Abstract

This paper considers an online retailer and his or her manufacturer, both facing financial constraints and wishing to get loans from their e-commerce platform-backed finance company. Based on shared transaction data and monitored sales accounts, a tripartite loan contract is proposed to coordinate three parties’ actions in this supply chain financing problem. We prove that the proposed loan contract aligns the decentralized decision-makings of each party and duplicates the optimal channel performance under a fully integrated decision-making framework. A case study is then conducted to illustrate the performance of the proposed loan contract. The result shows that the proposed loan contract outperforms wholesale-price contracts, where coordination does not take place, and buyback contracts, where coordination happens between the retailer and the manufacturer only. Furthermore, a sensitivity analysis reveals that profit allocations among the lender, the retailer, and the manufacturer resulted from the proposed loan contract are more balanced when the cost-to-retail ratio or risk premium is high.

Introduction

Financial innovation has always been one of the most important drivers for the rapid development of e-commerce in China. E-commerce in China started booming in 2004, after Alipay was launched as a safe payment method and successfully solved the trust problem between online sellers and buyers. With the e-commerce growing and the number of users increasing, Alipay soon becomes one of the dominant e-wallets in China, used for both online and offline shopping. As a part of daily operations, a high volume of cash sits in Alipay’s deposit pool regularly. In 2014, 10 years after establishment, Alipay expands beyond payment service and becomes a full-fledged financial services company: Ant Financial, which aims at providing comprehensive financial services for small and micro enterprises and individual consumers. Over the same period, similar blueprint, and roadmap were witnessed in Tecent-backed Tecent Financial Technology and Jindong-backed JD Finance, all of which are listed as top 10 internet finance companies in China. As internet finance companies with their background rooted in e-commerce, extending their credit evaluation based not only on core companies’ creditworthiness but also business data-dependent credit analysis will become increasingly feasible.

On the other hand, it is not uncommon that both online business owners and their suppliers are start-ups, small, or micro companies, which therefore both face the problem of limited working capital. Traditionally, depending on the role played by these enterprises in a product supply chain, there can be different forms of provision of funding. One of the most popular short-term financing sources for retailers is trade credit, which is linked to supplier financing of retailers’ inventory (Devalkar & Krishnan, 2019; Fisman & Love, 2003; Petersen & Rajan, 1997). Another form of retailer financing is through financial intermediaries, such as banks (Zhou & Groenevelt, 2009). On the other hand, when manufacturers are in specific short-term cash needs, it is common to use certain short-term assets (Buzacott & Zhang, 2004), such as inventories, accounts receivable or purchase orders (Fenmore, 2004), as collateral for commercial loans. However, when both online retailers and their suppliers are start-ups, or small and micro companies, these financing methods are often of little help. Under these circumstances, financing based on transaction data gathered on e-commerce platforms offers an innovative solution. Historical e-commerce data provide a reliable reflection of real market demand, and allow platforms to monitor and predict future sales trend, which thus can be analyzed and exploited by platform-backed finance companies to justify a loan application. For example, JD.com is one of the largest B2C e-commerce platforms in China. JD Finance used to be a finance unit of JD.com and began operating as an independent company from 2013, focusing on providing financial services to JD.com’s business partners through technology solutions. Relying on the big data foundation accumulated by JD e-commerce system, JD Finance provides procurement financing for JD.com’s partners with a trackable proven business history. Instead of asking for collateral, JD Finance considers loan applicants’ business history, the credit worthiness of the buyer, the ability of the supplier to produce the goods, and then decide whether the financing transaction is profitable for all parties. It is reported (Li & Meng, 2016) that JD Finance has helped companies decrease comprehensive procurement costs by 15% on average, and currently has more than seven million enterprise clients.

This paper considers a situation discussed above, where both an online retailer and his or her supplier, which is a manufacturer, are facing short-term financial constraints and wish to obtain funding from their e-commerce platform-backed finance company. Due to the lack of collateral, the retailer agrees to release online transaction data to the lender. Therefore, the platform-backed finance company is allowed to monitor the account of the online retailer and observe the retailer’s real transaction before agreeing to lend money. We propose a coordinating loan contract for the platform-backed finance company, the retailer, and the manufacturer under this situation. We first prove that the channel profit can be maximized with the proposed loan contract. After that, with a case study, we show that the total profit can be allocated flexibly among the lender, the retailer and the manufacturer based on their respective market and bargaining powers by varying coordinating parameter values in the proposed loan contract. The proposed loan contract is then compared with a wholesale-price contract, where coordination does not take place, and a buyback contract, where coordination happens between the retailer and the manufacturer only, for assessing its benefits. Finally, we conduct a sensitivity analysis to investigate the conditions in which the proposed loan contract with demand information sharing can bring more salient benefits.

The organization of the paper is as follows. The next section reviews the related literature on supply chain coordination and supply chain financing. Section 3 describes the financing problem under this study. Section 4 discusses the base case of a fully integrated financial supply chain. Section 5 analyzes each party’s self-interested independent decision-making and derives conditions for coordinating parameters in the proposed loan contract. Section 6 presents a case study to validate the theoretical analysis above and illustrate profit allocation among the lender, retailer and manufacturer. The resulting channel performance is then compared with two benchmark contracts: the wholesale-price contract and the buyback contract. The impact of exogenous and endogenous parameters on the channel performance under three different contracts are further explored. The last section is reserved for conclusions and discussion, and all proofs of the propositions can be found in the appendix.

Literature Review

Our research lies at the interfaces of operational and financial decision-making in supply chain collaboration. In this section, we will review the most relevant literature in the streams of coordination contracts and supply chain financing.

Facing the challenge of global competition, enterprises seek to strengthen cooperation with their partners along supply chains to increase their competitiveness. It is well documented in the literature and practice that optimization made by a supply chain participant can lead to suboptimal outcome for the supply chain as a whole (Cachon, 2003; Hwan Lee & Rhee, 2010). To reduce this type of supply chain inefficiency, there are extensive studies in the literature proposing diverse coordinating mechanisms to align actions of each party in the chain to achieve better overall performance. The most extensively discussed coordination contracts include wholesale-price contracts (Chen, 2011; Choi & Guo, 2020; Özer et al., 2011), Two-part tariff contracts (Bonnet & Dubois, 2010; Cachon & Kök, 2010), revenue sharing contracts (Adida & Ratisoontorn, 2011; Cachon & Lariviere, 2005), buyback contracts (Doganoglu & Inceoglu, 2020; Hwan Lee & Rhee, 2010; Pasternack, 1985), quantity discount contracts (Chen, 2011; Su & Mukhopadhyay, 2012), and rebate induced contracts (Saha, 2013). For a comprehensive review of studies in coordination contracts in a stylized two-level supply chain, please refer to Cachon (2003) and Govindan et al. (2013).

Early research about supply chain coordination focused on operational decision. However, with increased financial pressure faced by global supply chains, studies about efficient supply chain financing are growing. Hwan Lee and Rhee (2010) investigate the impact of four widely discussed coordinating contracts on financing costs, and conclude that these contracts fail to achieve channel profit maximization if each supply chain partner seeks direct financing from a financial institution. Kouvelis and Zhao (2011) study a wholesale-price contract between a supplier and a financially constrained retailer, whose failure of loan repayment leads to a costly bankruptcy. Later, the authors (Kouvelis & Zhao, 2012) consider a trade credit contract for the same problem and conclude that the trade credit contract improves the supply chain efficiency. Luo and Zhang (2012) trade examine a similar problem and conclude that using trade credit can coordinate the supply chain with symmetric information, but fail to achieve it when information is asymmetric. Raghavan and Mishra (2011) investigate a capital-constrained supply chain and show that a lender who finances the manufacturer has a motivation to finance the retailer as well. Jing et al. (2012) study a similar case and demonstrate that, to improve the overall supply chain efficiency, the bank should finance the manufacturer if the production cost is low, but finance the retailer otherwise. Kouvelis and Zhao (2018) examine the impact of the credit rating of the supplier and show that there exists a threshold for it above which the supplier should offer trade credit. Hua et al. (2019) study a supply chain with a capital-constrained retailer ordering via the option contract from a supplier. Their analytic results show that in the presence of the retailer’s bankruptcy risk, the supplier should always finance the retailer at the risk-free interest rate. Ding and Wan (2020) consider a supply chain with a capital-constrained supplier and propose pay back contracts for the manufacturer to share the production risk. Recently, with multiple case studies, Martin and Hofmann (2019) pointed out that buyers increasingly offer financing alternatives to their suppliers. They emphasize that financial strategy alignment is a key prerequisite for successful supply chain finance practices.

The literature discussed above suggests that the way of financing supply chains plays an essential role in the channel performance. However, existing studies about coordination for financing supply chains is still limited. Dada and Hu (2008) consider a supply chain with a cash-constrained supplier and derives a non-linear loan schedule to achieve channel coordination. Lee and Rhee (2011) propose that suppliers can use trade credit plus markdown allowance to fully coordinate retailers’ decisions of order quantity to maximize the channel profit. Kouvelis and Zhao (2016) study contract design and coordination of supply chains with capital-constrained suppliers and retailers. They compare and evaluate the performance of revenue-sharing, buyback, and quantity discount contracts in the presence of default costs. Later, Kouvelis et al. (2018) extend the discussion to situation where the price of raw material is fluctuating. Yan and Sun (2013) study a supply chain finance problem with a manufacturer, a cash-constrained retailer and a commercial bank. They design a coordination mechanism using a wholesale-price contract with a finite loan scheme. Moussawi-Haidar et al. (2014) consider a three-level supply chain consisting of a capital-constrained supplier, a retailer, and a bank, and coordinate their decisions to minimize the total supply chain costs with delays in payments and a discount on the interest rate. They conclude that the proposed coordination mechanism achieves significant cost reduction. Xiao et al. (2017) consider a financially constrained supply chain in which a retailer has no access to bank financing due to low credit rating. They show that the revenue-sharing and buyback contracts can coordinate the supply chain, but only when the supply chain has a sufficient total working capital.

In the lase decade, the development of Internet technology has dramatically changed the traditional way of financial services in practice, such as payment, settlement, and risk management (Dong et al., 2020; Zhao, 2018). Financial innovations, such as online lending (Balyuk & Davydenko, 2019; Bertsch et al., 2020) and P2P lending (Serrano-Cinca & Gutiérrez-Nieto, 2016; Zhao et al., 2017), are creating opportunities and challenges for both borrowers and lenders. Within this context, this paper aims to coordinate a three-level financing supply chain consisting of an online retailer, a manufacturer, and their e-commerce platform-backed finance company. Both the retailer and the manufacturer are capital-constrained and wish to get loans from their e-commerce platform-backed finance company. Based on shared transaction data and monitored sales accounts, a tripartite loan contract is proposed to coordinate each participant’s decision to achieve the maximum channel profit and realize a flexible profit allocation. We prove that this contract design provides all parties with incentives to adopt this loan contract and each party’s profit can be improved.

This research differs from the earlier studies in supply chain finance from multiple aspects. First, the problem context is different. To the best of our knowledge, a financial supply chain consisting of an online retailer, a manufacturer, and their e-commerce platform-backed finance company has not been analytically discussed in literature so far. Most of existing studies about internet finance are qualitative or empirical (Zhao, 2018). Second, most previous research focused on coordination between retailers and manufacturers, while this study aims at coordinating a three-level supply chain finance (lender, retailer, and manufacturer) using loan contracts with adjustable loan contract parameters. Third, we apply the classical idea of risk and revenue sharing in supply chain coordination to demand information sharing, which has recently become feasible due to the development of modern Internet technology. Finally, sales accounts monitored by the e-commerce platform and repayment allocation order are designed as a way of risk control and loan settlement for the lender.

Problem Description

We consider a single-period product supply chain consisting of an online retailer and a manufacturer. Both of them are capital-constrained and wish to reduce working capital requirements by getting loans from their e-commerce platform-backed finance company. They face a situation similar to the classical newsvendor problem, where the retailer orders a single product from the manufacturer, and then sell it to final customers through an e-commerce platform, not knowing the actual demand at the time ordering. To get the loan from the platform-backed lender, the retailer agrees to release the transaction data from the platform to the lender for monitoring sales trend and estimating future demand. The retailer also agrees to receive sales revenue through a dedicated online account, which will be monitored by the lender and used preferentially for loan repayment. Based on historical transaction data, the lender decides whether or not to lend the money.

Let random variable

The cash constraints and the financing problem faced by the supply chain under the study is described as follows. At time zero, the retailer orders

Let the risk-free interest rate of the capital over period

Ll Loan amount specified in the contract (Lender’s decision variable);

Q Retailer’s order quantity (Retailer’s decision variable);

p Retail price per unit of product at time T;

c Production cost per unit of product;

w Wholesale price per unit of product;

Bm Own capital of the manufacturer invested in producing q products;

r Lender"s interest rate specified on the contract;

rf Lender"s risk-free interest rate;

φ Proportion of revenue shared to the retailer, where as the manufacturer’s is 1 φ;

ξ Customer demand during period T;

f(ξ) Probability density function of the customer demand; and

F(ξ) Cumulative distribution function of the customer demand.

The financing problem described above can then be characterized by a set of exogenous parameters

Centralized Financing Model

In this section, we first consider the base case of an integrated financing supply chain, where the lender, the retailer and the manufacturer act as an entirety. Then, we will discuss the optimal production quantity and corresponding profit for the whole channel under this circumstance.

Let πI denote the expected total profit of the integrated financing supply chain during period

where

Proposition 1 states that in the centralized financing model, where the lender, retailer and manufacturer aim to optimize the overall profit, πI is strictly concave in the production quantity

Coordinating Loan Contract

In this section, we propose a coordinating loan contract, which aligns the decision-making of these three parties in the supply chain finance described in Section 3. This proposed tripartite loan contract can be characterized by a set of three endogenous parameters (

In addition, this loan contract prescribes that the sales revenue realized on the e-commerce platform will be collected into a dedicated account monitored by the lender, which will be used for the loan repayment first. After making the full repayment

In the decentralized model, the sequence of events under the proposed loan contract is as follows.

At time zero, the lender, the retailer, and the manufacturer sign the tripartite loan contract (

Based on the tripartite loan contract above, the lender determines the loan amount

Based on the tripartite loan contract above, the retailer determines the order quantity

The manufacturer produces

The retailer sells the product at price

At the end of the sales season

In the proposed loan contract above, by consolidating demand information with financing services of e-commerce platforms, we extend two core ideas of supply chain cooperation—alliance formation and profit allocation—to financing e-commerce supply chains. By designing the priority and proportion of profit allocation appropriately, the proposed loan contract can motivate each party to make decisions identical to those in the centralized model, and further increases each partner’s benefit.

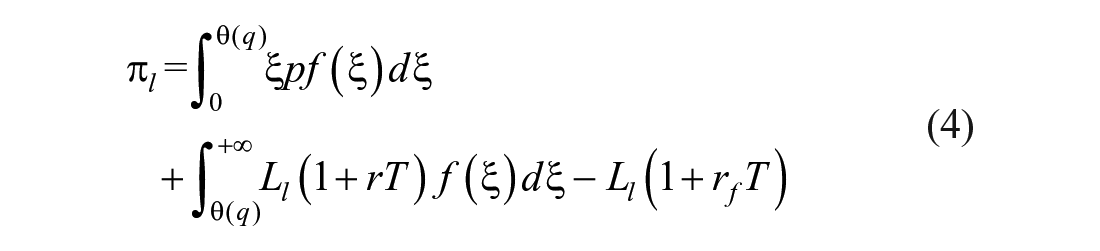

Lender’s Expected Profit

In this problem, the lender retrieves the product demand information directly from the e-commerce platform with an understanding that the retailer and the manufacturer are linked in this product supply chain. Both the retailer and the manufacturer are cash-constrained, and the lender needs to decide the amount of capital lent to the retailer and the manufacturer for production preparation under the contractual agreement. Given that the retailer and the manufacturer are cash-constrained, the loan amount offered by the lender will determine the quantity of the product that the manufacturer can produce. Specifically,

Let

The proof immediately follows.

When the realized demand is less than the threshold

Proposition 2 states that given the priority in revenue allocation for loan repayment under the proposed loan contract, the lender’s decision-making about the loan amount, which indirectly determines the quantity of the product that the supply chain can offer, can be simplified as a newsvendor problem.

Meanwhile, with the priority in revenue allocation specified in the loan contract, the sales revenue will be used to repay the lender’s loan first. Therefore, when the realized demand is equal to

Retailer’s Expected Profit

Now we turn to the retailer’s decision-making about the order quantity

As a result, the expected profit of the retailer is

Proposition 3 implies that when the profit margin, that is

Manufacturer’s Expected Profit

The manufacturer implements a make-to-order production strategy. In addition, the manufacturer agrees to invest the initial capital

It is worth noting that in the decentralized model, it may not be possible to realize the retailer’s optimal order quantity

Coordinating Decisions Through the Loan Contract

In this subsection, we develop the framework that coordinates each party’s decisions through the proposed loan contract. This framework can entice the decentralized model to achieve the optimal outcomes attained in the centralized model in Section 4.

1. (

2.

Under the proposed coordinating loan contract, when the realized demand is equal to

Proposition 6 suggests that when the manufacturer invests less(more) with his/her own capital, the lender charges a higher(lower) interest rate to align decision-makings of other parties. With the stochastic product demand in the market, a lower amount of the manufacturer’s own capital implies that the lender is exposed to a higher risk under this circumstance. As a result, the lender charges a higher interest rate for the greater risk. If the interest rate

In summary, we have proven that by choosing appropriate parameters (

Case Study

In this section, we conduct a case study of an international cosmetics company located in Guangzhou, China, to illustrate the coordination mechanism of the proposed loan contract and how the profit shall be allocated among channel participants.

Background of the Company

This case study examines the management challenges of a global cosmetics manufacturer, which produces and sells cosmetics such as skin care, hair care, and make-up products. This company’s head office, purchasing, sales and distribution outlet are all located in the heart of Guangzhou, China. Meanwhile, the company operates a factory, warehouses and a regional R&D center in a suburb, about 70 km from the head office. The company has a significant number of branches all over the country, each hosting one or more warehouses, and also overseas regional offices such as those in Australia, Malaysia, Indonesia, South Korea, and Vietnam. Through a network of retailers comprising 6,000 beauty boutiques and 1,000 beauty counters, the company sells various products overseas and distributes products locally. Additionally, this company offers products through direct selling in major cities.

In 2003, this company recorded sales of 2.4 billion yuan (US $385 million), but sales started to step down since then. From 2004 to 2008, the revenue decline was around 20% each year. Although closed several branches, pulled out of markets such as South Korea and Vietnam, laid off employees, and adopted cost-cutting measures in 2008, the company still could not fully recover from the downward trend. The sales went to 1 billion yuan (US $160 million), 700 million yuan (US $112 million), 600 million yuan (US $96 million), and 350 million yuan (US $56 million) from 2011 to 2014, respectively. The continuous declines were observed in 2015 and 2016 as well.

There were several reasons behind the disappointing financial performance such as dated branding, impacts from competitors, uncompetitive commission structure, and so on. However, among all of these, the most crucial reason was dysfunctional supply chain. The company used to be very successful in direct-marketing. However, in 1998, the Chinese government officially banned direct marketing and the company had to move to retail. Later in 2006, a set of new rules was released by the government which allowed companies to apply for a Direct Sales License for conducting single-level direct marketing. However, over this period, conventional retail sales has been replaced by online sales. Since then, this company has been losing marker share and could not maintain effective control over distribution channels.

In 2014, the company decided to embrace e-commerce and started to turn the direct-selling strategy to a digital strategy. Since then, the company has invested a lot into building partnerships with e-commerce platforms, such as JD.com and Tmall. As one of the efforts to strengthen cooperation with online retailers, the company helps partnered online retailers apply for procurement financing from JD finance to reduce their working capital requirement. With a tractable transaction record, most of the partnered online retailers on JD.com can successfully apply for procurement loans from JD finance.

The proposed loan contract aims to provide financing solutions which are likely to help the company establish demand-driven supply chains within this context. For example, by promoting the proposed loan contract, the company can reduce the capital threshold of entry for partnered online retailers and help increase their profits. In this way, the company can drive the entire supply chain more efficiently.

Coordination Mechanism of the Proposed Loan Contract

In this subsection, we conduct a case study of a supply chain consisting of this company and an online retailer for a single product, whose selling price

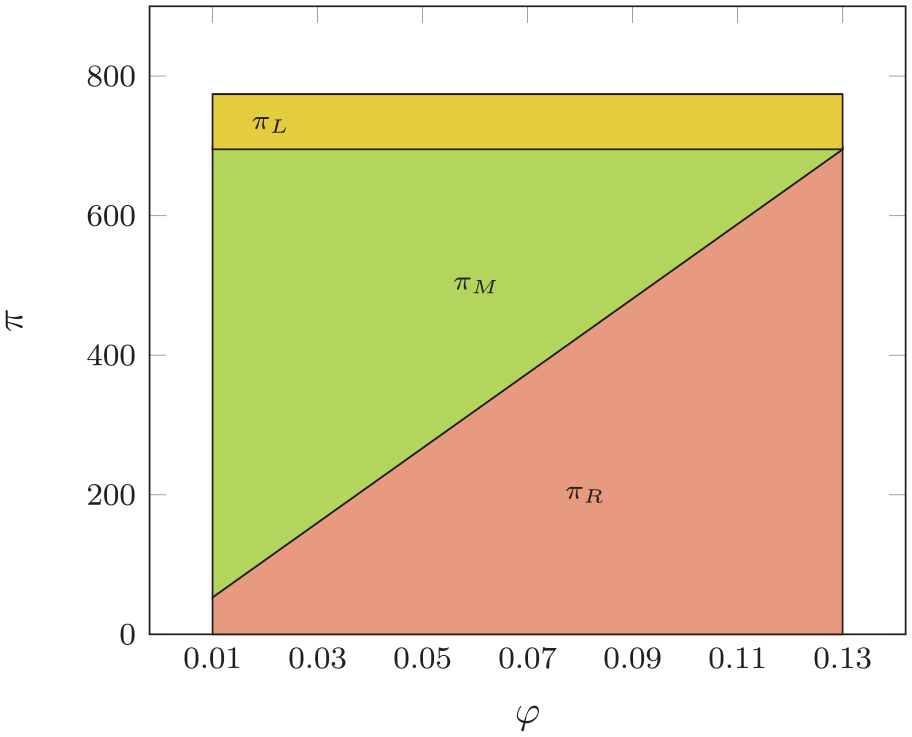

Expected Profits Resulting From the Centralized and Decentralized Models for the Financing Problem With a Set of Exogenous Problem Parameters (

Table 1 provides the following observations. First, the decentralized model can achieve the same decision and outcome as in the centralized model, which is visualized in Figure 1. Second, there exist multiple contract parameters which can achieve channel coordination. Third, while the values of

Coordination in decentralized model with exogenous parameters (

Impact of contract parameters (

Impact of contract parameter

Comparative Analysis

In this subsection, we compare the total channel profit and profit allocation of the proposed loan contract with two benchmarking contracts: (1) the wholesale-price contract between the manufacturer and the retailer, where coordination does not take place; and (2) the buyback contract coordinating the manufacturer and the retailer.

Benchmarking model 1: The wholesale-price contract between the manufacturer and the retailer without any coordination

In this scenario, we consider a wholesale-price contract between the manufacturer and the retailer. Both the retailer and the manufacturer are capital-constrained. Given the wholesale price

The optimal order quantity

The corresponding expected profits for the manufacturer, retailer, and lender are derived respectively as follows.

Benchmarking model 2: The buyback contract coordinating the manufacturer and the retailer

In this scenario, we consider a buyback contract to coordinate the decisions of the manufacturer and the retailer, where the manufacturer charges the retailer

For the product supply chain with cash constraints, the optimal order quantity,

Let

The expected profits for the manufacturer, the retailer, and the lender are derived as follows respectively.

Performance evaluation

We illustrate the performance of our proposed loan contract by conducting a numerical experiment on the problem with a selected set of exogenous parameters:

Channel Performance and Profit Allocation Under Wholesale-Price Contract, Buyback Contract, and Proposed Loan Contract for the Problem With a Selected Set of Exogenous Problem Parameters: (

Note: The maximum profits are in bold.

Table 2 shows that, compared with the wholesale-price contract and the buyback contract, the proposed loan contract not only realizes the highest total channel profit, but also leads to the highest profits for the lender and the product supply chain. In addition, distribution of profits among three partners are more flexible and better balanced. For example, to achieve coordination between the manufacturer and the retailer, the buyback contract has to set a high buyback price to encourage the retailer to order, which results in that a majority of the total profit is attained by the retailer, which may discourage the participation of the manufacturer. While for the proposed loan contract, with the

Sensitivity Analysis

In this subsection, we will examine the effects of exogenous problem parameters on the proposed loan contract’s performance in detail.

Effect of the cost-to-retail ratio

To examine the effect of the Cost-to-Retail Ratio

Effect of the Cost-to-Retail Ratio on the Performance of the Wholesale-Price Contract, the Buyback Contract, and the Proposed Loan Contract for a Selected Set of Exogenous Problem Parameters (

Table 3 provides the following insights. The proposed loan contract strikes a more balanced profit distribution between the lender and the product supply chain. For example, when Cost-to-Retail Ratio is 0.8, for the proposed loan contract, the lender obtains a profit of 76 (9.8%) out of the total 774. However, the lender obtains only a profit of 0 out of 338 with the wholesale-price contract, or a profit of 36 out of 717 (5.0%) with the buyback contract. This suggests that, with the classical wholesale-price contract and buyback contract, the role of the lender has only mild or even no effect. When the Cost-to-Retail Ratio increases, that is, the profit margin becomes lower and there is less to share among partners, this benefit is even more significant and more important. As we can see, when the Cost-to-Retail Ratio increases further to 0.9, that is, the cost accounts for 90% of the selling price, the capital cost starts to become a huge burden for the manufacturer. With the wholesale-price contract, due to high production and capital cost, the profit for the manufacturer becomes negative, which implies that the originally profitable business may fail because of financing cost. Under this circumstance, the buyback contract is not very favorable neither. To avoid a high capital cost, the production quantity is as low as 19, which leads to a small profit for the whole channel, 60, half of that for the proposed loan contract. On the contrary, the proposed coordinating loan contract still can attain a reasonably good profit and profit allocation. Such improvement is indeed very crucial to the success in this financing supply chain because it makes otherwise unprofitable business profitable by coordinating the parties involved.

Effect of risk premium

To examine the effect of the risk premium on the proposed loan contract’s performance, we adjust the exogenous risk-free interest rate

Effect of the Risk Premium on the Performance of the Wholesale-Price Contract, the Buyback Contract, and the Proposed Loan Contract for a Selected Set of Exogenous Problem Parameters (

FromTable 4, we observe that when the risk premium increases, the lender gains a higher proportion of the channel total profit. As we discussed in Section 5.4, this is because, for the proposed loan contract, to achieve the channel coordination, a higher lending interest rate co-occurs with a larger loan amount, which all together leads to a higher profit sharing portion for the lender.

Effect of demand variability

To examine the effect of demand variability on the proposed loan contract’s performance, we vary the demand distribution of the product among

Effect of Demand Variability on the Performance of the Wholesale-Price Contract, the Buyback Contract, and the Proposed Loan Contract for a Selected Set of Exogenous Problem Parameters (

FROM Table 5, first of all, we observe that, under a certain average demand level, as demand variability increases, the optimal production quantity and the expected total channel profit increase with all three contracts. This is because that given the production cost is lower than the retail price, the possibilities of higher demands leads to a larger optimal production quantity, which, in turn, leads to a higher expected total profit.

Secondly, compared with the wholesale-price and buyback contracts, the improvement in channel efficiency brought about by the proposed loan contract is quite stable. The proposed loan contract increases the total channel profit of the wholesale-price contract by 53% and the buyback contract by 8%, respectively, under all three demand distributions. Further, Table 5 shows that the profit allocation among three parties with the selected endogenous contract parameters (

Conclusions

This paper considers a supply chain consisting of an online retailer and a manufacturer in the context of e-commerce, both facing capital constraints and seeking funding from their e-commerce platform-backed finance company. Based on shared transaction data and monitored sales accounts, we propose a tripartite loan contract to coordinate the decision-making of three parties in this supply chain financing problem.

We prove that, under this proposed loan contract, the decentralized decision-makings of each party duplicate the optimal channel performance of a fully integrated decision-making framework. A case study is then conducted to demonstrate the performance of the proposed loan contract. The numerical results show that, compared with the other two benchmarking contracts (wholesale-price and buyback contracts), the proposed loan contract improves both the total profit of the channel and the profit of each party. This indicates that it offers each party certain incentive to participate in the proposed contract. Furthermore, there exists multiple sets of coordinating parameters for this proposed contract, allowing a high degree of flexibility in revenue allocation among participants based on their bargaining powers. At last, we analyze the effects of the cost-to-retail ratio, risk premium, and demand variability on the performance of the proposed loan contract. We found that the profit allocation resulted from the proposed loan contract is more balanced when the cost-to-retail ratio or risk premium is high.

Theoretical Contributions

This research contributes to the literature on supply chain coordination. The previous literature in supply chain coordination has largely focused on operational decisions and constraints, such as prices and stocking levels, and ignored the role played by capital constraints (Adida & Ratisoontorn, 2011; Cachon & Kök, 2010; Cachon & Lariviere, 2005; Choi & Guo, 2020; Doganoglu & Inceoglu, 2020; Hwan Lee & Rhee, 2010; Özer et al., 2011). Our research differs from previous studies by extending the idea of coordination to a three-level supply chain financing problem (lenders, retailers, and manufacturers). Specifically, with the proposed loan contract, we align the decentralized decision-makings of each party (lenders, retailers, and manufacturers) and duplicates the optimal channel performance under a fully integrated decision-making framework. We prove that, with adjustable contract parameters, the proposed loan contract improves both the total profit of the channel and the profit of each party in a decentralized decision-making environment. It provides important and necessary incentives and motivations for all parties in supply chain financing to participate and cooperate in the proposed loan contract.

This research also contributes to the literature in Internet financing and information sharing. Recently, scholars have been substantially attracted to financial innovations enabled by the development of Internet technology, such as online lending (Balyuk & Davydenko, 2019; Bertsch et al., 2020) and P2P lending (Serrano-Cinca & Gutiérrez-Nieto, 2016; Zhao et al., 2017). However, the discussion on sharing transaction data to justify loan applications is still limited in the literature (Pei & Yan, 2019). Substantial research has investigated the value of information sharing on inventory or replenishment management (Cachon & Fisher, 2000; Lee et al., 2000). Nevertheless, the benefit of information sharing is largely overlooked in credit verification in the existing literature. Our study, with analytical analysis and numerical examples, shows that the business history recorded on e-commerce platform can be employed by platform-backed finance companies to coordinate supply chain financing and achieve flexible revenue allocation.

Managerial Implications

This research presents implications to supplier-e-tailer supply chains and platform-backed finance companies to create win-win-win solutions through loan contracts and information sharing. Over the past decades, e-commerce platforms make it easier for small businesses to reach their consumers. Therefore, it is not uncommon that many businesses on e-commerce platforms run by micro-enterprises, and for which financial constraints are typical obstacles to their growth. Our study demonstrates that their online transaction data can be employed to justify their loan applications from their platform-backed finance companies, for which information distortion is not a concern. On the other hand, due to recent rapid development of platform-backed finance companies, financial practices in such loan contracts, such as information sharing, loan settlement, and risk management, have become much easier to implement. For example, the platform-backed finance companies can take advantage of dedicated accounts monitored by e-commerce platforms, like Alipay, for loan settlement and revenue allocation to control the risk.

Limitations

There are certain limitations in our study. First, we assume all parties analyze historical sales data in the same way and come up with similar estimates about future product demand. This is not necessarily true. Even with the same historical sales records, lenders, retailers and manufacturers can come up with different demand forecasts. Second, we assume that the manufacturer is flexible with the initial investment in production preparation. Thus, the proposed loan contract can be negotiated about the loan amount, interest rate, and revenue sharing ratio. If there exists strict capital constraints for the manufacturer, the proposed loan contract may not work. There are several research directions worth exploring in the future. Assessing the risk faced by the lender in such a loan contract is important since there is no collateral. The change in the demand may greatly impact the sales revenue, and therefore affect the loan repayment. In addition, fluctuation in retail price may exacerbated this risk.

Footnotes

Appendix

Proof of Proposition 1. The total profit of the centralized financing supply chain is given by

Taking the second order derivative of πI(q) with respect to

Therefore, πI(q) is strictly concave in

Proof of Proposition 2. The lender’s profit in the decentralized model with coordinating loan contract is given by

Taking the second order derivative of πl (q) with respect to

where

Taking the first order derivative of πl (q) with respect to

Proof of Proposition 3. The retailer’s optimal profit in the decentralized model is

Taking the second order derivative of πr(q) with respect to

When

Proof of Proposition 6. The private capital of the manufacturer,

It can be further written as

an implicit function

Using the implicit function theorem, we have

When

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported in part by the National Natural Science Foundation of China [grant number 71801233].