Abstract

In this paper, we aim to investigate the impact of the top management team (TMT) on the performance of cross-border M&A, using a sample of 270 cross-border M&A events of Chinese listed companies. We find that the heterogeneity of TMT characteristics could affect the performance of cross-border M&A in different ways. More specifically, a higher heterogeneity in gender can improve the M&A performance significantly, while more heterogeneities in tenure and overseas background lead to a significant reduction in long-term and short-term M&A performances, respectively. We believe that our study can contribute to a different perspective for the selection of the executive teams of M&A companies. This, in turn, is conducive to optimizing the structure of the senior management team, and may help companies make better decisions and improve their performance.

Keywords

Introduction

The top management team (TMT) is a paramount entity within an enterprise and plays a dual role as both decision-makers and implementers. Variation within the team in terms of demographics, such as family background, gender, age, educational background, tenure, and work style, can result in significant disparities in creative thought. The diversity of TMT can have a substantial impact on the enterprise’s decision-making processes, particularly in regards to strategical investment decisions that involve balancing local and overall interests, short-term and long-term interests, and economic and social benefits. The effects of this diversity, which arises from differences in cognitive abilities, value orientations, behavior patterns, and work experiences, may occur implicitly and be overlooked or underappreciated in the decision-making process.

One of the earliest studies on this topic was conducted by Cox and Blake (1991), who found that diversity in race, ethnicity, and gender was positively related to team innovation and problem-solving effectiveness. Subsequent studies have confirmed these findings and expanded on the concept of TMT heterogeneity by considering various dimensions of diversity (Lee et al., 2022; Ormiston et al., 2022). On the positive side, a highly heterogeneous TMT, that is the MTM members with different backgrounds, would have a deeper understanding of the complex environment, and can make more efficient decisions for the enterprise. Some scholars believe that the heterogeneity of the TMT is conducive to bringing more information and diversified cognition to the enterprise, so as to improve business performance. Ma et al. (2022) tested the impact of TMT experience heterogeneity on enterprise innovation quality, and found that TMT functional experience heterogeneity positively affects partner diversity to promote innovation quality. Tao (2018) took science and technology enterprises as the research object and found that the diversity of the TMT’s characteristics were positively correlated with corporate performance, that is, increasing the proportion of female leaders could improve corporate performance. Tihanyi et al. (2010) took 126 American electronic industry enterprises as research samples and found that tenure heterogeneity was significantly positively correlated with internationalization business performance. Senior executives with high tenure heterogeneity had richer social experiences and could resist various risks on the road of internationalization. Carpenter et al. (2004) found that the higher the educational level heterogeneity and tenure heterogeneity of executive teams, the more enterprises tend to globalize their strategy.

However, the mechanisms through which TMT heterogeneity can lead to improved firm performance are still not well understood. Despite the positive findings, there are also some studies that have found no significant relationship between TMT heterogeneity and firm performance. Some scholars believe that the heterogeneity of the TMT makes it difficult to communicate among members with different backgrounds, reduces the cohesion of the enterprise, and damages the business performance of the enterprise as well. The heterogeneity of the TMT may lead to the failure of the team, resulting in the formation of small groups within the enterprise. Barkema and Shvyrkov (2007) found that team members tend to identify more with individuals having similar characteristics and who enjoy more pleasant and cooperative. However, they tend to identify less with individuals who are different from them, which is likely to cause conflicts and affect the decisions of enterprises. Carpenter and Fredrickson (2001) proved that the heterogeneity of executive team functions is not conducive to the improvement of enterprise internationalization performance. The heterogeneity of executive teams leads to slow decision-making, which is not conducive to enterprise development. Members with similar tenure share a common cognitive structure, which greatly reduces the occurrence of team conflicts and promotes effective communication among team members. Boone et al. (2004) proposed that there is a critical value for the heterogeneity of the TMT, and if it exceeds the critical value, it will harm the interests of an enterprise. Amason et al. (2006) measured the performance of start-up enterprises by accounting indicators such as profit margins on sales (ROS), and found that the heterogeneity of the characteristics of senior management teams was significantly negative to the performance of enterprises. B. Liu et al (2015) took small and medium-sized enterprises as research samples and found that the greater the heterogeneity of age, tenure, and occupational background of the senior management team, the worse the business performance of the enterprise.

There have been several studies that have investigated the relationship between top management team (TMT) and M&As. These studies have sought to understand the impact of TMT on the success of M&A transactions. Xie et al. (2019) investigated the effect of executives’ foreign experience on cross-border M&A sustainability, taking a sample of Chinese listed companies that have completed cross-border M&As during 2008 to 2016. They found that the specific foreign experience based on target country significantly improves cross-border M&A sustainability, and executives with host-specific work experience plays a more important role than that of education experience. Parola et al. (2015) uncovered the performance effects of TMT gender diversity in M&A process. Their findings showed that TMT gender diversity is beneficial to pre-integration performance, but hinders post-integration performance. Meanwhile, the findings provide evidence that acquirer experience can overcome the negative effects of gender diversity in post-integration performance.

In addition, using both the educational background and employment history of the corporate executives and directors as social tie, Lin and Wang (2014) found that acquirer-target social ties have a significantly negative effect on post-merger performance. Meanwhile, the negative effect of social ties on post-merger firms’ short-term returns will decrease (become less negative) when the firms have good corporate governance mechanisms.

The literature suggests that TMT can have both positive and negative effects on the success of M&As. The specific effects of TMT heterogeneity on M&A success may depend on the type of heterogeneity and the context of the M&A. More research is needed to fully understand the relationship between TMT heterogeneity and M&A success.

Cross-border M&As are an important means for enterprises to carry out international business and a convenient way for enterprises to expand overseas markets and acquire advanced technologies. Since the reform and opening up, under the influence of economic globalization and the implementation of the “Belt and Road” strategy, the pace of cross-border M&A by Chinese enterprises has accelerated. Before 2018, the number and scale of Chinese cross-border M&As showed a growing trend of common growth. However, due to the escalation of China-US trade friction, since 2018, the scale of cross-border M&A by Chinese enterprises has continued to decline. Furthermore, not all enterprises have obtained the expected benefits in frequent cross-border M&A. The success rate of overseas M&A by Chinese enterprises from 1991 to 2013 was around 40 to 50%. Comparing with such rate in developed countries in Europe and America, there is still a great room for improvement for Chinese enterprises.

It is our interest to conduct an empirical test on cross-border M&A from the Chinese market by conducting tests on how TMT heterogeneity impacts on the performance of cross-border M&A of Chinese listed companies. As an important means of international operations, cross-border M&A is a convenient way for enterprises to explore foreign markets and acquire advanced technologies. There is abundant literature related to the performance of cross-border M&A, but there are still some deficiencies. Research on factors affecting the performance of cross-border M&A mainly focuses on institutional environment, cultural differences, and transaction modes, ignoring the main role of the senior management team. And little literature starts from the perspective looking at the heterogeneity of the TMT. Most of the studies on the influence of the characteristics of the TMT related to the performance of cross-border M&A start from the homogeneity of senior management teams, and there are few direct studies on the heterogeneity of TMT and the performance of cross-border M&A. Using the existing literature, it is relatively simple to study the relationship between the two, lacking of in-depth discussion.

Our study can contribute to literature in multiple ways. First, the prior literature remains mixed about the actual impact of TMT heterogeneity on firm value via different channels. By selecting 270 cross-border M&A events of Chinese listed companies, we are able to provide new evidence on how heterogeneity in TMT can affect corporate decision-making processes.

Second, our study can contribute to the literature studying the performance of cross-board M&A by Chinese public companies. China has become the second largest economy around the world and attracted more and more attentions from the researchers. To our knowledge, this is the first study to investigate the impact of TMT heterogeneity on the performance of cross-board M&As by China A-share companies. It will help a better understanding how China public companies are making their significant decisions.

Third, our findings contribute to the literature in cross-border M&A performance. The M&A performance could be affected by many factors. The management team is playing an essential role through this process. This study helps understand better on the mechanism how TMT could affect the performance of cross-border M&A.

The structure of the remaining research is as follows. We put forward eight hypotheses on how the four heterogeneity characteristics of TMT, that is, education, education, gender, overseas experience, and tenure, impact on long-term and short-term cross-border M&A performance in Part 2. Part 3 describes our model and data. Part 4 presents the regression estimation and robustness tests, and part 5 summarizes the paper.

Hypothesis

Heterogeneity of Education

The heterogeneity of education refers to the extent of differentiation of educational levels among members of the TMT. It has been established that a person’s educational level has a direct effect on their cognitive and problem-solving ability (Ge & Chen, 2016). This, in turn, has a significant impact on the day-to-day operation and major strategic decisions of enterprises.

Studies have shown that highly educated executives in enterprises have strategic thinking, possess a more long-term vision, and are less likely to harm the long-term development of enterprises for immediate interests (Gao & Wang, 2019). These executives tend to command higher prestige within the enterprise due to their superior learning, information collection, and information processing abilities. These qualities allow highly educated TMT members to adapt quickly to new environments and command greater credibility among their peers.

The education level of TMT members is, therefore, an important factor in determining the background and overall capabilities of the team. When senior management members possess higher educational backgrounds, it suggests that they have received a longer period of education, have a greater pool of knowledge, and are less likely to experience internal conflicts.

However, higher educational heterogeneity among TMT members may also lead to negative impacts. When there is a significant difference in the level of education received by senior executives, it can result in individualization and diversification often appear within the team. The difference between members to recognize, analyze, and solve problems is obvious, which leads to internal contradictions (D. S. Li & Wang, 2019). Furthermore, excessive heterogeneity in education can also lead to differences in decision-making, negatively impacting decision-making efficiency (Knight et al., 1999). Therefore, as for the relationship between the heterogeneity of the education level of the TMT and the performance of cross-border M&A of listed companies, we assume the following:

H1a: The heterogeneity of the education level of TMT is negatively correlated with the long-term performance of cross-border M&A.

H1b: The heterogeneity of the education level of TMT is negatively correlated with the short-term performance of cross-border M&A.

Heterogeneity of Gender

As society progresses, the prominence and impact of female managers in TMT continues to increase. Research has revealed that female managers tend to be better at forming positive relationships with external stakeholders, improving team decision-making abilities, and driving business performance when compared to male executives. Studies show that female managers tend to employ an interactive leadership style when making decisions and solving problems. This helps all members of the TMT to obtain complete information, so as to be flexible in responding to the dynamic environment (Wiersema & Bantel, 1992). Additionally, female managers are often characterized as being conservative, cautious, kind, and friendly, and are effective in supervising male managers (Gao & Wang, 2019). Female executives also tend to excel in communication and exhibit perseverance when facing challenges (W. M. Li & Huang, 2014). Furthermore, women are known for their sensitivity and attention to fostering mutual understanding and respect among team members (D. S. Li & Wang, 2019). The inclusion of female managers in the TMT can, to a certain extent, improve the social image of the enterprise, show its positive attitude toward women, gain a better reputation for the enterprise, help the enterprise to obtain resources, and improve the performance.

In cross-border business activities, it is crucial for enterprises to cultivate good relationships with external stakeholders. Female executives can leverage their unique strengths to establish a favorable image for enterprises, and promote the smooth development of cross-border M&A when they are in contact with the external environment. Therefore, we assume the following:

H2a: Gender heterogeneity of the TMT is positively correlated with the long-term performance of cross-border M&A.

H2b: Gender heterogeneity of the TMT is positively correlated with the short-term performance of cross-border M&A.

Heterogeneity of Overseas Background

The heterogeneity of overseas background among members of the TMT refers to the variations in their international experiences. When engaging in cross-border M&A, it is essential for enterprises to comprehend the host country’s economic and political landscape, cultural norms, and corporate culture. Senior executives with overseas background bring to the table their familiarity with foreign languages, cultures, and customs, as well as a larger network of social capital and international relationships (Ancona & Caldwell, 1992). This enhances their ability to gather valuable information, improves their cognitive skills and problem-solving abilities (O’Reilly et al., 1989), and ultimately reduces the risk and increases the profitability of cross-border M&A (F. C. Liu et al., 2017).

However, a diverse overseas background within the senior management team may pose short-term challenges in cross-border M&A. Senior management teams with rich overseas experience may be “acclimatized” (Yu et al., 2010). Although members with overseas experience have higher education levels and overseas experience, they may lack the local contacts (H. Li et al., 2012), thus reducing the short-term performance of an enterprise in cross-border M&A. Therefore, we assume the following:

H3a: The heterogeneity of the overseas experience of the TMT is positively correlated with the long-term performance of cross-border M&A.

H3b: The heterogeneity of the overseas experience of the TMT is negatively correlated with the short-term performance of cross-border M&A.

Heterogeneity of Tenure

The heterogeneity of tenure within a TMT can have a significant impact on various aspects of senior management, including industry cognition, interpersonal relationships, and experience accumulation (Gao &Wang, 2019). Generally, longer tenure among senior executives is typically associated with greater familiarity with the company, deeper emotional attachment, higher dependence, and a focus on long-term value (Carpenter & Fredrickson, 2001). Senior executives with similar tenure have higher loyalty to the company and lower turnover rate (O’Reilly et al, 1989). The longer the tenure of the TMT, the longer the TMT can maintain the stability of the team and reduce the conflicts among team members (Zhang, 2006).

However, it is important to note that longer tenure of the TMT members can also lead to a higher risk of conservative thinking, while senior executives with shorter tenure are often associated with more innovative ideas and make more flexible decisions. In the process of M&A, the combination of both long-tenured and short-tenured members can lead to a complementary advantage (Xu, 2017). However, research also shows that executives with different tenures have different feelings toward enterprises (Xu, 2017). The heterogeneity of the tenure of senior executives mean that they have different career stages within the company. They may have different opinions on the strategic choices and development paths of the company (W. M. Li & Li, 2015). In summary, we assume the following:

H4a: The heterogeneity of the TMT’s tenure is negatively correlated with the long-term performance of cross-border M&A.

H4b: The heterogeneity of the TMT’s tenure is positively correlated with the short-term performance of cross-border M&A.

Model and Data

We set up the following model to analyze the influence of heterogeneity of the characteristics of the TMT on the performance of cross-border M&A:

In the model, i represents the enterprise, t represents the year, and e represents the error term. TMAP specifically includes CAR or FAP, where CAR represents the short-term performance of an enterprise’s cross-border M&A, and FAP represents the long-term performance. Hgenit, Heduit, Hovsit, and Htenit are the heterogeneity of gender, education, overseas experience, and tenure of the TMT respectively. Mit is the control variable, including LEV, OCC, SIZE, and SOE, which represents the asset-liability ratio, ratio of the largest shareholder, the enterprise scale, and the type of enterprise ownership, respectively.

Referring to Pan and Yu (2014), we adopt CAR as the short-term performance measurement cross-border M&A. The announcement date of M&A is taken as the zero day of the event, (−150, −30) day is selected as the event estimation period, and (−5, 5) day is selected as the window period to calculate the excess return rate of individual stocks.

The formula is the cumulative abnormal return rate of a stock during the window period, where Rit is the actual return on the stock, and Rmt is the market return.

From the Zephyr Global M&A Transaction Analysis Database (Zephyr), we collected the 2010 to 2017 cross-border M&A events of Chinese enterprises listed in Shanghai and Shenzhen stock markets. All characteristics data of enterprise executives and the financial data of M&A were obtained from China Stock Market & Accounting Research Database (CSMAR), and the samples were processed as follows:

(1) Delete the enterprises whose stock code contains ST or ST* in the sample.

(2) Enterprises with incomplete data were excluded.

(3) Delete listed companies in the banking, insurance, and other financial sectors.

(4) Choose the event with the largest amount of overseas M&A if in the same period, the acquirer carries out multiple M&As.

According to D. S. Li and Wang (2019), there are two main methods for measuring the heterogeneity of executive team characteristics. The first method involves measuring categorical variables using the Herfindahl-Hirschman Index (HHI). The H value represents the level of differentiation in the executive team, and ranges from 0 to 1. The larger the H value, the greater the difference in that particular characteristic of the executive team. The second method involves measuring continuous variables using the coefficient of variation as the measurement index. The formula for calculating the coefficient of variation is the standard deviation divided by the mean of the values.

Following the definition of the senior management team in CSMAR, we use the information of CEO’s, deputy general managers, financial controllers, and other senior managers disclosed by the company to be considered as TMT member for our research. As for the measurement of heterogeneity of education (Hedu), we refer to the research of Yang and Zhang (2018), and assign a value to the education of senior executives according to the following criteria. People below junior college are assigned a value of 1. The value of a college degree is 2. The value of a bachelor degree is 3. The Master degree is 4, and the doctoral degree is 5. The HHI of Hedu is calculated to measure Hedu according to the above assigned value. Hedu value is between 0 and 1, and the higher the value, the greater the heterogeneity of education among members of TMT.

Referring to W. A. Li et al. (2014) and other scholars, we use the proportion of female managers in the senior management team as a measured indicator of gender heterogeneity (Hgen). The HHI of Hgen is calculated according to the above assigned value.

We refer to F. C. Liu et al. (2017) and their approach to measuring the heterogeneity of overseas backgrounds (Hovs). We assign a value to the overseas background of senior executives: having no overseas background experience as 1; having overseas study experience as 2; having overseas work experience as 3; and for both overseas study and work experience as 4. The HHI of Hov is calculated according to the above assigned value. Hov value is between 0 and 1, and the higher the value, the greater the heterogeneity of overseas background heterogeneity among the TMT members.

We use the standard deviation coefficient of tenure to measure heterogeneity (Hten), that is, the ratio of standard deviation of tenure over the mean value of tenure year.

As to the control variables, the logarithm of the total employment of the company is selected as the measurement of the company size (SIZE). Generally speaking, the larger the enterprise, the greater the capital and more numerous the personnel, which is conducive to the smooth development of cross-border M&A activities. In addition, large enterprises are more able to resist the risk of cross-border M&A.

Asset-liability ratio (LEV) is the ratio of total liabilities and total assets of an enterprise. The asset-liability ratio has a far-reaching impact on enterprises.

The ownership concentration degree (OCC) reflects the ownership control status of an enterprise. The ownership concentration degree has a significant impact on the business decisions of enterprises. Enterprises with a high ownership concentration degree have more concentrated power and higher decision-making efficiency, but they are also prone to the problem of a lack of restraint to their power.

For ownership (SOE), we assign a value of 1 for state-owned enterprises and 0 for private enterprises. At present, state-owned enterprises are still the most important subject of cross-border M&A in China, and their special relationship with the government has a double-sided impact on the performance of cross-border M&A.

Factor analysis is used to estimate the long-term performance (FAP). According to Zou and Xie (2011), eight financial indicators were selected from four categories: the profitability, debt paying ability, growth ability, and operation ability to estimate the year end performance value. FAP is the difference of the estimated performance value between year T and T + 1.

Before factor analysis, KMO test and Bartley test should be used to judge whether it is suitable for factor analysis. Generally, if the KMO value is greater than 0.5 and the Bartley test p value is less than .05, then factor analysis is applicable to the sample data. This paper selects eight accounting variables of the year of M&A (T) and the year after M&A (T + 1) for factor analysis.

As can be seen from Table 1, KMO values are all greater than 0.5, and the p value of Bartley test was less than .05. The results indicate that the samples are suitable for factor analysis.

KMO and Bartlett tests.

We extract the factors from variables. From Table 2, we can see the degree of interpretation of different indicators from the percentage of variance. Taking the data in the year T as an example, we extracted three factors Y1, Y2, and Y3 from eight indicators, and the extracted factor variance contribution rate accumulatively reached 59.308%.

Variance Contribution on Year T.

It can be seen from Table 3 that Y1 mainly explains three indicators: X1, X2, and X6; Y2 mainly explains two indicators: X3 and X5; Y3 mainly explains three indicators: X4, X7, and X8.

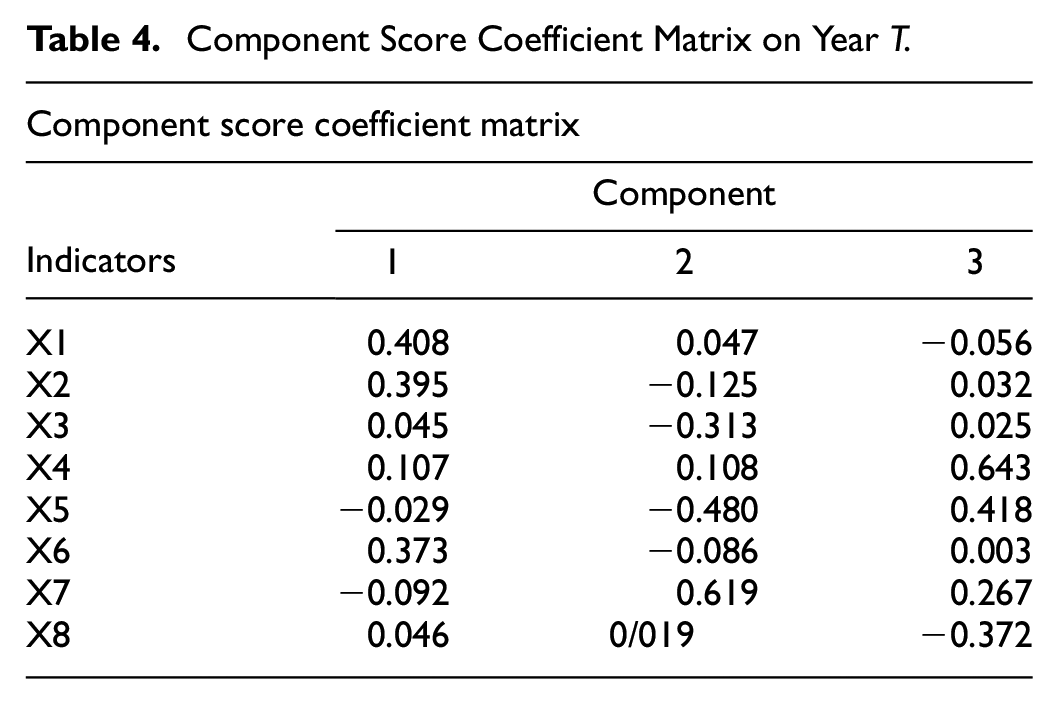

Component Matrix on Year T.

As shown in Table 4, taking the financial data of enterprises on the year T as an example, we can calculate the score of each factor according to the score of each indicator.

Component Score Coefficient Matrix on Year T.

Taking the financial data on year T as an example, the score function of the common factor can be known according to the factor score coefficient matrix table of Table 4. The weighted average of the common factor score according to the factor variance contribution rate in Table 2 is the comprehensive score function, and the comprehensive score can be calculated by inserting specific data into the composite score.

In the end, we obtained 270 cross-border M&A cases of Chinese enterprises from 2010 to 2017. The descriptive statistics includes the mean, standard deviation, minimum, and maximum values of each variable. The specific results are shown in Table 5 below.

Descriptive Statistics.

Table 5 shows that the average long-term performance of the dependent variable (FAP) is −2.38e-09, and the average short-term performance (CAR) is −0.220, indicating that the performance of cross-border M&A in recent years is not ideal. The average Hedu was 0.535, the minimum value was 0, and the maximum value was 1, with a large gap. The mean value of Hgen was 0.197, and the distribution was relatively uniform. The average Hovs experience was 0.112, and the overall distribution was relatively uniform. The average level of Hten was 0.495, the overall distribution was uneven, the maximum value was 1.603, the minimum value was 0, and the difference was large. In terms of the degree of centralization of the largest shareholder (OCC), the difference of ownership concentration is obvious. The average level of LEV is 1.621%, the minimum value is −4.6%, and the maximum value is 34.722%, indicating that the capital structure of enterprises varies greatly. The enterprise scale (SIZE) adopts the logarithmic form, with the average level of 8.409, the minimum value of 5.088 and the maximum value of 13.207, indicating that the scale difference of cross-border M&A enterprises is small. The mean value of enterprise ownership (SOE) is less than 0.5, indicating that private enterprises account for a large proportion of cross-border M&A enterprises.

We analyzed the correlation between heterogeneity of the TMT and the performance of cross-border M&A, in order to investigate whether there is multi-collinearity among various variables. Pearson correlation analysis test was conducted, and the results are shown in Table 6.

Correlation Coefficient Matrix.

Significance levels of 10%.

Significance levels of 5%.

Significance levels of 1%.

From the correlation analysis results, we can observe the magnitude of the correlation coefficient. When the correlation coefficient is greater than 0.75, there may be a problem of multi-collinearity in the model. As can be seen from the data shown in Table 6, the correlation coefficient between all the selected variables is lower than 0.75. The variance inflation factor analysis was carried out, and the results showed that the VIF values of all variables were less than the critical value of 10, so it demonstrated that there was no serious multi-collinearity problem between the variables in this paper.

Empirical Analysis

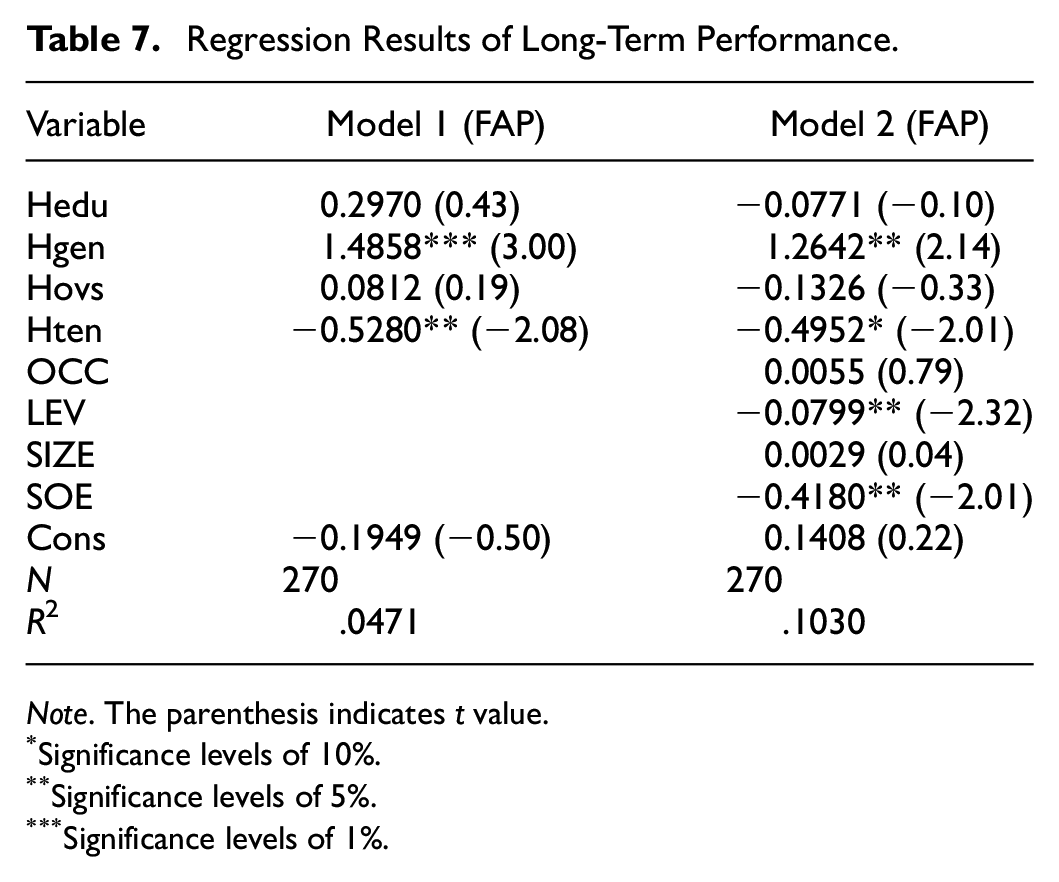

According to the models established above, data of heterogeneity of senior management team, long-term performance of cross-border M&A and other control variables were used for the regression analysis. Table 7 shows the regression results of the long-term performance model of cross-border M&A affected by heterogeneity of TMT.

Regression Results of Long-Term Performance.

Note. The parenthesis indicates t value.

Significance levels of 10%.

Significance levels of 5%.

Significance levels of 1%.

According to the results, hypothesis H2a and H4a that were proposed, have been verified. The regression coefficient between the gender heterogeneity of the TMT and the performance of cross-border M&A is 1.4858, and is a significant positive correlation at the level of 1%. This is because female executives are usually more sensitive to risks, and more meticulous in exploring and solving problems. Moreover, female executives have stronger teamwork abilities, which is conducive to improving their ability to solve complications of cross-border M&A. The heterogeneity of tenure is also significantly negatively correlated with the performance of cross-border M&A, with a correlation coefficient of −0.5280. This is because senior management teams with large tenure gaps tend to form small groups, resulting in faults and divisions, which intensifies the internal contradictions of the team and reduces the cohesion of the enterprise. This is not conducive to the rapid and effective decision-making processes of cross-border M&A. In addition, the corporate leverage ratio is also significantly negatively correlated with the performance of cross-border mergers and acquisitions at the level of 5%. The high corporate leverage ratio indicates that the financial risk of the enterprise is high. The ownership type of enterprise is significantly correlated with the performance of cross-border M&A. The correlation coefficient is −0.4180, indicating that the performance of cross-border M&A is significantly better than that of state-owned enterprises. This is because state-owned enterprises are associated with the government, and their special nature may become a stumbling block in the process of cross-border M&A. When faced with cross-border M&A of state-owned enterprises in many countries, the examination process will be more rigorous and even be rejected unreasonably. In all, the research shows that the null hypothesis H2a and H4a are valid according to the test results.

We further make an empirical analysis of the heterogeneity of the TMT and the short-term performance of cross-border M&A. As shown in Table 8, the regression coefficient between the heterogeneity of the education level and the short-term performance of cross-border M&A is −1.8917, which presents a significant negative correlation at the 1% confidence level. This is because the level of education affects the members’ cognitive ability, the way of thinking, and the ability to solve problems. Executives with different educational backgrounds tend to have communication barriers and have lower decision-making efficiency. The heterogeneity of the overseas experience of the TMT is also significantly negatively correlated with the short-term performance of cross-border M&A, with a correlation coefficient of −2.5327. The senior management with overseas experience may lack the connection with the local population and be unfamiliar with the local corporate culture, which would cause the culture crash among the TMT. At the 5% confidence level, the corporate leverage ratio is significantly negatively correlated with the short-term performance of cross-border M&A, with a correlation coefficient of −0.1092. The size of an enterprise is positively correlated with the performance of cross-border M&A, with a correlation coefficient of 0.3008. If the size of an enterprise is large, the funds and personnel are normally sufficient, which is conducive to resisting the risks in the process of cross-border M&A. Enterprise ownership was significantly correlated with the short-term performance of cross-border M&A, and the correlation coefficient is −0.5369. Therefore, hypothesis H1b and H3b are accepted for the short-term impact.

Regression Results of Short-Term Performance.

Note. The contents in brackets are T values.

Significance levels of 10%.

Significance levels of 5%.

Significance levels of 1%.

To ensure the robustness of the results, ROA is used as a long-term performance indicator for cross-border M&A. Table 9 shows the estimated results after indicator adjustment. Compared with the above estimated results, gender and tenure heterogeneity are confirmed to be valid in the robustness test, and the influence of corporate leverage ratio and corporate ownership is also verified. Thus, hypothesis H2a and H4a proposed in this paper have been verified.

Robustness Tests for Long-Term Performance.

Note. The contents in brackets are T values.

Significance levels of 10%.

Significance levels of 5%.

Significance levels of 1%.

At the same time, in order to verify the robustness of the short-term performance of cross-border M&A, this paper changes the event window period to (−1, 4) for the test, and Table 10 gives the estimated results of the short-term performance of cross-border M&A. The heterogeneity of education fails to pass the robustness test, while the heterogeneity of overseas experience is still significantly negatively correlated with the short-term heterogeneity of cross-border M&A, so hypothesis H3b is accepted.

Robustness Tests Short-Term Performance.

Note. The contents in brackets are T values.

Significance levels of 10%.

Significance levels of 5%.

Conclusion and Suggestion

The prior literature has shown that the heterogeneity of the TMT characteristics can affect the decision-making, management, and performance of the enterprise. However, it remains unclear on how such heterogeneity of the TMT can impact the business performance of the enterprise. Both positive and negative effects have been identified by the previous studies, implying that the TMT heterogeneity could be a “double-edged sword.” On the one hand, heterogeneity of the TMT can bring diversified information and improve the team’s problem-solving ability; on the other hand, heterogeneity of the TMT means that the team contains differentiation and individualism, which can easily lead to differences among members and reduce decision-making efficiency.

In this paper, we aim to investigate the impact of the TMT on the performance of cross-border M&A, using a sample of 270 cross-border M&A events of Chinese listed companies. We find that the heterogeneity of TMT characteristics could affect the performance of cross-border M&A in different ways. More specifically, we found that the increase in the proportion of female managers in senior management teams of Chinese listed companies has a significant positive impact on the long-term performance of cross-border M&A. It may be driven by two factors. First, the participation of female managers within the TMT can give play to the unique advantages of women and complement the advantages of male managers. Second, it is conducive to maintaining good connections with the external environment of the enterprise.

On the other side, we found that the heterogeneity of tenure in the TMT is negatively correlated with the long-term performance of enterprises. It may be attributed to the fact that the heterogeneity of tenures will affect the communication mode and efficiency between managers, and thus affect the conditions related to getting along with each other. When the heterogeneity of the TMT tenure is large, the members’ mutual recognition is low, which tends to affect the tacit understanding of the team, reduce team cohesion, and is not conducive to the improvement of corporate performance. In addition, the influence of heterogeneity of education level and overseas experience on cross-border M&A long term performance has not been confirmed.

We also find that the heterogeneity of overseas background of TMT is negatively correlated with the short-term performance of cross-border M&A. Although the senior management team with rich overseas experience can bring more efficient management methods to the enterprise, they may lack sufficient domestic work experience, and their working methods are prone to conflict with domestic managers.

In sum, we find that the heterogeneity of different TMT characteristics can affect the M&A performance in different ways. Such study contributes important practical implications, regarding how to improve corporate governance. For example, gender equality can play an important role, specifically in the process of cross-border M&A. Also, it is very important to maintain the stability of the senior executive team. Too much difference in the term of senior executive team members can easily lead to team fragmentation and division, and members are more likely to recognize members with similar characteristics to themselves because they have similar cognitive structures. Members outside the small group are often excluded, causing team conflicts and destroying team cohesion. Cross-border M&A are important strategic decisions for enterprises and require efficient cooperation within the senior executive team.

Based on our study, we found the firms’ performance has large room to improve by perfecting corporate governance. We suggest to promote gender equality in the labor market. Compared to male managers who tend to take risks and be innovative, female executives are more cautious and conservative in their actions. The decisions made by female managers are usually more prudent. At the same time, female executives have a higher ethical level and lower agency costs, which can avoid inappropriate actions taken by managers for personal gain. Therefore, enterprises should fully utilize the role of female executives, give women equal job opportunities and promotion channels, avoid setting a “ceiling” for female executives, and promote gender equality in the labor market. The participation of women in the senior executive team is beneficial for complementing and coordinating with male executives, promoting the smooth development of cross-border M&A.

We also suggest to maintaining the stability of the senior executive team. Enterprises should appropriately extend the term of senior executive team members, especially during cross-border M&As, to ensure the stability of the senior executive team. Too much difference in the term of senior executive team members can easily lead to team fragmentation and division, and members are more likely to recognize members with similar characteristics to themselves because they have similar cognitive structures. Members outside the small group are often excluded, causing team conflicts and destroying team cohesion. Cross-border M&A are important strategic decisions for enterprises and require efficient cooperation within the senior executive team. Therefore, enterprises should avoid frequent turnover of senior executive team members and ensure the stability of the senior executive team.

Due to our limited access to the data, we are unable to go further in looking at the issue in this study. For example, if we know what is the primary motivations for each M&A event, we are able to gain more insights how decisions were made given different reasons behind such corporate events. Also, if the properties of acquired firms of these M&A events are known, we can even understand more about the decision-making process. In general, we believe that our study can make significant contributions to the prior literature in related areas and more future studies are required to help understand this topic better.

Footnotes

Author Contributions

Conceptualization: Yingna Wu, Liang Ding, Jun Chen

Data curation: Xuan Song, Yingna Wu

Formal analysis: Yingna Wu, Liang Ding, Xuan Song, Jun Chen

Investigation: Yingna Wu, Liang Ding, Xuan Song, Jun Chen

Methodology: Liang Ding, Yingna Wu

Project administration: Yingna Wu

Software: Liang Ding, Xuan Song

Writing – original draft: Yingna Wu, Liang Ding, Xuan Song

Writing – review & editing: Yingna Wu, Liang Ding, Jun Chen

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

This article does not contain any studies with human participants or animals performed by the authors.