Abstract

The primary aim of our research was to examine the moderating role of prevention focus (PRE) and the mediating role of risk perception (RP) on the relationship between driving accident history (DAH) and insurance coverage (IC) decisions to test this moderated mediation mechanism. We collected survey data from 808 newly eligible voluntary automobile liability insurance policyholders in Taiwan and analyzed the data using PROCESS macro. The estimated results showed that PRE moderated the indirect effect of DAH on IC through RP. In general, a worse DAH would increase the RP of people who were high prevention-focused, thereby increasing their willingness to purchase a higher IC. Conversely, a worse DAH would not increase the RP of people who were low prevention-focused, and such people would not increase or would even decrease their IC. The results provide an explanation for the inconsistent paths from DAH to IC in the literature. From a marketing perspective of psychographic segmentation, our research helps insurance companies to determine what types of consumers they should pay more attention to and to formulate marketing strategies.

JEL: D91 G52 E21

Keywords

Introduction

The amount of insurance coverage an individual should purchase is a central topic in insurance studies (e.g., A. Cohen & Einav, 2007; A. Cohen & Siegelman, 2010; Sydnor, 2010; Szpiro, 1985). Some researchers have found that many people, for whom insurance is worth purchasing, may choose to curtail insurance coverage, while those who appear to be in less need of insurance may seek more insurance coverage, even at excessive prices (e.g., Cutler & Zeckhauser, 2004; Cutler et al., 2008; Michel-Kerjan & Kousky, 2010; Sydnor, 2010). People may also rely primarily on feelings and intuition rather than carefully thought processes when deciding the amount of insurance coverage to purchase (Austin & Fischhoff, 2010; Hsee & Kunreuther, 2000; Sunstein, 2003). In addition, the nature of this decision-making maybe a result of intuitive thinking related to experience and emotional reactions (Botzen et al., 2015).

To explain the influence of consumers’ past experience on their insurance purchase decisions, some insurance studies have adopted two concepts of intuitive thinking: the availability heuristic and representativeness heuristic. Availability heuristic describes people’s the tendency to how easily an instance comes to mind to judge the likelihood of an event. On the other hand, representativeness heuristic, which could lead to a cognitive bias known as the gambler’s fallacy describing the erroneous reasoning about the probability of future random events would be influenced by previous instances of this type of the event. (e.g., Jaspersen & Aseervatham, 2017; Lin, 2020; Papon, 2008). If the availability heuristic dominates an individual’s insurance consumption behavior, the individual tends to overestimate the probability of risk after experiencing losses, and they will thus be willing to buy higher insurance coverage. On the other hand, if the representativeness heuristics conquers, the individual often underestimates the risk after experiencing losses, thereby opting for not to increase or even decreasing their insurance coverage. In addition, price is also a key element in determining the amount of insurance coverage purchased (Esho et al., 2004). Previous literature has demonstrated a negative impact of insurance price on the willingness to purchase high insurance coverage (e.g., Awunyo-Vitor, 2012; Esho et al., 2004).

Most researchers investigated the availability heuristic and representativeness heuristic in natural hazard insurance (e.g., Browne & Hoyt, 2000; Tian et al., 2014; Yin et al., 2016); however, not many research efforts have addressed the influence of these psychological factors on automobile insurance. So, we took price effect into account and discussed its influences on automobile insurance demand. The objectives of this paper were not only to exam how the above factors influence consumers’ purchasing decisions on the amount of automobile liability insurance coverage, but also investigate whether and, if yes, when these factors will impact consumer’s decisions through introducing prevention focus (PRE) and risk perception (RP). Furthermore, we examined the impacts of these factors (PRE and RP) on the relationship between driving accident history (DAH) and purchasing decisions on the amount of automobile liability insurance coverage (IC). Based on the empirical evidence from a sample of voluntarily participating automobile liability insurance policyholders in Taiwan, we found that RP played a crucial mediation role in the relationship between DAH and IC. Moreover, we noticed that PRE moderated not only the relationship between DAH and IC, but also the relationship between DAH and RP. Our results showed that availability heuristic and the gambler’s fallacy coexist during the process of decision-making, and the effect of each of these factors on IC depended on an individual’s level of PRE. We believe that considering individual differences is a critical procedural measure when dealing with consumers’ insurance coverage selections.

Seeking to contribute to the literature aimed at consumers’ automobile insurance coverage decisions, this study includes the following four stages. First, this study provides a nonexistence examination of the moderated mediation mechanism on the relationship between DAH and IC. The analysis of this mechanism informs the impact of psycho-social variables on insurance purchasing, which consequently helps enrich studies on the behaviors of consumers in the insurance market. The findings on the moderating effect of PRE and the mediating effect of RP explain the inconsistent results of the path from DAH to IC in the literature (e.g., Hsu et al., 2015; Shi et al., 2012). Second, some previous studies have addressed the impact of PRE on the willingness of IC, but we believe that determining what amount of insurance coverage individuals prefer to pay plays a more crucial role in the field of insurance marketing. To fill this gap, our study focuses on the real amount of insurance coverage that consumers would choose rather than whether they are willing to buy. Third, some psychological studies on insurance purchasing behavior have placed substantial emphases on catastrophic risks such as flooding (Botzen et al., 2013), and they have involved hypothetical scenarios (Hsee & Kunreuther, 2000; Robinson & Botzen, 2019) and in-depth interviews with small samples (Austin & Fischhoff, 2010). Instead, our study considers insurance coverage decisions for everyday risk that people may encounter when driving in order to inform more common insurance decisions and consultation practices. We have analyzed answers from the consumers and data from an insurance firm to understand the psychological effects targeting in auto insurance marketing. Fourth, this paper outlines the practical implications of the findings for insurance companies. Prevention focus is not only a chronic characteristic that differs from one individual to another but also an induced state that is susceptible to contextual effects (e.g., Bian et al., 2019). Therefore, insurance companies can resonate with their potential consumers by creating matching marketing strategies through the perspective of psychological segmentation. Our results can help insurance companies understand consumer behavior, grasp their needs, and provide effective promotional plans. Because of the profound impact of marketing strategies on how people understand life, the world, and themselves, we cannot ignore the ethics in marketing strategies, especially in advertising (Brenkert, 1998; Murphy, 1998). Therefore, we should be careful about using prevention focus in insurance advertising. When making insurance advertisements, the insurers should not only consider whether they violate the law nor only focus on their own interests, but also take ethical factors into account.

Literature Review

Automobile Liability Insurance

Automobile insurance is used to cover the risk of liability loss exposures, property loss exposures, and personal loss exposures arising out of the ownership, maintenance, or use of automobiles (Cook, 2014). According to Li et al. (2013), the Taiwanese automobile insurance market is implemented with compulsory insurance and voluntary insurance. Compulsory insurance is only liable on no-fault compensation associated with the personal injury of the victim in a car accident, while voluntary insurance covers vehicle damage and voluntary liability as well as risks such as mishaps to the car itself, bodily injury, and other property damages caused in an accident. In our study, we focus on voluntary liability insurance, and its coverage is preserved for third-party victims. These are the victims who are outside of the covered car in a traffic accident due to the negligence of policyholders rather than policyholders themselves (Vaughan & Vaughan, 2008). Unlike the vehicle damage insurance, which depends on the value of policyholders’ own car, the automobile liability insurance is related to an estimation of the amounts of damage the policyholders are obligated to pay for the victims. Since the potential automobile liability exposure is theoretically unlimited, there is no fast and easy method to determine how much liability insurance should be purchased because policyholders do not know what kinds of objectives they may run into or how severe someone’s injury they may cause in advance. This makes it difficult to assess the severity of the potential damage since the exact amount of damage that the driver must pay if they are liable is unknown (Hamilton et al., 2002).

Availability Heuristic and Gambler’s Fallacy

According to the definition of the availability heuristic in Papon (2008), individuals may underestimate the likelihood of an event if they have never been exposed to it, whereas they will overestimate the likelihood of the event if they have experienced it. The results of Perloff (1983) study showed that the availability heuristic is strongly related to past experience (i.e., driving accidents), since personally experienced events are easier to access or recall from a cognitive perspective. Consequently, people become inaccurate in judging the relative risks involved in frequently occurring events due to availability risk (Levi, 2009). As Chen et al. (2022) indicated that drivers with no experience in accidents tend to underestimate driving risk. Therefore, individuals without past loss experience may dismiss the risk and remain uninsured, while those who have recently been involved in a loss tend to exaggerate the risk and purchase more insurance coverage.

As for the gambler’s fallacy, it describes the erroneous reasoning that the probability of a random event is less likely to occur in the future, if a comparable known event has occurred, and in a situation where these occurrences are independent of one another (Clotfelter & Cook, 1993). According to Kovic and Kristiansen (2019), the origin of the gambler’s fallacy is prior experience (i.e., driving accidents). If people believe that risk is cyclical, such as the gambler’s fallacy, they might think, “Since I had an accident this year, I am unlikely to have another accident in the next few years (Levi, 2009).” As a result, individuals underestimate the likelihood that the event they have just observed will reoccur because risk perception relies on past experience (M. Cohen et al., 2008). Therefore, if an individual has recently experienced a loss, they may be reluctant to purchase or increase their insurance coverage since they bet that the accident would not occur twice in a row (e.g., Ganderton et al., 2000; Jaspersen & Aseervatham, 2017).

In insurance context, many researchers have addressed the effect of availability heuristic and the representativeness heuristic on natural hazard insurance (e.g., Botzen et al., 2015; Tian et al., 2014). People who have experienced a flood have a strong awareness of flood risk and perceptions of the likelihood of flooding and damage, which in turn give rise to a strong desire for insurance (e.g., Botzen et al., 2015; Tian et al., 2014). Doidge et al. (2019) found evidence of the gambler’s fallacy from some experienced agricultural producers in land conversion and crop insurance decisions. Moreover, Kamiya and Yanase (2019) concluded that both availability bias and gamblers’ fallacy explain the effect of past loss experiences on earthquake insurance take-up. In this study, we aim to validate whether the purchasing behavior of automobile insurance can also be explained by the heuristics, since the fundamental principle of these different types of insurances is to allow consumers to pay a reasonable amount of money to prevent huge accident losses that may occur (Schlesinger, 2013).

Price Effect

In Taiwan, an insurance company determines the premium of an insured by their bonus-malus system (BMS), which takes the insured’s driving accident history into account (see Hsu et al., 2015, for a review). A high price of automobile insurance will be charged if one has a bad driving history (Li et al., 2013). Consequently, an individual with bad driving records may buy less insurance if they have a budget constraint (Austin & Fischhoff, 2010). This gives a good account of a negative correlation between driving accident history and insurance demand.

In insurance markets, policyholders may include their personal information in the decision to purchase insurance. When they have hidden information that is essential to the contract and cannot be observed by the insurer, adverse selection anticipates that high-risk people will increase their insurance coverage (Forsstedt, 2014). However, in the current study, driving accident history is a type of public risk information that can be obtained by consumers as well as insurers. Therefore, the problem of adverse selection can be ignored in our analysis.

Prevention Focus

The regulatory focus theory is a conceptual framework for motivation and behavior that is assumed to coexist in every individual who is fundamentally either promotion-focused or prevention-focused when making a decision, of which one may be temporarily or chronically stronger than the other (Higgins, 2000). That is, prevention focus and promotion focus have been conceptualized as independent constructs, and one of these two modes may be related to a certain phenomenon while the other may not (Keller et al., 2015). Promotion focus is concerned with an attainment of accomplishments, aspirations, and gains/non-gains, while prevention focus (PRE) is related to responsibilities, safety, and loss/non-loss. Individuals with promotion focus tend to be more sensitive to positive changes to the status quo, whereas individuals with prevention focus tend to be more sensitive to negative changes. Previous studies have found that, when people plan to build financial buffers, a stronger prevention focus is associated with less financial risk tolerance, which in turn provokes greater saving intention (Magendans et al., 2017). Cho et al. (2014) identified that prevention-oriented individuals are more likely to save for prevention goals, such as minimizing loss, being safe, and avoiding danger, than promotion-oriented people. Sekścińska et al. (2016) drew our attention to the fact that situational prevention-motivated people tend to build more conservative investment portfolios than situational promotion-motivated individuals. In our context, insurance is to accommodate uncertainty and a changing environment while avoiding losses and preserving capital (see Flitner, 2010, for a review). Therefore, in our study, attention will be given to the influence of prevention focus on automobile insurance.

Risk Perception

Risk perception is a subjective judgment made by people on the characteristics and severity of risks (Slovic et al., 1982). The effects of any variables on risk-taking behavior are mediated by risk perception (Sitkin & Pablo, 1992; Venkatraman et al., 2006). Researchers have always seen risk perception as an important predictor of risk prevention actions when people are facing diseases or negative events, and they have evidenced the positive relationship between risk perception and risk prevention behavior (Lopez-Quintero & Neumark, 2010; Rimal & Juon, 2010). Some insurance studies have even suggested that risk perception signifies risk mitigation behavior, such as insurance purchasing decisions (e.g., Botzen & van den Bergh, 2012; Jeleva & Villeneuve, 2004). For instance, insurance demand is low if risk perception is low (Zhou-Richter et al., 2010). As argued by Kunreuther (1996), people who believe the risk is unlikely to occur are not worried about the consequences and, accordingly, they do not want to buy insurance. If the risk is perceived to be relatively high, then the interest in purchasing insurance rises.

Hypotheses Development

In general, what influences decision outcomes the most is the actual condition in which people are making decisions. All sorts of things affect decision-making: the nature of the decision someone is making, the options available, the past experiences of decision makers, and so on. In general, people may become risk-averse, tending to avoid risk as much as possible, if they experienced prior losses (Hoffmann et al., 2013). However, in the field of insurance study, opinions diverge on the relationship between people’s driving accident history (DAH) and their purchasing decisions on the amount of automobile liability insurance coverage (IC). For instance, Hsu et al. (2015) have observed that people with bad driving records tend to purchase high automobile insurance coverage to protect themselves from the potential losses. However, Shi et al. (2012) have found that people with good driving records purchase high automobile insurance for a good driver discount, which provided an inducement to purchase. While it cannot be concluded whether driving accident history has a positive or negative impact on automobile insurance purchase decisions, the relationship between driving accident history and insurance coverage certainly exists. Therefore, we propose:

Hypothesis 1: DAH has a significant influence on IC.

Furthermore, we argue that the phenomenon of drawing conclusions about the effect of driving accident history on insurance coverage is due to the presence of other factors. Therefore, to ensure a thorough investigation, we will combine the two psychological factors of risk perception and prevention focus and put forward relevant hypotheses as follows.

Mediation Role of Risk Perception

Some insurance studies have suggested that risk perception (RP) is an important predictor of insurance purchasing decisions. For example, the insurance demand has been found to decrease if an insured’s RP reduces (e.g., Jeleva & Villeneuve, 2004; Spinnewijn, 2013; Zhou-Richter et al., 2010). Sitkin and Weingart (1995) have showed that the RP mediated the effects of outcome history on risky decision-making behavior. If we regard driving accident history as the outcome history and purchasing automobile insurance as a risky decision-making behavior, the mediation role of risk perception is expected.

As mentioned, both the gambler’s fallacy and the price effect can explain why people shrink their insurance coverage when they have a bad driving history. To clarify, when the gambler’s fallacy or the price effect dominates the other in the decision-making process of insurance coverage, we considered the mediation role of RP on the relationship between DAH and IC, as the individual’s risk perception would decrease affected by the gambler’s fallacy (M. Cohen et al., 2008). Therefore, if a bad accident history induces less risk perception, and less risk perception causes less insurance coverage purchase, we can conclude that the gambler’s fallacy exists. In other words, introducing risk perception as a mediator not only lets on about the contexts of the decision processes of insurance purchase, but it also distinguishes the influences of the gambler’s fallacy from the price effect on the relationship between DAH and IC to a certain extent. In light of these facts, we provide our second hypothesis as follows:

Hypothesis 2: RP mediates the relationship between DAH and IC.

Prevention Focus and Insurance

Prevention systems may affect drivers’ purchasing decisions on the amount of automobile liability insurance coverage (IC) for several reasons:

Chernev (2004) has showed that prevention-motivated individuals have a greater preference for maintaining the status quo than promotion-motivated individuals. Unlike other financial instruments, insurance is built primarily for dealing with the “pure risk” involving a chance of loss or no loss, instead of chance of gain or no gain (see Flitner, 2010, for a review). Insurance helps prevention systems be more affordable and accessible, since the fundamental principle of insurance is to allow consumers to spend small amounts of money, against the possibility of a huge unexpected loss, and to restore the status quo.

In addition, prevention focus (PRE) refers to obtaining security and avoiding harms. It underlies vigilance of safety and is highly compatible with avoidance strategies (Hamstra et al., 2011). Traditionally, insurance has been considered as the main tool for personal risk management. Purchasing insurance is related to prevention-centric behaviors, since it is associated with vigilance to avoid potential monetary losses. In our context, the purpose of people purchasing automobile liability insurance is to protect themselves from potential legal obligations and punishments when their car hurts others or damages another car or other property.

Moreover, we believe that prevention-focused individuals tend to purchase higher insurance coverage, since they want to avoid any anticipated regret. Based on the argument of Lim and Hahn (2020), chronically prevention-focused consumers are more likely to be regret minimizers because they tend to minimize negative outcomes. Avoiding regret by broadening insurance coverage is a strategy achieving a nonfinancial-prevention goal (Krantz & Kunreuther, 2007). Thus, prevention-focused individuals often view insurance as a protective device that helps them avoid future losses, maintain the status quo, and minimize regret.

Moderation Role of Prevention Focus

Some researchers have investigated the relationship between people’ past experience and their insurance decisions (e.g., M. Cohen et al., 2008), and some have even showed how the risk perception mediates this relation (e.g., Jaspersen & Aseervatham, 2017; Yin et al., 2016). However, we believe it is worth the effort to understand this decision-making process comprehensively by divulging the circumstance under which this relationship is positive or negative. In particular, we will focus on the relationship between driving accident history (DAH) and purchasing decisions on the amount of automobile liability insurance coverage (IC) by considering prevention focus (PRE) as a moderator. The different levels of PRE may be associated with stronger or weaker “avoidance” inclinations for undesired outcomes (Higgins et al., 1994). When facing potential monetary losses, individuals with a high prevention focus are more willing to adopt avoidance strategies than individuals with a low prevention focus.

Notice that budget constraints impact consumers’ insurance purchasing decisions as well. Individuals with a higher prevention focus accept a wider price range, while individuals with a lower prevention focus tend to narrow their latitude of price acceptance (Patil, 2011). As we noted earlier, if an individual has bad driving accident history, the price of automobile insurance increases. Individuals with a higher prevention focus may ignore the change of the price since they care more about potential monetary losses (Higgins et al., 1994), and accordingly, they buy more insurance coverage as an avoidance strategy to deal with potential losses.

When it comes to people with a low prevention focus and bad driving accident history, they are less sensitive to the consequences of potential losses (Higgins et al., 1994), but very sensitive to the increase in insurance prices (Patil, 2011). As a result, the high price suppresses their intention to purchase higher insurance coverage. This assertion leads to our third hypothesis, taking PRE as a moderator to analyze the relationship between DAH and IC:

Hypothesis 3: The relationship between DAH and IC is positive and rises sharply as PRE increases, and this relation turns negative as PRE decreases.

Let’s consider the relation between consumers’ driving accident history (DAH) and their risk perception (RP) by introducing the concept of individual differences. Opinions on this vary, as some researchers claim that the experience of traffic accidents promotes higher risk perception of drivers (e.g., Öhman, 2017), while others state the impact is not significant (e.g., Kouabenan, 2002). The heterogeneity of individuals’ characteristics may influence the effect of driving accident history on their risk perception. People distort a probability in decision-making when they are facing risks or undertaking other tasks (Zhang et al., 2020).

Let’s presume that prevention focus is related to a driver’s risk perception. Considerable evidence has shown that the tendency to overestimate the likelihood of a low-probability is a consequence of prevention focus (Kluger et al., 2004). Moreover, prevention focus influences risk perception significantly in different contexts, especially when people are driving (Werth & Förster, 2007). In light of these facts, we try to investigate the strength of the availability heuristic among people with different level of prevention focus. We thus claim that the availability heuristic would be more noteworthy for individuals with a higher prevention focus than those with a lower prevention focus. Specifically, the relationship between DAH and RP may be moderated by PRE. This leads to our next hypothesis:

Hypothesis 4: The relation between DAH and RP is positive and rises sharply as PRE increases, and this positive relation may be insignificant in people with low PRE.

Now, let’s assume that PRE and RP may both influence the relationship between DAH and IC. In general, when people with a relatively high prevention focus possessed bad driving accident history, they become more capable of recognizing and acknowledging their own past loss experience since they are more sensitive to the bad outcomes (Öhman, 2017) and want to avoid future negative events (Higgins et al., 1994). In terms of decision-making on the purchase of automobile insurance, they tend to increase their insurance coverage to protect themselves from potential losses. However, when people with a relatively low prevention focus encountered bad driving accidents, they are likely to disregard their loss experiences since they are less sensitive to these bad events (Öhman, 2017) and have less motivation to avoid the negative outcomes (Higgins et al., 1994). Thus, they would not increase their automobile liability insurance coverage. This leads to our last hypothesis:

Hypothesis 5: PRE moderates the indirect effect on the relationship between DAH and IC through RP. Specifically, we predict that among individuals who have high PRE, there will be a positive indirect effect of RP on the relation between DAH and IC. However, this indirect effect tends to be weaker, and it even becomes negative among individuals who have low PRE.

Previous studies have tested the effect of PRE on the willingness-to-pay of multi-year flood insurance (Botzen et al., 2013). However, few research efforts have inspected the moderating effects of PRE on the relationship between past experience and insurance coverage decision through RP. Aiming to understand this in the context of everyday driving risk, the main goal of this study is to test the role of PRE on the relationship between DAH and IC through RP. To achieve this goal, we have constructed the moderated mediation model, in which the possible moderating effects and mediating effects are modeled simultaneously, to explore plausible underlying processes of decision-making. The conceptual diagram of this study is summarized in Figure 1. Notice that it is an integration of moderation and mediation analysis into a single analytical model.

Conceptual diagram in the study.

Materials and Methods

Participants

A total of 808 newly eligible voluntary automobile liability insurance policyholders were recruited from an insurance company in Taiwan. As shown in Table 1, 54.2% of the participants were male, while 45.8% were female. The age of participants ranged from 20 to 77, with a mean of 37.87 and standard deviation of 7.44. Nearly 34.9% of participants had a bachelor’s degree or higher. The median annual household income was approximately NT$975,000 (US$34,700). As of December 31, 2020, the exchange rate was US$1 = NT$28.04. The mean years spent driving was 14.9, with a standard deviation of 7.2. The majority of participants (84.7%) were internal staff. The type of automobile insured was a private passenger vehicle with a policy period of 1 year. In Taiwan, voluntary automobile liability insurance provides supplementary benefits beyond compulsory automobile liability insurance. In Taiwan, automobile insurance consumers can obtain any coverage according to their risk appetite and income level. Insurance companies will calculate premiums based on the insurance coverage purchased by consumers, consumer demographic information, and experience rating coefficients calculated from claims reports (Li et al., 2013). There are more than 60% of car owners in Taiwan purchase this type of voluntary insurance that is included in non-life insurance. Taiwan’s 2021 non-life insurance premiums was US$ 24.36 billion. In addition, real GDP per capita this year is US$ 32,426.

Demographic Characteristics of Study Sample (N = 808).

Note. INC = annual household income; NTD = new Taiwan dollar; DY = driving years; GEN = gender (0 = Female, 1 = Male); EDU = education (0 = Junior college graduated or lower, 1 = Bachelor’ degree or higher); OC = occupation (0 = Internal staff, 1 = Field staff).

Procedure

This survey was conducted in two stages. In the first stage, we cooperated with an insurance company, inviting their consumers to complete a standardized, paper-pencil questionnaire with a risk perception scale and a prevention focus scale (see Appendix A). We offered a retail gift voucher of NT$100 (US$3.56) for each individual to encourage participation in the survey. Each participant was given detailed instructions before they answered the questionnaire and was informed that there were no right or wrong answers. The survey was processed anonymously, and the responses were kept confidential and not used for any other purposes. Each questionnaire took an average of 10 minutes to complete.

In the second stage, the participants’ basic information (i.e., gender, age, education level, occupation, driving years, and annual household income), records of their driving accident history within the past 2 years, and the amount of automobile liability insurance coverage purchased for the coming year were inquired from the information system of the company when the participants finished the survey. This study’s procedure has been reviewed by our institutional review boards, and it indicated that the survey did not need ethical approval, since the age of participates were all above 20 years old. No intervention or manipulation was necessitated.

Measures

Driving Accident History (DAH)

Participants’ driving accident history was measured according to the number of traffic accidents due to their faults during the last 2 years. The mean was 0.17, with a standard deviation of 0.37.

Amount of Liability Insurance Coverage (IC)

Consumers’ purchasing decisions on the amount of automobile liability insurance coverage was measured by the amount of coverage purchased from the newly eligible voluntary automobile liability insurance policy. Under the automobile insurance market in Taiwan, people are able to purchase any amount of coverage to protect themselves from potential financial losses. In this study, the amount of coverage ranged from NT$1.1M (US$38,732) to NT$5.6M (US$197,183). The mean of IC was NT$3.31M (US$118,040), with a standard deviation of NT$1.17M (US$41,000).

Risk Perception (RP)

The risk perception item was used to assess the subjective perception of traffic accident events. It referred to the assessment of how risky an individual is to a situation based on probability estimates. This risk perception item was a modified form adopted from the measure of perceived risk (Knuth et al., 2015), asking “How likely do you think you will be involved in a traffic accident in the coming year?” Perceived risk regarding a traffic accident was assessed by self-evaluating the likelihood on a scale from 0 to 100%. The mean and standard deviation of RP are 0.37 (37%) and 0.13 (13%), respectively.

Prevention Focus (PRE)

Participants’ prevention focus was measured by answering a modified form adopted from the General Regulatory Focus Measure (Lockwood et al., 2002). This scale responds to current and future events rather than past goal pursuits (Haws et al., 2010) and has been used as a measure of regulatory focus to predict risk tolerance when people plan to build their own financial buffer (Magendans et al., 2017) for many years. There were 9 items in this prevention focus scale, and a sample item was “In general, I am focused on preventing negative events in my life”. All items were rated on a 7-point scale, ranging from 1 (strongly disagree) to 7 (strongly agree), with the midpoint 4 labeled as neutral. The alpha coefficient for the prevention focus scale was .86 (N = 808), with the mean of 4.24 and standard deviation of 1.02

Control Variables (GEN, AGE, EDU, INC, OC, DY)

Referring to the outcomes from previous studies about insurance demand and risk perception, several relevant variables such as gender (GEN) (Jaspersen & Aseervatham, 2017; Öhman, 2017), age (AGE) (A. Cohen & Einav, 2007; Zhou-Richter et al., 2010), education (EDU) (Öhman, 2017; Robinson & Botzen, 2018) and annual household income (INC) (Andersson & Lundborg, 2007) were considered as control variables in our analyses. Moreover, previous research has indicated that occupation and driving experience could influence drivers’ levels of knowledge about risks and road accidents (Kouabenan, 2002). Thus, occupation (OC) and driving years of participants (DY) were also collected as control variables. The following nominal scales were used: GEN (0 = Female, 1 = Male), EDU (0 = Junior college graduate or lower, 1 = Bachelor’s degree or higher), and OC (0 = Internal staff, 1 = Field staff).

Data Analysis

The data analysis was conducted using SPSS 20.0 and PROCESS macro of Hayes (2018). Prior to the verification of our hypotheses, descriptive statistics and inter-correlations for all measures were examined. Besides, the data on promotion focus were also collected and analyzed when we did the pre-test. The results of the moderation test showed that the moderating effect of promotion focus did not exist when promotion focus and prevention focus were both treated as moderators. These results implied that promotion focus did not impact the relationship between driving accident history and insurance coverage. Thus, we did not consider promotion focus when we test our hypotheses. All pre-test results do not present to save space and can be obtained by email to the correspondence author.

A set of regression analyses for estimating and probing interactions among the variables was conducted to test our hypotheses. First, a simple mediation model was performed to test whether RP had an indirect effect on the relationship between DAH and IC with covariates (Hypothesis 1 and 2). Second, a simple moderation model was carried out to test the moderating role of PRE in the relationship between DAH and IC with covariates (Hypothesis 3). Finally, for testing Hypotheses 4 and 5, the moderated mediation model, with RP as a mediator and PRE as a moderator of DAH on IC, was used.

To probe the moderating effect of prevention focus, we adopted the Johnson-Neyman technique (Hayes, 2018; Hayes & Matthes, 2009) for identifying the regions of significance of the conditional effects of DAH on RP at values of PRE as well as DAH on IC at values of PRE. In order to allow the possible irregularity of the sampling distribution due to the indirect process, the bias-corrected bootstrap technique was administered to test the indirect and the conditional indirect effects (Hayes, 2018; Preacher et al., 2007), which also provided the index of moderated mediation. Specifically, if the index of moderated mediation was significantly different from zero, then we would conclude that the PRE serves as a moderator and RP serves as a mediator in the relationship between DAH and IC. Conversely, if this index was sufficiently close to zero, then the proposed moderated mediation model was not suitable.

Results

Inter-Correlations Analysis

Table 2 shows the correlation matrix. In our sample, RP, compared with the other variables except the controlled variables, had a highest positive correlation with PRE (r = .55, p < .01). The positive correlation between RP and IC (r = .39, p < .01) indicated that consumers would purchase more insurance coverage if their risk perception was relatively high. The positive correlation between PRE and IC indicated a higher-level prevention focus is associated with a higher amount of insurance coverage (r = .22, p < .01). PRE had a weakly negative correlation with DAH (r = −.07, p < .05). Besides, DAH was correlated negatively to IC (r = −.10, p < .01). Thus, our hypothesis 1 is supported primarily.

Inter-Correlations for all Measures (N = 808).

Note. DAH = driving accident history; IC = amount of automobile liability insurance coverage; PRE = prevention focus; RP = risk perception; GEN = gender (0 = Female, 1 = Male); INC = annual household income; EDU = education (0 = Junior college graduated or lower, 1 = Bachelor’ degree or higher); OC = occupation (0 = Internal staff, 1 = Field staff); DY = driving years.

p < .05. **p < .01.

Estimation and Inference

The results from the analyses testing whether RP mediated the relationship between DAH and IC are showed in Figure 2. Consistent with our expectation, the effects from DAH to RP (a = −0.034, p < .01) and RP to IC (b = 1.068, p < .01) were significant. In addition, the indirect effect of DAH to IC mediated by RP was significant (

Mediation effects of RP on the relationship between DAH and IC.

The relationship between PRE and IC by grouping participants into whether they experienced driving accidents during the past 2 years is presented in Figure 3. As shown, this relation was not significant if participants had not experienced any driving accidents; however, the relation appeared to be positive among the people who had experienced driving accidents. This result demonstrated the moderating effect of prevention focus on the relationship between PRE and IC, indicating that among people with a high prevention focus, having been involved in a traffic accident within the past 2 years, is more likely to purchase a higher liability insurance. On the other hand, people who have driving accident history is less likely to purchase high insurance coverage if the consumers are lower prevention-focus oriented. Thus, the moderator role of prevention focus on the relationship between driving accident history and insurance coverage has been revealed.

The relationship between prevention focus and amount of automobile liability insurance coverage.

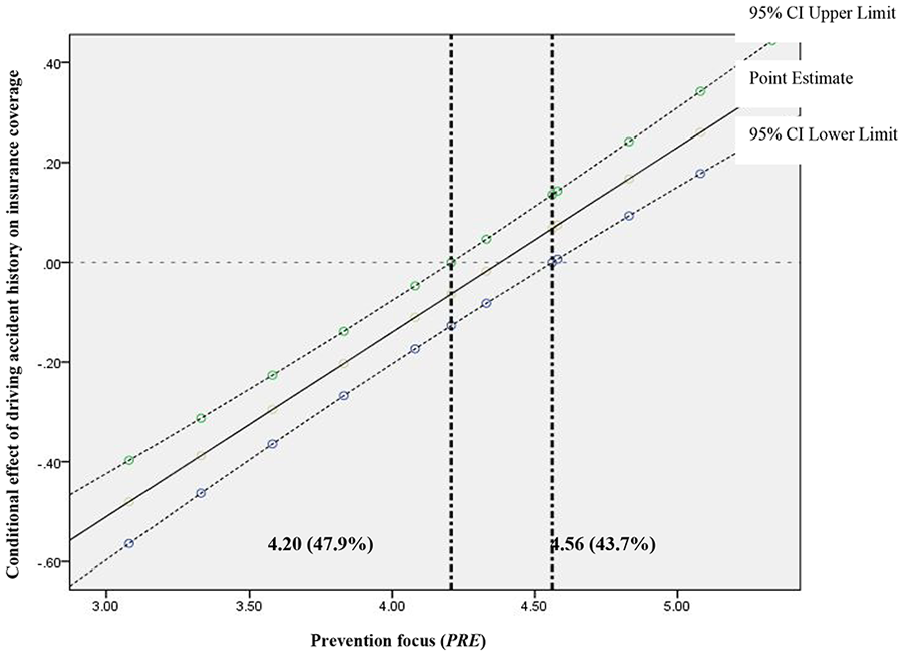

We took PRE as the moderator to test whether the relationship between DAH and IC depended on PRE (Hypothesis 3; see the results in Table 3). The computed F-statistics showed that the overall goodness of fit of the models was satisfactory. The coefficient of interaction between DAH and PRE was significant (B = .370, p < .01), indicating that prevention focus moderated the relationship between DAH and IC. Figure 4 presents the conditional effect (the solid line) of DAH on IC across the distribution of PRE. The two dashed lines represented the lower and upper bounds of the 95% confidence interval of the conditional effect. The sets of points at which the confidence interval is wholly above or below 0 are defined as the regions of significance. As can be seen, when PRE was greater than 4.56, the effect of DAH on IC was statistically positive; whereas when PRE was less than 4.20, the effect of DAH on IC was significantly negative. If the PRE was between 4.20 and 4.56, there is no sufficient sample evidence to warrant the relationship between DAH and IC. These findings support Hypothesis 3 to show that among individuals with low PRE, the relationship between DAH and IC is negative. The relation flattens and even appears positive as PRE increases.

Moderation Analysis Results (N = 808).

Note. DAH = driving accident history; PRE = prevention focus; RP = risk perception; GEN = gender (0 = Female, 1 = Male); Ln (IC) = logarithm of the amount of automobile liability insurance coverage; Ln (INC) = logarithm of annual household income; EDU = education (0 = Junior college graduated or lower, 1 = Bachelor’ degree or higher). OC, occupation (0 = Internal staff, 1 = Field staff); DY = driving years.

p < .05. **p < .01.

The Johnson-Neyman regions of significance for the conditional effect of driving accident history on amount of automobile liability insurance coverage at values of prevention focus.

Hypothesis 4 predicted a contingent effect of DAH on RP, with PRE serving as a moderator. Figure 5 expresses the relationship between PRE and RP by grouping our participants into whether they have experienced driving accidents (closed dots) or not (open dots) during the past 2 years. Some interesting findings were revealed here. First, among participants who had no driving accidents, the relationship between PRE and RP was positive, indicating that higher prevention-focused people were sensitive to perceive driving risks. Second, this positive relationship was increasingly stronger among participants who had experienced driving accidents, implying that both the gambler’s fallacy and availability heuristic coexist. In other words, people with a low prevention focus tended to ignore their worse driving accident history and even perceive less risk (i.e., the gambler’s fallacy), while those with a high prevention focus were much more sensitive to their past loss experience and have a higher level of risk perception (i.e., availability heuristic). Therefore, a moderating effect of PRE on the relationship between DAH and RP has been revealed. This study did not directly assume the gambler’s fallacy in Hypothesis 4. We only hypothesized that the positive relation between driving accident history and risk perception may become insignificant if people are low prevention-focus orientated. The authors will provide further interpretations in the discussion section.

The relationship between prevention focus and risk perception.

The results of risk perception with respect to the DAH, PRE, and DAH × PRE were listed in Table 4. The computed F-statistics suggested that the proposed model fits the data reasonably well. Specifically, it showed that the relationship between DAH and RP was contingent on PRE, with a significant coefficient of interaction DAH × PRE on RP (B = .083, p < .01). By implementing the Johnson-Neyman technique (Figure 6) to analyze the effect of DAH × PRE, we found a similar patter as in the Figure 4. The regions of significance were where the prevention focus was less than 4.10 or greater than 4.56. Such results explained that among individuals with a high prevention focus, the relationship between driving accident history and risk perception is positive, and this relation become less positive among those with a low prevention focus. Therefore, these findings supported the first part of Hypothesis 4 that the relationship between DAH and RP is getting positive sharply as PRE increases; however, for people who are low in prevention focus, the relation, instead of being positive, was significantly negative unexpectedly.

Moderated Mediation Analysis Results. (N = 808).

Note. DAH = driving accident history; PRE = prevention focus; RP = risk perception; GEN = gender (0 = Female, 1 = Male); Ln (IC) = logarithm of the amount of automobile liability insurance coverage; Ln (INC) = logarithm of annual household income; EDU = education (0 = Junior college graduated or lower, 1 = Bachelor’ degree or higher); OC = occupation (0 = Internal staff, 1 = Field staff); DY = driving years; W = index of moderated mediation; CI = confidence interval.

p < .05. **p < .01.

The Johnson-Neyman regions of significance for the conditional effect of driving accident history on risk perception at values of prevention focus.

Hypothesis 5 stated that the effect of DAH on IC was carried indirectly through RP, with this process being moderated by PRE. The prior analysis established that the path from DAH to RP was moderated by PRE. We then investigated whether RP mediated the effect of DAH on IC and whether PRE moderated the relation among DAH to RP to IC (see Table 4). The computed F-statistics suggested that the proposed model fits the data reasonably well. By holding DAH and PRE constant, we found that participants who perceived higher RP exhibited a stronger tendency to purchase more IC (B = .511, p < .01). In addition, the coefficient of the interaction of DAH and PRE (B = .327, p < .01) is less than the coefficient of the interaction in Table 3 (B = .370, p < .01). Therefore, RP partially mediated the effect of DAH on IC, which was consistent with the empirical results from some simple mediation analyses (Hayes, 2018).

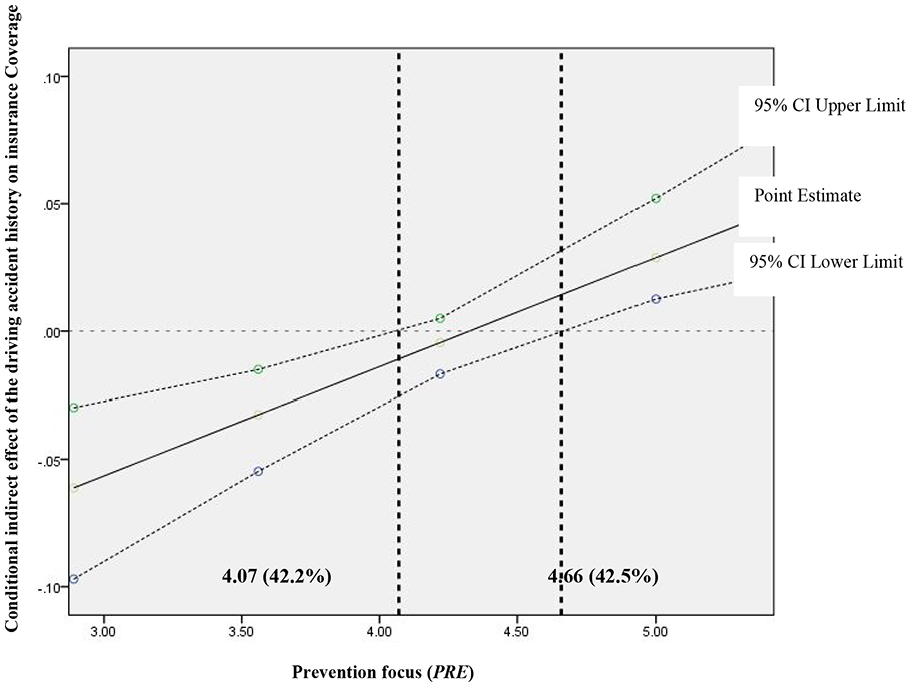

A statistically significant index of moderated mediation serves as the evidence of the moderated mediation effect (Hayes, 2015). In our study, the index of moderated mediation was significant (W = .042, CI [.022, .067]), suggesting that the indirect effect of DAH on IC through RP was moderated by PRE. We depicted the conditional indirect effect as the solid line in Figure 7. The upward slope of this line indicated that the conditional indirect effect rose as the prevention focus increased. We also generated 95% bias-corrected bootstrap confidence intervals for this effect at various values of PRE on the basis of 5,000 bootstrap samples. As shown in Figure 7, we found that the positive conditional indirect effect was statistically significant when prevention focus was greater than 4.66, while the negative conditional indirect effect was statistically significant when prevention focus was lesser than 4.07. These results indicated that among those with higher prevention focus, the indirect effect was positive, meaning that worse driving accident history led to greater risk perception, which in turn resulted in higher intention to purchase insurance coverage. On the other hand, among those with lower prevention focus, the indirect effect was negative, meaning that individuals’ risk perception did not increase with worse driving accident history. In other words, they did not perceive themselves as being involved in more risky situations, consequently resulting in a relatively low insurance coverage. Overall, the results supported Hypothesis 5.

The bias-corrected bootstrap regions of significance for the conditional indirect effects of driving accident history on amount of automobile liability insurance coverage as a function of prevention focus through risk perception.

As noted, the analyses also included a number of control variables: gender (GEN), age (AGE), education (EDU), annual household income (INC), occupation (OC), and driving years (DY). Looking at the effects of these variables, we found that, in general, gender (GEN) and age (AGE) had effects on RP. Women and older people reported higher levels of risk and concern than men and young people. Older people tended to purchase a large amount of insurance in order to avoid potential loss. As for the variable of occupation (OC), participants who were field staff tended to buy higher insurance coverage. The results from the impact of annual household income (INC) on IC indicated that perceived risk increased gently as income increased.

Discussion

In order to explore the underlying psychological processes on insurance coverage decision-making, our primary goal was to probe the role of PRE on the relationship between DAH and IC through RP, so one can apply the concepts to contribute towards better informing insurance markets. We have considered insurance coverage decisions for everyday driving risk and analyzed relatively large, real-world sample data from the automobile liability insurance. Overall, the findings corroborate our primary hypotheses, and the outcomes are in line with our predictions. The summary, the important implications from our study, and the recommendations for further research will be expatiated as follows.

Summary

First, our mediating effect test indicates that RP plays a partial mediating role in the relationship between DAH and IC. Worse driving history is related to less insurance coverage purchase, and we found that both the price effect and gambler’s fallacy can explain this result. In particular, RP, which is considered to be associated with the gambler’s fallacy, accounts for about 29% of this negative effect, while most of the negative effect, about 71%, is accounted for by budget constraints. In addition, the results of gender and age are consistent with the findings of Öhman (2017) and Hsu et al. (2015). The results of occupation indicated that field staff tended to buy higher insurance coverage since they were confronted with road accidents on a daily basis (Kouabenan, 2002). As for annual household income (INC), its result is consistent with research by Andersson and Lundborg (2007), who found that perceived road risk increases with an increase in income.

Second, we found that PRE moderated the relationship between DAH and IC (Hypothesis 3). Economists have argued that if driving accident records are known by insurance companies, individuals who possessed driving accident records have no incentive to buy more insurance coverage (e.g., A. Cohen & Siegelman, 2010). Under this situation, the short-term budgeting constraints discourage consumers to purchase insurance coverage if they are charged higher insurance prices due to their worse driving accident history. It must be noted that worse driving accident history is related to less insurance coverage, and this only applies to individuals with a low prevention focus. As for individuals with a high prevention focus, although they will be charged a higher price for insurance coverage, worse driving accident history instead implies more insurance coverage. Hence, individual differences should be a critical consideration when dealing with personal insurance coverage selection.

Third, we found that PRE moderated the effect of DAH on RP (Hypothesis 4). Our results show that policyholders with a high prevention focus are willing to recognize their driving accident history because they are more sensitive to negative outcomes. Moreover, this discovery highlights the viewpoint that PRE will lead to overweighting a low-probability event and result in an increase in RP (Bryant & Dunford, 2008; Kluger et al., 2004). This result is also consistent with Botzen et al. (2015) and Tian et al. (2014) who concluded that people who experienced floods tended to have greater risk perception of floods. It is interesting to note that the relation between DAH and RP, which was originally expected to remain positive though insignificant, has been found to be significantly negative among the policyholders with low PRE.

Finally, we have found that the indirect effect of DAH on IC through RP was contingent on PRE (Hypothesis 5). In fact, previous literature has demonstrated that the nonlinear probability weighting (i.e., a tendency to overweight these small probabilities) is an underlying psycho-behavioral response when people are making decisions on what amount of insurance that they should purchase (Barseghyan et al., 2013). People with higher PRE are more likely to overweigh the low-probability of loss. Therefore, for consumers with high PRE, DAH increases their RP, resulting in higher IC, indicating the existence of availability bias. Surprisingly, we have discovered that among those with low PRE, there is a negative indirect effect. In other words, low prevention-focused people tend to purchase lower insurance coverage when they possessed worse driving accident history. This is probably not only because they would be charged a higher insurance price (price effect), but also because they perceive themselves as less exposed to the risk of driving (gambler’s fallacy). According to Jaspersen and Aseervatham (2017), if a loss event occurs, people will judge its occurrence in the next periods as less likely. In our context, people with low PRE may trigger the use of the representativeness heuristic after the prior traffic accidents within the past 2 years. Consequently, they may think that these past accidents would not happen to them again in the coming year, which in turn would mean they buy less insurance coverage. These results are similar to the findings of Kamiya and Yanase (2019) for earthquake insurance. They found that both availability bias and gamblers’ fallacy explain the effect of past loss experiences on earthquake insurance take-up. As for the domain of driving, Levi (2009) concluded that a lack of accident experience would yield significantly lower scores of risk estimations of drivers and increase the prevalence of self-protective behaviors. According to Kunda (1990) which denoted that motivational factors may influence the perception of risk, we believe that prevention focus is the key to explain why both availability bias and gamblers’ fallacy co-exist in our context. To sum up, our study has provided empirical evidence for the argument that PRE plays a key factor in individuals’ RP in accordance with their driving accident history and, therefore, it has a major effect on the insurance purchasing decisions.

Contributions, Implications, and Recommendations

This study has gone some ways towards enhancing our understanding of the effect of prevention focus (PRE) in the relationship among risk perception (RP), driving accident history (DAH), and consumers’ purchasing decisions on auto insurance coverage (IC). Our findings have provided some important implications for improving automobile insurance marketing through a psychological approach.

First, a consumer who plans to buy automobile insurance may not be able to interpret their own driving styles, such as angry, reckless and careless, anxious, or careful driving, into accurate estimates of probability of an accident or scale of loss. In reality, this probability is almost never an objectively measured occurrence (Siegelman, 2004). In fact, to ensure an accurate portrayal of insurance coverage choice, earlier studies have indicated that studying the choices consumers make in insurance markets needs to include the psychological factor, which is not captured in standard economic models (e.g., Barseghyan et al., 2011). We have introduced PRE and RP to explore the relevant psychological mechanism substantially. Some controversial findings in the early literature (e.g., Hsu et al., 2015; Shi et al., 2012) can also be solved to a certain extent by employing the moderated mediation model from our study. We have also demonstrated that incorporating psychological factors into the model provides an effective means of demystifying the internal complexities associated with insurance purchasing behavior.

Second, two fundamental questions for insurance purchasing are identified: Should an individual buy insurance? And if yes, what insurance coverage would an individual prefer to buy? (Holtan, 2001) Previous studies have addressed the purchasing willingness of catastrophe insurance (e.g., Botzen et al., 2013), but the studies estimating the amount of insurance coverage an individual would like to buy were inadequate. Many people make the mistake of buying too little or too much insurance coverage (Kunreuther et al., 2013). The difficulty in buying a right amount of insurance coverage is compounded by the fact that people usually fail to purchase essential insurance coverage and spend too much on insuring unimportant risks (Vaughan & Vaughan, 2008). In light of these facts, we collected real-world data to analyze the role of prevention focus and risk perception in individuals’ choices, which would further be beneficial to figure out the psychological mechanism of insurance consumers.

In practice, insurance companies usually aim their efforts and resources to a target market consisting of a specific group of consumers. Beyond traditional market segmentation (i.e., the divisions of consumers based on geographic units, demographic variables, and their purchasing behavior), psychographic segmentation may help insurers address consumers’ needs through the division of individuals’ value, personalities, and attitudes. More often consumers’ regulatory states can be situationally induced (Higgins & Spiegel, 2004), either because people tend to think about certain products in a certain way or because they can actually be influenced on how they feel (Werth & Föerster, 2007). Insurance companies can motivate their potential consumers by offering a product or advertisement that fits with their regulatory focus, especially in those with low chronic prevention focus since they tend to inappropriately shrink their insurance coverage. Aaker and Lee (2006) demonstrated how companies can increase engagement by tailoring their message to fit consumers’ perspective. For example, insurers can use some prevention-focused messages or proverbs that can be presented as helping consumers avoid something negative or key pain points and helping them precisely perceive the traffic risk, which in turn encourages consumers to buy more insurance coverage to avoid potential monetary loss. Insurers can also design a scale to assess consumers’ prevention focus level according to the proverbs (Faur et al., 2017). Insurance agents may ask consumers to indicate their agreement with these proverbs before they make a decision about insurance coverage; gift vouchers can be used to encourage participation in this task. By identifying the prevention focus levels of their consumers, insurers can then be informed on how they should promote and advertise.

Another effective psychological marketing strategy for automobile insurance purchase is to manage online consumer reviews about the services offered by insurance companies. With the advancement of internet search capabilities, most consumers would look up relevant information about the product before making decisions. As a result, online consumer reviews, especially review volume (number of reviews available for a product) and review valence (ratings of a product), can significantly influence consumers’ purchasing decisions (Fox et al., 2018). In particular, review volume has a greater impact on consumers with a prevention focus in their decision-making and promote the sales of prevention-oriented products, such as insurance (Kordrostami et al., 2021). This point of view implies an effective marketing strategy for an automobile insurance product, which is based on prevention-focused mindset-based targeting: increase review volume appropriately while maintaining a decent review rating.

Our study has investigated consumers’ automobile insurance purchasing decisions through a psychological approach, and we would like to propose a number of aspects that could be examined by researchers to further test our framework. First, DAH is a type of public risk information related to the pricing decisions of insurance companies. Future studies could investigate whether the concepts of regulatory focus and RP could be applied to the relationship between purchasing decisions on the amount of automobile liability IC and other driving risk measures, such as overall distance driven, number of car rides, and speeding, that are unrelated to insurance prices (Geyer et al., 2019). Thus, one can construct a feasible way to scrutinize the existence of information asymmetry in insurance markets. Second, we have found an interesting result: low prevention-focused people who possess bad driving accident records tend to view themselves as a low-risk driver, which means that the gambler’s fallacy is more easily found in this group. Future studies could further explore this underlying mechanism. Third, other types of insurance policy, such as homeowner insurance, life insurance, or travel insurance, could also to be tested to understand the underlying psychological processes of coverage decisions. Fourth, since our participants were customers of a Taiwanese insurance company, the results may only be applicable to Asian cultural backgrounds. According to Hayakawa et al. (2000), automobile insurance purchase decisions vary across countries. That is because different countries have different designs of automobile insurance coverage and insurance marketing channel (Hsieh et al., 2014; Wang et al., 2010). For example, voluntary liability insurance includes third-party liability, accident liability, and other special liabilities in Taiwan. In particular, third-party liability and accident liability in Taiwan cover a third party inside or outside the vehicle. That is different from automobile insurance policies in the United States (Wang et al., 2010). Thus, we recommend that future studies include participants from various cultures and examine whether findings differ culturally. Fifth, it is beneficial to achieve insurers’ marketing goals by considering applications of regulatory fit. By well advising, insurance company can contextually activate consumers’ regulatory states to maintain their conditions of fit. Such marketing strategies remain open to various interpretations and are areas worthy of further study.

Footnotes

Appendix

Author Contributions

All authors contributed to the study conception and design. Material preparation, data collection and analysis were performed by Shi-jie Jiang, Feiyun Xiang, and Iris Yang. The first draft of the manuscript was written by Shi-jie Jiang and Feiyun Xiang. Iris Yang was responsible for writing-review and editing. All authors commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was financially supported by the Key Talents Project of Guangzhou University (Grant No. RZ2021011).