Abstract

The banking sector is the main source of finance for firms in the Middle East and North Africa (MENA) region and has certain peculiarities, for example, the significant presence of Islamic banking and low levels of competition. This study examines the influence of market structure (concentration and competition) on efficiency in a sample of 239 banks operating in the MENA region over a period from 2011 to 2020. Banking efficiency scores have been obtained with the Data Envelopment Analysis (DEA), the level of concentration has been measured by the Herfindahl-Harshman index and competition has been proxied by the bank-level Lerner index. We have assessed the relationship between competition and concentration on efficiency using Simar and Wilson’s two-stage approach. The robustness has been tested using the Generalized Method of Moments (GMM) system to mitigate potential endogeneity. The results indicate that concentration influences efficiency positively and market power negatively; in terms of the interaction between both variables, bank efficiency increases, in line with the bank specificity hypothesis (BSH). Although previous papers have used various indicators of concentration and competition, to our knowledge, this study is the first to examine their combined effects on bank efficiency in the MENA region. In addition, bank-specific characteristics (size, profitability, and capitalization) and bank type (Islamic, domestic) positively affect efficiency, as do indicators of financial inclusion, institutional framework, and financial development. These aspects allow us to extract relevant results that offer a number of practical implications for managers and policy makers to improve bank efficiency.

Introduction

Since the 1990s, MENA countries have undertaken banking deregulation policies with the objective of increasing competition (Zoghlami & Bouchemia, 2021). In most of these countries, there has been a wave of liberalization and the opening-up of banking markets with the aim of reducing the involvement of the public sector (Naceur & Omran, 2011). Furthermore, in response to the financial crisis, global financial regulators have launched several initiatives to minimize the likelihood of future banking collapses. In the MENA region, there has been notable progress in bolstering prudential regulations and adopting international standards, such as the Basel III requirements and International Financial Reporting Standards (IFRS), which enhance the concentration of the banking sector (Pacter, 2017; Prasad et al., 2016; World Bank, 2020).

The MENA economy’s banking sector is the main source of corporate financing (Chaffai & Coccorese, 2023) as equity and corporate bond markets are still relatively underdeveloped (Awartani et al., 2016). Banks are a key part of economic development (Mrad & Mateev, 2020), meaning that banking competition and its effects are of particular interest in these countries. In addition, investment in the region is particularly sensitive to declining lending rates (El Moussawi & Mansour, 2022), and efficiency gains positively affect investment and economic growth.

The banking sector in this area has high levels of public ownership and a lack of competition (Awartani et al., 2016; Zoghlami & Bouchemia, 2021). For a complete view of the banking market in which enterprises operate, it is essential to bear in mind that competition and concentration are two different components of market structure. There, banks operate under monopolistic competition with considerable market power (Elfeituri & Vergos, 2019; Issa et al., 2022; Polemis, 2015). In terms of the banking market, Zoghlami and Bouchemia (2021) note that it is “moderately concentrated,” although, in recent years, there has been a trend toward making it less so as well as reducing market power. The MENA region’s lower levels of competition relative to others are due to it having scant credit information, strict rules and regulations governing bank entry, and little development of alternative sources of financing (Issa et al., 2022).

Banks are one of the key players boosting economies and financial markets globally (Hunjra et al., 2022). Furthermore, several significant changes have taken place in the industry in recent years. As the banking industry has grown, so have the number of players, and Islamic banks (IBs) have become an essential part of the banking system (Saiti & Noordin, 2018). In fact, several large conventional banks (CBs) compete internationally with IBs to offer their services (El-Halaby et al., 2018). IBs have made inroads into the global financial system, their assets having risen from $195 billion in 2000 to $2.7 trillion in 2020 (Islamic Financial Services Board [IFSB], 2021). The emergence of IBs in the MENA region has had a notable effect on the market power of preexisting banks weakening; this is attributed to the fact that IBs are newcomers to the MENA market. With this in mind and so that they can spur the market and expand their client base, they have had to exert more pressure on pricing and margins (Chaffai & Coccorese, 2023). However, recently, there has been a trend toward convergence (Mateev et al., 2022; Moudud-Ul-Huq, 2021), which may undermine the originality of the Islamic banking industry and limit its expansion (Azmat et al., 2020).

The MENA region encompasses the Gulf Cooperation Council (GCC), which is abundant in both capital and petroleum resources. The banking industry in the GCC is a key source of financing for investments in the oil and gas sectors (Mohammad, 2020). Additionally, GCC countries collectively account for over 42% of the total assets in the global Islamic banking industry (IFSB, 2019). Banks in the GCC region exhibit distinct characteristics compared to non-GCC banks, as they tend to be more competitive, with most being state-owned (Al-Khouri & Arouri, 2016; Chaffai & Coccorese, 2023).

Increased competition in the banking market has forced banks to allocate their available resources more efficiently if they want to be more competitive (Casu & Girardone, 2009). IBs and CBs, as for-profit entities, have similar goals, such as to increase the wealth of their stockholders, meaning that it is necessary to measure the efficiency of these institutions. Previous studies have shown the positive effect of banking efficiency on society in terms of welfare (Shamshur & Weill, 2019).

Efficiency studies provide valuable benchmarking information for bank managers and policymakers regarding the improvements needed to enhance banking performance (Mohini & Vilvanathan, 2021). With increased competition from several new entrants, both incumbent and new banks in the MENA region makes efficiency a top priority for both sets of professionals and for regulators (Casu & Girardone, 2009; Fiordelisi et al., 2011).

The factors influencing bank efficiency have been widely examined in the extensive literature on banking. Multiple studies have identified market concentration and bank competition as key factors influencing bank efficiency (Thi My Phan et al., 2016). The empirical and theoretical literature show that market structure has controversial effects on the efficiency of the banking system. The Quiet Life hypothesis (QLH) reveals a positive connection between competition and banking efficiency while the Banking Specificities hypothesis (BSH) implies that more competition among banks is detrimental to efficiency.

The influence of market structure on efficiency has not yet received much attention in the literature, and mixed or inconclusive evidence has been found. Most of the studies so far have focused on banking sectors in developed countries, particularly within the EU and in the USA, with just a few in developing countries, such as in MENA economies. Of particular interest here is the unstable environment in some countries, with different levels of social and technological development. The presence of Islamic banks in the region adds an intriguing dimension to its unique banking system, as they operate under a different business model compared to conventional banks. All the above characteristics are considered attractive areas for research in the MENA region.

From this perspective, the structure of the banking market is a key concern for supervisory bodies, government officials, and central banks when formulating policy measures, particularly regarding the impact of banking competition and the sensitivity of investments to fluctuations in loan rates. Moreover, both theoretical and empirical evidence suggests that the level of competition in the banking sector can affect access to financial services for individuals and businesses, thereby influencing the overall welfare of the population.

This paper posits that recent global developments are altering traditional banking structures and have prompted concerns about how they may affect the industry’s efficiency levels. However, current research on the impact of market concentration and bank competition on bank efficiency in MENA countries has lagged behind these developments. Indeed, the influence of market structure on bank efficiency remains inconclusive and not yet clear.

Furthermore, studies analyze the links between competition, concentration, and efficiency separately. Only a few papers analyze the joint influence of competition and concentration on banking efficiency, even though they use various methods to measure concentration and competition (e.g., Attia & Alber, 2022; Chan et al., 2015; Otero et al., 2020; Thi My Phan et al., 2016).

In light of these dynamics, this paper seeks to address a gap in the literature by examining how market structure, specifically market power and bank concentration, affects the efficiency of the banking sector in the MENA region from 2011 to 2020. To achieve this objective, the study addresses the following research questions: (1) How does banking market power impact technical efficiency in the MENA region? (2) What is the effect of banking concentration on technical efficiency in the MENA region? (3) What is the combined influence of market power and banking concentration on technical efficiency in the MENA region?

Banking efficiency is obtained by the Data Envelopment Analysis (DEA), and banking competition is proxied by the bank-level Lerner Index (LI), a non-structural approach. Given the relevance of market concentration and the number of rivals competition-wise, the Herfindahl-Harshman index (HHI), a structural approach, is also used as an independent variable. In addition, the effect on banking efficiency of specific bank characteristics (size, profitability, liquidity risk, capitalization, and income diversification), types of banks (Islamic or conventional, Gulf or non-Gulf, foreign or domestic, listed or unlisted), macroeconomic variables, the institutional framework, financial inclusion, financial development, and Covid19 are analyzed.

At the methodological level, Simar and Wilson’s two-stage approach (2007) has been applied, specifically using the DEA at the first stage to estimate efficiency scores and then truncated regression estimation with double-bootstrap to investigate how competition as well as market concentration affects banking efficiency. However, competition or market concentration could also depend on banking efficiency, following the efficiency structure hypothesis (Casu & Girardone, 2009). If so, there would be reverse causation. To alleviate the concern about the potential endogeneity and the persistence in the dependent variable, we have used the Generalized Method of Moments (GMM) system, as proposed by Arellano and Bover (1995) and Blundell and Bond (1998).

This study offers three key contributions to the existing literature. First, previous literature mostly uses industry-level concentration as a proxy for competition in banks because it is easy to calculate. However, higher market concentration does not necessarily indicate low competition. To assess the influence of competition on bank profitability and stability in the MENA banking sector, we measure banking competition using the bank-level Lerner Index (LI) as a direct measure of market power. Secondly, while prior research has typically examined the relationships between bank market concentration-efficiency, and between bank competition-efficiency separately, this study is, to our knowledge, the first to develop a model that explores the interactions among market concentration and bank competition on banking efficiency in selected MENA countries. Third, we test the Quiet Life Hypothesis (QLH) and the Banking Specificities hypothesis (BSH) within these economies, offering targeted recommendations to enhance bank efficiency.

The findings of this paper present several public policy implications in terms of banking sector efficiency. First, the paper supports the concentration-increasing policies implemented by regulators in several countries. These policies are needed to boost efficiency. However, these requirements should also be balanced against the need to increase competition as a key driver of operational efficiency and innovation in the financial sector. Second, bank-specific characteristics (size, profitability, and capitalization) and bank type (Islamic, domestic) positively affect efficiency. Additionally, indicators of financial inclusion, the institutional framework, and financial development also have a positive impact on efficiency.

The remainder of the paper is arranged as follows: the literature and previous experience (section 2); the methodological approach adopted (section 3); data description (section 4); the empirical analysis and the results (section 5); in the final section, the conclusions are presented.

Literature Review

Banking Efficiency: Islamic Versus Conventional Banks

Islamic banks have become an integral part of the banking system in the MENA region, as they operate on a different business model and principles than conventional banks, significantly impacting both the efficiency and structure of the banking market.

The literature on the efficiency of Islamic banks (IBs) and conventional banks (CBs) presents varying perspectives, with contradictory findings. Some studies suggest that IBs are more efficient than CBs (Eyceyurt Batir et al., 2017; Saeed & Izzeldin, 2016), while others indicate the opposite (González et al., 2019; Safiullah & Shamsuddin, 2020). These inconsistencies may be attributed to differences in estimation techniques, sample sizes, geographical regions, or time periods analyzed.

Ali (2011) highlights that Islamic finance is gaining increasing importance in the MENA region and individual countries, as it meets consumers’ financial needs while respecting their religious values. This rising prominence makes the comparison of efficiency between IBs and CBs particularly relevant in this context.

IBs act as financial intermediaries adhering to the Shariah principle, which states that IBs must not engage in transactions based on riba (interest), gharar (risk or uncertainty), maysir (such as speculation or gambling), or haram (illegal) industries (such as tobacco, alcohol, or pork; Paltrinieri & Kutan, 2019). In other words, the financial framework for IBs is based on “no exposure to toxic assets,” on transforming conventional lending into transactions based on real economic services involving tangible assets, and on profit and loss sharing, similarly to equity-based finance in the sense that lenders own a stake in borrowers’ activities (Othman et al., 2017). In this situation, IBs may require significant human capital to develop Shariah-compliant tools and may need more input to assess and monitor borrowers than CBs do. Additionally, due to their business model, IBs engage in riskier activities and many financial instruments do not comply with Islamic principles, which may cause sometimes leading to undesirable outputs (Alexakis et al., 2019; Harkati et al., 2019). Indeed, these principles may affect input, output and production technology selection in IBs, which could hinder the maximization of their production and impose further constraints in achieving efficiency.

In contrast to previous literature, other characteristics of IBs may increase their efficiency relative to CBs (Bitar et al., 2018). The business model of the Islamic banking system, in which both the bank and the borrower share the risks and rewards of an investment, incentivizes IBs to adopt more prudent lending practices than CBs, which rely on an interest-based profit maximization system, ultimately resulting in lower efficiency compared to IBs. In addition, the latter rely on real economic transactions, backed by tangible assets, which can improve their efficiency and also mitigate risks associated with market volatility. On the other hand, borrowers from IBs may be willing to pay higher fees for the intangible benefits associated with the concept of a “psychic dividend,” as noted by Bollen (2007), which could further improve their efficiency. As a result, IBs can charge higher fees and interest rates, while still attracting a loyal clientele and maintaining high levels of efficiency.

Related Hypotheses: The Quiet Life Hypothesis Versus the Bank Specificity Hypothesis

Regarding the relationship between efficiency and competition, the literature highlights two approaches. The first is the Quiet Life hypothesis (QLH) which proposes that monopoly rents disincentivize cost concerns in banks in less competitive markets, leading to inefficient allocation decisions or the pursuit of other strategic objectives that negatively impact performance (Bakhouche et al., 2022; Haghnejad et al., 2020). The more relaxed attitude in the monopolistic market permits banks to be less concerned about cost efficiency (Otero et al., 2020), where those with a large market share put more of their attention and resources into reducing risks rather than maximizing earnings (Berger & Hannan, 1998).

The second, the Bank Specificity hypothesis (BSH), states that banks are less efficient in highly competitive markets. The banking sector has some characteristics that make it unique as an industry due to information asymmetries between banks and borrowers and related problems such as adverse selection and moral hazard (Coccorese & Misra, 2022). Increased competition may increase monitoring costs and may cause the relationship with clients to be shorter, which further decreases the efficiency of banks (Apergis & Polemis, 2016; Colesnic et al., 2020; Pruteanu-Podpiera et al., 2008). Thi My Phan et al. (2016) suggests 2 potential explanations for this outcome: higher financial costs and higher operating costs. Firstly, competition between banks leads to higher interest rates, which attract depositors and expand market share. Secondly, it may make the adverse selection of borrowers more likely, thus requiring additional resources (such as employees) to screen and monitor them. These aspects make them vulnerable to strict regulation and supervision, which may affect the influence of market power on efficiency in support of the BSH (Haghnejad et al., 2020).

Empirical Evidence on the Relationship Between Market Concentration, Competition, and Efficiency in MENA Banking

The empirical literature on the influence of market structure on efficiency is inconclusive, particularly in developing countries; some studies (Al-Gasaymeh et al., 2023; Alhassan & Ohene-Asare, 2016; El Moussawi & Mansour, 2022; Nguyen & Nghiem, 2017; Supangkat et al., 2020) accept the QLH, others reject it (Apergis & Polemis, 2016; Kuessi et al., 2023; Li & Li, 2020; Sari et al., 2022; Sarpong-Kumankoma et al., 2017), and Moyo (2018), and Nyangu et al. (2022) find mixed results.

The employment of various competition proxies may account for differences in outcomes. There is no agreement on the most suitable indicator for measuring competition. According to Yuanita (2019), structural measures of competition provide different results from non-structural ones when it comes to its effect on profitability in Indonesian banks.

Moreover, most studies analyze the relationships between competition, concentration, and efficiency separately. Only a limited number of papers explore the combined influence of competition and concentration on bank efficiency, and these studies employ various methods to measure concentration and competition, resulting in inconclusive findings. Otero et al. (2020) have studied a sample of MENA region banks from 2005 to 2012, pointing out that market concentration negatively affects efficiency, thus fulfilling the QLH. Regarding competition, it has a negative influence on efficiency. They have found support for the competition-inefficiency hypothesis due to the decline in bank-customer loyalty. Chan et al. (2015) studied a sample of the banking sectors in 5 countries belonging to the Association of Southeast Asian Nations (ASEAN) from 1998 to 2012, by investigating the influence of market structure on banking efficiency. The findings imply that market power, LI, is positively correlated with bank efficiency. Moreover, the higher the concentration level the lower the bank’s efficiency, and the interaction between the LI and banking concentration negatively impacts efficiency. Lastly, they found that even in highly concentrated banking sectors, a better institutional framework plays a significant mediating role in improving banking efficiency.

Other papers point out a positive connection between banking concentration and efficiency. Thi My Phan et al. (2016) examined the link between concentration, competition, and efficiency in six Asian countries from 2005 to 2012. The Stochastic Frontier Analysis (SFA) was employed to measure efficiency, and the LI was used to gage the level of competition; the findings revealed that competition negatively influences efficiency, whereas banking concentration improves it. Attia and Alber (2022) have analyzed the association between banking concentration, competition, and efficiency in the MENA from 2008 to 2018. They conclude that it is concentration, not competition, that leads to banking efficiency.

Methodology and Data

Dependent Variable: Banking Efficiency

The study of banking efficiency can be performed in several ways: (1), by running a traditional analysis of accounting ratios, or (2), by using the distance function approach, where best practice production is represented by a “production frontier” and each “production point” corresponds to a firm that is compared to this frontier. Efficiency is usually calculated using two methods: the DEA and the SFA. This paper applies the DEA (non-parametric approach) as it is the most commonly used technique to analyze banking efficiency (Nguyen et al., 2014).

The DEA is a mathematical method developed to estimate the efficiency of a set of similar decision making units (DMUs) that can use multiple inputs to produce multiple outputs. The CCR model considers the constant returns-to-scale (CRS) assumption in the definition of the production possibility set, and the BCC model variable returns-to-scale (VRS). The CCR model assumes that all DMUs operate at an optimal scale and the BCC model is appropriate when not all DMUs are operating at this capacity (the efficiency of each DMU being calculated by comparing it with respect to the frontier represented by the units that exhibit best practices and have a similar operational scale). Perfect competition in banks is unlikely, so the BCC model is more appropriate, hence rejecting the assumption that all banks analyzed operate at their optimal capacity (H. Banna et al., 2022).

Both DEA models can measure efficiency in output and input orientation alike. The output-oriented approach measures efficiency by determining how to increase outputs with fixed inputs. In contrast, the input-oriented method reduces input resources to attain a specific output level.

To calculate the technical efficiency of banks, the output-oriented BCC model has been employed, because economic units typically aim to maximize profits with an appropriate set of productive factors (inputs).

We have evaluated n DMUs (i = 1, 2, …, n) for each period t (t = 1, …, t), considering m outputs (r = 1, 2, …, m) that produce

where

According to the banking literature, the intermediation method is better for gauging overall bank efficiency levels, while the production method is more appropriate for assessing the efficiency of different branches of the same bank. As a result, the current study selects input-output variables using the intermediation method. Following the literature (Apergis & Polemis, 2016; Dong et al., 2014), Staff expenses, Fixed assets, and Deposits are selected as inputs. In contrast, Gross loans, Other earning assets and Non-interest income are chosen as outputs.

The suggested models meet the isotonicity requirement, which requires outputs not to decrease when inputs increase, in that the correlation coefficient must be statistically significant and positive between inputs and outputs (Bowlin, 1998). Furthermore, the correlation coefficients between the selected input and output variables must be less than 0.9 (Lee & Seo, 2017).

Independent Variables: Market Structure—the HHI and the LI

Generally, the literature regarding market structure measurement is classified into two principal branches:

-The structural approach, based on the SCP paradigm, infers the degree of competition from the structure of the market. In this paradigm, market structure is represented by market concentration indicators, and the HHI is often employed by researchers (Leon, 2015). The SCP paradigm argues that in a highly concentrated market, it is easier for companies to act non-competitively.

HHI is calculated as the sum of the market shares (assets) squared in the banking sector of the given period and given country. It is written as follows:

where N is the number of banks participating in the industry, and Si denotes the market share of the bank i. The HHI index ranges between 0 and 1, the value equal to zero being perfect competition, and one indicating perfect monopoly, the higher figure indicating more concentration.

However, some authors have doubts about the reliability of the SCP model. According to Demsetz (1973), the issue with using concentration metrics as proxies for competition is that when some banks become more competitive, they force less efficient ones out of the marketplace (“efficient-structure” hypothesis). Thus, a shift in market concentration may indicate variations in efficiency rather than a change in how competitive the market is. This indicates that competition and concentration are not necessarily directly related to each other.

HHI provides some information about the market’s level of competition, but more detail is needed regarding monopolistic power.

- The non-structural approach assesses the level of competition by using different models and assumptions; to do this, the behavior of companies is observed without explicitly using information on market structure. Given the problems presented by the Boone indicator and H-statistic (Cruz-García et al., 2021), the LI has been chosen as a proxy for the level of competition in our study (the difference between the price of banking products and their marginal cost as a proportion of the price of banking products) as a direct measure of market power based on the elasticity of demand regarding price. More specifically, this metric indicates the extent of a bank’s monopoly power in its industry by its rate of profit, taking a value between 0 and 1; the closer it is to 0, the less ability it has to charge a price above marginal cost and the more competitive market conditions become.

The clear advantage of utilizing the LI as a direct indicator of market power over other measures of competition is that it can be assessed at the bank-specific level and over time, thus identifying various behavioral patterns in the respective market and/or period (Chaffai & Coccorese, 2023). Furthermore, it does not demand the bank’s geographical market to be defined (Beck et al., 2013).

Specifically, the LI for a bank

where

To acquire

where

The following restrictions are imposed on regression coefficients to ensure the homogeneity of degree one in the input prices:

The estimated coefficients of the TCF are used to calculate the MC using the observations from each bank

We have also developed an interaction term between the HHI and the market power indicator to examine how market competition affects efficiency.

Control Variables

Several control variables have been added to the regression to limit omitted variable bias. First, bank-specific characteristics have been examined. Following El Moussawi and Mansour (2022), the logarithm of total assets has been used as a proxy for bank size. Large banks are expected to operate more efficiently due to economies of scale and scope. Following Guo et al. (2020), the net interest margin has been used as a proxy for profitability. Banks with higher profitability are likely to be more efficient. The liquidity ratio has also been used as an indicator of liquidity risk, following Ruziqa (2013). A low level of liquidity may force banks to increase cash reserves to reduce liquidity risk. As a result, they might need to use outside funding, which could affect their efficiency. A higher liquidity ratio is expected to lead to improvements in banking efficiency. In addition, the capital ratio has been taken into account as a proxy of capitalization, following H. Banna and Alam (2020). The capital ratio may well positively affect banking efficiency because banks with greater levels of capital have lower funding costs and lower bankruptcy risk as a consequence. Lastly, Non-interest income to Total revenue has been used as a proxy of revenue diversification, following Alhassan and Ohene-Asare (2016). Greater diversification of a bank’s income is expected to enhance banking efficiency.

Macroeconomic factors have been considered, including inflation and gross domestic product (GDP) growth. A negative link between inflation and banking efficiency and a positive one for economic growth are likely to occur (Phan et al., 2018). Lastly, domestic credit provided to the private sector as a proportion of GDP has been used as a proxy of financial development, following Sarpong-Kumankoma et al. (2017). It is supposed that financial development contributes to enhancing bank efficiency.

The influence of the institutional framework has also been also studied. To do so, government spending and monetary freedom have been used as indicators of economic freedom in each country belonging to the Heritage Foundation’s database. Higher levels of government spending and monetary freedom indicate, respectively, that there is lower burden imposed by government expenditures and higher price stability and reliability in the absence of government intervention (Chortareas et al., 2013). Higher levels of economic freedom are assumed to improve bank efficiency. Secondly, voice and accountability is included as a proxy for the quality of institutional development for each country (Worldwide Governance Indicators). It is likely that countries with higher civil liberties, political rights, and media independence have more efficient banks (Chortareas et al., 2013; Lensink & Meesters, 2014).

According to H. Banna et al. (2022), automated teller machines (ATMs) per 100,000 adults and commercial bank branches (CBBs) per 100,000 adults are specifically considered indicators of financial inclusion. Higher levels of financial inclusion are expected to enhance bank efficiency.

Research Model: The Relationship Between Market Structure and Efficiency

At the methodological level, when using a conventional two-step procedure, two significant problems may arise: (i) sample bias in the data-generating process (e.g., an inappropriate assumption of censored regression), and (ii) the independence of the efficiency scores cannot be maintained since they are obtained from a common sample, so the presence of serial correlation produces biased estimates of the standard errors and invalidates statistical inference. To address these issues, Simar and Wilson’s two-stage bootstrap approach (2007) has been employed. One of the problems with DEA is that it can produce biased estimates of θ. In the first stage, the bias corrected efficiency scores

where

Data and Descriptive Statistics

Our investigation uses an unbalanced panel data set based on 20 MENA countries (Algeria, Bahrain, Djibouti, Egypt, Iraq, the Islamic Republic of Iran, Israel, Jordan, Kuwait, Lebanon, Libya, Morocco, Oman, Palestine, Qatar, Saudi Arabia, the Syrian Arab Republic, Tunisia, the United Arab Emirates, and Yemen), which covers the period 2011 to 2020. After discarding banks lacking data and all unplausible data values that have arisen from our variables, we have acquired a final sample containing an unbalanced panel data set for 239 banks. Before discussing the empirical results, the descriptive statistics of all the study variables must be summarized. This descriptive analysis compares CBs and IBs. The bank data in the current study has been obtained from the Orbis BankFocus database (Bureau Van Dijk), and the data on the macroeconomic factors is from the World Bank’s World Development Indicators.

Tables 1 and 2 report the descriptive statistics of the variables included in the study, covering the years 2011 to 2020. The values vary between banks and countries; however, there are a few essential general observations.

Descriptive Statistics of Study Variables.

Mean of Variables Year-Wise.

To measure technical efficiency in percentage points we have inverted the efficiency scores (

In terms of market structure, the average value for the LI in MENA banks was 0.315 during the study period, thus showing a relatively high level of market power, with results similar to previous studies by Polemis (2015), and Issa et al. (2022). The average LI for CBs was 0.326, higher than for IBs (0.279), which is consistent with Meslier et al. (2017). MENA banks experienced an increase in market power between 2019 and 2020, indicating a decline in the market’s competitive conditions during the Covid19 crisis. The average HHI assets score in MENA banks was 0.212, considered to be “moderately concentrated” (Leon, 2015), while in the CBs it was higher than for their Islamic counterparts, in line with the findings of Mateev et al. (2022). In 2020, MENA banks became more concentrated.

Regarding bank-specific factors, for MENA banks, the average bank size, measured as the logarithm of total assets, was 8.46. Moreover, CBs had larger banks on average than IBs. During the Covid19 crisis, the size of MENA banks decreased. Based on performance, the average net interest margin was 3.19% for MENA banks, where IBs were less profitable than their conventional counterparts. In 2020, during the abovementioned health crisis, MENA banks were less profitable. With an overall average liquidity of 29.24% for both types of banks, CBs held more liquidity than IBs. During the emergency phase of the pandemic, MENA banks had a higher percentage of liquidity than in 2019. The mean of capitalization was 14.39%, which was higher in CBs than in IBs. It is observed that during the critical period, MENA banks had a higher capitalization ratio than in 2019. In terms of diversification, the mean was 28.76%, higher in IBs than in CBs. MENA banks increased their diversification in 2020, showing their ability to take advantage of the crisis to diversify their revenues.

Concerning macroeconomic variables, the average GDP growth was around 1.16%, and the standard deviation was 6.08%, showing a large difference in GDP growth among the countries in the sample. The Covid19 crisis resulted in a sharp decline in GDP growth in the MENA countries, while the average inflation rate was relatively high, at 4.83%. In addition, this unprecedented period caused a steep rise in the inflation rate of the MENA countries. The average ratio of domestic credit for the private sector to GDP during the study period was 62.28%.

Regarding institutional framework, average government spending was 65.48%, average monetary freedom was 73.82%, and average voice and accountability was 22.08%; these values show significant differences between the most and least developed economies.

Concerning financial inclusion during the study period, on average the sample countries had 42.07 ATMs and 13.99 CBBs per 100,000 adults. We have noted that the number of CBBs decreased in the more developed countries. This decline may be due to these countries adopting ATM technology and online services to deliver accessible banking services to everyone, replacing conventional ones.

Empirical Results and Discussion

Simar and Wilson Model for Banking Efficiency

The result of the truncated regression is presented in Table 3, which allows us to analyze the impact of several factors on the efficiency of banks, including those associated with concentration (the HHI) and market power (the LI).

Results of Truncated Regressions of Market Structure on Banking Efficiency Using Simar and Wilson’s Algorithm II (2011–2020).

Note. The table shows the results of Algorithm II by Simar and Wilson (2007) applied to truncated regressions. The dependent variable is the efficiency score obtained by the bootstrap method in the first stage applying the BCC model with output orientation. The inputs are Staff expenses, Fixed assets and Deposits. The outputs are Gross loans, Other earning assets and Non-interest income. The regressions have been estimated with 1,846 observations. We have applied the missForest package in R to impute missing values. Time dummies are included. 2,000 bootstrap replications have been used for the bias correction of the DEA scores and for the estimation confidence intervals of the regression coefficients.

**Indicates a statistical significance at 5% level.

Column (1) displays the outcomes of estimating Equation 2, including the variables of bank-specific characteristics and macroeconomic condition, and column (2) shows the interaction term between concentration and market power. Columns (3) to (8) contain the variables of financial inclusion (the number of CBBs and ATMs), institutional framework (government spending, voice and accountability, and monetary freedom) and financial development (domestic credit provided to the private sector as a proportion of GDP). Finally, in columns (9) to (12), bank type characteristics (Islamic, Gulf, domestic, and listed) can be seen.

When interpreting the results, it must be remembered that the higher the value of

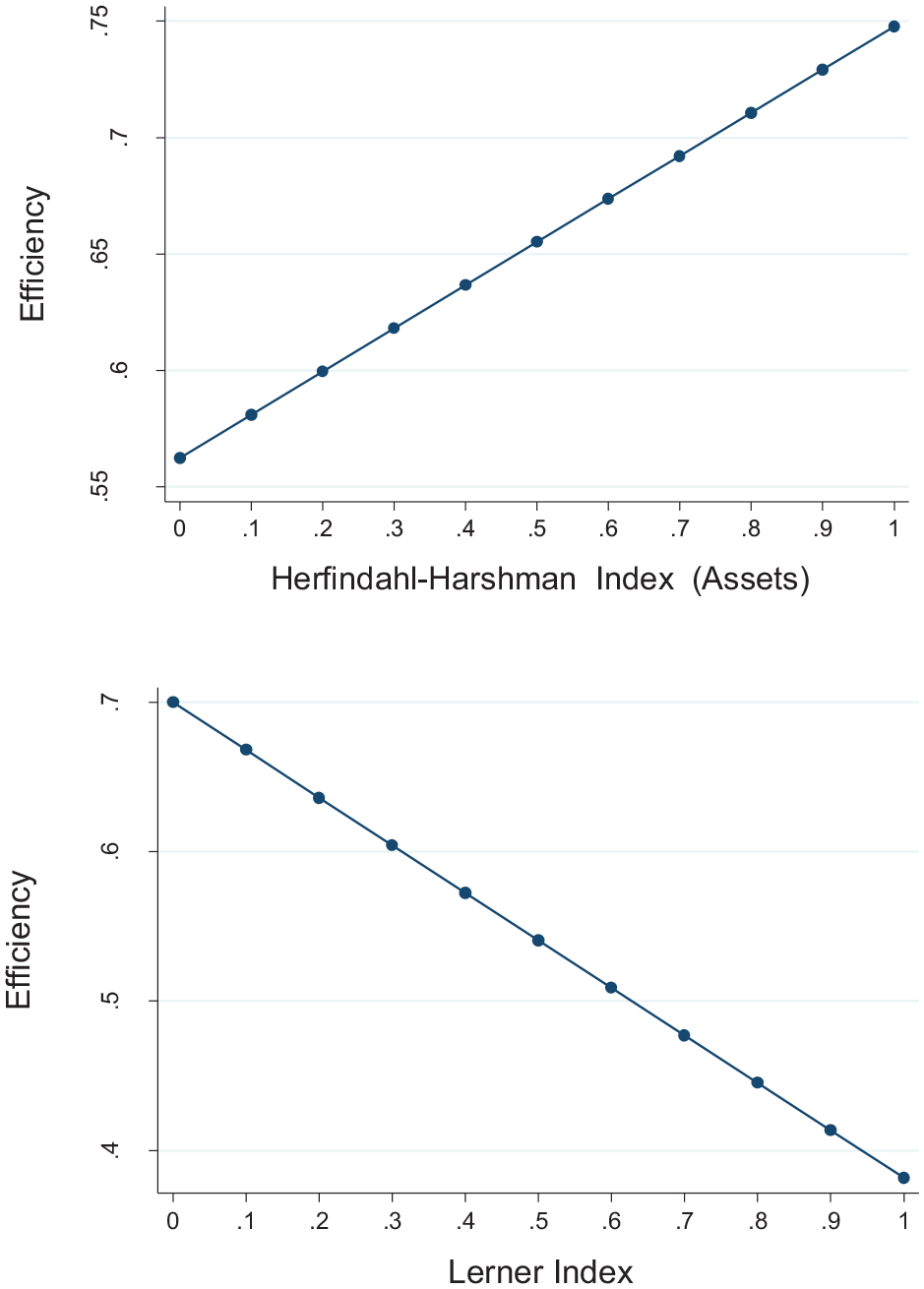

Thus, the association between the LI and efficiency is negative and statistically significant at the 5% level, that is, the greater a bank’s market power, the less efficient it is. Banks with greater pricing power can achieve higher margins between their output prices and marginal costs (Chan et al., 2015). In such cases, efficiency may not be prioritized. The QLH is fulfilled, in line with El Moussawi and Mansour (2022), and Alhassan and Ohene-Asare (2016).

Contrary to expectations, the more concentrated a country’s banking sector is when it has a high HHI, the more efficient its banks are, thus refuting the SCP paradigm and the QLH. These results are in line with Attia and Alber (2022) and Thi My Phan et al. (2016), who point out that increased banking concentration can help banks enhance their management quality in terms of efficiency. These results show the limitations of using market concentration as an indicator of competition, which does not always explain competition as measured by the Lerner index.

Figure 1 shows the linear relationship between LI or the HHI and banking efficiency, as assumed in our model.

Relationship between banking efficiency and competition indices: predictive margins.

Interestingly, the coefficient of the interaction between market power and concentration (Column 2) is positive and statistically significant. This suggests that banks with great market power in a highly concentrated market are more efficient; thus, our results reject the QLH.

Regarding the control variables, the results show that the coefficient of bank size is statistically significant and positive, indicating that the larger the bank, the more efficient it is, in line with El Moussawi and Mansour (2022). The higher the net interest margin ratio, the more efficient it is, as its estimated coefficient is positive. The more profitable banks tend to reduce production costs, thus improving efficiency (Guo et al., 2020). In most regressions, the relationship between the liquidity ratio and efficiency is not significant. Better-capitalized banks are usually more efficient, because the coefficients are positive and significant, albeit only slightly. The outcome is consistent with previous research by H. Banna and Alam (2020), which shows that higher capital reduces potential future losses. El Moussawi and Mansour (2022) mention that because shareholders monitor managers, banks can be driven to run efficiently and limit excessive risk-taking. Higher levels of revenue diversification lead to higher bank efficiency, in line with Alhassan and Ohene-Asare (2016).

Regarding macroeconomic variables, a negative association between GDP growth and bank efficiency can be observed. The negative effect of economic growth on efficiency could be explained by the fact that certain banks choose to invest in riskier assets; the negative correlation could also be attributed to the unstable growth rates in the MENA region. Such volatility reduces demand for banking services, worsens information asymmetry, increases defaults on payments and bank operating costs, and lowers efficiency (El Moussawi & Mansour, 2022). The influence of inflation on technical efficiency in the MENA countries is negative in some models, similar to Onen and Tunik (2017), while financial development leads to more efficient banks, in unison with Sarpong-Kumankoma et al. (2017). Columns 3 and 4 show that financial inclusion (measured by the variables ATMs and CBBs) positively and significantly affects banking efficiency (H. Banna et al., 2022).

Estimates have been made including different institutional variables, but only the estimated coefficient results for variables with significant influence on banking efficiency are shown. Improving the institutional environment-voice and accountability, and government spending—implies better banking efficiency. Like with the study of Chortareas et al. (2013), banks operating in countries with high degrees of economic freedom and proper governance tend to show higher levels of efficiency.

Finally, several dummy variables have been incorporated into the equations to determine whether banks are Islamic, domestic, listed or from the Gulf region, taking a value equal to 1 if true, or zero otherwise. IBs and domestic banks have positive and significant effects on efficiency. For banks that are listed or that are in the Gulf region, efficiency is negatively affected. In addition, Covid19 has no significant effect on levels of banking efficiency.

Our results show that IBs tend to be more efficient than CBs, which is consistent with the findings of Bitar et al. (2018). The same goes for Azzam and Rettab (2020), who also note that IBs are more innovative than their conventional counterparts due to their ability to adapt and make effective use of new technology, as well as having better standards of management, and higher levels of competition in the IB sector. While both IBs and CBs exercise market power, the latter may prioritize revenue from market power over efficiency and are therefore more likely to adopt “quiet life” behavior.

Our paper also reveals that banks in the Gulf region tend to be less efficient than their counterparts elsewhere. This finding is aligned with the results of previous research conducted by Bahrini (2017), which has indicated that the majority of non-Gulf banks were operating under increasing returns to scale, enabling them to achieve cost reductions. In contrast, most Gulf banks were running under decreasing or constant returns to scale, constraining their ability to lower costs. One possible explanation for this disparity is that Gulf banks are typically larger in size compared to non-Gulf banks, which may limit their cost-saving potential.

In addition, it suggests that domestic banks tend to be more efficient than foreign ones, which is consistent with previous research by Chaffai and Hassan (2019). The authors argue that domestic banks may benefit from organizational home advantages, including their knowledge of local market conditions and practices, which can enable them to better serve the needs of local businesses, and give them an edge over their foreign counterparts.

Finally, it indicates that unlisted banks exhibit greater efficiency than listed ones, as also noted by Ghosh (2014). This could be due to the lower agency costs faced by unlisted banks, which cover conflicts of interest that can arise between a company’s management team and its shareholders, and which may outweigh the benefits of market discipline and equity liquidity associated with listed banks.

Robustness Analysis

In this section we perform additional checks to verify the robustness of our empirical evidence. Firstly, given that one of the main problems in calculating efficiency using the DEA methodology is making the correct choice of outputs and inputs, we have modified them in the efficiency calculation. Hence, initially, we have incorporated non-performing loans (NPLs), which are measured by loan loss provisions, as an input (see Column 9 in Table 4). The inputs are Staff expenses, Fixed assets, Deposits, and Loan loss provisions, and the outputs Gross loans, Other earning assets and Non-interest income have been chosen. Finally, we have calculated cost efficiency (CE) according to the hybrid approach and with inputs and outputs similar to those defined by El Moussawi and Mansour (2022), who consider deposits as outputs and financial costs as inputs (see Column 10 in Table 4). In addition, we have incorporated non-performing loans as an input. As for the outputs, we have selected Gross loans, Other earning assets, Non-interest income and Deposits, while the inputs are Staff expenses, Operating expenses, Interest expenses and Loan loss provisions.

Results of GMM Regressions of Relation Between Market Structure and Banking Efficiency (2011–2020).

Note0. The dependent variable of regressions 1 to 8 is the bootstrapped efficiency score acquired by implementing the output orientation of the BCC model. Regression 9 incorporates non-performing loans (measured by Loan loss provisions) as an input, and in regression 10, the dependent variable is cost efficiency. Time dummies are included. AR(1) and AR(2) are the coefficients of first and second order correlation and applied on residual in differences. The joint validity of the instruments has been tested using the Hansen test of overidentifying restrictions.

*, **, and *** indicate statistical significance at 10%, 5%, and 1% levels respectively.

Secondly, the static panel data models are suitable for strictly exogenous variables. Because of the likelihood of “reverse causation” under the efficient structure paradigm, banking efficiency may affect market concentration and bank competition, which may therefore give inconsistent estimates. To prevent these endogeneity problems and to take the persistence of dependent variables into account, the GMM system, proposed by Arellano and Bover (1995) and Blundell and Bond (1998), has been applied with Windmeijer corrected standard errors in a two-step estimation.

Table 4 displays the estimated coefficients of the GMM system. The dependent variable of each column from 1 to 10 is the inverted bootstrapped efficiency score obtained by implementing the output orientation of the BCC model in the first stage.

All test prerequisites (Hansen, AR(1), AR(2)) are fulfilled as can be seen by the p-values; the results confirm the consistency of our dynamic panel data model. The outcome of the GMM system estimation is consistent with the previous findings and estimations both in terms of the coefficient signs and the level of significance between efficiency and market structure. Additionally, most of the control variables show results that are in line with the truncated regression model. Only income diversification and inflation show no significant effect. This implies that the results of the model are robust to change in empirical models. Of note is the positive and significant influence of the lagged dependent variable, which affirms the persistence of banking efficiency in the MENA region.

Conclusion

This paper analyzes the relationship between market structure, that is, market power and banking concentration, and the efficiency of banks in the MENA region by studying the Quiet Life Hypothesis (QLH) and the Bank Specificity Hypothesis (BSH). To do so, firstly, we have calculated the bias-corrected efficiency of MENA banks using the DEA, we have estimated bank-level LIs as a proxy for competition and done the same for the HHI for market concentration.

Our results indicate that the level of concentration positively affects efficiency, which refutes the QLH. As for market power, it negatively influences efficiency, thus supporting the QLH. When it comes to the combined effect of both variables, the coexistence of higher concentration and market power increases bank efficiency, supporting the BSH hypothesis.

The structural and non-structural approaches reveal different results that may help to design policies related to banking efficiency; if market concentration positively affects it, policymakers should not be concerned. If the QLH is fulfilled, measures to improve efficiency and competition are necessary (González et al., 2019).

Regarding bank-specific variables, size, profitability, capitalization, and liquidity positively affect efficiency in most of the models analyzed. Moreover, an effective institutional framework and adequate financial development, as proposed by economic theory, contribute to higher levels of efficiency. The results also show a strong relationship between banking efficiency and financial inclusion. IBs and domestic banks have positive and statistically significant effects on efficiency. Conversely, it is negatively affected in listed banks and those in the Gulf region.

The impact of this study extends beyond academic circles, offering valuable implications for policymakers, bank managers, regulators, and governments to enhance the efficiency of the MENA banking system.

The paper therefore supports the policies of increased concentration pursued by regulators in several countries to boost efficiency. In principle, this consolidation of the financial system can be seen as beneficial, especially if it also reduces excess capacity and improves operational efficiency. This has important policy implications in light of significant bank consolidation in the MENA region following the financial crisis and the implementation of Basel III requirements.

However, regulators in the MENA region must exercise caution when increasing concentration in the banking industry. Excessive concentration can lead to increased market power, which may result in larger institutions becoming more administratively and operationally complex, potentially undermining efficiency. Consequently, it would be more advisable for them to encourage mergers or acquisitions of smaller banks with less market power to improve efficiency. Additionally, increased market concentration could lead to higher costs and diminished effectiveness in banking supervision, while also exacerbating the problem of “too big to fail” institutions.

For MENA nations, which have a comparatively high level of banking sector concentration, this topic is especially crucial. The existence of larger financial institutions may not always imply less competition, based on the low degree of association between the LI and market share, which calls into question the ideal size of financial institutions.

Moreover, our results point to competition as a key driver of operational efficiency and innovation in the financial sector. However, these benefits need to be carefully weighed against potential drawbacks, such as increased risk-taking, which could lead to solvency issues and instability in the financial system.

Finally, we suggest that competition enforcement may not be equally beneficial in all countries. Bank supervisors and regulators in the MENA region must take into account the significant differences between Islamic banks and conventional banks, as well as the varying institutional contexts and levels of competition across MENA nations.

These elements enable us to derive meaningful insights with practical implications for policymakers, bank managers, regulators, and the government to enhance bank efficiency. From a policymaker’s perspective, it is crucial to establish long-term strategies that balance market power and bank concentration in the banking sector, as these factors significantly influence efficiency. For instance, supporting policies that promote the mergers of smaller banks can help them benefit from economies of scale, given that larger banks are often associated with greater efficiency. Furthermore, it is important to monitor market power closely, as its recent increase has been shown to negatively affect efficiency. Policymakers should also encourage the adoption of fintech and financial innovation to boost productivity, reduce costs, and control input prices, thereby enhancing bank efficiency. From a managerial perspective, bank managers should recognize that increased market power does not automatically lead to greater efficiency. They should focus on reducing production costs and optimizing resource allocation by continually improving their operational practices and management skills. For regulators, strengthening capital adequacy remains essential, as higher capitalization has been shown to improve efficiency. From a governmental standpoint, reinforcing the institutional environment is vital, as a robust institutional framework has been observed to enhance bank efficiency. These measures will enable more effective resource allocation by banks, benefiting society and fostering economic growth in the MENA region.

As with all papers, ours has some limitations, which should be the basis for future research and must therefore be mentioned. The main issue is that it is limited to the MENA region, thereby making it difficult to generalize its results. Despite this, the number of countries and the size of the sample analyzed make it relevant to a notable number of countries around the world, which in general, have institutional environments similar to those of many emerging countries. Second, this study specifically focused on a non-parametric approach, namely DEA, to measure bank efficiency. In terms of bank competition, we used a limited number of measures, precisely the HHI and Lerner index, which represent both structural and non-structural approaches, respectively. Future research could look at other developing countries, efficiency measures, and new variables such as Environmental, Social, and Governance (ESG), or globalization.

Footnotes

Ethical Approval

Not applicable.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge financial support provided by the Xunta de Galicia through research project Consolidación 2024 GRC GI-1866 Valoración Financiera Aplicada-VALFINAP (ED431C 2024/08).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be made available upon reasonable request from the authors.