Abstract

Tax credits for investment in productivity enhancement facilities, R&D facilities, and employment-creating initiatives are available to corporate taxpayers in Korea. These incentives are intended to motivate corporations to invest by providing financial support to improve their efficiency and help sustain their survival. This study aims to analyze whether corporations that claim investment tax credits (ITCs) in Korea actually achieve investment efficiency and increase corporate value. This study’s results are as follows. First, based on the statistical analysis of samples from small- and medium-sized enterprises (SMEs) and all corporations, we find empirical evidence that investments through claimed tax credits are inefficient from the standpoint of Tobin’s Q. This finding may be interpreted to mean that corporate taxpayers, including SMEs, consider tax savings more than investment efficiency in claiming ITCs. Second, in testing the investment efficiency for each ITC, we find that SMEs’ investment via employment-creating ITCs is more efficient than other investments with tax credits. This finding implies that SMEs should not only invest in physical facilities, but also retain human resources for sustainability. These results provide policy implications that employment creation should be considered when granting ITCs for SMEs’ efficient investments.

Keywords

Introduction

Corporate investment plays an important role in increasing future growth and profitability, given that investment creates opportunities to increase competitiveness in the market and corporate value. Accordingly, efficient investment is essential to increase corporate sustainability, and through such investments, future business opportunities can be expanded, and firm value can be increased (Dejan Ravšelj et al., 2019). The tax system is one of the factors that drive a corporation’s investment. Many previous studies have provided empirical evidence that the tax system can affect the investment behavior of a corporation and have suggested that tax credits can affect these investments (Ahn, 2011; Azevedo et al., 2021; Cummins et al., 1996; Egger et al., 2020; Pham, 2020; Rao, 2016; Sen & Turnovsky, 1990).

However, whether corporate investments with tax credit only receive tax benefits from the government or whether investment outcomes lead to future profitability, increase in firm value, and sustainability assurance remains unclear. Government support for corporations’ investment via tax credit may increase investment and potentially increase firm value (Chen & Yang, 2020; Dary & James, 2019; Luo et al., 2020; Lyon, 1989). However, the tax benefit allowed for assets designated under the tax law may induce investment in tax-preferred assets only, causing distortions to corporations’ overall investment, thereby lowering the level of profitability or cash flow to corporations (Hines & Park, 2019).

Under Korean tax law, investment tax credits (ITCs) are available for corporate taxpayers investing in productivity enhancement facilities, R&D facilities, and facilities with job creation to encourage investments by reducing tax burdens on corporations. If the investment is made in the qualified assets under the tax law, it will be a considerably more efficient investment than an investment made without tax credit because cash outflow from tax payment is reduced by the amount of ITC. However, if a corporation only considers the tax factor and fails to make a holistic investment decision, the investment will potentially fail. This phenomenon occurs because a corporation may make a non-optimal decision by focusing on tax-favored assets under the tax law and miss non-tax factors for an optimal investment.

The foregoing discussion may be more relevant to small- and medium-sized enterprises (SMEs) because they generally receive more investment incentives, including tax credits from governments, compared to non-SMEs. In addition, SMEs inevitably make and expand their investment to achieve higher sustainability and future growth potential (Chiao et al., 2016). In this regard, the relationship between tax incentives and investments for SMEs may be more pronounced than that for non-SMEs. Thus, analyzing whether SMEs’ investments in ITC increase the efficiency of the investment or simply lower the tax burden is noteworthy.

Prior studies on investment incentives, including tax credit, focus on how much investment increases because of incentives. In other words, prior studies mainly attempt to assess the effectiveness of these incentives by quantitatively analyzing the extent of investment increase. However, beyond the quantitative analysis of these investments, it is worthwhile to analyze how these quantitative investment incentives improve the qualitative share value of a corporation.

Therefore, this study aims to analyze whether investments that have received tax benefits have high investment efficiency using samples of Korean corporations that actually claimed ITC. In particular, ITC is available at preferential rates to Korean SMEs for various investments, such as investment in productivity enhancement facilities, R&D facilities, and facilities with employment. The government supports these types of investments because they are essential to ensuring the sustainable growth and survival of SMEs. Therefore, this study aims to answer the following research questions in the context of the ITC investment system.

First, it analyzes whether the investments of corporations receiving tax benefits, including SMEs, have high investment efficiency. We examine whether corporations’ investments are limited to tax savings only or efficient enough to lead to future sustainability.

Second, this study analyzes the investment efficiency of SMEs claiming the ITC. This approach is intended to analyze the level of investment efficiency of SMEs, which do not have sufficient manpower and management skills compared with large entities.

Third, among ITCs, such as facility investment for productivity improvement, R&D investment, and investment in job creation, this study investigates which investment is effective for SMEs.

This study contributes to the literature in the following ways: First, this study is distinguished from prior studies as it examines whether the value of corporate taxpayers who make investments and receive ITCs has increased. Prior research is limited to the investigation of whether governmental investment incentives, such as tax breaks, spur the investment of corporate taxpayers from a quantitative perspective. Second, this study provides test results based on data on ITCs claimed by corporate taxpayers, which increases the creditworthiness of the test results. Third, this study divides corporate investment into categories. We then analyze the effects of each investment category’s efficiency in adding value to the corporation as a whole, unlike prior research, which focused only on overall facility investment.

The remainder of this paper is organized as follows. Section 2 introduces the Korean tax incentive on investment and provides a review of the ITC and investment efficiency literature. Section 3 provides the hypotheses, research methodologies, and sample selection for the empirical research design. Section 4 reports the results of descriptive statistics and regression analysis. Finally, Section 5 summarizes the study results and presents the conclusions.

Korean Taxation for Investment and Literature Review

Korean Taxation for Investment

Tax incentives for Korean corporations’ investments are provided mainly at the determined tax calculation stage. In other words, investment is encouraged more through ITC than through accelerated depreciation or income deduction in Korea. In particular, more ITCs are provided to SMEs as a part of SME promotion policy.

These ITCs include the productivity enhancement facility ITC (hereinafter, “productivity ITC”), R&D facility ITC (hereinafter, “R&D ITC”), and ITC for investment with employment creation (hereinafter, “employment ITC”). Although various tax credits are available to SMEs in Korea, in addition to these tax credits, we mainly review three ITCs because other ITCs are insignificant and are limited to certain types of industries (e.g., pharmaceutical industry).

Productivity ITC has been implemented as an industrial support policy to enhance competitiveness by improving corporate productivity and the stability of the national economy. In the past, the industrial support tax system used to be applicable to a few specific industries; however, the system was amended to support areas that require common efforts across industries. Productivity ITC can be said to be a direct tax reduction system that brings direct financing effects to corporations; thus, the tax law sets the requirements for the claim of productivity ITC and follow-up maintenance. The facility scope for productivity ITC includes a facility that improves the production process or a facility for the automation and informatization of production and corporate management. The applicable rates for productivity ITC are 7% for SMEs and 1% to 3% for non-SMEs.

The R&D ITC supports investment in research and testing facilities and vocational training facilities, where research and testing facilities are for R&D and include dedicated facilities for strengthening national science and technology competitiveness. The applicable rates for R&D ITC are 6% for SMEs and 1% to 3% for non-SMEs.

An employment ITC is an employment-creating ITC that is claimable in proportion to the number of employees hired by a corporate taxpayer. Employment ITC is noticeably different from other ITCs in that employment ITC considers investment in physical facilities and employment. The ITC is applicable to investments in newly acquired facilities used by businesses. Employment ITC is claimable at a designated percentage of the investment made during the tax year. However, the amount of employment ITC can be further increased (or decreased) if the number of employees hired by a corporate taxpayer is higher (lower) compared with prior tax years. The applicable rates for employment ITC are 8% to 9% for SMEs and 5% to 8% for non-SMEs, which are subject to the number of employees.

Currently, productivity and R&D ITCs are integrated into a single tax credit system for investment in specific facilities. Employment ITC has been changed to tax credit claims for corporations that increase jobs without investments.

Based on a review of the three ITCs, the following are observed: First, the amount of the ITC claimable is determined at certain percentages of the amount of assets invested. However, the amount of claimable employment ITC is also affected by employment level. Second, SMEs may take more tax credits than non-SMEs, which is the case for all the tax credits discussed.

This study reviews the literature related to the ITC, the ITC’s investment inefficiency, and the research results thus far. Previous studies related to ITC generally conclude that the government’s tax benefits induce companies to increase their investments. Meanwhile, prior studies related to investment inefficiency have focused on corporate characteristics such as corporate management’s opportunistic behavior and corporate governance.

Literature Review on ITC

Generally, studies on investment-related taxes and tax credit systems have used structural models. Extensive follow-up studies have been conducted based on Harberger’s (1964) corporate tax effect, Jorgenson’s (1963) user cost theory, Hall and Jorgenson’s (1967)Q theory, and Summers (1981). Most of these studies estimate the investment function in a manner consistent with the prediction of the q theory (Auerbach & Hassett, 1992; Cummins et al., 1996; De Long & Summers, 1991; Goolsbee, 2003; Hayashi, 1982; Salinger, 1983). However, only a few studies have investigated the effect of the temporary ITC system, which is distinguished from the permanent tax reform effect, due to the difficulty of identification or not obtaining such an effect. Cohen and Cummins (2006) and Knittel (2007) reported that a meaningful investment response is unavailable even if a more generous depreciation is temporarily allowed. The general approach is to obtain a sense of the policy effect through a study that applies a macro model that assumes a general equilibrium to the investment model and includes a permanent corporate tax reduction system and the ITC (Abel & Elberly, 1982; House & Shapiro, 2006). In other words, the effect of the ITC system is commonly understood more structurally through a calibration method that examines the impact–response to determine how the temporary reduction of investment costs is shown under the economic fluctuation model, and the pattern is compared with the actual data (Abel & Elberly, 1982). However, only a few approaches are available for empirical analysis using micro company data on how the investment response appears in practice. Moreover, the effect of a short-term temporary ITC system during a recession period is difficult to characterize and analyze.

In addition, a few studies have applied quasi-experimental attempts to compare the level of investment before and after changes in the corporate tax system; these studies have used techniques in the fields of labor economics and applied metrology economics (Eissa & Liebman, 1996; Woo & Jun, 2009). Auerbach and Hasset (1992) showed that a correlation exists between tax change and investment composition in the 1986 TRA period in the United States, and this correlation was estimated as the effect of tax on investment. Recently, House and Shapiro (2008) presented and analyzed a methodology to identify the effect of providing a depreciation allowance bonus with a predetermined time limit. By identifying the effect of such accelerated depreciation, they theoretically and empirically show that the price elasticity of the supply of investment goods, not the investment act, is extremely high.

Based on the analysis that ITC and investment size have a positive relationship with Korean corporate data, studies suggest that investment elasticity exists in ITCs. H. S. Kim (2007) estimated the GMM using corporate panel data from 2002 to 2004, and when 1% is reduced in corporate investment costs due to tax credit, major corporations are 0.37% to 0.80%, and SMEs are 0.47% to 1.41%. Research results that further increase investment when ITCs increase are also presented. In addition, the results show that the tax price elasticity of long-term investments is 0.73 to 2.06 for small corporations and 0.52 to 0.92 for medium corporations.

Song (2009) also applied a fixed-effects model to corporate panel data from 2002 to 2005 in Korea. Consequently, major corporations showed almost unit elasticity by increasing their investment by 0.99% to a 1% reduction in corporate investment costs. SMEs’ investment increases by only 0.054%, which shows the relatively high effectiveness of tax support in large corporations. In addition, D. H. Kim (2006) analyzes the effect of tax reduction and exemption using the effective corporate tax rate and finds a significant negative relationship between investment and effective corporate tax rates. On this basis, an effect of tax support, such as tax credit, exists.

Ahn (2011) analyzed SMEs in the manufacturing industry from 2005 to 2009, showing that investment increased significantly in the group with a high tax burden, and no significant change occurred in the group with a low tax burden if tax credit is provided. The author proved that the investment intention and size of a company are influenced by the degree of corporate investment-related tax benefits. In addition, S. H. Kim and Son (2006) used corporate cross-sectional data that included tax reductions and exemptions in 2001, suggesting that the elasticity of the investment scale for tax credits is 0.7739 to 0.7792 and that an increase in tax credits promotes corporate investment.

Weon and Kim (2006) analyzed the effect of investment-related tax credit systems on investment using data on tax reductions and exemptions of Korean corporations from 2002 to 2003 by dividing the sample into large firms and SMEs. They present empirical evidence that the ITC has a positive effect on corporate investment, and the investment elasticity is more than twice that of large firms (0.306) than that of SMEs (0.135).

Literature Review on Investment Inefficiency

Investment efficiency is directly related to the firm value. An efficient investment increases firm value by generating a positive net present value for the firm, whereas an inefficient investment leads to over-or underinvestment and reduces firm value. Therefore, investment activities that determine investment efficiency are an important part of corporate management. Thus, investment decisions require considerable research and effort given that the results of investment decisions have long-term effects on corporate value.

In previous studies, efficient investment has been defined in various ways. McNichols and Stubben (2008) defined efficient investment as the state in which a corporation invests, corresponding to its investment opportunities and internal financing capabilities. Biddle et al. (2009) defined efficient investment using two models: (1) investment to mitigate the level of over (or under) investment in relation to the ratio of cash and debt held by the company or (2) investment corresponding to the corporation’s sales growth rate. In other words, if an investment is made at a point that deviates from the optimal level, reflecting factors such as leverage, investment inefficiency will occur. Previous studies have documented that a company’s investment efficiency is affected by various factors and is pronounced differently. The phenomenon by which corporate investment deviates from the appropriate level of investment can occur in two directions: overinvestment and underinvestment. Accordingly, investment efficiency can be achieved when the investment is made at an optimal level rather than at an over- or under-invested level. If the actual investment level of a company is higher than the optimal investment level, the investment efficiency of the company is lowered because of excessive investment. If the actual investment level is less than the optimum level, then investment efficiency is undermined due to underinvestment (Biddle & Hilary, 2006). Therefore, the investment efficiency of a corporation is determined by the degree to which its investment level deviates from the optimized investment level.

In contrast, Ha and Feng (2018), who analyzed labor investment efficiency, showed a significantly negative relationship between labor investment inefficiency and accounting conservatism, which recognizes expected losses in a timely manner. They documented that a firm maintaining accounting conservatism shows more efficient decision making regarding labor investment. In addition, Kang and Cho (2017) find that as the quality of accounting information increases and competition within the industry to which a company belongs intensifies, labor investment efficiency increases by suppressing managers’ incentives to make opportunistic decisions and alleviating information asymmetry between managers and external investors. Lee and Mo (2020) reported that the more financial analysts predict a company’s profits, the more effective external governance role they play, which leads to more efficient labor investment decisions. In particular, they found that financial analysts’ predictions greatly increase a company’s labor investment efficiency for a company with a large amount of internal cash. Taken together, most studies related to investment efficiency have analyzed corporate characteristics such as managerial opportunistic incentives and corporate governance.

Hypothesis Development and Research Methodologies

Hypothesis Development

According to previous studies, a company’s investment can be affected by various factors, including tax. When corporate taxpayers face lower tax rates and more tax benefits, they increase their investment size, and the ITC, which reduces the final tax burden on taxpayers, is a strong investment incentive (Egger et al., 2020; Pham, 2020). However, whether these tax credits result in investment efficiency remains unclear. In particular, if the ITC is available for designated assets under tax law, corporations may make tax-motivated investments only in specific tax-preferred assets, which may potentially reduce investment efficiency (Hines & Park, 2019). Accordingly, a corporation may fail to make investments corresponding to its own investment opportunities and internal financing capabilities when focusing on the tax perspective, and an optimal level of investment, thus, may not be reached. In particular, it is worth analyzing whether government tax policies promote efficiency in corporate investments. This is because such an investment becomes efficient only when corporate value is improved from a mid- to long-term point of view, although tax benefits increase net cash flow to corporate taxpayers in the short term. Therefore, we develop Hypothesis 1 as a null hypothesis as follows:

Hypothesis 1: ITC is not related to investment efficiency.

Conversely, SMEs may have relatively inadequate investment experience compared with non-SMEs in a business environment for various reasons, including a lack of investment professionals. SMEs’ asset management may not be relatively effective or efficient, and investment may be insufficient compared to non-SMEs due to financial constraints and lack of social networks (Centobelli et al., 2019; Martinez-Cillero et al., 2020; Nguyen, 2020). Therefore, given that the Korean tax system provides preferential tax treatment for SMEs, there is a high possibility that SMEs will make investments that deviate from the appropriate level when they are more concerned about tax savings. This prediction can be confirmed in the case of SME corporate taxpayers, who can take more ITCs than non-SMEs. In addition, since SMEs have lower levels of capital-raising capacity and financial soundness than large enterprises, there is a possibility that SMEs are weaker in making investment decisions from a mid- to long-term perspective. Therefore, it is expected that SMEs are more likely to make investment decisions by focusing on short-term tax benefits rather than on the effect of increasing corporate value through investment. Thus, Hypothesis 2 was developed in the form of a null hypothesis as follows:

Hypothesis 2: The investment efficiency of SMEs does not differ from that of non-SMEs.

Research Methodologies

This study, following previous studies, defines investment inefficiency as over- or under-investment from the level of appropriate investment for corporations. To measure investment efficiency from this viewpoint, equation (1) is formulated according to McNichols and Stubben (2008) as the OLS regression model.

INVEST: Change in tangible and intangible assets divided by total assets;

TOBINQ: Sum of market capitalization and liabilities divided by total assets;

QRT2: 1 if Tobin’s Q is in the second quartile; otherwise, 0

QRT3: 1 if Tobin’s Q is in the third quartile; otherwise, 0

QRT4: 1 if Tobin’s Q is in the fourth quartile; otherwise, 0

CFO: Cash flow from operating activities divided by tangible assets;

GROWTH: Natural logarithm of the ratio of total assets in the current year to the total assets in the previous year.

In equation (1), the dependent variable INVEST is corporate investment size, measured as an increase in tangible and intangible assets. McNichols and Stubben (2008) reported that a company’s investment is determined by investment opportunities and internal financing capability, and used Tobin’s Q (Q) and operating cash flow (CFO) as explanatory variables. In addition, considering the relationship between investment opportunity and investment, they divided investment opportunities into four quartiles by having dummy variables (QRT2, QRT3, and QRT4) and added interaction variables with investment opportunities (Q) into equation (1). Moreover, the asset growth rate (GROWTH) and prior year’s investment level (INVEST) were controlled.

Equation (1) shows the relationship between the factors influencing investment and the level of appropriate investment. An inefficient investment is an investment made over or under the level explained by the explanatory variables. We define investment inefficiency as the absolute value of the residual (ε) for each company estimated by regression analysis by industry year. If the absolute value of ε is large (small), the inefficiency of the investment increases (decreases). To better interpret the test results, we define the efficiency of investment (EFFICIENCY) as the 1−absolute value of ε, and use this variable as a dependent variable. In this study, equations (2) and (3) were established to test Hypotheses 1 and 2, respectively. As a result of analyzing the effects of the fixed effects model and the random-effects model through the Hausman test, the null hypothesis that there is no difference in the estimators of these two models was adopted. Therefore, equations (2) and (3) were constructed as random effects models of industry and year.

EFFICIENCY: 1 − absolute value of ε (investment efficiency);

SME: 1 for SME, 0 otherwise;

CREDIT: investment tax credit divided by tax calculated before application of tax credit

TOTAL: Total investment tax credit divided by the calculated tax. The total amount of tax credits include the following investment tax credits: (1) Productivity ITC, (2) R&D ITC, and (3) Employment ITC.

PROD: Productivity ITC divided by tax calculated before tax credit

RND: R&D ITC divided by tax calculated before tax credit;

EMPINVEST: Employment ITC divided by tax calculated before tax credit;

SIZE: Natural logarithm of total assets;

ROA: Net income divided by total assets;

MTB: The sum of the market value of equity and total liabilities divided by total assets

CFOSALES: Cash flow from operating activities divided by sales;

DIVIDEND: 1 if there is cash outflow for dividend payment, otherwise 0;

AGE: Natural logarithm of the number of years after the KOSPI or KOSDAQ listing

LOSS: 1 for accounting net loss, 0 otherwise;

CASH: Cash and cash equivalents divided by total assets;

LEVERAGE: Total liabilities divided by total assets;

ΣYEAR: Year dummy variables;

ΣIND: Industry dummy variables.

In equation (2), to test Hypothesis 1, the main variable of interest CREDIT is productivity ITC, R&D ITC, or employment ITC. In equation (3), to test Hypothesis 2, SME × CREDIT, the main variable of interest, is an interactive variable between CREDIT and SME. The control variables are the factors that affect investment efficiency used in previous studies.

Sample Selection

We obtained financial data from KIS-VALUE, which is an authoritative financial database in South Korea. With respect to the data related to the ITC, we hand-collected the information after reviewing the information from tax returns filed by corporations for the period 2011 to 2015. The data are obtained privately from tax agents who help corporate taxpayers file tax returns. Accordingly, using various investment-related tax credit data, it is possible to compare multiple tax credits, which has not been possible in previous studies. In particular, in the case of SMEs, the relationship between investment efficiency and tax credits must be analyzed carefully using available tax data because SMEs may receive multiple qualifying tax benefits that are difficult to categorize without tax returns.

The final sample consists of 1,081 firm–year observations for the 2011 to 2015 period that meet the following conditions:

Listed firms on Korean stock exchanges (i.e., KOSDAQ and KOSPI)

Firms with available financial data

Firms in which financial statements are audited by independent auditors with unqualified opinions.

Test Results

Descriptive Statistics

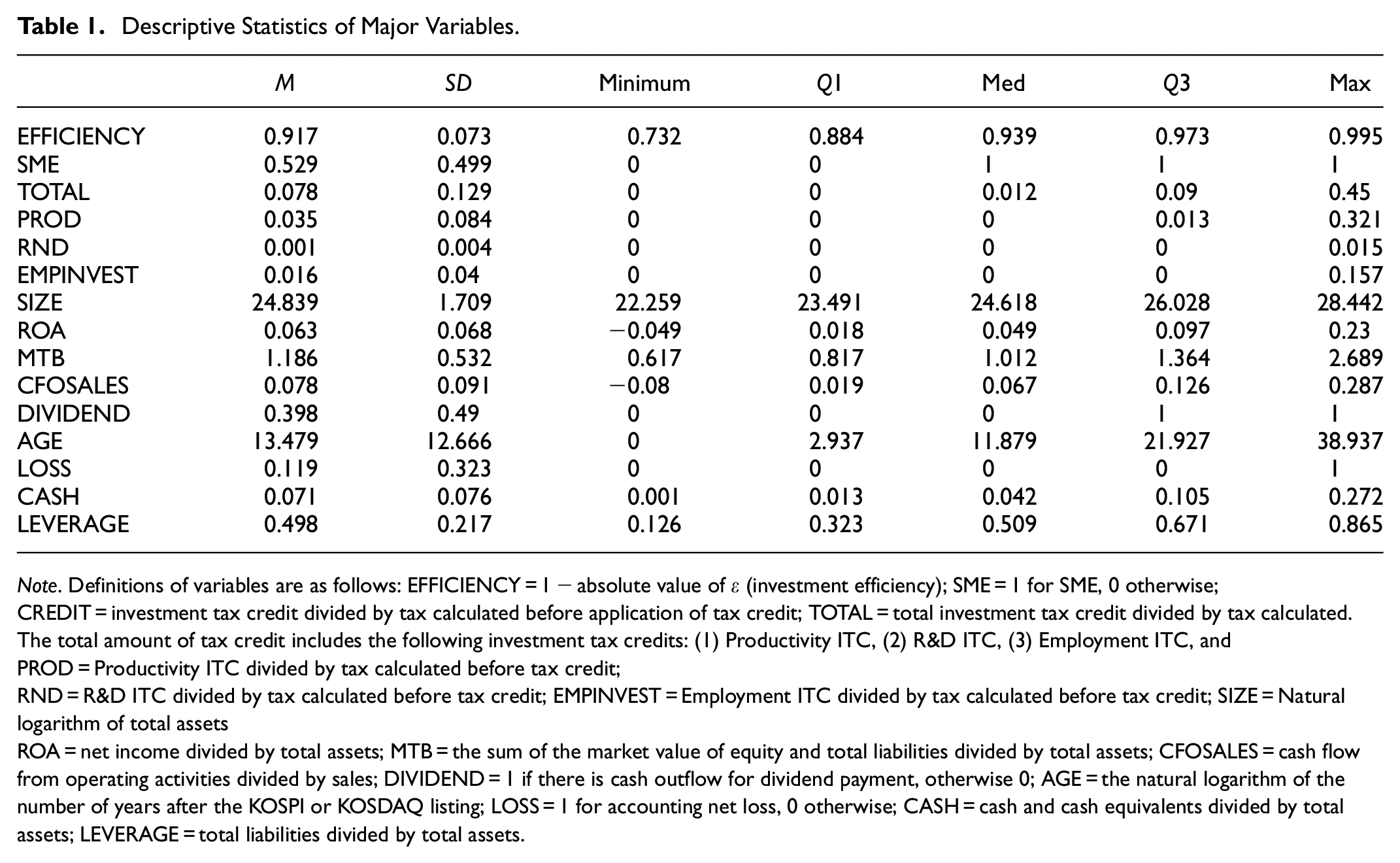

Table 1 presents the descriptive statistics. EFFICIENCY has an average of 0.917 and a median of 0.939, indicating that certain samples have relatively high efficiency, and the distribution is skewed to the right tail. The average of SMEs is 0.529, which indicates that SMEs receive more tax credit than non-SMEs in the sample. This result may be attributed to the fact that high tax credit rates are available to SMEs and the tax credit requirements for SMEs are relatively relaxed. The average total ITC size (TOTAL) is 0.78, which indicates that tax credit accounts for approximately 7.8% of the tax calculated on average. PROD (productivity ITC divided by the tax calculated before the tax credit) has an average of 3.5% and EMPINVEST (employment ITC divided by the tax calculated before the tax credit) has an average of 1.6%. (R&D ITC divided by the tax calculated before the tax credit) has an average value of 0.1%. We expect that RND is low because another tax credit is available for R&D expenditure other than R&D ITC, and the benefit from this other tax credit is higher and broader in terms of credit rates and R&D scope.

Descriptive Statistics of Major Variables.

Note. Definitions of variables are as follows: EFFICIENCY = 1 − absolute value of ε (investment efficiency); SME = 1 for SME, 0 otherwise; CREDIT = investment tax credit divided by tax calculated before application of tax credit; TOTAL = total investment tax credit divided by tax calculated. The total amount of tax credit includes the following investment tax credits: (1) Productivity ITC, (2) R&D ITC, (3) Employment ITC, and PROD = Productivity ITC divided by tax calculated before tax credit;

RND = R&D ITC divided by tax calculated before tax credit; EMPINVEST = Employment ITC divided by tax calculated before tax credit; SIZE = Natural logarithm of total assets

ROA = net income divided by total assets; MTB = the sum of the market value of equity and total liabilities divided by total assets; CFOSALES = cash flow from operating activities divided by sales; DIVIDEND = 1 if there is cash outflow for dividend payment, otherwise 0; AGE = the natural logarithm of the number of years after the KOSPI or KOSDAQ listing; LOSS = 1 for accounting net loss, 0 otherwise; CASH = cash and cash equivalents divided by total assets; LEVERAGE = total liabilities divided by total assets.

With respect to other variables, SIZE has an average (median) of 24.839(24.618); ROA, 6.3% (4.9%); MTB, 1.186 (1.012); CFOSALES, 0.078 (0.067); DIVIDEND, 0.398 (0); AGE, 13.479 (11.879); LOSS, 0.119(0); CASH, 0.071(0.042); and LEVERAGE, 0.498(0.509).

Regression Results

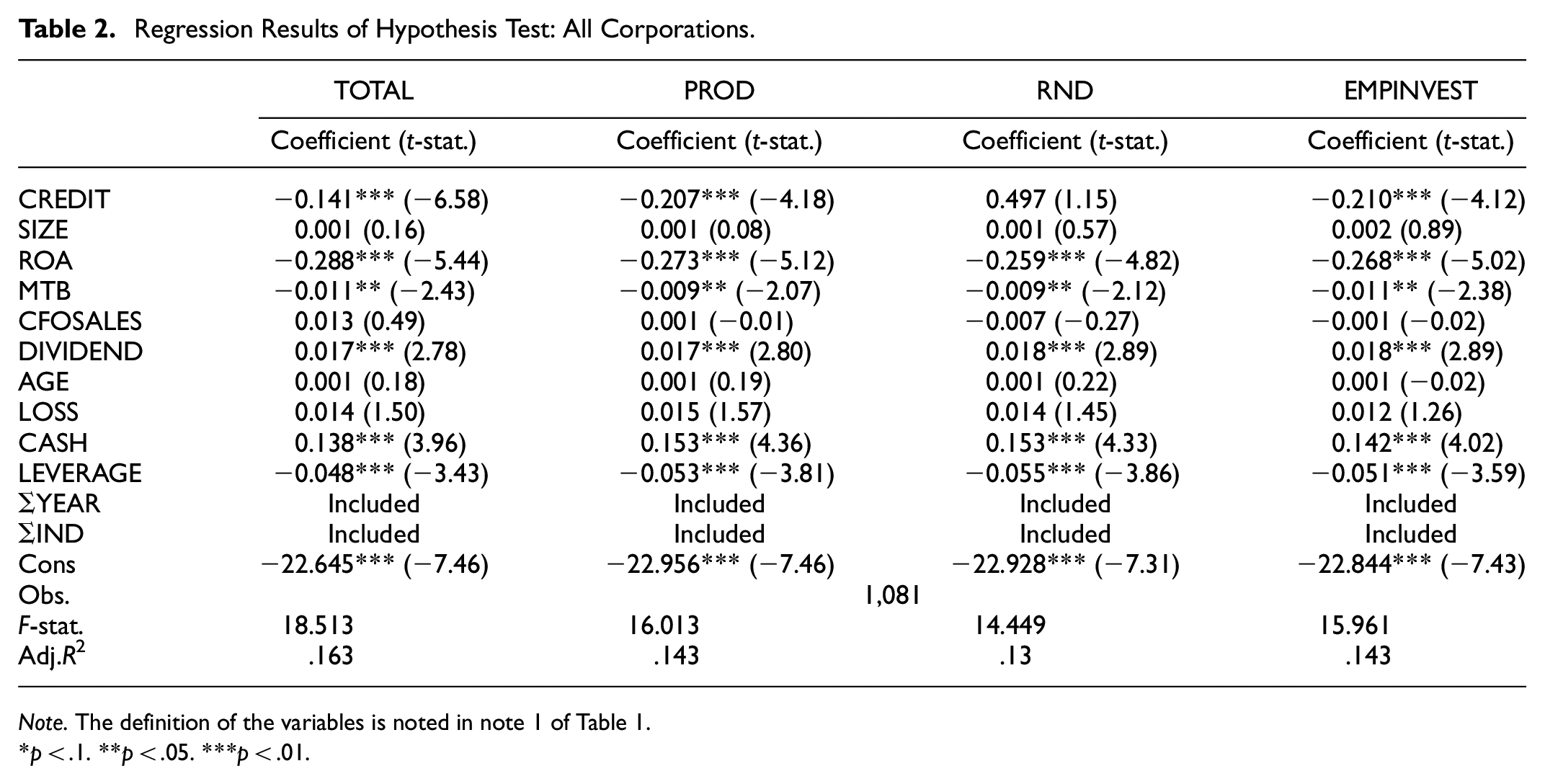

Table 2 shows test results on the relationship between ITC and EFFICIENCY (investment efficiency) for a sample of all corporate taxpayers including SMEs. TOTAL (total ITC divided by the tax calculated) has a significantly negative coefficient estimate of −0.141 (p < .01) in a relationship with EFFICIENCY. In addition, PROD (productivity ITC divided by the tax calculated before the tax credit) and EMPINVEST (employment ITC divided by the tax calculated before the tax credit) also show significantly negative coefficient estimates of −0.207 (p < .01) and −0.21 (p < .01). RND (R&D ITC divided by the tax calculated before the tax credit) has an insignificant coefficient of 0.479. These results indicate that corporations receiving tax benefits from ITCs may not make investments efficiently. Particularly, the efficiency of investment is lower even in the case of PROD, which encourages corporate taxpayers to invest in productivity enhancement facilities. However, RND shows a coefficient of 0.497 (t-stat. = 1.15), which is statistically insignificant; however, the efficiency of R&D investment is not shown to be negative compared with other investments. This result provides implications that R&D investments may potentially achieve investment efficiency with a marginal significance level.

Regression Results of Hypothesis Test: All Corporations.

Note. The definition of the variables is noted in note 1 of Table 1.

p < .1. **p < .05. ***p < .01.

With respect to the control variables, ROA, DIVIDEND, CASH, and LEVERAGE have coefficients of −0.288 to −0.268 (p < .01), 0.017 to 0.018 (p < .01), 0.138 to 0.153 (p < .01), and −0.055 to −0.048 (p < .01), respectively. These results indicate that investment efficiency is likely to be higher (lower) when ROA is lower (higher), leverage is lower (higher), dividend is higher (lower), and cash holdings are higher (lower).

These test results show that corporate taxpayers’ investments with tax credits may not be efficient and that their investment decisions may be made for tax-saving purposes only. The policy goal of providing tax incentives for investment is to help corporations make proper investments and strengthen their competitiveness for corporate sustainability. However, if corporate investment is inefficient and driven only by tax-saving purposes, the government’s tax incentive system would be rendered ineffective. In other words, the ITC system may drive corporations to invest only in tax-preferred assets, which leads to distorted and inefficient investments. In particular, the negative relationship between PROD and EFFICIENCY drew our attention. Although corporate taxpayers invested in facilities to improve their productivity, our results show that the investment may be inefficient, which remarkably departs from the very purpose of the tax policy. Based on these test results, ITCs may potentially be effective only for the alleviation of the tax burden for taxpayers.

The above results may be attributed to the limitation that tax credit is only applicable to corporations with net income for tax purposes. Tax credit is only applicable to corporations paying taxes because of positive taxable income and not to corporations with losses. Given that the government provides tax benefits only to profit-making companies, which may sometimes not require further investment, ITCs may result in inefficient investment. Meanwhile, a corporation that has a loss cannot make investments that are eligible for ITC, which may result in a failure to provide incentives for loss-making companies in need of investment for sustainability. Moreover, corporations that can raise funds through capital markets may make suboptimal or unnecessary investments to maximize their tax savings. Corporations may elect the second choice of tax-preferred assets for tax savings instead of the best investment option, which can be utilized via external financing. In other words, corporations with no investment needs or best investment choices make unnecessary or suboptimal investments to reduce their tax burden by taking ITCs available for limited qualified assets under tax law.

Table 3 presents the test results from the analysis of investment efficiency. In the TOTAL column, a dummy variable representing SMEs (SME) has a significant negative correlation with EFFICIENCY (coefficient estimate: −0.020 (p < .01)). The same results were found in the PROD (coefficient estimate: −0.021 (p < .01)) and EMPINVEST (coefficient estimate: −0.026 (p < .01)).

Regression Results of Hypothesis Test: SMEs.

Note. The definition of the variables is noted in note 1 of Table 1.

p < .1. **p < .05. ***p < .01.

These test results may imply that SMEs that receive tax benefits are likely to fail to achieve investment efficiency in utilizing ITCs. In other words, SMEs’ investments may reduce their tax burdens through ITCs; however, they cannot sufficiently reach an appropriate efficiency level for sustainability. SMEs’ financial constraints and lack of social networks may make it difficult for them to invest appropriately investment (Nguyen, 2020). Moreover, they may make excessive investments to obtain more tax savings given that SMEs can take higher ITC rates than non-SMEs. Another possible explanation is SMEs’ lack of asset management skills after investment. SMEs’ asset management skills may be insufficient for an increase in firm value after investment in assets (Centobelli et al., 2019). The information asymmetry SMEs face may be another reason for this phenomenon. Given that the level of information asymmetry of SMEs is relatively higher than that of large companies, investments by SMEs may be less likely to be appreciated in the capital market. Therefore, low investment efficiency may be perceived as the low degree to which SMEs’ investments lead to an increase in firm value.

The control variables show the following results similar to those in Table 2. ROA and LEVERAGE show significant negative coefficient estimates of −0.258 (p < .01) to −0.285 (p < .01) and −0.046 (p < .01) to −0.052 (p < .01), respectively. DIVIDEND and CASH also showed statistically significant positive coefficients of 0.017 (p < .01) and 0.138 (p < .01) to 0.153 (p < .01), respectively.

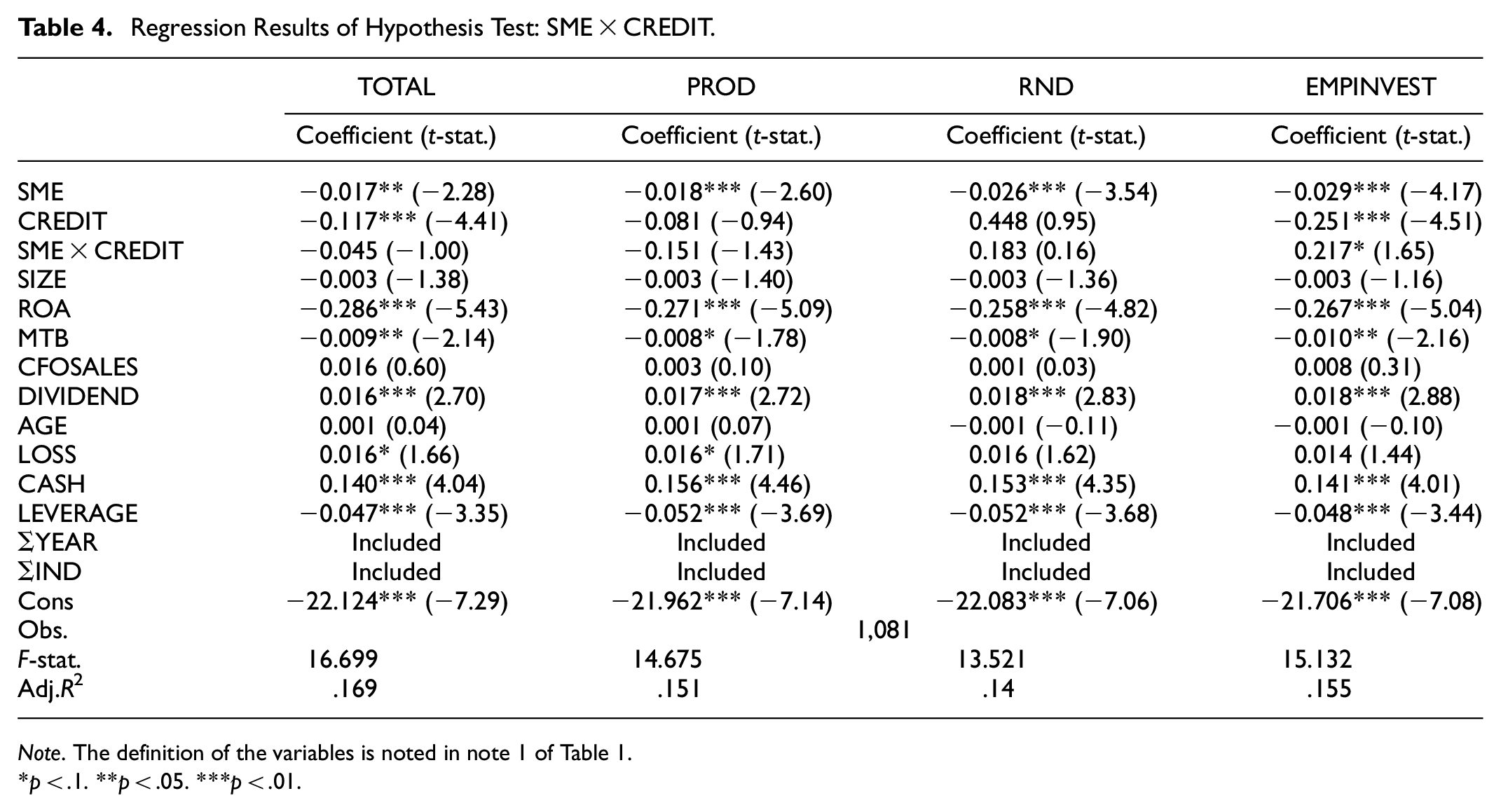

Table 4 presents the test results of the analysis on the efficiency of investment of SMEs claiming ITC. The interaction variable (SME × CREDIT), which is equal to 1 when an SME claims an ITC, has statistically insignificant coefficient estimates of −0.045 (t-stat. = −1.00) if CREDIT is TOTAL, and −0.151 (t-stat. = −1.43) if CREDIT is PROD. Although these variables have marginally significant coefficients, the negative coefficients may indicate that SMEs’ efficiency of investment eligible for tax credit may be lower than for large corporations for overall investment (TOTAL) and productivity enhancement facility investment (PROD).

Regression Results of Hypothesis Test: SME × CREDIT.

Note. The definition of the variables is noted in note 1 of Table 1.

p < .1. **p < .05. ***p < .01.

However, EMPINVEST (employment ITC) shows a statistically significant value of .217 (p < .1), indicating that SMEs’ investment in employment creation is relatively more efficient than other investments with tax credit. This result may imply that SMEs’ investment through tax credit becomes efficient if the investments are supported by human resources. If SMEs that may experience a lack of facility investment skills are supported by appropriate personnel, they can make efficient investments that have a positive effect on the increase in firm value. Conversely, investment in physical facilities alone, such as investment eligible for productivity ITC, may not increase investment efficiency, leading to lower sustainable profitability.

Although many previous studies have documented that a corporation’s performance (including productivity) improves when a physical facility investment is made, other studies have argued that a statistically insignificant relationship exists between facility investment and corporate performance (Hendricks et al., 2007). The latter studies claim that investment in physical facilities alone does not necessarily improve the sustainable performance of a corporation, but that human resources are also required to help improve corporations’ performance. Thus, the invested facilities may not be properly utilized unless suitable human resources are available. Sufficient human resources may be necessary for investment efficiency, which contributes to improving corporate performance.

Conclusions

Corporate investment leads to corporate sustainability by increasing future growth and profitability. This is particularly true for SMEs that have higher future growth potential. The Korean tax law allows corporate taxpayers to take ITCs to encourage them to invest in their future growth and profitability, and more ITCs are available for SMEs. This study examines whether investments that received ITC have investment efficiency in addition to tax savings by using samples of Korean corporations that actually claimed ITC. Our study presents the following test results:

First, the investments of companies that received ITC were found to be inefficient. A possible explanation for this finding is that their investment decisions may have been made only for tax-saving purposes. This result may also be attributed to the fact that tax credit is only applicable to corporations, excluding loss-making firms, for tax purposes.

Second, the level of investment efficiency is also low, even for SMEs that can claim higher ITC rates. This result may be because SMEs, which tend to have insufficient personnel and management skills, achieve less investment efficiency than non-SMEs. The higher ITC rates and information asymmetry for SMEs may be another possible reason for this finding.

Third, despite the above results, when SMEs make investments eligible for tax credit considering employment creation, the level of investment efficiency is found to be higher. In contrast, in the case of investment in productivity enhancement facility investment, SMEs’ investment efficiency is not perceived to be achieved. These test results suggest that SMEs’ investments must be supported by manpower for investment efficiency.

This study investigates whether the investments subject to tax credit provide investment efficiency for corporations that claim ITCs. Previous studies have focused on analyzing the relationship between investment and taxation. This study is different in that it analyzes samples of corporations that take ITC to examine whether investment efficiency is achieved by investments eligible for ITCs.

This study provides policy considerations for governments concerning their incentives to encourage a corporation to increase investment, as these incentives need to promote corporate value. By taking these incentives, companies can increase sustainability from a mid- to long-term perspective. This study also provides a practical implication that companies need to adjust the amount of investment in consideration of the efficiency of the investment, rather than simply increasing the investment to reduce short-term cash outflow by receiving more tax benefits.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.