Abstract

Advances in technology have fueled industrial development and industry change. Digital transformation (DT) arises from integrating digital technology into traditional industries. The convergence of digital technology and traditional finance, giving rise to fintech, is progressively reshaping the current financial service model. DT empowers commercial banks to unlock the value of data as a production factor, enabling the provision of diverse financial products and services that offer crucial financial support for the digital economy. This study aims to investigate the link between commercial banks’ DT and their Financial Performance (FP), along with identifying influencing factors. Employing mechanism analysis, the research utilizes data from China’s commercial banks from 2011 to 2021. Empirical fixed-effect regression analysis is used to examine the impact of DT on FP, accounting for mediating effect. The results suggest that bank digital transformation (BDT) improves the FP of commercial banks. Moreover, bank efficiency, operational capacity, and profitability act as mediators in the correlation between BDT and the FP of commercial banks.

This study concentrates on Chinese commercial banks to assess the impacts of their DT, adding to the current research on this subject. It also provides valuable insights for investors considering commercial banks, holding significant practical importance.

Plain language summary

Technological advances have fueled industrial development and transformations. Digital transformation (DT) results from the integration of digital technology into traditional industries. The convergence of digital technology and traditional finance, giving rise to fintech, is progressively reshaping current financial service models. It empowers commercial banks to unlock the value of data as a production factor, thereby enabling the provision of diverse financial products and services that provide crucial financial support to the digital economy. The purpose of this study is to further explore the impact of bank digital transformation (BDT) on the financial performance (FP) of commercial banks, and what factors affect the relationship. Adopting a mechanism analysis, this study utilizes data from China’s commercial banks from 2011 to 2021. An empirical fixed-effects regression analysis was used to examine the impact of DT on FP, accounting for the mediating effect. The sample data includes listed and unlisted commercial banks. After processing the sample data, 1,562 sample data were finally obtained. The results continue to demonstrate a robust positive and significant correlation between the dependent variable (ROA) and the independent variable (DT of commercial banks) (b = 0.776, p < 0.01). That is to say, BDT improves the FP of commercial banks. Moreover, bank efficiency, operational capacity, and profitability act as mediators of the correlation between BDT and the FP of commercial banks. This study takes China commercial banks as the research object, which not only tests the achievements of DT of banks, but also enriches the related research on DT. Meantime, it is helpful to investors who like commercial banks and has good practical significance.

Introduction

The progress in artificial intelligence (AI) has fueled the advancement of digital technology, propelling the globe into the digital economy era, surpassing the era dominated by the Internet (Li et al., 2020). The rapid development of video conferences, online classrooms, and online consultation has injected new vitality into the construction of the digital economy (Zhao et al., 2022). The development of digitalization has not only changed residents’ existing consumption patterns but also significantly impacted the traditional banking industry (Chunfang et al., 2022). The emergence of online shopping has dramatically affected offline physical stores. The rise of third-party payment systems has influenced the traditional banking business model, prompting the industry to undergo successive DTs due to external environmental shifts. Concurrently, the advent of COVID-19 has expedited the DT processes within commercial banks (Kan et al., 2022).

In response to the evolution of the digital economy, the Chinese government has issued pertinent documents. In September 2019, the FinTech Development Plan (2019–2021) underscored the government’s commitment to advancing FinTech (Li et al., 2022). Moreover, China’s State Council revealed a comprehensive plan outlining initiatives aimed at fostering digital economy growth during the 14th Five-Year Plan era spanning from 2021 to 2025 (Luo & Zhou, 2022). Recognizing the emergence of a new technological revolution and a rapid industrial transformation, this plan acknowledges the prevailing trend of pervasive DT. It emphasizes the need to expedite the DT of various services including commerce, logistics, and finance (Zaki, 2019).

In the financial industry, DT can provide feasible technical solutions for financial innovation, make financial services more intelligent and efficient, and thus reduce the cost of financial services (Y. Chen, Kumara, & Sivakumar, 2021). Concurrently, DT has the capacity to partially surmount constraints related to time and space, catering to diverse financial service recipients and enhancing the marginal utility for financial consumers (Lorek & Spangenberg, 2014).

In the banking industry, blockchain technology is applied to China’s digital yuan; big data is used to screen customers; AI is used for outbound transactions. At the same time, the integration of financial services such as intelligent teller machines and smart point-of-sale machines indicates not only the embrace of digital technology but also the fruition of DT endeavors within commercial banks. As trailblazers in informatization, commercial banks are proactively or reactively engaging in DT efforts to align with industry trends and address competitive pressures (Wang & Wang, 2022). As one of the tools of DT, FinTech is used by commercial banks in scene construction. Integrating cloud computing, AI, 5G, and other technologies into various scenarios has innovated the financial service model (Khattak & Yousaf, 2021). Simultaneously, the issuance of government documents and the impact of COVID-19 have prompted commercial banks to engage in DT, either proactively or reactively (Tian et al., 2022). DT for commercial banks is an ongoing process, presenting a substantial opportunity for gaining a competitive edge (Naimi-Sadigh et al., 2021). Through DT, commercial banks have saved service costs, optimized service processes, and achieved differentiated services, which can enhance their competitiveness and improve their customer service capabilities. Therefore, for a prompt advancement in DT and infrastructure development, commercial banks ought to extensively implement digital technologies across various sectors (Su et al., 2022).

In order to do this research well, firstly, the literature is reviewed through meta-analysis. The keywords “DT of banks” and “FP” are used to screen 52 articles in China National Knowledge Infrastructure (CNKI) and Web of Science. However, only five articles are suitable for this study, four based on Vietnamese, African, and Serbian studies. However, China is a socialist country, and the business model of commercial banks is different from other countries. Therefore, it’s imperative to scrutinize the DT within Chinese commercial banks. Although DT has become a strategic priority for commercial banks, existing literature has several limitations. Most studies rely on case analyses, qualitative methods, or focus solely on IT adoption. Moreover, empirical evidence on the mechanisms through which DT affects FP remains scarce. This study addresses these gaps by employing a panel dataset of both listed and unlisted banks in China, and by analyzing efficiency, operational capability, and profitability as mediating pathways between BDT and FP.

During the literature review, it becomes apparent that utilizing digital technology enables commercial banks to innovate, enhance product offerings, and elevate service quality. VOICAN (2023) highlights the increasing trend of commercial banks embracing DT, integrating data into their asset management. Commercial banks leverage digital technologies like big data, AI, and blockchain to enhance customer service efficiency. Simultaneously, they extract valuable data from internal and external sources, thereby augmenting the value of their data assets. Carbó-Valverde et al. (2020) pointed out that information technology is deeply integrated into all sectors of the economy and society, and banking is no exception. Using digital technology has become an indispensable part of commercial banks’ activities to create value for customers and sell commercial banks’ products. For example, the “different people different website page” service of mobile banking (He et al., 2020). The characteristics of commercial banks make them more susceptible to the influence of digital technology. Commercial banks demonstrate innovation in digital technology through their transformation processes. Utilizing digital technology, they revamp traditional business processes, enhance customer communication, and elevate product lines and service quality. This shift makes it easier to fund ongoing investments in intellectual and technical staff, raise R&D costs, and speed up the creation of new products—all of which encourage internal innovation in commercial banks. According to Omarini (2017), DT enhances the innovation capabilities of commercial banks. This improvement is achieved through independent research or collaboration with FinTech companies to develop new products that enhance traditional offerings of commercial banks. Hawes and Chitra (2016) argued that commercial banks, by consistently reinforcing FinTech infrastructure, can propel DT. This process enhances extensive data analysis and new technology development, driven by scientific and technological innovation. They actively promote research and development of novel products, expedite market share acquisition, and accomplish rapid internal operational progress.

In addition to Chinese studies, we incorporate several international contributions. For instance, Theiri and Hadoussa (2023) examine digitization’s effect on bank performance in an African context, while Papathomas and Konteos (2023) provide a strategic framework for DT in European financial institutions. Opuni-Frimpong et al. (2025) analyze digital financial service policies and their impact on bank performance in emerging economies. These works provide comparative insights that complement our analysis of Chinese commercial banks.

In essence, prevailing literature predominantly focuses on bank digitization and its efficiency, lacking comprehensive investigation into the FP of commercial banks. Concurrently, there is a scarcity of thorough research on the underlying mechanisms. The research methods are mainly literature review and case analysis, and even less research is carried out through empirical analysis.

The primary goal of this study is to investigate an association between commercial banks’ FP and DT. This research explores the intricate relationship between banks’ DT and the FP of commercial banks using heterogeneity analysis analysis. On one front, the study examines the effects of banks’ DT, providing valuable insights for the enduring growth of commercial banks. On the other front, it addresses FP inquiries of interest to investors and shareholders, potentially garnering additional support from these stakeholders. In the long run, the DT of banks serves as a pivotal avenue for the sustainable progress of commercial banks and plays a significant role in shaping China’s digital economy (Tsindeliani et al., 2021). Therefore, this study has good theoretical and practical significance.

In comparison to existing literature, this paper makes several significant contributions. Initially, this research widens the spectrum of factors influencing the FP of commercial banks by specifically concentrating on the DT of banks. Past research has delved into the correlation between commercial banks’ FP and elements like operating model, governance structure, risk model, and strategic investments. However, minimal focus has been directed toward evaluating the influence of banks’ DT.

Additionally, this paper delves into the mechanisms through which the DT of commercial banks impacts their FP. By scrutinizing the mediating effects of DT on bank efficiency, managerial capability, and profitability, this study offers insights that aid commercial banks in comprehending the DT process.

Literature Review and Research Hypothesis

The innovation-driven development strategy theory posits that technological advancements prompt industry changes, accelerate innovation within commercial banks, and foster their DT. The ongoing integration of financial technology into commercial banks has altered traditional channels and processes, thereby bolstering the banks’ abilities in customer acquisition, business development, research and development, and guiding business development toward online and intelligent avenues. More specifically, DT has the potential to enhance both interest and non-interest income for commercial banks, decrease operating costs at bank branches, and elevate the customer experience. As a result, this has ultimately contributed to the expansion of operating results within commercial banks.

Additionally, the DT of banks has resulted in a significant increase in non-interest income. FinTech advancements have been instrumental in driving this DT within banks. Among the outcomes of this transformation is the emergence of mobile banking, enabling customers to conveniently purchase insurance, funds, precious metals, financing, and other products offered by commercial banks, all from the comfort of their homes. The number and total amount of non-deposit products sold by commercial banks through mobile banking are increasing yearly, especially with the appearance of COVID-19. As consumer spending declines, surplus funds are redirected toward acquiring short-term financing products, insurance, and funds, thereby bolstering non-interest income for commercial banks (Alzoubi et al., 2022).

Simultaneously, the DT of banks has led to a surge in interest income. The DT within banks has streamlined both the loan and approval processes. Simultaneously, the DT of banks has caused a notable increase in interest income (ElMassah & Mohieldin, 2020). Within banks, DT has optimized the lending and approval process (Khanboubi et al., 2019). The access to credit information systems and the optimization of risk models enable commercial banks to quickly and comprehensively grasp the credit situation of lenders. It is convenient and quick for loan customers with good credit information to apply for loans through commercial banks. Commercial banks give credit consumption loans to their high-quality customers in advance and push them to target customers through SMS, mobile banking, WeChat banking, online banking, and other channels. Customers can withdraw and reuse funds conveniently and quickly when they need them. The aforementioned loans have contributed to the increase in interest income for commercial banks.

In addition, the DT of banks has reduced branch operating costs (Naimi-Sadigh et al., 2021). During the digital economy era, widespread Internet usage coupled with China’s banking policy support has precipitated a decline in commercial bank customers and a substantial reduction in ATM numbers (Kitsios et al., 2021). Especially in the coming period of COVID-19, customers in China were required by the epidemic prevention policy and could not go out. Most customers solve their daily financial needs through electronic channels (mobile banking, online banking, etc.) (Zhou et al., 2021). Commercial banks, as enterprises, mainly implement the policy of “Reducing the number of storefronts and counters.” Reducing the area of business branches has saved the rent and reduced the operating cost (Schwanholz & Leipold, 2020). The downsizing of counters has freed up tellers, redirecting them toward marketing roles and other positions. This shift has enhanced operational efficiency and marketing performance within commercial banks, consequently boosting their FP.

Furthermore, banks’ DT has enhanced the overall customer experience. The integration of intelligent machines, made possible through this transformation, has enabled the substitution of numerous counter transactions with automated processes (Lee & Lee, 2019). If the cash recycling machine can replace the cash deposit and withdrawal at the counter, customers do not have to wait in line for business. Liberated tellers can serve marketing customers and solve the problem of customers not being able to use machines, thus enhancing customers’ goodwill. Investing in a coin exchange machine solves customers’ trouble depositing and changing small changes. Customers can now conveniently deposit and withdraw change directly via coin changers without requiring counter assistance. This optimized process addresses the issue of extended counter occupancy durations, thereby enhancing the operational efficiency of commercial banks (Hofmann, 2020). Consequently, this improvement elevates the customer experience, leading to heightened psychological satisfaction. The customer experience is enhanced, and the psychological satisfaction is higher. Accordingly, efforts (or perceived efforts) are related to more positive evaluations of results-for example, efforts spent in time, labor, pain, or money (Laursen & Fiacconi, 2021). Customers’ time and energy in handling business through commercial banks will be reduced, and their satisfaction will be high, which will not only increase their goodwill toward commercial banks but also increase the number of times and types of business they go to banks, thus increasing their viscosity with commercial banks and improving their FP. Following the “circle marketing” theory, enhanced shopping and banking service experiences prompt customers to share their positive encounters with friends in their social circles (Wang et al., 2023). Consequently, DT serves as a catalyst, attracting new customers to commercial banks and enhancing their FP. This transformation is pivotal for industrial upgrading and fostering economic growth. Commercial banks can provide customers with better experience and better services through DT, thus promoting business performance growth and improving FP. In this study, BDT is defined as the systematic application of emerging digital technologies—such as artificial intelligence, big data analytics, blockchain, cloud computing, and mobile platforms—to transform commercial banks’ operations, product delivery, customer interaction, and internal governance.

In conclusion, the DT within banks has emerged as the strategic focal point for commercial institutions. This transformation not only reshapes the service channels of these banks, enhancing customer experiences and satisfaction, but also caters to the increasingly diverse and personalized needs of people. Through technical equipment upgrades driven by DT, commercial banks have significantly enhanced their management, decision-making, and service capabilities. This enables them to conduct business management and innovation with greater speed and efficiency while concurrently reducing human resource costs, thereby maximizing FP. The integration of big data, AI, blockchain, and other digital technologies by commercial banks enables comprehensive data analysis. This analysis doesn’t only target customers but also provides a deep understanding of the types and levels of risks faced by these banks. It allows for timely detection of potential risks. Additionally, post DT, banks acquire the capability to predict forthcoming risks, thereby enhancing the risk management capacities of commercial banks. Building on these findings, this paper puts forth research hypothesis 1:

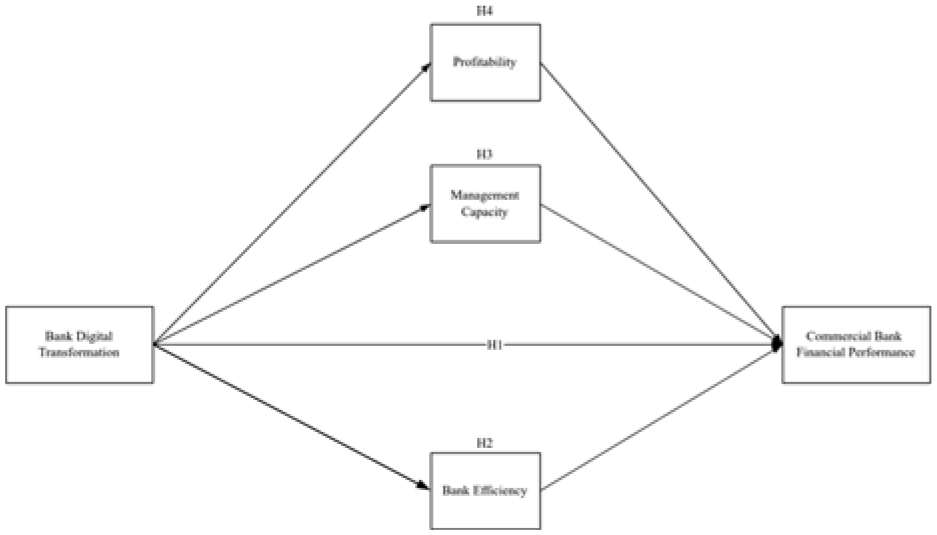

H1: Banks’ DT has the potential to enhance commercial banks’ FP.

According to traditional banking theory, the advancement of digital technology hasn’t diminished the significance of branches and physical outlets of commercial banks in mitigating information asymmetry. The moderate distance between the physical branches of commercial banks and lenders is an essential factor in determining companies’ financing costs. Empirical analysis shows that the geographical distance between commercial banks and companies is inversely proportional to the corporate loan interest rate. Due to the DT in commercial banks, there has been a decline in physical branch numbers, prompting customers to adopt alternative channels for their transactions. From the customer’s point of view, the offline business process is complicated, and there are transportation and time costs, such as going to and from the bank and waiting on the spot. However, the independent service technology of online and mobile banking can reduce customers’ transaction costs, enhance the customer experience, and have a ‘substitution’ effect on offline channels. Viewed from the standpoint of commercial banks, the approval and setup of offline physical branches entail prolonged timelines and increased operational expenses. Establishing branches consequently elevates the operating costs for commercial banks. Conversely, online channels offer a partial solution to these challenges. In terms of social welfare, banks’ DT empowers commercial banks to facilitate online loan approvals in regions with sparse branch presence, lower average household income, and significant COVID-19 outbreaks. Consequently, this DT enables an enhancement in both the efficiency of commercial banks and customer satisfaction (Liu et al., 2018).

Enhancing bank efficiency plays a pivotal role in boosting the competitiveness of commercial banks and fostering their capacity for sustainable development (Tan et al., 2021). Therefore, in the financial market, bank efficiency has become one of the critical indicators of concern for regulators and investors. DT significantly influences bank efficiency primarily through improvements in operational efficiency and customer service effectiveness.

Following the DT, commercial banks experience enhanced operational efficiency, consequently contributing to an improvement in their FP (X. Chen, You, & Chang, 2021). Internally, DT within commercial banks optimizes office processes. Additionally, financial sharing aids in streamlining internal fund utilization, thereby maximizing the benefits derived from available funds (Pramanik et al., 2019). The optimization of the office system can realize online and timely approval, which includes employee leave and financial reimbursement. From a business operations standpoint, the integration of smart machines and tools within branches can diminish wait times and streamline individual customer transactions, ultimately enhancing operational efficiency and customer contentment. This improved operational efficiency concurrently diminishes operating costs for commercial banks while augmenting revenue from available funds. Consequently, such enhancements significantly bolster the FP of commercial banks. Therefore, banks’ DT aids in enhancing commercial banks’ FP through heightened efficiency.

Introducing DT can enhance customer service efficiency, thereby positively impacting the FP of commercial banks. Moreover, in the customers’ perspective, employees displaced by smart machines can redirect their focus toward marketing activities. Intelligent outbound calls save the account manager’s time so that the account manager can have more time to serve customers and improve his professional ability to serve customers better (Pantano et al., 2020). The improvement of customer service efficiency will increase customer satisfaction. Account managers’ professional expertise enables them to better understand the requirements of incoming customers, attracting customer funds and subsequently boosting the FP of commercial banks. External marketers equipped with smart tablets can conduct door-to-door marketing and manage customer transactions remotely, further enhancing customer outreach and service. For customers doing business, the account manager can handle the collection code and POS machine on-site, which can minimize customers’ waiting time through online approval. Enhanced operational efficiency and heightened customer satisfaction levels have the potential to enhance the FP of commercial banks (Zhu & Jin, 2022).

Moreover, the DT of banks encompasses business innovation. The introduction of mobile and online banking has not only provided convenience for customers but has also boosted the non-interest income of commercial banks. If customers buy gold through mobile banking, they can order online, deliver it to the door by express delivery, and open an invoice online. Enhancing customer service efficiency within commercial banks has increased customer loyalty, thereby augmenting asset income and ultimately improving their FP.

To conclude, the DT of banks amplifies technological spillovers, consequently enhancing bank efficiency, which, in turn, positively influences the FP of commercial banks. Hence, this study proposes Hypothesis 2:

H2: The enhancement of commercial banks’ FP is facilitated by the improved efficiency brought about by the DT of banks.

Agency theory demonstrates that the functioning of commercial banks primarily relies on professional managers, specifically the presidents. Because most shareholders and investors of commercial banks are not directly involved in the operation, it is difficult for them to know the progress and effect of DT in time because of the influence of information asymmetry. Therefore, through signal transmission, shareholders and investors primarily analyze the operating ability of commercial banks through their financial reports. Operating ability is the decision-making ability of commercial banks on their operating strategies and plans, including internal conditions and excellent development potential. The operating ability is the size of the operating results determined by the quality of commercial banks and the size of their net profit (Donnellan & Rutledge, 2019).

The continuous improvement of operating ability is the foundation of commercial banks’ survival. In the face of homogeneous products and fiercely competitive markets, maintaining the continuous improvement of commercial banks’ operating ability has become the primary task for their survival and development (Song et al., 2020). At the same time, the resource-based theory shows that commercial banks are a collection of resources with potential productivity. Banks’’ DT means that resources will be invested in the direction of DT, including organization, coordination, and talent recruitment.

The operating ability of commercial banks mainly depends on how to use limited funds to bring more significant benefits. Following the DT of banks, big data can assist commercial banks in identifying customers with favorable credit profiles. By selectively allocating limited funds to particular users and enterprises through targeted customer marketing initiatives—such as intelligent outbound calls and AI-driven marketing—commercial banks can potentially decrease the non-performing loan ratio. This approach enhances the operational capability of banks, subsequently leading to an improvement in their FP (C. Chen et al., 2020). Institutional theory shows that the external environment affects the behavior of commercial banks. The emergence of COVID-19 led to the idle funds of commercial banks. Some clients face difficulties attending work, resulting in decreased incomes and an increased rate of non-performing loans. Commercial banks need to strategize on allocating idle funds to customers with reliable credit and repayment capabilities. Via DT, commercial banks have refined their credit models, enabling real-time monitoring of loan customer situations and effectively diminishing the non-performing loan rate. Additionally, financial sharing aids commercial banks in maximizing fund utilization and efficiently mobilizing available funds. This encompasses internal fund borrowing, improved capital utilization efficiency, and bolstering operational capacity, consequently enhancing the FP of commercial banks (Königstorfer & Thalmann, 2020).

Based on the signal transmission theory, commercial banks have strong operating ability, which can attract investors’ attention more efficiently, improve their financing and sustainable development ability, and thus improve their FP. The operational capacity of commercial banks mirrors their long-term and sustainable profitability. Therefore, Hypothesis 3 was formulated in this study:

H3: Enhanced operational capabilities resulting from the DT of banks contribute to the improved FP of commercial banks.

Profitability represents the capacity of commercial banks to generate profits, serving as their primary business objective. To achieve more stable long-term profitability, commercial banks focus on diversifying business settings, implementing robust risk prevention and control systems, and enhancing internal management systems (Hayati et al., 2022). Traditional commercial banks primarily derive profits from the deposit and loan spreads inherent in their deposit and loan businesses. As China advances its interest rate marketization reform, pure interest income might struggle to adapt to this evolving trend. Schumpeter’s innovation theory illustrates that innovative intermediary business practices can introduce fresh avenues for profit growth within commercial banks. Therefore, commercial banks’ development goal is to improve profitability by mediating business innovation and DT.

The one-stop service platform, fostered by innovative mediation business channels, offers convenience for customers to comprehend the mediated business products offered by commercial banks. This platform not only addresses information asymmetry issues between commercial banks’ mediated business products and customers but also reduces the matching costs associated with these products. Following banks’ DT, smaller commercial banks have the opportunity to collaborate with other banks or directly with gold and fund companies to enable online product consignment. This collaboration expands the range of bank products available, enhances non-interest income, boosts profitability for commercial banks, ultimately contributing to an improvement in their FP (Wenker, 2022). Post DT, regional banks overcome geographical limitations, allowing cardholders to directly invest and finance through commercial banking systems such as mobile banking, WeChat banking, online banking, and similar platforms. Commercial banks can activate a bank card at home, effectively solving the problem of critical customers arriving with difficulty. Commercial banks can realize remote audits and on-site activation of payment codes when marketing acquiring merchants. The mobile banking of commercial banks can be connected to the shopping platform and realize the sales of products by their reputation. Connect the campus, parking lot, and hospital platforms through the payment code to solve the payment problems (Abdelmaboud et al., 2022). The DT of banks has not only streamlined processes but has also diversified profitability, thereby enhancing the FP of commercial banks.

In summary, banks’ DT stimulates innovation within the commercial banking sector. By directly offering intermediate business products to customers, commercial banks can generate value for themselves. The innovation of mediating business products stands at the core of mediating business innovation. Concurrently, the innovation in mediating business products serves to alleviate capital constraints, optimize income structures, and enhance the capability of banks. As a result, this study proposes Hypothesis 4:

H4: The profitability resulting from the DT of banks enhances the FP of commercial banks.

Figure 1 depicts the model utilized in this investigation.

Research model.

Research Design

Sample Selection and Data Source

This study utilized a dataset comprising Chinese commercial banks, encompassing both listed and unlisted banks. The data spanned from 2011 to 2021. To improve data reliability and estimation accuracy, observations with substantial missing values or inconsistent reporting were excluded. In addition, a small number of extreme outliers were filtered based on distributional diagnostics. The final dataset contains 1,562 bank-year observations.

It is important to note that while the dataset includes both listed and unlisted banks, some commercial banks that were delisted, merged, or restructured during the study period may not be captured due to data limitations. Therefore, our findings reflect banks for which continuous and complete information was available between 2011 and 2021. The information sources encompassed the “BDT Index” from the Digital Finance Research Center of Peking University, official bank websites, and the Cathay Pacific database.

To minimize the impact of outliers on research outcomes, continuous variables underwent truncation by 1% upwards and downwards. Moreover, some continuous variables underwent logarithmic transformation to alleviate the interference of heteroscedasticity on the research results.

Definition of Variables

Dependent Variable

Listed commercial banks often employ metrics such as Tobin’s Q, Return on Assets (ROA), or Return on Equity (ROE) to evaluate their FP (Szegedi et al., 2020). The Tobin Q value is frequently utilized as a crucial indicator for assessing the FP or growth of commercial banks or companies. Different industries tend to adopt varying methods to measure FP, often due to the diverse degrees of capital utilization across sectors. For banks, insurance companies, securities companies, and other enterprises focusing on capital operation, it is more critical to use ROA to judge FP. At the same time, because the research object covers unlisted commercial banks, its market value cannot be obtained. Therefore, this study draws lessons from and adopts ROA to measure the FP of commercial banks; that is, the ratio of net profit to total assets is used as a proxy variable. Hence, this study employs ROA as a measure of the FP of commercial banks, following the approach suggested by Nawaz and Ohlrogge (2022). This indicator utilizes the ratio of net profit to total assets as a proxy variable.

Independent Variable

Scholars reviewing the current research methodologies regarding the DT of banks commonly employ various measures. These metrics encompass various indicators such as the count of monthly active users in mobile banking, technology investment, and the frequency of the term ‘DT’ within annual reports of commercial banks (Guo & Xu, 2021; Zhu, 2023). Yet, according to Xie and Wang (2023), existing index measurement methods exhibit certain limitations, failing to entirely capture the extent of DT within commercial banks. Thus, this study uses the BDT Index developed by the Digital Finance Research Center of Peking University in 2022 as a proxy variable to evaluate the degree of BDT. The index consists of three dimensions: digital strategy, digital business, and digital management. Digital strategy is assessed through the frequency of key digital terms (e.g., AI, blockchain, big data) in annual reports. Digital business focuses on the integration of digital services and fintech innovations. Digital management includes digital governance structure, talent strategy, and inter-organizational cooperation. This index has been applied in several peer-reviewed studies to evaluate DT in Chinese banks (Xie & Wang, 2023; Zhu & Jin, 2023). Although the BDT Index was formally released in 2022, it was constructed using retrospective data spanning from 2011 to 2021. Publicly available sources such as annual reports and regulatory disclosures were used to ensure historical consistency. As a result, the index offers dynamic year-by-year measurements that align with the research timeframe (Zhu & Jin, 2023). Importantly, the BDT Index is constructed as a dynamic, time-varying indicator with annual values from 2011 to 2021. Each year’s index score reflects contemporaneous textual and financial disclosures of each bank, making the proxy suitable for panel data regression analysis and capturing longitudinal trends in DT.

Although several studies have used IT expenditure, fintech investment levels, or the number of mobile banking users as proxies for DT, these metrics typically capture only one aspect of digitalization. In contrast, the BDT Index incorporates strategic, business, and management-level transformations, allowing a more holistic assessment. As noted by Xie and Wang (2023), such multidimensional indicators offer better explanatory power for bank-level performance differences.

Mediator Variable

Bank efficiency. Learned from the methodologies of previous researchers, bank efficiency is often assessed by multiplying the income-cost ratio by a negative value (Muharsito & Muharam, 2023; Zhu & Jin, 2023).

The operational capability of commercial banks, as observed in prior studies, is commonly assessed using metrics such as the total assets turnover rate and net profit growth rate (Binsaddig et al., 2023). To maintain the research’s credibility, this study incorporates the net profit growth rate and total asset turnover rate as metrics for assessing operational capabilities.

The profitability of an enterprise can be measured by many indicators, such as the net profit rate of sales and the fluctuation of stock price (Taha et al., 2023). This study focuses on commercial banks, encompassing both listed and unlisted banks. Considering data availability and the distinctive traits of commercial banks, this research utilizes capital intensity and the profits-to-cost ratio as proxy variables for gauging profitability indicators (Gao & Jin, 2022). Among them, capital intensity is a measure of the capital return ability of commercial banks, and it is a reverse indicator. Hence, the proxy variable for profitability involves multiplying the capital intensity by a negative value. The cost-to-profit ratio showcases the profit generated by commercial banks per 100 yuan of cost consumption, serving as a positive indicator representing the ratio of total profit to total cost.

The selection of mediating variables is grounded in prior research on how DT enhances organizational performance. Efficiency captures the extent to which DT reduces costs and streamlines processes. Operational capability reflects how DT enables faster service delivery and asset utilization. Profitability measures the financial return of these improvements. These mediators collectively reflect the transformation path from digital initiatives to financial outcomes.

Control Variable

To eliminate the influence of other factors, this study considers control variables such as enterprise size, solvency, growth, enterprise age, equity concentration, and enterprise nature (Liu et al., 2022). At the same time, the annual effect is controlled. These variables were selected based on prior empirical studies in the banking literature as they represent key bank-level characteristics affecting FP. For instance, size and leverage influence resource capacity and risk exposure, while ownership concentration and nature affect governance structures. Including these controls helps isolate the specific impact of BDT. Table 1 lists the variables and their definitions.

Variable Definitions.

Model Design

Benchmark Regression Model

Based on the research hypothesis 1, this study constructs the benchmark models (1) and (2) regarding Gao and Jin (2022). The model (2) has more control variables than the model (1). If α1 in the model (1) and β1 in model (2) exhibit significance, it corroborates hypothesis 1: the FP of commercial banks has improved due to the advancement of DT within the banking sector.

To address potential reverse causality, this study adopts a time-lagged design by using the BDT Index in year t−1 to predict FP in year t. This approach strengthens causal interpretation and aligns with practices in prior panel data research.

Mediating Effect Model

Hypotheses 2 through 4 are scrutinized to explore the influence of DT within banks on the FP of commercial banks. Referring to the practice of Zhou et al. (2021), a three-step regression was conducted based on model (2), and regression models (3)–(15) were constructed to control the annual effect. Hypothesis H2 underwent testing through models (3)–(5), suggesting that the enhancement in bank efficiency due to the DT of banks has led to the enhanced FP of commercial banks.

Models (6)–(10) were utilized to test Hypothesis H3, demonstrating the favorable influence of improved operational capabilities, resulting from the DT of banks, on the FP of commercial banks.

Hypothesis H4 underwent testing through Models (11)–(15), indicating that the improvement in commercial banks’ FP due to banks’ DT is linked to enhanced profitability.

According to the mediating effect test procedure proposed by Baron and Kenny (1986), the analysis follows a sequential three-step approach. In the first step, if the coefficient β1 (representing the effect of the independent variable on the dependent variable) is not statistically significant, the mediation test is terminated. If β1 is significant, the second step tests whether χ1 (the effect of the independent variable on the proposed mediating variable) is significant. If χ1 is not significant, the procedure stops. If both β1 and χ1 are significant, the third step includes both variables in the regression model. In this final step, if δ1 (the adjusted effect of the independent variable on the dependent variable) is no longer significant and δ2 (the effect of the proposed mediator on the dependent variable) exceeds β1, full mediation is inferred. If both δ1 and δ2 remain significant, partial mediation is indicated (Vo et al., 2020).

Among them, ROA stands for FP of dependent variable commercial banks, BDT stands for DT of independent variable banks, BE stands for mediating variable bank efficiency, NPGR and TAT stand for mediating variable operating ability, BC and CI stand for mediating variable profitability, Control stands for control variables, α, β, χ, and δ stand for the coefficient of each variable, ε represents a random disturbance term, and Year stands for annual effect.

Research Results

Descriptive Statistics

The dependent variable, FP of commercial banks, demonstrates an average value of 86.77, with a standard deviation of 65.11, a minimum of −77.98, and a maximum of 371.8. These figures portray considerable dispersion among commercial banks regarding their FP, indicating varying degrees of success within the industry. The independent variable, representing the progress of DT, showcases an average of 27.67, a standard deviation of 42.80, and ranges from 0 to 159. These statistics highlight significant discrepancies in the DT progress among commercial banks, showcasing varying speeds and stages of adoption, possibly reflecting divergent strategic planning approaches. The mediating variable, bank efficiency, displays an average of −37.89, a standard deviation of −15.90, and ranges from −104.2 to 0, suggesting substantial diversity in efficiency levels among commercial banks, potentially influenced by their degree of DT. Operational capabilities, reflected in the mediating variables, exhibit substantial differences among commercial banks, with an average net profit growth rate of 41.67 and standard deviation of 248.9, and an average total assets turnover rate of 2.708 and standard deviation of 1.449. These disparities underscore significant operational differences among commercial banks, possibly linked to their nature and scale. Regarding profitability, the average profitability ratio demonstrates 0.797, with a standard deviation of 1.680, suggesting relatively minor disparities among commercial banks in terms of profitability. Table 2 presents the descriptive statistics of the sample dataset.

Descriptive Stats.

Relevancy Analysis

Table 3 showcases the analysis results of the sample data, revealing a noteworthy positive correlation of 0.044 (at the 10% significance level) between the FP of commercial banks (dependent variable) and the DT of banks (independent variable). This correlation moderately supports Hypothesis 1, suggesting that the enhancement in FP of commercial banks is linked to the DT of banks.

Relevancy Analysis.

Note. Please be aware that in the table, “*”, “**,” and “***” denote significance at the 10%, 5%, and 1% levels, respectively.

In addition, the VIF test is used to verify whether there is multicollinearity between variables. The test results show that the variance expansion factor is <4, with an average of 2.17. Multicollinearity’s impact on the study’s results is negligible since none of the variables exhibited VIF values surpassing the standard threshold of 10. Hence, there’s no substantial concern regarding multicollinearity influencing the outcomes of this analysis.

Empirical Analysis Results

Benchmark Regression

Upon conducting the initial Hausman test in this study, the obtained p value was below .05. Consequently, the empirical analysis utilized the fixed effect model with the control year. Table 4 illustrates the outcomes derived from the benchmark regression analysis, with column (1) indicating the exclusion of control variables. Remarkably, the findings indicate a positive influence of banks’ DT on the FP of dependent commercial banks (b = 0.155, p < .01).

Baseline Regression.

Note. The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01.

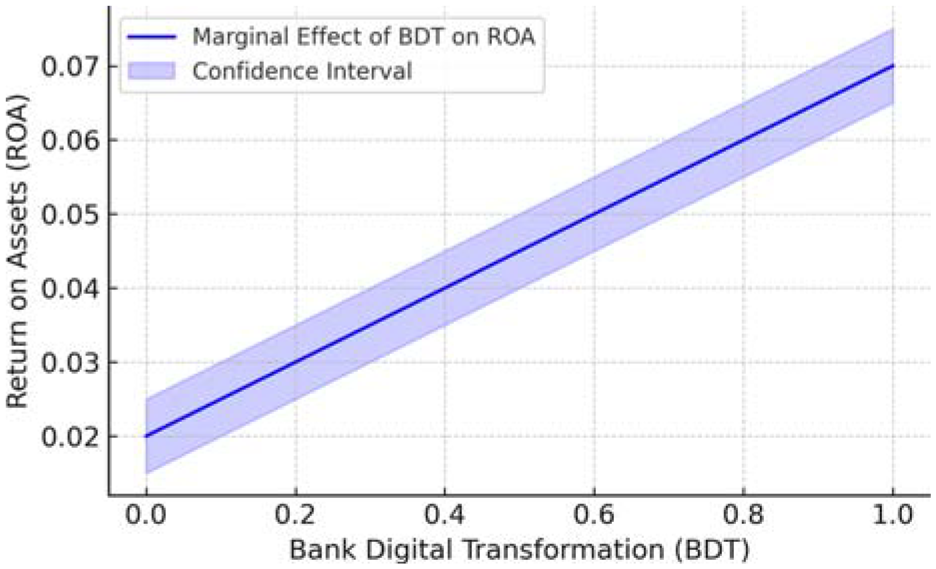

Upon the incorporation of control variables in column (2), the results continue to demonstrate a robust positive and significant correlation between the dependent variable (ROA) and the independent variable (DT of commercial banks; b = 0.776, p < .01). Notably, the correlation coefficient between the FP of dependent commercial banks and the DT of independent banks increased following the addition of control variables. Moreover, the R-squared value surged from .111 to .313. These findings indicate that including control variables significantly influences the relationship between the FP of dependent commercial banks and the DT of independent banks. Thus, reinforcing hypothesis 1, highlighting the pivotal role of DT in augmenting the FP of commercial banks. To enhance the interpretability of our findings, Figure 2 visualizes the marginal effect of BDT on ROA. As shown, the positive and stable relationship corroborates the baseline regression results.

Marginal effect of BDT on ROA.

Mediating Effect Test

Mediating Effect Test of Bank Efficiency

The examination of the mediating effect of bank efficiency is delineated in Table 5, utilizing a three-step regression analysis. In column (1), a substantial positive correlation is evident between the FP of dependent commercial banks and the DT of independent banks (b = 0.776, p < .01). Transitioning to column (2), the mediating variable, bank efficiency, manifests a notable and positive correlation with the independent variable, BDT (b = 0.060, p < .01).

Regression Analysis of Bank Efficiency Intermediary Effect.

The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01, ** for p < .05, and * for p < .1.

Moving to column (3), both the FP of dependent commercial banks and the DT of independent banks remain positively and significantly correlated (b = 0.710, p < .01). Moreover, the FP of dependent commercial banks exhibits a noteworthy positive correlation with the mediating variable, bank efficiency (b = 1.104, p < .01). These results signify that bank efficiency partially mediates the impact of BDT on the FP of commercial banks. Essentially, the improvement in bank efficiency acts as a pathway through which BDT enhances the FP of commercial banks. Thus, this analysis provides support for hypothesis 2.

Mediating Effect Test of Operating Ability

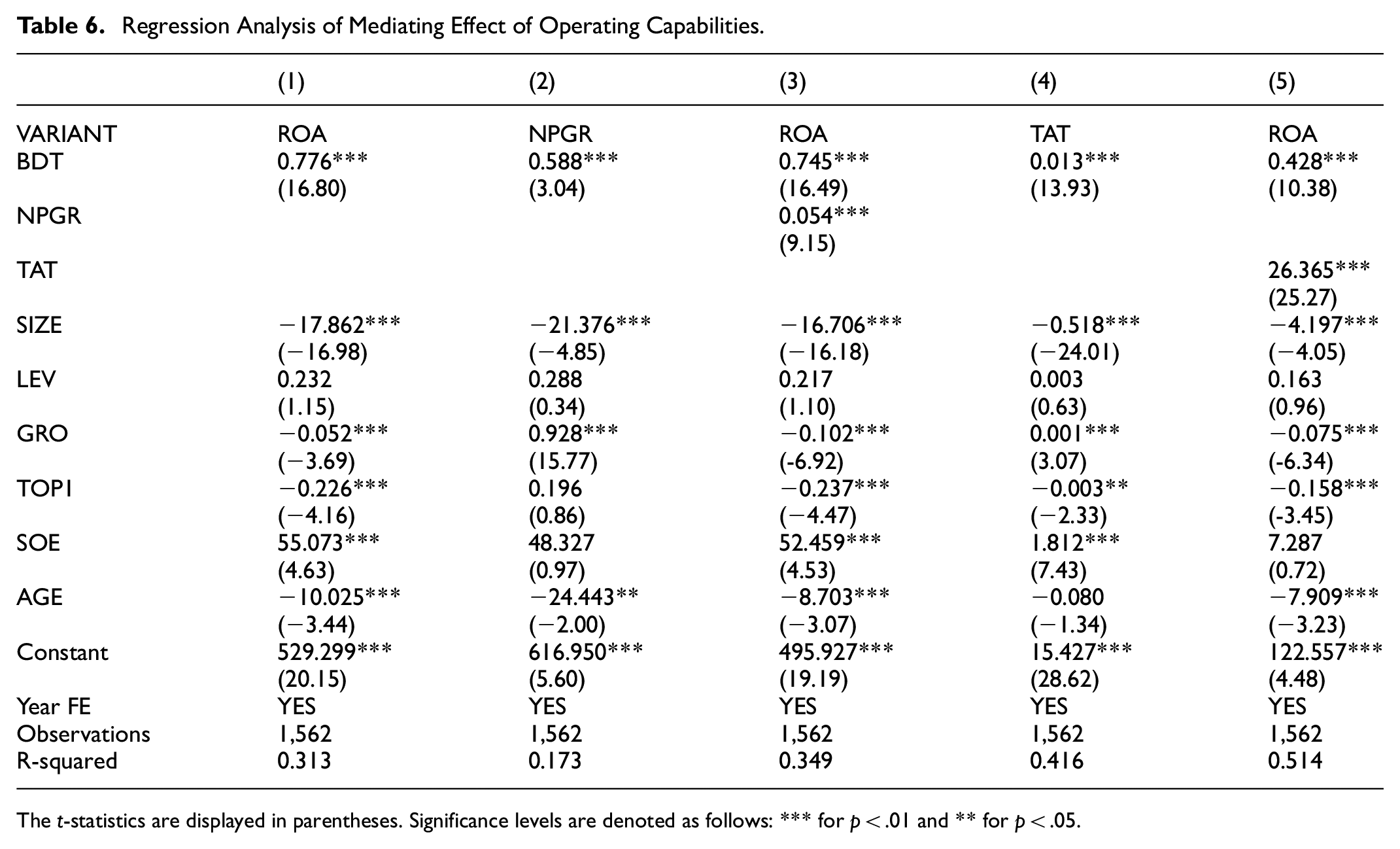

Table 6 displays the test outcomes for the mediating effect of operating capability. A three-step regression analysis was employed. Columns (1)-(3) present the mediating effect examination utilizing the net profit growth rate as the proxy variable, while columns (1), (4), and (5) showcase the mediating effect test involving the total assets turnover rate as the proxy variable.

Regression Analysis of Mediating Effect of Operating Capabilities.

The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01 and ** for p < .05.

Mediating Effect Test of the Growth Rate of Net Profit in Proxy Variables

In column (1), a significant positive correlation was observed between the FP of commercial banks (dependent variable) and the DT of banks (independent variable; b = 0.776, p < .01). Moving to column (2), a significant positive correlation is noted between the intermediary variable, net profit growth rate, and the independent variable, BDT (b = 0.588, p < .01). Furthermore, in column (3), the FP of commercial banks demonstrates a substantial positive correlation with the DT of banks (b = 0.745, p < .01). Additionally, the FP of commercial banks shows a positive correlation with the intermediary variable, net profit growth rate (b = 0.054, p < .01).

The findings suggest that the net profit growth rate functions as a partial mediator in the relationship between bank DT and commercial bank FP. Essentially, the improvement in commercial banks’ FP as a result of DT is aided in part by the development in their operational skills. Consequently, hypothesis 3 receives preliminary support.

Mediating Effect Test of Total Assets Turnover Ratio in Proxy Variable

In column (1), a significant positive correlation is evident between the FP of commercial banks (dependent variable) and the DT of banks (independent variable) (b = 0.776, p < .01). Moving to column (4), a significant positive correlation is noted between the intermediary variable, total assets turnover rate, and the independent variable, BDT (b = 0.013, p < .01). Furthermore, in column (5), the FP of commercial banks demonstrates a significant positive correlation with the DT of banks (b = 0.428, p < .01). Additionally, the FP of commercial banks shows a positive correlation with the intermediary variable, total assets turnover rate (b = 26.365, p < .01).

These findings suggest that the total assets turnover rate functions as a partial mediator in the relationship between banks’ DT and the FP of commercial banks. Thus, the enhancement of FP among commercial banks resulting from the DT of banks is partially facilitated by the improvement in their operational capabilities, particularly in terms of total assets turnover rate. Therefore, hypothesis 3 gains further support.

Mediating Effect Test of Profitability

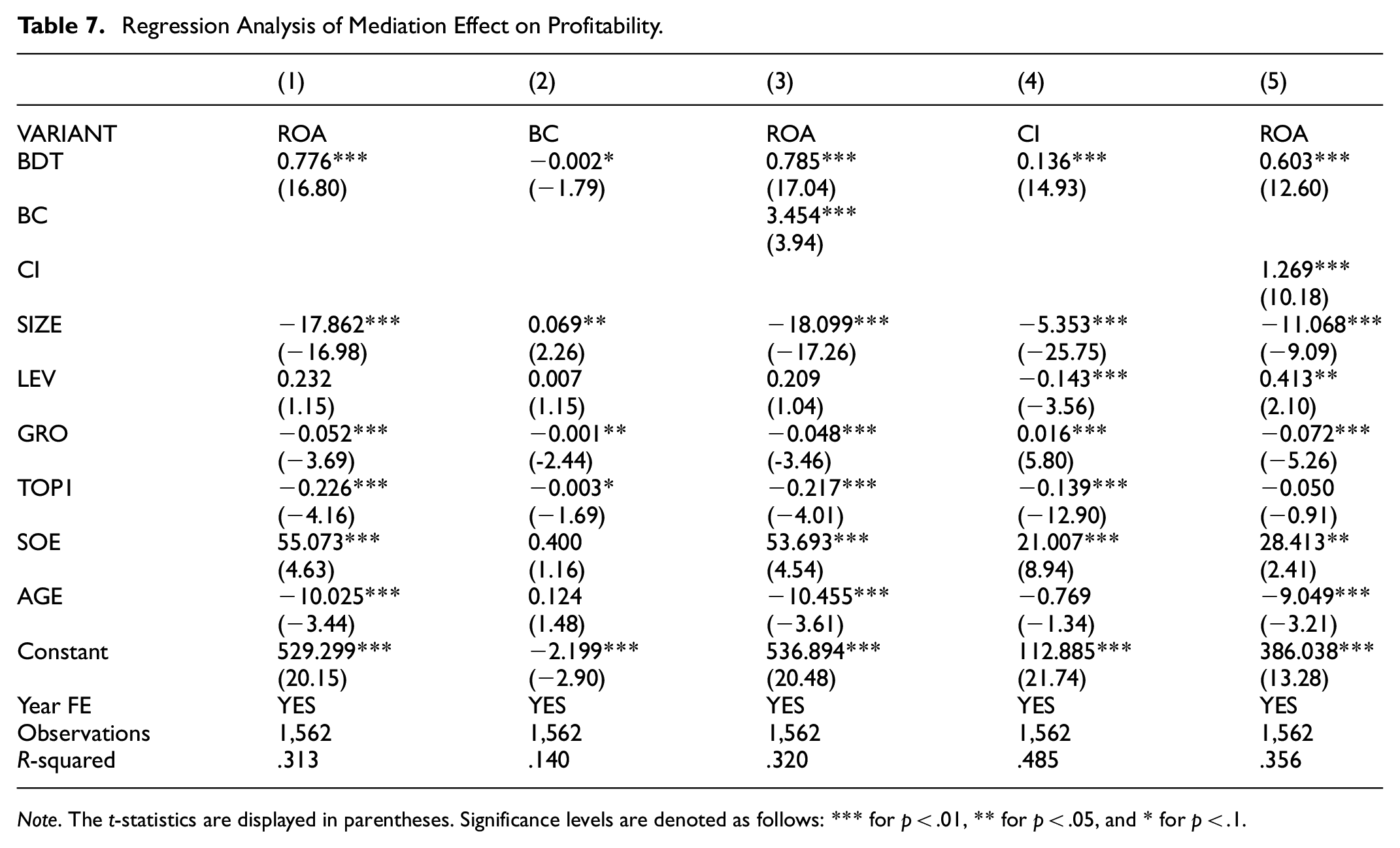

Table 7 exhibits the outcomes of the mediating effect analysis concerning profitability, utilizing a three-step regression analysis. Columns (1)–(3) present the test for the mediating effect involving the agent variable, cost-profit rate, while columns (1), (4), and (5) display the mediating effect examination of the proxy variable, capital intensity.

Regression Analysis of Mediation Effect on Profitability.

Note. The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01, ** for p < .05, and * for p < .1.

Mediating Effect Test of the Cost-profit ratio in Proxy Variable

In column (1), a significant positive correlation is observed between the FP of commercial banks (dependent variable) and the DT of banks (independent variable; b = 0.776, p < .01). Moving to column (2), there is a negative and marginally significant correlation between the intermediary variable, cost-profit rate, and the independent variable, BDT (b = −0.002, p < .1). Furthermore, in column (3), the FP of commercial banks demonstrates a significant positive correlation with the DT of banks (b = 0.785, p < .01). Additionally, the FP of commercial banks displays a significant positive correlation with the mediating variable, cost-profit rate (b = 3.454, p < .01).

The analysis reveals a negative correlation between the mediating variable, cost-profit ratio, and the independent variable, BDT. However, both the dependent variable, FP of commercial banks, and the mediating variable, cost-profit ratio, display positive correlation coefficients with the independent variable, BDT. This shows a growing link between commercial banks’ FP and DT, indicating a mediating role (Wang et al., 2022).

The findings suggest that the cost-profit ratio functions as a partial mediator in the link involving commercial banks’ DT and FP, with signs of a potential masking effect. Primarily, DT of banks can boost commercial banks’’ FP by increasing their profitability. Hence, hypothesis 4 gains initial support.

Mediating Effect Test of Capital Intensity in Proxy Variable

In column (1), a significant positive correlation is observed between the FP of commercial banks (dependent variable) and the DT of banks (independent variable) (b = 0.776, p < .01). Moving on to column (4), there is a substantial positive correlation (b = 0.136, p < .01) involving the intermediary varying, capital intensity, and the standalone variable, BDT. Furthermore, in column (5), the FP of commercial banks demonstrates a significant positive correlation with the DT of banks (b = 0.603, p < .01). Additionally, the FP of commercial banks displays a significant positive correlation with the mediating variable, capital intensity (b = 1.269, p < .01).

These findings suggest that capital intensity acts as a partial mediator in the relationship between banks’ DT and the FP of commercial banks. Hence, the improvement in the FP of commercial banks resulting from the DT of banks is partially facilitated by the enhancement in capital intensity, ultimately contributing to increased profitability. Therefore, hypothesis 4 gains further support.

Robustness Test

To affirm the credibility of the aforementioned conclusions, this study employs the following methodologies to assess their robustness.

Replace the Dependent Variable

Unlike other industries, commercial banks mainly rely on interest margins as their primary source of income, and regulators and investors often pay attention to their net interest rate of return (Puspitasari et al., 2021). Henceforth, this study opts to substitute the dependent variable of commercial banks’ FP with the net interest rate of return. Specifically, the net interest margin represents the ratio of net interest income to total interest-bearing assets.

Table 8 shows the benchmark regression analysis results for the association within the DT of institutions and the FP of financial institutions after changing the dependent variable. In the initial column (1) without any control variable, a notable positive correlation emerges between the dependent variable, commercial bank FP, and the independent variable, BDT (b = 0.439, p < .01).

Baseline Regression Analysis After Changing the Dependent Variable.

The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01, ** for p < .05, and * for p < .1.

Moving to column (2), the control variable is introduced based on the setup in column (1), revealing a significantly positive correlation between the FP of the dependent variable and the DT of the independent variable (b = 1.163, p < .01). This inclusion of control variables amplifies the correlation coefficient from the previous setup. Additionally, the R-squared value escalates from .031 to .116, indicating that the incorporation of control variables influences the relationship between the FP of dependent commercial banks and the DT of independent variable banks. Thus, hypothesis 1 is once again substantiated, suggesting that the DT of banks indeed fosters the FP of commercial banks.

Moreover, the regression outcomes derived from modifying dependent variables highlight an unchanged relationship between the DT of banks and the FP of commercial banks. This further corroborates the reliability of the study’s conclusions.

Two-Stage Least Squares Model (2SLS) Test

To prevent result deviation stemming from endogenous issues like missing variables and mutual causality, this study adopts the approach used by Gao and Jin (2022), employing the 2SLS method for endogeneity testing. Select one period before (BDT-1) and one period after (BDT+1) the banks’ DT as instrumental variables, respectively.

Regression models (16) and (17) represent the initial and subsequent stages of 2SLS(BDT-1), while regression models (18) and (19) correspond to the primary and secondary stages of 2SLS(BDT+1).

The analysis involves two distinct datasets: BDT-1 representing the previous period’s data and BDT+1 indicating data from the period before that. The regression outcomes for 2SLS are detailed in Table 9.

Analysis Utilizing the 2SLS Regression Method Involves Testing.

Note. The t-statistics are displayed in parentheses. Significance levels are denoted as follows: *** for p < .01 and ** for p < .05.

For BDT-1, the regression coefficients demonstrate a strong association between BDT and BDT-1 in the first stage (column 1), yielding a coefficient of 0.850 (significant at the 1% level). In the second stage (column 2), following the simulation of BDT and BDT-1, the regression coefficient between BDT and the FP of commercial banks stands at 0.885 (significant at the 1% level). Moreover, in Table 9, the Kleibergen-Paap rk LM statistic indicates the identification of tool variables at 276.169 (p-value: .0000), confirming their identifiability. Simultaneously, the Cragg-Donald Wald statistic registers at 5960.312, surpassing the critical value of the Stock-Yogo weak ID test (with a 10% judgment level of 16.38), affirming no issues with weak tool variables. These results reaffirm the significant positive correlation between banks’ DT and the FP of commercial banks, supporting the validity of hypothesis 1 even after accounting for endogenous issues.

Regarding BDT+1, similar analyses reveal a strong correlation between BDT and BDT+1 in the first stage (column 1) with a coefficient of 1.020 (significant at the 1% level). In the second stage (column 2), post-simulation, the regression coefficient between BDT and the FP of commercial banks is 0.775 (significant at the 1% level). The Kleibergen-Paap rk LM statistic in Table 9 attests to the identifiability of tool variables at 230.585 (p-value:.0000), while the Cragg-Donald Wald statistic, at 12,000, surpasses the critical value of the Stock-Yogo weak ID test (with a 10% judgment level of 16.38), confirming no concerns regarding weak tool variables. These findings reaffirm the significant positive correlation between banks’ digital transfer and the FP of commercial banks, providing further evidence supporting the validity of hypothesis 1 even after addressing endogenous considerations.

Conclusions and Suggestions

Discussion

Through DT, commercial banks have expanded channels, optimized processes, innovated products, improved their customer acquisition, business, R&D, and management capabilities, pushed commercial banks to be online, scene-based, and intelligent, improved their digital level, and accelerated digital progress. Commercial banks have experienced enhanced FP due to their DT, aligning with Do et al. (2022) research findings. Moreover, the study reveals a more substantial impact corresponding to the scale, indicating that larger-scale transformations yield more pronounced effects. This digital evolution within banks has shown improvements in efficiency, operational capabilities, and profitability, a trend also corroborated by Zhu and Jin (2023). This study contributes to the theoretical literature by adopting a mechanism-based analytical framework to link BDT with FP, thereby moving beyond direct effect analyses. It also provides managerial implications for commercial banks by identifying key internal performance drivers that can be optimized through digital strategies. These insights are particularly relevant for financial institutions in emerging economies undergoing rapid digitalization.

Conversely, Boufounou et al. (2022) highlighted that while customers exhibit satisfaction post-transformation, employees often face increased overtime demands during the adjustment period. Additionally, their research emphasizes the urgency of DT in commercial banks, particularly accentuated by the influence of COVID-19. This urgency undoubtedly expedites the progress of banks’ DT, consistent with the findings presented in this paper.

However, findings by Nguyen-Thi-Huong et al. (2023) present a contrasting view, suggesting that the DT within banks has a negative impact on the FP of commercial banks, diverging from the outcomes of this study. Nonetheless, their research aligns with this study’s results, indicating that banks’ DT enhances efficiency and operational capabilities.

Further exploration indicates that commercial banks encounter market competition and pressure to adopt DT. Drawing from the resource-based theory and the paradox of banking profitability, limited infrastructure resources pose obstacles to DT. This is due to the necessity of R&D expenses and the recruitment of scientific and technical personnel, making it challenging for smaller banks to observe immediate results. This notion is also supported by Xie and Wang (2023), who found that banks’ DT did not notably affect their FP in a given year. However, it showcased a positive impact on subsequent FP in the following years.

Existing research indicates that the impact of banks’ DT on the FP of commercial banks varies due to numerous influencing factors, leading to inconclusive findings. However, limited research focusing on Chinese commercial banks has resulted in a gap, attributable to the distinct scale and nature of these banks, contributing to this research void.

Building upon an investigation into Chinese commercial banks, this study delves deeper into understanding the influence of banks’ DT on FP through mechanism analyze. The findings offer valuable theoretical support for enhancing the DT of commercial banks. In the broader scope, this study suggests that the DT of commercial banks is both feasible and imperative in the long term. Consequently, it advocates for intensified and sustained efforts toward DT within commercial banks.

Research Conclusion

This study focuses on empirically investigating the correlation between banks’ DT and the FP of China’s commercial banks. Additionally, employing a heterogeneity approach, this paper explores the varying impacts of banks’ DT on the FP of these commercial banks. Furthermore, it examines this influence through mediating variables such as bank efficiency, operating ability, and profitability. To ensure the robustness of the findings, various tests are conducted, including alterations in the dependent variable and the application of the two-stage least square method.

After conducting extensive research and analysis, it becomes evident that banks’ DT has significantly enhanced the FP of commercial banks. Mechanism analysis results further elucidate that the DT of commercial banks contributes to their improved FP by enhancing efficiency, operational capabilities, and profitability. To ensure the reliability of the findings, rigorous robustness tests were conducted. These tests involved altering the dependent variable and employing the two-stage least square method. The consistency of the research outcomes following these adjustments confirms the support for research hypotheses 1–4.

Suggestions

Banks’ DT shortens commercial banks’ business processing time and reduces the business error rate, thus improving the business ability of commercial banks (Chang et al., 2020). Commercial banks have realized the customization and diversification of products through DT and improved their research development and innovation capabilities. Simultaneously, it enhances the FP of commercial banks (Venturelli et al., 2018). Moreover, to align with the advancements in the digital economy and bolster their competitiveness, continuous implementation of DT is imperative for commercial banks, aiming to expedite this transformation process (Zhang et al., 2021).Drawing from this study, the subsequent recommendations are proposed:

(1) Commercial banks need to carry out DT continuously;

(2) Commercial banks ought to tailor their DT strategies in accordance with their unique characteristics;

(3) Commercial banks can further improve their customer service level through DT;

(4) During DT, commercial banks must prioritize and reinforce their risk prevention and control measures. These risks include cybersecurity vulnerabilities, data privacy concerns, regulatory uncertainties, and operational complexity. For example, digital platforms may be more exposed to hacking and fraud, while the use of big data and AI necessitates strong data governance frameworks. Therefore, it is essential for commercial banks to integrate digital risk management into every phase of their transformation efforts.

Limitations

First, commercial banks differ from ordinary enterprises, so this study’s conclusion may not apply to other industries. Secondly, Sino-foreign joint venture commercial banks remain understudied. Additionally, various factors impacting banks’ DT warrant further discussion and research.

Second, the study focuses solely on Chinese commercial banks, whose institutional characteristics and regulatory environments may differ significantly from those of banks in other countries. Therefore, while the findings contribute valuable insights for emerging market contexts, caution is advised when generalizing them to developed economies.

Moreover, since the emergence of the novel coronavirus, there has been a decline in customer footfall at banks, leading to an increased emphasis on mobile banking activities. This situation has compelled commercial banks to expedite their DT efforts. Looking ahead, the DID (Difference-in-Differences) model could serve as a valuable tool for investigating the impact of the novel coronavirus on the DT and FP of commercial banks.

Footnotes

Acknowledgements

We would like to thank Anyang Institute of Technology for supporting this research. We would like to thank Professor Jin Shanyue for revising the paper.

Authors’ Note

We confirm that neither this manuscript nor any part of it is currently under consideration or published in any other journal. All authors have approved the manuscript and agree to its submission to your journal.

Author Contributions

Zhu Yongjie, responsible for writing the paper and organizing the data;

Jin Shanyue, responsible for revising and polishing the paper.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This article received financial support from Anyang Institute of Technology. The funding information is: Anyang Institute of Technology Doctoral Research Start-up Fund 40076512

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data available on request from the authors. The data that support the findings of this study are available from the corresponding author upon reasonable request.