Abstract

The fulfillment of corporate social responsibility remains crucial for companies to maintain competitiveness in today’s rapidly developing digital landscape. A truly robust corporate social responsibility strategy involves avoiding “doing bad” and actively engaging in “doing good.” This study uses data from 692 A-share listed companies from 2013 to 2021 to analyze the relationship between top management team (TMT) functional experience, executive incentives, and corporate social responsibility behavior. The research suggests that such heterogeneity enhances responsible behaviors and reduces irresponsible behaviors of firms, and functional experience centrality enhances responsible behaviors but does not reduce irresponsible behaviors. By adopting a stakeholder and behavioral segmentation method into the firm’s corporate social responsibility, it was observed that TMT functional experience heterogeneity enhances responsible behaviors of internal stakeholders while reducing irresponsible behaviors of external stakeholders, whereas TMT functional experience centrality primarily enhances responsible behaviors of internal stakeholders. When compensation incentives exceed a certain threshold to align with the expectations of TMT, members can leverage their experience to enhance responsible corporate behavior and reduce irresponsible behaviors. However, equity incentives must be controlled within certain thresholds to effectively harness the heterogeneous functional experience of TMTs and address irresponsible corporate behavior.

Keywords

Introduction

Digitalization has brought unprecedented opportunities and positive effects for companies; however, it also comes with a series of negative challenges that place higher demands on corporate social responsibility. Most existing studies view corporate social responsibility behavior as a holistic concept (Hur et al., 2019; Mark et al., 2025). This approach pits responsible behavior against irresponsible behavior, overlooking the possibility that the two can coexist and operate independently. A few scholars have studied corporate irresponsible behavior separately (Yue et al., 2024; A. Q. Zhang & Gao, 2020), but they fail to analyze its relationship with responsible behavior in depth. Recently, some scholars have shifted their focus to studying responsible and irresponsible behavior simultaneously (Fu et al., 2020; Ma & Huang, 2023). They argue that both types of behavior can coexist within a firm, and irresponsible behavior often receives more attention from managers due to its distinct nature. Peng and Liu (2016) state that the relationship between responsible and irresponsible behavior should be like the motivation-hygiene factor within the two-factor theory. This analogy highlights the independence of responsible and irresponsible behavior: simply increasing responsible behavior cannot fully offset the negative effects of irresponsible behavior (Sun & Ding, 2021). Only by reducing both simultaneously can the overall level of corporate social responsibility be genuinely enhanced. This study focused on the simultaneous presence of responsible and irresponsible behavior in firms and argues that firms are not always overly concerned with irresponsible behavior, but rather, choose to behave differently depending on their needs. Furthermore, the fundamental purpose of a business is to generate profit, and corporate social responsibility serves as a strategic tool to enhance long-term profitability (Che et al., 2022). To achieve this, companies must align their operations with the expectations and demands of key stakeholders (Freeman, 1984). This study builds on this foundation by further subdividing corporate social responsibility behavior into responsible and irresponsible behavior toward internal and external stakeholders, which has also been neglected in previous studies.

Executive decisions determine company direction. Numerous recent studies on the impact of top management team (TMT) on corporate social responsibility behavior have focused on TMT characteristics, such as gender, age, education, tenure, and TMT’s individual functional background (Kwon et al., 2023; Manner, 2010). When TMT members have limited information about a particular task, they are exposed to a significant degree of information ambiguity, increasing decision-making risks. However, this can be counteracted by the members’ experiences. Among the various experiences of TMT (Yang et al., 2020), this study focuses on the TMT’s functional experiences. According to Yang et al. (2018), functional experience is crucial knowledge acquired by managers in their work. A firm’s executive functioning experience records the process of executive mobility, is a way for executives to enhance their competence through functional changes, and shapes their behavioral style (X. Wang et al., 2023). Functional experience heterogeneous teams with a diversity of cognitive structures and backgrounds can provide differentiated options for the enterprise to choose and reference, so as to achieve better results for the strategic options (Mitchell et al., 2021). The richness of an executive member’s functional experience enriches the executive’s perspective on issues and better prepares him or her to deal with the complexities that arise in operations (Duan et al., 2023). However, the only study on the heterogeneity of functional experience is that of Ma and Huang (2023), which verified a nonlinear relationship on social responsibility. The influence of functional experience on corporate social responsibility behavior warrants further research, which will not only validate existing findings but also provide new insights into its role in corporate social responsibility behavior.

Existing research on the moderating effects of TMT characteristics about corporate social responsibility can be categorized into two main types: The first involves the role of external pressures, such as industry competition intensity, institutional pressures, and media scrutiny (Chiao et al., 2025; Sun & Govind, 2022). The second is the internal governance mechanism, which is typically manifested in executive compensation incentives and power distance (Gala et al., 2024; Shu & Xiong, 2019). Compared to external pressures, this study argues that internal stimuli may be more effective in enhancing corporate social responsibility performance. As “rational economic beings,” executives seek to maximize their gains by enhancing corporate performance and operational efficiency. Incentives thus serve as a critical managerial instrument: under the premise of securing higher returns, they effectively motivate TMT members to fully leverage their expertise and skills, thereby facilitating strategic decisions that support the company’s long-term development. Executive incentives, such as compensation and equity-based rewards, serve as contractual mechanisms designed to align managerial behavior with organizational goals (Jensen & Meckling, 1976). These incentives not only motivate executives to pursue value-maximizing strategies but also regulate their decision-making processes, particularly in areas like corporate social responsibility (Flammer et al., 2019). However, the existing literature has yet to reach a consensus on how compensation or equity incentives moderate the relationship between TMT and corporate social responsibility. Some studies suggest that incentives can align executives’ interests with the organization’s long-term performance, thereby enhancing their commitment to corporate social responsibility (Shu & Xiong, 2019). Others argue that an excessive focus on financial rewards may lead to short-termism, which could potentially undermine corporate social responsibility initiatives (Aldogan Eklund et al., 2024). In addition, previous studies have mainly examined the linear moderating effect of incentives without exploring the optimal thresholds or conditions under which incentives are most effective. Therefore, this study introduces executive incentives as a threshold variable to determine their effectiveness in driving executive team experience to reduce corporate social responsibility behavior. By determining the optimal level of incentives, the positive effects of TMT functional experience on corporate social responsibility behavior can be better realized.

Drawing from the upper echelons theory and imprinting theory, this study investigates the relationship between the TMT functional experience, executive incentives, and corporate social responsibility among 692 A-share listed companies. It focuses on the following questions:

(1) How does functional experience in TMTs affect firms’ responsible and irresponsible behaviors?

(2) What is the impact of TMT’s functional experience on the responsible and irresponsible behaviors of internal and external stakeholders after dividing corporate social responsibility into internal and external responsibilities?

(3) Are there optimal incentive bands or thresholds for compensation and equity incentives that enable TMT members to effectively leverage their experience to enhance corporate social responsibility?

Theory and Hypotheses

Corporate Social Responsibility

In most studies, corporate social responsibility stands for corporate “doing good,” and it is usually defined as socially beneficial behavior by companies (Hur et al., 2019). Corporate social irresponsible behavior is often colloquially referred to as “doing bad” and is characterized by “unethical and morally repugnant behavior” (Lin-Hi & Müller, 2013). The conflation of responsible and irresponsible behavior tends to result in a “good-bad offset” of corporate social behavior, leading to the masking of “bad” corporate behavior. Studying irresponsible behavior separately and equating corporate improvement of irresponsible behavior with improved levels of corporate social responsibility (Lange & Washburn, 2012) is an approach that subconsciously views corporate improvement of irresponsible behavior as antithetical to the enhancement of responsible behavior. The real meaning of reducing the level of corporate social responsibility should be to enhance responsible behavior and reduce irresponsible behavior. This study argues that the improvement of the level of corporate social responsibility includes not only the reduction of irresponsible behavior but also the further enhancement of the responsible behavior of companies. We define enhancing responsible corporate behavior and reducing irresponsible corporate behavior:

Reducing corporate irresponsible behavior means that an enterprise corrects behavior that causes potential or actual adverse impacts and/or harm to its stakeholders in the course of its operations by taking a series of proactive measures (Tan et al., 2024).

Enhancing responsible corporate behavior refers to a series of proactive initiatives by enterprises to continuously optimize and strengthen their performance in fulfilling their responsibilities in various aspects, including economic, social, and environmental aspects, to achieve harmonious coexistence and sustainable development between enterprises and society (K. Zhang & Hao, 2024).

Integration of Upper Echelons Theory With Imprinting Theory

Corporate social responsibility, as a type of corporate strategy, is ultimately formulated and implemented by TMT. The upper echelons theory states that because of the decision-makers’ limited rationality and insufficient information for decision-making, the managers’ own experience, characteristics, mind, and state of mind all influence their decision-making (Hambrick & Mason, 1984). According to this theory, it can be inferred that the experiences of TMT affect both the responsible and irresponsible behaviors of a firm (Ma & Huang, 2023).

The concept of imprinting is illustrated by Marquis and Tilcsik (2013), who argue that the establishment of an organization, going public, or a major organizational experience are sensitive periods for firms, and that these phases have an impact on the organization that tends not to dissipate over time, but rather is persistent. Imprinting theory further explains how executives’ functional experiences shape their values and behavioral patterns through critical periods in their careers (Tian et al., 2022). For example, the functional experiences accumulated by executives during early career stages or critical events can have a lasting impact on their subsequent decision-making. If executives are exposed to socially responsible practices during their early experiences, such experiences can create a “responsibility imprint,” making them more inclined to promote corporate responsible behavior in future decisions. Conversely, if their experiences are more focused on short-term performance or neglect social responsibility, an “irresponsibility imprint” may form, leading to poor corporate social responsibility behavior.

By integrating the upper echelons theory and imprinting theory, we can gain a more comprehensive understanding of the impact of TMT functional experience on corporate behavior. Imprinting theory explains how executives’ experiences during critical periods shape their values and perceptions, which have a long-term impact on the formation and application of their functional experience (Tang et al., 2024). Meanwhile, the upper echelons theory emphasizes how these values and perceptions influence corporate decision-making through the background characteristics of the executive team (Zeng et al., 2020). The combination of these two theories provides an integrated perspective that highlights not only the lasting impact of critical experiences on executive decision-making (Wesley et al., 2022), but also how these imprints, when aggregated within TMT, shape the organization’s strategic direction and social responsibility performance (Osses & David, 2024).

Hypotheses

Top Management Team Experience and Corporate Social Responsibility

Heterogeneity of TMT functional experience refers to the variability in the number of different functional positions team members have held within the organization, reflecting the degree of variation in the functional positions experienced by team members (Yang et al., 2018). Heterogeneous teams with diverse cognitive structures and backgrounds can provide differentiated options and perspectives and better cope with uncertainty, leading to more optimal strategic choices. On the one hand, functional experience heterogeneity can provide TMTs with diverse information-processing perspectives, which makes managers more sensitive to changes in their environment (Bantel & Jackson, 1989). Upper echelons theory suggests that functional context can influence managers’ knowledge structures, cognitive patterns, and value orientations. Therefore, managers with different functional backgrounds will have different perceptions of the same issue, such as corporate social responsibility, with different perceptions and solutions (Lu et al., 2023). On the other hand, functional heterogeneity prevents management teams from falling into groupthink (Hambrick & Mason, 1984). Highly functionally heterogeneous executive teams can bring together different professional skills and management competencies, enabling them to consider all aspects of a company’s situation.

As a sustainable investment that integrates social, environmental, and economic benefits, social responsibility strategies are characterized by high investment and slow results. However, a good corporate social image can help enterprises establish long-term competitive advantages. Heterogeneous TMTs with functional experience can fully analyze the current situation of the company and make the right decisions. Therefore, we propose the following hypothesis:

March and Simon (1958) find that managers who have experienced a relatively homogeneous range of functions have accumulated experience that helps them perform routine tasks well but with a relatively narrow perspective. TMT functional experience centrality reflects the richness of TMT members’ own functional experience.

According to upper echelons theory and imprinting theory (Tang et al., 2024; Tian et al., 2022), with a production and R&D background, TMT members are more concerned about producing new products, reducing production lines, and enhancing production technologies. TMT members with management backgrounds focus on behaviors such as philanthropy. Managers with financial backgrounds are concerned with the flow of funds and other related issues. Managers with marketing experience focus on marketing products and receiving feedback from the market. When participating in a company’s strategy development, executives from different functional backgrounds always propose appropriate courses of action from their professional perspectives (Yao et al., 2015). The richer the functional backgrounds of TMT members, the more they can bring diversified professional perspectives, multichannel market information, and what needs to be paid attention to in each company’s business segments (Buyl et al., 2011). Moreover, there are differences in the thinking styles of team members from different functional backgrounds. Managers with experience in production, R&D, and marketing are more rational in their thinking; more sensitive to production, R&D, and market data; and often tend to reduce technology and products (Goodwin et al., 2009). Managers with backgrounds in management and human resources think relatively emotionally, and communication is their way of solving problems (X. Wang et al., 2023). Work experience from different functional backgrounds also has a significant impact on shaping executives’ cognitive foundations. TMTs with broader functional backgrounds are better able to deal with the complexity of their environments (Mitchell et al., 2021).

The functional experience of the TMT can comprehensively assess the current situation of the enterprise and propose problems that need to be addressed and solved (Shen et al., 2012). For example, managers engaged in financial management evaluate corporate philanthropic inputs from the perspective of financial budgets, and managers working in marketing pay more attention to customer feedback on products. When there is a problem with the product, the marketing department needs to recall the problematic product as soon as possible, the production department should test the product in time to determine the root cause of the problem, and the management department should respond to the concerns of customers and the media. Executives with strong functional experience can start from their own departments to collect information on the causes and processes of irresponsible behaviors, which can shorten the time for the enterprise to solve the corresponding problems and reduce losses. Therefore, we propose the following hypothesis:

Threshold Effects of Executive Incentives

Compensation Incentives

Expectancy theory posits that the effectiveness of incentive mechanisms largely depends on the psychological expectations of those being incentivized. Compensation systems that are linked to executive performance play a critical role in incentivizing behavior, particularly in corporate governance processes where managers make most strategic decisions. Previous research indicates that linking executive compensation to firm performance not only mitigates principal-agent problems but also encourages risk-taking behavior (Coles et al., 2006; Zuo & Tang, 2014). When executives perceive a direct link between their efforts and monetary returns, they are more likely to take positive action in favor of the company. For instance, compensation incentives can motivate executives to pursue performance-based rewards while avoiding financial inefficiencies, which improves the allocation efficiency of corporate resources (Xu & Feng, 2017).

However, two issues arise when using compensation incentives to motivate team members. First, inconsistency between compensation and executive expectations can lead to ineffective incentives. When executives perceive their compensation to be insufficient, they may engage in self-interested behaviors, including resource-taking or cost-cutting measures that undermine corporate social responsibility (Q. Li et al., 2018; Kou et al., 2023). Second, compensation incentives may be subject to diminishing marginal utility. As Zuo and Tang (2011) has pointed out, the additional incentive effect of compensation declines once compensation reaches a sufficiently high level. In this case, executives may become complacent and reduce their efforts while continuing to receive satisfactory rewards. This effect is particularly pronounced in high-performing or mature firms, where additional monetary incentives may no longer trigger additional effort or socially responsible actions. Therefore, simply increasing compensation incentives for executives is not always beneficial. Only when incentive intensity surpasses a specific threshold or falls within an optimal range can it effectively motivate the TMT to leverage their functional experience heterogeneity/centrality and positively influence corporate social responsibility behavior. Accordingly, we propose the following hypotheses:

Equity Incentive

Equity incentives are widely recognized as an effective tool to motivate managers to pursue long-term corporate goals by aligning their interests with those of shareholders (Manso, 2011). Unlike short-term compensation methods, equity incentives encourage executives to focus on the long term and consider the ongoing value of the company. As Laux (2012) argues, traditional compensation approaches may not generate sufficient incentives, while linking long-term results to equity can better align managerial behavior with organizational performance.

For TMT members with functional experience, equity incentives can enhance their ability to utilize domain-specific knowledge to improve corporate governance. Such teams are better able to reduce operational risks and costs (Dhaliwal et al., 2011; Guenster et al., 2011), capitalize on market opportunities (Öberseder et al., 2014), and promote long-term strategic positioning (Barnett & Salomon, 2012). Additionally, equity incentives encourage socially responsible strategies that promote legitimacy, stakeholder support, and long-term firm value. However, the relationship between equity incentives and managerial behavior is not strictly linear. For instance, Zhao et al. (2024) document a nonlinear effect, suggesting that managerial shareholding can only increase firm value to a certain extent. When shareholding is at a moderate level, managers are more likely to balance their personal interests with firm performance and use their functional experience to develop and implement corporate social responsibility programs. This may enhance the company’s social image, stabilize stock performance, and generate long-term returns. Beyond this optimal range, excessive shareholding may lead executives to pursue personal interests or be excessively risk-averse, thus weakening their incentives to prioritize corporate social responsibility. Based on this, this study argues that TMT functional experience heterogeneity/centrality can be effective in enhancing responsible behavior or reducing irresponsible behavior when equity incentives are within a reasonable range. Therefore, we propose the following research hypotheses:

Methods

Pre-research

The combination of interviews and secondary data was found to explain the research questions well (Kelly et al., 2024). We referred to the studies by Williams and Shepherd (2017) as well as S. Wang et al. (2016), and introduced interviews as a pre-research. Thematic analysis was used to analyze the interview data we obtained (Braun & Clarke, 2006; Gioia et al., 2013). Braun and Clarke (2006) emphasized that thematic analysis focuses on describing themes related to the research question, meaning that researchers start from predefined themes or a coding framework to identify corresponding evidence in the data, thereby confirming themes relevant to the research problem. Executives from three listed companies were selected for short interviews. Relevant information has been included in the appendices. Appendix 1 contains information about the companies that were interviewed. Appendix 2 presents a summary of the interview content, and Appendix 3 includes thematic analysis graphics drawn based on the interviews. Through these interviews, we preliminarily found that the functional experience of TMT influences corporate social responsibility behavior. This preliminary validation provides a foundation for subsequent hypothesis testing using extensive secondary data.

Sample and Data

The Research Report on CSR of China mentions that the social responsibility strategies of Chinese enterprises began in 2012, and the number of enterprises disclosed to the CNRDS (Chinese Research Data Services) gradually increased after 2012. Owing to the lag in corporate responses and the need to retain as much data as possible, this study sets the starting year of the data as 2013. This study uses a sample of 692 A-share listed companies (ordinary shares issued by companies registered in China, denominated and settled in RMB, and traded on the Shanghai or Shenzhen Stock Exchange) covering the period from 2013 to 2021. The sample is screened as follows: (1) companies with ST (Special Treatment) and ST* are excluded; (2) the financial industry is removed; and (3) samples with missing and abnormal data are not included. Data on social responsibility strategies is from the CNRDS database, and top management team functional experience, financial, and executive incentive data are taken from the CSMAR (China Stock Market & Accounting Research) database. Continuous variables are winsorized at the 1% level to mitigate the disturbance caused by extreme values.

Variable Measurement

Dependent Variable

This study fully considers each measurement method and seeks to select data from official databases that can reveal both responsible and irresponsible behavior. The CESG (formerly the CCSR) in the CNRDS database made it possible to obtain data for this study. It is an official Chinese database consistent with the measurement methodology of foreign KLD (Kinder, Lydenberg, Domini & Co. Inc.) databases. The database focuses on strengths as responsible behaviors and concerns as irresponsible. It covers the following six dimensions: “Philanthropy, Volunteerism and Social Controversies,”“Corporate Governance,”“Diversity,”“Employee Relations,”“Environment,” and “Products.” A company’s corporate social behavior was also assessed by assigning a value of 1 or 0 to each strength or concern. Responsible behavior is measured by the total number of strengths, and irresponsible behavior is measured by the total number of concerns across the six dimensions of strengths (Di Giuli & Kostovetsky, 2014). To compare responsible and irresponsible behavior, this study standardizes responsible and irresponsible corporate behavior (Koh et al., 2014; Mattingly & Berman, 2006).

Internal stakeholders include executives, employees, and shareholders, while external stakeholders include consumers, suppliers, the government, communities, and the media. In this study, according to the different stakeholders, the responsible and irresponsible behaviors of a company are categorized as internal stakeholder responsible behavior, internal stakeholder irresponsible behavior, external stakeholder responsible behavior, and external stakeholder irresponsible behavior.

Independent Variable

Referring to Cannella et al.’s (2008) categorization idea, the functional experience was classified into nine categories with the following coding rules: 1 = production, 2 = research and development, 3 = design, 4 = human resources, 5 = management, 6 = marketing, 7 = finance, 8 = financial, and 9 = legal. The CSMAR database uses the above numbers to represent executive functions. We can use these numbers to determine the number of functions each TMT member has experienced and how they have changed.

Functional Experience Heterogeneity

The heterogeneity of the functional experience of the team was calculated using Blau’s (1977) categorization index, which is given in the following formulas:

Where i denotes the category, n denotes the number of categories, and Pi is the proportion of the number of executives of functional type i to the total number of teams. The Blau index takes values between 0 and 1, with larger values indicating a higher degree of heterogeneity.

Functional Experience Centrality

The functional backgrounds of the team members were divided to differentiate the number of their functional positions so that the average could be calculated (Chen, 2011; Yang et al., 201867).

Xi denotes the number of functional positions each executive team member has experienced. The larger the TFC, the more the enrichment of the functional experience.

Moderator Variables

Referring to the measurement of compensation incentives by scholars, such as Y. X. Li et al. (2007), Ln is taken as a proxy variable for compensation incentives for the top three executives’ total compensation disclosed by the company at the end of the year.

Referring to the measurement of equity incentives by scholars, such as Bergstresser and Philippon (2006), the ratio of the number of equity shares granted to executives at the end of the year to the company’s total equity capital was used as a proxy variable for equity incentives.

Control Variables

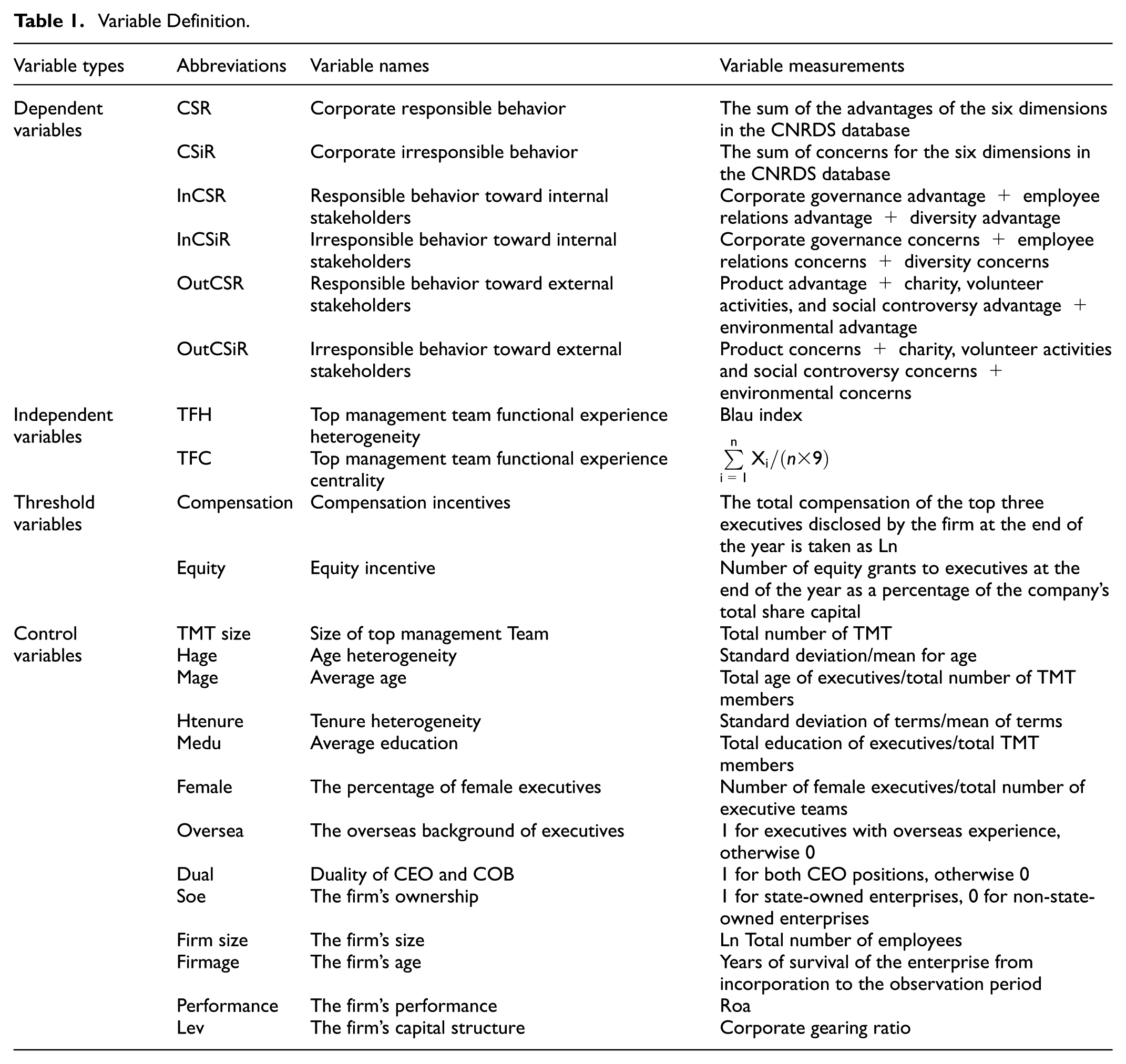

Drawing on previous research concerning TMT experience (Y. Y. Kor, 2003; Yang et al., 2020) and corporate social responsibility (Fu et al., 2020), this study incorporates the following control variables: TMT-level variables comprising TMT size, age heterogeneity, average age, tenure heterogeneity, average education, proportion of female executives, and executives’ overseas experience; and firm-level variables including ownership, firm size, firm age, firm performance, and capital structure, as presented in Table 1.

Variable Definition.

Results

Model Selection

In this study, the Hausman test was conducted on the sample data, and the results showed that the p value was close to 0 (p = .000), indicating that the fixed-effect model was appropriate.

Description and Correlation Analysis

Table 2 presents the results of the descriptive statistical analyses of the main variables. Responsible and irresponsible behaviors are standardized to have a mean of 0 and a standard deviation of 1. The mean heterogeneity of the functional experience is 0.687, and the standard deviation is 0.090. This suggests that there are significant differences in the functional backgrounds of TMT members in the sample firms. The average value of TMT functional experience centrality is 0.239, and the standard deviation is 0.052. This suggests that each TMT member is not highly enriched in terms of functional experience. The mean value of compensation incentives is 14.774, with a standard deviation of 0.801, indicating that there is a large gap in compensation levels between different firms. The mean value of equity incentives is 0.042, and the standard deviation is 0.103, which means that there is a gap in the percentage of executive shareholding between different enterprises.

Descriptive Statistics and Correlation Analysis.

p < 0.1. **p < .05. ***p < .01.

Regression Analysis

Table 3 shows the regression results examining the relationship between TMT functional experience and corporate responsible behavior.

Regression Results.

p < 0.1. **p < .05. ***p < .01.

The regression coefficient for Model 1 is 0.328 (p < .01), indicating a significant positive relationship between TMT functional experience heterogeneity and responsible behavior. This finding supports H1a that TMT functional experience heterogeneity can help enterprises enhance their responsible behavior. Model 2 reveals a significant negative association (β = −.326, p < .05) between functional experience heterogeneity and irresponsible behavior, supporting H1b. This finding indicates that TMT functional experience heterogeneity can help enterprises reduce their irresponsible behavior. Model 3 examines the effect of TMT functional experience centrality on responsible behavior and shows a positive relationship (β = .364, p < .1). The results indicate that TMT functional experience centrality can help enterprises enhance their responsible behavior, which supports H2a. However, Model 4 finds no significant relationship between TMT functional experience centrality and irresponsible behavior (β = −.097, p > .1). H2b is thus rejected, which posits that TMT functional experience centrality can help enterprises reduce their irresponsible behavior.

To further validate how TMT functional experience focuses on the responsible and irresponsible behaviors of the company, corporate responsible behavior was divided into responsible and irresponsible behaviors toward internal and external stakeholders according to stakeholders.

According to Freeman (1984), it is through interaction with stakeholders that an organization achieves its goals and grows, and the success of an organization depends largely on its ability to manage and coordinate its stakeholders. The fulfillment of social responsibility can be a signal between the firm and its various stakeholders (Cheng et al., 2024), and the firm communicates that it is concerned about the interests of its various stakeholders by being more socially responsible (Simmons, 2004). Responsibility to internal stakeholders is seen as a fundamental social responsibility of the firm, while responsibility to external stakeholders is a response to their requirements or expectations, and active fulfillment of such responsibilities can shape the social image of the firm (Hawn & Ioannou, 2016). By dividing corporate social responsibility into responsibilities to external stakeholders and to internal stakeholders, it is more likely to find out how experienced managers pay attention to and deal with responsible and irresponsible behaviors toward different stakeholders. The results are presented in Table 4.

Regression Results on the Impact of Internal and External Stakeholders.

p < 0.1. **p < .05. ***p < .01.

The regression results in Table 4 show that Model 5 of TMT functional experience heterogeneity on responsible behavior of internal stakeholders is 0.483 (p < .01); the regression coefficient of Model 7 is −0.163, which fails the test of significance; and Model 6’s regression coefficient is −0.169, which does not pass the test of significance; the regression coefficient of Model 8, TMT functional experience heterogeneity on external stakeholders’ irresponsible behavior is −0.317 (p < .05). Model 9 is the result of functional experience centrality on the responsible behavior of internal stakeholders (β = .603, p < .05), but Model 10, Model 11, and Model 12 are not significant. The above results show that heterogeneity of TMT functional experience has a comprehensive effect, enhancing responsible behavior of internal stakeholders while reducing irresponsible behavior of external stakeholders. In contrast, TMT functional experience centrality has a more limited impact, reducing only responsible conduct directed at internal stakeholders. A combined comparison of the results in Tables 3 and 4 shows that TMT members should not only select managers who have extensive functional experience themselves but should also pay attention to the heterogeneity of the functional experience of the executive team.

Threshold Effect

This study introduces executive incentives as threshold variables to investigate how companies should choose the right incentives to make the best use of their TMT’s experience to enhance corporate responsible behavior. To determine the number of thresholds for incentives, the bootstrap method of sampling for threshold effects was conducted under single, double, and triple threshold assumptions; the obtained F and P-values are reported in Table 5:

(1) A single-threshold model is used to study the relationship between TMT functional experience heterogeneity, compensation incentives, and responsible behavior;

(2) A double-threshold model is used to study the relationship between the TMT functional experience heterogeneity, compensation incentives, and irresponsible behavior.

(3) A single-threshold model is used to study the relationship between TMT functional experience centrality, compensation incentives, and responsible behavior;

(4) The threshold effect is not significant in the test of compensation incentives on the relationship between TMT functional experience centrality and irresponsible behavior.

(5) The threshold effect is not significant in the test of equity incentives on the relationship between TMT functional experience heterogeneity and responsible behavior.

(6) The double threshold model is used to study the relationship between TMT functional experience heterogeneity, equity incentives, and irresponsible behavior.

(7) The threshold effect is not significant in the test of equity incentives on the relationship between TMT functional experience centrality and responsible behavior.

(8) The threshold effect is not significant in the test of equity incentives on the relationship between TMT functional experience centrality and irresponsible behavior.

Threshold Effect Model Test..

p < 0.1. **p < .05. ***p < .01.

Table 6 presents the threshold variables for executive incentives. Figures 1 to 4 show the likelihood ratio (LR) plots for the compensation and equity incentive threshold effects. From the LR plots, it can be concluded that the thresholds are valid.

Threshold Variable Estimation Results.

Functional experience heterogeneity, compensation incentives, and responsible corporate behavior.

Functional experience heterogeneity, compensation incentives, and irresponsible corporate behavior.

Functional experience centrality, compensation incentives, and responsible corporate behavior.

Functional experience heterogeneity, equity incentives, and irresponsible corporate behavior.

Table 5 shows that several threshold effects between executive incentives and TMT functional experience dimensions fail to reach statistical significance. Specifically, the results indicate that compensation incentives do not exhibit a significant threshold effect in the relationship between TMT functional experience centrality and corporate irresponsible behavior. In this specification, the p-values for single-threshold, double-threshold, and triple-threshold are all higher than 0.1. Therefore, we conclude that H3d is not supported. Similarly, with respect to equity incentives, the data do not support a threshold effect between TMT functional experience heterogeneity and responsible behavior. Since the p-values of the single-threshold, double-threshold, and triple-threshold models are not significant (p > .1), we reject H4a. Furthermore, the threshold effect of equity incentives between functional experience centrality and responsible behavior is not significant, with p > .1 for single, double, and triple thresholds. Therefore, H4c is not supported. Lastly, the threshold effect of equity incentives does not hold between functional experience centrality and corporate irresponsible behavior, as p > .1 for the single, second-order, and third-order thresholds. Thus, H4d is also not supported.

We conducted further analysis on the results that passed the threshold effect tests. Table 7 shows the regression results of the threshold effect. Model 13 indicates that when compensation incentives are below the threshold value of 16.176, the regression coefficient of the TMT functional experience heterogeneity on responsible behavior is 0.331 (p < .01); when compensation incentives exceed the threshold value of 16.176, the coefficient increases to 0.540 (p < .01). The rise from 0.331 to 0.540 suggests that once compensation incentives surpass the threshold of 16.176, TMTs with diverse functional experience are more motivated to engage in responsible behaviors to earn higher compensation. H3a is tested.

Threshold Effect Regression Results.

p < 0.1. **p < .05. ***p < .01.

Model 14 shows that when compensation incentives are less than the threshold value of 14.874, the regression coefficient of TMT functional experience heterogeneity on irresponsible behavior is −0.300 (p < .1). When compensation incentives are greater than the threshold value of 14.874 and less than 15.627, the regression coefficient is −0.444 (p < .01). When compensation incentives are greater than the threshold value of 15.627, the regression coefficient is −0.258. These results indicate that compensation incentives are best utilized when the threshold is between [14.874 15.627]. An appropriate range exists in which compensation incentives can satisfy the TMT to reduce irresponsible behavior. H3b is tested.

Model 15 shows that when compensation incentives are less than the threshold value of 16.176, the regression coefficient of the TMT’s functional experience centrality on responsible behavior is 0.127 (p < .01); when compensation incentives are greater than the threshold value of 16.176, the regression coefficient is 0.247 (p < .01). The change in the regression coefficient from 0.127 to 0.247 indicates that when compensation incentives cross the threshold value of 16.176, TMT functional experience centrality is more motivated to enhance responsible behaviors to earn more compensation. So H3c is tested.

The results of Model 16 show that when equity incentives are less than the threshold value of 0.257, the regression coefficient of TMT functional experience heterogeneity on irresponsible behavior is −0.366 (p < .05). When equity incentives are greater than the threshold value of 0.257 and less than 0.297, the regression coefficient is 0.520 (p < .01). When equity incentives are greater than the threshold value of 0.297, the regression coefficient is 0.053. From the above results, it can be seen that the equity incentives are less than the first threshold value of 0.257, and TMTs with heterogeneous functional experience are motivated to reduce the firm’s irresponsible behavior to obtain equity. When equity incentives lie in the interval [0.257 0.297], the management team rapidly reduces the firm’s performance through irresponsible behavior to obtain more equity incentives. When the second threshold of 0.297 was crossed, the equity incentives ceased to work. The above results suggest that there exists a threshold value for equity incentives within which it is possible to motivate TMTs with heterogeneous functional experience to reduce irresponsible corporate behavior. H4b is tested.

Discussion and Contributions

Discussion of Findings

This study uses data from 692 A-share listed companies from 2013 to 2021 to analyze the relationship between TMT functional experience, executive incentives, and corporate social responsibility behavior. The results of all hypotheses have been presented in Table 8. Our findings support H1a and H1b, suggesting that TMT functional experience heterogeneity significantly enhances responsible behavior and reduces irresponsible behavior. This indicates that teams composed of members with diverse functional backgrounds are more capable of recognizing, interpreting, and responding to multifaceted corporate social responsibility requirements. These results are consistent with Lu et al.’s (2023) argument that a broader cognitive base facilitates the development of a more comprehensive corporate social responsibility strategy. In our study, H2a is supported, showing that TMT functional experience centrality can help firms increase responsible behaviors. This suggests that individual executives with extensive functional experience can use their expertise to support responsible behaviors. However, the hypothesis that TMT functional experience centrality can help firms reduce irresponsible behavior is not supported (H2d). This is different from Ma and Huang (2023), who concluded that experienced executives would be more concerned about corporate irresponsible behavior. A reasonable explanation is that executives with deep functional experience may find it more beneficial and less risky to proactively engage in corporate social responsibility than to reduce irresponsible behavior, which often involves reputational or legal risks and greater internal resistance.

Summary of Hypotheses Testing and Results.

Furthermore, we categorized corporate social responsibility based on different stakeholder groups into internal and external stakeholders. The findings demonstrate that TMT functional experience heterogeneity can comprehensively improve corporate social responsibility performance: It not only enhances responsible behaviors toward internal stakeholders but also reduces irresponsible behaviors targeting external stakeholders. In contrast, the influence of TMT functional experience centrality appears more limited, only improving responsible behaviors toward internal stakeholders. The evidence substantiates that TMT necessitates both diversified functional expertise among individual members and heterogeneous functional background composition at the team level.

In the context of executive incentives, we observe a threshold effect of compensation incentives. Specifically, compensation must surpass a critical threshold (16.176) to activate the positive effects of TMT functional experience heterogeneity on improved behavior (H3a) and TMT functional experience centrality on the same outcome (H3c). Additionally, within the optimal range of [14.875 15.627], TMT functional experience heterogeneity also helps reduce irresponsible behavior (H3b). These findings indicate that modest, targeted financial incentives can motivate executives to use their functional expertise for responsible governance, as long as the incentives are perceived as sufficiently rewarding. This aligns with the research argument advanced by scholars Xu and Feng (2017). However, since H3d is not supported, compensation incentives do not have a threshold effect on the relationship between TMT functional centrality and irresponsible behavior. This may be due to the complexity of addressing irresponsible behavior. Even if individual executives have extensive functional experience, corporate irresponsibility may stem from conflicting interests or various non-financial factors. These complexities make it difficult to effectively motivate executives through compensation alone to drive change or take responsibility for correcting irresponsible practices.

As for equity incentives, the results are even more interesting. We find support for H4b, which states that TMT functional experience heterogeneity reduces irresponsible behavior when equity remains below 25.7%. At this threshold, equity incentives align executives’ interests with the long-term goals of corporate social responsibility while preventing over-control and opportunism. This finding is consistent with Zhao et al. (2024). Conversely, H4a is not supported, indicating that equity incentives do not significantly promote responsible behavior. This may be because equity encourages long-term value maximization but also fosters risk aversion, making executives less likely to pursue corporate social responsibility strategies with uncertain short-term returns. In addition, we find that H4c and H4d do not hold. Equity incentives have no significant threshold effect on the relationship between functional centrality and corporate social responsibility. One possible explanation is that executives with extensive professional experience may develop entrenched behavioral patterns that prioritize their specialized functional expertise, such as technical performance or operational control, over broader social concerns. Even as equity holders, their individual actions are often insufficient to change the overall course of corporate social responsibility practices, and they face risk. Therefore, equity incentives have not been very effective in motivating TMT functional experience centrality to fulfill social responsibilities.

In summary, the discussion mentioned reveals a divergence from previous research (Fu et al., 2020; Ma & Huang, 2023), which suggested that managers predominantly focus on corporate irresponsible behaviors. Our study demonstrates that TMT members do not consistently overemphasize irresponsible corporate actions. Specifically, executives with extensive functional experience exhibit a stronger propensity to enhance responsible corporate behaviors, while functionally heterogeneous TMTs show comparable attention to both responsible and irresponsible behaviors. Notably, teams with diverse functional expertise can compensate for the shortcomings of individual experienced executives in addressing irresponsible behaviors. Regarding incentive mechanisms, our results indicate that compensation incentives must meet executive expectations to be effective; equity incentives require careful scope control; and neither compensation nor equity incentives significantly influence irresponsible behavior modification among functionally experienced executives. These insights show that while cultivating individual managers with rich functional expertise remains important, organizations must simultaneously build functionally heterogeneous TMTs to address corporate social responsibility challenges more effectively.

Contributions

Theoretical Contributions

Much of the existing research has centered on corporate social responsibility in its entirety (Mark et al., 2025). And some studies concentrate exclusively on irresponsible behavior (Yue et al., 2024). This study incorporates both responsible and irresponsible behaviors into the research framework, not only analyzing how various factors influence them but also refining corporate social responsibility behavior to consider its impact on internal and external stakeholders. This approach expands upon previous studies that solely examined corporate social responsibility as a unified concept and provides a new perspective on the study of corporate social responsibility.

Previous studies have mostly used upper echelons theory to explain the impact of functional experience heterogeneity on corporate social responsibility while ignoring the impact of the richness of executives’ own functional experience, which leaves a mark on the executives themselves for each of their functional experiences (Y. Kor & Tan, 2025; Tang et al., 2024). The combination of upper echelons and imprinting theory explains why TMTs with different experiences focus on different aspects of corporate social responsibility. It makes up for the fact that previous studies have always focused more on functional experience heterogeneity and neglected TMT functional experience centrality.

Existing studies primarily examine the linear moderating effects of incentives (Aldogan Eklund et al., 2024; Shu & Xiong, 2019). Departing from prior research, this study posits that the effectiveness of incentive mechanisms depends on their alignment with executive expectations. Consequently, we conceptualize incentives as threshold variables to investigate how compensation incentives and equity incentives drive executives to leverage their functional experience, thereby enhancing corporate responsible behaviors or reducing irresponsible behaviors. Our findings reveal that compensation incentives prove more effective than equity incentives in motivating executives to apply their functional experience toward reducing responsible behaviors. Furthermore, when TMTs utilize heterogeneous functional experience to address irresponsible behaviors, appropriate boundaries must be established for equity incentives to prevent potential adverse effects. These findings not only extend the research on incentive mechanisms but also provide new insights into the underlying mechanisms linking TMT characteristics and corporate social responsibility.

Practical Contributions

This study shows that companies should improve their corporate social responsibility by promoting responsible behaviors and reducing irresponsible ones. As the digital age progresses, companies need to not only fulfill their traditional social responsibilities but also tackle the new challenges of digital transformation. Digital technologies provide new opportunities to strengthen corporate social responsibility efforts, but they also introduce issues like data security risks and privacy breaches. Enterprises should adapt to evolving times, continue to do good things, and avoid doing bad ones.

TMT functional experience plays a crucial role in the fulfillment of corporate social responsibility. First, TMT functional experience centrality can strengthen responsible corporate behaviors. Thus, in developing executive capabilities, emphasis should be placed on cultivating cross-functional experience and diverse perspectives through rotations and training across different roles. Second, TMT functional experience heterogeneity enables firms to both increase responsible behaviors and reduce irresponsible behaviors. Therefore, executives should be selected from diverse functional departments within the enterprise when forming a TMT. At the same time, team members can be formed through different channels: internal recruiters can reduce the time for members to bond; external recruiters can bring in new recruits with fresh perspectives into the organization. Enterprises should encourage more communication and cooperation among executive members to increase tacit understanding and improve decision-making efficiency and science.

Because compensation incentives can only work when they meet the expectations of executives, it is necessary for companies to set reasonable evaluation standards to motivate executives to utilize their knowledge to obtain appropriate salaries. Enterprises can also provide appropriate equity incentives to avoid the emergence of a dominant TMT and undermine the positive incentive role of equity incentives. Companies can combine multiple incentives to satisfy executives’ needs for higher income.

Limitations and Future Agenda

To measure corporate social responsibility, the CNRDS database contains a limited number of firms, and the data sample had to be culled due to the presence of more years of missing data for some firms. However, over time, more firms will reveal information about social responsibility, and a larger sample size will make the conclusions of this study more convincing. This study did not examine the possible path relationship between TMTs’ functional experience and corporate social responsibility. Whether such a path exists and explains well needs to be verified in future studies. Furthermore, digitization is only used as a backdrop in this study, and future research could utilize digitization as a specific variable to explore how it affects the relationship between TMT functional experience and corporate social responsibility, and to determine whether it exhibits distinctive features that validate and extend our findings. Lastly, although we employed the interview method, it is not the primary approach of this study. Future research could increase the interview sample size or utilize a suitable questionnaire to further enhance our findings.

Footnotes

Appendix

Location: 1 business offline, 2 businesses online, for a total of 202 min.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Sichuan Province Key Research Base for Philosophy and Social Sciences in Higher Education Institutions, Civil-Military Integration System and Mechanisms Innovation Research Center (JHRH2025-003); Sichuan Provincial Key Research Base for Philosophy Social Sciences, Sichuan Tourism Development Research Center (LY24-16).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statements

The data in this article can be accessed from the CNRDS database (https://www.cnrds.com) and CSMAR database (![]() ).

).