differential response to a monetary tightening and both interest rate and financial accelerator variables appear to be central in explaining the differential response.

Using an equilibrium-correction model is estimated, the findings in Ryan-Collins, Werner, and Castle, (2016) suggested short-term and long-term interest rates and broad money do not appear to influence nominal GDP significantly. VAR estimate revealed that the real economy credit growth variable is strongly exogenous to nominal GDP growth (see also Grigoli, Herman, Swiston, & Bella, 2015; Kandil, 2014; Rosoiu, 2015a).

Afonso, Araújo, and Fajardo (2016) argue that the processes involved—from the formulation of then monetary instruments to their implementation and consolidation in developing countries—are often carried out in response to a succession of internal and, principally, external crises. Besides, Leith, Moldovan, and Rossi (2015) contend that in developing economies, the presence of deep habits at empirically estimated levels can imply large externalities that significantly affect the conduct of monetary policy.

Moreira, Chaiboonsri, and Chaitip (2016) applied the Markov-switching models and a Bayesian VAR to verify empirical linkage between expected and effective short-term interest rates in Brazil. The main findings support the theoretical idea which argues that Central Bank can smooth adjustments of effective short-term interest rates, given that these last ones have effects on expected short-term rates, thereby influencing long-term interest rates, which are essential for controlling output activity and price changes. Also, the MS-models showed that the magnitude or significance of these empirical relationships is more under a “higher response regime.” Similarly, Partachi and Mija (2015) emphasized that MPR influences the direction of the national economy and stimulates interest for refinancing banks as they require more loans, used for lending to the economy, thereby stimulating economic activities and fostering sustainable growth (see Donath, Veronica, & Oprea, 2015; Jain-Chandra & Unsal, 2014; Lerskullawat, 2017; Matemilola, Bany-Ariffin, & Muhtar, 2015; Rosoiu, 2015b; Wulandari, 2012).

Kalu (2017) analyzed the nature of the relationship between monetary policy and private sector credit in Nigeria. The cointegrating regression results revealed evidence of a long-run relationship between monetary policy and credit to private sector. The long-run parameter estimate stability tests support cointegration in the presence of structural breaks. On the contrary, error correction model (ECM) results showed that changes in credit have positive and significant short-term influence on changes in monetary policy. The findings further indicate unidirectional causality running from credit to monetary policy.

Fu and Liu (2015) investigated the monetary policy effects on corporate investment adjustment, using a sample of China’s A-share listed firms within the period 2005 and 2012. The results showed that corporate investment adjustment is faster in expansionary than contractionary monetary policy periods. The study showed that an increase in the growth rate of money supply or credit accelerates adjustment. The monetary channel was also found to have significant asymmetry, whereas the CRDT has none.

Data and Method

The research design for this study is ex post facto, because the events we are studying had already taken place. This design can also be referred to as comparative research, which is applicable for studies geared toward ascertaining the cause–effect association between the independent and dependent variables (Onwumere, Onodugo, & Ibe, 2014). Determining cause–effect relationships among our selected variables is the major aim of this study; hence, our data are of secondary nature, collated from the Central Bank of Nigeria (CBN) Statistical bulletins for various years, covering the period 1981-2014. The annualized time series data will be analyzed using the ECM, whereas the Johansen cointegration approach will be employed to test for the long-run relationship among the series. In other words, the underlying assumption is that all variables are integrated of Order 1 or I(1). The speed of adjustment will be ascertained based on the ECM and will be able to tell us the rate at which the previous period disequilibrium is adjusted toward equilibrium path on an annual basis.

Model Specification

It is our aim to derive the output effect of monetary policy transmission channels. To achieve this, we estimate for the industry the linear regression equation:

where Y is the real output (measured as annualized percentage contribution of the industrial sector to GDP), CRDT is the credit channel (measured as the ratio of private sector credit to GDP), INT is the interest rate channel (this is the real lending rate), and EXR is the exchange rate channel.

Equation 1 is our baseline long-run model for determining the industry effects of monetary policy transmission in Nigeria.

It has been vastly buttressed in recent literature of financial econometrics that upon the establishment of a long-run relationship, there is need to integrate a model which accommodates for short-run dynamic adjustment process, which is the speed of adjustment from short-run disequilibrium to long-run equilibrium. Based on this, we developed ECM by modifying Equation 1 as follows:

where ∆ denotes change; i and j are lag lengths; n is number of lags; δt−1 is the error correction term (ECT) (and speed of adjustment), which is integrated at Order 0, 1(0); β0 is the constant term; β1–β6 are coefficients; and μ t is the error term.

The Johansen cointegration will be employed to test for the cointegrating relationship among the variables given the fact that all our series are stationary after first differencing (i.e., at Order 1). However, in a situation where some of the variables have unit root, we will have to develop the Autoregressive Distributed Lag (ARDL) or Bound Test model for co-integration which merges the two steps suggested by Engel and Granger (1987) into a one-step function. The model substitutes

Equation 3 is arrived at by solving for δ t in Equation 1 and then lagging the outcome by one period. The result is substituted for ät−1 in Equation 2 to arrive at Equation 3.

Results and Analysis

Unit Root Test

The result in Table 1 indicates that the variables attained stationarity at the same orders of integration. Y, CRDT, INT, and EXR are stationary at first difference, I(1). When the order of integration among variables are all I(1), the appropriate technique for cointegration testing is the Johansen cointegration test; otherwise, the ARDL would apply. Hence, we use this approach to ascertain a long-run relationship among our variables.

ADF Unit Root Test Result.

Source. Kalu (2017) and Lerskullawat (2017).

Note. ADF = Augmented Dickey-Fuller; Y = real output (measured as annualized percentage contribution of the industrial sector to GDP); GDP = gross domestic product; CRDT = credit channel (measured as the ratio of private sector credit to GDP); INT = interest rate channel (this is the real lending rate); EXR = exchange rate channel.

Model Estimations

The results reported in Table 2 reveals that CRDT, INT, and EXR jointly have a long-run relationship with the real industrial output (Y). We observe that there are four cointegrating equations. For our purpose, we are interested in the variables moving together, hence jointly in the long run. Given this finding, we shall estimate the long-run industry effect of monetary policy based on our baseline model and, after that, apply the ECM to determine the speed of adjustment toward long-run equilibrium.

Result of Johansen Cointegration Test for a Long-Run Relationship.

Note. Trace and Max-eigenvalue tests indicate four cointegrating equations at the .05 level. Y = real output (measured as annualized percentage contribution of the industrial sector to GDP); GDP = gross domestic product; CRDT = credit channel (measured as the ratio of private sector credit to GDP); INT = interest rate channel (this is the real lending rate); EXR = exchange rate channel; CE(s) = cointegrating equations.

Denotes rejection of the hypothesis at the .05 level.

MacKinnon–Haug–Michelis (1999) p values.

The results in Table 3 indicate that CRDT, INT, and EXR have a negative influence on real industrial output (Y). A unit change in credit to the private sector leads to 24.1% decline in real output (Y). When INT rises by 1%, real industrial output falls by 37.2%. Therefore, an increase in interest rate is expected to raise the cost of funds and slow down economic activities. This outcome supports one of the theoretical foundations of this discourse that interest rate is negatively related to real output. However, the evidence on private sector credit does not support the a priori expectation which states that credit to the private sector has a direct influence on real output. Exchange rate equally has a negative but nonsignificant effect on Y.

Estimate of Long-Run Effect Based on Baseline Model.

Source. Kalu (2017) and Lerskullawat (2017).

Note. Prob(F statistic) = .000232, R2 = .86, Adjusted R2 = .74, DW = 1.796801. CRDT = credit channel (measured as the ratio of private sector credit to GDP); GDP = gross domestic product; INT = interest rate channel (this is the real lending rate); EXR = exchange rate channel; DW = Durbin–Watson.

The regression estimate in Table 4 reveals that all the regressors exert negative influence on industrial sector output. This result shows that monetary policy has relatively the same effect on output both in the long run and the short run. It is worthy to note that the negative influence of INT on Y is of less magnitude in the short run—a unit change in leads to 0.24% decline in real output, but the effects get more significant in the long run at 37.2%. The ECT has the right sign and is significant at 5%. The ECT indicated the speed of adjustment toward long-run equilibrium. The result, therefore, shows that 72.2% of the deviation from equilibrium path is corrected on an annual basis.

Short-Run Estimate Based on Error Correction Model.

Note. Y = real output (measured as annualized percentage contribution of the industrial sector to GDP); GDP = gross domestic product; CRDT = credit channel (measured as the ratio of private sector credit to GDP); INT = interest rate channel (this is the real lending rate); EXR = exchange rate channel; ECT = error correction term; DW = Durbin–Watson.

Validity and Stability Tests

In the results reported in Table 5, Breusch–Godfrey Serial Correlation Lagrange multiplier (LM) Test indicates that our model has no serial correlation. This confirms the result of Durbin–Watson (DW) result in Table 3 which shows the same result. The second test for heteroskedasticity reveals that our model is homoskedastic. These results are desirable and confirm that our overall results are not spurious hence reliable.

Serial Correlation and Heteroskedasticity Tests.

Source. Kalu (2017) and Lerskullawat (2017).

The p values of the t test, F statistics, and the Likelihood ratio in Table 6 show that the null hypothesis that the model is correctly specified is accepted. This also indicates that the model does not have any specification error. This result is confirmed by the Cumulative Sum Control Chart (CUSUM) test below.

Ramsey RESET Test.

Source. Kalu (2017) and Lerskullawat (2017).

Note. RESET = Regression Equation Specification Error Test; Y = real output (measured as annualized percentage contribution of the industrial sector to GDP); GDP = gross domestic product; CRDT = credit channel (measured as the ratio of private sector credit to GDP); INT = interest rate channel (this is the real lending rate); EXR = exchange rate channel.

The graph in Figure 7 shows that our model is stable. Its stability is explained with the blue line within the upper and lower bound red lines. The above plot remaining within the critical bounds of the 5% significance level also reveals that our model is correctly specified.

Recursive estimate’s CUSUM test.

The normality test result is presented in Figure 8. The result shows that the series are normally distributed as indicated by the p value of the JB statistic.

Histogram normality test.

Conclusion and Recommendations

Variation in monetary policy stance is expected to have an effect on industrial sector productivity. Determining the appropriate policy of choice remains the role of the central bank that sets policy targets and determines transmission channels that will produce expected result. This study was aimed at ascertaining the industry effects of monetary policy and find out whether monetary policy transmission channels jointly have a long-run relationship with industrial output growth in Nigeria. Our baseline regression result reveals that the private sector CRDT, INT, and the EXR all have a negative effect on real output growth (Y). The ECM estimate relatively corroborates the above findings. However, the degree of responsiveness of Y to changes in the monetary policy was found to be higher (or more significant) in the long-run compared with the short-run dynamics. For instance, 1% change in INT caused Y to fall by 0.24% in the short run and by 37.2% in the long run. Same unit change in EXR leads to 3.9% decline in Y in the short run and 12.9% fall in the long run. The magnitude of effect of CRDT on Y appears stable both in the long run and short run at 24.07% and 24.09%, respectively. Moreover, the Johansen cointegration test results indicate that monetary policy transmission channels jointly have a long-run relationship with industrial output growth. This finding was confirmed by both the Trace and the Max-Eingen tests. The ECM result further confirmed the cointegrating association and revealed a speed of adjustment of 72.2%. This implies that disequilibrium in the system is corrected at the rate of 72.2% annually. Based on the findings, we recommend that credit should be made available to the productive sectors of the economy at a competitive rate with adequate monitoring. Concerted efforts toward effective guidelines and supervision are also recommended to ensure that credit is not diverted to unproductive sector of the economy. The key implication is that private sector credit, interest rate, and exchange rate are effective channels for monetary policy transmission in Nigeria, and a policy action should be put in place to effectively harness these key channels to stimulate the real sector of the economy and boost economic activities. It is therefore important that the monetary authorities consider these variables as major channel for monetary policy implementations. Another critical policy implication is that rising interest rate stifle growth and the policy makers must take policy actions to stabilize MPRs and implement effective foreign exchange policy aimed at stimulating real output growth in the economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.