Abstract

This study investigates the impact of fintech on SMEs’ total factor productivity (TFP, input-to-output efficiency) and their bargaining power (the ability to negotiate favorable terms with suppliers and customers). We use a sample of SMEs listed on China’s A-share market between 2011 and 2019. We construct a regional fintech index using Baidu search data. To ensure our findings are robust, we controlled for endogeneity and used different approaches to calculate TFP and to measure fintech. Our results show that fintech significantly improves SME productivity by strengthening their bargaining power. A unique aspect of our study findings is how fintech boosts TFP via raising SME bargaining power, significant results are observed in the eastern regions and manufacturing sector in China. This study expands the literature by showing fintech’s role beyond financial intermediation, highlighting its strategic function in improving productivity and bargaining power. Overall, our findings enrich academic debate and provide practical insights for policymakers and the business community.

Plain Language Summary

We examine how fintech affects Chinese SMEs’ total factor productivity (TFP—the efficiency of turning inputs into outputs). Our results show that digital finance and tools (e.g., AI, blockchain, big data) can lower costs and strengthen firms’ bargaining power. We also observe that the effects are strongest in manufacturing and in China’s eastern region, where digital infrastructure and adoption are deeper. This finding confirms the pattern observed in previous studies. The results of the analysis encourage leaders and policymakers to create settings that support the growth of fintech. They can greatly boost SME productivity that is crucial for economic growth in any nation particularly in developing countries such as China. Enhancing efficiency in small and medium companies may result in wider benefits for the economy including greater employment levels and more market competitiveness. This investigation underscores the requirement for directed methods for blending technology into commerce and creates a robust groundwork for more extensive inquiries into the wider financial effects of fintech in underdeveloped regions and industries.

Introduction

In China, small and medium-sized enterprises (SMEs) represent the essential pillar of national economic and social development, connecting business operations in the industrial chain from upstream to downstream. These entities are also fundamental engines of economic expansion and technological progress, presenting a unique aspect of the country’s vibrant economic landscape. Nevertheless, the interaction of SME-specific factors with a banking system largely dominated by big banks leads to a clear preference in allocating financial resources to larger companies (Zhang et al., 2021). SMEs typically face with financing problems, and traditional banks do not cater as much to their specific needs (Abraham & Schmukler, 2017). Moreover, this phenomenon is not only observed in China. International studies show that leading banks prefer larger enterprises globally due to lower risk and higher profitability (Berger & Black, 2011; Stein, 2002). Thus, in general, SMEs in China have limited access to affordable finance, reducing their bargaining power and ability to enhance TFP. This paper explores whether fintech development can foster productivity gains among SMEs in China, especially through its effect on strengthening firms’ bargaining power in supply chains.

The financing barriers faced by SMEs are persistent and limit innovation, investment, and long-term growth (Guo et al., 2023). Traditional banking systems struggle to meet these needs due to asymmetric information and rigid lending models (Wang et al., 2024). These challenges highlight the rationale for this study: to examine whether fintech can address such barriers and improve SME productivity. The objective is to provide clear evidence of how fintech development contributes to TFP through both access to finance and bargaining power channels for SMEs.

Given these challenges, the rise of financial technology (fintech) provides SMEs with practical tools to relieve financing pressures and strengthen their day-to-day operations. In the Chinese context, “fintech” showcases technology and financial services integration, which results in significant changes in business models, technology usage, and financial operations and products. This shift has helped achieve cost reduction and operational improvements in financial services (Financial Stability Board, 2016). In particular, fintech changes the provision of financial services. It broadens the spectrum of these services in China, including detailed user profiling, precise risk assessment, and simplified business processes (Demertzis et al., 2018). These innovations are important in the elimination of the asymmetry of information problems and ethical risks of financial institutions and businesses, especially SMEs. The positive response to the relief of financial and cash flow problems promotes TFP growth within China’s economic environment.

The fast development of fintech has disrupted the global finance system, making way for new growth factors. This fintech wave has created chances for SMEs in China. Although fintech is well-studied in terms of its wider consequences, there still needs to be more understanding of its effect on the performance and growth of publicly listed SMEs in China. Moreover, China provides a unique setting for this study. It has been experiencing fast growth in fintech, and has developed a robust digital infrastructure as well as a large SME sector with significant regional variation. Such conditions make it possible to discover the mechanisms that cannot be observed in other economies. These features make the Chinese SME context especially relevant for policymakers and business community. The case shows how fintech can promote productivity growth. The lessons learnt are useful for other emerging economies with large SME sectors.

Recent studies have focused on the importance of big data and blockchain in fintech, to increase financial inclusivity and making of equitable funding access. For instance, Chen, Wu, and Zhang (2023) show that digital transformation improves firm performance in China’s listed firms. Similarly, Rizvi et al. (2024) emphasize that AI-driven fintech tools enhance resilience and efficiency during market volatility. These findings highlight the growing role of advanced technologies in shaping SME outcomes. Fintech is shown to improve lending and financial services facilitated for Chinese SMEs, and thus increases their performance (H. Li et al., 2024). While fintech has been widely studied for its role in improving access to finance and innovation (Abbasi et al., 2021; Karim et al., 2022), few studies focus on its impact on productivity in the context of Chinese SMEs (Bollaert et al., 2021; Elisa et al., 2021; Thakor, 2020). Our study attempts to offer a unique contribution through coverage of the under-researched area of how fintech affects the total factor productivity (TFP) of China’s publicly listed SMEs. Consequently, we specifically assess how the development of fintech influences these SMEs, indicating that fintech is an important driver of their TFP. In addition, our research investigates how fintech improves firm bargaining power, which in turn, positively influences TFP. Such thorough consideration of the impact of fintech on the operational efficiency and growth prospects of publicly traded SMEs in China serves as a notable fill in the current literature.

The literature on fintech and firm performance continues to expand. Yet essential knowledge gaps remain. Research studies frequently employ national or bank-level indicators but fail to consider the heterogeneity of fintech development across locations. Most research focuses on financial inclusion and innovation (Ba et al., 2020), or broader digitalization impacts (Chen, Zhang, & Wang, 2023), but pays less attention to direct productivity effects linked specifically to fintech use among SMEs. How fintech influences productivity through supply chain bargaining power is less examined in the current literature. Moreover, there are few studies that explicitly examine the bargaining-power channel or measure regional fintech development at the city-level. Most studies use national indices or bank-level data, and thus overlook regional heterogeneity. We address this by building a regional fintech index and testing the bargaining-power mechanism directly for SMEs. China is also a valuable case. The country experiences fast fintech expansion while maintaining a substantial small and medium enterprise sector and significant regional differences. The institutional and economic environment in China provides an optimal setting to study how fintech development at the regional level affects SME productivity.

This study attempts to fill these gaps and makes five contributions. First, it constructs a novel regional (city-level) fintech index using Baidu Search Index data, providing a detailed and dynamic view of regional fintech development. Second, it introduces and tests a new mechanism, showing that fintech can raise SME productivity by strengthening firms’ bargaining power in supply chains. Third, it focuses on publicly listed SMEs on China’s ChiNext and SME boards, an innovation-driven segment often overlooked in prior research. Fourth, this study implements three econometric methods which include the Levinsohn and Petrin (2003) approach and GMM estimation and instrumental variable techniques to obtain robust causal inference. This study investigates regional and industry heterogeneity to demonstrate how fintech impacts productivity differently across China’s various economic regions.

This study extends the current literature which demonstrate how fintech development impacts firm productivity through various mechanisms. Guided by Song et al. (2021), Levine and Warusawitharana (2021), and Yan (2022), we analyse a dataset of China’s publicly listed SMEs from 2011 to 2019 to investigate the relationship between fintech and total factor productivity (TFP). This study contributes to existing knowledge by examining how fintech influences both operational practices and strategic choices of SMEs, beyond its role in financial access. Furthermore, we examine the mechanism by which fintech improves SMEs’ bargaining power within their supply chains and find stronger effects in eastern regions and the manufacturing sector. These findings provide valuable insights for SME strategy and policy design. This study aims to enhance existing academic discussions. It also seeks to provide practical value for policymakers and financial professionals who utilize fintech as an innovation and growth tool.

The remainder of the article is structured as follows, building on the above contributions: Section “Literature Review and Hypotheses Development” develops the research hypotheses. Section “Data and Models” outlines the data, variables, and the models used in this study. Section “Results and Discussion” analyses the regression results for the first hypothesis, while section “Mechanism Analysis of Fintech’s Impact on SMES’ TFP” presents the findings for the second hypothesis. Section “Analysis on Heterogeneous Effects” explores the heterogeneous effects of the underlying mechanism. The last section offers conclusions and policy implications derived from the study.

Literature Review and Hypotheses Development

Literature Review

Fintech and Productivity

The term fintech originally referred to the combination of banking and IT according to Bettinger (1972), but now represents technology-based financial innovation that reshapes financial markets, institutional structures, and business models (Financial Stability Board, 2016, 2019; Knewtson & Rosenbaum, 2020; Philippon, 2016). As a disruptive force, it reduces inefficiencies in traditional banking and is a central part of financial innovation (Bunnell et al., 2020).

Research shows fintech reduces information asymmetry, improves governance, and enhances access to financial services (Hajek & Henriques, 2017; Lin et al., 2015; Liu et al.,2020; Thakor, 2020; Vives, 2019). It also improves bank efficiency without raising default risk (Chen et al., 2021; Fuster et al., 2018; Gong et al., 2021; Li & Jiang, 2021).

Fintech at the firm level expands credit availability while reducing financing barriers and enhancing resource distribution which leads to increased total factor productivity (TFP; Ba et al., 2020; Li et al.,2020; Sheng et al., 2020; Guo, 2019; Song et al., 2021).Big data, cloud computing, and AI strengthen competitiveness through demand forecasting, customer targeting, and operational resilience (Allen et al., 2021; Babilla, 2023; Gomber et al., 2018; Peng & Ma, 2022; Zhao et al., 2021).

The majority of research studies employ national- or bank-level indicators (Ba et al., 2020; Song et al., 2021), with relatively less attention to regional heterogeneity. Recent work (Yang & Liang, 2024) highlights uneven productivity effects across industries. This study attempts to address this literature gap through the development of a regional (city-level) bank FinTech index to examine SME productivity.

Financing Constraints and Resource Allocation

One of fintech’s key contributions is its ability to ease funding restrictions and improve credit allocation (Guo, 2019; Li et al., 2020; Sheng et al., 2020). It provides financing through digital networks, peer-to-peer lending, and big data analytics, which are often unavailable to small and medium-sized enterprises (SMEs) under traditional banking (Ba et al., 2020; Song et al., 2021). This access reduces firms’ reliance on intermediaries and narrows information gaps between borrowers and lenders (Ba et al., 2020; Song et al., 2021).

Machine learning and alternative credit scoring allow lenders to assess risk more accurately, lowering barriers for SMEs without collateral or credit histories (Allen et al., 2021; Gomber et al., 2018). These tools improve loan evaluations and the speed of fund allocation, enabling institutions to support firms with stronger growth prospects (Liu et al., 2020; Vives, 2019).

Evidence shows that fintech reduces frictions by cutting transaction costs and accelerating credit delivery. Huang et al. (2020) found that Chinese digital lending platforms expanded SME credit access during liquidity shortages. Hua and Huang (2020) find that firms in regions with higher fintech adoption experienced more stable financing during the financial crisis.

By improving capital allocation, fintech reduces inefficiencies that hinder productivity. Li et al. (2025) find that adoption shifts credit from low- to high-productivity firms, raising efficiency. This mechanism is particularly relevant in developing economies where financial frictions remain significant (Babilla, 2023; Peng & Ma, 2022).

Overall, fintech lowers financial frictions by enhancing information, broadening access to external finance, and allocating credit more effectively. These mechanisms form a key channel through which fintech contributes to firm-level productivity growth.

Fintech, Innovation, and Operational Efficiency

The implementation of fintech enables companies to achieve higher innovation levels and operational efficiency through digital tools for automation, data analytics, and risk management. The combination of AI, cloud platforms, and blockchain technology enables cost reduction and resource optimization which supports digital transformation to boost productivity and resilience (Guo, 2019; Zhao et al., 2021). The technology enables financial institutions to create tailored products that match firm-specific innovation requirements thus reducing development costs (Allen et al., 2021). Big data analytics allow companies to forecast market demands and create customer profiles, so they can modify their production to meet market requirements (Shi & Wang, 2025). In supply chains, fintech platforms decrease transaction costs while building trust between partners. Therefore, it enables SMEs to scale their operations more efficiently (Babilla, 2023; Peng & Ma, 2022). The adoption of such tools leads firms to develop stronger resilience and efficiency, particularly during times of market volatility (Rizvi et al., 2024). Fintech reduces financial barriers in the market and fosters digital innovation. In addition, it also supports operational improvements. As a result, fintech creates another channel that enhances SME productivity and competitiveness.

Regional Heterogeneity in Fintech Development

Most empirical studies about fintech and productivity rely on national or bank-level data measures. These may hide regional variations and industry-specific patterns (Ba et al., 2020; Song et al., 2021). Fintech development demonstrates different patterns across regions. The impact of fintech on firm performance depends on institutional quality, market maturity, and industry structures. Research indicates that differences in digital infrastructure and financial inclusion across regions influence how firms benefit from fintech adoption (Chen, Zhang, & Wang, 2023; Wang et al., 2024).

Recent studies show that small and medium enterprises (SMEs) in cities with stronger fintech ecosystems achieve higher productivity gains than those in less developed areas (Huang et al., 2020; Hua & Huang, 2020). The growth of local fintech operations increases competition between financial institutions. At the same time, it reduces financing gaps and produces positive effects that boost business efficiency (Wang et al., 2024).

Despite these insights, relatively few studies explicitly measure fintech development at the city or regional level. This gap limits our understanding of how local conditions mediate the productivity effects of fintech. This study addresses this limitation by constructing a regional bank fintech index. This allows us to examine regional heterogeneity and analyze how localized fintech development influences SME productivity outcomes.

Research Position and Contributions

Although the current literature explored fintech’s impact on finance, innovation, and productivity, there are still some research gaps remain. The majority of studies adopt national- or bank-level indicators which fail to consider regional heterogeneity and mechanisms such as bargaining power (Li et al., 2025; Song et al., 2021). Despite the important role that SMEs play in emerging economies such as China, little direct attention has been paid to them.

This study makes three contributions. Firstly, this study develops a new bank fintech index at the regional level to capture regional variation. Secondly, it examines how fintech improves SME productivity by strengthening their bargaining power in supply chains. Thirdly, it applies robust econometric methods and explores heterogeneity across regions and industries. The research extends the fintech-productivity literature and provides new insights for SME strategy and policy development.

Hypotheses Development

Hypothesis 1

Based on these insights, we assume that fintech innovations can diminish financing frictions, improve credit allocation and increase the operational capacity of SMEs. These processes imply that fintech is likely to affect the productivity of SMEs significantly. Hence, we propose Hypothesis 1 as follows:

This hypothesis tests whether fintech development raises SMEs’ TFP. It is built on both theory and empirical evidence that digital finance improves operational efficiency and productivity in SME settings.

In Porter’s (1979) framework, bargaining power is central to competitive advantage and shapes outcomes along supply chains, including supplier control over input costs and customer influence on prices (Suutari, 2000). Evidence shows non-linear effects: supplier power has an inverse U-shaped relation with firm performance, while customer power has a U-shaped relation (Tang, 2009); strong customer power can also induce firms to evade environmental regulation, reducing dynamic green TFP (Li & Chen, 2019). We therefore test whether fintech strengthens SMEs’ bargaining power and, through this channel, raises TFP and competitive advantage in the digital-finance era. Fintech improves access, efficiency, and customization for SMEs that face resource-allocation frictions, where bargaining power strongly affects behavior and performance. By broadening access to financial data and services, and by using blockchain and smart contracts for transparent, secure transactions, fintech reduces information asymmetry and, together with peer-to-peer lending and crowdfunding, expands financing options that strengthen SMEs’ negotiating positions. Digital financial services narrow SMEs’ information gaps, improving operations and management and supporting more efficient supply chains, which is associated with higher TFP (Zhang et al., 2023).

Hypothesis 2

We further assume that fintech will enhance the bargaining power of SMEs in the supply chain by reducing information asymmetry, lowering the cost of transactions, and offering alternative sources of financing. Greater bargaining power gives SMEs the ability to negotiate favorable terms with suppliers and customers, which again can further increase productivity. Based on these, we propose Hypothesis 2 as follows:

This hypothesis tests whether fintech raises SMEs’ TFP by strengthening their bargaining power. Fintech broadens financial inclusion, delivering better lending terms, wider funding sources, and customized products. This allows SMEs to secure funding on more favorable conditions and invest in processes and technologies that lift TFP.

Mechanisms are straightforward. Stronger bargaining lets SMEs negotiate lower rates and easier repayment, which cuts capital costs and frees cash for productive assets. Tailored products improve cash flow management and reduce liquidity risk. Greater choice of platforms supports more ambitious growth and innovation. Together, these effects align firms with the right finance and increase the efficiency of capital use.

Testing H2 clarifies the channel from fintech to productivity. It shows how the fintech ecosystem directs funds to SMEs and helps them use those funds more effectively, linking bargaining power to observed gains in TFP.

Data and Models

Sample Data

In response to the substantial disruption caused by COVID-19, this research focuses on the pre-pandemic era and specifically on SMEs from Chinese companies listed between 2011 and 2019 to strategically respond to this situation.

We consider the period 2011 to 2019 for the following reasons. First, this period spans a decade of fast fintech growth in China, such as the growth of digital credit platforms, mobile payment systems, and big data analytics, which are of great relevance to SME financing and productivity. Second, this time frame will enable us to see how fintech was affecting SME productivity during relatively stable economic times, but not during the COVID-19 pandemic. Including data after 2020 would confound the long-term structural impacts with the short-term effects of pandemic shocks for fintech. Third, this decade has witnessed significant reforms affecting SMEs in China. Therefore, it is an ideal period to assess the interaction between fintech adoption and SME development.

We categorize SMEs according to the official criteria issued by the Ministry of Industry and Information Technology of the People’s Republic of China (2011). The guideline defines SMEs by total assets, annual revenue, and number of employees. In the retail sector, SMEs are defined by either having fewer than 300 employees or annual revenue under 200 million RMB. In the industrial sector, which includes mining, manufacturing and the supply of electricity, heat, gas, and water, an enterprise is an SME if it has fewer than 1,000 employees or an annual turnover of below 400 million RMB.

The primary dataset for the municipal fintech index is based on keyword search frequencies from Baidu, supplemented with the data from the Wind Database, the China Stock Market and Accounting Research (CSMAR) Database, and the Chinese Research Data Services (CNRDS) Platform. This study selects SMEs listed on the ChiNext and SME boards, where firms are recognized for creativity and growth potential, providing a wide observation of their performance and operational strategies during this period.

This choice is intentional and aims to adaptive behaviors and economic tactics needed to cope with rapid economic changes. We excludes the SMEs that went through an Initial Public Offering (IPO) before or during the sample years, together with those identified with ST, ST*, and PT labels. Firms with fewer than 3 years of financial data or missing data were also excluded. In order to minimize the influence of outliers, winsorization was performed on continuous variables at 1% and 99% cut-off points, resulting in a robust sample of 1,075 SMEs, and a total of 6,715 unbalanced observations.

Variables

Measurement of TFP

The Olley and Pakes (1996) method (OP method) and the Levinsohn and Petrin (2003) method (LP method) are usually adopted to estimate the total factor productivity (TFP) of enterprises. Both methods effectively address the selectivity and simultaneity biases associated with OLS estimation. Nevertheless, the OP method constraint on the investment amount might cause sample loss (Lu & Lian, 2012) and thus result in bias in the estimation. Wooldridge (2009) improved the LP method using the Generalized Method of Moments (GMM) one-step estimation, drastically reducing the estimation bias that arises from endogeneity. Based on this, Rovigatti and Mollisi (2018) further improved the method by integrating dynamic panel instruments (Blundell and Bond, 1998), thus reducing the problem of observation loss and being suitable for panel data with large N and small T dimensions.

In this study, the Cobb-Douglas function is adopted as the preset function. Here, the total output of an enterprise is measured by its operating income, capital input by the net amount of fixed assets, labor input by the number of employees, and intermediate input by the sum of operating costs and period expenses, subtracting depreciation, amortization, and employee compensation. Given the characteristics of each method, we utilize the LP method (Levinsohn & Petrin, 2003) to estimate enterprise TFP for three reasons. First, it avoids the sample loss that occurs with the OP method (Levinsohn & Petrin, 2003). Second, it provides a better solution to address simultaneity bias than ordinary least squares (OLS) (Malik, 2015). Third, it is well-suited for panel data on SMEs, where the size of the firm and the input decisions vary widely (Waldkirch & Ofosu, 2010). These qualities make the LP method a more reliable method of estimating productivity in our context. Furthermore, for robustness check, we employ the methods developed by Wooldridge (2009) and Rovigatti and Mollsi (2018) to estimate the TFP of enterprises.

Measurement of Fintech Development

To measure the development of fintech, this study adopts a comprehensive approach, reflective of the contemporary empirical methods utilized in the field. Drawing from various methodologies, including the Digital Financial Inclusion Index by Institute of Digital Finance, Peking University (Guo et al., 2023; Hou & Li, 2020; Peng & Ma, 2022), the regional distribution of fintech firms (Song et al., 2021), and text mining analyses based on Baidu News (Li et al., 2020) or the Baidu Search Index (Sheng & Fan, 2020), our research primarily utilizes a text mining method grounded in the Baidu Search Index.

Under this process, fintech was broken down into core components including payment and settlement, resource allocation, information intermediation, wealth management, regulatory technology, and underlying technology, corresponding to the strategic areas identified in the Fintech Development Plan (2022–2025) by the People’s Bank of China (2022). This classification allowed us to define 36 key words, reflecting the multi-layered essence of fintech, coming from industry forums and reports such as the New Financial Summit, the Qingdao·China Wealth Forum, and the Progress Amidst Change—The Top 10 Keywords of Financial Technology in 2020 (Iyiou, 2020).

In the regional analysis, the Baidu Search Index served as an indicator of the search frequency of fintech-related keywords across varied cities, offering the regional picture of the involvement of the fintech (e.g., “2012 + Beijing + big data”). The Baidu Search Index is an affluent internet user database, and it serves as a critical analytical platform that reflects user demand and trends, thus aiding in real-time tracking and macroeconomic forecasting (Liu & Xu, 2015; Ripberger, 2011). We chose the Baidu Search Index for three reasons. First, it captures real-time digital activity. Second, it reflects regional differences in fintech awareness. Third, it is widely used in economic research as a proxy for online demand and market development (X. Li et al., 2024; Liu et al., 2021).

In addition, we further strengthen the regional fintech measure (at the city-level) with two additional indicators: regional fintech firm counts from the CSMAR Database and the Digital Financial Inclusion Index compiled by the Institute of Digital Finance, Peking University (Guo et al., 2020). Using these independent sources provides a triangulated, quantitative assessment of fintech development across China. The regional index is constructed by summing fintech keyword search frequencies for each city and applying a natural log transformation. This systematic construction captures the breadth of the fintech landscape and its relevance for Chinese SMEs, mapping scale and operational reach so we can analyze effects on TFP and bargaining power. Beyond the regional measure, we also build a firm-level fintech variable from annual report keywords and use it as a robustness check; Appendix Table A3 reports consistent results for TFP. We do not adopt it as the main indicator because data coverage varies across regions and years.

Our regional approach draws on established concepts and prior evidence, using search indexes and CSMAR firm counts, and reflects spatial heterogeneity documented by Ding et al. (2022) and H. Li et al. (2024). It captures broader economic and social impacts across Chinese cities and aligns with studies that emphasize regional analysis for macroeconomic consequences. Accordingly, we retain the regional measure as the primary, given its broader applicability and alignment with established practice, and treat the firm-level measure as a robustness check.

Control Variables

To account for the heterogeneity across firms, we include various control variables, such as financial ratios and firm-level characteristics. These variables help isolate the impact of fintech on productivity by reducing the omitted-variable bias. For example, leverage and liquidity ratios reflect financing structure and short-term solvency; profitability ratios show operational efficiency; and firm-size controls indicate scale effects. We control for these variables to ensure that the estimated relationship between fintech adoption and SME productivity is not confounded by the underlying firm fundamentals. The selected variables are: natural logarithm of total assets (Firm Size), the debt-to-asset ratio (Leverage), the return on equity ratio (Profitability), the cash flow-to-asset ratio (Cash Flow), the ratio of management expenses to operational income (Management Expenses Ratio), and a dummy variable for state-owned enterprises (Property Nature). Additionally, we incorporated the ratio of scientific research expenditure to regional gross domestic product (Research and Development) and the per capita gross domestic product (Urban Development), both expressed as natural logarithms. Table 1 presents the variables utilized in the empirical analysis.

Description of the Variables.

Models

The formulation of our models is based on the theories of financial intermediation and resource allocation which suggest that the reduction of financing friction improves the performance and productivity of firms (Wang et al., 2021; Xiao et al., 2022). The evolution of fintech is also assumed to make SMEs more productive. It improves the access to finance and operational efficiency, and also enhances firm’s bargaining power in the supply chains (Porter, 1979; Yang & Liang, 2024). Based on these theoretical reasons, our econometric models examine the relationship between fintech development and the productivity of SMEs, by controlling for firm- and region-specific heterogeneity. As a result, in order to investigate the relationship between the development of fintech and TFP of SMEs, we develop the following model:

In this model, TFPm,i,t represents the Total Factor Productivity (TFP) of firm i in city m during year t. Fintech refers to fintech development. X encompasses a set of control variables at both the firm and city levels. Ind signifies industry fixed effect; Year denotes the year fixed effect, and Yeart × Indi captures the combined industry-year fixed effects (Moser & Voena, 2012), which aids in mitigating endogeneity concerns. The term ε represents the random error. α refers to the estimated coefficients; therefore, a significantly positive coefficient of Fintech (α1) indicates that fintech would positively influence the TFP of SMEs, thereby confirming the first hypothesis.

Results and Discussion

In this section, we report the descriptive statistics of the key variables and the regression results from the baseline model which we use for testing the two hypotheses. We also present a series of robustness checks to verify the reliability of the findings. To improve readability, Figure 1 summarizes the key findings across specifications; detailed tables follow.

Estimated effects of fintech on SME productivity.

This figure provides a summary of the estimated coefficients of fintech on SME total factor productivity (TFP) for key dimensions: the baseline specification (Section “Results and Discussion”), the mechanism tests (Section “Mechanism Analysis of Fintech’s Impact on SMES’ TFP”), and the heterogeneity analyses (Section “Analysis on Heterogeneous Effects”). Dots are point estimates and the whiskers are 95% confidence intervals. There are labels on the x-axis that are associated with Table 4 (baseline), Table 8 to 9 (mechanisms), and Tables 10 and 11 (heterogeneity). Across specifications, fintech is associated with greater SME productivity. Moreover, both the bargaining-power and efficiency channels contribute, and the strongest effects are observed in the manufacturing sector and the eastern region. For the central and western regions, the effect is not significant, as shown by the grey whisker.

Our results are consistent with other international literature. Similar patterns were also observed in other economies, for example, in Central and Eastern Europe (Niţoi & Pochea, 2016), Japan (Otsuka, 2023), and Chile (Almeida & Fernandes, 2011), where infrastructure and innovation capacity shape productivity gains. We also find that manufacturing SMEs benefit more from fintech than firms in other sectors. A comparable pattern has been observed in Brazil, where financing channels play a more significant role in increasing productivity in manufacturing industries than in services (Barufi et al., 2016). In Vietnam, SMEs in the food manufacturing industry rely more heavily on finance and integration than service firms (Nguyen & Nguyen, 2017). Taken together, this evidence suggests that fintech adoption widens existing structural divides. It favors regions with stronger infrastructure and industries with higher financing needs. This highlights the need for targeted policies to ensure more inclusive productivity growth.

Overall, we observe a significant effect of fintech on SMEs’ productivity, however, some findings were not as strong as we expected. For example, fintech had no significant effect on SME productivity in China’s central and western regions. This is likely due to the differences in infrastructure, digital adoption, and local institutions. The weaker role for bargaining power in other sectors (e.g., service) compared to manufacturing also indicates structural differences. These results enrich our understanding by showing that the benefit from fintech is dependent on local and industry conditions rather than being uniform. This study also has boundaries that point to new directions for research. The sample is limited to listed SMEs between 2011 and 2019. This provides us with a stable pre-pandemic setting but may not capture the unlisted or micro-enterprises. Keeping in focus the pre-COVID period minimizes short-run shocks, though subsequent studies can test how the pandemic accelerated fintech adoption. Together, these factors highlight areas for further research. Importantly, they do not weaken the core finding that fintech raises SME productivity, especially through bargaining power in manufacturing firms and in more advanced regions.

Descriptive Statistics

Table 2 displays the descriptive statistics for the selected key variables. The mean of the variable TFP is 8.307, the mode is 8.237, and there is a small standard deviation, suggesting an ideal data distribution. The standard deviation is .843, showing the degree of variability of TFP. The mean of Fintech is 7.390, and the standard deviation is 1.057, showing notable diversity among different cities. Further, the mean of Property Nature is .135 with a median of 0, indicating that most of the SMEs in the sample are owned privately. A similar variety is also seen in other variables.

Descriptive Statistics of Key Variables.

Table 3 provides the correlation coefficient matrix for each variable. The analysis suggests a significant positive correlation between Fintech and TFP, which is consistent with the theoretical prediction. In addition, only the correlation coefficient between Research and Development and Urban Development is larger than .6. There is no evidence of multicollinearity among the other variables.

Pearson and Spearman Correlation Matrix.

Note. The table, shaped as a rectangle, displays a correlation matrix with correlation coefficients in each cell. A diagonal line drawn from the top-left to the bottom-right corner divides the rectangle into two triangles. The upper triangle shows Spearman correlation coefficients, while the lower triangle presents Pearson correlation coefficients.

, **, and *** denote significance at 10%, 5%, and 1% levels, respectively.

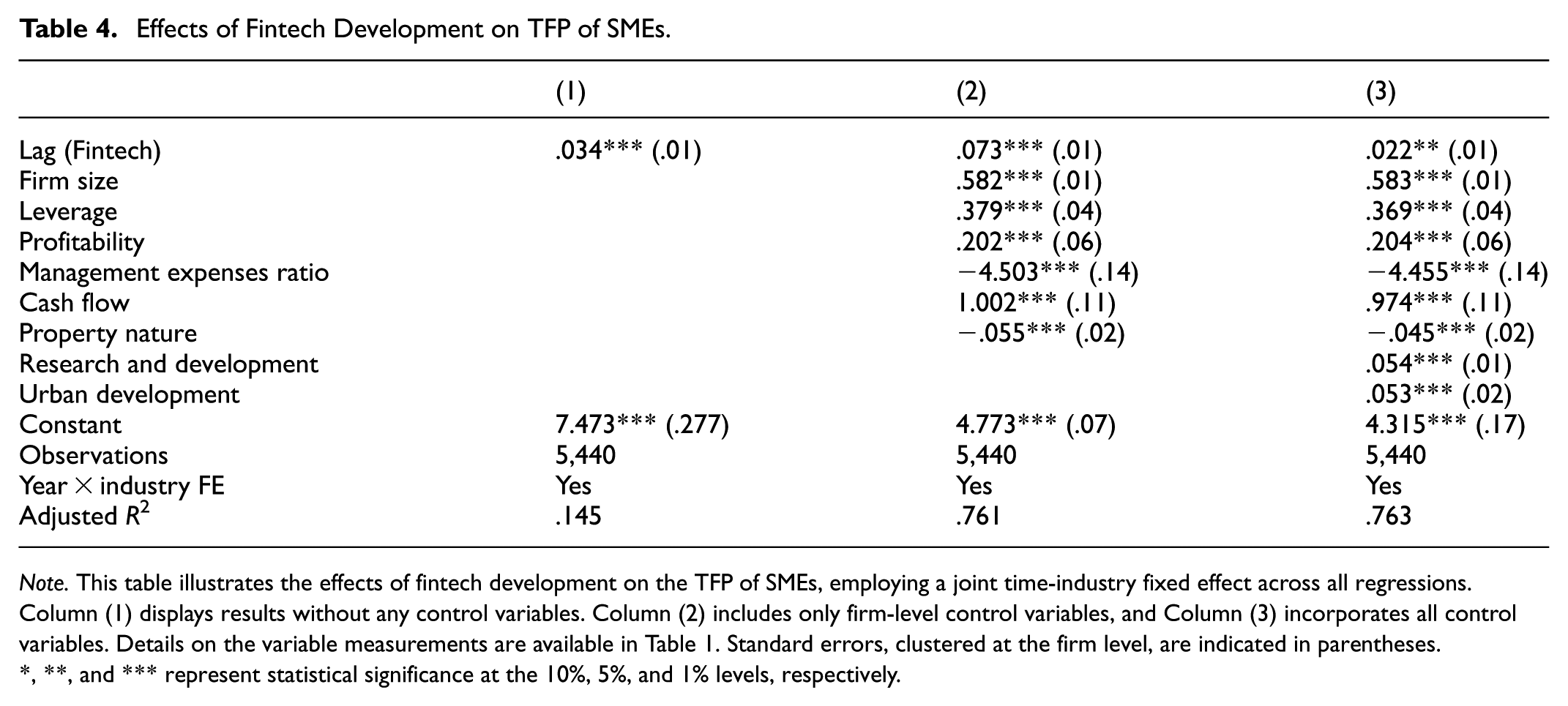

Baseline Results

As shown in Table 4, the coefficient of Lag(Fintech) is positive across all models, indicating that development of fintech in prefecture-level cities significantly promotes SMEs’ total factor productivity (TFP), which confirms Hypothesis 1. This effect stems from fintech’s technological capabilities improving production techniques, reducing information asymmetry and simplifying supply chain.

Effects of Fintech Development on TFP of SMEs.

Note. This table illustrates the effects of fintech development on the TFP of SMEs, employing a joint time-industry fixed effect across all regressions. Column (1) displays results without any control variables. Column (2) includes only firm-level control variables, and Column (3) incorporates all control variables. Details on the variable measurements are available in Table 1. Standard errors, clustered at the firm level, are indicated in parentheses.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Results in column (3) are consistent with prior studies, showing that larger firms enjoy higher TFP, as measured by the positive coefficient on firm size at the 1% significance level. Leverage, Profitability, Cash Flow, Research and Development, and Urban Development are also significant, indicate that sound financial structure, strong earnings, liquidity, government support and advanced urbanization all support TFP. Conversely, a high Management Expenses Ratio reduces TFP through higher operational costs and less funding for innovation. The negative coefficient of Enterprises Ownership Property suggests state-owned enterprises struggle to raise TFP due to weaker innovation and conservatism.

We tested for multicollinearity, especially given the number of control variables. The variance inflation factor (VIF) analysis (Table A1 of the Appendix) shows no issues. The VIF values for all variables are below the threshold for multicollinearity, confirming variable independence and result reliability.

Our study investigates the effect of historic fintech adoption (lagged fintech) on the total factor productivity (TFP) of SMEs. Regression results show a significant positive effect of fintech on TFP, with the lagged fintech variable having a coefficient of .034. After adding extra socio-economic variables at a firm level, such as Firm Size, Leverage, Profitability, Management Expense Ratio, Cash Flow, and Property Nature, the relationship strengthened, and the lag(Fintech) coefficient reached .073. This implies that the impact of fintech adoption on TFP results from complex relationships between fintech adoption and these variables. We also explored potential mediating effects to examine how socio-economic factors could moderate the effect of fintech on TFP. The Sobel test, reported in Table A2 of the Appendix, reported significant mediation effects for all variables considered (p < .05). This result is consistent with Bloom and Van Reenen (2007), who showed how technology and management practices together determine productivity.

Robustness Test

Alternative Measures of Fintech

As a robustness check, we follow prior work (Guo et al., 2023; Hou & Li, 2020; Song et al., 2021) and substitute our fintech variable with two proxies: the Digital Financial Inclusion Index (DFI) from Peking University and the regional count of fintech firms. Then we re-estimate Equation 1 using their lagged values. In Table 5, columns (1) and (2), both proxies remain positive and statistically significant at the 1% level, confirming a stable association between fintech development and SMEs’ TFP. The DFI captures the breadth and persistence of digital financial access and use, while firm counts provide a concrete picture of the expanding fintech landscape and potential indirect benefits for SMEs.

The Effects of Fintech Development on TFP of SMEs: Robustness Tests.

Note. This table presents the outcomes of the robustness checks. Column (1) presents the regression results using Digital Financial Inclusion Index data. Column (2) displays the regression outcomes employing the number of fintech companies data. Column (3) details the results with TFP recalculated via Rovigatti and Mollsi’s (2018) method. Column (4) displays the results using TFP recalculated according to Wooldridge’s (2009) method. Column (5) reveals the outcomes based on the sample data from the tumultuous years of 2015 and 2016. Variable measurements are detailed in Table 1. Standard errors, clustered at the firm level, are indicated in parentheses.

, **, and *** represent significance levels of 10%, 5%, and 1%, respectively.

We also construct a firm-level fintech measure by counting fintech-related keywords in annual reports (Appendix Table A3) and transforming frequencies into logarithms for consistency with our main construction. Although coverage is uneven across regions and years, the firm-level results exhibit the same sign as the city-level analysis (Table 4), reinforcing our main findings.

Given broader spatial coverage and alignment with regional studies that document heterogeneity and macroeconomic consequences of fintech (Ding et al., 2022; H. Li et al., 2024), we retain the city-level index as the primary measure and treat the DFI, firm-count, and firm-level indicators as robustness checks. Together, these alternatives support the conclusion that fintech development is positively associated with SMEs’ TFP.

Alternative Methods of Calculating TFP

We also adopted the methods of Wooldridge (2009) and Rovigatti and Mollsi (2018) to calculate the TFP of SMEs separately, and regressions were performed using Equation 1. Column (3) in Table 5 presents results using TFP recalculated through Rovigatti and Mollsi (2018) method, while Column (4) provides results using TFP recalculated through Wooldridge’s (2009) method. In both cases, the Lag (Fintech) coefficient is significantly positive at the 5% level, consistent with our baseline results and thus confirming the robustness of our findings.

Mitigating the Impact of Other Factors

To further solidify the robustness of our research, we consider the influence of external events and policy changes on financial services and corporate policy-making. For instance, the Chinese stock market crash of 2015 to 2016 illustrates the pronounced effect on company valuations amidst highly volatile trading activities. Such a unique market condition could, in fact, cause the results we obtained from our study to be biased.

To avoid this, we specifically exclude the data from the crisis years of 2015 and 2016, which could obscure the true effects we aim to measure. This elimination is intended to refine our regression analysis by reducing the impact of this market anomaly and preserving the integrity of our conclusions. The regression results in Column (5) of Table 5 further substantiate this methodological adjustment, which supporting our initial findings and affirming fintech’s significant role in enhancing SMEs’ TFP. As a result, by excluding data influenced by the stock market crash, this study not only confirms its conclusions but also more accurately reflects the ongoing influence of fintech on SME productivity.

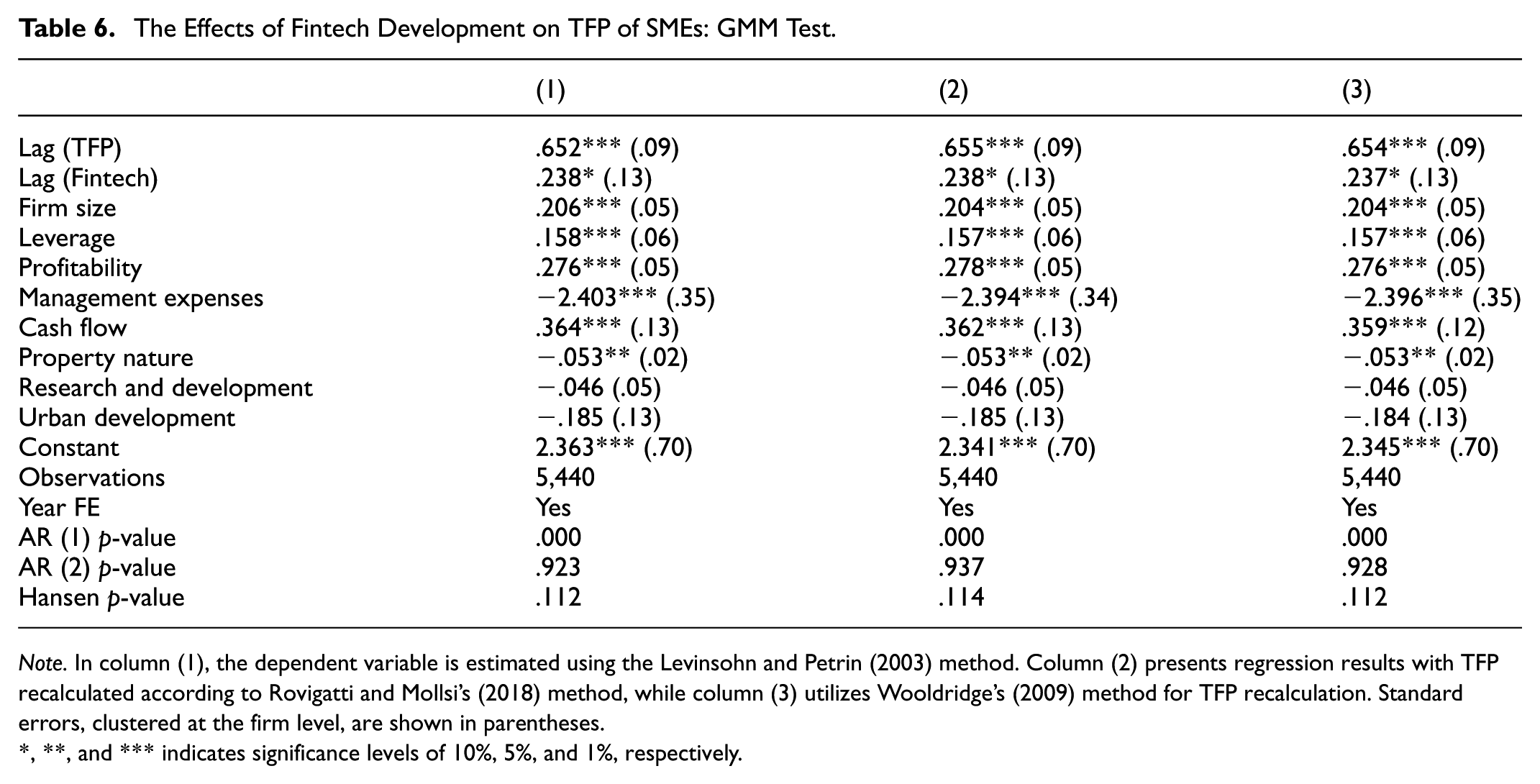

GMM Test

Given the inherent inertia in economic behavior, serial correlation might be observed in the TFP of SMEs. To address this problem, we employed the two-step Generalized Method of Moments (GMM) to enhance the robustness of our findings. The results are reported in column (1) of Table 6 using the Levinsohn and Petrin (2003; LP) method for the measurement of the dependent variable. Moreover, alternative measures of explanatory variables are presented in the paper using different estimation techniques summarized in columns (2) and (3) of Table 6. In particular, column (2) reports regressions based on TFP recalculated with the Rovigatti and Mollsi (2018) approach, and column (3) presents results using Wooldridge’s (2009) method. The fintech coefficient is positive across all regression models and achieves statistical significance at the 10% level or better. These findings are consistent with previous research and, thus, validate our study’s reliability and consistency. Compared to fixed effects or standard instrumental-variable approaches, the generalized method of moments (GMM) is more suitable in our context. Because the lagged productivity variable makes our panel model dynamic, we use GMM to avoid bias in the estimates (Das, 2019). In addition, the variables representing the development of fintech and bargaining power might be endogenous; therefore, GMM can reduce reverse causation and omitted-variable bias (Bun & Sarafidis, 2013). Finally, the two-step system GMM accounts for unobserved heterogeneity across firms and regions and provides more reliable estimators.

The Effects of Fintech Development on TFP of SMEs: GMM Test.

Note. In column (1), the dependent variable is estimated using the Levinsohn and Petrin (2003) method. Column (2) presents regression results with TFP recalculated according to Rovigatti and Mollsi’s (2018) method, while column (3) utilizes Wooldridge’s (2009) method for TFP recalculation. Standard errors, clustered at the firm level, are shown in parentheses.

, **, and *** indicates significance levels of 10%, 5%, and 1%, respectively.

Endogeneity Test

Although our regression model controls for many factors that influence both fintech and the TFP of SMEs, an improvement in SMEs’ TFP could affect the development of fintech in that region. In addition, potential omissions or measurement errors of fintech variables may bias estimates. To deal with endogeneity problems from reverse causality, omitted variables, or measurement errors, we used an instrumental variable approach for additional model estimation.

Using the method of Song et al. (2021), this study uses the average fintech index of other cities in the same province as an instrumental variable for fintech. This choice of instrumental variable meets two key criteria: relevancy and exogeneity. In terms of relevance, cities of the same province often share similar economic development levels, so fintech development tends to move together. Concerning the exogeneity, regional segmentation of credit financing and limited bargaining power of SMEs indicate that fintech development in other cities within the same province is unlikely to affect the TFP of SMEs in the focal cities directly.

The results of the regression are presented in Table 7. In the first stage, the instrument is strongly correlated with local fintech, with coefficients significant at the 1% level. In the second stage, fintech remains a positive and significant determinant of SMEs’ TFP. Weak instrument tests confirm the validity of our instrument, and additional specifications using alternative TFP calculations (columns 3–6) yield consistent signs and significance. Together, these findings mitigate concerns about endogeneity and reinforce the conclusion that fintech development contributes to higher SME productivity.

The Effects of Fintech Development on TFP of SMEs: Endogenous Test.

Note. This table reports the results of the endogeneity test by method of the instrumental variable. The instrumental variable is the average fintech index of other cities in the same province. The dependent variable (TFP) in column (2) is calculated using the method of Levinsohn and Petrin (2003), while the method of Wooldridge (2009) is applied for column (4), and Rovigatti and Mollsi’s (2018) approach is employed for column (6). The standard errors are clustered at the firm-level in parentheses.

, **, and *** denotes significance at 10%, 5%, and 1% levels, respectively.

Mechanism Analysis of Fintech’s Impact on SMEs’ TFP

Previous discussions showed that the development of fintech could lead to the growth of SMEs’ TFP. A crucial area for further investigation is understanding the mechanisms through which fintech influences enterprise TFP. In this section, we examine whether fintech can enhance TFP by providing companies with improved bargaining power in an enabling capacity.

Stakeholders such as dealers (customers) and suppliers act as collaborators and competitors to enterprises (Fernandez et al., 2014). A high concentration among customers and suppliers can erode enterprise profits by reducing sales and increasing costs. To sustain operations and control risks, enterprises may reduce investment in research, and development (R&D) which is the main driver for TFP (Amable et al., 2010). Fintech, however, provides SMEs with more choices, improves supply chain management, increases negotiation power, reduces financing constraints, and channels funds into innovation and R&D.

To examine this channel, we adopt the approach of Fang (2017) and Gu and Wang (2021). We use the total purchase proportion from the top five suppliers as a measure of supplier concentration and the total sales proportion to the top five customers as an indicator of customer concentration. We then calculate the supply chain concentration (SCC) using the entropy method and natural logarithm transformation. SCC is an inverse index, a larger value indicates higher supplier and customer concentration and weaker bargaining power.

Following Baron and Kenny (1986), we employ a mediation effect model, as shown in Equations 2 and 3.

The results in Table 8 show that fintech significantly reduces SCC (column 1) and that SCC negatively affects TFP while fintech remains positive (column 2). These findings indicate that supply chain concentration acts as a mediating factor, supporting Hypothesis 2. Fintech thus enhances SMEs’ bargaining power, reinforcing TFP. The integration of big data, cloud computing, and blockchain further improves supply chain management, strengthens SMEs’ negotiating position, and facilitates innovation and R&D. We also perform a Sobel test to confirm the mediation effect found in our analysis. The test yields a p-value of .004, indicating a valid mediating effect accounting for 13.4% of the total effect. Moreover, a bootstrapped analysis of 1,000 random samples also shows significance with a direct effect of −.017 (p-value = .033). These findings confirm the mediating role of bargaining power and enhance the robustness and reliability of our conclusions.

The Effects of Fintech Development on TFP of SMEs: Mechanism Tests.

Note. This table outlines the mechanisms through which fintech development influences the Total Factor Productivity (TFP) of SMEs. The findings from Equation 2 are presented in Column (1), while Column (2) displays results derived from Equation 3. Standard errors, clustered at the firm level, are indicated within parentheses.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

In addition, we investigate operational efficiency as another mechanism. Previous studies indicate that digital technology greatly enhances TFP throughout the industrial chain. For instance, upstream enterprises improve their productivity by adopting new digital technologies, and downstream firms respond by refining production management, raising overall operational efficiency (Bartel et al., 2007; Castro & McQuinn, 2015; Yang et al., 2022). To capture this, we use inventory turnover, measured as the cost of goods sold divided by average inventory, as an indicator of operational efficiency. Our empirical tests, based on (2) and (3), examine how fintech influences inventory turnover rates and thus fosters TFP growth.

Results in Table 9 indicate that fintech significantly boosts inventory turnover rates and, therefore, improves operational efficiency. These results provide insights that fintech not only supports SMEs financially but also improves efficiency, showing its role extends beyond traditional finance to broader productivity gains.

The Effects of Fintech Development on TFP of SMEs: Mechanism Tests.

Note. This table outlines the mechanisms through which fintech development influences the Total Factor Productivity (TFP) of SMEs. The findings from Equation 2 are presented in Column (1), while Column (2) displays results derived from Equation 3. Standard errors, clustered at the firm level, are indicated within parentheses.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

Analysis on Heterogeneous Effects

There are three reasons why we pay attention to regional and industry heterogeneity. First, fintech development is highly uneven across cities in China (Zhao et al., 2022), which can be explained by the differences in digital infrastructure, financial inclusion, and local institutional conditions (Song et al., 2020). Thus, the regional differences are captured by our city-level fintech index. Second, industries differ in their reliance on external finance and supply chain coordination. Manufacturing SMEs are relatively more capital- and working-capital-intensive and have longer cash-conversion cycles than their service-sector counterparts (Rajan & Zingales, 1998). In turn, the increase in bargaining power due to fintech innovations is likely to increase total factor productivity more significantly for manufacturing SMEs (Zhu & Yu, 2024). Third, we focus our analysis on these two dimensions of policy relevance to maintain statistical power and increase interpretability. Other variables (e.g., ownership structure, firm size, or age) are included in the models as control variables and are examined in robustness check. These dimensions are secondary to our main question of the bargaining-power channel.

Regional Heterogeneity

To examine and ascertain the regional dependency of these mechanisms, we divided our sample into two groups based on the firms’ locations: one for the eastern regions and the other for the central and western regions. We then re-evaluated these groups using the mediator effect model outlined in section “Mechanism Analysis of Fintech’s Impact on SMES’ TFP.”

The regression results for both groups are shown in Table 10. Columns (1) to (3) provide the results for the eastern region, while columns (4) to (6) focus on the central and western regions. The results show that in the eastern region, fintech improves the market position of SMEs by reducing supply chain concentration, thereby increasing TFP. However, this mediator effect is not significant in the central and western regions.

The Effects of Fintech Development on TFP of SMEs: Regional Heterogeneity Test.

Note. This table illustrates the impact of fintech development on the TFP of SMEs, taking into account regional heterogeneity. Columns (1) to (3) present the findings for the eastern region, while columns (4) to (6) detail the results for the central and western regions. Standard errors, clustered at the firm level, are indicated in parentheses.

, **, and *** represent statistical significance at the 10%, 5%, and 1% levels, respectively.

In contrast to the central and western regions, the eastern region has higher economic growth, advanced technology, more marketization, more abundant resources, and relatively sound infrastructure. These strengths not only provide a good basis for fintech development but also provide substantial support for SMEs, especially in the areas of human resources acquisition, productivity improvement, and financing accessibility. Besides, the diversification of dealers and suppliers in SMEs in this region makes SMEs gain higher bargaining power and, in turn, further enhance their productivity.

Industrial Heterogeneity

To explore if industry-specific variations exist in the interplay between fintech, bargaining power, and SMEs’ TFP, this study categorizes the samples into two groups: manufacturing and other industries according to the enterprises’ industrial classification. This approach facilitates an examination of the mediating effect in these sectors.

The regression results for the manufacturing sector are reported in Columns (1) to (3) of Table 11. This indicates that fintech enhances firms’ bargaining power, increasing SMEs’ TFP, thereby implying a mediating role of bargaining power in the manufacturing industries. In comparison, other industries show an alternative pattern, as Columns (4) to (6) indicate. In this case, although fintech positively affects SMEs’ TFP, bargaining power does not act as a mediator. This difference stems from manufacturers’ increased vulnerability to supply chain pressures from suppliers and dealers, which weakens their bargaining power. Nevertheless, fintech provides a new path for manufacturers by enabling the use of AI, blockchain, and other technologies. The technologies facilitate effective market monitoring, thus liberate firms from a centralized supply chain, and boost productivity. They also support SMEs’ innovation and the research, which leads to high-quality development.

The Effects of Fintech Development on TFP of SMEs: Industrial Heterogeneity Test.

Note. This table illustrates the impact of fintech development on the TFP of SMEs, accounting for industry heterogeneity. Details on variable measurements can be found in Table 1. Columns (1) through (3) present results from the eastern region, while results from other industries are featured in Columns (4) through (6). Standard errors, clustered at the firm level, are indicated in parentheses.

, **, and *** denotes significance levels of 10%, 5%, and 1%, respectively.

Conclusion

In China’s transition toward high-quality economic development, utilizing emerging financial technologies to improve SMEs’ Total Factor Productivity (TFP) is crucial. This paper analyses regional fintech development on the TFP of SMEs, using a sample of China’s A-share listed SMEs from 2011 to 2019. We developed a keyword lexicon from relevant meeting and policy documents. We used Python to scrap the annual average Baidu search index across various provinces and cities, thus quantifying the development level of fintech. The results of our research suggest that regional fintech progress has a significant impact on the TFP of SMEs. These findings remain valid after controlling for endogeneity, adopting different approaches to measure fintech development, employing various methods to calculate TFP, and excluding specific influential factors for robustness.

This study offers several practical and policy implications. First, the development of fintech is necessary to support SMEs’ transformation into high-quality development and is one of the key areas in financial supply-side reform in China. Our estimates show that an increase in the bank fintech index is associated with higher productivity of SMEs. This suggests that initiatives to expand digital credit analytics and supply-chain finance can raise productivity. As a result, managers might consider using fintech tools to enhance supply-chain bargaining power, lower costs, and improve operational efficiency.

Second, SMEs could use fintech to improve the efficiency of the supply chain systems, leading to less reliance on limited suppliers and distributors, thus enhancing TFP. Technologies such as blockchain, big data, and cloud computing can decrease information asymmetry, help firms identify credible partners, and foster trust. This not only stabilises supply chains but also creates opportunities for mutually beneficial outcomes.

Third, it is important for policymakers to strengthen financial regulation and establish systems to mitigate risks associated with fintech. Although fintech has several advantages, it also brings significant regulatory issues, including market and legal risks. Fraud and misuse can be prevented by improving financial supervision. The government could also use AI-based, data-driven systems to maintain constant and real-time monitoring, which would enhance macro-prudential regulation and still allow the gain in SME productivity via fintech.

This study also has boundaries that point to new directions for research. The sample is limited to listed SMEs in China between 2011 and 2019. It may not fully represent smaller, unlisted businesses. At the same time, this period covers a decade of rapid fintech expansion before the pandemic. It allows us to focus on structural effects without the short-term disruption of COVID-19. Future research could extend the analysis to unlisted firms or use post-pandemic data to capture new developments in digital finance. Our study also centers on a regional (city-level) fintech index and the bargaining-power mechanism. This provides novel insights, while leaving room for further studies to test other measures of fintech development and additional channels. Such work would complement our findings and deepen understanding of how fintech affects SME productivity.

The study also has social and practical implications. By expanding digital credit analytics and supply-chain finance, fintech can enable SMEs to gain a better market position and support innovation. Financial institutions and policymakers can use these insights to develop targeted programs to improve access to finance for SMEs, decrease costs, and facilitate sustainable growth. For a broader perspective, our findings also have wide relevance and policy implications. Many emerging economies face similar challenges, namely, limited SME financing and uneven regional development. China’s experience shows how digital financial systems can boost the productivity of SMEs by increasing bargaining power and operational efficiency, especially in the manufacturing sector and developed regions. For policymakers working in other contexts, we believe that three priorities stand out: the strategic distribution of resources to digital infrastructure, the enabling of competitive fintech ecosystems, and the balancing of innovation with effective regulation. All of these are critical for ensuring inclusive productive growth.

Footnotes

Appendix

Regression Results of Fintech Impact at Firm Level.

| Variables | TFP |

|---|---|

| Lag (fintech) | .035*** (.01) |

| Firm size | .578*** (.01) |

| Leverage | .371*** (.04) |

| Profitability | .208*** (.06) |

| Management expenses | −4.499*** (.13) |

| Cash flow | 1.008*** (.11) |

| Property nature | −.043*** (.02) |

| Research and development | .0568*** (.01) |

| Urban development | .063*** (.02) |

| Constant | 5.251*** (.24) |

| Year × industry FE | 5,440 |

| Observations | Yes |

| Adjusted R2 | .765 |

Note. This table presents the regression results of fintech impact on the TFP of SMEs, measured at the firm level. We collected firm-level fintech data by extracting keyword frequencies from corporate annual reports, detailed in section “Variables” The table illustrates results from a comprehensive analysis incorporating variables described in Table 1. Standard errors are clustered at the firm level and are shown in parentheses.

Significance level of 1%.

Acknowledgements

We would like to express our gratitude to the editors and anonymous reviewers for their insightful comments and suggestions.

Ethics Considerations

This study did not involve human participants or animals. Ethics approval was therefore not required.

Consent to Participate

Not applicable.

Author Contributions

Yanjuan Cui: Writing – Review & Editing, Methodology, Conceptualization, Supervision, Funding acquisition. Xinwei Wang: Writing – Original Draft, Methodology, Data Curation, Software, Format Checking. Hong Lin: Original Draft, Methodology, Data Curation, Software. Xingang Wang: Writing – Review & Editing, Methodology.

Funding

The authors disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The Scientific Research Project of the Education Department of Liaoning Province (LJ112410173045); 2024 Liaoning Province Social Sciences Planning Fund Project (L24AJY006); Research Project of Liaoning Province of Social Sciences (2022lslybkt-008); Scientific Research Project of Dongbei University of Finance and Economics (DUFE202104).

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used in this study are available for research purposes subject to approval by the Shenzhen CSMAR Data Technology Co., Ltd. Interested researchers can contact Shenzhen CSMAR Data Technology Co., Ltd to request the data. The data used in this study are available from the corresponding author upon reasonable request.