Abstract

After more than 30 years of using Activity-Based Costing (ABC) to determine costs, just a few studies have analyzed its publications. This article aims to conduct a systematic, comprehensive literature review analyzing papers on ABC to overview what has been researched and give future research directions. The study includes descriptive, relational and content analyses of 1,260 articles retrieved from Scopus over 32 years (1988–2019). Our research shows publication trends, the most influential journals, authors and countries, citations, H-index, authorship, objectives, keywords co-occurrences, and research methods. Moreover, twelve objective categories are proposed. The results show a still-growing interest in ABC, especially in health and manufacturing, where there have been more practical applications. The case study is the most used research methodology, and the United States is the leading country regarding academic productivity and citations. The study provides useful information for professionals and business managers, and academics.

Keywords

Introduction

It has been over 30 years since the first conceptual papers on a new cost system, Activity-Based Costing (ABC), were published (Cooper, 1988; Cooper & Kaplan, 1991, 1992; Kaplan, 1989). This system was a better alternative to traditional costing systems (McGowan, 1998), which were based on the volume of production and had received considerable criticism (Cooper, 1987; Cooper & Kaplan, 1988) as they provided a very simplified view of the organization (Mévellec, 1993).

The ABC system proposes product cost determination through the activities carried out in the company. It considers that these activities and how they are performed consume the company’s resources. Therefore, the activities consume the company’s resources and not its products. Identifying these activities should ensure better cost allocation reducing remarkably indirect costs as those costs are now direct with ABC. Then, products consume these activities besides other direct costs. Cost drivers distribute the costs of activities among the products that consume them. In this sense, cost drivers can be the number of labor hours, orders completed, or any unit that links activities and costs.

Probably, the ABC innovative procedure and its diffusion and wide implementation in different industries have led it to be considered one of the most important management innovations of the 20th century (Bjørnenak & Mitchell, 2002; Mol & Birkinshaw, 2014) and one of the most studied (Gosselin, 2007; Zawawi & Hoque, 2010).

Although it was well-received academically and professionally, it also has some detractors (Gosselin, 1997; Malmi, 1997). Many of these criticisms, such as the method’s complexity and cost, were addressed by Kaplan and Anderson (2004), who proposed a simplified version: Time-Driven Activity-Based Costing (TDABC). This evolution of ABC relies on time as the unique cost driver.

Nevertheless, multiple case studies apply ABC in different sectors and contexts. For example, in textile manufacturing (Prasetyowati et al., 2019; Tsai, 2018b), electronic devices (Calvi et al., 2019), paper industry (Tsai & Lai, 2018), forging industry (Rezaie et al., 2008), electric technologies (Bharara & Lee, 1996; Tsai et al., 2015), among others. In the energy field, we find applications in thermal power plants (Dwivedi & Chakraborty, 2016; Feng et al., 2008), in energy systems in Taiwan (Yang, 2018) and in heating and biomass-based energy (Korpunen & Raiko, 2014). Likewise, ABC has been applied in logistics, for example, in a logistics distribution center in Chile (Durán et al., 2019) or the logistics of construction materials (Fang & Ng, 2019). In the construction sector, we find, for example, applications of ABC to analyze hidden costs in a construction project (Shao et al., 2018), to predict costs in the construction of prefabricated units with uncertainty (Wang et al., 2018) or to reduce environmental impact in-wall supply (Yi et al., 2017). Finally, it has also been applied in service sectors such as financial services (Barakat et al., 2017), tourism (Noone & Griffin, 1997, 1999) and healthcare (Leahy et al., 2017; Shander et al., 2010).

Despite the recognized importance of ABC and the significant amount of literature addressing cost issues through this system, ABC’s academic reviews are few and out-of-date, as seen in the next section. A cost system, such as the ABC, with more than 1000 articles published in the Scopus database, deserves to be analyzed in-depth to provide future research directions for academics and ideas of implementations for professionals. So, a comprehensive review of this literature is needed to provide an overall understanding (Zawawi & Hoque, 2010).

Therefore, analyzing this previous research is the main objective of the paper. So, this work aims to cover the gap of synthesizing ABC’s academic publications’ evolution to highlight its use, motivations and find future research directions.

In the next section, previous ABC reviews are detailed to justify the need for the present review. Afterwards, the methodology used in the review is explained. Then, the discussion and results section in section four displays the findings of the descriptive, relational and content analyses conducted. Finally, the conclusions section highlights the main contributions.

Previous Research Reviewing ABC

Shortly after ABC appeared, some literature reviews were published, including this cost system, among others. Some considered ABC as another model within management accounting research (Shields, 1997; Staubus, 1990). Other authors only focused on empirical research using it (Ittner & Larcker, 2001). But Zawawi and Hoque (2010) highlighted it as an essential innovation in the field. They analyzed 89 papers, 19 combined with Activity-Based Management (ABM).

The first review focusing specifically on ABC was published in 2002. It was authored by Bjørnenak and Mitchell (2002). These authors reviewed 404 articles published in 17 accounting journals from the United Kingdom and the United States during 1987 to 2000 (14 years) to learn about ABC’s beginnings how it was disseminated, researched, and developed.

Other narratives and traditional reviews on ABC were the studies of Gosselin (2007). He reviewed this cost system, implementation and consequences for 17 years (1988–2004) from its beginnings until the appearance of TDABC. More recently, and in the specific case of production, Momeni and Azizi (2018) carried out a narrative literature review on order management and inventory control. They concretely analyzed the degree of ABC use in those functions.

Besides the narrative reviews found, previous research has also conducted other types of reviews, such as systematic literature reviews (SLR) (Toronto Health Economic Technology Assessment Collaborative, 2013), bibliometric reviews (Fitó Bertran et al., 2018; Terzioglu & Chan, 2013), or meta-analyses (Alcouffe et al., 2019). For example, Vargas Alves et al. (2018) conducted a SLR on 27 English papers on ABC and TDABC applied to cancer, determining the trend of publications over the years, the countries where the studies were done, and the most preferred techniques of cancer prevention, diagnosis and treatment. Terzioglu and Chan (2013) studied 77 articles published in accounting journals, on ABC and ABM, through a bibliometric review, over 12 years (2001–2011), concluding that the manufacturing sector is the priority area of ABC research and that the research was mainly conducted by survey and case studies. Other bibliometric studies include Kuo and Hang (2014) work, which analyzed ABC’s intellectual structure to understand its evolution and critical ideas. They applied co-citation analysis (co-citation correlation matrix), multivariate statistical techniques: factor analysis, cluster analysis and multidimensional scaling (MDS) considering 61 publications, with 20 or more citations, in academic and professional accounting journals over 11 years (1988–2008). There are some examples of meta-analyses and statistical analyses (Tarzibashi & Ozyapici, 2019; Vargas Alves et al., 2018) applied to previous findings reported by academic research on ABC. Concretely, Alcouffe et al. (2019) reviewed 24 documents related to product diversity and ABC’s adoption through a meta-analysis (ANOVA, Egger’s test). By searching the keywords “Activity” and “Costing” in the title, and “ABC” in the text, they concluded a significant and positive relationship between product diversity and ABC adoption. Likewise, Tarzibashi and Ozyapici (2019) reviewed 37 articles that dealt with the relationship between the number of general costs and the results of implementing ABC and TDABC. These authors concluded that there are differences between both systems: the more indirect costs, the more differences between methods in terms of implementation.

Considering the years covered by previous reviews, the number of articles they included and the different typologies of literature reviews conducted, we believe our work represents a relevant contribution to the ABC literature. It spans from the beginning of the ABC to 2019 inclusive (32 years). More than 1200 articles are analyzed. Moreover, it contemplates a broad approach, including a systematic and bibliometric revision that involves descriptive, relational and content analyses.

Methodology

We used a systematic literature review (SLR) to achieve our objective of analyzing ABC literature. This methodology is characterized by allowing other researchers to replicate the search. In this sense, this review follows the criteria established by Tranfield et al. (2003) and Thorpe et al. (2005) for conducting SLR. Works based on SLR must indicate the methodology used and provide a detailed description of the process followed to guarantee objectivity and transparency in documenting all the procedures executed (Denyer & Neely, 2004).

This approach is highly used in management for getting an overview of the topic (Ginieis et al., 2012; Niñerola et al., 2020).

Keywords and Database

On the one hand, two keywords were used: “activity-based costing” following Kuo and Hang (2014) and “activity-based cost,” as they are the most representative of this system. Besides, we included their variations: capital letters, lowercase, and hyphens between words. These words had to appear in the title, abstract or keywords. Through this search, 1,507 and 293 articles were obtained, respectively, for each keyword. “ABC” as a keyword was not used since it retrieved many papers not related to management accounting. Moreover, the ABC documents that used the acronym also used the full name applied in the search.

On the other hand, Scopus was the database chosen due to its academic relevance and its coverage of peer-reviewed publications (Martín-Martín et al., 2018; Mingers & Leydesdorff, 2015).

Search Criteria and Articles Selection

The analyses included only articles (no proceedings, letters, reviews or notes). Moreover, they should be published in their final version in scientific journals and written in “English” or “Spanish.” Therefore, the search was carried out at two different moments: October 2019 and March 2020 (to update it).

Figure 1 shows the PRISMA statement (Preferred Reporting Items for Systematic Reviews and Meta-analyses) (Moher et al., 2010). After the screening and eligibility stages, 1,260 articles were considered for analysis.

PRISMA.

Units of Analysis and Data Processing

Following Niñerola et al. (2019), the descriptors identified in each article for carrying out the subsequent analyses were: year of publication, citations, type of authorship (academic, professional or both); country of affiliation of the authors, journal, title, keywords, research method and objectives of the paper. In addition, the homogenization steps conducted before the analyses should be highlighted for consistency of the results. For example, the country acronyms UK—United Kingdom or USA or US—United States; origin names as Deutschland—Germany, España—Spain; keywords abbreviations with the same meaning, and so on.

Two software were used for data processing: Excel to carry out calculations, tables and graphs, and VOSviewer (van Eck & Waltman, 2017) to visualize scientific maps (co-citation, co-occurrence, and network analysis).

On the other hand, we classified the main goals of the papers by applying content analysis techniques. During the data analysis, objectives were defined after reading the title, abstract, and on many occasions, the full texts of the selected articles. Therefore, they derived from the content rather than from literature or theory. Subsequently, they were grouped into 12 categories following the similarities with those proposed by Innes et al. (2000) and Kuo and Hang (2014). To guarantee the results’ consistency, two authors were independently working on the open coding process to identify the objectives. Afterwards, the three authors discarded duplications, discussed discrepancies, and ensured the validity of their classification

Discussion and Results

Results are presented in the following six subsections. First, a descriptive and relational analysis of ABC publications’ was done concerning its trend over time, the most cited articles and the leading journals (including a bibliographic coupling analysis). Second, authors’ descriptive analyses were conducted according to the typology of authorship (academic or professional), the number of publications per author, citations and H-index, and a relational co-authorship analysis to identify the main clusters (research groups). Third, the countries with the most publications and the most citations received are shown. Fourth, keywords are analyzed, identifying those more relevant according to their co-occurrence in literature. Fifth, the different research methodologies used, their evolution and frequency are examined, and the economic sectors where case studies were focused. Finally, the content analysis of the articles determines the main objectives pursued and how the literature on the cost system has evolved.

ABC Publications Evolution

In this section, we analyzed, firstly, on a descriptive analysis basis, the trend of publications, the top ten cited articles, the journals that published papers on ABC and their citations and secondly, we conducted a relational analysis of journals.

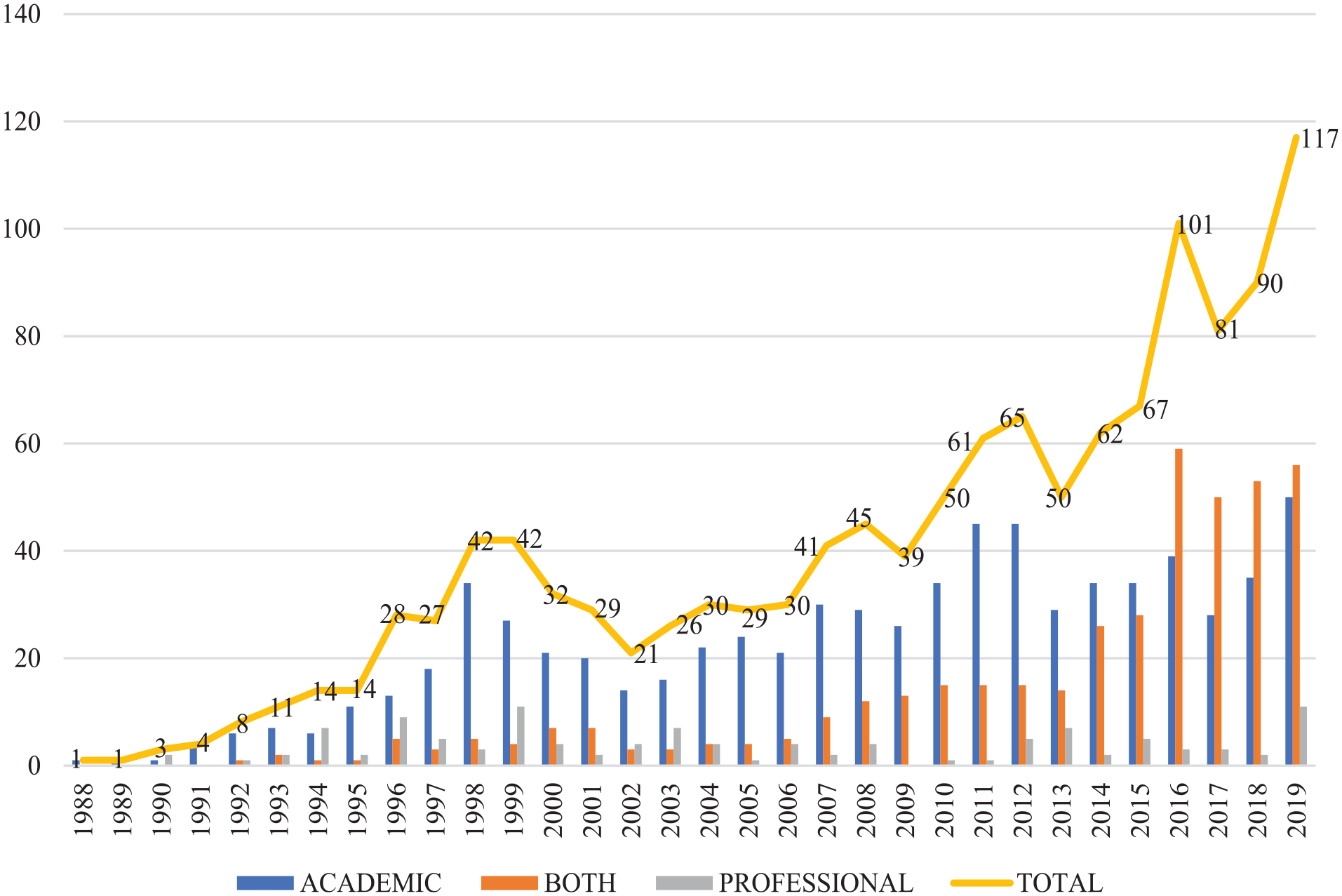

Firstly, seeing Figure 2, we can conclude that the publications using ABC as a cost system are growing during the period studied. From the first article identified in 1988 to 117 documents published in 2019, the number of papers per year has been oscillating but increasing overall. Considering only the last 4 years, we can count 389 articles representing more than 30% of the total. It means that ABC still catches the research’s attention and practitioners, although it has been more than 30 years since it appeared. Therefore, the number of articles published could be considered a proxy for the interest of the management accounting community for ABC (Gosselin, 2007).

Publications trend.

Secondly, the 1,260 articles received 16,951 citations, averaging 1.78 per article. However, the top 10 cited documents received 2,022, 12% of the total. Finally, it should be noted that the most relevant article is from the medical field (Shander et al., 2010) (Table 1). The importance of the health field in a method usually increases the number of joint collaborations between academics and practitioners, in this case, doctors (Niñerola et al., 2020). In this sense, we saw in Figure 2 the publication growth tag as BOTH.

The TOP 10 ABC Articles in Terms of Citations.

Note. c/y = citations per year; AOS = Accounting Organizations and Society; IJPE = International Journal of Production Economics; EJOR = European Journal of Operational Research.

From this Table 1, we can also highlight that the Accounting, Organizations and Society journal has published four of these TOP articles, followed by Management Accounting Research and International Journal of Production Economics with 2. On the other hand, the authors are mainly from the US, a country with a high tradition in research and cost management.

Thirdly, we found 726 different journals in the database. Five hundred seventeen journals published one article related to the topic studied, 104 have published two, 44 journals account for three articles, 23 published four of them, and 38 have published five or more articles about ABC.

Nevertheless, these 38 journals more interested in ABC published 311 articles, representing 25% of the total. In this sense, International Journal of Production Economics ranks first with 35 articles, followed by International Journal of Production Research with 28 and Management Accounting Research with 22. The first two journals have continuously published articles addressing cost issues applying ABC, while Management Accounting Research has not published this topic since 2011 (Figure 3). This fact suggests that journals with a professional and multidisciplinary approach are more interested in publishing articles using ABC than journals in accounting.

Leading journals.

Lastly, as expected, journals with more articles typically receive more citations (Figure 3). However, in this review, the journal Transfusion stands out. With only five articles and 597 citations, it gets the highest number of citations per year (90.33 citations per year [c/y]). The International Journal of Production Economics is second (81.87 c/y and 1,337 in total), followed by Management Accounting Research (74.99 c/y and 1,373 total citations) and the International Journal of Production Research (68.17 c/y and 784 total citations). The explanation of this anomaly with the journal Transfusion is due to its belonging to the medical field. In this research area, papers generally get a higher number of citations. For example, the article written by Leahy et al. (2017) has 100 citations and 33.33 c/y while the work of Shander et al. (2010) counts 449 citations and 45 c/y.

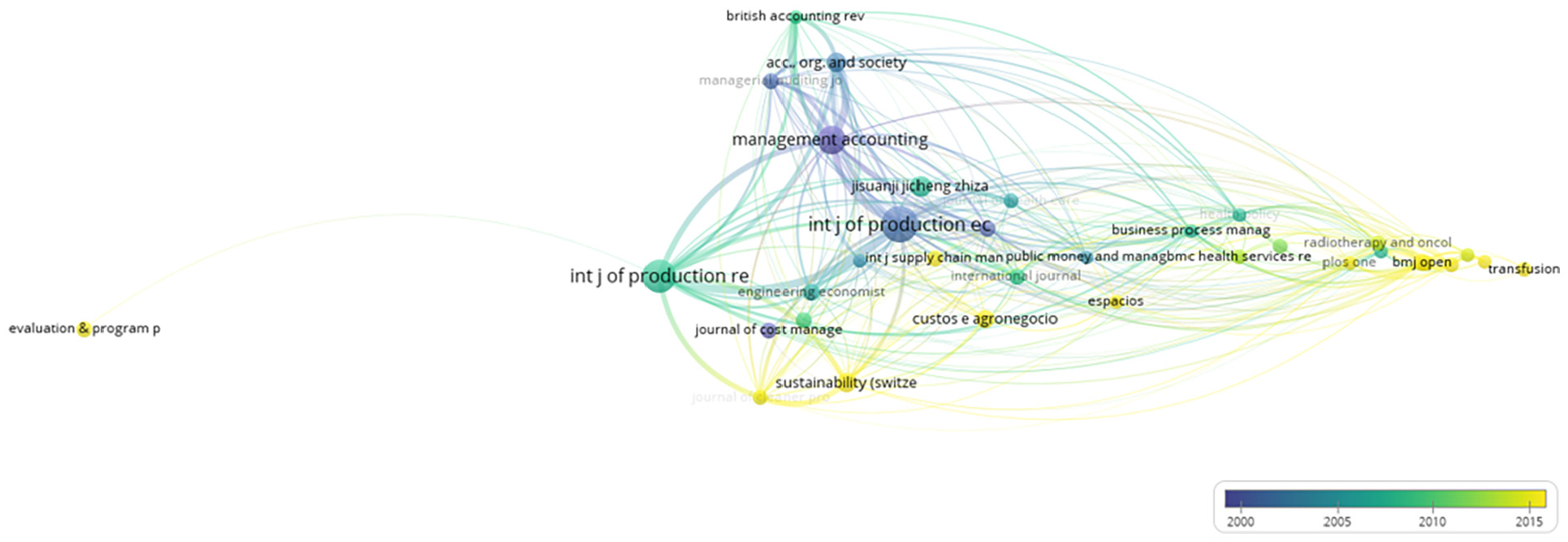

On the other hand, besides the descriptive analysis of the database journals, we conducted a relational analysis. The bibliographic coupling technique uses citation analysis to establish a similarity between documents and occurs when two works refer to a third common work in their bibliographies. In this sense, the bibliographic coupling can be applied to journals to identify similarities. Furthermore, this technique divides the bibliometric material into clusters, represented by different colors, permitting the visualization and analysis of items that share references (Waltman et al., 2010).

It should be noted that the bibliographic coupling has been carried out considering journals that have published at least five articles on ABC as is the default threshold established by the software and commonly accepted (Figure 4).

Bibliographic coupling.

Nodes represent the number of journal citations, and the distance between them approximates their relatedness. The more citations they share, the stronger their bibliographic link (indicated by the line thickness). It should be pointed out that in VOSviewer each item only can belong to a single cluster (van Eck & Waltman, 2017).

Journals that cite identical bibliographic material are expected to have similar research profiles and be interesting for the same audience. In this sense, we identify four clusters (Table 2) that show the different research areas where ABC has been applied. Cluster 1 (red) corresponds mainly to health journals. Cluster 2 (green) corresponds to journals primarily dedicated to engineering, technology, management and business. Cluster 3 (blue) includes specialized journals on accounting and finance. And cluster 4 (yellow) groups journals related to production and logistics.

Cluster Analysis Based on Bibliography Coupling.

Note. IJPR = International Journal of Production Research; CIMS = Computer Integrated Manufacturing Systems.

On the other hand, analyzing the bibliographic coupling from an evolution point of view (Figure 5), we observe that journals such as International Journal of Production Economics; Management Accounting Research, and Accounting, Organizations and Society published more articles at the beginning of the period studied. On the contrary, it is observed that journals focusing on health and production and planning have published research on ABC more intensively in the last few years. It seems to indicate that the interest in applying ABC in those areas is growing nowadays, especially considering the large volume of articles that have been published in recent years. This fact may also suggest the importance of ABC at the decision-making level, not only focused on the management accounting area.

Bibliographic coupling evolution.

Authors Analysis

In this subsection, first, we analyzed the type of authorship, authors by the number of published articles, countries, and H-index, considering the number of publications and the citations as the unit analysis. Then we did a relational analysis (co-authorship).

Considering the number of published articles, the publications’ evolution shows the topic’s sustained interest, especially since 2004 (Figure 2); 4,636 authors have written about the ABC system, 3,078 men (66.4%) and 1,455 women (31.4%). In 93 cases (2%), the gender could not be identified because they were professionals (consultants, advisers, or doctors) who wrote a single article and signed with initials or as an organization.

Moreover, 724 articles have been written exclusively by academics (57.5%), 114 papers by professionals (9.0%), and 420 papers (33.3%) have joint authorship between both. The number of collaborations between academics and professionals has increased, being the highest in 2016 (Figure 2). The explanation can be twofold. On the one hand, ABC requires particular knowledge provided by specialized professionals (practitioners and consultants) in the method. On the other hand, professionals have access to important information on technical innovation, and their contributions to articles can be attractive to journals readers. Moreover, they can be interested in these publications for the promotion and reputation obtained from showing their developments (Bjørnenak & Mitchell, 2002).

Additionally, implementations are increasing in different sectors. Each sector may have different production processes, organizational models, and so on, making the participation of experts in the implementation necessary. This is especially relevant in many case studies of real implementations carried out and published. Publications with exclusive professional authorship are maintained over time, although fewer than others. So, this indicates a practical interest in ABC. These findings are consistent with previous reviews (Bjørnenak & Mitchell, 2002).

Regarding the most productive authors, 34 authors with five or more articles on ABC have been identified (Table 3). They have received 5,058 citations, with an annual average of 9.44 (c/y). Tsai, W.H. is the most prolific author with 29 articles, and he also ranks first in terms of citations, with 844 citations and 35 c/y. It should be noted that most of these articles focus on joint product mix decisions in manufacturing companies, more specifically on green manufacturing companies, green recycling, carbon taxes and sustainability in some cases. On the other hand, 20 out of 29 of his papers are published after 2010. Kaplan, R.S., the forefather of ABC, ranks second with 16 articles on ABC and 427 citations (with the second-highest annual average being 23), followed by Subramanian, S., Roodhooft F., and Tangka F.K.L. with 15, 12, and 10 articles, and 160, 587, and 101 citations, respectively.

Authors With Five Publications or More.

Nineteen authors of these 34, who accumulate 133 articles and 2,410 citations, are from the US, the leading country in publications on ABC. In the second place, with two authors, we found authors from Taiwan (35 articles and 964 citations), Belgium (20 and 820), Netherlands (11 and 224), and India (10 and 18).

Then, we analyzed these 34 authors by their H index, quantifying individual scientific production by comparing the number of articles and citations (Hirsch, 2005). The highest H index (including all author publications, not only those on ABC) is 40, held by Saigal C.S. It means that this author has at least 40 articles published that, at least, received 40 citations. In contrast, the highest H index calculated exclusively for articles published on ABC is 15. It corresponds to Tsai, W.H. This result is expected as he has many publications on the topic. Nevertheless, comparing both indexes (total and ABC) it can be deduced that the area of management accounting, at least in the specific case of ABC, receives fewer citations on average than other research areas.

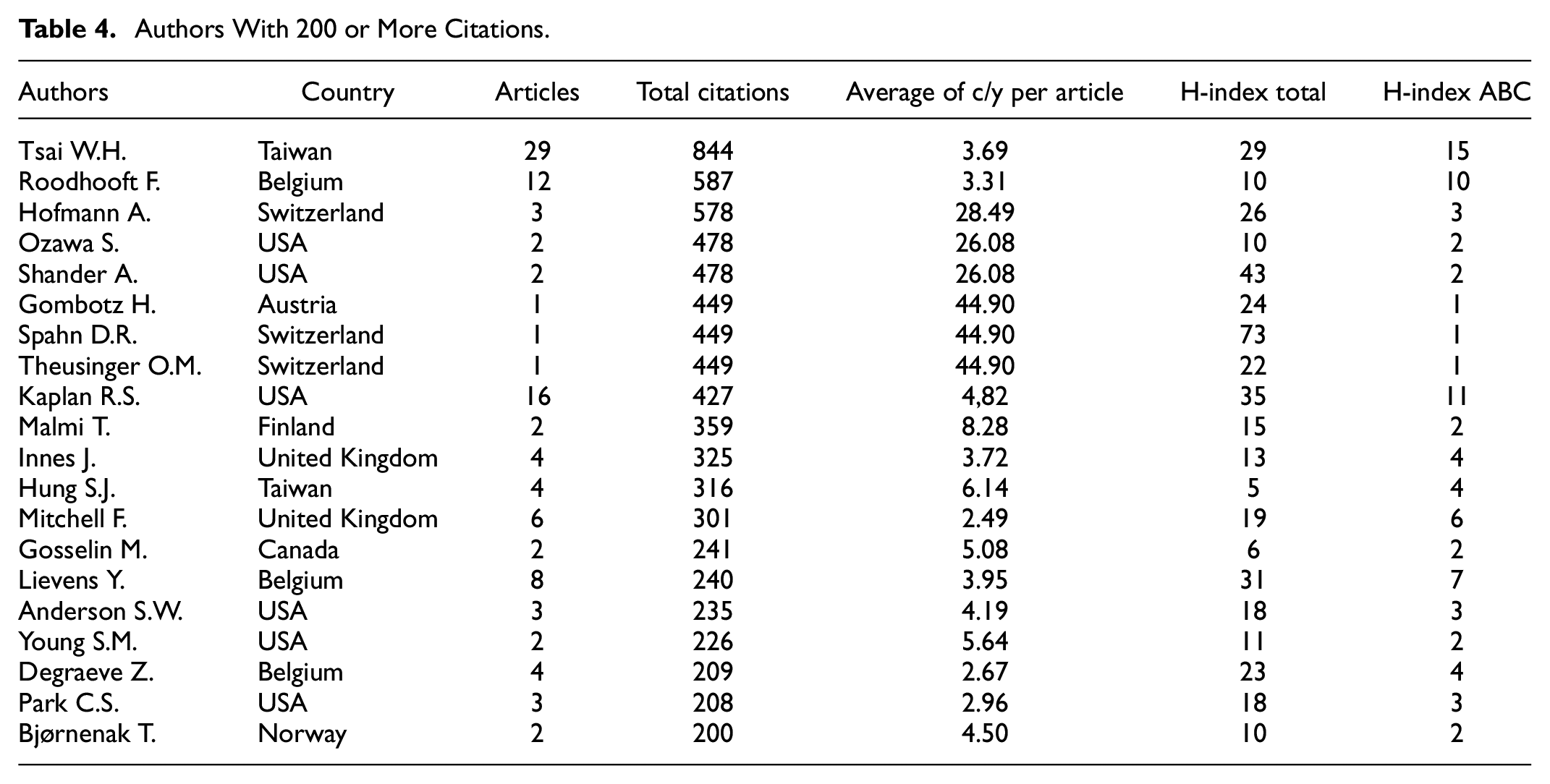

On the other hand, considering the citations as the unit of analysis instead of the number of publications is observed that 20 authors received more than 200 (Table 4), a significant number to guarantee the impact of an author on a topic (Niñerola et al., 2019). As in the previous analysis, Tsai, W.H. ranks first, with 844 citations and 29 articles, followed by Roodhooft, F., with 587 citations and 12 articles. Notably, authors such as Hofmann, A., with three papers, Ozawa, S. and Shander, A., with two, and Gombotz, H., Spahn, D.R., Theusinger, O.M. with only one, occupy the following places regarding the number of citations. It highlights their high impact with few articles. Also, it must be noted that the number of total citations is not directly related to the average annual citations per article that authors received.

Authors With 200 or More Citations.

Again, from these 30 authors, those from the US are the most cited, followed by Swiss (with 1476), Taiwanese (1160), and Belgian (1030).

Regarding H-index analysis, the highest H index of the most cited authors is 73. Spahn, D.R hold it. On the other hand, concerning only ABC papers is 15. It corresponds to Tsai, W.H. Comparing both indexes (total and ABC), it can be deduced that the area of management accounting, at least in the specific case of ABC, receives fewer citations on average than other research areas.

Besides the descriptive analysis of authorship, a relational analysis of co-authorship was conducted. The co-authorship analysis aims to identify authors working together to see the field’s degree of collaboration. We found 149 authors that have published at least three articles. We use a threshold to ensure they are highly interested in the topic and have not used it only circumstantially.

The co-authorship analysis reveals that 37 related authors (Figure 6) form 7 clusters with a minimum of 3 authors in each one. The first cluster (red) is led by Tsai, W.H., the author with the most articles published on ABC (29) and the most cited. Authors from this cluster have mainly published articles on ABC and decision models related to sustainability, the green economy, carbon rates, and the environment in different sectors. The second (green) has mainly published articles on TDABC in the health field, especially cancer. The third (dark blue), led by Roodhooft, who is the fourth author in the number of articles (12) and citations (587), has published mainly on ABC and decision models, mathematical programming and also on ABC and TDABC in the medical field. The fourth (yellow) has been dedicated to publishing conceptual TDABC works and cancer-related empirical studies of kidneys and the prostate. The fifth (purple), with Kaplan, R.S. at the fore, who is second in the number of articles (16) and citations (427), includes publications of both conceptual and empirical articles basically in the health field (treatment of children’s diseases, arthroplasties, spine, among others). The sixth (orange) has been related to TDABC applied to libraries. Finally, the seventh one (light blue) applied TDABC to health and, more specifically, to maxillofacial surgery. As can be observed, the health sector stands out above any other sector.

Co-authorship analysis.

Geographical Analysis

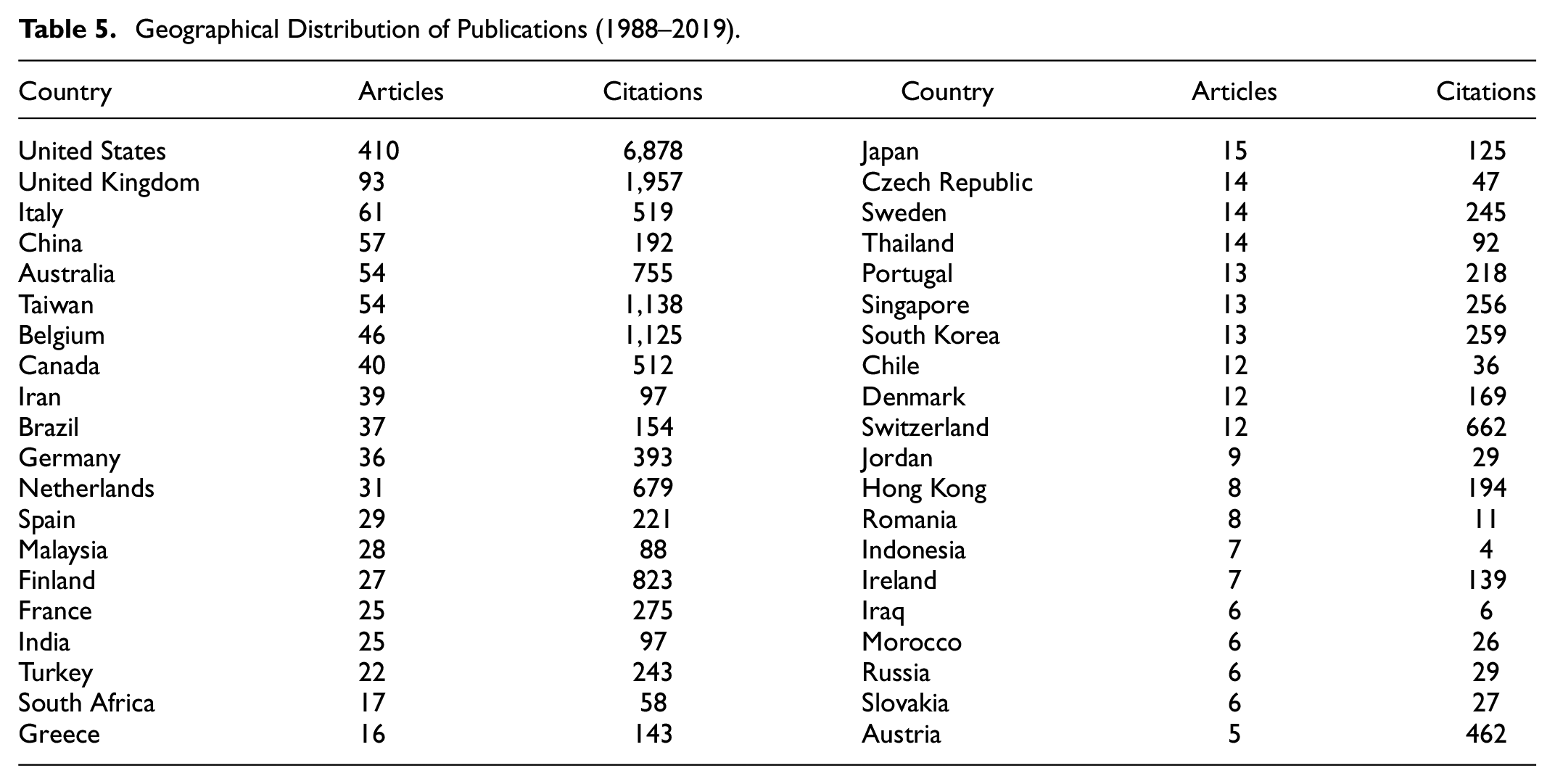

The 1,260 articles in the analysis have been written by authors affiliated with universities from 83 countries. There are 30 countries whose universities published at least ten articles on ABC. It shows that ABC caught the attention of research worldwide (Table 5). As expected from previous analyses, the first country in the ranking is the United States, with 410 documents and 6,878 citations. The United Kingdom and Italy follow it in the number of publications. As Jones and Dugdale (2002) indicated, developments in ABC research were expected to be found mainly in the US since the entrepreneurs of ABC reside in the US, and the development of ABC was, at its beginnings, a response to the emergent manufacturing environment in the US (Jones & Dugdale, 2002).

Geographical Distribution of Publications (1988–2019).

However, these results do not coincide with Fitó Bertran et al. (2018) because they only study the literature published in the Management Accounting Review, an English journal specialized in the field. In this case, the UK was in first place (22.92%), followed by Scotland (12.5%) and the US in third place (12.50%). Previously, Bjørnenak and Mitchell (2002) reached the same conclusion when analyzing specific UK journals. Again, they found UK authors were in the first place (44%) followed, in this case, by US authors (23%). In contrast, our finding is consistent with Terzioglu and Chan (2013), that analyzed 77 articles on ABC until 2011. The US, UK, and China authors are the most prolific in their review. Moreover, we can find some developing countries in Table 5, such as India, Brazil, and Malaysia. This fact shows the attention that ABC has achieved worldwide, not only in developed countries.

Keyword Analysis

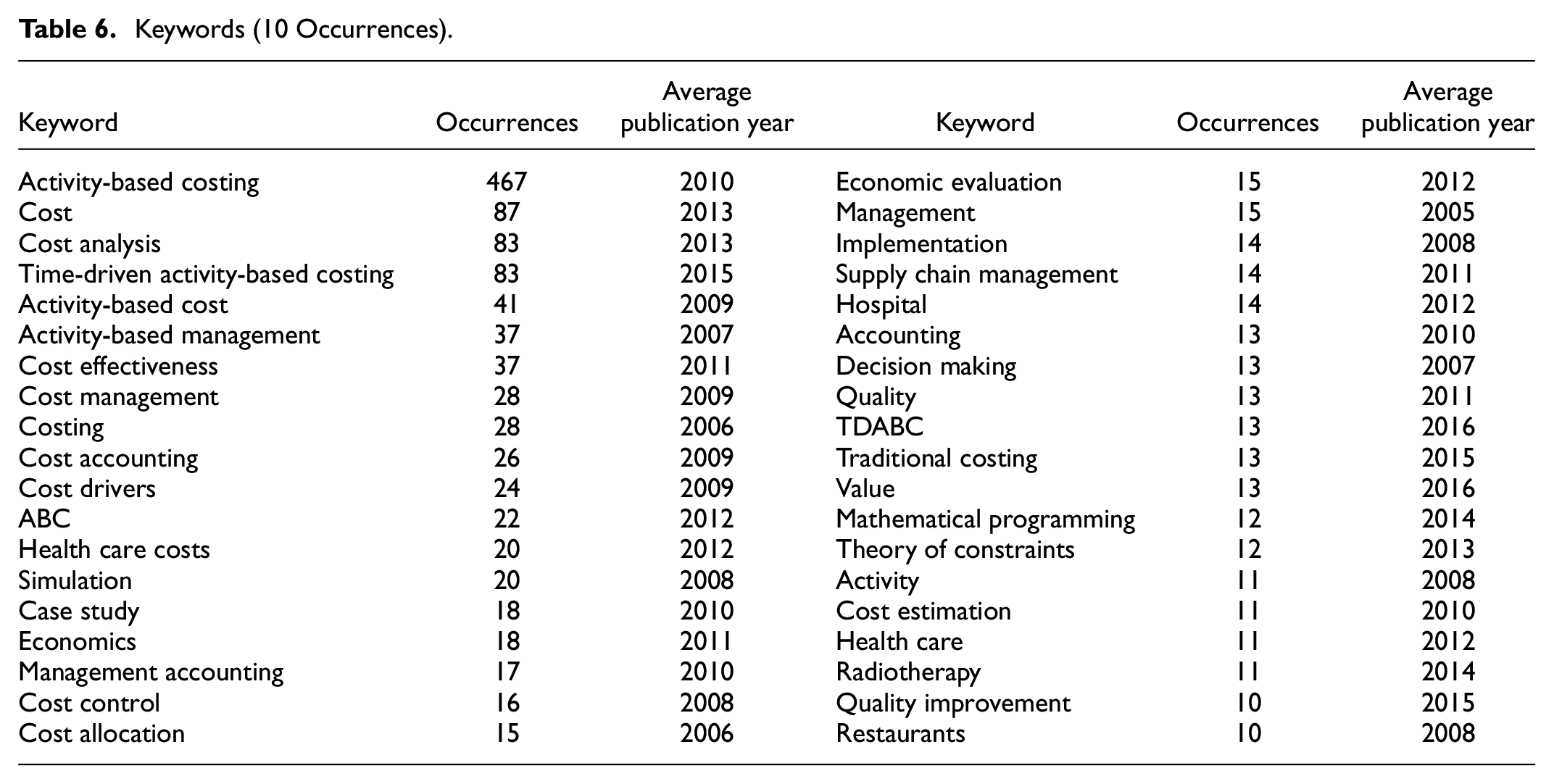

In all articles, authors use keywords to give insight into their work. These keywords are related to the topic, the methodology used, the application sector, the country of implementation, and so on. In this review, 2,325 different keywords have been identified. Thirty-eight of these words appear at least 10 times, 86 appear 5 times, 128 appear 4 times, 211 appear 3 times, and 427 appear 2 times.

Getting an overview of what is happening in the research field through keyword analysis is possible. Among the most repeated, as it could be expected, we find “activity-based costing” in the first place with 467 occurrences, followed by “cost,” with 87, “time-driven activity-based costing,” and “cost analysis,” with 83 each (Table 6).

Keywords (10 Occurrences).

Eighty-six keywords have been analyzed according to when they were used (five-time occurrence is the VOSviewer default value). Seeing the evolution of the keywords, it is possible to identify trends in the field. In this sense, Activity Based Costing, the most repeated one, was more frequent in the past than at present. It is the same for cost-related keywords, such as cost control, cost allocation, costing, product costing, profitability, or other concepts like restaurants, simulation, process, outsourcing, management, diffusion, implementation, and cost drivers. All of them were more used in the first years of the study.

On the contrary, TDABC, Time-Driven Activity-Based Costing, Value, Health Care Value, Health Economics, and Tuberculosis, are more present in new articles. This fact gives clear evidence that ABC system was more focused on the costing process or their profitability at the beginning. However, lately, the objective has turned to its applicability, especially in the health sector, with the new extended TDABC system. These results may be complemented by analyzing the objectives of the ABC articles developed below. So far, these results seem to show the evolution and the direction of the research in the field.

Research Methods

It has been used a broad range of methodologies for addressing ABC research. Following the classification proposed by Bjørnenak and Mitchell (2002), our results indicate that the papers included in the review mainly use case studies. Seven hundred forty-four articles (more than 50%) used this methodology, including multiple sources of evidence such as observations, data from the company databases, participation in the companies, and so on (Lueg & Storgaard, 2017) (Table 7).

Research Method Evolution (1989–2019).

Source. Own elaboration.

Note. The total in the table is different from the total number of articles analyzed because some articles use more than one research method.

This result does not coincide with Fitó Bertran et al. (2018). The survey was the first research method in their study, with 37.50%, while the case study was in second place, with 27.058%. However, their study only focused on one journal: Management Accounting Research, so it seems this journal was more interested in surveys. Also, it contrasts with Bjørnenak and Mitchell (2002) obtained based on an analysis of only 10 academic research journals. The survey was again the first research method (20.8%), followed by theoretical concepts, developments, and mathematical modelling. In fourth place, they found case studies with 15%. Also, Terzioglu and Chan (2013), who studied 77 articles published in accounting journals, concluded that the survey was the most used research method. They did this study during the period 2001 to 2011.

Nevertheless, the predominant research method was the case study method in Lueg and Storgaard (2017) on articles focused on adopting and implementing the ABC system. Also, Zawawi and Hoque (2010) indicated that in their review, the percentage of case study research had increased compared to Shields’ review (Shields, 1997). In fact, the case study research method is paramount to better understanding cost systems and the change that their implementation implies in companies (Zawawi & Hoque, 2010). Overall, we can conclude that accounting journals are less prompt to publish case studies than journals of other fields, such as engineering, health, or energy.

On the other hand, 205 papers in our database propose or analyze a model, 188 are conceptual, 176 use secondary data for applying statistics, 108 use a questionnaire, 13 are literature reviews, and 10 are simulations (Table 7). Our findings suggest that previous reviews were limited in the number of journals analyzed. They excluded many publications in other professional journals that may be more interested in the diffusion of real case studies. Moreover, case studies have been published more in the last 10 years than at the beginning of ABC.

The application of ABC in many different economic sectors is evident, as reported in the literature (Bjørnenak & Mitchell, 2002). We can draw some conclusions by analyzing deeper where case studies have taken place (industry) and considering that not all the articles deal with one sector. In this sense, some papers include more than one (27 articles).

As shown in Figure 7, the application of ABC has been mainly in the health sector. Five hundred thirty-three papers (42.3%) are implementations or discussions of the method in this sector. The ABC has been wildly used in health to determine the cost of a process or a treatment providing valuable information for decision-making (Vargas Alves et al., 2018). Manufacturing is the second most important ABC application industry to achieve greater efficiency with 294 papers (23.3%). On the contrary, in services, logistics and other sectors are sparingly applied.

Sectoral distribution of the case studies.

These results contrast with the conclusions of the bibliometric review of Terzioglu and Chan (2013) and Lueg and Storgaard (2017). The first two authors concluded that the manufacturing sector and surveys were the most used sector and research method in ABC, followed by the case study. Lueg and Storgaard (2017) studied 27 articles focused on adopting and implementing ABC from 1989 to 2015. The majority of these articles included organizations in the manufacturing industry. The explanation for these facts may rely on the period, and the number of articles analyzed. The first authors included papers from 2001 to 2011, and the second ones only studied 27 articles. The present review extends the period until 2019 and starts before and analyses 1,260 articles. There have been many implementations during this time, especially in health, using case studies and TDABC. That is seen in the keyword analysis, where health care value and health economics appear recently. Keel et al. (2017) raised the interest in gradually implementing TDABC in the healthcare system. ABC and TDABC are cost systems that can help analyze the cost of value in health (Vargas Alves et al., 2018).

Objectives

In this section, a content analysis of the papers is carried out to identify the objectives pursued in each article (one article can focus on only one objective or more than one). To guarantee the results’ consistency, two authors were independently working on the open coding process to identify the objectives.

“Determine costs” is the most repeated objective of the articles on ABC, as it is the biggest node in Figure 8 with 968 articles. The most cited articles with this objective are Ben-Arieh and Qian (2003) with 149 cites; Kim et al. (1997) with 158; Shander et al. (2010) with 449 (with an average of 45 c/y); Tsai and Hung (2009a) with 173. This objective is directly related to “decision making” (with 167 articles), “procedure costing” (with 130 articles), “cost savings” (with 121 articles) or “comparison with traditional cost systems” (with 84 articles), according to the links between nodes that represent co-objectives in the papers.

Main objectives evolution.

With “decision making” as one of its main objectives, the most cited articles with are Kee and Schmidt, (2000); Kim et al. (1997); Roodhooft and Konings (1997) with 99, 158, 99, and 137 cites, respectively. With “procedure costing” we find Laviana et al. (2016) and Tsai and Hung (2009b) with 75 and 173 cites, respectively. The more cited articles focused in the objective of “cost savings” among others are Cobb et al. (1995) and LaLonde and Pohlen (1996) with 99 and 79 cites, respectively. Finally, the most cited papers of “comparison with traditional cost systems” are Baykasoğlu and Kaplanoğlu (2008), Ben-Arieh and Qian (2003), and Lievens et al. (2003) with 74, 149, and 106, respectively.

The average year of publication seen through a color scale shows the evolution of the objectives (Figure 8). Objectives that appear at the beginning of the period (dark blue) are: comparison with traditional cost systems, overhead costs allocation, product design costs, capital investment valuations, and capital investment decisions. That result mostly coincides with what we obtained with the most used keywords in the early years of the analysis.

On the contrary, time identification, time process determination, value, cost-effectiveness, product mix optimization, strategic management, effectiveness, carbon emissions costs, and supply chain management are objectives of the most recent papers. Therefore, ABC is nowadays used for sustainable and strategic management, as new research areas for this cost system, and especially its simplified version, TDABC, as the time is recurrently calculated.

Meanwhile, objectives such as determining costs, saving costs, decision-making, pricing, calculation of cost variation, and quality improvement have been maintained or widely researched in the middle years. It makes sense since the ABC system pursues cost calculation in companies, and these objectives are directly related. A special mention of the healthcare sector is needed, where more real experiences of ABC and TDABC implementation have been published. This fact can be due to the need and interest of health centers in having relevant information about the cost of treating certain diseases, such as cancer, or specific surgeries. Not all countries have a national and public health system subsidizing these services. For this reason, cost information is relevant to ensure sufficient revenue.

Finally, all these objectives were classified into 12 categories following the similarities with those proposed by Innes et al. (2000) and Kuo and Hang (2014). In addition, three authors discarded duplications, discussed discrepancies, and ensured the validity of their classification.

Results show that the primary category was stocks valuation identified in 997 articles (Table 8). This is coherent given ABC is a costing system and the main objective of it is to determine the costs of products and services. Moreover, Table 8 also includes the most cited paper in each category, Shander et al. (2010). The Stocks valuation category includes the most cited paper with 449 citations in total and 44.9 cites per year (Shander et al., 2010). So, we can affirm that determining the cost is the main interest of authors when using ABC. In the second place, we find cost Modelling category with 482 articles, and activity performance and quality measurement and improvement occupy the third with 315. Although other categories of objectives have less articles, we would like to mention Decisions and strategy (200), Cost reduction, cost management and cost control (197), ABC or TDABC implementation (159), Profitability and customer profitability analysis (159), Product and service pricing (113), Time reduction and time management (100) as they have more than 100 articles published. Nevertheless, the high number of links of the publications’ objectives and their variety indicates the great interest that the development of ABC has maintained over time.

ABC Objectives Categorization.

Taking into account the previous keyword and objectives analyses developed in this review, and also with the evolution proposal made by Gosselin (2007), Kuo and Hang (2014), Fitó Bertran et al. (2018) we raise the following evolution of the literature on ABC that is included in Table 9.

ABC Stages in Literature.

Source. Own elaboration.

The evolution of the literature about ABC has gone through different stages. We identify first (late 80s to early 90s) the beginnings of ABC, with definitions and specific functions of this cost system. Later (early 90s to mid 90s), some literature focused on ABC’s validation and methodology. After that (the mid-90s to 2000), much literature is published on ABC’s implementation process and diffusion. Although, case studies focused on real implementation cases continue to be published today, especially in the health care sector. After 2000s some other contents appear in the literature of ABC as management decision-making, risks and benefits assessment, society and social behaviors of ABC’s development process, and so on. A special mention is required to the appearance of TDABC as the ABC’s evolution which caught the attention of researchers and professionals and represented a revolution in the field of cost management. For each stage, some of the most remarkable objectives have been included in Table 9. Anyway, they could also be found in publications of other stages. Obviously, the limits of these stages can not be accurate.

Conclusions

The present article aims to review articles that use ABC indexed in the Scopus database to confirm that the ABC system is based on a solid theoretical model applicable to companies of different sectors. This is analyzed by means of a systematic literature review.

First, previous literature reviews on ABC, such as Staubus (1990), Shields (1997), Gosselin (2007), have been analyzed. However, looking at reviews that only include ABC, not other cost methods, the last published covers the period until 2011. It is a bibliometric study of only 77 articles (Terzioglu & Chan, 2013). Therefore, our first contribution is the period analyzed; more than 30 years (1988–2019), from the beginning of ABC system. The review includes 1,260 articles on ABC and its latest simplified version TDABC. Considering that the broadest literature of ABC carried out previously analyzed 404 articles (Bjørnenak & Mitchell, 2002), the volume of articles included in this review is the second contribution. In our opinion, this volume gives a greater significance to the results.

This work provides an updated review of the developments carried out on ABC during a long period of study. It shows how the ABC system is well established in the literature. Some articles are published in relevant journals from different fields, highlighting that it remains interesting for academics and professionals. However, results suggest that journals with a professional and multidisciplinary approach are more interested in publishing articles using ABC than journals in accounting. This may be because ABC has had such wide acceptance and implementation in many sectors.

Our review’s different results help academics conduct future studies that build systematically on previous research and if they are interested in learning about literature reviews. For accounting and management professionals, it helps to easily expand knowledge and coverage within their economic sector and assess the most common goals of ABC implementation. It provides a frame of reference with valuable information about the possibilities and objectives of ABC implementation in all types of companies. Also, it allows both to keep updated with the developments and especially the trends of ABC and TDABC systems.

More specifically, our results contribute to the literature on ABC in different ways. First, they can provide useful information for professionals, business managers, and academics since there are a large number of professional authorship. These professionals (practitioners and consultants) provide a broader real view of the implementation cases of ABC in terms of highlighting problems encountered and overcome, providing practical details of the process, and so on. These professionals are expected to contribute to scientific articles that are practical and useful for other professionals. This can interest academics because it brings them closer to the real business world and also for other professionals who can learn from these experiences. There is a growing interest in the ABC cost system, especially its simplified version TDABC. In this sense, the research has been conducted mainly through case studies in different sectors. Healthcare and manufacturing are the economic sectors with more applications, which have grown recently. This fact corroborates that the ABC system currently has a solid theoretical basis and is applicable to different organizations. In addition, in an economically unstable and inflationary context, the ABC system can be even more attractive for companies since it provides detailed and valuable cost information for decision-making.

The most prolific authors are from the US, followed by Taiwan and Belgium. Therefore, it is not surprising that the US is the leading country in terms of the number of papers and citations. United Kingdom, Italy, and China continue the ranking in the number of articles on ABC. Nevertheless, authors from 83 developed and developing countries have published articles on ABC. This result confirms the broad scope of the diffusion and acceptance of ABC. Besides the long period included, another relevant contribution of this study is its broad methodological approach, including a systematic and bibliometric revision that involves descriptive, relational, and content analyses. The content analysis shows that, over the years, the main objective of the articles on ABC has been the stock valuation, identified in 997 articles, followed by designing cost models and improving and measuring the performance and quality of the activities. These results could be expected as ABC is a cost system and confirms again that publications are interested in this central aspect. On the other hand, looking deeply at when the objectives were settled, not all of them are being researched nowadays.

Articles previously focused on comparing ABC with traditional cost systems, allocating overhead costs, calculating product design costs and others related to capital investments. On the contrary, the objectives currently focus on identifying times of activities and processes, quantifying the value, cost-effectiveness, and issues related to the environment and sustainability. These issues indicate the lines for future research on the topic.

Despite the review’s extension and contributions, using a single database should be mentioned as a limitation. Although Scopus has excellent publication coverage (over 23,452 peer-reviewed journals) from different fields (Life Sciences, Social Sciences, Physical Sciences, Health Sciences), other sources can always be an extra contribution. However, many articles’ overlap between databases (Martín-Martín et al., 2018).

There are still some aspects of the publications on ABC that could be deeper analyzed. Therefore, as future research lines, we can mention: a deeper literature review of ABC and TDABC focused mainly on the health sector since there is a large number of case studies already published, a meta-analysis of this literature to show which variables influence their impact measured traditionally (databases where the publication is indexed, quartile, impact factor, etc.) or almetrics values (impact measured as the number of shares, readers or likes, for example in Facebook, Instagram, Twitter, etc.) to know the impact get in social media as an alternative channel of diffusion of this innovative management tool or references managers like Cited U Like or Mendeley or usage metrics.

Footnotes

Author Contributions

All the authors designed the research. A.N. and M-V.S-R collected the data. A.N. and A-B.H-L performed the analysis of data. Finally, the paper is written by A.N., A-B.H-L, and M-V.S-R.-L. All the authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.