Abstract

Intelligent technology solutions have revolutionized banking and enhanced the overall efficiency of financial institutions worldwide. As banks endeavor to evolve into comprehensive financial service hubs, this study examines the impact of intelligent technology solutions on the efficiency of a sample of Chinese banks and analyzes efficiency trends over time based on two vectors affecting intelligent technology (enterprise-side innovation and consumer-side co-creation). The study builds upon the parameter non-frontier method (ACF) to measure efficiency and examines intelligent technology solutions and channel usage in China from 2007 to 2017. The results indicate that intelligent innovation and consumer co-creation within intelligent channels both have significant positive impacts on banking efficiency. Moreover, these impacts have gradually surpassed traditional banking innovations and consumer participation in traditional self-service channels. In some ways, consumer participation’s positive impact on banking efficiency is even greater than banks’ institutional innovation. Notably, the relative influence of intelligent innovation and consumer participation on bank efficiency has shifted, and customer participation now occupies a more important position. Based on these findings, banks would be well advised to develop intelligent technology solutions along two paths: enhancing institutional technology and supporting consumer participation.

Introduction

As banks have evolved over the past decade, so have the risks incurred by the industry. The Chinese banking industry’s non-performing loan ratio reached 1.92% at the end of 2020, and the industry’s profitability performance was volatile throughout the 2010 to 2020 decade (Fukuyama & Tan, 2022). One reason for this is institutional inefficiency in areas such as customer acquisition ability and risk control. Many banks are seeing declining profitability and growing portfolio risk. Previous studies have attempted to address the problem with proposals to reform management systems, optimize market structures, and limit bank size. However, the rapid digitalization of business worldwide has challenged conventional business models by breaking down industry boundaries. The advent of intelligent technology offers both opportunities and challenges for banks that are reliant on conventional financial services operating systems (Weill & Woerner, 2015), and the industry’s need to focus on intelligent technology is urgent.

Research on intelligent financial technology solutions has increased exponentially in recent years. Studies have looked at the application of intelligent technologies (Carbó Valverde et al., 2020; Klus et al., 2019 ) and their impact on customers (Kotarba, 2016; Shahid et al., 2022; Sishu, 2022), as well as the qualitative impact on specific operational segments (Arcand et al., 2017; Kaabachi et al., 2019; Klus et al., 2018; Sishu, 2022) and on the banking and financial industry as a whole (Bömer & Maxin, 2018; Holotiuk et al., 2018; Jayawarsa et al., 2021). Research suggests that ongoing innovation including technological research and development, product innovation, and service innovation at banks has led to efficiency improvements. However, consumer participation in banking services creation is an equally important factor. Many intelligent technologies are self-service technologies, and so adoption of them requires consumer participation (Li et al., 2021; Moliner et al., 2018; Tuan, 2022). As consumer participation increases, the process of service value creation grows spontaneously (Pansari & Kumar, 2017) through reduced labor costs, lowered risk, greater convenience and overall efficiency. Intelligent terminal business management has matured, and many consumers now consider this method of banking safer, more convenient and more hygienic, especially in the post-pandemic era (Ahir et al., 2020). With increased consumer engagement, the value of such services has grown (Pansari & Kumar, 2017). As people become more skilled and efficient in this value co-creation activity, costs and risks continue to decline for banks even as efficiency gains rise.

Although some scholars have looked at consumer engagement in intelligent environments, to-date studies have mainly examined customers’ willingness and propensity to engage from a marketing perspective (Sashi, 2012), the relationship between the level of engagement and perceptions of technology (Franke et al., 2013; Islam et al., 2020), and/or the impact of consumer engagement on customer satisfaction (Pansari & Kumar, 2017; Yi et al., 2021) and sense of efficacy (Scherer et al., 2015). In fact, the study of consumer engagement in intelligent environments has been the focus of research in the field of marketing, while consumer engagement in value co-creation has essentially been considered a psychological topic. There are few studies on the objective effects of value co-creation, and there is a dearth of research on the impact of consumer engagement on the efficiency of firms, that is, the extent to which consumer engagement in intelligent environments contributes to banking efficiency. Taking into consideration the emerging dynamics of consumer engagement, we chose to investigate the objective effects of consumer engagement on banking efficiency in intelligent technology environments. We then examined the paths through which consumer engagement can positively impact banking efficiency in the context of banking processes.

Using data from Chinese banks, we looked at two vectors of intelligent technology solutions and examined the impact of both institutional innovation and consumer participation on banking efficiency. In addition, to avoid the limitations of some previous studies, we studied the dynamic paths of the impacts. Thus, our study clarifies the practical effects of intelligent institutional innovation and consumer co-creation and helps banks in emerging market economies identify ways to improve efficiency.

This paper contributes to the existing corpus of literature in three main ways. First, this study regards the implementation of intelligent technology solutions by banking institutions as a unique business model and views the impact of such solutions through two lenses: institutional innovation and consumer engagement. It confirms that consumer engagement is not simply a marketing concept but a mode that has an impact on the operations and development of relevant enterprises. Second, to the best of our knowledge, there is little quantitative empirical research about the impact on bank efficiency at the enterprise level, so we use data to quantitatively measure the impact of consumer engagement on bank efficiency in a terminal channel. Finally, current studies on banking efficiency generally employ frontier function methods, such as DEA and SFA. However, such calculations yield ratios rather than absolute values, and it is difficult to meet the requirements of data volume. Therefore, given the ongoing comprehensive transformation of bank operations, this study adopts a semi-parametric non-frontier method (ACF method) and uses the added value of banks’ overall business as output to measure banking efficiency. As a result, this study overcomes the theoretical and practical shortcomings of previous studies that viewed banks merely as deposit-and-loan manufacturing businesses and disregarded the fact that many of today’s banks function as comprehensive financial service providers. Moreover, it elucidates the bank’s decision-making mechanism more clearly.

Literature Review

The Impact of Intelligent Technology Innovation on Banking Efficiency

Intelligent technology innovation is comprised of new products, new services, new production processes and/or new organizational forms (Frame & White, 2004). Extant studies on the adoption of intelligent technology solutions by banks have focused generally on enhancements such as back-end systemic upgrades (artificial intelligence technology, big data, blockchain, etc) (Lu et al., 2019; Khalil et al., 2022), front-end application interface optimizations, or intelligent terminal deployments (STM machines, mobile apps or virtual banks, etc) (Jones & Gong, 2021; Srivastava & Vishnani, 2021), and business model advances achieved by these improvements (such as intelligent marketing, intelligent customer service, automatic risk control, and others (Klus et al., 2018; Li et al., 2021; Williams & Moons, 2010). To-date, these studies have been largely qualitative. From these studies, it is apparent that intelligent banking entails not only technological innovation per se, but also the commercialization of technological innovations, such as novel intelligent terminals, virtual financial products, and intelligent investment advisory services, all of which involve long processes of research and development, trial operations, iteration and improvement before eventually finding acceptance by consumers.

Banks implement intelligent technology in order to achieve various efficiencies. First of all, the deployment of intelligent terminals reduces customer dependence on traditional branches, minimizes the need for service personnel and lowers operational costs (Khan, 2022; Klus et al., 2019; Mai et al., 2012). Secondly, using technology engine upgrades, such as big data technologies, transaction matching software, and rapid loan approval systems, intelligent banking facilitates the transmission of financial services and enables customers to complete transactions quickly, accurately and securely. In this way, intelligent technology improves the efficiency of financial resource allocation (Kotarba, 2016). Finally, intelligent risk identification and management systems have proven to be agile, effective and economical in identifying and mitigating various risks (Rogers, 2010).

The Impact of Consumer Participation on Banking Efficiency

Intelligent banking technology has fostered a range of business model innovations leading to channel (Barrett et al., 2015), service (Campbell & Frei, 2010; Rogers, 2010) and product enhancements. A key aspect of these intelligent or smart technologies is that they are self-service technologies, and their adoption and use require customer trust, acceptance and participation. For example, customers must spend time to understand and use STMs (smart teller machines) and mobile apps, as the basis of big data precision marketing and automatic risk management relies on consumers’ usage and transmission of data on these terminals (Moliner et al., 2018). Consumers using these technologies do not simply function as service recipients; they also actively participate in service value creation (Pansari & Kumar, 2017; Zott & Amit, 2007).

Such customer involvement has three characteristics. First, customers operate intelligent devices independently, deploying their own time, skill and effort, and obviating the labor of certain bank employees in so doing. In this sense, they contribute to reducing the bank’s labor costs and create value for the institution. Second, consumers determine when, where, and how much effort to contribute to the value-creation process based on utility maximization, which can include subjective factors such as efficacy and objective factors such as a comparison of opportunity costs and benefits. This is different from the decision-making basis in customer relationship management (CRM), where consumers are merely service recipients (Franke et al., 2013). Third, although consumers have participated in this type of value creation since banks began deploying ATMs (automated teller machines), previously their participation was fixed, simple, and single-function. Now, with intelligent terminals, consumers are able to participate in more complex value creation activities involving more advanced, sophisticated financial products and services.

Consumer participation has a positive impact on bank efficiency through the various paths. First, consumer effort replaces employee labor, thereby, in some sense, transferring those labor costs to customers (Alvarez-Milán et al., 2018; Patrício et al., 2011; Second, intelligent technology solutions enable consumers to participate in expanded financial service scenarios and increase the configurable scope of bank resources. As they develop ways to transmit financial services more efficiently (e.g., push loan recommendations to customers in consumption scenarios), banks can implement intelligent risk management systems based on each individual consumer’s self-service behavioral data and thereby predict and control risk quickly and accurately. They can then offer personalized risk pricing in real time. Third, a bank can identify target consumers by actively setting the parameters of an intelligent institutional system to recognize certain self-service transaction characteristics and follow up with personalized marketing strategies (Campbell & Frei, 2010).

Methods

Estimation Approach

Productivity Estimation

There are various ways to evaluate bank efficiency, including production theory, intermediary theory, asset theory (Collard-Wexler & De Loecker, 2016; Elyasiani & Mehdian, 1990; McKee & Kagan, 2018 ). As banks gradually evolve into more comprehensive financial service providers (Song et al., 2018), the impact of intelligent technology is widespread (Fumiko et al., 2020), and so, based on our research purpose, we have endeavored to measure efficiency in terms of the full menu of each institution’s financial services. Therefore, we have incorporated both production theory and intermediary theory in our definition of efficiency, such that banks use as few resources as possible to provide comprehensive financial services, and a bank’s efficiency is the overall ratio of financial services provided relative to its assets, intermediate inputs and labor invested.

Previous studies on banking efficiency generally employed frontier function methods, such as DEA (Data Envelopment Analysis) and SFA (Stochastic Frontier Analysis). However, the economic meaning of the DEA method is unclear, and its calculation is a ratio rather than an absolute value, and thus it is not appropriate for further influential factor research. The SFA method uses a specific distribution hypothesis for non-efficiency terms that is difficult to satisfy and also requires that the study of factors affecting efficiency be conducted simultaneously with the efficiency measurement (a one-step method). This greatly increases the number of parameters that must be estimated and the sample requirements to the point where data in emerging market economies is insufficient (Aigner et al., 1977; Kato & Kodama, 2014; Olley & Pakes, 1992).

This study employs a semi-parametric non-frontier autocorrelation function (ACF) method for the following reasons: (1) The result of this method can be further used to study the influencing factors of the measured production function. However, it is not necessary to use a one-step method in the study, so the sample size required is relatively small (Ackerberg et al., 2015; De Loecker & Warzynski, 2012). (2) It identifies efficiency by generating proxy variables through the enterprise’s decision-making process. This avoids the problem of the error term and efficiency term hypothesis, and the economic significance is clear (Olley & Pakes, 1992). (3) In recent years, this type of methodology has gradually expanded from application in the manufacturing sector to use in service companies, including e-commerce retail and logistics, and lessons from such previous research have informed this study (Doraszelski & Jaumandreu, 2013; Stiel et al., 2015; Trax et al., 2015).

The logarithmic form of a Cobb-Douglas production function is as follows:

where yit is the logarithm of the output of enterprise i at time t, lit is the logarithm of variable labor input, and kit is the logarithm of capital stock. ωit is the efficiency of the enterprise. Some efficiency shocks, such as breakthroughs in technology or improvements to management capabilities or consumer quality, can be observed (or predicted) by an institution. The random error ϵit is the sum of the efficiency shocks which aren’t observed (or forecasted) by managers who make production decisions at time t. Unexpected efficiency shocks might include management errors or production problems that have unintended effects on efficiency. Since ωit is known by the enterprise, it inevitably affects operational decision making. Thus, ωit is related to certain inputs and may create endogenous problems. Olley and Pakes (1992) used the timing of information availability relative to such decisions to establish a structured model. In this way, they solved the endogeneity problem and split ωit from ϵit simultaneously. The model was adapted by Levinsohn and Petrin (2003) and Ackerberg et al. (2015) to deal with the more complex decision-making logic of financial service entities, such as banks.

First, suppose that a bank’s financial service production flow follows a flexible translog form since it is not bound by the assumption that the elasticity of output is constant. The technological progress is Hicks neutral:

where yit is the logarithm of comprehensive financial service output of bank i during time t. lit represents the logarithm of variable labor input, and kit is the logarithm of capital. ω it is the banking efficiency that can be observed by the bank’s decision-makers. The bank will then adjust the number and proportion of production factors, such as labor and intermediate inputs, according to ωit.ϵit is a random error that is irrelevant to the factor input because it can’t be observed by decision-makers. We suppose ω it follows a first-order Markov process:

Furthermore, according to Ackerberg et al. (2015), as bank employees’ labor contracts are always long-term and executed in advance, the intermediate inputs will follow and rely on labor input. Thus, it is appropriate to introduce labor input into the decision function of the bank’s intermediate input (mit) together with capital and efficiency.

The demand for intermediate inputs is a strictly monotonic function of efficiency. Efficiency can be presented by the inverse of the demand function for intermediate inputs.

By plugging this into Equation (2), we have the following:

Notably, βk, βl, βu, βkk, and βlk cannot all be identified. Thus, we merge them into:

Since the specific form of Φ is not known, non-parametric methods can be employed. Here, a quadratic polynomial is used to obtain an unbiased approximate estimate, which is the total output value filtering out random errors. Given a parameter vector β*= (βl, βk, βll, βkk, βlk), the efficiency ωit can be written as a function of Φit and the parameter vector:

Next, we make a second-order approximation with the first-order Markov property of Equation (2):

The innovation term ξit is obtained from the residual term. Five moment conditions should be constructed according to the number of parameters to be estimated. The capital investment kit is decided at the beginning of the period, which is not related to ξit, and the labor input lit decisions relate to the current efficiency and innovation. However, the lag term lit-1 of the previous period has nothing to do with them; thus sufficient moment conditions can be established to execute the generalized method of moments (GMM) estimation.

Finally, this study uses the bootstrap method to calculate the standard deviation of parameter estimates (Wooldridge, 2009).

Methodological Approaches

In studying the relationship between intelligent innovation and banking efficiency, it is necessary to consider, on the one hand, that corporate innovation improves banking efficiency directly by enhancing operational processes. On the other hand, consumer participation actually increases the amount of available labor for the bank. Traditional efficiency research methods, such as SFA, combine a variety of possible influencing factors to study their relationship to corporate efficiency. However, this does not accurately replicate a bank’s decision-making processes, and structural modeling, such as ACF, can solve this problem better. Therefore, we examined the effect of consumer participation on bank efficiency by distinguishing the various labor vectors (employees and consumers) when establishing a production function.

According to Field et al. (2012), when consumers participate in the service production process, their decision-making motivation differs from that of employees, who are tasked with making optimal decisions about their respective inputs and outputs based on utility functions and cost functions, respectively. There are two reasons for the difference. First, from a theoretical perspective, consumer participation is determined by consumer interests, while the decision-making behavior of the enterprise is guided by innovation. It is difficult for one side to predict the behavior of the other in a given period. Moreover, practically, the driving forces of participant participation in service creation depend upon individual needs, trust in a company’s technology, and the impact of social networks, while the main factors affecting bank innovation are the company’s financial goals, strategic intentions, and the competitive environment. Therefore, the term of these two vectors in the production function are independent of each other, as illustrated here:

where

Note that Tit is the bank’s existing corporate intelligent technology innovation and Cit is the consumer participation in intelligent termina.

Variables

Production Function Variables

The ACF method requires determination of labor, capital stock, and intermediate inputs (Ray & Das, 2010; Staub et al., 2010). As per established practice, the number of bank employees is used as the labor input variable (Parrotta et al., 2014). However, unlike manufacturing firms, fixed capital accounts for only a small part of the capital investment in banks’ operations. Additionally, capital investments include cash and central bank deposits, funds from interbank and other financial institutions, available-for-sale financial assets, customer loans and advances. The intermediate input is defined as operating management fees plus interest and handling expenses (Crespi & Zuniga, 2012).

This study focuses on the banking industry’s ongoing transition into a comprehensive financial services hub. Therefore, the value added, computed as the difference between total sales (revenue) and intermediate costs (selling expense), is used as the output in the function. There are several reasons for this. (1) This output measure is comprised of the banks’ comprehensive operations and reflects the overall value of the institution as a comprehensive financial hub, whereas previous studies frequently used loans as output, thus implying that banks are merely lending institutions (Bramulya et al., 2016). (2) Furthermore, this output measure is in line with the basic requirements of the ACF method that output should reflect added value (Ackerberg et al., 2015). (3) It also has the advantages of both the intermediary method (the variables are clearly quantitative) and the production method (the economic significance of output is clear) (Growitsch et al., 2009).

Factors Affecting Banking Efficiency

In this study, we consider intelligent technology innovation and consumer participation in intelligent technology as the main factors (vectors) influencing efficiency.

We used the number of intelligence-related patents to represent a bank’s intelligent technology innovation. However, there are two caveats to note. First, the basis for innovation is research and development, which must then be converted into patents. These are crucial for financial organizations since they do not produce tangible products (Gotsch & Hipp, 2012). Second, innovation in the financial industry includes not only technological innovation, but also management, channel, service, and business model innovation. When these types of innovations are manifested in the form of patents or trademarks, they have already been implemented and had an impact on operations (Alvarez-Milán et al., 2018; Snyder et al., 2016). Thus, in this study, we have applied the current value of patents directly rather than the lagged value.

We used consumer transaction volume in intelligent channels (including STM, online banking and mobile banking) to represent consumer participation for several reasons. First, customer participation reflects the amount of consumer labor input and is usually measured as the amount of time input. Assuming that the amount of service per unit of time is relatively stable, the amount of labor input can be derived from the amount of service created (Parrotta et al., 2014; Trax et al., 2015). Secondly, customer participation is a dynamic process that includes participation behaviors and transaction results. Participation behavior in intelligent channels is virtually impossible to quantify using transaction results, but measuring transaction volume (i.e., the entire process of customer self-service participation in intelligent channels) is feasible (Fang et al., 2011; Sashi, 2012); Finally, previous studies that analyzed customer participation in service transactions with SST (self-service technology) determined that adoption of intelligent technology solutions is more dependent on customer operations than traditional self-service machines, further validating the status of customer participation (Field et al., 2012; Zhang & Joglekar, 2016).

Control Variables

(1) Important control variables related to bank intelligent technology:

Before intelligent technology solutions were implemented in banking systems, ATMs and other types of non-intelligent equipment had already begun to involve customer participation. Moreover, innovation in the banking sector goes beyond intelligent technology innovation. Therefore, this study introduces customer participation in traditional self-service machines and innovations other than intelligent technology solutions as control variables. Customer participation in traditional self-service machines is measured by the transaction volume of traditional self-service equipment such as ATMs and CRS (Cash Recycle System) terminals. Other innovations not related to intelligent technology are represented as the number of patents and new products unrelated to intelligent technology solutions (Field et al., 2012).

(2) Other control variables:

In addition to corporate innovation and consumer participation control variables, certain macro factors may also affect efficiency, including the macro market structure represented by banks’ deposit market share and operating conditions of banks represented by the proportion of non-interest income. The number of transactions on STMs of some banks may not be disclosed in some years. But because the transaction volume of STMs is small, we can ignore this small effect. All variables in this study are shown in Table 1:

Research Variables.

Date Sources

We studied the top 58 banks in China, as measured by assets, from 2007 to 2017. These banks all have the following features. First, from 2007 to 2017, there was a complete and continuous organizational structure and operating process for each bank. Second, around 2007, intelligent technology solutions and terminals were introduced to provide financial services to customers. This study extracts the annual transaction volume of ATMs, CRSs, STMs, online banking, and mobile banking channels from the WIND database, BVD-ORBIS Bank Focus database, and the annual reports of the 58 banks. ORBIS Bank Focus is the authoritative analysis database of the global banking industry, providing detailed data of operation and credit analysis of more than 44,000 major banks and important financial institutions and organizations in the world. It is also the most frequently referenced bank professional analysis database among academic papers in the field of international financial research. Wind database covers global financial market data and information, including stocks, bonds, futures, foreign exchange, funds and other varieties, providing accurate, timely and complete financial data information continuously. And they are publicly available and socially accepted. The banks’ financial data and company value data and other control variables were extracted from annual reports and CSMAR databases (Wooldridge, 2009). After testing, we found that all variables rejected the null hypothesis that there is a unit root, and all variable series were stationary (Choi, 2001; Levin et al., 2002).

Results

Time Trends of Bank Intelligent Technology Solutions

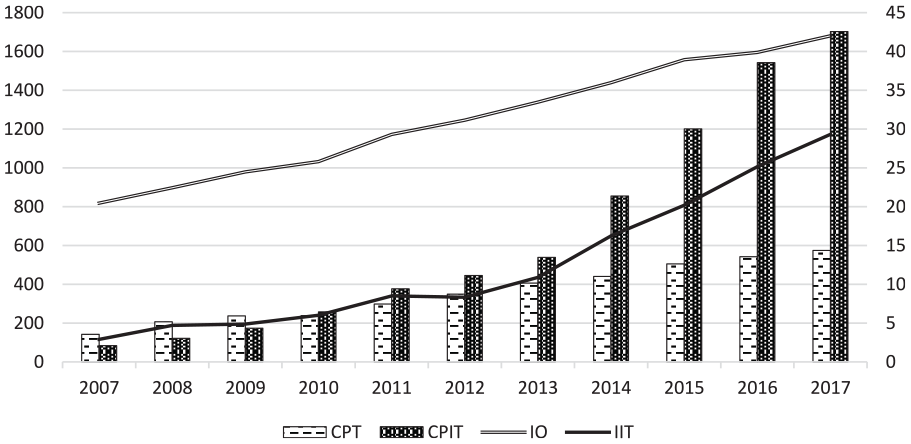

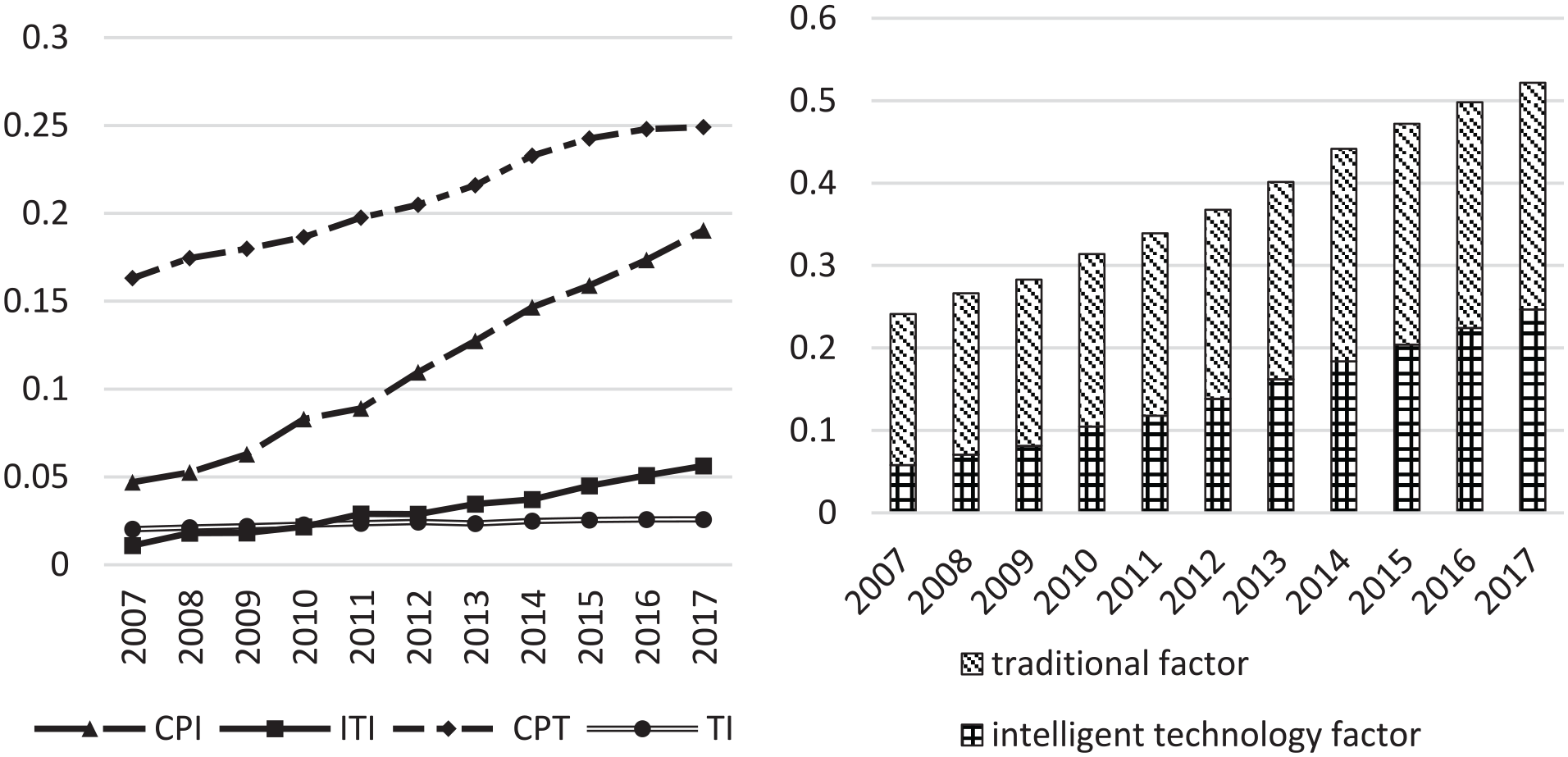

As Figure 1 shows, innovation and consumer participation in the banking sector based on intelligent technology solutions has been on the rise since 2007. This trend accelerated in 2014 (for consumer participation in intelligent channels) and 2013 (for intelligent innovation related advances). Even as intelligent innovations were being developed, banks were also implementing other more traditional innovations, and physical branches were deploying traditional self-service equipment to encourage customers to participate in service creation, albeit at a slower pace than the development of intelligent technology.

Time trends of major banking efficiency factors.

The ratio of traditional banking innovations and intelligent innovations decreased from 6:1 in 2007 to less than 2:1 in 2017. More striking is the pace of consumer participation. Consumer participation in intelligent channels had surpassed consumer participation based on traditional self-service equipment by around 2010, and by 2017 was nearly three times greater.

Measurement of Banking Efficiency

As stated previously, the parametric frontier method has evolved since Olley and Pakes (1992). This study also uses the LP method (Levinsohn & Petrin, 2003) and the GNR method (Gandhi et al., 2011) simultaneously to supplement and verify the ACF method. In our GNR model, the output variable of the production function is replaced by the total amount of sales (revenue). We estimated the product function with these three methods and obtained similar results(For panel data and such estimation methods, R2 above 0.5 is already a good result), as shown in Table 2. The following is based on the results obtained by the ACF method.

The Results of ACF Function Estimation.

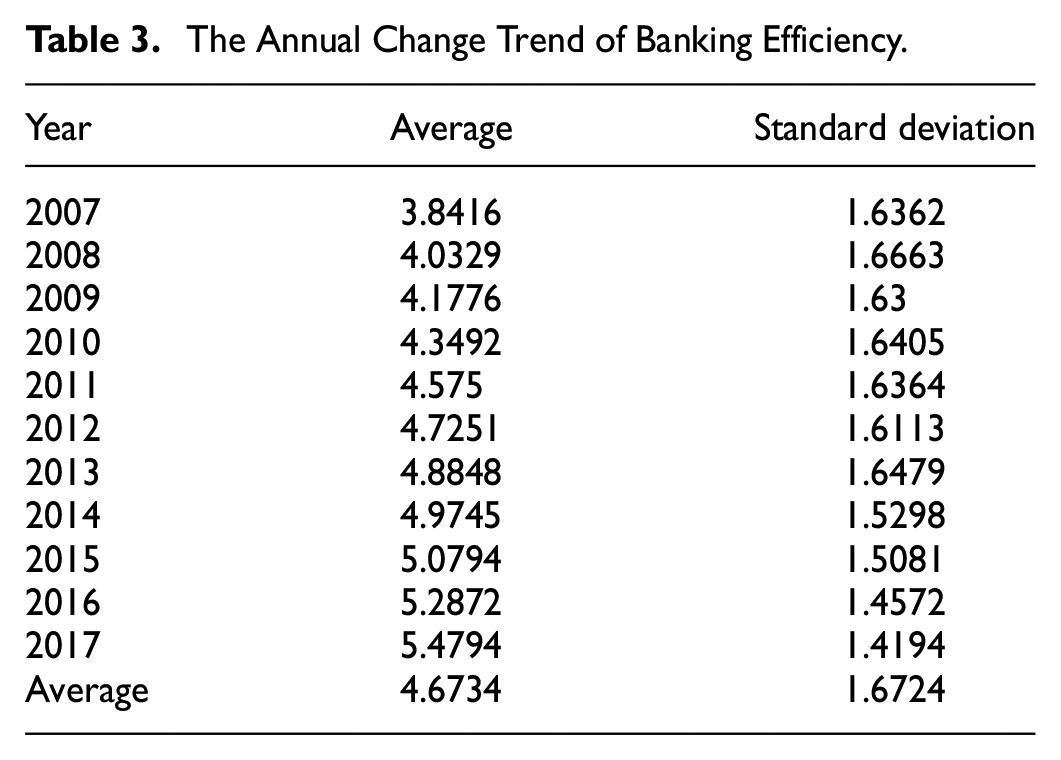

Table 3 shows that, on average, banking efficiency from 2007 to 2017 is 4.6734, which is higher than the average level (4.1603) of the broad service industry in the same period. It is equal to the average efficiency of the manufacturing industry from 2005 to 2010, although the growth is a bit slower. Internationally, the comparison is lower than the financial sector efficiency level calculated by Parrotta et al. (2014) using data from European countries, such as Denmark, from 1980 to 2005.

The Annual Change Trend of Banking Efficiency.

The annual changes reveal that the growth of banking efficiency was relatively stable from 2007 to 2010. The growth rate suddenly accelerated in 2011 and 2012 from about 0.1 to more than 0.2. However, it slowed again in 2013 and 2014, with an increase of less than 0.1. After 2015, there was relatively rapid growth again.

Comparing the distribution in 2007 and 2017 (Figure 2), we find that banking efficiency in 2007 showed a clear chi-square distribution, and a large number of banks fell below the average level. A few highly efficient institutions raised the average significantly. By 2017, the banking efficiency distribution characteristics show a more normal distribution, the peaks of which are close to the mean. This indicates that after several years of development, bank efficiency is more evenly distributed, and most of the banks that were lagging in efficiency in 2007 have made efficiency improvements.

Frequency distribution of banking efficiency in 2007 and 2017.

Impact of Intelligent Technology on Banking Efficiency

Basic Descriptive Conclusions

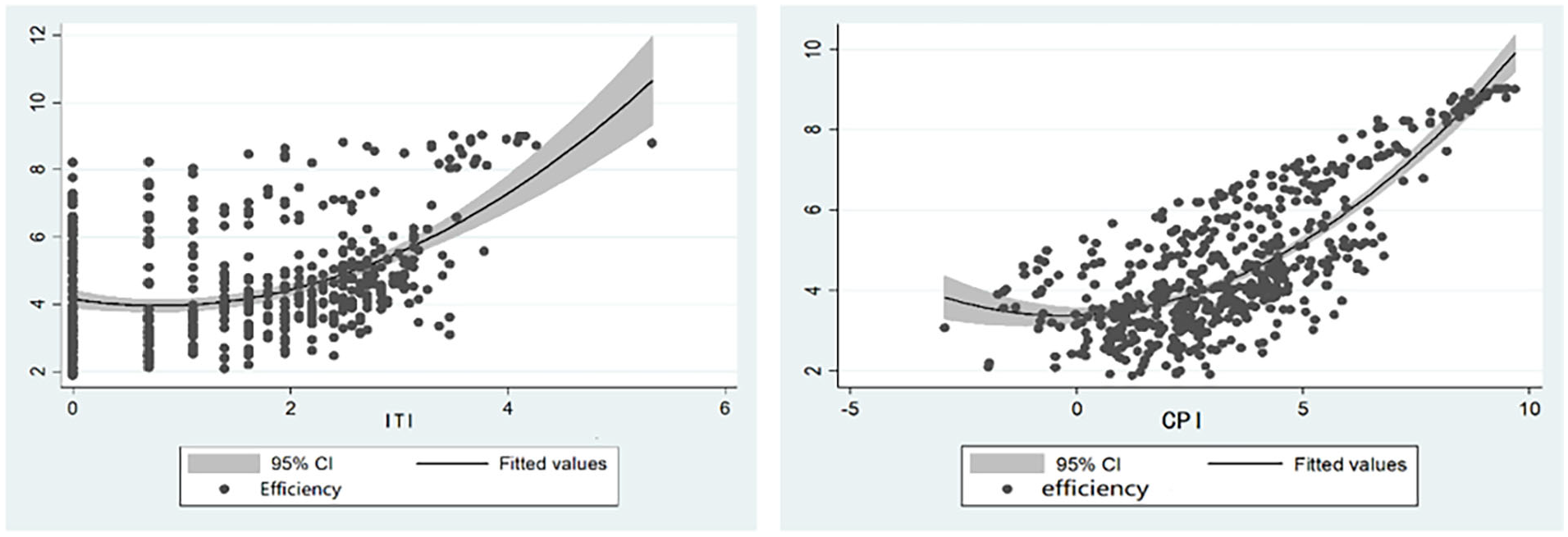

Figure 3 shows a clear positive correlation between intelligent innovation and consumer participation within intelligent channels and banking efficiency separately. (The graph on the left of Figure 3 shows intelligent technology innovation on the horizontal axis and banking efficiency on the vertical axis. The graph on the right has consumer participation on the horizontal axis and banking efficiency on the vertical axis. The scatter plot and the fitting curve indicate that there is obvious positive correlation.)

Relationship between intelligent innovation and consumer participation in intelligent channels and banking efficiency.

Figure 4 comprehensively shows this positive correlation on a three-dimensional coordinate axis. The full sample indicates that the positive correlation between consumer participation and banking efficiency is stronger than that between online banking-related innovation and banking efficiency.

Joint relationship between online banking innovation and online banking consumer participation and banking efficiency.

Estimation Results

Next, we used R for estimation analysis. Since the F = 87.14 and the Hausman test chi2 = 28.91, a fixed-effect model was selected. Here we use the robust method to modify the heteroscedasticity and obtain a robust t-value. The estimated results are as follows:

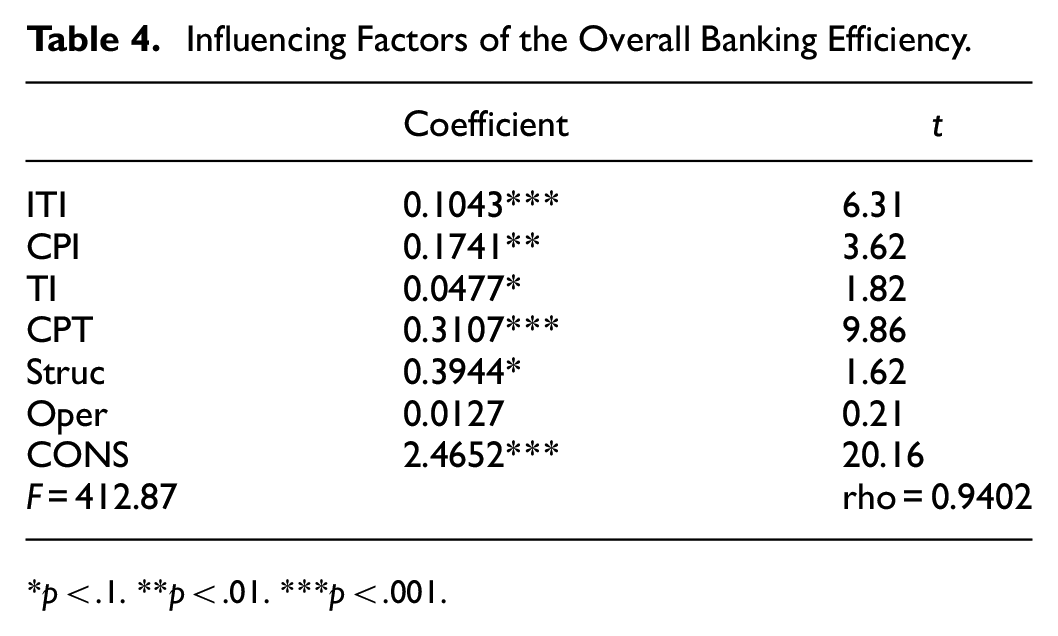

Since t value is greater than the critical value and sig is less than 0.1,0.05 or 0.01 pairs should be from * to ***. It can be seen from Table 4 that the two intelligent technology solution factors and the one control variables all had significant positive impacts on banking efficiency, which is in line with the theoretical expectations and the image of correlation analysis described earlier. Consumer participation in traditional self-service channels (CPT) had the strongest influence on banking efficiency.

Influencing Factors of the Overall Banking Efficiency.

p < .1. **p < .01. ***p < .001.

Our study focuses on two intelligent technology solution factors. Customer participation in intelligent channels had a stronger marginal effect on bank efficiency than intelligent innovation solutions. Each unit of customer participation in intelligent channel transactions (logarithm, the same below) increased bank efficiency by 0.1741 units, while intelligent innovation solutions boosted efficiency by only about 0.1 units. Other innovations unrelated to intelligent technology had the weakest effect of 0.0477 units on bank efficiency. In summary, based on analysis of the entire period from 2007 to 2017, the most important factor affecting the overall efficiency of Chinese banks was consumer participation in traditional self-service channels. The two factors related to intelligent technology solutions also played a crucial role, while the role of other innovations was relatively weak.

Based on our analysis of the empirical estimation results and the practical reasons underpinning them, we draw the following conclusions. A comparison of consumer participation and institutional innovation reveals that the receiving side factors in this industry have become more important than the supply side factors (i.e., institutional innovation). In other words, consumer participation in service creation and continuous increases in consumer value co-creation capacity have an important impact on the quality and quantity of banking services. There are several likely reasons for this. In a service industry, barriers due to ordinary innovation are lower than in a manufacturing industry (Greenhalgh & Rogers, 2012), and companies can more easily overcome most barriers by actions such as purchasing and imitation (Llerenaa & Millot, 2013). Moreover, efficient consumers are very important in service industries. Campbell and Frei (2010) noted that some banks actively seek to attract high-quality and high-spending consumers. This phenomenon is significant enough to interfere with the research on the impact of corporate technology improvement on banking efficiency. Therefore, with the development of intelligent self-service technology solutions, attracting more efficient consumers or improving consumer efficiency has a stronger positive impact on bank efficiency than institutional innovation.

Based on a comparison of two different banking innovations, the effect of non-technical ordinary innovation on banking efficiency was minimal during the study period. However, innovations that have a significant impact on banking efficiency are often deployed in combination with intelligent technology. In the tertiary industry, the application of intelligent technology has long been considered a cutting-edge technological innovation (Yoo, 2010). Intelligent innovations that combine intelligent technology solutions with other innovations (channel, service, management, and even business model innovations) have a stronger positive impact on firm profitability in the current economic environment (Vadell & Orfila-Sintes, 2008). Intelligent innovations are often integrated with consumer participation, thereby making their positive impact on efficiency even stronger (Chu, 2013).

Customer participation in traditional self-service machines had the strongest impact on bank efficiency. This means that although the trend of smart banking services has become more and more significant, there are still a large number of consumers in China who mainly use traditional self-service terminals for simple financial services such as deposits, withdrawals and inquiries.

The previous section discussed the marginal effect of various influencing factors, but it is important to note that the amount of input from these factors varies. By multiplying the estimated coefficients with sample observations, we can observe the specific role and proportion of each factor in driving efficiency increases (Sissoko, 2011).

Figure 5 shows that the contribution of different factors to the improvement of banking efficiency followed a consistent pattern throughout the observation interval. The contribution of consumer participation in traditional self-service equipment yielded the greatest impact, followed by consumer participation in intelligent online platforms. However, the contribution of consumer participation in intelligent channels increased at a remarkable speed, and the gap between the contributions of these two factors was greatly reduced by 2017. Intelligent innovation’s impact was smaller than the two aforementioned factors, but it developed at a relatively stable speed. Ordinary innovation had the least impact, and its growth almost stagnated after 2011 as its influence was surpassed by intelligent innovations in that year.

Factors affecting overall banking efficiency.

We summarized the effects of the two vectors of intelligent technology and compared this to the summed effect of the two traditional factors. The former’s role in improving efficiency was weaker in 2007 but increased and became more and more important year by year. By 2017, the relative importance of the two reversed for the first time, and the influence of intelligent factors on bank efficiency took predominance. This confirms the conclusions of many previous studies on micro-subjects (consumers) that the adoption of intelligent channels is not simply a concept of psychology or marketing but a mode that has real impact on financial institutions’ efficiency and output quality. A comparison of the effects of intelligent technology innovation and customer participation in intelligent channels shows that consumer participation occupies a dominant position. Comparing consumer participation in intelligent channels and in traditional channels, we found that the former is overtaking the position of the latter.

The Time Trend of the Impact of Intelligent Technology on Banking Efficiency

This research relies on temporal research to determine the influence trends of various factors over time, to explore the development path of the impact of intelligent technology on banking efficiency, and to predict its future development. Based on today’s economic and technological environment and current banks’ operational situations and efficiency developments, we believe it is appropriate to divide the research timeline into three periods. First, 2007, the year before the 2008 economic crisis, was a time of peak development for traditional banks in the pre-economic crisis era and also the year when banking efficiency began to rise rapidly. Second, the 2008-2012 period was a time when banking efficiency increased steadily. The third period is post-2013. At the end of the 2012, the Chinese government promulgated “the Financial Development and Reform in Twelfth Five-Year Plan,” which focused on comprehensive banking development. Yu’ebao was launched, exerting a great deal of external competitive pressure and prompting banks to embrace intelligent innovation. At the same time, this was also the stage where the growth rate of banks’ efficiency experienced a decline and then an accelerated rise.

It is clear from Table 5 that of the two non-intelligent factors, traditional banking innovation had a greater ability to improve bank efficiency in 2007. At that time, customer participation in intelligent channels was also a factor that contributed to institutional efficiency. The two vectors related to intelligent technology (intelligent innovation and consumer participation) had weak impacts on banking efficiency, although intelligent channel consumer participation had a significant impact on banking efficiency earlier than intelligent innovation. Unlike manufacturing industries, where technical factors tend to drive efficiency gains, consumer demand often precedes and may even drive technological progress in service industries. Consumer demand for transactional capabilities in intelligent channels spontaneously emerged with the development of various types of online consumption and novel payment scenarios instead of following the development of intelligent technology.

Research on Factors Affecting Banking Efficiency in Different Time Periods.

p < .1. **p < .01. ***p < .001.

Since F tests = 89.72 and Hausman tests chi2 = 17.62, for banks from 2008 to 2012, we used a fixed-effect model. The estimation results indicate that during this period the positive impact of intelligent innovation had become significant, and its unit influence surpassed that of consumer participation in intelligent channels, indicating that intelligent banking’s effect on banking efficiency was mainly driven by technology advances in the early stage. The unit influence of the two intelligent technology related vectors (customer participation and institutional innovation) also increased significantly from 0.127 to 0.162, and from 0.04 to 0.22, respectively. Meanwhile, the unit influence of consumer participation in traditional self-service channels increased slightly, and the level of consumer participation capacity during this time was stable and comprehensive. The unit influence of traditional institutional innovation declined sharply from 0.46 to 0.11, and its significance also declined.

As F tests = 37.21 and Hausman tests chi2 = 101.78, a fixed-effect panel model was selected for research in the period after 2013. The results show that after 2013, the effect of intelligent innovation dropped sharply. At the time, however, the impact of consumer participation in intelligent channels on banking efficiency was still increasing sharply, reaching about 0.35. Meanwhile, the unit influence of consumer participation in traditional self-service channels gradually decreased to about 0.21, which indicates that consumer participation in intelligent channels replaced consumer participation in traditional self-service channels during this period and became the most important factor affecting banking efficiency. This differs from the research conclusions derived throughout the entire research interval.

In summary, consumer participation in traditional self-service channels has had a significant impact on banking efficiency, but its influence is slowly declining. The unit influence of consumer participation in intelligent channels on banking efficiency has been increasing since 2007. The unit influence of intelligent innovation rose from 2008 to 2012 but fell again after 2013. This process explains the changes in banking efficiency during the study period in China and is congruent with the continuous trend of intelligentization, in which consumer participation has played an important role. Financial institutions that have embraced intelligent technology solutions can be considered to be at the forefront of this trend.

Robustness Tests

(1) Robustness test using the stochastic frontier analysis (SFA)

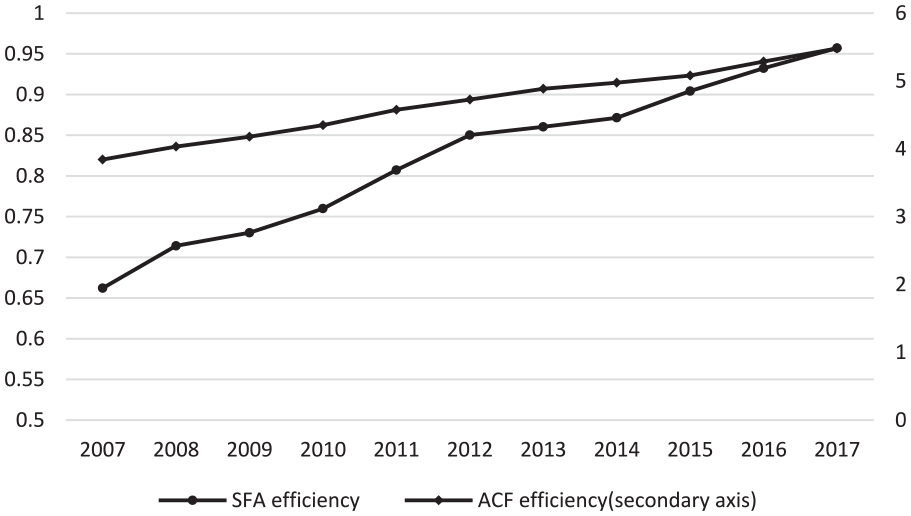

The OP method and its subsequently improved ACF method were first employed to study the manufacturing sector, so studies that have applied these methods to the service sector industries are few and new (Parrotta et al., 2014). Therefore, we employed the SFA method (McKee & Kagan, 2018), which is more commonly used in the study of banking industry efficiency, for robustness testing. The results are shown in Figure 6. Profit efficiency, as measured by the SFA method, is less than the conclusion obtained in the study itself because it measures the ratio of actual efficiency to optimal efficiency (it must be less than 1). However, the SFA method calculations of the trend of efficiency changes are very similar to the results of our study.

Comparison of results of different efficiency measurement methods of sample banks.

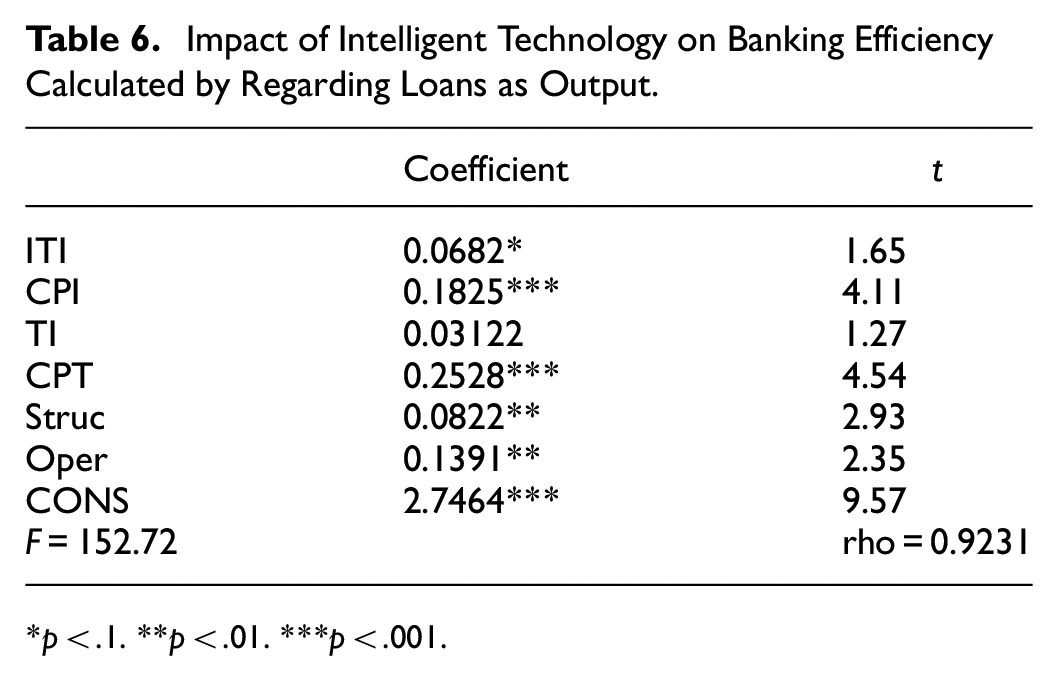

(2) Robustness test comparison between value added output and loans output

Measuring efficiency using value added as output has been applied in other service industries, but it has rarely been used in the banking industry. Here, we use loans with price deflating as the proxy variable because it is a more common output variable in traditional studies (Fiordelisi et al., 2011). Banking efficiency is measured and its relationship with intelligent technology vectors is estimated in Table 6.

Impact of Intelligent Technology on Banking Efficiency Calculated by Regarding Loans as Output.

p < .1. **p < .01. ***p < .001.

These results show that banking efficiency obtained by this method was also affected by intelligent innovation and consumer participation, much like the case where banking efficiency was measured using value added as output. In general, the research conclusions about the impact of intelligent technology and other factors on banking efficiency in this study are robust.

Concluding Remarks

Conclusions and Implications

Generally, intelligent innovation and consumer participation in intelligent channels both have positive impacts on banking efficiency. This study meets Moliner et al.’s (2018) inference, and it also provides an objective measurement of the impact of customer engagement in intelligent terminal channels on banking efficiency. Our results show that the influence of intelligent technology vectors on bank efficiency is not only the result of technological innovation, but that consumer participation also plays an important role. Consumer participation in intelligent channels, as a new business model, is not just a marketing concept, but a phenomenon that has real objective impact on banks’ operations and development.

The following results emerge from a comparison of numerous influencing factors regarding intelligent technology’s impact on banking efficiency. First, compared to Alvarez-Milán et al.’s (2018) study on consumer participation, we further analyzed consumer participation and bank innovation and found that consumer participation in both traditional self-service channels and in intelligent channels positively impacts banking efficiency and that these both exceed the impact of institutional innovation. Thus, in this service industry, the receiving-side vector (i.e., consumers who participate in service creation and continuously improve their service co-production capacity) has become more important to banking efficiency than the supply-side vector (i.e., institutional innovation). Secondly, the effect of ordinary innovation on banking efficiency improvement during the study period was very weak. Consistent with the findings of a previous study by Tiberius and Rasche (2017), we found that innovations that have significant impact on banking efficiency were often combined with intelligent technology solutions. Thirdly, during the overall research period, consumer participation in traditional self-service channels was the most important factor affecting banking efficiency, ranking slightly higher in importance than consumer participation in intelligent channels.

From the perspective of time trends, intelligent technology solutions and intelligent channel consumer participation have had differing impacts on banking efficiency. The impact of intelligent technology solutions had not been fully realized in 2007, although consumer participation in intelligent (smart) channels had begun to have a positive impact on banking efficiency at that time. Therefore, we posit that consumer demand for intelligent technology solutions spontaneously arose as various types of online consumption and financing scenarios were developed. The impact of intelligent channel consumer participation on banking efficiency has increased since 2007 and has now reached most-important status, while the impact of intelligent innovation had been increasing since 2008 and fell again in 2013.

These results show that the impact of the two vectors of intelligent banking technology have undergone a leap-frogging process of importance to banking efficiency. Consumer participation in intelligent channels has become the most important influence on banking efficiency, but this was not always the case. What’s more, as suggested by Haddad and Hornuf (2019), the unit impact of ordinary innovation has declined since 2008 to the point that it no longer significantly affects efficiency.

Consumer participation in smart channels continues to be a key influence on banking efficiency, and this reflects the ongoing intelligentization trend of banks in China. Since 2015, intelligent banking technology solutions have entered the standardization phase. Various regulations such as the Guidance on the Healthy Development of Internet Finance have been implemented, and banks have cooperated with various fintech companies to develop intelligent solutions, implement intelligent risk control mechanisms, and advance consumer-friendly interfaces.

This study contributes to the existing literature in three main ways. Firstly, our research perspective differs from that of existing literature that focuses on macroeconomic development levels, governmental regulation, and market competition as efficiency levers, and instead seeks to identify practical institutional methods to enhance banking efficiency. We view intelligent financial institutions that develop and deploy intelligent technology solutions as a unique business model and look at the impact of two vectors (i.e., institutional innovation and customer engagement) on banking efficiency. Integral to this novel business model, intelligent banking technology is agile, effective and economical. It can effectively identify and dispose of various risks, automatically match supply with demand, and enable consumers to complete complex transactions easily. Thus, it is of more practical significance to combine intelligent banking with intelligent technology solutions when assessing the overall impact on bank efficiency. Secondly, existing research related to intelligent technology solutions in the financial services industry focuses mainly on macroeconomics and regulation. It is mostly qualitative research that lacks firm-level quantitative analysis. Most extant consumer engagement-related research is limited to the marketing field and does not address the impact of consumer engagement on the efficiency of firms. This study extracts annual transaction volume from ATMs, CRSs, STMs, online banking, and mobile banking channels from the WIND database, BVD-ORBIS Bank Focus database, and the annual reports of the 58 banks; obtains the bank data of China’s top 58 banks based on assets from 2007 to 2017; and uses this data to quantitatively measure the impact of customer engagement on bank efficiency. Thirdly, in terms of measurement methods, traditional studies on banking efficiency generally utilize frontier function methods such as DEA and SFA (Shamshur & Weill, 2019), but both have inherent problems. This study innovatively adopts a semi-parametric non-frontier method (ACF method) and uses the added value of banks’ overall business as output to measure efficiency. Traditional efficiency research methods, such as SFA, rely on a variety of possible influencing factors to directly study their relationship with corporate efficiency. This, however, does not align with bank decision-making processes, and structural modeling, such as ACF, can solve this problem better. Thus, this study eliminates the theoretical and practical shortcomings of previous studies that regarded banks as merely manufacturers of deposits and loans, a view that is inconsistent with the fact that banks are becoming more and more comprehensive. Moreover, it elucidates the bank’s decision-making mechanisms more clearly.

Recommendations and Future Research Prospects

The impact of intelligent technology solutions on banking efficiency is strong, and it is driven not only by technological advances but is also by consumer participation in the service creation process. Going forward, banks should endeavor to develop intelligent technology using these two driving factors simultaneously in order to enhance efficiency.

On the one hand, banks should continue to develop and improve intelligent technology solutions, focusing on initiatives aimed at improving the security of intelligent terminals, developing effective data security measures, improving users’ security perceptions, optimizing the interface and convenience of intelligent systems, and creating points of differentiation in APP and STM interfaces. Bank executives should promote the development of mobile intelligent terminals, including mobile APP, and novel payment and open banking systems which can access more scenarios. Finally, banks should leverage technology to improve and individualize services based on consumer needs and preferences.

Banks should also implement strategies to facilitate and encourage consumer participation in intelligent channels, such as: when setting up a mobile APP or STM interface, take steps to ensure that it is friendly and attractive to novices. Second, actively expand the use of online intelligent banking systems at various venues, such as shopping malls, medical facilities, educational sites and other locations to attract consumers with less traditional financial needs; Third, banks should promote active consumer engagement in addition to participation in financial transactions. This might include encouraging consumers to forward notices, make comments and leave feedback on Twitter and WeChat. Finally, focus on promoting customers who participate in service creation via traditional self-service machines to the intelligent environment by introducing mobile apps to them, vigorously deploying STMs, and encouraging branch employees to offer customers self-service guidance.

Despite its contributions, this study has several limitations. First, the study focuses on the performance of enterprises but does not consider the impact of consumer benefits. While it is difficult to obtain consumer-level data, this is an important avenue to pursue. Second, intelligent technology has brought new risk to banks, which this study does not address mainly because there is no acceptable method yet to quantify risk in efficiency studies. Finally, this study does not compare the impact on different kinds of banks because the sample size is not large enough. Given these limitations, we plan in future research to expand the sample size or use a more scientific sampling method to conduct robustness studies, extend the research method by introducing variables that can represent risk, or collect micro-level data to conduct consumer-level research.

Footnotes

Acknowledgements

The authors would like to express their gratitude to Associate Professor Dr. Shaohua Yang from Anhui University of Technology for his insightful comments and directions on this paper. The authors would like to express their gratitude to Siyuan Gui and Haowu for their helping to revise the manuscript. The author is grateful to the anonymous referees of the journal for their extremely useful suggestions to improve the quality of the article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Innovation Fund of Research Institute of International Economics and Management, Xihua University (Grant No. 20210014)

Date Availability Statement

The raw data supporting the conclusions of this article will be made available by the authors, without undue reservation.