Abstract

According to the reality of China, we divide Internet finance into four parts as Internet payment services, Internet financing services, Internet financial management services, and online banking business of traditional commercial banks, to discuss the impact of Internet finance on the profit efficiency of commercial banks. Our theoretical analysis shows that the external impact of Internet finance will reduce the profit of commercial banks, but Internet financing and Internet financial management have less influence, and the financial Internet business can improve the profit efficiency of commercial banks to some extent. An empirical test of Chinese data provides support for these predictions, it suggests that the estimated impact is significant and robust. Furthermore, differences in ownerships and profit efficiency of commercial banks will be at work.

Introduction

In recent years, China’s financial industry has been in constant reform and innovation, such as the gradual promotion of interest rate liberalization, exchanging rate liberalization, and the steady opening of the capital market. The emergence of Internet finance has stimulated the innovation power of financial markets and financial products, and to some extent, promoted the institutional reform process of the financial industry.

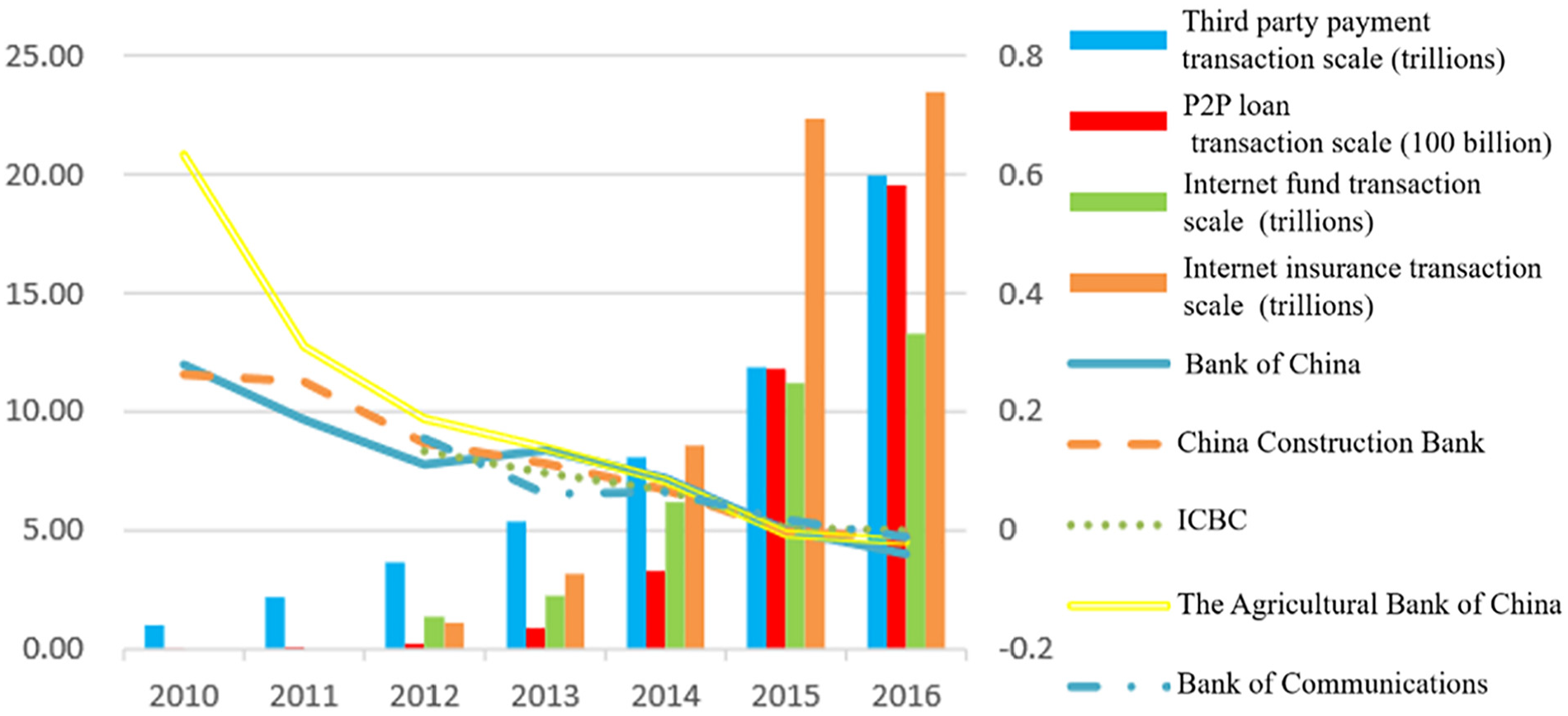

The rapid development of Internet finance has not only facilitated people’s lives, but also brought great impact on traditional financial institutions. The most affected ones are traditional commercial banks. As the most direct reflection, the profit growth rate of China’s five state-owned banks has declined sharply (Figure 1). According to the annual report, in 2016, the net profit of Industrial and Commercial Bank of China rose 0.01% and net profit of Bank of China, China Construction Bank, Agricultural Bank of China, and Bank of Communications decreased 3.96%, 1.10%, 1.83%, and 1.08%, respectively. While the growth of profits slowed down, the total number of commercial bank employees and business network points began to decline gradually in recent years. By the end of 2016, five state-owned firms employ a total of 172.2 million, down 1% from the end of 2015; the number of all the institutions is 70,783, decreased by 0.2% over 2015.

The growth rate of net profit and the scale of Internet financial market of the five major state-owned commercial banks.

Data Sources

Bank annual report, Wind-database, iResearch, and Online loan platform.

After the development of Internet finance, on the one hand, the penetration of non-financial institutions into the financial market broke the monopoly of commercial banks on the “dual market” of savings and loans, squeezed their profits. On the other hand, the advanced technology in the field of Internet finance can produce technology spillover effect on commercial banks. The improvement of traditional business and management mode of commercial banks reduces their operating costs, improves operational efficiency, and impels the innovation of commercial banks’ management concepts and business models. The impact of Internet finance on commercial banks is undoubted. The bank assets figured more than 90% of China’s financial assets is an important driving force for China’s rapid economic development. Profit efficiency measures the degree of profit maximization, reflects the extent to which commercial banks use scarce resources. Therefore, it is extremely necessary to explore the impact of Internet finance on the profit efficiency. In recent years, commercial banks have implemented a number of institutional reforms, and their efficiency has always been paid attention to by scholars. What’s more, the concept of “Internet +” has been continuously implemented, and the development of Internet finance is in the ascendant. Its influence on commercial banks has already appeared and will continue to expand. We explore the impact of Internet finance on the profit efficiency mostly from the perspective of the external impact of non-financial institutions’ Internet finance business on commercial banks. This provides a reasonable economic explanation for the decline of bank performance, which helps commercial banks to rationally treat the development of Internet finance and rationally use Internet technology to improve their profit efficiency.

Internationally, most Internet finance companies use Internet platforms and information technology to network their products and services. Therefore, when scholars discuss the impact of Internet finance on the efficiency of commercial banks, they mostly analyze the mechanism of Internet technology promoting commercial banks to improve their profit efficiency. In China, the application of Internet technology by commercial banks is only a small part of Internet finance, and more non-financial institutions provide financial services through the Internet platform. Therefore, exploring the development of Internet finance affects the domestic literature of commercial banks, and more reflects the external impact of Internet financial enterprises on commercial banks. The impact channels can be roughly divided into the following aspects.

Firstly, the rapid development of Internet finance has seized the market of commercial banks and has caused a violent impact on its various businesses. In the short term, with its convenient and fast operating advantages and rich investment channels, Internet finance has caused a large number of depositors losing of commercial banks, diverting bank deposits (Gong, 2013; Zheng & Liu, 2014), pushing up the capital cost of commercial banks (Zheng, 2014), decreasing the growth rate of loans and deposit, and brought about more risk (Chen et al., 2020); on the other hand, the marginalization of commercial bank payment functions (Wang, 2015), reducing the income of intermediary business (Zhang & Yang, 2013), diverting quality credit resources (Wu et al., 2015; Q. J. Zhang & Liu, 2017), and weakening the profitability of commercial banks (Sun & He, 2015). In long-term trends, the development of Internet finance is bound to seize the core business market of commercial banks (Zeng, 2012), and the impact on traditional finance is “infiltration and even subversion” (Wu, 2014).

Secondly, Internet finance has improved the profit efficiency of commercial banks through technology spillovers and demonstration effects (Fu et al., 2020; Liu & Yang, 2017). Internet financial enterprises have more advanced technical means and more avant-garde service concepts. Commercial banks can improve their product innovation speed and service level by imitating their business methods and product structure (Gong, 2014; Wei & Ling, 2013). Reshaping its lending model (Peng & Li, 2015), accelerating financial disintermediation from channels, funds, information, and customer relationships (Yuan et al., 2013), reducing the technical costs of commercial banks (Zou et al., 2017), strengthening risk control capabilities, thereby improving their comprehensive competitiveness (Wang et al., 2021). Moreover, many scholars find that Internet finance companies have broken the monopoly position of commercial banks in the “dual market” of savings and loans by competing with commercial banks (Guan et al. 2014; Liu, 2016). The squid effect can stimulate the bank’s sense of crisis and force the bank to carry out business innovation and strategic transformation (Chu & Guo, 2014; Dong et al., 2020) to promote the profit efficiency of commercial banks.

Thirdly, the Internet finance industry has also had a positive impact on commercial banks through the mobility and linkage effects. The flow of personnel in Internet finance companies is mainly achieved through three channels of transfer of entrepreneurs, technicians, and scientific research institutions (Liu & Lin, 2016), thereby improving the quality and technical level of commercial banks. In the cooperation between commercial banks and Internet finance companies, on the one hand, commercial banks can provide Internet finance companies with business support such as liquidation and fund transfer (Shen & Guo, 2015). On the other hand, Internet finance companies can provide a large amount of data for commercial banks to conduct market analysis, which makes the procyclicality of commercial banks less than before (Yao & Song, 2021). However, Internet finance has also a great risk spillover effect on the banking industry, mainly from risk transfers caused by vast business transactions between them (Chen et al., 2019; Xiao, 2019).

There are a lot of fruitful results for the definition, nature, and development mode of Internet finance, but a few studies focus on the profit efficiency of commercial banks by Internet finance. There is no consensus on the theoretical mechanism of Internet finance affecting commercial banks, and they all discuss their impact on commercial banks by using Internet finance as a single entity. However, the business content of Internet finance is diverse, and the impact on different businesses of commercial banks is also different. Comparing the previous research literature on this issue, our article contributes to the literature as follows.

First, a stochastic frontier approach (SFA) is used to measure the profit efficiency of commercial banks. Most scholars still use the financial indicator method to measure the efficiency of commercial banks. Most use the bank’s net profit (or net income)/average total assets (ROA) and bank net profit (or net income)/average total capital (ROE; Akhisar et al., 2015). Considering that financial indicators cannot reflect the overall efficiency of banks (Sherman & Gold, 1985), and the selection of financial indicators is subjective, this paper uses the SFA in the parameter method of total factor productivity to study the impact of internet finance on the profit efficiency of commercial banks, which can comprehensively measure the efficiency of commercial banks.

Futhermore, the existing research uses no macro industry data, only time series data, to measure the level of development of Internet finance. A few scholars have used text mining to measure the development level of Internet finance, relying on the frequency of news related to Internet finance. Some questions remain over the scientific efficacy of this method. This paper, therefore, when measuring the Internet business of commercial banks, use the micro-variables of the scale of online banking transactions, creating panel data which are more convincing when it comes to horizontal analysis and comparison between banks.

Finally, the non-financial institutions’ Internet finance business is divided into three parts in this paper: Internet payment, Internet capital raising, and Internet financial management. Since the development of early domestic Internet finance mainly concerns the rise of third-party payment institutions, the existing literature on the development level of Internet finance mostly adopts third-party payment scale-related variables. But nowadays Internet capital raising and Internet financial management are becoming more mature, and the impact of this on commercial banks cannot be ignored. Besides this, different Internet financial services have different market environments and product characteristics. It is not reasonable to confuse them to discuss their general impact on the profit efficiency of commercial banks. Therefore, this paper measures the development level of Internet finance by the transaction size variables of Internet payment, Internet capital raising, and Internet financial management.

In Section 2, we discuss the mechanism of Internet finance affecting the profit efficiency of commercial banks. Section 3 explains our empirical approaches, the variables, and data. Section 4 contains our baseline and heterogeneous results. Finally, Section 5 concludes.

Theory

Since the development of Internet finance, the rich forms of content have changed, and various divisions can be made according to different standards. This paper divides Internet finance into Internet payment services, Internet financing services, and Internet financial management services carried out by Internet companies, as well as financial Internet services carried out by traditional financial institutions. When discussing the impact of Internet finance on the profit efficiency of commercial banks, what is essentially discussed is the impact on the input and output of commercial banks, such as the reduction of input in the case of constant output, or the production of unchanged investment. An increase means the profit efficiency of commercial banks rises, and a decrease means vice versa. The following discusses the mechanism of the impact of different Internet finance businesses on the profit efficiency of commercial banks.

The Theoretical Mechanism of Internet Payment Affecting the Profit Efficiency of Commercial Banks

Before the birth of Internet payment, a large number of risk-averse customers and customers with less funds to purchase wealth management products used to deposit funds into banks, save a portion of their working capital as demand deposits, and then withdraw a small portion of their cash for daily use. After the Internet payment is accepted on a large scale, users have more choices to transfer the idle funds to the accounts paid by the third party to facilitate daily consumption transfer; on the other hand, the third-party payment platform that cooperates with the e-commerce platform, due to the delayed payment function, can precipitate a large amount of capital flow. For example, for Alipay customers, after the buyer pays and confirms the receipt, the funds still stay in Alipay, and the average stay is 3 to 7 days, which will divert the deposits of commercial banks to a certain extent. It also pushes up the deposit interest rate of commercial banks.

According to Metcalfe’s law, the use value of the Internet has increased with the increase of network users, and the market demand has also increased. Therefore, the scale of Internet payment will continue to expand rapidly, which will inevitably have a greater impact on the intermediary business of deposits and commission income of commercial banks, reducing the number of commercial banks and Output price. In the short term, due to factors such as wage stickiness and scale immutability, it is difficult for commercial banks to make fixed adjustments such as labor input and material capital investment, and it is difficult to make corresponding adjustments according to the reduction of business volume. Therefore, the input factors are basically unchanged. In the case of a significant reduction in the output of commercial banks, their investment has not decreased year-on-year, so the profit efficiency of commercial banks will drop significantly. Thus, we propose the following hypothesis.

The Theoretical Mechanism of Internet Capital Raising Affecting the Profit Efficiency of Commercial Banks

This article has the aid of the concept of “The Long Tail” first formalized in Anderson (2006) to describe the market tail demand ignored by most enterprises. If the loan market demand curve is assumed to be subject to the Pareto distribution, under the premise of resource (funds) scarcity, information asymmetry caused by adverse selection and moral hazard, high information screening costs, plus compliance with the traditional commercial loan business model “Two-eighth law” loan business model, traditional commercial banks often lend to large-scale enterprises with good loan experience, while directly abandoning loans that are to small such as micro-enterprises or individuals with no loan records, in line with the Pareto distribution demand curve.

However, Internet capital raising has opened up new lending markets. Internet capital raising services such as P2P online loans and microfinance loans are located on the long tail of traditional commercial banks. By using Internet technologies such as big data, cloud computing, and block chains, the credit level of borrowers can be controlled efficiently and cheaply, which improves the allocation dilemma of small and micro enterprises in the traditional financial credit system and forms a small-scale economy with small-scale demand, showing the tail of the Pareto distribution of the demand curve. Therefore, although the lending business of Internet capital raising and traditional commercial banks partially overlap and break the monopoly position of commercial banks in the capital lending market, the online lending business is more complementary to the market At both ends of the demand curve, the impact on the commercial bank’s loan business will not be particularly large. However, since the de-intermediation of Internet capital raising increases the interest rate of capital lenders relative to bank deposits, it will attract a large amount of funds with certain risk-taking ability to flow into the online loan market, thus diverting the deposits of commercial banks. Therefore, the development of Internet capital raising has reduced the number of deposits of commercial banks. While the interest rate of output prices has fallen, deposit interest rates have risen, in the short term, the labor input, material capital investment, and loanable capital investment factors of commercial banks are difficult to do. With the corresponding adjustments, the difference between output and input factors is reduced, that is, the profit efficiency is reduced. Based on these, the second hypothesis is proposed as following.

The Theoretical Mechanism of Internet Financial Management Affecting the Profit Efficiency of Commercial Banks

China’s Internet financial management and Internet payment serve as bilateral market, such as Alipay’s payment business and the Internet financial management business of the balance treasure. Because the two markets can be seamlessly linked, instant arrival and no handling fee, and the investment risk of Internet financial management is much lower than that of general investment products, and the yield is much higher than that of bank demand deposits. Therefore, it has attracted a large number of idle funds originally deposited in demand. Therefore, the emergence of Internet financial management will use the Internet payment to significantly divert the deposits of commercial banks, so that the current demand deposits that have been used to deposit in commercial banks will be transferred to the short-term, high-interest Internet financial management market.

However, in the short term, Internet financial management will not have a significant impact on the intermediary banking business of commercial banks. Internet financial management products rely on the Internet payment platform, the purchase amount is extremely low, the risk is also low, and it is easy to use, and immediately arrives at the account, attracting a large number of customers. But its yield is still not as good as that of traditional commercial banks’ wealth management products, mainly targeting young users who are accustomed to using the Internet, and it is more convenient for customers to use idle funds to obtain higher returns. Thus, we propose the following hypothesis.

The Theoretical Mechanism of Online Banking Business Affecting the Profit Efficiency of Commercial Banks

In addition to the third-party Internet non-financial organizations from outside to usurp and expand the traditional financial markets of commercial banks, the rise of Internet finance will also help commercial banks upgrade their traditional businesses and services through the use of Internet platforms and improve the management mode, so as to reduce the business cost of commercial banks and improve the operational efficiency of commercial banks. Through the reverse mechanism, technology spillover and cooperation effect, the development of financial Internet will reduce the labor input and material capital input factors of commercial banks, and can also improve the total amount of deposit and loan and non-interest income of commercial banks, so as to improve the profit efficiency of commercial banks. Based on these, the last hypothesis is proposed as following.

Methodology

Empirical Approaches

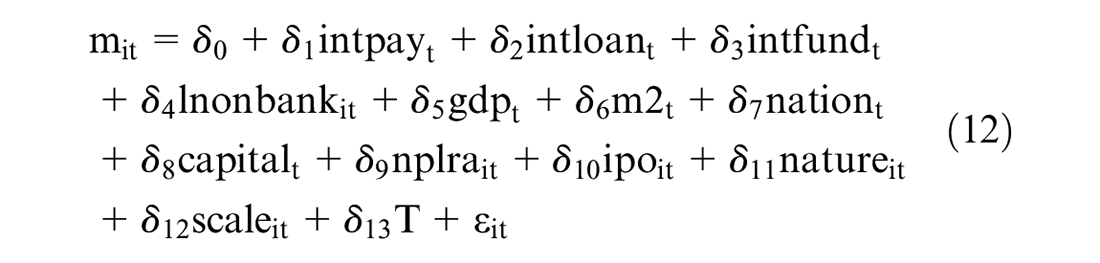

The stochastic frontier model (SFA) of the parametric method is used to solve this problem, which formulated the concept and estimation by Aigner et al. (1977), and the frontier surface is assumed to be a transcendental logarithmic production function to estimate the profit efficiency of commercial banks. According to the regression method, we can divide the literature that use SFA to analyze enterprise efficiency into one one-step method and one two-step method: The first step in the two-step method is to estimate the efficiency level of each production unit in the efficiency frontier model, and the second step is to take the estimated efficiency value as the dependent variable and regression analysis of the factors that may affect the efficiency level. In one step, simultaneous equations are used to estimate the efficiency and identify the causes of inefficiency. The main drawback of the two-step method is that in the first step the inefficiency term is assumed to be the same distribution, and in the second step it is assumed to conform to some functional relationship. However, one-step method needs to estimate a large number of parameters at the same time, which requires a higher sample size and more stringent assumptions. We study the impact of Internet finance on the profit efficiency of commercial banks. Internet finance is still a new thing in China. There is no systematic long-term statistical data. The third-party Internet financial data of non-financial institutions only has macro data published in recent years. The financial Internet data of traditional commercial banks can only be collected from the annual reports published by each commercial bank and the relevant indicators are published. Therefore, due to the limitation of sample size, this paper uses the two-step method for maximum likelihood estimation. The main steps of the model are as follows.

The first step is to build stochastic profit frontier function through input index and output index.

Besides,

Thus, in order to estimate the invalid rate, the conditional mean and mode number of

Further, the point estimate of the efficiency level of each production unit can be obtained from the following formula:

Among them,

a. when the inefficiency term obeys the truncated normal distribution:

b. when the inefficiency term obeys the semi-normal distribution:

c. when the inefficiency item obeys the exponential distribution:

In the second step, the bank profit efficiency level is calculated by the average value of the inefficient disturbance term obtained in the first step, and the regression explanation is performed. The profit efficiency of the i-th bank at t can be expressed as:

Wherein, dependent variable

Further, returning to the efficiency level:

Among them,

Based on the analysis and comparison of the production function and the inefficiency term hypothesis, this paper uses the surpassing logarithmic function to construct the alternative profit function, and incorporates the equity capital and time trend term in the original model to more accurately measure the bank output. And the impact of technological advances on bank profits (Mamonov & Vernikov, 2015).

This form has the following advantages over the Cobb-Douglas function.

It does not violate the curvature characteristic and is suitable for the case of multiple output of the enterprise; It can provide a second-order approximation for the potential frontier on the mean of the data, so it has higher flexibility (Kumbhakar & Lovell, 2012); It is the basis for many empirical estimates and decompositions of the efficiency level; It incorporates the interaction terms of input and output variables, which can better fit our country. The objective situation of commercial banks’ scale returns is variable, and it can ensure that the profit function has sufficient flexibility (Chi et al., 2005). Moreover, previous studies have shown that the results obtained beyond the logarithmic function are also better than the C-D function (Baten et al., 2015), so they have been widely adopted by scholars (Berger et al., 2008; Kumbhakar & Wang, 2007).

The profit frontier model to be adopted in this paper is as follows, which is the specificization of (1).

Among them, we use the bank asset size

The profit efficiency model proposed in this paper is as follows, which is the specification of (10).

Among them, dependent variable

Variables Description

We use the pre-tax profit as the dependent variable of the random profit frontier function. However, due to the negative pre-tax profit of some commercial banks during the sample period, in order to make their logarithm value greater than zero for estimation, this paper uses

Drawing on previous scholars’ research, this paper uses labor price, material capital price, and loanable capital price as the input price of commercial banks, and uses net loan, total deposit, and non-interest income as output quantity (Berger et al., 2010). Among them, the labor price is the labor cost of the unit assets, that is, the ratio of employee compensation to total assets; the price of material capital is the sum of the non-interest expenditure of a unit of fixed assets, that is, fees and commissions, investment losses, changes in fair value, exchange losses, operating expenses and non-operating expenses, and its ratio to fixed assets; the price of loanable funds is the interest expense of unit deposits, that is, the ratio of interest expenses to total deposits absorbed. Among the output quantity, the loan is the net loan value, that is, the net value of the total loan after deducting the non-performing loan; the deposit is the absorption of total deposits; the non-interest income is the fee and commission income, the investment income, the fair value change income, the exchange income, and other business income and the sum of non-operating income.

When dealing with the input price, it is endogenous to use the factor input price of each bank, which violates the hypothesis of exogenous factor input price in production function (Patti & Hardy, 2005; Tan & Li, 2016). Due to the wide geographical dispersion of China’s commercial banks and the limited geographical restrictions, the business competition between different types of commercial banks is also fierce. Therefore, this paper adopts the average input factor prices of all commercial banks except the estimated banks in the sample. All currency variables in the text have removed the inflation effect.

The dependent variable of the profit efficiency function is the profit efficiency value obtained from the inefficiency value estimated in the first-order random profit frontier model. In the independent variables, the level of Internet payment development

Among the bank characteristic variables, the total assets of more than 4,000 billion yuan are divided into large enterprises, the total assets between 500 billion yuan and 400 billion yuan are divided into medium-sized financial enterprises, the total assets between 5 billion yuan and 500 billion yuan are divided into small financial enterprises, the total assets under 5 billion yuan are divided into micro-enterprises. {based on 2015. 9. 28 People’s Bank of Japan, together with the CBRC, CSRC, and CIRC and the National Bureau of Statistics released the financial industry standard enterprise-type plan.}. Based on this, the bank size dummy variables scale2, scale3, and scale4 are respectively set in the text to indicate whether the bank is a small-scale bank, a medium-sized bank, and a large-scale bank. According to the ownership property of the sample bank, the bank is divided into state-owned large commercial bank, joint-stock commercial bank, urban commercial bank and rural commercial bank. And the corresponding dummy variables nature2, nature3, and nature4 are set accordingly. In addition, we set up the non-performing loan rate variables of banks and the virtual variables of whether the banks are listed in the estimated period to control the risk status and characteristics of the sample banks.

Among the control variables at the industry level, this paper adds the proportion of the assets of five state-owned commercial banks to the total assets of the banking industry to reflect the industrial structure of the banking industry, and sets up the proportion of commercial credit to the private sector in the GDP to reflect the importance of the banking industry to the capital market (J. H. Zhang & Wang, 2011). In addition, this paper adds the growth rate of GDP and the proportion of money supply in GDP as macro-level control variables to reflect the level of economic and financial development.

Data and Summary

Firstly, the financial data of 235 domestic commercial banks in 2005 to 2016 were taken as samples, using random profit frontier model to estimate the value of the bank’s profit efficiency. Secondly, due to the short development period of Internet finance, Internet capital raising, and Internet financial management have only started systematic data since 2009 and 2012 respectively, and each database has no systematic micro statistics for the internet finance business of various commercial banks in China.

After consulting the annual reports of more than 100 major commercial banks, the author selects 33 commercial banks which have published the transaction scale of online banking from 2012 to 2016 as samples to estimate the impact of Internet Finance on the profit efficiency of commercial banks, Which include five major state-controlled commercial banks, nine joint-stock banks, sixteen urban commercial banks, and three rural commercial banks.

The bank’s characteristic variables in the random profit frontier model and the profit efficiency model are derived from the financial statements in the Guo Tai An database and the annual reports published by banks. Among the macro and industry variables used in the profit efficiency model, the GDP growth rate and the broad money supply indicator data are from the National Bureau of Statistics database; the five major state-owned bank assets and the total financial assets of the banking institutions are derived from the annual report of five major state-owned commercial banks, the financial statements in the database, and the China Banking Regulatory Commission database. The bank’s credit data for the private sector comes from the World Bank database. The data required for Internet payments, Internet capital raising, and Internet financial management variables comes from the wind database. The variable of internet finance is expressed in logarithm of the scale of commercial bank online banking transactions, and the data comes from the annual report of the sample bank during the sample period. The descriptive statistics and main variable definitions of the estimated model are shown in Table 1.

Summary Statistics and Definition of Variables.

Note. The units of the amount variable are all yuan, capital is a percentage, and the units of other specific variables and growth variables are 1.

Results

Baseline Results

Because the model contains dummy variables such as ownership attributes that do not change with time, it cannot be estimated in fixed effects; otherwise, the data belongs to large N small T, if the fixed-effects model has a large loss of degrees of freedom, this article chooses to use a random-effects model to estimate the heteroscedasticity robustness in the second step of panel data regression. The panel unit root test on the data shows that the data is stable. The correlation coefficient matrix between the variables is shown in Table 2, where u is the efficiency level of the commercial bank (assuming that the inefficient terms obey a semi-normal distribution).

Correlation Matrix.

To select the most suitable model, and test the robustness of the model estimation, the estimation results under various settings are given in Table 3. Model 1, Model 2, and Model 3, respectively, assume that the inefficiency term obeys the truncated normal distribution, the semi-normal distribution, and the exponential distribution. The empirical results for the sample bank are as Table 3:

Regression Results of Stochastic Profit Frontier Model and Profit Efficiency Model.

Note. Statistical significance at the 10%, 5%, and 1% levels are indicated by *, **, and ***, respectively, with t value in parentheses.

The first part in Table 3 is the estimation result of the stochastic profit frontier model. ll is the log-likelihood function value reported by the three models for MLE estimation. Hu is the test result of the unilateral error term. Model 1 reports the z value and rejects the null hypothesis at the level of 1%; Model 2 and Model 3 report the log-likelihood values, both at the 1% level Significantly. That is to say, all three models affirm the rationality of using inefficient unilateral distribution. sigma2, sigma_u2, and sigma_v2 are compound variance, inefficiency term variance, and random interference term variance, respectively. The inefficiency terms of models 1 and 2 fluctuate much more than the fluctuations of random disturbance terms. In order to understand the proportion of the inefficient term in the error term, the lambda in the table is the ratio of the standard deviation of the inefficient term to the standard deviation of the random interference term, and greater than 1 indicates that the fluctuation of the inefficient term is greater than the fluctuation of the random interference term; The gamma is the proportion of the variance of the inefficient terms in the compound variance. The gamma values of Model 1 and Model 2 are as high as .999 and .724, which indicates that when the inefficient terms are assumed to obey the truncated normal and semi-normal distributions, the actual profit of the commercial bank Most of the difference from the theoretical profit is due to inefficiency, and the random interference term only accounts for a small part.

The second part of Table 3 is the statistical characteristics of the profit efficiency levels of commercial banks estimated by the three models. It can be seen that the estimation results of Model 1 and Model 3 are very similar, and the difference is accurate after four decimal places. The average profit efficiency estimated by the three models is between 0.71 and 0.81, the lowest value is between 0.10 and 0.17, and the highest value is between 0.93 and 0.95. It can be seen that the profit efficiency levels estimated by the three models are not much different. The average profit efficiency of Model 2 is 0.718, that is, the actual profit of commercial banks is 28.2% lower than the theoretical profit when the technical level and input factors are unchanged; the actual profit of the lowest profit efficiency bank in the sample is only 16.5% of its theoretical profit, the highest profit efficiency of the bank’s actual profit reaches 93.6% of its theoretical profit, the difference is large, so further analysis of factors affecting the bank’s profit efficiency level, making the bank’s actual profit more likely to be close to the theoretical profit is very meaningful.

The third part of Table 3 is an explanation model of profit efficiency. The significance of the explanatory variables estimated by the three models is exactly the same as the sign of the coefficient, and there are only small differences in the size of the coefficients, which proves that the estimated profit efficiency model is robust to a certain extent. As the above analysis shows that it is most appropriate to assume the inefficiency term as a semi-normal distribution, the following part of this paper focuses on the empirical results of Model 2.

The Impact of Internet Payment on the Profit Efficiency of Commercial Banks

Internet payments will significantly reduce the profit efficiency of commercial banks. The result of Table 3 shows that the impact coefficient of

The Impact of Internet Capital Raising on the Profit Efficiency of Commercial Banks

The development of Internet capital raising will slightly reduce the profit efficiency of commercial banks. As far as Internet capital raising is concerned, the impact coefficient of

The Impact of Internet Financial Management on the Profit Efficiency of Commercial Banks

The development of Internet financial management will also reduce the profit efficiency of commercial banks. The influence coefficient of intfund is negative at the significant level of 1%, indicating that the development of Internet fiancial management will also have a significant negative impact on bank profit efficiency, but the impact coefficient is −.301, which is relatively small. As mentioned in Hypothesis 3, although Internet financial management diverts deposits from commercial bank, which reduces the source of funds for commercial banks. The financial management period of commercial banks is long and fixed, the yield is generally more than 5%. Meanwhile, the threshold of Internet financial management applications is generally 1 yuan or even 0.1 yuan, and the yield is generally below 4%. Therefore, the negative effect of Internet financial management on the profit efficiency of commercial banks is relatively small.

The Impact of Online Banking Business on the Profit Efficiency of Commercial Banks

The development of online banking business of commercial banks will help improve the profit efficiency of banks. The coefficient of

Moreover, ownership can also significantly affect the profit efficiency of commercial banks. The dummy variables of urban commercial banks, state-controlled banks, and joint-stock commercial banks are significantly negative at the level of 1%, 5%, and 10%, respectively, indicating that compare with the ownership of other commercial banks (mainly rural commercial banks), the profit efficiency of state-owned banks, joint-stock banks, or urban commercial banks are relatively low. Among them, urban commercial banks are more profitable than state-owned commercial banks and joint-stock commercial banks.

Heterogeneous Impact

The above analysis is based on the whole sample. To investigate heterogeneity, we split the whole sample into several subsamples to check whether the different ownership banks and different scale banks has suffered heterogeneous impact.

Ownership Structure

First, we split the sample into three groups: the state-owned banks, the joint-stock banks, and the urban banks, which result has been reported in column (1) to (3) of Table 4, respectively, in order to analyze the impact of Internet finance on different ownership of commercial banks. Since the financial data of rural commercial banks in the internet is too small to be effectively estimated, it will not be discussed here.

Impact of Internet Finance on Commercial Banks With Heterogeneous Ownership Structure.

Note: Statistical significance at the 10%, 5%, and 1% levels are indicated by *, **, and ***, respectively, with t value in parentheses.

In general, it can be seen that the impact of Internet finance on commercial banks with different ownership is identical, but the degree is different. The biggest impact of Internet payments is on joint-stock commercial banks and state-owned commercial banks. And the biggest impact of Internet capital raising is on urban commercial banks, the possible cause is that the main customers of urban commercial banks are small and micro enterprises and individuals, which are overlap with the main customers of Internet finance. The Internet financial management business has a relatively large impact on the profit efficiency of joint-stock commercial banks. As far as the internet business of commercial banks is concerned, the expansion of transaction scale of online banks of urban banks can slightly improves their profit efficiency at the significant level of 10%, while state-owned holding commercial banks and joint-stock commercial banks has no significant effect on their profit efficiency. The possible reason is that the management system of state-owned commercial banks and joint-stock firms are inelastic, therefore, the technology spillover effect and demonstration effect of Internet finance are not obvious; comparatively, urban commercial banks have clear property rights, simple structure, and can respond to the impact of Internet finance more quickly.

Scale

Threshold regression, by looking for structural mutation points in the sample as a grouping criterion, expands the grouping test of nonlinear econometric models, which is more scientific and convincing. Internet payment, Internet capital raising, and Internet financial management are used as the independent variables corresponding to the threshold effect in turn, to check whether there is a threshold, a double threshold, and even a triple threshold. The statistical results obtained are shown in Table 5. The results show that when the bank asset size is used as the threshold variable, and Internet payment, Internet capital raising, and Internet financial management are used as the independent variables corresponding to the threshold effect, the threshold is 25.916, and the statistical value is significant at 1%. And there is a double threshold effect when the Internet loan scale is used as the independent variable corresponding to the threshold variable. The LR test results for the single threshold effect are shown in Figure 2. Therefore, the impact of Internet finance on the profit efficiency of commercial banks has a single threshold effect on asset size. Based on above, we divide the sample banks into two-component samples with small assets and large assets, and the regression results are shown in Table 6.

Threshold Effect Test of Bank Asset Size.

Note. Statistical significance at the 10% is indicated by *** with t value in parentheses.

Single-door LR test of asset size.

Impact of Internet Finance on Commercial Banks With Heterogeneous Size.

Note. Statistical significance at the 10% and 1% levels are indicated by * and ***, respectively, with t value in parentheses.

The columns (1) and (2) in Table 6 show the results of the regression of small-scale commercial banks and large-scale commercial banks, respectively. It can be seen that the Internet financial services of third-party non-financial institutions have a statistically significant effect on the profit efficiency of commercial banks of different scales at a significant level of 1%. It’s worth noting that the impact coefficient of Internet payment, Internet capital raising, and Internet financial management on the profit efficiency of large-scale commercial banks is greater than that of small-scale commercial banks, indicating the impact of third-party Internet financial institutions on the profit efficiency of large-scale commercial banks are more serious than on small-scale commercial banks. Moreover, the online banking business has only a significant impact on the profit efficiency of small-scale commercial banks, which because the system and product adjustment of small-scale commercial banks are more flexible, and they can quickly absorb the technology spillover effects of Internet finance.

Concluding Remarks

In this investigation, the aim was to assess the impact of Internet finance on the profit efficiency of commercial banks from both external and internal aspects. Constructing a panel data set of 235 commercial banks in China during the 2005 to 2016 period, this study utilized a stochastic profit frontier model, to analyze the impact of the development of internet finance on the profit efficiency of commercial banks in China. The results of this investigation show that the Internet finance of non-financial institutions and the online banking business of commercial banks both affect the profit efficiency of commercial banks. Heterogeneous analysis shows that joint-stock commercial banks have suffered the greatest impact from Internet payment and Internet financial management, while urban commercial banks have suffered the greatest impact from Internet capital raising, and state-owned commercial banks have been relatively less affected by Internet finance. The Internet finance of non-financial institutions has had a strong impact on large-scale commercial banks, and online banking business performed by commercial banks increases the profit efficiency of small-size commercial banks.

Based on the above conclusions, the findings of this study suggest that the following three aspects are crucial for commercial banks to cope with the impact of Internet finance. First, this study’s findings imply that commercial banks should make full use of their competitive advantages, consolidating a monopoly position within the loan business in the high-quality customer market. They should adhere to the market positioning of a high-end, wealth management customer base, and optimize the payment settlement category to increase market share. Commercial banks can differentiate customers with different needs; for example, for micropayment customers the priority is to optimize and especially quicken their micropayment services.

Second, findings suggest that commercial banks should establish data analysis platforms to mine existing data for integrated analysis, effectively transforming data into information resources. From here, deep data mining can be implemented on the basis of data sets to achieve more efficient operations at a lower cost. With years of monopoly in China’s financial industry, commercial banks have accumulated a large amount of data on customer credit status and behavioral characteristics. On the one hand, commercial banks can segment customers through basic customer information, financial assets and trading behaviors to provide personalized services, identify potential customers, create new financial products, and expand the market of wealth management products, while on the other, they can conduct in-depth analysis of industry structure, product structure, and customer structure of various businesses of the bank through data integration, and provide data support for business management decisions as well as the rational allocation of labor, funds, and resources.

Thirdly and finally, in terms of technical defects, the findings of this study have a number of practical implications. Findings suggest that commercial banks would benefit from strengthening their analysis of customer needs, and using the Internet to provide products that can truly improve customer experience as well as increasing sales profits, rather than removing traditional services to the Internet. This thesis suggests that a reasonable approach for commercial banks would be to learn more about Internet technologies as soon as possible, and commit to utilizing and providing more cooperative resources. These may include creating customer financial databases and providing strong financial support with Internet companies to integrate resources and utilize complementary advantages.

Footnotes

Acknowledgements

The authors sincerely thank Mengshi Li, Hao Li, and Zhihang Zhou for their help in editing and correcting the language of this paper, and for their comments and suggestions to improve this study.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.