Abstract

Tax and economy go hand in hand, and whenever any overhaul in tax structure takes place, it becomes essential to evaluate its effect on its sector and concerned businesses. The present study examines the effect of Goods and Service Tax (GST) on Indian Micro, Small and Medium Enterprises (MSMEs) business performance. Data were collected through a structured questionnaire from 404 registered MSMEs. The partial least square equation modeling results emphasized an overall positive impact of GST on business performance. The path model demonstrated that determinants of GST- change in the tax system, technology transition, and tax awareness and knowledge have enhanced the performance in terms of ease of doing business, operational efficiency, and increased profitability and have reduced the working capital blockage of funds. However, in contrast, the GST compliance system has increased the compliance burden on the firms, which harmed their performance. Further, the study examined that MSMEs’ size, turnover, and form impact the performance through the GST compliance system of the enterprises. The results may benefit the policymakers and other emerging economies in focusing on the tax reform factors which enhance the performance leading to better economic growth in the future with the support of MSMEs’ better performance.

Introduction

Tax reform is a systematic step to curtail fiscal imbalance and create a stable environment for the economy to function smoothly and achieve economic growth. Tax policies play a significant role in innovation, harmonizing and rationalizing trade mechanisms and promoting investments, which leads to higher revenues (Ahmad & Stern, 1991; Dyreng et al., 2020; Gale & Samwick, 2014; Ngwaba & Azizi, 2019). The objectives of a tax policy or system could be achieved with the support of public or private sector enterprises (De Paepe & Dickinson, 2014; Long & Miller, 2017). Tax reforms through better business tax design influence a business’s formation, expansion and operation. Tax policies impact business investment decisions and strategies (Hassett & Hubbard, 2002; Higgins et al., 2015; Miles & Snow, 2003). They helped lower the tax on business, became moderators to modernize business operations with the introduction of new technology and paved the way to expand businesses globally (Guziejewska et al., 2014; Masso et al., 2013).

Businesses have the potential to enhance economic growth and efficiency through better performance (Hines, 2017) as they contribute directly to the economy by providing valuable goods and services (Doner & Schneider, 2000; Jones-Smith et al., 2020). Among these enterprises, micro, small and medium enterprises (MSMEs) hold a key position as they constitute 90% of world businesses (Asian Development Bank Report, 2020; World Bank Report, 2021). They have more growth potential than large units in terms of increased sales, profits, and productivity (McKenzie & Woodruff, 2017). They are the largest generator of employment globally; 7 out of 10 jobs are created by them (U.N. Report, 2021; Harvie, 2008, 2015).

The expansion of the MSME industry worldwide led to the propagation of research on them. MSMEs are the most responsive to reforms, particularly to national tax reforms, due to limited economies of scale (Ocheni, 2015). Different implications have been observed in the MSME sector in different countries after tax reform. Freudenberg et al. (2017) empirically verified that business firms had gained cash flow benefits after tax reform, particularly small firms of Australia. Plesko and Toder (2013) recorded an increase in tax burden by businesses in terms of their revenue loss due to changes in tax rates in the United States. Even small firms’ entrepreneurial activities have shown a sensitive effect on tax reforms in generating and utilizing tax benefits (Cullen & Gordon, 2006). Malaysian and New Zealand firms faced compliance challenges after reforms in the tax system (Buchan et al., 2012; Ramli et al., 2015). Other tax reforms’ impacts were evaluated on MSME’s trade (A. K. Sinha et al., 2021); compliance behavior, and costs (Inasius, 2019; Matarirano et al., 2019). Policymakers, academic economists, and the government are at a standstill in the fiscal policy debate regarding the effect of tax regime reform on business performance. In recent times, the focus of policymakers has shifted from revenue generation to better performance of the business, which ultimately influences economic growth (Greene, 2021; Hines, 2017).

The present research has been conducted in one of the world’s developing countries- India, which reformed its indirect tax structure on July 1, 2017, by implementing Goods and Service Tax (GST). To our knowledge, the literature is short on what is the impact of GST on MSMEs’ business performance-financial and operation. What is the path through which different changes in tax regime affect the business? What are the different aspects of the GST taxation system that affect the business?-need to be addressed. Hence the present paper explored the effect of GST on the business performance of MSMEs. Furthermore, MSMEs in India play a dominant role as they contribute around 95% of the industrial output, 29% to the Gross Domestic Product (GDP), and 49% to the exports. They gained net foreign exchange earnings of INR 343,743 million in 2018 to 2019 compared to INR 171,706 million in 2017 to 2018 (MSME, Annual Report 2020-2021).

Further, we have selected one of the industrial states from North-Punjab for our study. In 2019 to 2020, Punjab’s MSMEs showed an increase in the growth rate of 5% in economic activities and 10% in employment generation. Further, they contributed 26.66% to Gross State Value Added. By 2019, the MSME sector has shown overall progressive growth in Gross Capital formation of 14.1% in the Gross State Domestic Product (Economic and Statistical Organization, Punjab 2019-2020, retrieved from https://esopb.gov.in). Moreover, MSMEs play a substantial role in India’s social and economic development by assuring a balanced income and wealth distribution approach, enhancing employment opportunities and regional development through industrialization in backward regions. Therefore, foreign investors remain interested in investing in the MSME sector and the study may provide them with empirical results to play safer bets after the reform in the tax system.

Based on the survey conducted on Indian MSMEs, we examine the impact of GST on their business performance. This paper has several contributions to existing literature and practice. Firstly, this paper evaluates the direct impact of the change in tax system compared to the previous tax system on business performance, which is one of the significant contributions of this research strand. The restructuring of the tax system eliminates loopholes and inviolable preferences, which occurred in the previous tax system (Pechman, 1987). It is essential for policymakers to learn the effect caused by the new system to analyze whether the objectives of reform are achieved.

Secondly, the impact of the GST compliance system and its burden on business performance are examined. Past studies observed the effect of tax reform on tax compliance (Claus, 2014; Peprah et al., 2022), compliance cost (Sandford et al., 1989) and the attitude of taxpayers toward tax compliance (e Hassan et al., 2021). However, to this date, how the tax compliance system after tax reform affects business performance remains untouched, which is the key contribution of the present research.

Thirdly, the study examines the impact of the technological transition that occurred in GST. When the government initiates reform, it takes every possible step to bring technological advancement and innovation. I.T. innovation provides opportunities for businesses to expand globally (Caniëls et al., 2015; Dahnil et al., 2014). The Indian government took the initiative to launch a tax portal, Goods and Service Tax Network (GSTN), to lend an easy hand to administer tax matters to all taxpayers (Sury, 2019). The study contributed in evaluating the effect of technological transition in GST on the business performance of MSMEs.

Fourthly, the study examined the impact of tax awareness and knowledge on performance levels. Firms invest in human capital to gain in innovation and earn higher profits as defined by human capital theory (Becker, 1960). Therefore, when the reform is implemented in a country, skill training coupled with tax awareness and knowledge programs are provided by business entrepreneurs. Tax awareness and knowledge reduce misconceptions and negative perceptions about the new tax system (Eriksen & Fallan, 1996; Lewis, 1982; Mei Tan & Chin-Fatt, 2000; Vogel, 1974). In addition, it helps a business to follow and implement the system in its operations and enables them to abide by tax laws.

The paper focuses on this new aspect of Goods and Service Tax and business performance. We expanded the literature on business performance by examining the impact of change in tax system, technology transition, tax compliance system, compliance burden, and tax awareness and knowledge. In addition, the study also contributes to the effect of firms’ characteristics of MSMEs (size, turnover and form- partnership, companies, proprietorship firm) on tax compliance system. Finally, it demonstrates how increase or decrease in turnover, change in size and forms of units influence the compliance mechanism, which ultimately affects the performance level.

The empirical findings may benefit the government and other developing countries in understanding the different aspects and determinants of GST that might impact business performance. In terms of future research work, it is essential to identify how indirect tax system (GST) indicators impact business performance, which in turn might influence the economies’ business cycles. In addition, the results from the present research strand may assist the government of other countries, which are planning to adopt the same indirect tax structure in the near future, or alterations in their tax structures.

Literature Review and Hypothesis Development

The business performance measure (BPM) system is considered an essential tool to identify the key factors of the transition of the systems that may influence the business performance of micro, small and medium firms, especially in many research areas related to business and social science studies (Franco-Santos et al., 2007; Mann & Kehoe, 1994). The system suggests the critical elements of implementing a new system that impact the performance are strategic assessment, technological support, the transition to new processes, functional design for education, and compliance of recent changes (Mulhearn & Vane, 2020). Such a framework is based on the fact that a single implementation factor cannot solely impact business performance. A combination of different factors is required to give a more balanced depiction of the unit’s overall impact on its business performance after implementing GST in India. Based on the factors identified by the BPM system, the key determinants of GST implementation impacting business performance are- change in the tax system (the transition to new processes), technological transition for tax system (technological support), GST compliance system (compliance of recent changes), tax awareness and knowledge (functional design for education).

The paper’s literature review explores the studies related to tax reform and business performance. It depicts the relationship between business performance and key GST determinants adopted for the study. The GST determinants, namely, change in the tax system, technological transition for tax, GST compliance system, compliance burden, and tax awareness and knowledge. These determinants are based on established theories (explained in detail below, in the literature of each factor separately). Further, the firms’ characteristics studies with regard to performance are also described. The literature and relationship of each GST determinant with business performance lead to hypothesis development.

Change in the Tax System

Tax reform is a policy implementation by which alterations and amendments are made in the tax system to reduce inefficiencies, overcome the loopholes of the prevailing tax regime and boost the country’s economic growth by generating higher revenues (Bekoe et al., 2016; M. G. Rao, 2006; Vasanthagopal, 2011). Further, the change in tax system is done to remove the inefficiencies and distortion in its economy (Theory of Optimal Taxation) (J. Slemrod, 1990).

In India, the indirect tax structure perceived a shift from Value Added Tax (VAT) to Goods and Service Tax on July 1, 2017. Under the VAT system, different tax rates existed for the same product in different states. It led to a complex tax system, hard to manage and even harder to claim tax credits for the products- manufactured and sold inter-state (Sree Kantaradhya, 2000). GST implementation brought uniformity in the tax rates for all the products throughout India (Khoja & Khan, 2020; Sury, 2019). VAT led to complexities and unorganized administrative costs (Aruna, 2019). In addition, the VAT system in India was prone to double taxation (Singh, 2017; Vasanthagopal, 2011).

Past studies conducted in different countries where a similar indirect tax structure was applied confirmed different implications of GST on business performance. It brought evenness to the tax structure and broadened the refund mechanism (Hoseini & Briand, 2020). It has helped in reducing the tax burden of end-users and producers, both of which led to the balanced growth of the economy through centralized distribution. It has encouraged investments and savings (Narayanan, 2014).

The related hypothesis is:

H1: Change in tax system positively affects the business performance of MSMEs.

Technology Transition for Tax

MSMEs in emerging market economies are marching toward market integration and eliminating national boundaries, and technological advancement has increased. Bird and Zolt (2008) opined that technology resolved many issues of businesses, such as fraud and unwanted administrative costs. Technology led to the e-filing of registration and tax returns and has lessened the firms’ burden (Barbone et al., 2012) as paperless compliances save the time of firms and organizations (Ojha et al., 2009). Through technology and smart automation, the workload of administration and businesses has decreased drastically (Gerger, 2019).

Neirotti et al. (2018) observed that technological transition had opened gates for MSMEs to expand globally. Technological developments are made for the easy mobility of funds and their global reach (Eichfelder & Schorn, 2012). However, in the past, SMEs have shown a slow adoption rate, which led to unsuccessful I.T. implementation due to limited I.T. skills, strategy, lack of access to capital resources, and costs of installing the new system (Nguyen, 2009; Rahayu & Day, 2015; Sugiharto et al., 2010). The Indian government took the initiative to incorporate a special tax portal- Goods and Service Tax Network (GSTN), which needs to be evaluated regarding the business performance of MSMEs. A few recent studies on GSTN concluded that it had increased the installation cost as an up-gradation of the accounting system, and a change in the documentation process is required by the firms (James Mary et al., 2020).

The related hypothesis is:

H2: Technological transition positively affects the business performance of MSMEs.

GST Compliance System

When a change in the tax system is done, the operating framework for its compliance also changes. MSMEs are required to change and install a new compliance system and strategies (Digal, 2020). Past studies revealed that MSMEs’ indirect tax compliances (GST) demand more time than direct taxes such as income tax, personal tax, or capital gains (Hansford & Hasseldine, 2012). To comply with tax rules, regulations and laws, SMEs rely on external sources such as auditors, tax consultants and lawyers. It adds up to additional costs in professional fees, audit fees, consultation charges etc. (Eichfelder & Vaillancourt, 2014; Hanefah et al., 2002; Sandford et al., 1989). A comparative study done in Australia by (Pope & Mohdali, 2010; Tran-Nam, 2000) observed that under the GST tax regime, tax compliance cost is higher in comparison to the VAT and sales tax system.

GST impinged the documentation, accounting system and compliances of SMEs in Malaysia, Australia, and New Zealand (Breen et al., 2002; Evans et al., 1996; Gunz et al., 1995; Siddiq & Sathya, 2017). As a result, it has consumed more time to comply with the new compliance procedures, thereby increasing the burden. Moreover, the complex system might hamper the expansion of business and breeds ground to tax evasion and corruption (Vashchilko, 2010; Zelekha, 2017). Malaysian SMEs have major complexities in complying with GST procedures. Monthly returns, allocation of GST items and non-GST items, documentation of each good and service under the respective head, and their tax rates have consumed much time due to which the business has suffered (Kannaa, 2015).

The related hypothesis is:

H3a: GST compliance system negatively impacts the business performance of MSMEs.

Compliance Burden

The change in the compliance system- its rules, regulations, number of returns and documentation process demands personnel training and advancement in the accounting system. It has consumed much time of the firms, which augmented their burden (CChen & Taib, 2016; Nagel et al., 2019; Siddiq & Sathya, 2017). Compliance burden refers to the valuation of time and effort to comply with the changed compliance system after the tax reform (J. B. Slemrod & Venkatesh, 2002). In the PriceWaterCooper Report (2011), it was observed that firms spent 39% more time complying with the system in the U.K. when complicated and ambiguous tax rules existed. Further, it was observed that when multiple tax systems existed, the firms spent 31% extra in adhering to different tax systems compared to single consolidated systems. So, in the present study, firstly, the impact of the compliance system is evaluated on the time firms spend (compliance burden) to evaluate whether the compliance system has increased the burden. Later, the impact of compliance burden is examined (as a mediator) on business performance.

The related hypothesis is:

H3b: The compliance burden (time spent) has a negative impact on the business performance.

Tax Awareness and Knowledge

A successful implementation of tax reform in businesses and the economy demands proper awareness and knowledge about it. Tax knowledge is the fundamental reason due to which all taxpayers (individuals, companies, associations, etc.) comply with taxation rules, as it leads to lawful compliance and implementation of taxation policies in their business as they know the consequence of their action, that is, after-effects in the form of penalties and fines (Theory of Reasoned Action) (Rahmayanti et al., 2020).

Tax knowledge includes general and technical tax knowledge regarding the tax system and its compliances (Bornman & Ramutumbu, 2019; Wong, 2015). Imperative studies have shown a strong positive impact of tax knowledge on business. It helps SMEs to determine accurate tax liability and lead to timely tax compliance (Baru, 2016; Fauziati et al., 2020). As lawful abiding of tax laws after proper understanding leads to lower legal costs due to cut off in fines and penalties (Adam & Webly, 2012; Berhane, 2011; Faizal et al., 2019; Saeed, 2020). Moreover, it prevents the afraid reaction of new reform amongst small firms and enables them to follow GST rules to their advantage (Kanda et al., 2018; Mohan & Ali, 2018). Australian firms suffered a business loss due to insufficient knowledge about the changed taxation policies (McKerchar & Hansford, 2015). Likewise, Loo (2016) and Loo et al. (2014), have observed a substantial negative impact on the compliance behavior of Malaysian firms.

When firms are not fully aware of their tax exemptions, tax subsidies, and tax holidays, they directly hamper their businesses’ growth and profit margins. (Faridy et al., 2014; Freudenberg et al., 2017). Tax awareness and knowledge tend to impact business performance (Bhalla et al., 2022a, 2022b). Firms hire external tax experts and outsource tax-related matters to Big 4 accounting firms with specialized tax knowledge for tax planning to minimize the risk of investments and tax penalties (Empson, 2001; Frecknall-Hughes & Kirchler, 2015; Gracia & Oats, 2012; Mulligan & Oats, 2016; Organization for Economic Co-operation and Development (OECD), 2009). Outsourcing firms’ tax affairs and experts’ consultancy adds to extra costs.

The related hypothesis is:

H4: Tax awareness and knowledge positively affects the business performance of MSMEs.

Firms’ Characteristics

The firms’ characteristics have been found to affect the business performance of MSMEs (Bhalla et al., 2022a, 2022b). Tax reform broadened the economy’s tax base by accumulating a large number of firms in the tax net. Small firms have to get their registrations, tax returns, maintenance of records, and licenses upgraded. So, with a change in threshold limit (turnover prescribed for tax registration), small firms must comply with the new compliance system. This states a direct relationship between turnover and a firm’s tax compliance (Y. Sinha & Srivastava, 2020; Sury, 2019). The regulatory/ compliance burden strain on small firms is greater than on large firms. Choong and Lai (2006) and Saira et al. (2010) examined a relationship between the level of awareness, educational background, communication tools, demographic variance, income, and employment of SMEs.

Research Design and Methodology

The population, sample size and sampling technique applied are explained in Section 3.1, followed by the development of the questionnaire and its constructs in Section 3.2. Further, Section 3.3 demonstrates the research methodology adopted in the present research to achieve the objectives.

Population and Sample Size

The primary data was collected through a structured questionnaire, which was administered to top management personnel of the MSMEs who handle their tax affairs via post, hand, e-mails, Google forms, and personal meetings.

The study has been conducted in one of the emerging states of India- Punjab. Punjab, one of India’s influential states, emerged as a textile industry hub. They are the primary source of India’s woolen production (95%), sewing machine production (85%), and India’s sports goods production (75%). Punjab’s MSMEs contribute around 14.1% to Gross Domestic Product and 26.6% to Gross State Value Added. In addition, they have generated around 1.5 million employment opportunities (Department of Industries and Commerce, Government of India, February 2022). Punjab has a total of approximately 11 lakh registered MSMEs. Based on the population standard deviation at 95% level, the sample size of 581 has been evaluated. A total of 424 samples were collected [70.67% response rate (424/600)], from which we omitted 20 responses due to non-responses. The sample size at 95% confidence based on registered MSMEs as per MSME Report 2017 to 2018 comes to

Further, the sample size has been allocated by applying two-stage sampling techniques. Firstly we divided the population into three strata as the population comprises three types of units (micro, small, and medium). Then based on the number of registered MSMEs, we applied the proportionate random sampling technique on the formed strata. The final sample consisted of 45% small units (182); 44% micro (177), and 11% medium enterprises (45) (refer to Table 1).

Profile of MSME Units.

Source of Definition: Micro, Small and Medium Enterprises Development (MSMED) Act, 2006

Data

Data collected through structured questionnaire are explained in this section, which compromises dependent variable- business performance and independent variables—change in tax system, technology transition for tax, GST compliance system, compliance burden, and tax awareness and knowledge (refer to Section 2).

Business Performance

For measuring business performance, we have used subjective measures as MSMEs are hesitant to reveal their exact figures publically. Furthermore, subjective measures have been widely accepted in various studies conducted by Dess and Robinson (1984), Vij and Bedi (2016), Wall et al. (2004). Further, subjective measures, that is, the perception of the performance, are considered more valid and reliable than actual financial figures as they are comparable industry-wise, sector-wise, and in performance (Dess & Robinson, 1984; Masa’deh et al., 2015). In total, 15 statements were asked from the respondents on ease of doing, working capital, profitability, and operational efficiency on the Likert Scale 1 to 5 (Hoseini & Briand, 2020; Jacobson, 1987; Sury, 2019).

GST Determinants

Change in Tax System

To measure the impact of change in tax system, we asked about their perception of respondents on the transparency, robustness and efficiency it brought. Further, the perception of input tax credit mechanism, prevention of stock leakages and progressive tax system were also asked (Chandak, 2019; Kadir et al., 2016; S. R. Rao, 2017; Silpa et al., 2018; Wilks et al., 2019). Finally, the respondents were asked to rate their responses on a five-point Likert scale (1 = strongly disagree, 5 = strongly agree).

Technology Transition for Taxation System

The technological aspect of the change in the taxation system is related to tax management, filing of returns, record and documentation work (Dey, 2020; Internet and Mobile Association of India (IAMAI), 2016; Lesage et al., 2020). The respondents’ perceptions were asked regarding the technological advancement done in the GST on a Likert scale of 1 to 5. The tax reform launched Goods and Service Tax Network (GSTN), which handled all GST-related matters on a single platform.

GST Compliance System

The perception of respondents regarding the GST compliance system has been measured on the aspects related to assessment procedure, technical jargon faced, hindrance in expansion of businesses, tax administration and non-time costs involved (Breen et al., 2002; Cléroux, 1992; Evans et al., 1996; Gunz et al., 1995; Kannaa, 2015; Pope & Mohdali, 2010; Schmidt et al., 2007; Tran-Nam, 2000). Accordingly, GST compliance perception on business performance is measured on a five-point Likert scaling (1 = strongly disagree, 5 = strongly agree).

Compliance Burden

The compliance burden is measured through the average time spent by the MSME in complying with the GST compliance system. The respondents were asked to rate the time on a four-point scale for training the staff, solving the issues related to tax returns, and managing the queries related to amendments in GST Act at times (CChen & Taib, 2016; PriceWaterCooper Report, 2011, 2017; Sandford, 1995; J. B. Slemrod & Venkatesh, 2002; Tran-Nam, 2000). Here scale used was, 1 = up to 3, 2 = 3 to 6, 3 = 6 to 9, and 4 = 9 to 12 months.

Tax Awareness and Knowledge

The tax knowledge and awareness were measured regarding the GST on tax rates, tax rules, tax regulations, threshold limits, general tax knowledge, and legal knowledge (Bornman & Ramutumbu, 2019; Cooper & Robson, 2006; Libby & Luft, 1993). The awareness level among MSMEs is measured for training sessions, seminars and conferences on GST conducted by government and private organizations (Ahamad Nawawi & Ming, 2010; Carolina & Simanjuntak, 2011; Choong & Lai, 2006; R. K. Rao et al., 2019). The respondents were asked to rate their responses on the Likert scale of 1 to 5 (1 = strongly disagree, 5 = most agreed).

Firms’ Characteristics

The firms’ characteristics information related to the type and form of firms and annual turnover was also collected (Seens, 2013; Srivastva, 2021).

Where,

Methodology

To examine the effect of GST, we developed a path model by applying partial least square equation modeling (PLS-SEM). The PLS-SEM is adopted over other traditional regression techniques as other techniques have certain limitations as—(i) not readily applicable to censored data (ii) less desirable optimal properties than maximum likelihood (iii) poor extrapolation properties (iv) sensitivity to outliers (Kritzer, 1976; NIST-SEMATECH, 2012).

For business performance, the functional model is developed where GST determinants are considered as it function, represented in equation (1) below:

Here, the GST determinants are, change in the tax system, technology transition for tax, GST compliance system, compliance burden, tax awareness, and knowledge. Thus, equation (2) can be written as:

Along with GST determinants, the various firm characteristics considered are form, turnover and type (as stated in Sub-section 3.2.3) to analyze their indirect impact on business performance via compliance burden. Further, the impact of tax awareness and knowledge has been indirectly observed through the change in tax system and technological transition. It was observed to provide insight into whether tax awareness and knowledge about change in the tax system and technological transition impact performance.

Data Analysis and Interpretation

Firstly, the statistical properties of SEM model are explained in Section 4.1, followed by measurement model results in Section 4.2

Statistical Fit of the Model

Firstly, the internal reliability and validity are examined for all the constructs- GST determinants, business performance and firms’ characteristics. Table 2 exhibits strong composite and internal reliability as the composite reliability values lie between 0.837 and 0.932 and for Cronbach alpha are above the limit of .70 (lies between .712 and .908) (Hair et al., 2011; Nunnally, 1978). Thus, the given values of the constructs reflect the good internal reliability of the model.

Construct Reliability and Validity.

Source. Authors’ compilation.

Further, to examine the constructs’ convergent validity, the average variance extracted (AVE), and factor loading values are examined (Fornell & Larcker, 1981). The values are above the critical threshold limit of 0.50, that is, lies between 0.567 and 0.720, which lends support to convergent validity (Bagozzi et al., 1991).

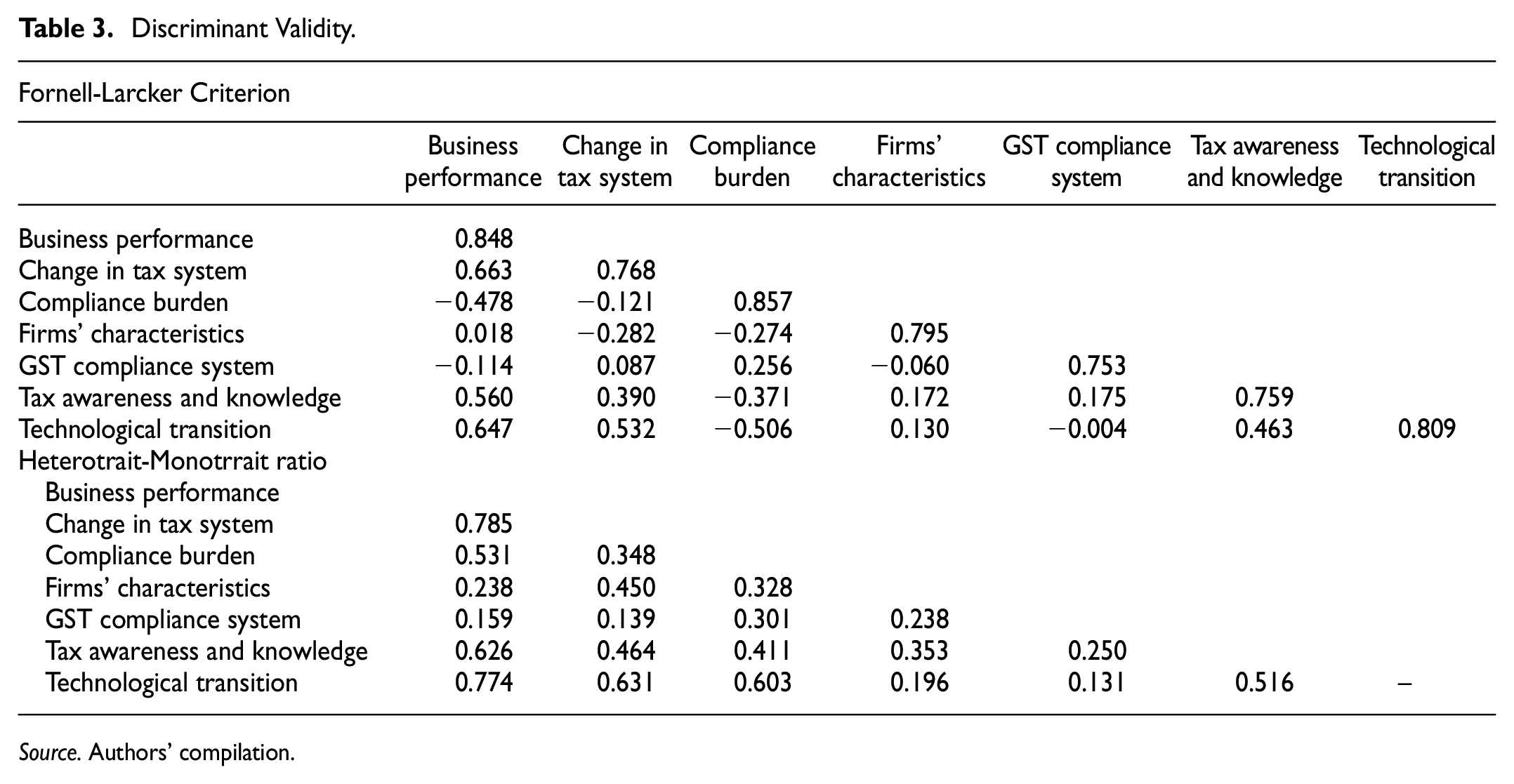

Discriminant validity was examined by taking into account two criteria: Fornell and Larcker criterion and the Heterotrait-Monotrait ratio (Hair et al., 2011). Fornell and Larcker’s criteria were measured by comparing the values of the square root of AVE (Fornell & Larcker, 1981). It is recommended that the value of the square root of AVE should be larger than the inter-construct correlations, as stated in Table 3. The results confirm that the reflective construct exhibits discriminant validity. Later, the Heterotrait-Monotrait Ratio, which is less than the threshold value of 0.85 for all the constructs (Kline, 2011), reveals the discriminant validity of the model.

Discriminant Validity.

Source. Authors’ compilation.

For the good fit model, we have tested chi-square statistics, normed fit index (NFI), and Standardized Root Mean Squared Residual (SRMR).

Table 4 demonstrates the model fit results for the measurement model. The accepted model fit value for the model, with chi-square statistics, is 853.188, NFI is 0.863, and SRMR is 0.083, which is above the acceptable range (NFI ≥ 0.90) and SRMR is near 0.08, as recommended by Muller (1996), Kline (1998), which proposes a good fit of the model. The measurement model results are significant at 1% level (p < .000).

Model Fit Indices.

Source. Authors’ compilation.

The absence of collinearity among the GST determinants and business performance was established, as each indicator’s variance inflation factor (VIF) value was lower than 5 (Hair et al., 2011). The indicators were considered valid as their VIF value is below 5 and loading value is above 0.6 (Hair et al., 2011) for all the variables used in the model (Table 5).

Variance Inflation Factor.

Source. Authors’ compilation.

Measurement Model Results

The path model developed depicts the impact of GST determinants on performance level in Figure 1, and path coefficient results are shown in Table 6. The PLS-SEM model explains a total of 67.4% of the variation (refer to Figure 1; for the bootstrap model, refer to Appendix A1).

Effect of GST on business performance of MSMEs: PLS-SEM analysis.

Structural Model Analysis.

Source. Authors’ compilation.

Significant at p-value: ***p ≤ .01. **p ≤ .05. *p ≤ 0.10.

To begin with, the first determinant taken was the change in the tax system. It positively enhances the performance, as stated in Table 6; the β-value is .503 (t-statistics 5.717; p < .000). This signifies acceptance of hypothesis H1: Change in tax system positively affects MSMEs’ business performance. Thus the results support that the change in the tax system has removed the inefficiencies that existed in the earlier system. It emerges to be a progressive (0.835), robust (0.658), and transparent system (0.865) that led to better business performance. The higher outer loading of each construct of the tax system supports the findings that it has a strong and influential impact on the performance level of MSMEs.

Another determinant used in the study is technology tax transition, which enhanced the performance (β-value .185, t-statistics 1.844; p-value: .066). Thus, the results support hypothesis H2: Technology tax transition positively affects MSMEs’ business performance. It highlights that Goods and Service Tax Network (GSTN) has led to better tax governance (0.846) and tax administration (0.831) of the MSMEs. It saved a lot of time (0.747). Thus, the findings support that technology has positively enhanced performance.

With the change in tax system and technology, the operating framework of the compliance system also changes. In the study, we determined the impact of the GST compliance system directly on the performance and indirectly through compliance burden (time spent in complying with the new system) on business performance, as shown in Figure 1. The direct impact of the GST compliance system has a negative impact on the performance β-value −.145 (t-stats.: 1.848; p-value: .065). GST compliance system has increased the burden by blocking the time of MSMEs β-value .241 (t-stats.: 1.754; p-value: .080). Further, GST compliance system via compliance burden harms the performance β-value: −.198 (t-stats.:2.071; p-value: .039). The good news is that even when R-squared is low, the significant p-values still indicate a real relationship between the significant predictors and the response variable. The low R-squared graph shows that even noisy, high-variability data can have a significant trend. The trend indicates that the predictor variable still provides information about the response even though data points fall further from the regression line Interpreting a regression coefficient that is statistically significant does not change based on the R-squared value. The results stated in Table 6 suggest that the GST compliance system negatively impacts performance directly and indirectly by taking the compliance burden as a mediator. Thus, it supports the hypothesis H3a: GST compliance system negatively impacts the business performance of MSMEs and H3b: The compliance burden (time spent) has a negative impact on the business performance.

Further, the direct and indirect impact of tax awareness and knowledge has been empirically verified. Table 6 demonstrates that tax awareness and knowledge have a direct positive impact on business performance. This implies that proper awareness and knowledge about the tax system enhances the performance of MSMEs, which is evident from the β-value: .247 (t-stats.: 3.181; p-value: .002). Thus, it supports hypothesis H4: Tax awareness and knowledge positively impact the business performance of MSMEs. Furthermore, The indirect effect of tax awareness and knowledge is also observed. It positively enhances the understanding of change in tax system and technological transition implemented in the GST. The results emphasized that tax awareness and knowledge have enhanced the understanding of change in tax system 0.390 (t-stats.: 4.605; p-value: .000) and technological transition 0.463 (t-stats.: 5.396; p-value: .000).

Further, the effect of firm characteristics is also measured on the compliance burden and tax awareness. With the change in type (0.803), form (0.768), and turnover (0.812), the burden on MSMEs gets influenced, which is significant at 1% significance level (p < .000). The results state that an inverse relationship exists between size, turnover and type of MSMEs and compliance burden, β-value: −.259 (t-stats.: 3.561; p-value: .000). As the turnover increases and type (micro, small, and medium) changes, the burden to comply with new tax returns and tax filing issues increases, as the compliances vary with different types of units—micro, small, and medium.

Table 7 demonstrates the acceptance of all the hypotheses of the study. The results of the Blindfolding procedure run in Smart PLS for the higher-order model of study. Q 2 values higher than 0.0, 0.25, and 0.50 depict the PLS-path model’s small, medium, and large predictive relevance (Hair, 2019). All Q 2 values were found to be near 0.50, that is, 0.458 for the model depicting larger predictive power of the PLS model of the study. The results support the predictive significance of the model.

Acceptance and Rejection of Hypothesis.

Discussion and Conclusions

It is a well-known fact that economic development is linked with the taxation system. Therefore, tax reforms are carried on to enhance economic growth and businesses. The implementation of the consolidated indirect taxation system in India was the Goods and Services Taxation system, which provided an opportunity to examine its effect on business performance, particularly for Micro, Small and Medium Enterprises (MSMEs).

The study conducted a primary survey on 404 registered MSMEs of Punjab and applied PLS-SEM. Four significant findings of the study related to change in tax system, GST compliance system, compliance burden, technological transition for tax, tax awareness, and knowledge.

The most notable finding is the effect of change in the tax system on business performance. The present findings support that the GST system has brought transparency and robustness to the indirect tax structure, which enhanced the operational efficiency of the MSMEs. Further, the study suggests that the availability of input tax credits and prevention of stock leakages has contributed to MSMEs’ performance by reducing the working capital blockage of funds. Singh et al. (2018) examined that change in the tax system brought relief to manufacturers by simplifying the earlier tax system’s complexities and increasing supply chain management efficiency.

The study’s other notable findings are the impact of the technology transition on tax. The latest technological aspect of GST has amplified its performance. Technological advancement in tax reform focused on the simplicity of tax design and transparency in tax administration. The robust system has saved MSMEs’ time by simplifying the cumbersome paperwork processes, leading to ease of business. As supported by the study of Supardianto et al. (2019) state that technology plays an essential part in easing out the working and providing MSMEs a global platform (Ojha et al., 2009).

The study’s other finding is the significant impact of tax awareness and knowledge on performance levels (based on human capital theory). The study suggested that proper tax awareness and knowledge aided the MSMEs in abiding with the new taxation system, filing tax returns on time, and saving them from fines and penalties, thereby increasing the profit margins of the units. Further, the study’s findings suggested that seminars, workshops, and conferences conducted on tax reform by government and private organizations have helped MSMEs learn the applicable new taxation rules, regulations, and GST models. Therefore, proper awareness and knowledge of GST lead to its lawful tax compliance. A similar opinion is observed by Nyamwanza et al. (2014) that a low level of tax knowledge directly affects the SMEs’ business by lowering the profit margins. Atawodi and Ojeka (2012) and Cuccia (2013) opined that the lack of tax knowledge led to complexity regarding SMEs’ regulations, which negatively impacted the business and led to tax non-compliance (Rahmayanti et al., 2020).

The uniqueness of the study lies in evaluating the impact of firm characteristics, that is, MSMEs’ size, turnover, and forms, on business performance. The overall impact on micro, small, and medium units is difficult to understand without considering the firms’ characteristics on the tax compliance system. Findings state that the change in turnover, diverse forms, and different types (size) of MSMEs positively influence the level of awareness and negatively on the compliance burden level. Because the variation in size and change in turnover level and forms (partnership, proprietorship, and companies) determine tax compliances of a firm, that is, the number of tax returns, invoice records, documentation of accounts, applicable tax rates, rules and due dates.

The study established a negative impact of GST compliance system on performance, both directly and indirectly (through compliance burden as mediator). The new GST compliance system has increased the compliance burden in terms of efforts and time spent complying with new compliance rules and procedures. The increase in the number of tax returns, and documentation processes, led to the slow progression of business expansion and proved to be a hindrance. Similar implications were analyzed in Malaysian and Australian firms (CChen & Taib, 2016; Siddiq & Sathya, 2017).

Conclusion

The overall results highlighted that GST has positively enhanced the business performance of MSMEs. Changing the tax system brought transparency and the availment of input tax credits under the GST regime led to reduced working capital blockage funds of the MSMEs. Further, the technological transition through the Goods and Service Tax Network (GSTN) led to easy tax governance and strong tax administration at a single I.T. tax platform, which enhanced the operational efficiencies and ease of doing business. Nevertheless, in contrast to it, the GST compliance system led to an increase in the number of tax returns and a rise in the documentation process, which increased the compliance burden (time spent) on MSMEs.

Tax awareness and knowledge have significant direct and indirect effects on business performance. The in-depth knowledge of GST rules and models enhanced the performance of MSMEs. Indirectly, understanding the tax system change and technological transition led to ease in doing and augments the operational efficiencies of the MSMEs.

Policy Recommendations

The practical implications are for policymakers, government, and MSMEs. The results may prove beneficial for the policymakers and governments of developing countries as they can focus on formulating simple, straightforward and not cumbersome compliance processes and procedures. Tax compliance is crucial for governments as it directly influences their revenue collection. Whenever the compliance system is cumbersome and becomes hard to follow, it leads to tax evasion. The simplification of the compliance procedures would prove beneficial to both government and businesses in multiple ways. First, simplifying the tax return filing and documentation process would reduce the taxpayers’ money, time and tax burden. Second, the more straightforward tax procedures would raise the tax compliance rate, reducing tax evasion, and generating more revenue for the government. Further, they must conduct training programs and workshops to sharpen the technical skill of small to reduce the compliance burden, which leads to the expansion of small businesses globally.

In terms of limitations, the sample for the current study represents Indian MSMEs, and thus, it is possible that factors that are unique in one developing country may vary in other countries MSMEs that follow different indirect tax structures.

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

The complete data set of the responses that support this study’s findings are available from the corresponding author upon reasonable request.