Abstract

This study enriches the current literature because it is the first to examine how foreign ownership and Investor attention affect the risk-taking behaviors of property and casualty insurance companies in Vietnam. This study is unique because it tests whether foreign ownership moderates the relationship between investor attention and the risk-taking behavior of insurance firms or vice versa. This study employs the Random Effect Models, Generalized Least Squares, Johnson-Neyman test, and simple slope analyses to analyze 28 property and casualty insurance companies from 2010 to 2022. The findings indicate that foreign ownership and investor attention increases the risk-taking behaviors of insurance firms. Moreover, the findings indicate that foreign ownership moderates the relationship between investor attention and the risk-taking behavior of insurance firms in Vietnam. The findings align with agency theory, stakeholder theory, limited attention theory, and prior literature. This study supports managers and policymakers in developing the insurance sector sustainably, especially in emerging markets.

Introduction

The insurance industry is vital for the economy, enabling risk transfer through insurance and reinsurance services and bolstering financial stability. This sector drives economic growth, significantly impacting stakeholders, and has become a key player in finance. Although the insurance sector is the least risky due to lower liquidity exposure (Caporale et al., 2017), growing integrations with financial markets, other intermediaries, and financial deregulations have heightened complexity and risk (Sharpe & Stadnik, 2007).

This study is conducted in Vietnam for the following reasons. Firstly, Vietnam’s Gross Domestic Product (GDP) has steadily increased, with an average annual growth rate of around 6% to 7% in recent years. The insurance industry accounted for around 1.5% of Vietnam’s GDP in 2010. By 2020, this proportion had risen to approximately 3.2%, indicating a substantial increase in market size. Besides, Vietnam offers significant market potential due to its large population, rising middle class, and growing consumer demand. Foreign investors see opportunities for market expansion and increased profitability by establishing a presence in Vietnam. Secondly, Vietnam’s participation in international trade agreements, such as the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP) and the European Union - Vietnam Free Trade Agreement (EVFTA), has provided favorable conditions for foreign investors and contributed to the growth of foreign ownership. These agreements have reduced trade barriers, improved market access, and provided legal protection for investments, making Vietnam an attractive destination for foreign companies. In 2020, despite the challenges posed by the COVID-19 pandemic, Vietnam attracted approximately $28.53 billion in foreign direct investment (FDI). Thirdly, investor attention is increasingly popular due to the development of internet services in Vietnam, implying that consumers have greater access to information before acquiring insurance policies. In Southeast Asia, Vietnamese internet development is only behind Singapore, Thailand, and Malaysia. The increase in traffic comes from user demand in the context of the Covid-19 lockdown, causing businesses to implement digital transformation. The role of insurance has gained prominence, particularly in light of the COVID-19 pandemic, which has amplified health-related challenges faced by both businesses and individuals. This has led to an increased interest in insurance as a protective measure. As public awareness of insurance importance grows in Vietnam, investors may engage in information-seeking behaviors to comprehend insurance products, coverage options, and providers. The diverse range of insurance needs, spanning life, health, property, and business insurance, is expected to drive substantial inquiries. Globally, the Gulf Cooperation Council (GCC) countries, characterized by shared oil and gas resources and cultural similarities, focus more on non-life insurance. Notably, motor and health insurance constitute the leading non-life segments within the GCC, contributing approximately half of the region’s non-life premiums (Bansal & Singh, 2021). Finally, the insurance industry is undergoing significant transformation due to the interplay of finance and technology. On the one hand, insurance is progressively becoming integral to individuals’ risk perception. Conversely, crises and economic downturns have spawned a multitude of insurance policy challenges (Y. S. Chen et al., 2022). The emergence of Artificial Intelligence (AI) is further shaping the industry, urging the adaptation of business models to align with AI-driven trends (Zarifis & Cheng, 2023).

In addition, the Vietnamese insurance industry has also been growing dramatically recently. The total premium of property and casualty insurance in 2020 reached 57 trillion Vietnam dong (VND), almost three times higher than in 2010. From 2015 to 2021, the total premium revenue in the Vietnam market has grown impressively from 19% to 26% per year. Life insurance premium revenue increased from 24% to 35% per year, and property and casualty insurance premium revenue increased from 8.5% to 16% per year. Furthermore, one of the essential functions of insurers is quantitative risk management, and risks represent threats and potential opportunities. Effective risk management helps insurers maintain a balanced portfolio of policies and avoid excessive exposure to high-risk or unprofitable segments (Akotey & Abor, 2013). Furthermore, risk management ensures that invested assets are diversified and generate adequate returns, helping insurers maintain solvency and meet policyholder claims even during adverse economic conditions. It also ensures they operate within acceptable risk thresholds.

Our study significantly extends the literature in the following ways. Firstly, Wen et al. (2019) and Gul et al. (2011) employed Ordinary Least Squares (OLS) to examine investor attention’s effect on financial risk. Besides, ElBannan (2015) and M. Chen et al. (2017) studied the impact of foreign ownership on the risk-taking of financial firms, and they employed Ordinary Least Squares (OLS), Random Effect Models (REM), and Fix Effect Models (FEM). However, Akbar et al. (2017) indicate that traditional estimations such as OLS, REM, and FEM may violate the heteroskedasticity and autocorrelation assumptions. Therefore, we close the Generalized Linear Model (GLM) to overcome potential heteroskedasticity and autocorrelation issues. Secondly, previous literature has examined the relationship between foreign ownership and the risk-taking behavior of insurance firms (M. Chen et al., 2017; ElBannan, 2015). Our study extends the literature by employing investor attention and foreign ownership interaction. Our study complements prior studies because we implement the Johnson-Neyman test to explore whether foreign ownership moderates the relationship between investor attention and risk-taking behavior. Johnson-Neyman estimations identify ranges of the moderator that exhibit significant predictor-outcome connections, shedding light on instances where moderation effects alter variable associations. Finally, our study is like Duong et al. (2022) because we collect investor attention data from Google Search Volume. While Duong et al. (2022) focused on constructing the investor sentiment index, our study is the first to examine how investors’ attention affects the risk-taking of insurance companies in Vietnam.

Che (2019) and Kouzez (2021) conducted research in developed countries such as the US and France, and their findings indicated that foreign ownership (FO) increases risk. In contrast, Ehsan and Javid (2018) as well as Agoraki et al. (2011) examined countries in developing and transitional stages, revealing that FO reduces risk. Our study focuses on Vietnam, a developing nation. However, our results align with Che (2019) and Kouzez (2021), suggesting that FO amplifies risk. Moreover, we discovered that foreign ownership moderates the connection between investor attention and risk-taking behavior.

Our study has yielded striking findings. Our analysis reveals that foreign ownership positively correlates with insurers’ risk-taking tendencies. Specifically, a percentage increase in foreign ownership reduces the Z-score (as the proxy of insurers’ risk) by 0.0057 percentage points, indicating elevated distress risk. These outcomes are consistent with previous research by Agoraki et al. (2011) and Ehsan and Javid (2018), aligning with the principles of agency theory. Furthermore, our investigation indicates that heightened investor attention influences insurers’ risk-taking behavior. Notably, a percentage increase in investor attention leads to a Z-score decrease of 0.3141 percentage points, signifying an increased distress risk. These results align with the concepts put forth by the limited attention theory and concur with the study by Hao and Xiong (2021). Finally, we figure out that the negative impacts of foreign ownership on the Z-score are even more pronounced when insurance firms have greater investor attention. These findings are consistent with research by Hao and Xiong (2021), M. Chen et al. (2017), and Kouzez (2021).

The structure of our paper is as follows. Section 2 describes the literature review and developing research hypotheses. Section 3 illustrates the data collection and methodology. Section 4 discusses the findings. Finally, section 5 is the conclusion.

Literature Review

The Proxies of Risk-Taking Behaviors

Extensive scholarly literature has examined diverse capitalization measures, such as solvency margins, required solvency margins, and ratios, to appraise firms’ financial robustness Rubio-Misas, 2020). However, constraining the analysis solely to capitalization metrics might be unduly limiting, necessitating a broader analytical framework to encompass the multifaceted determinants influencing insurers’ financial soundness (Cummins et al., 2017). An alternative gauge of risk, the Z-score, which transcends capitalization and bankruptcy considerations, offers an informative marker of insurers’ fiscal health (Pasiouras & Gaganis, 2013). Although conventionally employed within the banking domain, recent scholarship has also applied the Z-score to evaluate the financial viability of insurance firms (Rubio-Misas, 2020). Characterized by simplicity and transparency in computation (Bongini et al., 2018), the Z-score accommodates listed and unlisted entities. Its versatility extends to insurers adopting diverse risk strategies (Pasiouras & Gaganis, 2013); nonetheless, its utility is counterbalanced by limitations stemming from accounting quality concerns in nascent financial systems (Laeven & Majnoni, 2003) and its firm-centric evaluation that may disregard systemic repercussions (Bongini et al., 2018).

Theories

Agency theory is a contractual agreement between principals and agents to operate in the principal’s best interests. Suppliers, creditors, stockholders, and managers are all examples of agents. However, the interests of these parties may not be matched, resulting in agency costs (M. Chen et al., 2017). According to agency theory, ownership separation stimulates managers’ self-interest at the expense of shareholders, and international investors invest in other nations in search of a good return. As a result, foreign investors implement effective management monitoring to avoid managerial expropriation (Tornyeva & Wereko, 2012). Therefore, foreign investors also help reduce risks (Tornyeva & Wereko, 2012). Foreign investors frequently bring a fresh perspective and a distinct set of expectations, which can improve corporate monitoring and discipline (Wen et al., 2019). They are more prone to question management decisions and hold managers accountable for their judgments. This greater scrutiny can eliminate agency conflicts by aligning managers’ interests with those of shareholders.

Furthermore, foreign investors are less likely to be susceptible to the same biases or conflicts of interest as domestic investors by investing in companies from various countries and industries. Their existence broadens the shareholder base and minimizes power concentration, making it more difficult for any group to wield undue influence or engage in opportunistic behavior. Furthermore, foreign investors frequently bring knowledge, resources, and best practices from their home countries or international markets. This can include worldwide market knowledge, industry-specific experience, advanced technologies, managerial methods, and network connections. By pooling their resources, foreign investors can help improve corporate governance, risk management, and overall business success. Their participation can assist in reducing agency disputes caused by knowledge asymmetry and improve decision-making efficiency and effectiveness.

According to stakeholder theory, when managing risk, financial organizations should consider the interests of all stakeholders, including international investors. S. Chen et al. (2019) investigated the impact of foreign ownership on risk-taking behavior in financial organizations using stakeholder theory. Foreign ownership may impact the financial firm’s ability to manage risk. Foreign investors, for example, may have different risk management procedures or be unfamiliar with local rules, which could result in heightened risk. Foreign ownership may imply more significant risks since foreign investors are focused on generating shareholder profit, which can lead to conflicts with other stakeholders. As a result, foreign ownership can influence risk-taking behavior, such as underwriting and investment decisions.

The limited attention theory highlights the significant impact of information overload on investors’ decision-making processes. According to this theory, investors are exposed to vast information, leading to a diverse range of processing abilities (Hao & Xiong, 2021). In this context, individual investors are prone to becoming distracted by trivial and irrelevant details, diverting their attention from more critical aspects of their investment decisions. The rise of the internet has amplified this challenge. The sheer volume of online information can overwhelm investors, making it difficult for them to discern accurate and credible information from the noise. This inundation of data creates obstacles in the quest for precise and trustworthy information essential for making informed investment choices. When investors grapple with sifting through the abundance of information and attempting to identify relevant and reliable data, they may encounter several difficulties. These difficulties can lead to errors in judgment and suboptimal decision-making. Mistakes in assessing an investment’s true potential and risks can occur due to the inability to filter out extraneous information and focus on what truly matters. Therefore, investors misjudge the company. Besides, some investors have good information processing ability, leading to heterogeneous beliefs even on the same information on the internet, increasing the idiosyncratic risk of individual stocks.

Foreign Ownership and the Risk-Taking Behavior of Insurance Companies

Prior research investigated the association between ownership structure and risk, but mixed findings exist. ElBannan (2015), Agoraki et al. (2011), and Ehsan and Javid (2018) found that foreign ownership is associated with low risk-taking behavior. ElBannan (2015) stated that foreign companies have stable funding sources since they can access international markets and depend on their parents. Besides, they follow considerate policies in pricing and evaluating risks, contributing to risk reduction. Agoraki et al. (2011) and Ehsan and Javid (2018) argued that foreign investors have advanced information technology, which helps conduct operations among countries. Advantages of human resources, such as offering high skills to managers to work in their branches worldwide or training the local staff to work for them, contribute to better controlling risk. Foreign ownership, compatible with agency theory, reduces risk-taking behaviors. Foreign investors and the firm’s managers have a conflict of interest. As a result, we provide the following hypothesis:

H1: Foreign ownership negatively affects the insurers’ risk-taking behavior.

Conversely, Amor (2017) and Lassoued et al. (2016) reveal a positive relationship between foreign ownership and risky behavior. They argued that foreign owners would select new foreign managers who are often ill-informed about conditions in the nations where they operate due to their limited understanding, resulting in higher risk. Besides, M. Chen et al. (2017) and Kouzez (2021) reveal a positive relationship between foreign ownership and risky behavior. They demonstrated that foreign financial firms experience an informational disadvantage in a new market compared to domestic enterprises. Second, they are connected to their headquarters. If the parent corporations experience a crisis at home, they can reallocate resources to foreign branches, which decreases loans and forces them to accept risky assets transferred from headquarters. Their results are consistent with stakeholder theory. As a result, we provide the following hypothesis:

H2: Foreign ownership has a positive relationship with insurers’ risk-taking behavior.

Investor Attention and the Risk-Taking Behavior of Insurance Companies

Hao and Xiong (2021) report a positive relationship between investor attention and risk-taking behavior. They argue that many information sources on the internet will affect their accuracy, which increases the barrier to distinguishing accurate information, causing these investors to misjudge the company. Besides, some investors have good information processing ability and vice versa, leading to heterogeneous beliefs even on the same information on the internet, increasing the idiosyncratic risk of individual stocks. These results are consistent with the limited attention theory. Therefore, we propose the following hypothesis:

H3: Investor attention has a positive relationship with the insurers’ risk-taking behavior.

On the other hand, Wen et al. (2019), Gul et al. (2010), and Gul et al. (2011) find an inverse relationship between investor attention and risk-taking behaviors. Investor attention reduces information asymmetry because they are actively seeking relevant information. When investors search for information about a stock, they will efficiently collect and process the stock information. Therefore, these investors will have valuable information, and managers’ difficulty withholding bad news would reduce the information asymmetry between the companies and investors (Ding & Hou, 2015). These results are consistent with the agency theory. From the above arguments, we propose the following hypothesis:

H4: Investor attention negatively affects the insurers’ risk-taking behavior.

Investor Attention, Foreign Ownership, and the Risk-Taking Behavior of Insurance Companies

Insurance companies owned by foreign entities tend to take on higher levels of risk due to a combination of factors. M. Chen et al. (2017) and Kouzez (2021) shed light on this trend, highlighting that foreign financial firms, including insurers, often face an informational disadvantage when entering new markets compared to their domestic counterparts. This disadvantage arises from their limited familiarity with local market conditions, regulations, and consumer behaviors, which can lead to riskier decision-making. These foreign-owned insurers might also be interconnected with their parent financial firms in their home countries. Capital could be reallocated from foreign branches during an economic downturn in the parent company’s home market. This capital reallocation might result in reduced lending activities by the foreign branches and an increase in the acquisition of risky assets transferred from the headquarters. This scenario introduces an additional layer of risk to the foreign-owned insurers as they become exposed to the parent company’s financial challenges. Shifting focus to investor attention, Hao and Xiong (2021) emphasize that the level of attention from investors correlates with increased risk for insurance firms. Investors are exposed to many information sources in an era of information abundance on the internet. However, the proliferation of information can lead to complexities in evaluating the accuracy and reliability of the information received. This increased complexity acts as a barrier, making it challenging for investors to distinguish valuable insights from noise. Consequently, investors may misjudge a company’s prospects based on inaccurate or conflicting information, contributing to heightened risk. From the above arguments, we propose the third hypothesis:

H5: The interaction term between foreign ownership and investor attention positively increases risk taking behavior.

Other Determinants of Risk-Taking Behaviors

We estimate the insurance size by taking the natural logarithm of total assets. Because of the supposed availability of strong corporate governance structures and heightened regulatory scrutiny, larger insurers are thought to be less likely to engage in profit management. This is consistent with Che (2019), which found that larger insurers face more specialized regulatory inspections, fostering greater openness and accountability. Furthermore, the paragraph cites studies by Hammami and Boubaker (2015) and ElBannan (2015) that show a negative relationship between the scale of financial organizations, particularly insurers, and their risk-taking proclivity. Because of their scale, larger insurers may take a more risk-averse stance, which has ramifications for stability. The interaction, however, is complicated, as Chang et al. (2018) note that insurers can be biased.

Bierth et al. (2015) and Chang et al. (2018) highlight leverage’s significance in driving systemic risk contribution, implying its role in amplifying insurers’ impact on the broader financial system. Vo (2016) supports this by showing a negative correlation between leverage and risk-taking, suggesting that a higher leverage ratio encourages cautious risk attitudes. However, Kouzez (2021) argued that higher leverage levels are associated with lower risk within the insurance sector. This could stem from insurers’ risk aversion due to potential financial strain from defaults, regulatory limitations on leverage, enhanced investor confidence in stable financial positions, liability matching concerns, and the desire to mitigate systemic risk. However, the intricate relationship between leverage and insurance risk is influenced by factors like business models, market conditions, regulations, and strategic decisions made by insurers.

We include age, defined as the total years of establishment. Akbar et al. (2017) and Quaye et al. (2014) highlight that older firms exhibit more excellent stability, possibly due to accumulated experience. Bhagat et al. (2015) report a negative correlation between firm age and risk, suggesting that older insurers possess enhanced risk management skills.

Data and Methodology

Data

We obtain data from audited financial statements and Finpro, Vietnam’s premier data provider. We followed Dao (2022) to start our sampling period from 2010 to prevent the impacts of the financial crisis in 2008 on our regression results. We follow Eastman et al. (2018) in excluding insurance businesses with negative assets, capital, or net premiums. We follow Duong et al. (2023) in excluding data with inadequate information to calculate the needed variables. We also follow Duong et al. (2022) and winorize our sample at the 5th and 95th percentiles to mitigate the extreme value issue. The final sample includes an unbalanced panel of 251 annual observations from 28 property and casualty insurers from 2010 to 2022.

Variable Definitions

Dependent Variable (Z-Score)

The primary dependent measure of the regression analysis is the Z-score, widely used in empirical research to indicate distress risk (Dbouk et al., 2020; Elamer et al., 2018). Precisely, the Z-score is estimated as Z-score =

Investor Attention (TREND)

In academic research, the Google search volume index (SVI) has been employed by multiple studies to quantify investor attention toward stock prices, as demonstrated by Ding and Hou (2015). Since 2004, Google Trends has furnished weekly data on search frequency trends for specific terms, accessible at http://www.google.com/trends. This data reflects the ratio of searches for a given keyword to the total search volume over time. Investors’ searches often align with their interest in economic and financial events, as noted by Ding and Hou (2015), which underpins the utilization of SVI as a surrogate for gauging customer attention. Notably, considering Google’s dominance as the foremost search engine in Vietnam, as highlighted by Duong et al. (2022), it serves as a dependable source for procuring annual search data related to insurance companies, thereby serving as a proxy for measuring investor attention, particularly within the Vietnamese financial context.

Foreign Ownership (FO)

Prior studies examined the relationship between ownership structure and company risk (ElBannan, 2015; Huang et al., 2012). Following Huang et al. (2012), we calculate foreign ownership by the percentage of ownership owned by foreign investors.

Interaction Terms (FO * TREND)

We follow Saghi-Zedek (2016) to add the interaction term FO*TREND. This interaction term allows us to test whether insurance firms with higher foreign ownership and investor attention have higher risk-taking behavior.

Model Construction

Prior studies estimate Return on Risk-Weighted Assets (RROA) and Return on Risk-Weighted Equity (RROE) to measure the volatility of profitability. These are the risk-taking measures employed commonly in non-financial corporations. This study measures insurance firms’ risk-taking by calculating the Z-score, the most frequently used ratio in financial studies (Dbouk et al., 2020; Elamer et al., 2018). The Z-score reflects insurer stability and is inversely related to risk-taking because a higher Z-score implies lower default risk (Elamer et al., 2018).

We follow ElBannan (2015) to employ model (1) to examine the effect of insurers having foreign ownership on Vietnam’s insurers’ risk-taking behaviors. We follow Hao and Xiong (2021) to employ model (2) to examine the effect of insurers’ investor attention on Vietnam’s insurers’ risk-taking behaviors. We add investor attention and foreign ownership in the model (3) to estimate the impact of foreign ownership or investor attention on Vietnam’s insurers’ risk-taking behaviors. We follow Saghi-Zedek (2016) to add FO*TREND in the model (4) to estimate the interaction between insurers having foreign ownership and investor attention on the risk-taking behaviors of insurance companies. The econometric form of these models is stated as the following specifications:

Where Z-SCORE proxies for insurers’ risk-taking, insurers take more risk when Z-SCORE is low. The explanatory variables are foreign ownership (FO), investor attention (TREND), and CONTROL, which denotes a set of control variables. We include four control variables such as total asset (SIZE), leverage (LEV), and year of establishment (AGE); the sign of “i” indicates cross-sections; the notation of “t” is time; “α” stands for intercept; ε is the error term. The

Estimation Procedure

To examine the effect of foreign ownership and investor attention on risk-taking in Vietnam’s insurers, we employed OLS, FEM, and REM. Following Duong et al. (2022), we used the Hausman and Breusch Pagan test, which showed that the random effects model is more appropriate for the study. However, Akbar et al. (2017) suggest that traditional estimations such as OLS, REM, and FEM may violate the heteroskedasticity and autocorrelation assumptions. Then, we employed the Durbin-Watson and Laplace Likelihood Ratio Test and found evidence that REM violates the autocorrelation and heteroskedasticity assumptions. Finally, we follow Pathan (2009) in employing GLM to effectively address issues related to the analysis’s autocorrelation and heteroskedasticity assumptions. Data dependency over time is called autocorrelation, whereas heteroskedasticity refers to uneven degrees of variability in error terms. Adopting Pathan’s approach demonstrates the researcher’s commitment to including a solid statistical tool within the study, strengthening the thoroughness and dependability of the study’s findings within the academic world.

In addition, this study employs moderated regression analysis. It employs Johnson-Neyman estimations to assess the potential moderating role of foreign ownership in the association between investor attention and risk-taking behavior. The Johnson-Neyman estimation method is a statistical approach utilized to examine moderation effects within regression analysis. Moderation arises when the impact of an independent variable on a dependent variable varies depending on the levels of another variable, called the moderator. Johnson-Neyman estimation aids in identifying specific values or ranges of the moderator where the connection between the predictor and outcome variables achieves statistical significance. This technique allows researchers to pinpoint circumstances wherein the moderator’s influence on the predictor-outcome relationship becomes noteworthy. Additionally, this testing procedure enhances comprehension of moderation effects and reveals the conditions under which associations between variables experience alteration.

Empirical Results and Discussion

Descriptive Statistics

Table 1 displays the sample’s descriptive statistics. According to this table, the average Z-score in Vietnamese insurers is 2.601, with a standard deviation of 0.995. This high standard deviation and the wide Z-score range indicate a significant cross-sectional variance in business risk. Furthermore, it has a right-skewed distribution because the average Z-score exceeds the median. The average FO is 50.944%, suggesting that foreign investors own 50.944% of all property and casualty insurance enterprises. The average TREND is 2.047, meaning that investors pay 2.047 attention to the insurance industry. The average TREND in Vietnam’s insurers is lower than in China, at 9.68 (Hao & Xiong, 2021), because China ranks first in the world regarding the population of countries and territories, while Vietnam ranks 14th. The average SIZE of insurers in Vietnam is 29.177, significantly higher than the average in China, just 18.27 (Che, 2019). LEVERAGE and AGE have a mean of 35.964 and 14.888, respectively.

Descriptive Statistics.

Note. Table presents the descriptive statistics. The data sample consists of 251 observations of 28 Vietnam property and casualty insurers from 2010 to 2022. All variables in the model are described in Appendix A.

Pearson Correlations Matrix

Table 2 shows the moderate relationships between variables. The most significant correlation between SIZE and LEV is approximately 0.56, indicating no possibility of multicollinearity. In addition, we examine the variance inflation factor (VIF) for multicollinearity. The mean VIF of the sample data is 1.665, indicating no multicollinearity.

The Pearson Correlation Matrix.

Note. Table presents the Pearson correlation matrix among independent variables. The sample has 28 Vietnamese insurers from 2010 to 2022. All variable definitions are reported in Appendix A. The symbols ***, **, and * signify the 1%, 5%, and 10% significant levels, respectively. The p-values are enclosed in parentheses.

Estimation Results From the Random Effect Model

We follow Shan et al. (2018) and Duong et al. (2023) to use the Hausman and Breusch-Pagan test to select the best analytical estimation method from OLS, FEM, and REM. According to the Hausman and Breusch-Pagan test, the REM is the best estimator for this research. Table 4 summarizes the REM estimations.

Table 3 shows the REM results for the entire sample. Table 3 demonstrates that FO and TREND significantly negatively impact risk, meaning that insurers with foreign ownership lower risk, as do insurers with investor attention. Furthermore, Table 3 shows that FO*TREND has a considerable positive influence on risk, meaning that insurers with investor interest and foreign ownership face additional risk.

Regression Results From Random Effects Model.

Note. This table displays the estimation results from Random Effects Model. Appendix A contains all of the variable definitions. The symbols ***, **, and * signify the 1%, 5%, and 10% significant levels, respectively. The t-values are in parentheses.

On the other hand, the Laplace Likelihood Ratio Test for Heteroscedasticity indicates that REM violates heteroskedasticity assumptions. Thus, we implement the Generalized Linear Models (GLM) to estimate the findings and report the results in Table 4.

Regression Results From Generalized Linear Models.

Note. Table displays the regression results from Generalized Linear Models. From 2010 to 2022, 28 Vietnamese insurers were included in the sample. Appendix A has all variable definitions, with p-values in parenthesis. The symbols ***, **, and * denote the significance levels of 1%, 5%, and 10%, respectively.

Regression Results From Generalized Linear Models

Table 4 shows that foreign ownership has a negative relationship with the Z-score. A percentage increase in foreign ownership reduces the Z-score by 0.0067 percentage points, implying higher risk-taking behaviors. The findings align with Amor (2017) and Kouzez (2021). Foreign ownership would select new foreign management who, due to their limited understanding, are frequently ill-informed about conditions in the nations where they operate, resulting in greater risk. The findings are also consistent with the stake theory, which states that foreign-owned companies take more risks to maximize shareholder value, which might lead to conflicts with other stakeholders (S. Chen et al., 2019). The findings support Hypothesis 2.

Table 4 shows that investor attention has a negative relationship with the Z-score. Specifically, a percentage increase in investor attention increased risk by 0.1953 percentage points. The findings are congruent with those of Hao and Xiong (2021) and the limited attention theory. They said there are too many information sources on the internet, which raises the barrier to differentiating accurate information, causing these investors to misjudge the company. Furthermore, some investors have strong information processing abilities, while others do not. This results in disparities in perceptions even on the same information on the internet, raising the idiosyncratic risk of individual equities. The results are consistent with hypothesis 3.

Tables 4 and 5 report that the interaction term (FO*TREND) negatively affects the Z-score, implying that insurers with investor attention and foreign ownership take additional risks. The results are consistent with M. Chen et al. (2017), Kouzez (2021), and Hao and Xiong (2021). Insurance companies under foreign ownership often embrace greater risk, driven by several factors. M. Chen et al. (2017) and Kouzez (2021) reveal that foreign financial firms, including insurers, confront a disadvantage in new markets due to their unfamiliarity with local conditions, regulations, and behaviors, leading to riskier choices. These foreign-owned insurers might also face additional risk through their connection to parent companies in their home nations. Besides, Hao and Xiong (2021) indicate that investor attention also magnifies risk. In an internet-rich environment, abundant information sources lead to complexities in assessing accuracy, hindering the distinction between valuable insights and noise. This complexity prompts misjudgments by investors, amplifying risk for insurance firms. The results support hypothesis 5.

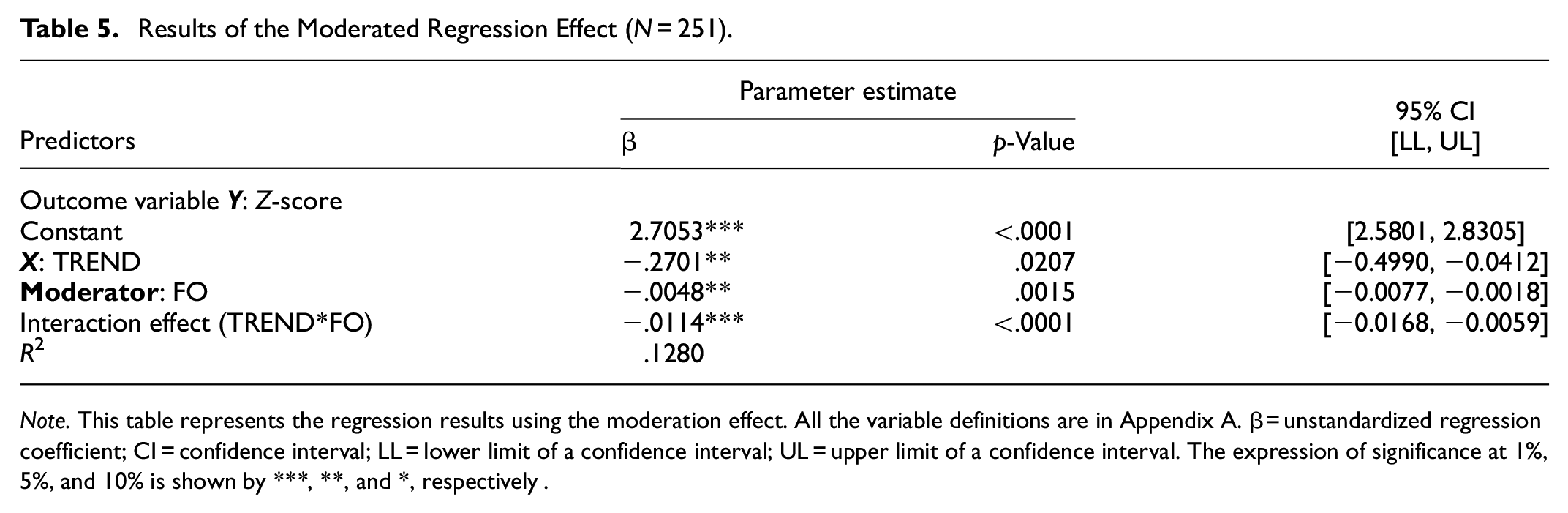

Results of the Moderated Regression Effect (N = 251).

Note. This table represents the regression results using the moderation effect. All the variable definitions are in Appendix A. β = unstandardized regression coefficient; CI = confidence interval; LL = lower limit of a confidence interval; UL = upper limit of a confidence interval. The expression of significance at 1%, 5%, and 10% is shown by ***, **, and *, respectively .

This study adopted the Johnson–Neyman technique and Simple slope analyses to clarify the moderation effect, following He and Ismail (2023), Compton et al. (2023), and Sarintohe et al. (2023). This approach identified significant thresholds for the direct impact of TREND on Z-score across varying FO levels, as illustrated in Figure 1. Specifically, Figure 1 shows that the moderation effect was significant when foreign ownership was below −47.482% or above −4.26%; between these values, the effect was not statistically significant. Moreover, Figure 2 portrays Simple slope analyses, revealing how TREND impacts Z-score with high FO, average FO, and low FO conditions. Notably, Figure 2 indicates a stronger association between TREND and Z-SCORE exists with higher foreign ownership (one standard deviation above the mean) than lower FO levels (one standard deviation below the mean). In short, the findings suggest that foreign ownership moderates the relationship between investor attention and the risk-taking behavior of insurance firms in Vietnam.

Johnson–Neyman plot showing the moderating effects of FO on the association between TREND and Z-SCORE.

Simple slope analyses for the effect of TREND on Z-SCORE with high FO (1 SD above the mean), average FO (mean), and low FO (1 SD below the mean).

Table 4 reports that a higher leverage ratio reduces risk in the insurance industry. This could be attributed to insurers’ risk aversion due to potential financial pressure from defaults, legislative restrictions on borrowing, increased investor confidence in stable financial situations, liability matching concerns, and a desire to manage systemic risk (Kouzez, 2021).

Table 4 shows a negative relationship between insurance size and risk-taking behavior. Specifically, Table 4 indicates that the coefficients of size in all models are positive and significant with Z-score, implying larger firms have lower distress risk. S. Chen et al. (2019) indicated that large insurers are less likely to engage in earnings management because they have stable company governance mechanisms and are subject to more special regulatory inspections. Moreover, larger firms have fewer financial constraints, so they have diversified financing channels, which reduce their distress risks. Finally, the findings suggest that older insurance firms exhibit reduced risk levels due to their accumulated risk management experience. Akbar et al. (2017) and Quaye et al. (2014) also report a positive association between firm age and financial stability.

Conclusion and Recommendation

This research explored how foreign ownership and investor attention affect the risk-taking behaviors of insurance companies in Vietnam. We employ Random Effect Models, Generalized Linear Models, and the Johnson-Neyman test to analyze an unbalanced sample of 28 Vietnamese property and casualty insurance companies from 2010 to 2022. The findings report that higher foreign ownership and investor attention motivate risk-taking behaviors of insurance firms in Vietnam. Additionally, our analysis reveals that heightened investor attention plays a role in shaping insurers’ risk-taking behavior. Finally, we figure out that foreign ownership moderates the relationship between investor attention and the risk-taking behaviors of insurance firms.

This study offers practical recommendations to foster sustainable development within the insurance industry. Firstly, insurance firms should consider reducing foreign ownership to mitigate risks. Currently, foreign investors in Vietnam possess the authority to hold shares and contribute capital up to 100% of the charter capital of insurance enterprises and reinsurance entities. However, such high foreign ownership thresholds can elevate risk levels for insurance companies operating within the Vietnamese market. Policymakers should persist in refining foreign ownership regulations, particularly within industries with potential high-risk characteristics, such as the insurance sector. Implementing more stringent oversight of foreign ownership ratios can curtail the potential global financial repercussions on markets during crisis scenarios. Additionally, policymakers should actively encourage domestic financial institutions to invest in the insurance industry. This strategic move can alleviate dependency on foreign investment and concurrently enhance risk management practices.

Secondly, policymakers must issue appropriate policies to manage insurers and the market, such as cybersecurity, to limit fake news affecting insurance businesses. Besides, many sources of information on the internet will affect the accuracy, increase the barrier to distinguishing the correct information, making these investors misjudge the company, so the government should enact a law to penalize such misleading information published on the internet. Moreover, strengthening regulatory oversight of insurance companies can help ensure they provide accurate and transparent information to investors. Regulatory bodies can conduct audits, impose reporting requirements, and establish mechanisms for monitoring compliance.

Finally, the government should reinforce the information disclosure requirements for insurance companies to improve transparency. Mandating transparent and standardized reporting formats can make it easier for investors to compare and analyze information across different companies. Additionally, governments can collaborate with industry associations and self-regulatory bodies to establish best practices and codes of conduct for insurance companies. Encouraging industry self-regulation can be an effective way to promote transparency and accountability.

Although this study contributes to the growing insurance literature, it has data limitations. Specifically, the number of publicly traded Vietnam insurers is smaller than in emerging countries. Moreover, Vietnam is a frontier country, so the findings may differ from those of developed markets. Therefore, we suggest that future research examines this topic across countries to generate in-depth insights.

Footnotes

Appendix

Variables Definition.

| Variables | Notation | Definition | Reference |

|---|---|---|---|

| Dependent variables | |||

| Z-Score | Z-SCORE | The total return on assets plus equity to assets is divided by its standard deviation. | Dbouk et al. (2020) |

| Independence variables | |||

| Foreign ownership | FO | Foreign investors’ ownership percentage | Loncan (2020) |

| Investor attention | TREND | Investor attention indicator is computed from the natural logarithm of the total number of searches from Google Trends. | Hao and Xiong (2021) |

| Interaction term | FO*TREND | This interaction term allows us to test whether insurance firms with higher foreign ownership and investor attention have higher risk-taking behavior. | Saghi-Zedek (2016) |

| Control variables | |||

| Leverage | LEV | The total owner’s equity ratio to total assets | Bierth et al. (2015) |

| Insurer size | SIZE | Natural logarithm of an insurer’s total assets. | Bierth et al. (2015), Duong et al. (2023) |

| Firm age | AGE | The number of years of its establishment | Bansal and Singh (2021), Duong et al. (2023) |

Acknowledgements

We thank Mr. Tran Duc Thanh, a post-graduate student from the Faculty of International College of Sustainability of Innovations, National Taipei University, Taiwan, for helping us at the early stage of this study. We also thank anonymous reviewers for constructive feedback, which helped improve the manuscript significantly.

Author Contribution Statement

Hoang Nguyen Tien (

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by Ton Duc Thang University, Van Lang University, and Ho Chi Minh University of Banking, Vietnam.

Ethical Statement

This article contains no studies with human or animal subjects.

Data Availability Statement

The data used to support the findings of this study are available from the corresponding author upon request.