Abstract

Due to many social problems caused by Internet consumer finance, Internet consumer finance regulation has always become one of the main concerns of governments and society. Based on a novel three-dimensional mixed strategy game matrix, this paper constructs a tripartite evolutionary game model for regulators, Internet consumer financial institutions, and consumers. In this model, we establish the dynamic replication equation of the three parties above, analyze the influence of factors on the tripartite strategy selection and discuss the stability of model equilibrium points through numerical simulation. The results show that the model will get six evolutionary stable points in Internet consumer financial regulation under different conditions. Moreover, strict regulation, verification, and contract keeping are the most ideal evolutionarily stable strategies. In addition, three critical factors affect the evolution results of the three parties, namely losses to institutions caused by loose regulation and verification, punishment for loose verification under strict regulation, and losses from breaking the contract.

Keywords

Introduction

Internet consumer finance is an innovative financial service method that provides consumer loans to consumers of all levels in a new model (Huang, 2015; J. Wang et al., 2010). Based on traditional consumer finance, it uses New Tech such as the Internet, big data, blockchain, and AI and has recently become a highly recognized financial service (Brian, 2011). However, this service mode deviates from the traditional financial regulatory system. Internet consumer finance carries certain financial risks, which may trigger consumer debt crises and economic and social problems, especially in the past 3 years of COVID-19. Effective monitoring of Internet consumer finance has become a significant challenge for the government (Zhang, 2021). Therefore, it is crucial to build a systematic regulatory model to regulate Internet consumer finance participants and industry development.

With the steady improvement of residents’ income levels, the public has achieved consumption upgrading (D. Han & An, 2022). Their consumption concepts have undergone disruptive changes, achieving a significant leap from survival oriented to development oriented. Internet consumer finance is one of the essential manifestations of inclusive finance. However, the regulation of Internet consumer finance has yet to keep up with its development. The lack of regulatory mechanisms in the field of Internet consumer finance not only damages the rights and interests of institutions and consumers and causes a series of chain reactions (D. Liu, 2021; Shen et al., 2021; Yan, 2019). Although the government and Internet consumer finance institutions have established a credit scoring system through legislation and Big Data Platform supervision and review, more work needs to be done to ensure its effectiveness and safety. Therefore, constructing a valid regulatory method that can analyze the strategic choices of multiple parties has become the main entry point for regulation (Cigu et al., 2020; Eichengreen, 2021; Fu, 2021; Q. Wang, 2019).

Various methods exist to address regulatory issues, mainly divided into four categories: legal system (Groll et al., 2021), computer technology (Wen, 2021; Z. Wu & Zhou, 2023), econometric statistical methods (Ouyang & Mo, 2016), and evolutionary game methods (M. Wei et al., 2021). Econometric statistical methods include factor analysis (J. Wang et al., 2022), Logistic regression (M. Guo, 2016; J. Wang et al., 2022), Generalized ARCH (GARCH) (H. Li & Wang, 2018), Vector Autoregressive Model (VAR) (Ouyang & Mo, 2016), Cox proportional-hazards model (Cox) (C. Li & Shen, 2018), etc. Computer technology includes artificial intelligence (AI) (Wall, 2018), cloud technology (Liao, 2021), blockchain (Gozman et al., 2020; Zhang, 2021), and so on.

The evolutionary game model is a commonly used way in the regulatory field to analyze the strategies of entities. The traditional game theory assumes that subjects are perfectly rational and make decisions under complete information. However, it is tough for participants in real economic life to do that. The evolutionary game differs from traditional classical game theory, which does not require participants to be wholly rational or states of complete information (Simon, 1954). Firstly, a payment function is transformed into a fitness function under the selection and variation mechanisms. Then, the dynamic replication equation is calculated by using the evolutionary game matrix. Finally, multiple solutions are obtained to determine whether the solution conforms to the evolutionary stability strategy. Due to many regulatory participants in the Internet consumer finance industry, two-party evolutionary game models are challenging to analyze the strategic interactions among the three parties. Therefore, it is necessary to introduce the tripartite evolutionary game into regulating the Internet consumer finance industry.

Here we can get the motivation for this paper:

The evolutionary game model can thoroughly analyze the regulatory issues of multiple parties in Internet consumer finance.

The tripartite evolutionary game model can better make the strategy choices of different entities from a global perspective.

According to evolutionary game theory, this paper establishes a three-dimensional tripartite evolutionary game model to explore the issue of Internet consumer finance regulation. We have developed the following research content:

Firstly, based on bounded rationality and the significant constraints of Internet consumer finance, the tripartite evolutionary game model’s relevant hypothesis and main parameters are proposed.

Secondly, we built a tripartite evolutionary game model to analyze the triple entities’ evolutionary behavior and equilibrium points.

Thirdly, the constructed tripartite agent evolution model verifies the parameters’ impact on evolution strategies under different conditions.

Literature Review

Internet Consumer Finance Regulation

The Internet consumer financial regulation research mainly focuses on three aspects: legal system, regulation technology, and econometric statistical methods. Many scholars have made remarkable achievements in legal regulation. Laguna de Paz (2023) focused on the role of Big Tech in the financial system and considers whether we need to formulate special laws and regulations for them. Mufarrige and Zywicki (2021) argued that Epstein’s concept would establish a more stable and efficient financial custodial framework. Groll et al. (2021) showed that economic and political factors affect the strictness of financial market supervision, and political factors are more likely to lead to inefficient regulation. S. Wang (2022) and D. Liu (2021) proposed that all countries should clarify the obligations and responsibilities of each regulator through legislation. Jones and Knaack (2019) suggested creating a new standard-setting department to regulate Fintech. Therefore, the steady and orderly development of the Internet financial market and a sound legal system go hand in hand. Improving relevant laws and regulations is the foundation for the stability of Internet finance (Q. Wang, 2019; Zhu, 2019).

Some studies have discussed the feasibility of using regulatory technology to enhance the degree of Internet financial regulation. S. Wang (2017) proposed that Internet financial institutions could use the mature products and solutions of third-party technology companies to improve their ability to supervise and control risks. With the rapid development of network technology, improving the level of regulation technology can speed up the transformation of the supervision mode (Chang & Hu, 2020; J. Wu, 2020). Wall (2018) started with a high-level overview of AI, analyzed its advantages and disadvantages, and discussed how AI affects the financial system’s evolution and regulation. Based on the experiments of the Bank of England and the Financial Conduct Authority, Micheler and Whaley (2020) summarized the advantages and disadvantages of integrating AI into regulatory law. Zhang (2021) and Gozman et al. (2020) addressed the problem of data authenticity and security. Based on blockchain technology, we could find the source of data. Therefore, applying blockchain technology to regulation can reduce the burden of laws and regulations. Liao (2021) analyzed the differentiated characteristics of cloud technology, built a data rights protection system, and refined the financial data governance rules in the cloud technology field. Cao (2021) built an Internet financial regulation system based on the RAROC pricing model to increase the efficiency of Internet financial regulation. Consequently, moderately innovative Internet financial regulation technology can improve the quality and efficiency of regulation, control risks, and solve the problems encountered in Internet Finance operations faster.

In addition, some scholars have also introduced econometric methods in Internet consumer finance. J. Wang et al. (2022) constructed a binary Logit model based on the actual loan records of Renren Loan to measure and predict the credit risk of borrowers. M. Guo (2016) built a four-dimensional indicator system to calculate the risk probability of internet consumer finance platforms through factor analysis and logistic generalized regression analysis. H. Li and Wang (2018) used Yu’ebao as an example to conduct an early warning analysis on internet consumer finance using GARCH control charts. Ouyang and Mo (2016) constructed Pareto extreme value distribution and historical model based on Var, which can accurately measure the risk level of internet finance. C. Li and Shen (2018) made a Logit and Cox proportional risk regression model to study internet consumer finance risks. They found that the main factor affecting platform risk is the degree of information disclosure, which is directly proportional to the platform’s risk resistance.

Evolutionary Games

The evolutionary game combines the notion of evolution with game theory, overcomes the limitations of static analysis, and can well analyze the decision-making changes among various subjects. Some scholars also use evolutionary games to explore regulatory issues. H. Liu and Ge (2020) analyzed the game process of government auditing and supervision in Internet finance through the evolutionary game model. Feng et al. (2020) created a dynamic game model of Fintech regulation under asymmetric information. Yang and Zhang (2020) built an evolutionary game model for the regulatory decision-making option of the third-party trading platform. X. Wang and Ren (2021) constructed an evolutionary game model between e-commerce platforms and consumers under the punishment and incentive mechanism of the governments. They analyzed the influencing factors and evolutionary path of strategic decisions. H. An et al. (2021) simulated the dynamic game process between financial supervision and reformation according to the evolutionary game model. Weng and Luo (2021) built an evolutionary game model for an online car-hailing platform and proposed the regulation mode of platform enterprises and regulators. Deng (2021) made an evolutionary game analysis on P2P using the nonlinear system stability theory. M. Wei et al. (2021) analyzed the evolution law of P2P risk. Thus, the evolutionary game model can analyze each participant’s decision-making behavior path in the regulatory process.

Model Hypothesis and Construction

Model Hypothesis

Internet big data platforms are the direct integration between institutions and consumers. The regulation of internet consumer finance mainly includes three significant participants: regulators, internet consumer finance institutions, and consumers. When consumers enter the market, concealment and non-standard auditing in borrowing information and auditing processes may occur due to their respective interests. At the same time, the punishment and severity of regulators can also affect institutions’ decision-making. Therefore, regulators, internet consumer financial institutions, and consumers will be set as the game subjects in the evolutionary game model of this article, which focuses on studying their strategic choices and stable equilibrium points.

Based on the above hypotheses, the three-party game strategy and the main parameters of the model can be summarized as shown in Table 1.

Main Parameters of the Model.

Model Construction

Based on the above hypotheses, the mixed strategy game matrix of regulators, Internet consumer financial institutions, and consumers is constructed in Table 2.

The Mixed Strategy Game Matrix.

Note. Remarks:

Model Stability Analysis

Strategy Stability Analysis of the Regulators

The expected incomes of strict and loose regulation are E11 and E12, respectively. In addition, the average expected incomes of the regulators’ are E1. According to the mixed strategy game matrix, the formula can be obtained as shown in Equations 1 to 3.

The dynamic replication equation of regulators is shown in Equation 4.

If

If

The Equation 5 can be derived from the Equation 4.

When

When

Phase diagram of regulators’ policy evolution.

When the initial choice of the regulator’s strategy is in space V1,

When the initial choice of the regulator’s strategy is in space V2,

Proposition

Strategy Stability Analysis of the Internet Consumer Financial Institutions

The expected incomes of strict and loose verification are E21 and E22, respectively. In addition, the average expected incomes of the Internet consumer financial institutions’ are E2. According to the mixed strategy game matrix, the formula can be obtained as shown in Equations 6 to 8.

The dynamic replication equation of Internet consumer financial institutions is shown in Equation 9.

If

If

The Equation 10 can be derived from the Equation 9.

let

When

When

Phase diagram of institutions’ policy evolution.

When the initial choice of the institution’s strategy is in space V1,

When the initial choice of the institution’s strategy is in space V2,

Proposition

Strategy Stability Analysis of the Consumers

The expected incomes for keeping and breaking the contract are E31 and E32, respectively. Moreover, the average expected incomes of the consumers’ are E3. According to the mixed strategy game matrix, the formula can be obtained as shown in Equations 11 to 13.

The dynamic replication equation of consumer is shown in Equation 14.

If

If

The Equation 15 can be derived from the Equation 14.

When

When

Phase diagram of consumers’ policy evolution.

When the initial choice of the consumer’s strategy is in space V1,

When the initial choice of the consumer’s strategy is in space V2,

Proposition

Stability Analysis of System Strategy

When the duplicated dynamic equations are equal to zero, the speed and direction of strategy adjustment of the three players in the game do not change, indicating that the three players have reached a relatively stable equilibrium state. Let

The Jacobian matrix of the system is shown in Equation 16.

According to hypothesis 4, r2 is higher than r1. The eigenvalue λ3 of points E3 and E7 are greater than 0, and the eigenvalue λ3 of points E4 and E8 are less than 0. In other words, E3 and E7 are unstable, and the stability of the other six points is uncertain and needs further discussion.

Case

Case

Case 1.2:

When Lb is more minor than

When

When Li is higher than

When

When P is higher than

To sum up, the stability of all equilibrium points is shown in Table 3.

Stability Analysis of Equilibrium Point.

Experiment Simulation

In order to directly observe the evolutionary trajectory of the three parties and the influence degree of parameters, this paper uses Matlab to conduct simulation experiments on the evolution stability strategy and related parameters. From the perspective of the whole regulation process of Internet consumer finance, the equilibrium point (1,1,1) is a choice suitable for the industry. That is the strict regulation, strict verification, and keeping the contract. The main reasons are as follows. The regulator strictly regulates the behavior of Internet consumer financial institutions. In this way, institutions will be strict verification to prevent people from losing trust and avoid losses to society. Moreover, institutions choose strict verification and timely update consumers’ behavior database, which can screen out dishonest customers. In addition, when consumers pay their bills on time, the institutions can avoid unnecessary losses and thus maintain their normal operations. This paper analyzes the sensitivity of parameters B, A, Cr, k, D, C, Ci, P, and f under the strategy of equilibrium point (1,1,1). Set the following parameters to

The Revenue Analysis of Strict Regulation

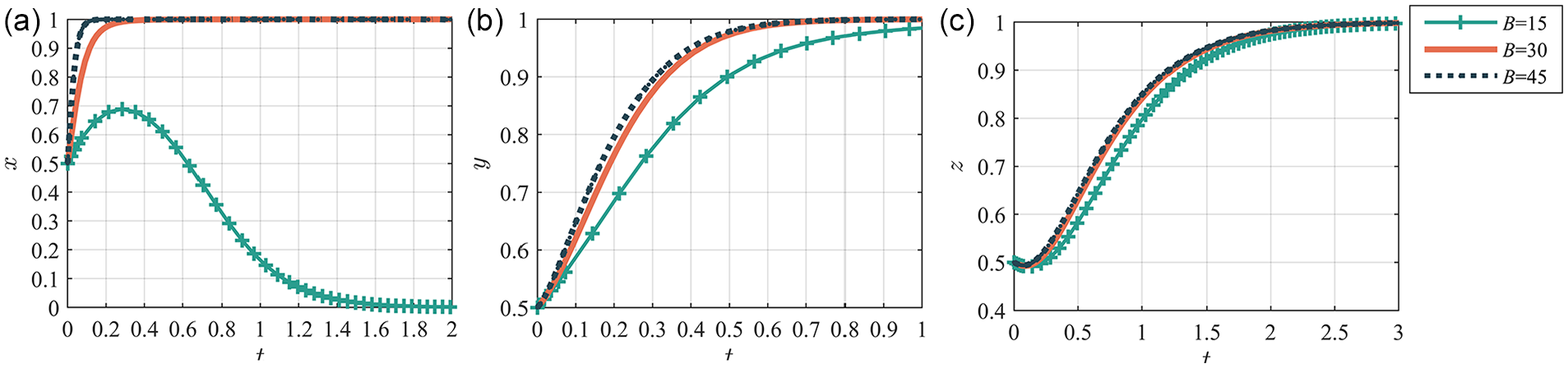

Under the conditions of the above parameters, we change the revenue of strict regulation (B). When B values are 15, 30, and 45, we can obtain the evolutionary stability strategy of the participating entities.

Figure 4a shows that when B is small, the proportion of strict regulation will increase first and then evolves into a stable strategy of loose supervision. When B continues to grow until

The effect of tripartite subjects’ strict regulation revenue on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

According to Table 3, when

Numerical simulation of evolutionary stability strategy: (a) E4 (0,1,1) and (b) E8 (1,1,1).

The Revenue Analysis of Loose Regulation

Under the conditions of the above parameters, we change the revenue of loose regulation (A). When A values are 12, 18, and 24, we can obtain the evolutionary stability strategy of the participating entities.

Figure 6a shows that when A is small, regulators will choose strict regulation through trade-offs to ensure the healthy development of the industry. As A increases, regulators will benefit more from loose regulation. Thus, the rate of choosing strict regulation will decrease. However, it will still evolve into a rigorous regulatory strategy ultimately. When the revenue of loose regulation is too significant, the Internet consumer finance industry will fall into chaos. At this time, the regulatory authorities will strengthen the supervision and strictly regulate the development of the industry. Meanwhile, as shown in Figure 6b and c, the changes in A have no evident impact on the decision- making choices of institutions and consumers. And the industry development is in an ideal state.

The effect of tripartite subjects’ loose regulation revenue on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

The Cost Analysis of Loose Regulation

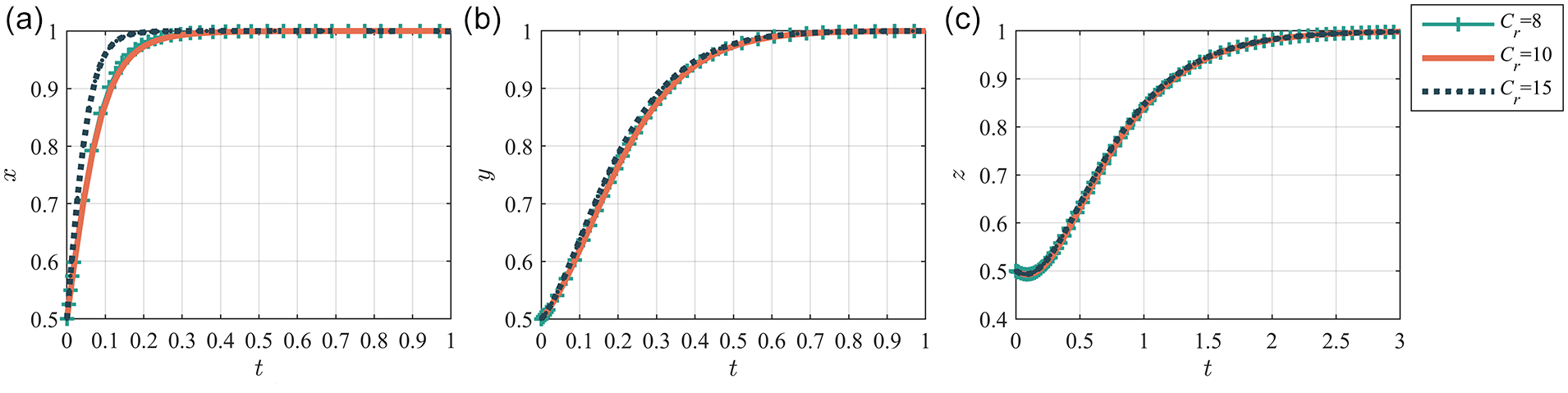

In the perfect state of E8(1,1,1), we change the cost of loose regulation (Cr). When Cr values are 8, 10, and 15, the evolutionary stability strategy of the participating entities obtained is shown in Figure 7.

The effect of tripartite subjects’ loose regulation cost on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

Figure 7 shows that the changes in Cr will not affect the strategies of regulators, Internet consumer finance institutions, and consumers. In this state, the progress of the Internet consumer finance industry is standardized and ideal. Regulators choose strict regulation to maintain industry order and protect consumers’ legitimate rights. The strict verification of Internet consumer finance institutions has played an excellent regulatory role in consumers keeping the contract.

The Strict Degree Analysis of Regulation

Under the conditions of the above parameters, we change the strict degree of regulation (k). When k values are 1, 1.5, and 2, we can obtain the evolutionary stability strategy of the participating entities.

Since k ≥ 1 and the cost of strict regulation of regulators is kCr, as shown in Figure 8a, regulators will evolve into strict regulation in an ideal state. When k increases, the cost of strict regulation increases simultaneously. Hence, the rate of choosing strict rules decreases. When k is too high, the cost of strict regulation also increases. There will be loose regulation in the industry, leading to chaos. Therefore, regulators will increase the rate of strict regulation to regulate industrial development. As shown in Figure 8b and c, the changes in k do not significantly influence the decision-making choices of institutions and consumers, and the industry development is in an ideal state.

The effect of tripartite subjects’ strict degree of regulation on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

The Revenue Analysis of Strict Verification

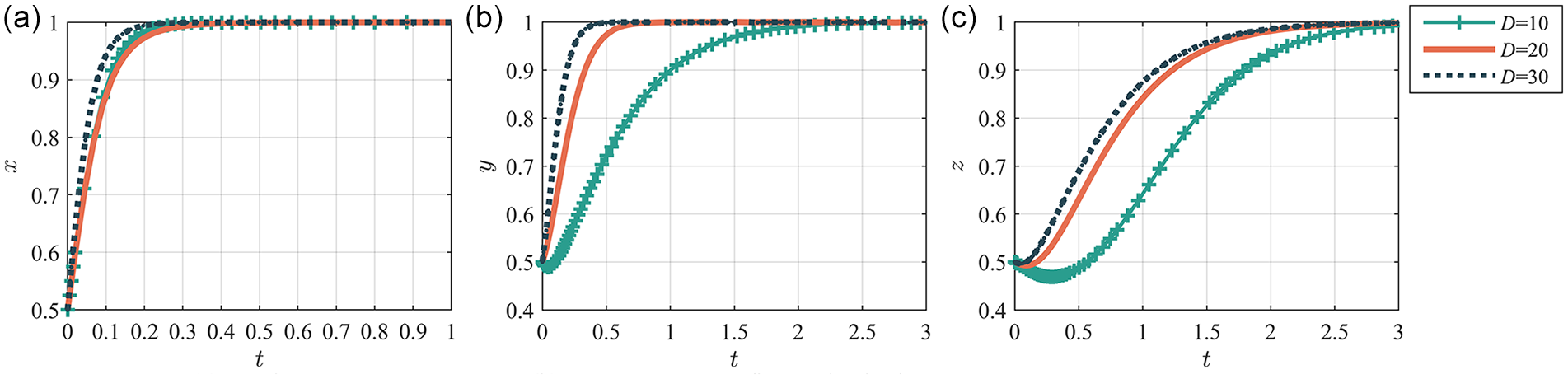

Under the conditions of the above parameters, we change the revenue analysis of strict verification (D). When D values are 10, 20, and 30, the participating entities’ evolution and stability strategies are obtained in Figure 9.

The effect of tripartite subjects’ strict verification revenue on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

We can see from Figure 9 that the change in D has a relatively small impact on regulators’ selection of regulatory strategies. As D increases, the more revenue the regulators can obtain. Regulators can further strengthen regulation by upgrading their regulatory system and expanding their workforce, thereby speeding up strict regulation. With the increase of D, institutions will also accelerate the pace of strict verification under high-pressure conditions to regulate their operations because of regulators’ strict regulation. Moreover, consumers will eventually evolve into keeping the contract strategies due to some of the rewards and penalties imposed by institutions.

The Additional Benefit Analysis of Strict Long-Term Verification

Under the conditions of the above parameters, we change the additional benefit of strict long-term verification (Ri). When Ri values are 5, 10, and 15, the development and stability strategies of the participating entities obtained are shown in Figure 10.

The effect of tripartite subjects’ strict long-term verification of additional benefits on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

From Figure 10, the changes in Ri have no significant impact on the strategies of regulators, Internet consumer finance institutions, and consumers. Under these conditions, the progress of the Internet consumer finance industry is in an ideal state. Regulators choose strict regulation, leading institutions to choose strict verification and avoid punishment. Furthermore, institutions use a systematic verification model to screen default-prone consumers. Further analysis reveals that the higher Ri, the faster institutional and consumer strategies evolve. Meanwhile, when the additional benefit of strict long-term verification is low, institutions are more likely to adopt proactive strategies to gain a better reputation and attract consumers to enjoy the service.

The Revenue Analysis of Loose Verification

In the perfect state of E8(1,1,1), we change the revenue analysis of loose verification (C). When C values are 20, 25, and 30, the development and stability strategies of the participating entities obtained are shown in Figure 11.

The effect of tripartite subjects’ loose verification revenue on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

With the increase of C, institutions can gain more revenue. Therefore, the rate of choosing strict verification strategies slows down. And the rate of consumers keeping the contract policies will also decrease. Regulators will accelerate the selection of strict regulation strategies to regulate the development of the industry. Ultimately, the three parties will still choose strict regulation, strict verification, and keeping the contract strategies.

The Operating Costs Analysis of Loose Verification

Under the conditions of the above parameters, we change the operating costs of loose verification (Ci). When Ci values are 10, 25, and 40, we can obtain the development and stability strategies of the participating entities.

Because the loose degree of verification f is a fixed value greater than or equal to 1, the cost of strict verification of institutions is kCi. Figure 12 shows that as Ci increases, kCi continues to grow. When Ci reaches a certain threshold, the evolution strategy of institutions changes from a strict verification strategy to a loose one. And the evolution strategy of consumers changes from keeping the contract strategy to breaking the contract strategy. The evolution rate of regulators, institutions, and consumers grows with the increase of Ci. The above results indicate that the higher the operating cost of strict verification for Internet consumer finance institutions, the greater the temptation of loose verification for institutions, which can hinder the healthy development of the industry. Regulators are more likely to choose stricter regulatory methods to regulate the industry.

The effect of tripartite subjects’ loose verification operating costs on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

The Punishment Analysis of Loose Verification During Strict Regulation

Under the conditions of the above parameters, we change the punishment of loose verification during strict regulation(P). When P values are 10, 15, and 20, we can obtain the evolutionary stability strategy of the participating entities.

Figure 13 shows that the evolution rate of regulators choosing strict regulation increases rapidly with the continuous increase of P and ultimately stabilizes with the adoption of all rigorous regulation strategies. The evolution strategy of institutions has changed from loose verification to strict verification. At the same time, the evolution strategy of consumers has changed from breaking the contract to keeping the contract. And when

The effect of tripartite subjects’ punishment for loose verification during strict regulation on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

According to Table 3, when p = 10, the stability conditions of point E5(1,0,0) are satisfied. The numerical simulation result of the evolutionary stability strategy is shown in Figure 14.

Numerical simulation of evolutionary stability strategy.

The Loose Degree Analysis of Verification

Under the conditions of the above parameters, we change the loose degree of verification (f). When f values are 1, 1.2, and 1.5, we can obtain the evolutionary stability strategy of the participating entities.

Figure 15 shows that when f increases, regulators regulate the pace of evolution more quickly and strictly to ensure the industry’s standardized development and avoid adverse events. If institutions’ loose degree of verification is constantly increasing, it will lead to more relaxed lending and repayment. Therefore, the evolution rate of consumers’ choice to keep the contract will also slow down.

The effect of tripartite subjects’ loose degree of verification on evolutionary stability strategies: (a) regulators, (b) internet consumer finance institutions, and (c) consumers.

Evolutionary Stability Strategy Analysis

As the evolutionary stability of points E4, E5, and E8 has been discussed above, the evolutionary stable strategies of points E1, E2, and E6 will be further analyzed.

For E1(0,0,0), meet

Numerical simulation of evolutionary stability strategy: (a) E1 (0,0,0), (b) E2 (0,0,1), and (c) E6 (1,0,1).

For E2(0,0,1), meet

For E6(1,0,1), meet

Conclusions and Suggestions

Conclusions

This paper firstly constructs a tripartite evolutionary game model for regulators, Internet consumer financial institutions, and consumers. Then the stability of the three-party strategy selection and the equilibrium strategy combination of the game system is analyzed (T. Wang et al., 2023; Zhao & Tian, 2023). Finally, we discuss the effectiveness of the system equilibrium strategy combination and the influence of various parameters on strategy selection through numerical simulation. It is worth mentioning that the paper constructs a three-dimensional tripartite main body mixed strategy game matrix, which can analyze the evolution process of the behavior of the three parties.

Firstly, we obtain six evolutionary equilibrium points In different cases by analyzing the stability strategy of the model. Among them, the equilibrium point E8(1,1,1) is in an ideal state. The evolutionary stability strategy is strict regulation, strict verification and compliance. At this time, the profits of strict regulation by the regulators are higher than those of loose regulation under the strict verification of Internet consumer financial institutions. Moreover, the punishment imposed by the regulators on the loose verification of institutions is higher than the difference between the profits of loose and strict verification of institutions.

Secondly, according to the analysis of six evolutionary equilibrium points, three critical factors affect the evolution results of the three parties: losses to institutions caused by loose regulation and verification, punishment for loose verification under strict regulation, and losses from breaking the contract.

Thirdly, the equilibrium point of the above evolutionary game model shows that the regulators should choose a strict regulatory strategy. The punishment of the regulators has actively standardized the auditing behavior of Internet consumer financial institutions and significantly promoted the development of the industry. On the contrary, if the punishment of the regulators are low, the Internet consumer financial institutions may relax audits, which may lead to bad debts and financial chaos.

Finally, Internet consumer financial institutions act as regulators and the regulated. Therefore, this paper’s tripartite evolutionary game model can offer theoretical support for Internet consumer finance supervision. Furthermore, this model also guides the government to establish industry standards to ensure the stable growth of Internet consumer finance.

Suggestions

Based on the above conclusions, we put forward relevant suggestions to solve the problem of Internet consumer financial regulation.

From the perspective of regulatory authorities, it is necessary to formulate relevant regulatory laws and policies to supervise industrial behaviors. Secondly, regulatory authorities should constantly improve the nationwide personal credit investigation system to facilitate the verification of personal information. At the same time, regulators also should determine an appropriate amount of fines to punish Internet consumer financial institutions for their loose verification. Finally, regulators need to improve supervision technology. Based on traditional methods, technology supervision should be widely applied. We must create a dual-dimensional regulatory system of law and technology to promote the progress of the Internet consumer finance industry.

From the perspective of Internet consumer financial institutions, they should receive rewards from the regulatory authorities as long as institutions can carry out strict verification. At the same time, regulatory incentives should also encourage Internet consumer financial institutions to verify consumers’ information strictly for a long time. In addition, institutions should measure consumers’ repayment ability and consumption behavior according to the detailed indexes. Then institutions divide consumers into different levels and formulate corresponding lending limits. Furthermore, institutions should constantly upgrade the verification technology and consumers’ database to weed out ineligible consumers for loans and prevent loan fraud.

From the consumers’ perspective, consumers’ repayment on time can reduce certain losses of Internet consumer financial institutions. Therefore, institutions can take steps to encourage consumers to keep contracts and pay bills on time. For example, Internet consumer financial institutions should appropriately increase the amount of lending for consumers who pay their bills on time. On the contrary, institutions should increase penalties for losses for consumers who fail to pay. Moreover, the regulatory authorities need to instill the right consumption concept and cultivate consumer awareness of credit risk. The government should remind consumers not to borrow blindly on unnecessary excessive demand and emphasize the importance of credit in consumer loans.

Limitations and Future Work

The research model in this article has certain limitations. Except for the three parties mentioned in the model, the game situations of other participants in Internet consumer finance is not considered. In future research, we should consider games between traders and the game between sellers and Internet consumer financial institutions. In addition, we should further introduce the consumer credit rating system into the model for supervising Internet consumer finance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The National Social Science Fund of China (No. 19BJY246), The Natural Science Fund Project of the Science and Technology Department of Jilin Province, China (No.20190201186JC), and The Science and Technology Development Plan Project of Changchun Science and Technology Bureau (No. 21ZY61).

Ethical Statement

None of the above is covered in this paper.