Abstract

This study examines the impact of the regional old-age dependency ratio on the collection efficiency of public pension funds using statistical data on contributions of public pension schemes for urban employees in 31 Chinese provinces and municipalities between 2010 and 2015. An inverted U-curve relationship between the regional old-age dependency ratio and the collection rate of public pension funds was observed with a single threshold value of .5439, thus, suggesting the need for a change in the soft constraints on collection responsibility and an optimization of the institutional structure underlying public pension schemes.

Keywords

Introduction

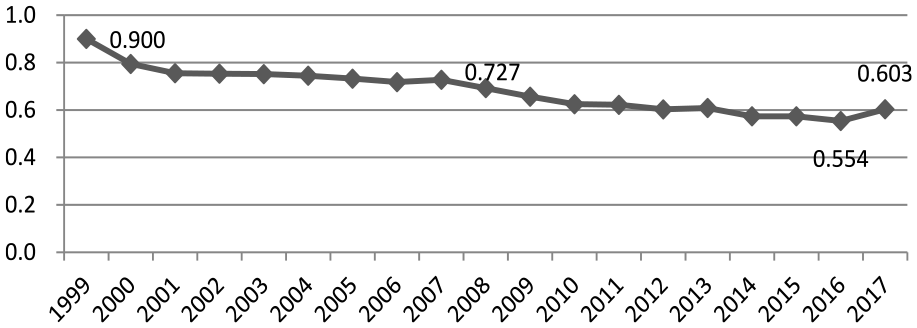

Due to China’s increasingly aging population and the subsequent significant increase in the number of urban retirees, large annual payments are being disbursed by pension funds, and ensuring the sustainability of such payments is a concerning issue. 1 Since the establishment of the basic old-age insurance system for urban employees in 1997, the collection rate 2 of public pension funds has declined annually (from 90% in 1999 to 60.3% in 2017; Figure 1). As a result of this low collection rate, the deficit of national public pension funds in China has reached nearly 500 billion Yuan in recent years. 3 Thus, further research is currently necessary for determining how to improve the collection efficiency of public pension funds and effectively meet ever-rising pension payments.

Collection rates of public pension funds from China’s urban employees 1999 to 2017.

Existing studies have cited three major reasons to explain the low public pension funds collection rate. First, because the collection powers have been split between two authorities, the collection of premiums has low enforceability (J. Q. Liu, 2011; H. Liu & Liu, 2020; Yang, 2010). Second, because of the relatively high statutory contribution rate, operating costs of enterprises have increased; therefore, enterprises have found ways to reduce their contributions by underreporting their employee headcount and salary bases (Feldstein & Liebman, 2006; Zheng, 2015b). Third, to reduce labor costs, ease the burden on enterprises, and attract foreign investment, local governments have deliberately relaxed the collection and management of public pension funds, and this has helped to reduce collection efficiency (Gillion et al., 2000; Ma and Yang, 2010; H. R. Peng et al., 2018).

Senior Chinese government leaders have not relaxed the requirements for the collection of social security contributions. Indeed, in recent years, the Chinese government has introduced several policies and measures to ensure that social security contributions are paid. Plans for the Reform of the State Tax and Local Tax Collection Administration System was issued in 2018; it stipulated that taxation authorities should uniformly levy all social insurance contributions from January 1, 2019, onwards. The Comprehensive Plan for Reducing Social Insurance Contribution Rates (No. 13 [2019] of the General Office of the State Council), which was issued in 2019, stipulated that the employer contribution rate toward basic old-age insurance for urban employees would be reduced to 16 % as of May 1, 2019. These two measures effectively strengthened contribution collection and greatly reduced social insurance expenditures for enterprises. Did these policies and measures actually help to improve the declining collection rates of the public pension funds?

By estimating the collected incomes of local public pension funds from 2019 to 2020, this study found that, among 31 provinces and municipalities in mainland China, 18 witnessed an increase in their collection rate and the remaining 13 witnessed a decrease 4 ; these included the provinces of Heilongjiang, Gansu, and Sichuan. Overall, the collection rate did not significantly improve in the country as a whole (Figure 2).

Collection rates of public pension funds for urban employees in provinces and municipalities of mainland China in 2019 and 2020.

From this perspective, existing studies have failed to fully explain the low collection rates of public pension funds in China’s urban areas. Concerning the three above-mentioned explanations for low collection rates from existing studies, measures such as strengthening collection agencies’ enforcement powers and reducing the statutory contribution rate have failed to significantly increase collection efficiency in different parts of China. While local governments have taken part in a “race to the bottom” by relaxing supervision and reducing labor costs in their respective regions, this step does not account for the above-mentioned differences in collection rates among regions.

This current study utilized the contribution-related collection data of public pension funds for urban employees in 31 Chinese provinces and municipalities from 2010 to 2015 to establish a dynamic panel threshold model and examine regional pension burdens’ non-linear impacts on the collection rate of public pension funds. In addition to providing a new explanation for the low collection efficiency of public pension funds in China’s urban areas, our findings also empirically support the need to examine local governments’ economic behaviors in the context of social insurance system building.

The rest of this article is arranged as follows: the second section describes China’s public pension system and fund income and expenditure arrangements; the third section contains the literature review; the fourth section proposes the research hypotheses and states the econometric model and methods adopted by this current study; the fifth section tests the non-linear impact and threshold effect of regional pension burdens on the collection rate of public pension funds, and the sixth section puts forward policy suggestions, and finally the research conclusion.

Public Pension System in China

In 2005, China established a public pension system for urban employees in accordance with the principle of combining “social pooling and individual account.” The public pension fund is divided into a social pooling accounts and an individual account. The employer contributes 20% of the employee’s total wages to the social pooling account, which is a form of social mutual assistance, while the employee contributes 8% of his/her wage to his/her own individual account.

From the perspective of the funds collected, China’s urban workers’ public pension funds conduct the local overall planning, while local governments are responsible for collection. Since the reform of China’s tax collection administration in 2018, all urban employee old-age insurance contributions have been levied by the taxation authorities, but due to a “vertical + local” dual management system was adopted by the taxation scheme, Local governments still need to assume the corresponding responsibility for collaborative collection and supervision. From the perspective of pension payments, local governments are responsible for ensuring that basic pensions are paid on time and in full, while the central government and local governments at all levels assume the fiscal responsibility of ensuring the funds are available for pay-out. Based on this institutional arrangement, because basic financial security is provided by the central government, local governments may determine the strength of their collection and supervision efforts concerning local public pension funds based on their own burdens, thus affecting the collection efficiency of public pension funds.

Literature Review

The problem of public pension funds’ low collection efficiency has attracted significant global scholarly attention. Most relevant studies have discussed the reasons underlying the evasion and avoidance of old-age insurance contributions based on system design factors and the behaviors of enterprises and governments. All these studies have arrived at basically the same conclusion regarding the negative incentive created by an excessively high statutory contribution rate. However, few empirical studies have examined the local government pension burden’s impact on the collection efficiency of public pension funds.

Old-age insurance contributions, which have an inter-generational redistribution function, essentially function as a payroll tax; therefore, extensive literatures on tax evasion and avoidance have formed a reference for this study. Cintra (2010) discovered that the payroll tax rate in Brazil was around 35% (with businesses bearing the majority of the tax burden) and that, to evade and avoid taxes, businesses typically hired informal employees and outsourced labor. Williams and Horodnic (2016) and Nola et al. (2019) found that some European enterprises concealed total wages and profits by paying their employees directly in cash in order to evade and avoid payroll taxes. Benzarti and Harju (2020) discovered that, when payroll taxes rose, Finnish enterprises typically laid off low-skilled and conventional manual workers in order to pay fewer taxes. L. X. Li et al. (2021) found that small and cash-constrained private enterprises in China were more likely to evade and avoid payroll taxes due to fiscal austerity measures and stricter enforcement of value-added tax collection.

The impact of statutory contribution rates on enterprises’ evasion and avoidance of contributions as well as public pension funds’ collection efficiency has been studied extensively in the literature. Since China’s statutory contribution rate is much higher than those of most other countries around the world, 5 many scholars have focused on studying cases in China. Feldstein (2003) noted that China’s higher statutory contribution rate reduced the willingness of enterprises and employees to participate in insurance schemes; this helped to decrease the actual collected income of public pension funds for urban employees to less than one-third of the theoretical value. Nyland et al. (2006) examined enterprise audit data from the Shanghai Municipal Bureau of Social Security and discovered that, in 2002, approximately 80% of enterprises failed to contribute social insurance premiums on time and in full at the higher statutory contribution rate. According to Rickne (2013) and Chaudhry et al. (2016), an excessively high statutory contribution rate for old-age insurance can reduce enterprises’ cash flow and thus lower their production efficiency; this, in turn, imposes a heavy cost burden on enterprises and induces them to evade and avoid social insurance contributions.

Research in this area has found that the characteristics of enterprises influence their evasion and avoidance of social insurance contributions. According to Feng et al. (2012), a lowering of the contribution rate has little effect on increasing the level of old-age insurance participation in enterprises with higher levels of human capital, but it has a greater effect on enterprises with lower levels of human capital. Wu (2017) found that, when the statutory contribution rate was higher, among large enterprises, the degree of contribution evasion was lower than that of small enterprises; the degrees of contribution evasion (under different types of ownership) of enterprises are (from highest to lowest) as follows: foreign-owned enterprises, private enterprises, and state-owned enterprises. We must note that little difference has been observed in the contribution evasion of enterprises in different types of industries and involving different technologies. J. Y. Li and Wang (2020) revealed that when an enterprise’s public pension funds contribution ratio was higher, the degree of its tax avoidance would be greater; also, this effect is more significant in enterprises with higher financing constraints, lower profitability, and lower cash holdings.

The strength of government supervision during the implementation of the old-age insurance system is an important factor influencing enterprises’ evasion and avoidance of contributions. Echevarría and Iza (2006) found that the collection efficiency of public pension funds could only be improved through supervision and the implementation of punitive and coercive measures. Almeida and Carniero (2012) discovered that more frequent auditing of businesses could improve compliance with social insurance contributions in Brazil. Yang (2010) suggested that strengthening the internal audits of public pension funds would effectively remove the problems of arrears and evasion. Jiang et al. (2017) found that increasing the severity of punishment for contribution evasion by enterprises and management departments of public pension funds would effectively curb this problem. H. Liu and Liu (2020) asserted that taxation authorities’ collection of social insurance contributions has significantly increased the likelihood that enterprises will participate and contribute; the impact was more significant among non-state-owned enterprises, small-scale enterprises, labor-intensive enterprises, and enterprises with lower wages.

As part of the process of global economic integration, national and local governments may seek to reduce the burden on enterprises by relaxing oversight over their contributions to old-age insurance, thereby increasing the nation’s or regions’ ability to attract capital. This can lead to a race to the bottom with regard to collecting contributions, thus resulting in low collection efficiency. According to Zodrow and Mieszkowski (1986) and Keen and Marchand (1997), a tax revenue-related race to the bottom among local governments can minimize public goods, particularly social security. Tanzi (2002) observed that regulatory competition that began to emerge within the welfare state for “downward” levels of social security could be attributed to the pressures and risks associated with market constraints and capital flight. According to Whyte (2019), the taxation-related race to the bottom among certain countries has deprived the rest of the world of the funds necessary for investing in healthcare, education, social security, and poverty alleviation. Z. W. Peng (2009, 2010) pointed out that, in order to attract investment, local governments may compete to relax social insurance supervision and that there is a tendency to compete to reduce social insurance costs. According to H. R. Peng et al. (2018) and Lu et al. (2019), local governments may participate in an inter-governmental race to the bottom by reducing their efforts to collect social insurance contributions with the aim of reducing the burden on enterprises and promoting economic growth in their regions.

The above-discussed literature forms an important reference for this study; however, regarding the problem of low collection efficiency at the local level in China, the race to the bottom explanation is insufficient for describing and depicting the collection behaviors of local governments. To date, few researchers have addressed the low collection efficiency of public pension funds from the standpoint of soft budget constraints. Due to soft budget constraints, when the income and payment of local government public pension funds are out of balance (and thus resulting in a greater deficit), the central government has a strong incentive to help local governments for the sake of maximizing social welfare (Inman, 2003; Velasco, 1999). In the course of central government undertaking responsibility of ensuring the funds are paid for relief, local governments may hold that the order of their regions’ position in the central government’s aid list is linked to the amount of aid funds; this could result in debt reliance among local governments (Guo et al., 2016). Therefore, among all local governments with varying pension burdens, there is a significant lack of motivation to devote substantial efforts to collecting public pension funds; consequently, deficits continue to grow. To compensate for rising deficits, the central government typically increases transfer payments to local governments. Based on this understanding, this study examines the impact of the old-age dependency ratio on the collection efficiency of public pension funds for urban employees from the perspective of soft budget constraints.

Research Hypotheses, the Econometric Model, and Data

Research Hypotheses

For local governments, the collection of public pension funds is a multi-objective decision that requires consideration of both the region’s economic vitality and the burden of contributions on regional enterprises. Under a given statutory contribution rate, if the pension burden and payment pressure of a given region are satisfactory relative to the regional economics, paying the basic pension in full will not put too much pressure on enterprises. Consequently, the local government may increase collection efforts, and a positive correlation is observed between the payment pressure of public pension funds and the collection rate of funds in a given region.

Due to its own economic basis and financial capacity, a local government has a limited responsibility to ensure the full payment of public pension funds. When the pension burden becomes too high and a large deficit is seen in public pension funds, even if the collection rate is high, the collected income for public pension funds may not be enough to cover current pension payments. For example, in Heilongjiang Province, an old industrial base in Northeast China, the large outflow of workers has led to deficits in the public pension funds in recent years. The annual cumulative deficit of pension funds exceeded 40 billion yuan between 2016 and 2020. 6 Despite exploring other sources of potential income, this deficit could not be overcome, and Heilongjiang had to apply for central government subsidies, use surplus funds from individual accounts, or borrow from the national social security fund to ensure regular payment of public pension funds.

Thus, when payment pressure of public pension funds becomes relatively high, the local governments’ subject responsibility toward pension payments inevitably becomes a "soft constraint." The central government bears the responsibility for providing financial assistance toward the basic old-age insurance system through issuing central financial subsidies and allocating central regulation funds. When there is excessive payment pressure on local governments related to public pension funds and the actual contribution rate is high, these local governments can “rightfully” transfer some of the responsibility for guaranteeing that public pension fund payments are covered by the central government. In such cases, to ensure the economic vitality of the enterprises in the regions, local governments may reduce, to some extent, the efforts devoted to public pension funds collection and supervision work. Under such circumstances, a negative correlation is seen between the payment pressure of public pension funds and the collection rate of public pension funds in a region.

The subsidies provided by the central and local governments to public pension funds for urban employees between 2011 and 2015 are shown in Table 1. The table shows that the scales and trends of subsidies provided by the central and local governments to public pension funds for urban employees varied enormously. The size of central financial subsidies was large and increased each year, whereas the size of local financial subsidies was small and grew slowly. This indicates that in China’s super-aging society, with its increase in population life expectancy, the ever-increasing pension fund payment deficits are largely covered by the central government.

Subsidies Provided by the Central and Local Governments to Public Pension Funds for Urban Employees From 2011 to 2015 (100 million Yuan).

Based on the above analysis, the following hypotheses are proposed: In the institutional environment of soft-budget constraints on pension payments, the payment pressures of public pension funds show an inverted U-curve relationship with collection rate, first showing an increase and then a decrease, with a possible single threshold between the payment pressures of public pension funds and collection rate.

Settings of the Econometric Model

In the context of an aging population, the old-age dependency ratio can indicate the payment pressures of a region’s public pension funds. The higher the old-age dependency ratio, the greater the payment pressures of regional public pension funds. Using the old-age dependency ratio as a measure of the payment pressure of a region’s public pension funds, its impact on local government collection efficiency is investigated. Given the dynamics and continuity of public pension funds collection rate, as well as the endogeneity of old-age dependency ratio, the following dynamic panel model was chosen as the basic model:

Where =

The most typical feature of the dynamic panel model is that the explanatory variables contain the one-period lag of the explained variable. The generalized method of moments (GMM) approach is used to estimate equation (1) to solve the endogeneity problem in the one-period lag of the explained variable. Meanwhile, since the old-age dependency ratio may have a threshold effect on the public pension funds collection rate of the local government, a threshold estimation is introduced based on equation (1) to construct a dynamic panel threshold model, as shown in equation (2), in which I is the threshold indicator function, and λ is the threshold value to be estimated.

Data Sources and Variable Selection

The panel data from 31 provincial-level regions in mainland China (2010–2015) were used as the research sample for this study. Data on the collected revenues of public pension funds in various regions come from the China Pension Report (2011–2016). As the National Bureau of Statistics no longer discloses data on the collected revenues of regional public pension funds, the data in this study are only up to 2015. Data on average wage growth, ownership structure, regional economic development level, and capital intensity were collated and calculated from the China Statistical Yearbook and the China Labour Statistical Yearbook. As the values of the relevant variables involving currency are large, all such values were converted using logarithmic processing to reduce the impact of heteroscedasticity. Data on statutory contribution rates for all provinces and municipalities are derived from the China Pension Report (2012–2016) and the official websites of local human resources and social security bureaus.

The other relevant variables are shown in the Appendix, and the descriptive statistical analysis is shown in Table 2.

Descriptive Statistics of Major Variables.

The descriptive statistics for the major variables are as shown in Table 2. In terms of the statutory contribution rate, the mean statutory contribution rate in all regions of the country from 2010 to 2015 was 27.7%. The lowest was 22% (Guangdong and Zhejiang provinces, 2010–2015), and the highest was 30% (Shanghai, 2010–2012, and Heilongjiang and Jilin, 2010–2015). The mean collection rate during the observation period was 0.62, with the lowest value being 0.337 (Fujian Province, 2012) and the highest value 1.135 (Gansu Province, 2011). The revenue collected from Gansu Province in 2011 included overdue contributions. In terms of the old-age dependency ratio, the mean value from 2010 to 2015 was .396, the lowest value was .102 (Guangdong Province, 2014) and the highest .728 (Heilongjiang Province, 2015). During the observation period, the mean value of the actual contribution rate was .123, the minimum value was .067 (Guangdong Province, 2014), and the maximum value was .215 (Gansu Province, 2011).

Analysis of the Empirical Results

Examination of the Non-Linear Relationship and Threshold Effect

Based on model (1) in the previous section, this study first uses dynamic panel estimation to test the effect of the old-age dependency ratio on the collection efficiency. In the model, the collection rate comprehensively reflects the characteristics of local economic development and the strength of premium collection. The strength of collection also affects the number of insured active workers, which in turn affects the old-age dependency ratio, indicating that the old-age dependency ratio is endogenous to a certain extent.

The current old-age dependency ratio is affected by the historical old-age dependency ratio, while the current collection rate is less affected by the historical old-age dependency ratio. Based on this consideration, we try to use the first-order and the second-order lagged term of the old-age dependency ratio as instrumental variables in the dynamic panel estimation to deal with the endogeneity problem present in the model and obtain the estimation results using the systematic GMM two-step method.

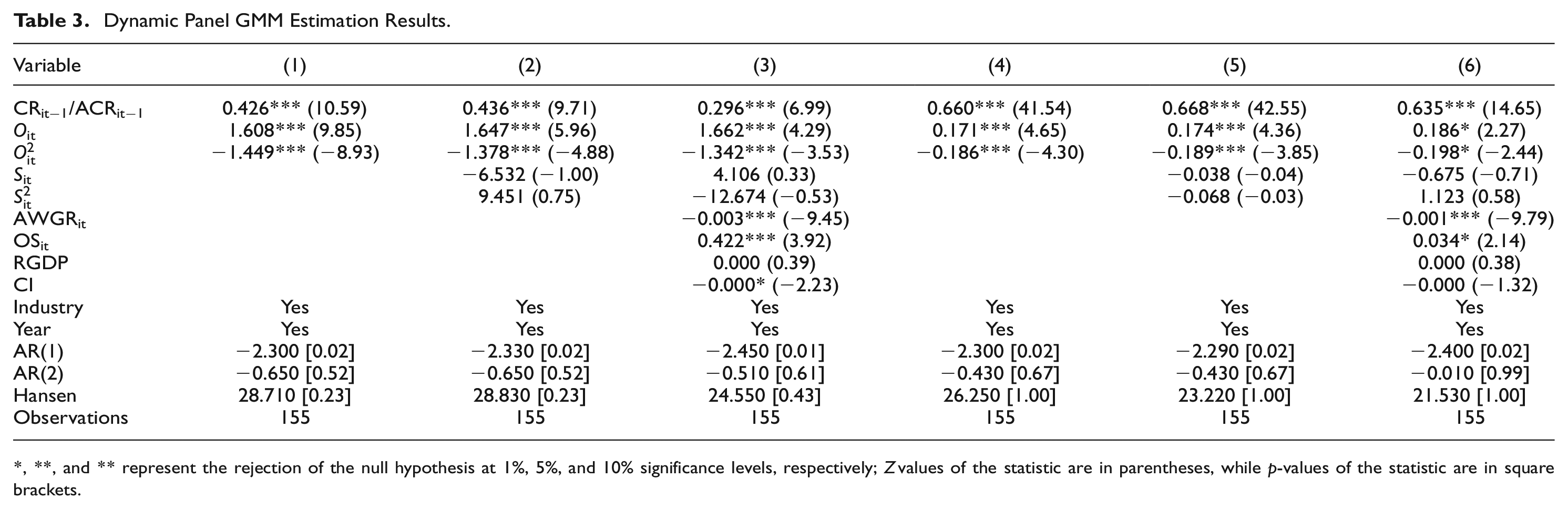

Table 3 presents the model-estimation results. The Hansen test demonstrated that there is no overidentification in the instrumental variables and that the instrumental variable settings are reasonable. AR(1) and AR(2) tests also showed that there is no second-order serial correlation. Estimating the non-linear effect between public pension funds collection rate and old-age dependency ratio, it can be seen the coefficients of the old-age dependency ratio are all significantly positive, and their square terms are all significantly negative (in the first three columns of Table 3). The estimation results support our research hypothesis about an inverted U-curve relationship between public pension funds collection rate and old-age dependency ratio.

Dynamic Panel GMM Estimation Results.

, **, and ** represent the rejection of the null hypothesis at 1%, 5%, and 10% significance levels, respectively; Z values of the statistic are in parentheses, while p-values of the statistic are in square brackets.

Based on the dynamic panel threshold model with endogenous variables proposed by Caner and Hansen (2004), this study first used the forward orthogonal deviations transformation approach proposed by Kremer et al. (2013) to eliminate the individual fixed effects of related variables. The one-period lag of public pension funds collection rate was then used to estimate the one-period lag of old-age dependency ratio and exogenous variables with the panel least squares method to obtain the fitted value of the one-period lag of public pension funds collection rate. The fitted value serves as a proxy variable for the one-period lag in public pension funds collection rate. The threshold value of the old-age dependency ratio on collection rate was then calculated using the estimation method of a non-dynamic panel threshold model. The sample was divided into different intervals based on the threshold value, and the threshold coefficient was estimated at each interval using the two-step system GMM method. The estimation results in rows 1 and 2 of Table 4 show that the old-age dependency ratio has a single threshold effect on collection rate at the 5% significance level, with a threshold value of .5439. Furthermore, the likelihood ratio test revealed the existence of a single, relatively significant threshold value (see Figure 3).

Threshold Value Estimation and Significance Test.

Single threshold LR map of threshold effect regression.

Dynamic Panel Threshold Estimation

In the subsequent step, we estimated the impact of pension payment pressure on collection efficiency using a dynamic panel threshold model. The sample was divided into two intervals with the old-age dependency ratio based on the above-mentioned threshold value of .5439. To resolve the problem of endogeneity, the first-order and second-order lagged values of the old-age dependency ratio were used as instrumental variables, and the two-step system GMM method was used to test the threshold effect of the old-age dependency ratio on collection rate. In the estimation results in the first column of Table 5, the Hansen’s test results show that the instrumental variables used in this study are reasonable, and the AR(2) test results show that there is no serial correlation.

Dynamic Panel Threshold Estimation Results.

According to the estimation model of the old-age dependency ratio and collection rate, there are greater differences in the coefficients of the major variables when the old-age dependency ratio is greater than .5439 and when it is less than or equal to .5439 (see column 1 of Table 5). When the old-age dependency ratio is greater than .5439, the coefficient of the old-age dependency ratio is −.149, which is not significant. 7 When the old-age dependency ratio is less than or equal to .5439, the old-age dependency ratio coefficient is .294, which is very significant, this demonstrates that pension payment pressure has a positive slope threshold effect on fund collection rate.

Robustness Test

The robustness test was primarily conducted in two phases. First, the core variables were substituted, which primarily entailed replacing public pension funds collection rate with the actual contribution rate of public pension funds as the explained variable and examining the robustness of the results. Changes in public pension funds collection rate are primarily caused by changes in the ratios of the number of people enrolled in old-age insurance and the ratio of income to public pension funds contribution in collection revenue, which eventually result in a change in the public pension funds actual contribution rate. If the research findings are robust, the direction of the impact of the old-age dependency ratio on the public pension funds actual contribution rate should be the same as the direction of the impact of the old-age dependency ratio on the public pension funds collection rate. Second, a system GMM estimation was conducted using the higher-order lag variable of the old-age dependency ratio as its instrumental variable.

Non-Linear Relationship Test

After substituting the variables, we used the old-age dependency ratio’s first- to fifth-order lag variables as its instrumental variables. The test results show that the impact of the old-age dependency ratio and its square term on the actual contribution rate of public pension funds (columns 4, 5, and 6 in Table 3) are in the same direction as their impact on public pension funds collection rate (columns 1, 2, and 3 in Table 3). This indicates an inverted U-curve relationship between the old-age dependency ratio and the actual contribution rate of public pension funds, thus demonstrating that the estimation results are robust.

Threshold Effect Test

After substituting the variables, the threshold value estimation and significance results (rows 3 and 4 in Table 4) show that only a single threshold exists in the model and that the threshold value is consistent with the first two rows. Only the F value and the corresponding critical value show a change after the variable substitution, indicating that the estimation results are robust.

Dynamic Panel Threshold Estimation

After substituting the variable and using the high-order lag variable of old-age dependency ratio as its instrumental variable, the dynamic panel threshold estimation results in the second column of Table 5 show that the sign and significance of old-age dependency ratio did not change significantly, which is consistent with the results in the first column. When the old-age dependency ratio is greater than .5439, there is a non-linear inverted U-curve relationship between the old-age dependency ratio and the actual contribution rate of public pension funds, which is consistent with the previous analysis results demonstrating that the research findings are robust.

Policy Recommendations

Using panel data of provinces and municipalities in mainland China from 2010 to 2015, this study developed a dynamic panel threshold model to test the impact of the old-age dependency ratio on the collection efficiency of public pension funds for urban employees. This study revealed how pension payment pressure is a direct factor that determines the collection efficiency of public pension funds. Due to regional differences in terms of the pension burden and financial capabilities, as well as the ability of local governments to rely on central government finance, the former is free to determine the strength of their collection and supervision efforts. To improve the collection efficiency of public pension funds, the following measures are therefore suggested.

First, there is a need to change the institutional environment of soft constraints on responsibilities. Relevant laws and regulations should be promulgated to further clarify the specific responsibilities of the central and local governments in the old-age insurance system to increase the motivation of local governments to achieve greater collection efficiency. The first step is to clarify the fiscal responsibilities of the central and local governments. All funds relating to contributions and payments of public pension funds should be under the unified management of the central government, while the deficits of pension fund payments in regions with higher old-age dependency ratios should be jointly borne by the central and local governments. The second step is to clarify the basic accounting and information management responsibilities of local government departments. Local social insurance departments should be responsible for pre-collection work and ensuring the authenticity of the basic accounting of contributions. Primary-level government departments should manage the accounts of system members to ensure accuracy and consistency of information relating to their survival, employment, and coverage. The third step is to strengthen the supervisory responsibility of local governments toward old-age insurance. The development of old-age insurance should be included in the performance evaluation indicators of local governments at all levels to ensure accountability.

Second, it is necessary to optimize the institutional structure. Using the opportunity presented by placing pensions under the state’s unified administration, it is necessary to optimize the system structure simultaneously and resolve the problems of fund deficits faced by the pension system in current and future payments after the current contribution rate of schemes is lowered. A non-contributory institutional pillar is recommended to be built to support the reduction of old-age insurance contributions while also providing a certain level of pension protection. The funds for the non-contributory pillar can be drawn from revenues earned through state-owned assets and general taxation, while the responsibility of raising funds should be reasonably shared by the central and local governments. On this basis, it is necessary to determine an appropriate enterprise contribution rate to improve the collection efficiency of public pension funds.

Conclusions

The research in this study shows that there is an inverted U-curve relationship between old-age dependency ratio and collection rate of public pension funds for urban employees. The impact of the old-age dependency ratio on the collection rate of public pension funds has a significant single-threshold effect, and the threshold value is .5439. When the old-age dependency ratio is less than or equal to .5439, increasing the old-age dependency ratio will correspondingly increase the collection rate of a local government’s public pension funds; when the old-age dependency ratio exceeds .5439, a further increase in the old-age dependency ratio will lead to a decrease in the regional collection rate of public pension funds.

The soft budget constraints imposed on public pension funds payments by local governments are apparently the root cause for the above-mentioned phenomena. When the old-age dependency ratio is less than or equal to a certain threshold, the increase in the old-age dependency ratio will lead to an increase in the pressure to balance the revenue and payment of public pension funds. To ensure pension payments are made in full, the local government will increase the collection efficiency of public pension funds, and hence a positive correlation is noted between old-age dependency ratio and collection rate; when the old-age dependency ratio exceeds a certain threshold, to avoid imposing a heavy burden on the development of enterprises and weakening the competitiveness of the regional economy, the local government will choose to transfer a part of the responsibility for pension payments to the central government and reduce its efforts to collect pension contributions; hence, a negative correlation develops between the old-age dependency ratio and the collection rate.

At present, China strives to bring public pension funds for urban employees under the unified administration of the central government, the local governments’ responsibility for making pension payments has decreased, which may further deteriorate the institutional environment of soft constraints imposed on local governments’ responsibilities and reduce the collection efficiency of public pension funds. It is necessary for the Chinese government to take measures to change the institutional environment of lenient constraints on local government responsibilities, while focusing on improving the structure of the public pension system.

Footnotes

Appendix: Definitions of Relevant Variables

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Key Program of National Social Science Foundation of China (Grant No.21AGL023), the Postgraduate Scientific Research Innovation Project of Hunan Province (Grant No.CX20210545), and the Postgraduate Scientific Research Innovation Project of Xiangtan University (Grant No. XDCX2021B030).