Abstract

This study examines US cross-border mergers and acquisitions (M&As) from 1990 to 2014, analyzing acquirer motivations and their long-term market performance implications. Diverging from previous research, it investigates how pre-merger driving factors impact post-merger synergies. Lower book-to-market ratios and higher debt ratios signal aggressive and leveraged expansion strategies. Profitable firms with high asset turnover and institutional ownership exhibit greater motivation for takeovers. Post-M&A, larger acquirers with higher dividend payouts, profitability, conservative management, and operational efficiency achieve superior long-term returns. Corporate governance factors play a role, with increased institutional ownership enhancing long-term performance, while high ownership concentration among the top shareholders hinders it. The study provides insights into the motivations and long-term implications of cross-border M&As by examining the impact of pre-merger factors on post-merger synergies.

Introduction

Cross-border mergers and acquisitions (M&As) have become a dynamic and increasingly prevalent phenomenon in today’s globalized business environment. Driven by firms’ pursuit of synergies, international expansion, and alignment with global sustainability objectives, these transactions offer immense potential yet remain complex and unpredictable. The motivations and determinants of successful cross-border M&As continue to puzzle researchers and practitioners, with empirical evidence reflecting diverse outcomes across different countries and contexts. Studies by auditing firms, such as KPMG, highlight significant failure rates driven by factors including cultural incompatibility, differences in employee values, incompatible information systems, and insufficient financial resources to support ongoing operations and seize new opportunities (Goerdeler, 1999).

This study delves into the unique dynamics of cross-border M&As, which differ substantially from domestic deals due to additional complexities, such as country risk variations, cultural differences, and regulatory disparities. These distinctions imply that acquirers must consider unique factors that can either hinder or facilitate successful transactions. Understanding these challenges is crucial for developing strategies that mitigate risk and enhance the likelihood of post-merger success.

This study aims to shed light on the motivations and sources of synergies for cross-border M&As through three specific research questions. First, we explore how firm characteristics influence managerial decisions regarding M&As, considering factors such as risk exposure, profitability, and financial flexibility. Second, we investigate the strategic issue of international expansion through cross-border M&As, examining how motives can stem from firms’ desire for diversification and the role of institutional investors in driving M&A activity. Finally, we analyze the post-M&A performance of firms to understand the long-term implications of these transactions.

To address these complexities, this research focuses on three pivotal questions. First, we examine how firm-specific characteristics—such as risk exposure, profitability, and financial flexibility—influence managerial decisions regarding M&As. Second, we investigate the strategic drivers of international expansion through cross-border M&As, including firms’ diversification motives and the influence of institutional investors in catalyzing M&A activity. Finally, we analyze post-M&A performance to understand the long-term implications of these transactions.

The preparation phase of cross-border M&As is critical for the success of subsequent implementation. This phase demands rigorous financial restructuring and comprehensive due diligence to assess the target company accurately. Key considerations include determining an accurate valuation using methods like Net Present Value (NPV) derived from discounted cash flows and the market capitalization approach (DePamphilis, 2019). However, the decision to engage in cross-border M&As is a strategic imperative for board directors, often influenced by capital market imperfections that make diversification attractive (Adler & Dumas, 1975; Errunza & Senbet, 1984). Additionally, corporate governance mechanisms, notably the role of institutional investors, play a vital role in shaping M&A activities. Differences in governance standards across countries can motivate M&As, particularly when the combined entity adopts superior governance practices, thereby benefiting target shareholders (Erel et al., 2012). This study evaluates how various types of institutional investors impact M&A decisions and subsequent long-term performance.

While previous studies suggest that acquirers often underperform in the long run after cross-border M&As (Black et al., 2007; Conn et al., 2005; Gregory & McCorriston, 2005), there is also contrasting evidence (Ahmed & Elshandidy, 2018). To address these inconsistencies, our research investigates the relationship between pre-merger drivers and post-merger synergies in U.S. cross-border M&As from 1990 to 2014, focusing on firm characteristics, operational performance, and corporate governance factors.

Our findings offer critical insights into how acquirer characteristics, operational performance metrics, and corporate governance factors influence the motivations for and performance of cross-border acquisitions. We find that firms with lower book-to-market ratios, higher debt ratios, and lower payout ratios signal aggressive, leveraged expansion strategies, exhibiting strong market performance and growth potential. Acquirers with higher profitability and substantial institutional ownership are more likely to pursue takeovers. In the post-M&A phase, larger acquirers with higher dividend payouts, robust profitability, conservative management, and operational efficiency tend to achieve superior long-term returns. However, higher asset turnover and horizontal M&As negatively affect M&A pursuits and long-term acquirer performance.

Moreover, our analysis indicates that cross-border acquirers often have lower institutional shareholder holdings, suggesting resistance to M&As by firms with higher institutional ownership or block holders. Increased aggregate institutional ownership enhances post-acquisition performance, underscoring the benefits of institutional monitoring. Conversely, a high concentration of institutional block holders negatively impacts acquirer returns, implying that excessive control by a few large entities may hinder value creation and long-term performance.

This study contributes to the literature by exploring the motivations behind cross-border M&As, examining how operational metrics change post-transaction, and assessing the linkages between M&A drivers and long-term stock and operating performance.

The remainder of this study is structured as follows: Section 2 reviews related literature and identifies critical factors influencing synergies in cross-border M&As. Section 3 outlines the empirical data and methodology. Section 4 presents the empirical findings, and Section 5 concludes the study.

Literature Review and Hypothesis Development

Firm Characteristics and the Resource-Based View

The resource-based view (RBV) of the firm suggests that companies engage in mergers and acquisitions (M&As) to access valuable resources and capabilities that can provide competitive advantages (Barney, 1991). Cross-border M&As allow firms to diversify their operations internationally and exploit firm-specific assets across different markets (Errunza & Senbet, 1984). Furthermore, the preparation phase, which includes financial restructuring and rigorous valuation of target firms through methods such as discounted cash flow analysis and market capitalization, is pivotal for ensuring the strategic fit and accurate pricing of these transactions (DePamphilis, 2019). The transaction cost theory also supports cross-border M&As as a way for multinational enterprises to internalize cross-border intermediate product markets and reduce transaction costs (Buckley & Casson, 1976).

Firm characteristics like size, valuation ratios, and capital structure influence a company’s ability to successfully acquire and integrate resources through M&As based on the RBV (Wernerfelt, 1984). Larger acquiring firms tend to have more slack resources to leverage for international expansion (Penrose, 1959). Based on asset advantages, they are more motivated to engage in cross-border M&As, as they have organizational resources and capabilities that multinational enterprises can transfer (Lee & Rugman, 2012), deploy, and exploit to achieve competitive advantage in foreign markets (Basuil & Datta, 2019; Rugman & Verbeke, 2002). While small firms can engage in takeovers, they often face unique challenges and limitations compared to giant corporations with more substantial resources.

Regarding capital structure, some researchers find that firms with low debt levels are more motivated to engage in cross-border M&As due to their financial flexibility (Moeller & Schlingemann, 2005; Tao et al., 2017). In contrast, others propose that highly leveraged firms may be motivated to reduce debt through successful international acquisitions (Opler et al., 1999), subject to financial constraints in acquiring (Maloney et al., 1993).

Concerning the book-to-market ratio, some research indicates that firms with a higher book-to-market ratio, signaling potentially undervalued assets (Lang et al., 1989), are more motivated to seek undervalued assets through cross-border M&As (Agrawal et al., 1992; Aktas et al., 2011). Others argue that these firms may also face higher risks associated with such investments (Chatterjee, 2009).

For dividend policies, acquirers with significant growth opportunities may be motivated to pursue M&A transactions, maintain lower dividend payouts, and retain cash flow for investment (Dittmar & Dittmar, 2008; W. Li & Lie, 2006). Besides, financially constrained acquirers may be less inclined to pay high dividends, preserving cash for potential acquisitions (Almeida et al., 2004; Custódio & Metzger, 2014). Conversely, acquirers may increase dividends before or after an acquisition to signal their stock is overvalued, making stock-based acquisitions more attractive (Brav et al., 2005).

Drawing from previous theories, we suggest a new hypothesis regarding certain firm traits and their unclear influence on the drivers and outcomes of international M&A deals.

Hypothesis 1a: Acquiring firms’ sizes, book-to-market ratios, capital structures, and specific dividend policies significantly influence their motivation to engage in cross-border mergers and acquisitions.

Building on Hypothesis 1a, these characteristics based on the RBV determine whether acquirers can successfully integrate and leverage acquired resources post-merger for improved long-term performance. We investigate the impact of operational improvements concerning M&A motivations on the acquiring firm’s long-term performance.

Regarding firm size, larger acquiring firms often have the resources and capabilities to manage complex international transactions effectively and may benefit from economies of scale and scope. Consequently, these firms are generally better equipped to extract synergies based on RBV and create value in the long run through cross-border M&As (Barney, 1991; Gregory & McCorriston, 2005). Chi (1994) explores the theoretical connections between the RBV and Transaction Cost Economics (TCE), demonstrating that the attributes enabling an asset to form the foundation of a firm’s sustainable competitive advantage also likely increase the costs associated with trading the asset or its services in the market. Small acquirers exceed the performance of large acquirers over the sample period; however, large acquirers seem to perform relatively better during financial crises.

The book-to-market ratio, indicating the undervaluation or overvaluation of a firm’s stock, is another focal point in M&A research. Studies have explored how firms with higher book-to-market ratios, reflecting undervaluation (Lang et al., 1989), are likely motivated to engage in cross-border M&As to acquire assets. However, the relationship between this characteristic and long-term M&A performance is mixed, with some studies indicating positive effects while others suggest potential risks associated with such acquisitions (Booth et al., 2001).

The acquiring firms’ capital structure, the debt-equity mix, is critical in understanding long-term M&A performance. Tao et al. (2017) show that acquirers use M&As to reduce deviations from the optimal debt level before deals. Firms with lower debt levels may have greater financial flexibility to manage cross-border M&As successfully. In contrast, highly leveraged firms may engage in such transactions to improve their financial position, diversify risks, or enhance long-term profitability.

The signaling effect presents a mixed phenomenon regarding dividends. Firms that maintain or increase dividends after a merger can signal their confidence in the combined entity’s future cash flows and profitability, positively impacting investor perceptions and stock prices. Conversely, dividend cuts may be seen as a negative signal (Andres et al., 2009). Based on the literature review, we formulate the following hypothesis.

Hypothesis 1b: Acquiring firms with larger sizes, higher book-to-market ratios, lower debt levels, and specific dividend policies are more likely to achieve synergies and exhibit improved long-term performance in cross-border mergers and acquisitions.

Operational Performance, Resource-Based View, and Industrial Organization Economics

We investigate the motivations behind M&As for foreign targets and further understand the acquirer’s concern about target firms’ characteristics at the initial stage of the M&A process. Weber (1996), Larsson and Finkelstein (1999), and Zollo and Meier (2008) show that integration of the decision-making process after M&As can help transfer acquirers’ capabilities, cut costs, and achieve synergy. Additionally, the integration can be beneficial in managing functions such as marketing, inventory, and others. Regarding capital expenditure, studies show that firms with substantial capital expenditure budgets are motivated to engage in cross-border M&As to access technology (Aktas et al., 2011). Still, other research suggests that firms with lower capital expenditures may also be motivated by the need to gain technological advantages (Collins et al., 2009).

Acquirers likely pursue international acquisitions to access complementary resources and capabilities to improve operational metrics like profitability, asset efficiency, margins, and costs (Barney, 1991). Therefore, we construct the following hypothesis.

Hypothesis 2a: Acquiring firms’ return on assets, total assets turnover, profit margin, cost of goods sold, and capital expenditure significantly impact the motivation for cross-border M&As.

Whether the acquirers can manage the post-M&A integration process would affect the realization of synergies (Haspeslagh & Jemison, 1991; Jemison & Sitkin, 1986). Therefore, the appropriate integration approach should consider the types of synergy and implementation problems due to different firm characteristics. There are many possible changes in operations after acquisitions, and we expect that at least three changes could have a significant impact on the acquirer’s long-term performance: (1) profit margin, (2) capital expenditures, and (3) costs of goods sold. Changes in these variables may indicate that acquirers improve operations by reducing costs, increasing production capacity, using new or complementary techniques, and increasing market shares after M&As. Therefore, another issue in this paper is how these changes affect post-M&A performance. This line of reasoning sets the stage for examining the role of operational synergies in shaping post-M&A performance.

If acquirers successfully leverage synergies from the deal, this should translate into enhanced operational performance and market valuations over the long run based on the RBV. Based on the existing evidence, we construct the hypothesis below.

Hypothesis 2b: When acquiring firms realize operational synergies after M&As, this should be reflected in long-term market performance improvements like increased profit margins, reduced capital expenditures, or lower costs of goods sold.

Horizontal M&As are often driven by the pursuit of synergies, such as cost savings through economies of scale, increased market power, and reduced competition. Research suggests that horizontal M&As tend to perform better in profitability and operational efficiency due to the potential for cost savings and market power gains (Devos et al., 2009; Hoberg & Phillips, 2010). However, increased regulatory scrutiny and antitrust concerns may offset the potential for improved profitability, which can lead to divestitures or blocked deals (Aktas et al., 2011).

As mentioned above, the resource-based view (RBV) of the firm suggests that companies engage in mergers and acquisitions (M&As) to access valuable resources and capabilities that can provide competitive advantages (Barney, 1991). Acquirers that target firms in the same industry, in horizontal M&As, typically aim to access crucial resources for industry-wide competitive advantage and firm profitability. Haleblian et al. (2009) find that horizontal M&As would change the competitive environment for surviving firms in that industry. For example, acquiring firms can create more value by reducing price competition in inputs and/or outputs. Additionally, Berger et al. (1998) show that the reduction of commitment from newly created firms to customers might impact firms’ profitability after M&A activity. These findings on horizontal M&As imply that non-horizontal M&As would perform poorer than horizontal M&As (Healy et al., 1992; Jensen, 1986).

In contrast, Kruse et al. (2007) find opposite results: non-horizontal M&As perform better after the events. Overall, horizontal and non-horizontal M&As differ in their potential for synergies based on factors like economies of scale/scope, market power effects, and resource complementarities (Hitt et al., 2001). Specifically, the industrial organization economics view suggests horizontal M&As creating market power and rationalization benefits give more opportunities for synergistic gains versus diversifying non-horizontal M&As. However, Matsusaka (1993) documents that non-horizontal M&As can create value through improved resource allocation and new growth opportunities, implying that acquirer shareholders benefit from diversification acquisitions. The author infers managerial objectives did not drive diversification.

Therefore, we take the type of M&A, whether horizontal or non-horizontal, into account in the analysis. Based on the existing evidence, we construct the following hypothesis.

Hypothesis 2c: Due to potential economies of scale/scope, horizontal M&As should perform better than non-horizontal M&As in the long run.

Corporate Governance and Agency Theory Perspective

The decision to extend a firm’s operations to foreign countries through cross-border M&As is a critical issue for a board of directors. Theoretically, cross-border M&As can be driven by the desire for diversification. Adler and Dumas (1975) and Errunza and Senbet (1984) clearly state in their theoretical models that corporations can diversify internationally due to imperfections in the capital market. The mechanism of corporate governance may be another factor that causes cross-border M&As, especially the role of institutional investors. Erel et al. (2012) argue that governance-related differences across countries can motivate M&As if the combined firm has better protection for target-firm shareholders due to higher governance standards in the country of the acquirer.

Corporate governance should have a substantial influence on M&As. Many variables can proxy for a firm’s corporate governance, and institutional ownership is crucial. In cross-border cases, foreign institutional investors also play a role in prompting changes in corporate governance practices, as do domestic institutional investors (Ferreira et al., 2010; Ferreira & Matos, 2008). Andriosopoulos and Yang (2015) find that institutional investors increase the likelihood of M&As. Additionally, institutional ownership concentration and foreign institutional ownership increase the likelihood of cross-border M&As. From an agency theory perspective, institutional investors and block holders have incentives and the ability to monitor management (Shleifer & Vishny, 1986). Their influence may encourage cross-border M&As to diversify risks and create shareholder value. Their investment horizons may influence short- and long-term acquisition preferences (Chen et al., 2007). Therefore, we analyze the impact of institutional ownership on M&As and construct the following hypothesis.

Hypothesis 3a: Higher institutional ownership or the presence of block holders in the acquiring firm increases the motivation for cross-border M&As.

Several studies have investigated the relationship between institutional ownership, the presence of block holders, and the long-term performance of acquiring firms after cross-border mergers and acquisitions (M&As). The hypothesis suggests that higher institutional ownership or the presence of block holders in the acquiring firm is associated with improved long-term performance following cross-border M&A transactions.

Chen et al. (2007) show that institutional investors with long-term investments who are active investors will commit to monitoring firm governance and managerial decision-making. Their presence can encourage the firm to adopt strategies and make decisions that enhance long-term shareholder value rather than focusing solely on short-term gains (Cronqvist & Fahlenbrach, 2009). Andriosopoulos and Yang (2015) show that across all three types of institutional investors, categorized by their holding periods; there exists a negative relationship between the holding horizon and the likelihood of cross-border M&As. The authors also find evidence that institutional investors with medium- and long-term investment horizons are more actively involved in a firm’s decision-making to avoid reducing the value of their investments. Based on the information advantage and the role in the active corporate governance mechanism, we expect that institutional ownership should affect the acquirers’ long-term performance after M&As.

Building on Hypothesis 3a, the monitoring role of institutional investors/block holders (Shleifer & Vishny, 1986) should also increase value creation from M&As over the long run by reducing agency costs. Similarly, block holders, defined as investors holding a substantial percentage of a company’s outstanding shares, can also contribute to improved long-term performance after cross-border M&As. Block holders have a significant ownership stake in the firm, which gives them a solid incentive to actively monitor and influence the firm’s strategic decisions, including cross-border M&A transactions (Edmans, 2014; Shleifer & Vishny, 1986).

Their involvement can help mitigate agency problems and ensure cross-border M&As are undertaken to maximize long-term shareholder value (Chen et al., 2007; Cronqvist & Fahlenbrach, 2009). Additionally, block holders may possess industry-specific knowledge and expertise, which can contribute to the successful integration and performance of the combined entity after the cross-border M&A (Bena et al., 2017). Therefore, we construct the following hypothesis.

Hypothesis 3b: Higher institutional ownership or the presence of block holders in the acquiring firm leads to improved long-term performance after cross-border M&As.

This study underscores the importance of rigorous financial evaluations during the preparation phase of M&A deals. While the study emphasizes the assessment of pre-merger financial conditions, it does not explicitly evaluate specific valuation processes, such as discounted cash flow analysis or market capitalization methods. Instead, it focuses on how preparatory financial assessments contribute to understanding the broader determinants of successful cross-border M&As and achieving long-term operational synergies.

Data and Methodology

Data Screening

Transaction data from the Thomson Reuters SDC Worldwide Mergers and Acquisitions database covers cross-border acquisitions from 1990 to 2014. Data screening criteria include:

(1) Acquirers are common stocks of firms listed on NYSE, AMEX, and NASDAQ, excluding ADRs, REITs, closed-end funds, and partnerships.

(2) Deals are completed mergers, exchange offers, and majority interest acquisitions.

(3) Financial (SIC 60–69) and utility (SIC 49) industries are excluded due to regulatory restrictions and distinct accounting practices.

(4) Cases of multiple M&As within 3 years are excluded to avoid statistical dependence and potential bias from high-growth or financial distress firms.

Daily returns, market indices, shares outstanding, and firm capitalization are from CRSP. Accounting data (sales, costs, R&D, advertising, income, expenditures, assets, debt, and equity) is from Compustat.

A propensity score matching method (X. Li & Zhao, 2006) is employed to construct the matching sample, using a logistic model with the dependent dummy set to 1 for cross-border acquirers and 0 for non-M&A firms with the same 2-digit SIC code. Independent variables include firm size, book-to-market ratio, and 6-month pre-announcement cumulative excess returns. The propensity score model is estimated annually, and each non-M&A firm with the closest score to a cross-border acquirer is included.

Sample Summary and Characteristics

We first provide the summary statistics of the number of US firms that completed cross-border M&As during the period from 1990 to 2014 in Table 1. Horizontal M&As are deals where the acquiring and target firms have the same 3-digit SIC codes.

Number of Samples.

Note. This table presents data on cross-border M&A occurrences in the United States from 1990 to 2014. For each M&A, the samples are categorized into horizontal and non-horizontal transactions within 2-year intervals.

Table 1 illustrates that 1,066 US companies conducted cross-border M&As between 1990 and 2014, with a peak in activity observed from 1996 to 2001. Although horizontal M&As outnumbered non-horizontal ones, the distinction is not readily apparent.

Next, we summarize statistics of variables for sample firms in Table 2, including mean, median, standard deviation, 10th and 90th percentiles, and first and third quartiles. The variables can be classified into firm characteristics, operational efficiency, and corporate governance. The firm characteristics include firm size (SIZE), denoting the natural log of the firm’s market capitalization, book-to-market ratio (BM), debt ratio (DR), and payout ratio (PR). The measures of operational efficiency are return on total assets (ROA), total assets turnover (TOT), profit margin (PM), cost of goods sold (COGS) scaled by sales, and capital expenditure (CAPX) scaled by sales. As to corporate governance, we include various characteristics of institutional holdings, such as institutional holding percentage (H_PERCT) denoting institutional holdings divided by total outstanding shares, institutional holding competition (H_HHI), top 10 institutional holdings density (TOP10), and top 10 institutional holding percentage (TOP10_PERCT). Institutional holding competition (H_HHI) is measured by the Herfindahl-Hirschman Index (HHI). It is the sum of the squares of the percentage of institutional holdings concerning outstanding shares. The value of the HHI ranges from zero to one. A higher HHI indicates a lower level of holding competition and vice versa. The density of the top 10 institutional holdings (TOP10) stands for the top 10 institutional holdings divided by total institutional holdings. The top 10 institutional holding percentage (TOP10_PERCT) presents the top 10 institutional holdings divided by total outstanding shares.

Acquirers’ Characteristics.

Note. This table summarizes the basic statistics of all empirical variables for the analyses in this paper. The firm characteristics include SIZE, BM, DR, and PR. The operational efficiency measures are ROA, TOT, PM, COGS, and CAPX. Corporate governance includes H_PERCT, H_HHI, TOP10, and TOP10_PERCT.

From Table 2, we find that the acquirers of cross-border M&As typically have BM far less than one, both in mean and median. This implies at least two empirical results of the acquirers’ characteristics—first, the acquirers have better-than-average market performance. Second, the acquiring firms have substantial growth opportunities. Both explanations are consistent with the market observations. Because cross-border M&As are riskier and need more resources, the acquirers with better market performance and growth opportunities can merge or acquire foreign targets.

Moreover, we find that the 90th percentile of DR is 46.6%, which implies that firms with high leverage tend to pursue riskier investment projects, which are cross-border M&As, in this paper. This observation is consistent with the existing evidence. Therefore, the acquirers have similar appetites for risk in their investment and financial decisions. In sum, we find that firms tend to have better operational performance and pay out less when they plan to acquire foreign targets. This result is consistent with the empirical observation that cross-border M&As are riskier and require more resources on M&As.

Finally, institutional ownership plays a vital role in corporate governance. Therefore, we expect institutional ownership to substantially impact the motivation of M&As and the long-term performance after M&As. We also summarize statistics of institutional holdings of cross-border acquirers. First, the statistics show that the mean of H_PERCT and H_HHI are 0.328 and 0.174. Suppose a lower H_PERCT and a higher H_HHI exist than other firms. In that case, it indicates that the institutional investors of cross-border acquirers are in a less competitive environment, and we may imply that institutional investors of cross-border acquirers have a relatively weak institutional monitoring function than other firms.

Furthermore, from Table 2, TOP10 and TOP10_PERCT have a mean of 0.767 and 0.224. Suppose a higher TOP10 and a lower TOP10_PERCT exist. In that case, we expect that the top 10 institutional investors have a more significant impact on institutional ownership but a lower impact on the shareholders’ ownership in cross-border acquiring firms than in other firms. This expectation implies that cross-border M&As would be more likely to be accepted by the board of directors when most top 10 institutional investors agree on the deals. This observation offers a specific viewpoint to the related literature.

Extending market share is one of many strategic reasons for a company to initiate cross-border M&As. In order to understand the attributes of a company pursuing cross-border M&As, we separate horizontal M&As from non-horizontal M&As in the cross-border samples and summarize the firm characteristics in Table 3.

Summary Statistics with Respect to the Type of Cross-Border M&As.

Note. This table summarizes statistics of types of cross-border M&As. The Firm characteristics include SIZE, BM, DR, and PR. The operational efficiency measures are ROA, TOT, PM, COGS, and CAPX. Corporate governance includes H_PERCT, H_HHI, TOP10, and TOP10_PERCT.

Panels A and B in Table 3 show that the capital structure differs slightly between horizontal and non-horizontal M&As. In cross-border M&As, the DR of non-horizontal acquirers is 20.9% in the mean and 17.0% in the median. The horizontal acquirers, however, have a lower DR, 18.4% in the mean and 12.9% in the median. The non-horizontal acquiring firms have a higher leverage than the horizontal acquirers. In addition, TOT is also high in non-horizontal M&As, which implies that the non-horizontal acquirers utilize their assets more efficiently than their horizontal counterparts in cross-border M&As. As to other characteristics, such as SIZE, BM, and H_PERCT, horizontal and non-horizontal acquirers have no substantial differences. Therefore, we expect that the types of M&As may not play a vital role in cross-border M&As.

Correlation Matrix

The correlation between any two factors is essential, and we have to check it before the regression analysis for two reasons. First, we would like to find out how these factors are related to the correlation matrix. The simple correlation coefficient provides valuable information about the relationship between any two variables. Second, we eliminate the multicollinearity problem in the regression analysis by avoiding adding the variables with high correlation in the same regression. The correlation matrix can help us make a judgment in this matter. Next, we summarize the correlation matrix of empirical variables used in Table 4.

Correlation Matrix for Cross-Border M&As.

Note. This table summarizes the coefficient of correlation for all variables in the cross-border empirical model. The firm characteristics include SIZE, BM, DR, and PR. The operational efficiency measures are ROA, TOT, PM, COGS, and CAPX. Corporate governance includes H_PERCT, H_HHI, TOP10, and TOP10_PERCT. Superscripts *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

From Table 4, we focus on the cases where the correlation coefficient is greater than .4. First, we find that BM positively correlates with ROA with a coefficient of .44. This evidence implies that value firms have a greater ROA, which is consistent with the concept of value investment. In contrast, the growth firms with lower BM have relatively poor operational performance. Second, the results show that cross-border acquiring firms with a higher CAPX or COGS have poor profitability. The coefficients are very close to −1, which is perfectly negatively correlated. Therefore, these firms invest more when their earnings are relatively low.

Third, the correlation between H_HHI and SIZE is −.55, significantly different from zero. The evidence shows that institutional investors are more competitive when the firm is big. Regular institutional investors hold a large portion of a firm’s stock, especially when it is significant. In addition, H_HHI has a correlation of −.47 with H_PERCT. This result is also consistent with empirical practice that institutional investors are more dispersed when the institutional ownership is a significant portion of shareholdings. The greater the number of institutional investors, the more competitive the environment in a firm would be.

Finally, looking into the details of institutional ownership, we find that the top 10 institutional investors play an essential role in corporate governance. Many of them are block holders who own more than 5% of a firm’s outstanding shares. When institutional ownership is high in a firm, the institutional holding competition is low. The coefficient between H_PERCT and TOP10 is −0.63. However, H_HHI has a positive coefficient of 0.65 with TOP10. This result implies that the competitiveness would be lower if the top 10 institutional investors are the majority of institutional holdings, and it is also consistent with the general intuition. We find reverse correlation results between H_HHI and TOP10_PERCT, with a negative coefficient of −.40. The coefficient of correlation between H_PERCT and TOP10_PERCT is .93.

Variable Measures

This subsection discusses the three sets of variables used in the tests, including performance measures, a proxy of corporate governance, and acquirers’ operational ratios and characteristics.

Acquirers’ Changes in Operations

There are three changes in operational efficiency: profit margin (CHG_PM), capital expenditures (CHG_CAPX), and cost of goods sold (COGS), which are scaled by sales. We denote a variable as Xk and calculate its changes as follows:

where ΔXk represents the kth variable’s difference between the post- and pre-M&As operating performance, and t is the year relative to the announcement of M&As. We discuss the possible impacts of the three variables on acquirers’ long-run performance as follows.

(1) The profit margin, an accounting performance measure indicating profitability, is expected to impact market value if improved after M&As due to investor appreciation.

(2) US domestic acquirers can enhance performance by reducing excess capacity and capital investment (Devos et al., 2009; Maksimovic et al., 2011). However, M&As played a contractionary role in the 1970s to 80s due to excess capacity but an expansionary role in the 1990s with peak utilization (Andrade & Stafford, 2004). Thus, firms can improve operations by adjusting capital expenditures post-cross-border M&A.

(3) M&As realize economies of scale by lowering average fixed, production, and material costs, more pronounced for cross-border deals if target country costs are substantially lower. Moving production/operations to foreign targets additionally saves trade costs like transportation, tariffs, and border-related expenses. Consequently, acquirers’ post-M&A average cost of goods sold should decrease, boosting profitability.

Acquisition Characteristics

Horizontal M&As are transactions in which the acquirer and the target have the same 3-digit SIC code. This variable captures the effect that business-related M&As are more likely to create synergy than unrelated M&As. In addition, studies show that private target M&As perform better than those of public targets due to the transfer of new block holders (Harford et al., 2012) and a low likelihood of overpayment (Fuller et al., 2002). We construct a public dummy if the target is listed on a foreign stock exchange.

Other Factors

We use the acquirer’s characteristics as control variables: SIZE, BM, hi-tech industries, and industry competition. A hi-tech acquirer is identified by the 3-digit SIC codes of technological industries reported by the US Department of Commerce (28 industries) for M&As in the 1990s and by Kile and Phillips (2009) categories (11 hi-tech industries) for M&As in the 2000s.

The level of an industry’s competition is measured by the Herfindahl-Hirschman Index (HHI). We use Fama and French (1997) categories of 49 sectors to classify industries and calculate an industry’s HHI as follows:

where wj,y is the firm j’s market share in year y, defined as its sales divided by the total sales of the industry that it operates in (wj,y = Salesj,y/Salesj,y), and n is the number of firms in the industry. We assume that the higher an industry’s HHI, the lower its product competition in the market.

Long-Run Performance Measures

We use both buy-and-hold abnormal returns (BHARs) and the Fama and French (2016) model to evaluate a portfolio’s long-run performance. Three-year BHAR of a portfolio (BHARp) is calculated as follows:

where Rj, t, and Rmatching, t denote firm j’s return and its matching firm’s return on the day

Empirical Models

We further construct the empirical models based on the summary statistics results in Tables 2 to 4. The following equations state that the empirical models control firm characteristics, operational performance, and institutional ownership, such as SIZE, BM, PM, and other variables. In addition, we also control for yearly and industrial dummies, and these dummy variables control for differences among the years and industries. Three empirical models in this paper test different research questions.

We employ a logistic regression model (Equation 4) to assess the motivation of cross-border mergers and acquisitions (M&As). For Hypothesis 1a, which relates to acquiring firms’ characteristics, we include specific firm characteristics as independent variables in our model to determine their impact on M&A motivation. Similarly, Hypothesis 2a, concerning operational performance, is tested by incorporating operational metrics into our model. Hypothesis 3a, which addresses institutional investors, is explored by including relevant ownership variables in our regression. This approach allows us to empirically validate or refute our hypotheses, providing valuable insights into the factors driving cross-border M&A motivation while maintaining clarity and transparency in our research. The logistic regression model is as follows:

where the variables of the firm’s characteristics in Equation 4 are BM, DR, and PR, and the measures of operational efficiency are ROA, TOT, PM, COGS, and CAPX. As to corporate governance, we include the characteristics of institutional holdings, such as H_PERCT and H_HHI. The dependent variable yi,t = 1 for cross-border M&As, 0 for matching firms of corresponding M&As.

We employ regression analysis (Equations 5 and 6) using 3-year buy-and-hold raw returns (BHRs) and buy-and-hold abnormal returns (BHARs) to assess the long-term performance of cross-border M&As. Each acquirer is matched with a non-M&A firm with the highest propensity matching score (X. Li & Zhao, 2006) and operates in the same industry (2-digit SIC code) as the acquirer. BHAR is the difference in raw returns between acquirers and their matching firms. Specifically, we test Hypothesis 1b to examine the impact of acquiring firms’ characteristics on the post-M&A performance. Hypothesis 2b explores the relationship between operational performance, synergy realization, and long-term market performance. Lastly, Hypothesis 3b and 2c investigate the influence of institutional investors on the post-M&A long-term outcomes. By conducting these regression tests and incorporating relevant variables, we seek to empirically validate or refute our hypotheses and provide valuable insights into the connection between M&A motivations and post-M&A performance.

Horizontal M&As are deals where the acquirer and the target have the same 3-digit SIC code. The public indicates that the target firm is listed on a foreign stock exchange. We categorize the sample firms into two groups based on the shifts in their cost of goods sold, capital expenditures, and R&D expenses relative to sales after completing cross-border mergers and acquisitions (M&As). This classification scrutinizes the influence of such financial and operational variations on the motivation for M&As and their subsequent long-term performance. By comparing firms that undergo substantial changes in these metrics with those that do not, we gain valuable insights into the connection between post-M&A operational shifts and the overall success of these acquisitions.

This regression uses 3-year BHARs as the dependent variable and includes the yearly and industrial effects. The empirical model is as follows.

where the variables of the firm’s characteristics in Equation 5 are SIZE, BM, DR, and PR, and the operational efficiency measures are ROA, TOT, PM, CHG_PM, COGS, CHG_COGS, CAPX, and CHG_CAPX. As to corporate governance, we include the characteristics of institutional holdings, such as H_PERCT, CHG_PERCT, H_HHI, and CHG_HHI. Furthermore, we add BLOCK to the regression model to test its impact on BHARs. To further analyze the impact of corporate governance from institutional ownership, we set up the empirical model as follows:

where the additional variables in Equation 6 relative to Equation 5 are TOP10, TOP10_PERCT, and BLOCK.

Based on the empirical results, we can find which factors have more substantial predictive power for the long-term impact of cross-border M&As initiated by US firms on their long-term stock return and explore possible synergy sources.

Empirical Results

This section has two major parts: univariate analysis and regression analysis. First, we check the long-term market performance, measured by 3-year BHARs, of cross-border M&As concerning the changes in operational performance, which include profit margin, capital expenditure, and cost of goods sold. Next, we conduct the multivariate analysis by running the regression of long-term market performance.

Univariate Result

We analyze the motivation for cross-border M&As, a vital feasibility study done before conducting M&As. The long-term performance after M&As is another critical issue in this paper. First, we use the 3-year buy-and-hold returns to test the difference between acquiring firms and their matching firms. Second, we utilize the BHARs to conduct the regression analysis in the next section. For the univariate analysis, we summarize the buy-and-hold returns for cross-border acquiring firms and their matching firms in Table 5.

Summary Statistics of Performance After Cross-Border M&As.

Note. This table reports cross-border acquirers’ 3-year BHARs. The matching firms are selected by propensity scores from X. Li & Zhao (2006) using the criteria of SIZE and BM. The table has three classification factors scaled by sales: PM, CAPX, and COGS. The median of each variable separates the high and low subsamples.

We use three essential factors, PM, CAPX, and COGS, to separate the samples into low and high groups. First, our study builds upon previous research (Larsson & Finkelstein, 1999; Weber, 1996; Zollo & Meier, 2008), emphasizing integration’s importance in post-M&A decision-making. These studies highlighted the benefits of integration, including capability transfer, cost reduction, synergy, and improved function management. Our findings complement this prior research by focusing on Profit Margin (PM) and its impact on acquiring firms’ post-M&A performance, specifically 3-year buy-and-hold returns (BHRs) and buy-and-hold abnormal returns (BHARs). Our results support hypothesis 2b, highlighting that better profitability is essential for creating value in M&A transactions, affirming the value of integration, and profit margin improvement in creating firm value.

Second, capital expenditure might deteriorate the acquiring firms’ long-term performance, corroborating the findings of previous research (Aktas et al., 2011; Collins et al., 2009). Table 6 shows that the mean and median of BHARs are 16.3% and 16.0%, respectively, in the group with low CAPX, which is considerably higher than those with high CAPX. We expect that increasing capital expenditure after M&As may not be a good time for investment. Due to scarce resources and management capability, acquiring firms should have conservative investments after M&As to increase firm value from synergy instead of other investments in capital expenditures (Aktas et al., 2011). Our findings also substantiate that firms with lower capital expenditures may be motivated by the need for technological advantages (Collins et al., 2009). Therefore, we observe alignment with our hypothesis 2.2 that acquiring firms with low CAPX have better BHARs than those with high CAPX.

The Motivation Factors on Cross-Border M&As.

Note. This table reports how the motivation factors affect cross-border M&As. We classify these factors into three categories: (1) company characteristics, including BM, DR, and PR; (2) operational efficiencies, including ROA, TOT, PM, CAPX, and COGS; and (3) corporate governance, including H_PERCT and H_HHI. Numbers in parentheses are p-values. Superscripts *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Finally, from the point of view of the cost of goods sold, we find that firms with low COGS have better BHRs and BHARs than those with high COGS, aligning with our hypothesis 2b. Part of the reason for this result is consistent with what we addressed in profit margin. The gross profit margin is the sales minus the cost of goods sold. Therefore, a high cost of goods sold implies low gross and net profit margins if other revenues and expenses remain constant. We analyze the cost of goods sold because of the economies of scale. If cross-border M&As are horizontal and the market share increases after M&As, then the cost of goods sold should decrease substantially. Eventually, the acquiring firms can improve their performance through the effect of the economies of scale. Indeed, we find that the result is sound in our sample.

Motivation of M&As

To analyze whether the factors significantly impact the motivation of cross-border M&As, we regress the cross-border M&As on three sets of factors, including acquiring firms’ characteristics, operational performance, and corporate governance. The factors of acquiring a firm’s characteristics include SIZE, BM, DR, and PR. The factors of operational efficiencies include ROA, TOT, PM, CHG_PM, COGS, CHG_COGS, CAPX, and CHG_CAPX. Corporate governance factors include H_PERCT, CHG_PERCT, H_HHI, CHG_HHI, TOP10, and TOP10_PERCT.

From Table 6, we uncover significant insights regarding the impact of acquiring firms’ characteristics on the motivation behind cross-border M&As using the regression Equation 4. We consider previous research that has yielded mixed findings regarding the relationship between the book-to-market (BM) ratios and cross-border M&A motivation. Aktas et al. (2011) and Agrawal et al. (1992) suggest that firms with higher BM ratios are more motivated for cross-border M&As, while Chatterjee (2009) argues that these firms face higher risks. Our findings offer a unique perspective by empirically examining this relationship. Contrary to some previous expectations, our results consistently show that lower BM ratios have a negative and statistically significant impact on cross-border M&A motivation. The coefficients (−0.114, −0.107, −0.109, −0.109, −0.114, and −0.105 in models 1–6) suggest that firms with lower BM ratios tend to engage more aggressively in cross-border M&As, aligning with our hypothesis 1a.

The non-consistency between our findings and some previous research implies that the BM ratio’s influence on cross-border M&A motivation is more nuanced and context-dependent than previously thought. Firms should consider the specific characteristics of their BM ratios and strategic objectives when assessing cross-border acquisitions, acknowledging potential variations in motivations. This nuanced perspective can help firms make more informed decisions and manage associated risks effectively in their cross-border M&A activities.

Furthermore, we also find that the debt ratio (DR) exhibits a significantly positive impact on the motivation of cross-border M&As (coefficients are 1.178, 1.042, 1.253, 1.047, 1.029, and 0.810 in models 1–6). This result suggests that firms with higher DR are more inclined to pursue cross-border M&As through leveraging to enjoy the triumphant business return from the new market. This result aligns with our hypothesis 1a, that specific capital structures influence motivation for cross-border M&As. Dividend, in contrast to future growth, is the reward of historical operation, especially for the previous year’s dividend payout. The empirical result shows that the payout ratio (PR) has a consistently negative and statistically significant impact on M&A motivation (coefficients are −0.008, −0.008, −0.008, −0.008, −0.008, and −0.010 in models 1–6). This result aligns with our hypothesis 1a that acquiring firms with an aggressive expansion strategy may adopt low dividend payout policies to retain cash for potential M&As.

Regarding the empirical results from acquirers’ operational performance in Table 6, we find that the return on total assets (ROA) has a significantly positive impact on the motivation of cross-border M&As (coefficients are 0.959, 1.026, 0.995, 1.331, and 1.214 in models 1 and 3–6), affirming our hypothesis 2a that operational performance factors significantly influence motivation for cross-border M&As. With good trade records on operating capability and confidence in delivering higher asset returns, the companies with higher ROA are more likely to engage in cross-border M&As. Next, from the empirical result, we also find that the turnover on total assets (TOT) significantly negatively impacts the motivation of cross-border M&As (coefficients are −0.215, −0.396, and −0.526 in models 2, 5, and 6). This finding aligns with hypothesis 2a that certain operational factors, such as TOT, can deter firms from pursuing cross-border M&As. This result is straightforward from a management team’s perspective, as they do not have any incentive to expand business abroad through cross-border M&As to improve it, given that a satisfactory level of TOT has existed.

Concerning corporate governance, we find interestingly that both the percentage of holdings by institutional investors (H_PERCT; coefficients are −3.391, −3.281, −3.449, −3.428, −3.450, and −3.026 in models 1–6) and the Herfindahl-Hirschman Index (H_HHI; coefficients are −2.249, −2.555, −2.609, −2.504, −2.418, and −2.345 in models 1–6) show negatively significant effects on cross-border M&As. This finding supports our hypothesis 3a that companies with a higher H_PERCT and H_HHI tend to resist cross-border M&As more. We think institutional investors would prefer companies to stay and develop business in domestic markets, which is considered less risky than cross-border M&As.

Long-Term Performance After M&As

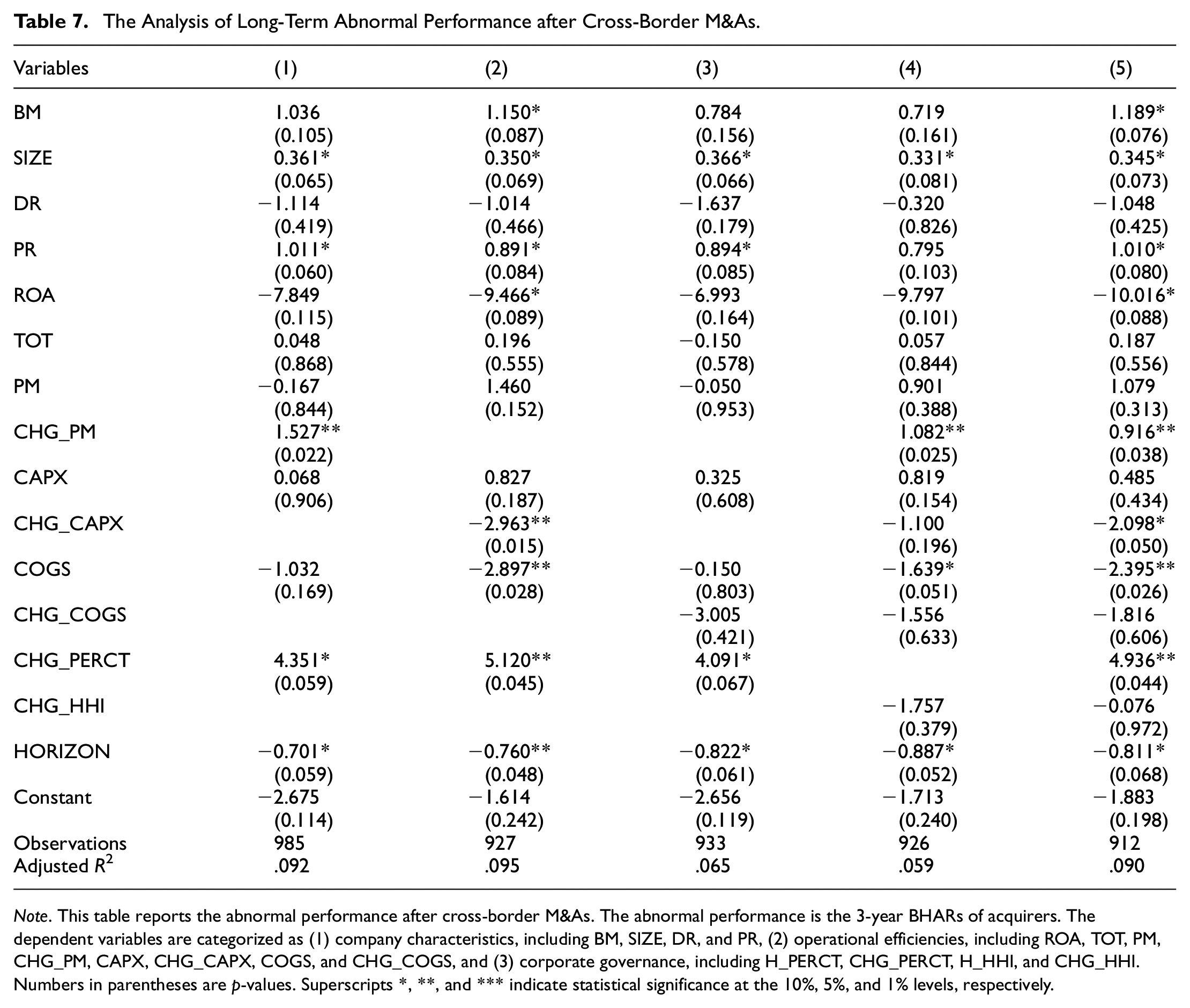

With the knowledge of the motivation of M&As from previous empirical results, we would like to analyze the long-term abnormal performance after cross-border M&As. From the empirical result in Table 7, running the regression Equation 5, we consider the size effect in cross-border M&As. Basuil and Datta (2019), Lee and Rugman (2012), and Rugman and Verbeke (2002) suggest that larger acquiring firms, with their substantial asset advantages, are more motivated for cross-border M&As due to their resources and capabilities that can be leveraged for competitive advantages in foreign markets.

The Analysis of Long-Term Abnormal Performance after Cross-Border M&As.

Note. This table reports the abnormal performance after cross-border M&As. The abnormal performance is the 3-year BHARs of acquirers. The dependent variables are categorized as (1) company characteristics, including BM, SIZE, DR, and PR, (2) operational efficiencies, including ROA, TOT, PM, CHG_PM, CAPX, CHG_CAPX, COGS, and CHG_COGS, and (3) corporate governance, including H_PERCT, CHG_PERCT, H_HHI, and CHG_HHI. Numbers in parentheses are p-values. Superscripts *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Our findings align with this perspective. We discover that the size of acquiring firms (SIZE) has a positively weak impact on buy-and-hold abnormal returns (coefficients are 0.361, 0.350, 0.366, 0.331, and 0.345 in models 1–5), indicating that larger firms tend to utilize their assets better and achieve anticipated synergy after an M&A, resulting in improved long-term performance. This supports our hypothesis 1b. This consistency underscores the significance of firm size in the success of cross-border M&As, highlighting that larger firms are well-equipped to harness the potential benefits of these transactions and enhance their long-term performance, which aligns with our expectations and previous research.

The payout ratio (PR) also shows a weak positive impact on acquiring firms’ BHARs (coefficients are 1.011, 0.891, 0.894, and 1.010 in models 1–3 and 5). This implies that higher PR attracts investors to buy its shares to enjoy the dividend, leading to positive long-term abnormal returns. Hence, our results support hypothesis 1b.

Regarding acquiring firms’ operational performance, we find the cost of goods sold (COGS; coefficient is −2.897, −1.639, and −2.395 in models 2, 4, and 5) and the change in capital expenditure (CHG_CAPX; coefficient is −2.963 and −2.098 in models 2 and 5) both have negatively significant associations with acquiring firms’ BHARs. These findings support hypothesis 2b, indicating that reducing COGS and capital expenditure after M&As can improve profitability and long-term abnormal performance. Furthermore, the change in profit margin (CHG_PM) is positively associated with acquiring firms’ BHARs (coefficient is 1.527, 1.082, and 0.916 in models 1, 4, and 5). This result aligns with the realization that operational synergies after M&As can positively impact long-term market performance. These findings are also consistent with the aforementioned univariate result. Therefore, our results are consistent with hypothesis 2b.

Regarding corporate governance, change in the percentage of institutional ownership (CHG_PERCT) is weakly positively associated with BHARs (coefficient is 4.351, 5.120, 4.091, and 4.963 in models 1, 2, 3, and 5). We believe that institutional investors are always more capable of sourcing potential investment targets in the market. The more significant the incremental percentage of institutional holding after M&As, the better long-term BHARs will be expected, supporting hypothesis 3b.

Concerning the factors regarding industries for the acquirers, the evidence shows HORIZON has a weak negative impact on acquiring firms’ BHARs (coefficients are −0.701, −0.760, −0.822, −0.887, and −0.811 in models 1–5). This finding indicates that acquirers do not enjoy preferential abnormal returns in cross-border M&As, even with business lines related to the target firms. It highlights the challenge of delivering synergy from such acquisitions, aligning with hypothesis 2c.

The Change of Institutional Ownership

While Table 7 provides a comprehensive analysis of abnormal returns following cross-border M&As, we further explore the role of corporate governance through the lens of institutional ownership. To reveal the relationship between acquirer performance and institutional ownership, we conduct multivariate regression analysis, running the regression Equation 6, and present the results in Table 8.

The Analysis of Long-Term Abnormal Performance concerning Institutional Holding after Cross-Border M&As.

Note. This table reports the abnormal performance after cross-border M&As with further consideration of institutional holding. The abnormal performance is the 3-year BHARs of acquiring firms. The dependent variables are defined in the same way as in previous tables. Numbers in parentheses are p-values. Superscripts *, **, and *** indicate statistical significance at the 10%, 5%, and 1% levels, respectively.

Corporate governance is recognized as a pivotal influence on the outcomes of international expansion via M&A (Andriosopoulos & Yang, 2015; Chen et al., 2007; Ferreira et al., 2010; Ferreira & Matos, 2008). However, limited research has examined how changes in ownership structure affect returns in this context. We address this gap by investigating the impact of shifting institutional ownership and concentration among the top 10 institutional owners on the long-term performance of cross-border acquiring firms.

We further analyze the performance of MB (market value/book value) and ROA after cross-border M&As and find that most of the results are consistent. From the results in Table 8, this study reveals nuanced effects. Increases in aggregate institutional ownership (CHG_PERCT) are positively associated with 3-year buy-and-hold abnormal returns (BHARs; coefficient is 4.431, 7.843, 6.033, and 5.055 in models 1–4), aligning with our hypothesis that greater institutional monitoring and expertise enhance performance. However, high concentration among the top 10 institutional owners (TOP10_PERCT) negatively relates to long-run BHARs (coefficient is −7.363 in model 2), suggesting excessive control by a few large institutions may impede value creation.

A higher increase of the largest block holders (over 5% ownership) also exhibits a negative relationship with BHARs (coefficient is −0.727 in model 3). This result implies that greater block holder ownership may deteriorate post-acquisition performance under certain conditions.

In summary, our findings provide novel evidence of the complex role of changing institutional ownership in shaping cross-border M&A outcomes. We highlight the influential yet contingent effects of shifts in ownership structure. These results carry important practical implications for optimizing governance decisions when expanding globally through acquisition.

Conclusions

This research has delved into the intricate world of mergers and acquisitions (M&As), focusing mainly on cross-border M&As within the United States between 1990 and 2014. Our study aimed to provide insights into two critical aspects of this corporate phenomenon: the motivations that drive acquirers to pursue cross-border M&As and the subsequent long-term market performance of these transactions. Throughout our investigation, we have uncovered valuable findings contributing to our understanding of the multifaceted dynamics of cross-border M&As.

Our analysis of the motivations behind cross-border M&As revealed several noteworthy patterns. First and foremost, we observed that firms with higher profitability and a penchant for conservative investments tend to achieve better long-term returns after such transactions. This finding suggests that strategic efforts to enhance profitability and operational efficiency post-M&A can result in favorable economies of scale. Furthermore, our study unearthed intriguing links between a firm’s balance sheet characteristics and its motivation for cross-border M&As. Lower book-to-market ratios were associated with a greater inclination toward aggressive cross-border M&As. In comparison, firms with higher debt ratios exhibited heightened confidence in leveraging for such transactions. We also explored the influence of dividend policy, finding that aggressive expansion strategies are often accompanied by lower dividend payouts to maintain ample cash reserves for potential M&A activities. Additionally, our analysis demonstrated that firms with a solid operational foundation characterized by higher returns on assets are more likely to embark on cross-border M&A journeys. In contrast, those with a high turnover on assets tend to show reduced motivation for such endeavors. Lastly, corporate governance emerged as a significant factor, with higher institutional ownership and a more concentrated ownership structure indicating resistance to cross-border M&As.

Transitioning to the examination of long-term market performance post-cross-border M&As, our findings further enriched our understanding. We observed that larger acquiring firms exhibit better long-term performance and realize more synergistic benefits following these transactions. Moreover, higher dividend payouts proved to be an attractive proposition for investors, positively impacting acquiring firms’ long-term performance. Operational factors also played a pivotal role, with reduced cost of goods sold and capital expenditure savings contributing to enhanced profitability and sustained post-M&A performance. The changes in profit margins also positively influence long-term performance. Corporate governance considerations remained relevant, with an increase in the percentage of institutional ownership following cross-border M&As being associated with improved long-term abnormal performance. In contrast, higher ownership concentration among the top 10 shareholders had a detrimental effect on long-term performance. Additionally, the type of M&A, differentiating between horizontal and non-horizontal transactions, yielded insights as horizontal cross-border M&As struggled to deliver expected synergies and preferred abnormal returns.

While our research has provided valuable insights, it is essential to acknowledge its limitations. We primarily focused on cross-border M&As within the US from 1990 to 2014, and market conditions may have evolved since then. Expanding the geographical scope and considering more recent data could yield broader insights. Future research opportunities lie in exploring the mechanisms through which firms realize synergy post-M&A and investigating industry-specific factors that influence the motivations and outcomes of cross-border M&As. In sum, our study contributes to the literature on cross-border M&As, offering insights into motivations and long-term performance while inviting further exploration into this complex corporate landscape.

Footnotes

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.