Abstract

This study aimed at analyzing the influence of the use of technology on the use of financial services and innovation of SMEs in Africa. The study further analyzes the mediating role of the use of financial services on firm use of technology-innovation relationships among SMEs in Africa. The study utilizes data retrieved from the enterprise survey portal. The analysis employs multiple regression to test the models using SPSS, and the Sobel test further examines mediation. The results reveal a significant positive association of firm use of technology on the use of financial services and innovation. Also, there is a positive association between the use of financial services and SME innovations in Africa. The study found partial mediation of the use of financial services on the use of technology-innovation relationships. The results have implications on African SMEs need to amplify the sensitization and emphasis on fostering the use of technology in innovating new products and processes. While promoting innovation, the use of technology can enhance financial inclusion resulting in wider and deeper financing options for enterprises in Africa, which are deeply hampered by financial and technological vulnerability.

Introduction

Notably, researchers confirm that SMEs comprise an important niche in developing the country’s economy and as a dynamic employment base (Aris, 2007; Beck et al., 2005; Kongolo, 2010). SMEs in developing economies accounted to encompasses at least half of business and form at least half an employment base (Alam & Noor, 2009). SMEs are well-thought-out to be the hinge of economic progress, and especially in Africa, they are means for life sustenance and survival (Aremu & Adeyemi, 2011). The infiltration of digital technology in these business operations has revolutionized the firm practices (Byrne et al., 2013; Hobijn & Jovanovic, 2001). Despite the challenges that digital technology has brought about, there is still ample and justifiable benefit that firms accrue from the utilization of technology. The waves of digital technology have obliged businesses to adjust and catch up with the rhythm of fast-moving and changing technology (Adeniran & Johnston, 2012). One of the notable areas that digital technology has intertwined with is the area of finance. There has been an increasing trend of technology to be used in devising new customized financial products and applied directly in the execution of such financial products (McKechnie et al., 2006). That is why we have fintech and digital finance, recent prominent phrases confirming the merging of digital technology and financial system. With the rapid progress of mobile money technology complementing, computer technology in Africa has optimized and simplified the utilization of many financial products and services. For instance, an online mobile money transfer can be undertaken instead of a bank money transfer. It helps in terms of cost reduction and cuts down the time lag (Truong, 2016). This discovery has become a vital support for the application and ongoing development of firm innovations. Besides, it has evolved the financial technology infrastructure sophisticating many applications, including financial management, data analysis, management of cash, automated transaction system, and loan management.

There is a relatively general low level of technological advancement in Africa, and the continent shows a deviant picture when it comes to ICT adoption, whereby few states have managed to profit from some ICT capacities and many still lag (Datta, 2011). Africa is vulnerable to problems of deep digital and financial illiteracy (Mabula & Ping, 2018). The situation is coupled with a low pace of technology and financial market powers that are underdeveloped. Therefore, when it comes to technology, the level that has been attained by developed countries is more at an advanced level. African countries still struggle with internet connectivity, application of emails, utilization of social media, and owning a website. These are challenges that are not in tandem with developed world technological level (Ejemeyovwi et al., 2019; Grimes et al., 2012; Hargittai, 1999) Also, in terms of financial markets and access to finance with exceptions of South Africa, Africa has a shallow and thin financial market characterized by inaccessibility to consumers (Pattillo et al., 2006). With reservations of many initiatives underway from the developed countries in enhancing the quality provision of formal financial services like insurance, savings, payment systems, credits, and pensions sustainably, most of the developing economies are still capped by a large share of their populations without access to basic financial services (Ouma et al., 2017). The trend that emerges from the body of literature regarding the low level of utilization of financial services and involvement in the financial market by both households and firms can also be traced to be attributed to financial illiteracy (Nunoo & Andoh, 2012). Besides these challenges, there are signs of improvement as there are many initiatives that have thriven though in an unsystematic manner to curb the situation of inaccessibility to technology and finances. Thanks to the prevalence of mobile phones that has increased the touch of technology adoption and has eased many financial transactions through mobile phone payments (Aker & Mbiti, 2010; Ejemeyovwi & Osabuohien, 2018). The firm’s utilization of financial products is an indicator of not only accessing services and products but also possessing the right skills and knowledge of handling such services and products (Fatoki, 2014). Researching on the financial literacy for microenterprises owners in South Africa employ the utilization of technology as one of the factors that determine their firm financial capability. In this survey, it was found that most of the respondent firms do not have emails and have no access to the internet at work; none of these surveyed firms had a website. The state shows how Africa is lagging in terms of adopting the utilization of technology to harness the yields that have been demonstrated achievable in the other part of the world. Digital technology is at the heart of firm innovation, but without access to proper financing, many ideas die without being implemented. Therefore, this study tries to assess whether there is a significant relationship amid the utilization of technology and the utilization of financial products by SMEs in Africa. We also assess the double array firm utilization of technology and financial services’ impact on innovation in terms of the ability to devise and introduce new products and create new, improved processes. The study further assesses the mediating role of the utilization of financial service on the utilization of technology-innovation relationship. We venture to analyze SMEs in Africa because most of these firms owned by individuals and families. The novelty of this paper is visualized in studying the association of utilization of technology, utilization of financial services, and innovation at the firm level in Africa whereby there is a dearth of related studies, especially in the region. Most of the ICT studies with financial inclusions have focused individual and household level (Andrianaivo & Kpodar, 2012; Diniz et al., 2012). The study uniquely analyses the mediation of the utilization of financial services on the utilization of technology and firm innovation, therefore, the study contributes to the existing literature on SME management and practices in the African context and the world at large.

Hypothesis Development

The study is motivated by the “Unified Theory of acceptance linked to the utilization of technology by Venkatesh et al. (2003). The author established this theory based on the synthesis of prior technological adoption and acceptance research. The theory comprises four key elements of performance expectancy, social welfare, effort expectancy, and facilitating features. These elements are presupposed to affect the behavior intentions to utilize technology. This study establishes the basis at the firm level; it focuses on performance expectancy, which is explained as the extent to which the utilization of technology shall deliver benefit to the consumer in performing innovative tasks. And the other different variables such as age, gender, and experiences are theorized to a reasonable different unified theory of acceptance and utilization of technology at the individual level (Venkatesh et al., 2012), at firm level factor like age of the firm, organization type, and size of the firm are the desirable factors.

Technology has intertwined itself in the financial market. It is not only applicable in improving and innovations of services available, but also it has become part and parcel of the current financial systems, products, and services (Mishkin & Strahan, 1999). Considering the extent of technology being used by the firms in their endeavor, some other internal and external factors need to be considered. SME adoption and utilization of technology have a positive relationship with sensitizing the firm to access and utilize financial services, which is another factor that contributes to enhancing the better performance of the firm (A. A. Karakara & Osabuohien, 2019; Mawona & Mpogole, 2013). Nevertheless, Africa has a lower level of ICT adoption, and access to financial services still is an issue at stake. Still, firms that have endeavored to venture into the utilization of present technology are better placed to access more financial products since most of these financial products and services are technologically based. We, therefore, argue that:

H1 For African SMEs, the utilization of technology has a positive association with firm utilization of financial services.

Many factors can be accounted for in the firm innovativeness. But the contribution of the utilization of technology optimally amplifies innovation to achieve the best results. An innovative firm has a sense of customizing its products and services to suit the current trends and satisfy the customer’s desire (Higón, 2012). Assert that SMEs ICT applications that are specifically focused on certain market applications display exemplary potentials for establishing innovative firm products with competitive advantages. Also Tan et al. (2009) signaled a less cost-effective device of communicating to customers was achieved in Malaysia by adopting new ICT. However, security was still a concern. There is no such business that is not connected somehow to technology. The technological process has greatly facilitated the new innovative conducts of improving the present methods and creation of novel services and products. The fact of prevalent detrimental factors on technological base in Africa results in exacerbated challenges in harnessing the desired results. ICT adoption by firms foster their innovative abilities and be better placed to compete in the industry and the entire market (A. A.-W. Karakara & Osabuohien, 2020).Holding other factors constant, therefore it is argued that:

H2 SME utilization of technology is positively related to firm innovation in Africa

H2a SME utilization of technology has a positively associated with the introduction of new products

H2b SME Utilization of technology is positively related to a significantly improved process

Financial access and actual utilization of financial services in Africa are considered to be among the factors that can enhance firm success (Fatoki, 2012; Fowowe, 2017). However, Africa has been a subject of a weak financial system predisposed to the weak institutional framework, in such a way the informal financial system has mushroomed and grasped a big share of the market, and this informality comes with a lot of challenges. Ceteris paribus, the availability of financing facilities, and actual utilization of it by firms can foster a firm endeavor to venture into technological processes. Without enough access to financing, the power of the firm to prevail is jeopardized. Particularly for SMEs obtaining financing and services from the banks at affordable cost and considerable terms are challenging (Rahaman, 2011). We, therefore, propose that:

H3 SME utilization of financial services has a positive association with the utilization of firm innovation

H3a utilization of financial products has a positive association with the introduction of new products

H3b SME utilization of financial products has a positive association with significantly improved process

The phenomenon to be examined is whether the firm utilization of technology is also influenced by firm utilization of financial services. Since presumptuously, we have theorized these two variables to positively influence firm innovation one of these variables can explain well the association of the other with SME innovation. Though we have hypothesized the direct linkage between innovation and the utilization of technology, it is imperative to demonstrate the examinable mechanisms and methods that may explicate the manifestation of these relationships. The extent of the utilization of financial services reflects access to such a service. And scholarly evidence provides for the vital contribution of the utilization of technology on access to financial service (Ivatury, 2009; McKechnie et al., 2006). The prevalence of digital financial products connotes the application of technology in enhancing the usability of financial products to consumers (Gomber et al., 2017). Therefore, there is part of UFS which is embedded with the utilization of technology. Furthermore, innovation has been demonstrated to be an artifact of technology (Calantone et al., 2002; Oliveira & Fraga, 2011). The firm now can access a wider market share because technology has injected reshaping and simplification of the products and services meeting the customer’s taste (Slater et al., 2014). Well-placed firm access to finances may facilitate the acquisition of novel technology which facilitates tech-based innovations. therefore, the more the firm can manage different sources of finances with the ideal mix can enable firm innovation in improving and devising new products and services (N. Lee et al., 2015). We therefore examine:

H4 For African SMEs, the utilization of financial services mediates the Utilization of technology and firm innovation association.

Literature

The utilization of technology at the level of the firm can be visualized in dual facets, the first being the technology that is dedicated to being utilized by financial firms in optimizing their operations in commercials such as banking, insurance, and microfinance. The second is the application of new technology to innovate and provide efficient financial services rendered to its customers. And these would include mobile payment apps, online money transfers, and digital loan management (Micu & Micu, 2016). Scholars have categorized the factors for ICT adoption into external and internal. The factors that internally influence the adoptions may comprise owner/managers features, firm features, acceptance and implementation costs, and the perceived return on investment, while the external factors include infrastructure, social, cultural, legal, political, and factors related to regulations (Dholakia & Kshetri, 2004). All these have a contribution to firm-level adopting technology. Firms can easily manage the internal factors of my strategizing for changes, but it is difficult to positively workout the external factors (Matthews, 2007). Argue that firms assimilate ICT into three distinct levels or stages which may encompass: elementary adoption, extensive, and sophisticated adoption. In the elementary adoption, the firm minimally utilizes IT services and products the firm operationalization; extensive adoption comprises of the presence of numerous transactional processes and machinery that utilizes ICT and sophisticated adoption imply that the joint-working of many and different systems that use and integrate ICT in its processes. Many of the businesses, especially in sub-Saharan Africa, fall in the category of elementary adoption. Scholarly literature suggests that there are three groups of factors and determinants concerning the adoption of ICT by firms. First are factors that are attributed to company staffs’ probability to utilize ICT, features the company operates in, and factors related to the characteristics of the firm (Tarutė & Gatautis, 2014). Another perspective of the utilization of technology by firms that were introduced by Consoli (2012) identifies four groups that are affected.

These features include performance, expansion, growth, and the ability to introduce new products. Each of the mentioned attainable terms reflects on efficiency, processes productivity, and quality of the products. And many scholars have provided that the utilization of technology has a considerable optimistic influence on economic growth and labor productivity (Ishida, 2015; Nica, 2015). More scholars provide that the utilization of technology enhances service delivery and improves the productivity of the firm while making services and products more tradable (Clohessy et al., 2016). The utilization of technology in the financial services phenomenon is a transfer of financial services and products through a unit of technological platforms and innovative financial business models (D. K. C. Lee & Teo, 2015). The other two synonymous words are digital finance and fintech. The definition of fin-tech generally accepted is lacking. Some definition focuses on companies that use technology to make financial systems functions efficiently (Schueffel, 2016), while some other scholar defines fintech as a combination of financial and technology services to finance companies and to their customers. Since fintech is more or less dedicated to finance companies as we explore the adoption of technology by other SMEs, we use the word “utilization of technology. FinTech’s besides offering bank-line services for receipt of financial transactions and facilitating loan process, also help in the pace of innovation for the firms, in turn, they rapidly increase their customer base. These are deemed to be flexible, accessible, and tailored products and services to their esteemed customers. Digitalization has penetrated digital financial services resulting in innovative financial technologies increasing individual, and businesses access to financial services and products (Alexander et al., 2017). Access financial services do not certainly connote consuming it. Some determinants may enhance or daunt consumers’ actual utilization of the service or product. The affordability, social dimensions, legal, and eligibility would be the other proxies that determine consumer’s ability to use a service or product. Access entails points of service delivery that are readily accessible in multiple locations (Beck & Peria, 2006). While the use is the actual consumption of such a service, the more summing term would be financial inclusion. Putting aside South Africa’s financial sector development, the rest of the countries in Africa possess the lowest level of development of the financial sector; the rural areas are more vulnerable. The bank penetration in Sub-Saharan Africa is considered to be below 35% and an approximation of 80% of Africa’s population they are constrained to access formal banking services and products (Demirgüç-Kunt et al., 2015). Enterprise survey data evidence that only 22% possess a loan or a line of credit and at least 45% of firms in Africa mention lack of access financial services as a key impediment to their progress (Demirguc-Kunt & Klapper, 2012). The discovery of digital finance deemed potential in enhancing the provision of cheap, fast, and more accessibility to finances by SMEs, which will convey better-quality answers than as it is a non-formal economy. The market for financial services and products is currently thriven by online financial services which either target SMEs or are suitable for their conditions have emerging and many potential streams are trying to take advantage of the present unexploited and enormous opportunity for enterprises to expand their productive capacity (Indjikian et al., 2002).

Innovation is distinctly defined considering its intricacy, and it can be traced from minor transformation for processes, existing products, and/services to advanced products, services, or products that come with first-time features in the market (Dibrell et al., 2008). Defining innovation in terms of process the scholars propose that it is concerned with the interaction between events and human resources in various stages determining the continuation of the adoption process. At the firm-level innovation has been categorized into the closed and open process.

The closed innovation model is where the enterprise generates its ideas and then create, market, and disseminate and support them on self-basis (Smallbone et al., 2003). On the contrary, open innovation involves firms drawing on internal and external ideas, direct them to the market while researching to determine ground-breaking chances (Enkel et al., 2009). Technology-based innovation enhances customer taste of their products and services relatively within the market by integrating advanced new technologies (Benner & Tushman, 2003). The philosophy of technology orientation echoes the technological push. The technological push means that consumers prefer products and services which are technologically leading (Gatignon & Xuereb, 1997). Tech-based SMEs are deemed to pave the way for the utilization of the current technology in devising novel services and products and considerable research resources and development as a result they excel in their technical expertise, a critical driver for break-through innovation (Zhou et al., 2005).

Methodology

Data for the study were accessed from Enterprise Surveys (http://www.enterprisesurveys.org). Enterprise surveys employ a standard questionnaire and collect data detailing the business conditions and operations including the information about owners and top managers. The data for the survey are collected using a global methodology that includes uniform standardized survey instruments and uniform sampling methodology. Data used in this study had was limited to 5 years from now 2014 to 2019 to maintain its timeliness and comparability. Therefore, a cluster of 5-year differences of data is considered to have minor outliers as per variable chosen in the analysis. Because the analysis also considers the ability of the managers to influence their utilization of technology and financial services which is typically based on the firm top manager’s ability to influence and make decisions thought to be more appropriate with small and medium firms, therefore, the analysis excludes the large firms. Table 1 displays the sample characteristics after data sorting. The data shows many small firms were involved in the study accounting for 66.8% remainder were medium. Services firms are account for 59.24% of the firms used in the study. A total of 11,504 firms are forming the sample, and Nigeria is depicted to have the largest number of 2,487 firms involved in the study, while the least number of 118 firms comes from Benin.

Sample African Countries with Corresponding Firm Sizes and Business Sectors.

Measures and Variables

Description of the measurements and variables that are used to determine the level of utilization of the utilization of technology, utilization of financial services, and firm innovations used in this study. For the utilization of technology (UT), we identified the following six variables:

Firm communication with clients and supplier via email (CCE), this is the indicator expressing the percentage of firms communicating with clients via email. The establishment of owning a website (EOW). The variable expresses whether the firm possess a website.

Firm premises having high-speed broadband connections. The percentage of firms having a high-speed broadband connection

A firm using the internet in ordering its purchases. The percentage of firms ordering their purchases through the internet

The practice of using internet connections in serving their clients

Whether the internet is used in developing and researching new ideas of services and products.

However, all the other variables exhibited no or very little data rendering them unsuitable to be useful in the analysis except for the two variables of CCE and EOW. Therefore, only two variables were included in the analysis. Communicating using email, establishing websites These variables show to what extent the firm involved adopted technology by

The actual use of the financial services and products present in the financial system is represented by (UFP). And, in our case, the utilization of financial products mirrors the degree of the firm actual utilization of financial products accessed (Marlow et al., 2013). Therefore, the following variables were identified.

An establishment having a saving or checking account (SCA)

An establishment having a facility of an overdraft (OF)

An establishment having a loan or a line of credit (LoC)

The variables indicate the firm extent of using financial products where (Wale & Makina, 2017) used the like variables when studying account ownership and usage of financial products

Innovation (IN) at a firm-level involves the introduction of new services, products, and methods which increases the firm value; it may also connote upgrading of the existing services, products, and methods.

Two variables deemed fit to reflect the firm innovations from the questionnaire.it also involves the improvement of the present products, services, and processes. In the enterprise survey questionnaire, two variables were identified to capture the SME innovation.

New product/service introduced over the last 3 years (IN)

During the last 3 years, there was a new or significantly improved process (NIP)

These are the variables that were also employed by Koellinger (2008). Table 2 displays the mean variables core, the standard deviation, and the Pearson correlation, which measures the direction and strength of the association of two variables, except age and size which are the control variables, the results are shown in the table display all variables have a significant positive correlation.

Correlation Among the Variables.

Significant at < .05.

Significant at < .001.

Analysis and Results Discussion

The main goal of this study was to assess the utilization of technology’s impact on firm innovation in the presence of the utilization of financial services and products. To evaluate the UFP impact on SME innovation in Africa and scrutinize the mediation effect of UFP on the UT-IN relationship. To test the hypotheses, multiple regression models were employed. To test the suitability of using regression analysis, normality of residuals and homogeneity was tested (Hair et al., 1998). An insignificant violation of the assumptions was detected. The test for mediation was undertaken using SPSS and Sobel test. Table 3 summarizes the multiple regression results. The results in the Model I confirm that the firm having its website and ability to communicate with its customers has a significant positive relationship with its capability to have a checking and savings account. The results in the model I confirm hypothesis H1, which proposed that the utilization of technology has a positive association with the firm utilization of financial services. The model also connotes that the firm size has a significant negative association with the utilization of financial services. Model II shows that firm possession of its website has a significant influence on a firm’s capacity to access overdraft services, but the model shows insignificant negative results of the firm practice of the utilization of email on having and servicing an overdraft facility. Again, these results partly confirm H1.

Multiple Regression Results.

Significant at < .05.

Significant at < .001.

Model III also confirms significant positive results of the firm’s ability to own its website on the ability to have and service a line of credit, but insignificant results are depicted when it comes to CCE and LoC association. These results also partly confirm H1. The results from multiple regression reveal that the adoption and utilization of technology by SMEs in Africa can enhance access and utilization of financial services, as it has been exemplified ICT play important merit in financial inclusion (Mawona & Mpogole, 2013). The results reveal that the utilization of technology positively influences African firms to have checking and savings accounts and access various forms of finances from a financial institution. These results provide empirical tests to Mawona and Mpogole (2013), where the utilization of ICT in terms of mobile money adoption is confirmed to enhance financial inclusion. The utilization of technology is considered to be a game-changer in advancing financial inclusions to African firms and individuals (Triki & Faye, 2013). In general stance, the results indicate that information and communication technology spurs availability of financial products which widen the avenue for financial products consumers (Ejemeyovwi et al., 2021).

The utilization of technology facilitates speedy information gathering, storage, retrieval, and exchange at a higher rate, thereby assist in optimal financial decisions. Model IV in Table 3 confirms that for the firm in Africa, communicating with clients using electronic means and owning a firm website has a positive significant relationship with the introduction of new products. The results confirm H2a, which proposed that the utilization of technology positively impacts SMEs’ innovation in Africa. Model V also presents results that affirm that there is a significant and positive relationship between the SMEs’ owning website and communication via email on the creation of the new significantly improved process. The results confirm H2b, which is projected as African SMEs use more technology its innovativeness also increases. The results confirm significant results on the H2, which proposed that the UT has an impact on firm innovation for African firms. The results provide more such empirical evidence of the technology enhance more innovation innovations by firms in Africa as it has been exemplified by Modimogale and Kroeze (2009), Mpofu et al. (2013), and Wolf (2001).

Model VI shows the results of the association between UFP and Innovation. The results confirm that there is a significant positive result on the association of SCA, OF, and LoC on the firm capability to initiate new products. These results support H3a. And lastly, Table 3 model VII affirms that there is a significant positive association between SCA, OF, and LoC on a firm’s ability to significantly improve its processes in Africa. The results support hypothesis H3b.

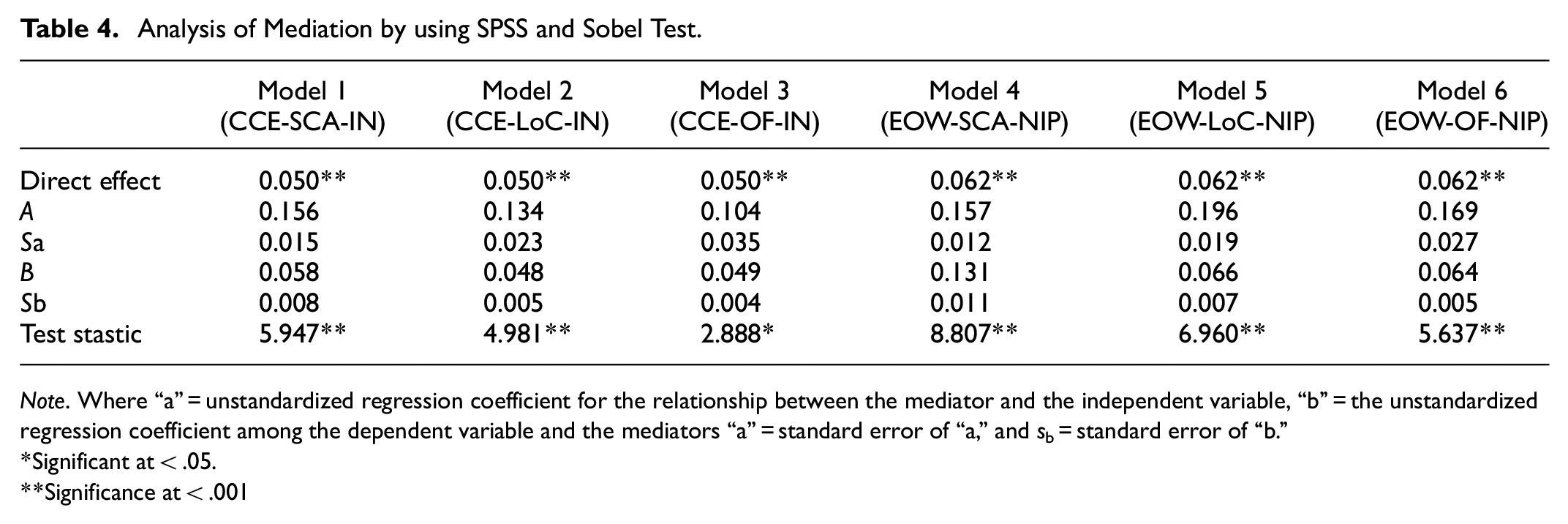

The Mediation of Utilization of Financial Products and Services (UFP)

Therefore, the study tested the mediating role of UFP on UT and IN relationships. We aimed to test whether the indirect effect of UFP fully or partially explains the effect of the UT and IN relationship. Table 4 shows how the various variables of UFP were tested on the mediation effect. The UT as an independent variable comprises of CCE and EOW, The IN as a dependent variable has IN, and NIP variables, and the UFP as the mediating have SCA, LoC, and OF. All these are tested in the various model display. First of all, examined the direct effect between the independent and dependent variables, all the results were significant as shown in Table 4. We tested for mediation by using linear regression on SPSS to obtain the unstandardized coefficients of the dependent and independent variables and their corresponding standard error. Then the result was input in the Sobel test of mediation an online calculator to check on whether the resultant Z statistic was significant (Cheung & Lau, 2008). The results show all the models tested were strongly significant except for model III, whereby OF is observed to have a weak impact on CCE and IN a relationship. The fact that we have a significant result in the direct effect between dependent and independent variable it connotes that the UFP mediation on UT-IN relationship is partial. That’s we have both indirect and direct effects significant. All the resultant effect was positive meaning that this is complementary partial mediation which indicates that the portion of the effect of UT on IN is mediated through UFP, while UT still explains a portion of IN that is independent of UFS. The results confirm hypothesis H4, which proposed the mediation effect of UFS on the UT-IN relationship.

Analysis of Mediation by using SPSS and Sobel Test.

Note. Where “a” = unstandardized regression coefficient for the relationship between the mediator and the independent variable, “b” = the unstandardized regression coefficient among the dependent variable and the mediators “a” = standard error of “a,” and sb = standard error of “b.”

Significant at < .05.

Significance at < .001

Conclusion and Recommendations

Although there are increased researches on ICT adoption by firms, relatively little is known on the empirical connections of the utilization of technology, financial inclusions, and innovations at the firm level in developing economies. As we focus on Africa, the region characterized by the low level of technology development and financial vulnerability, it still matters to undergo empirical investigation with unique antecedents for enhancing firm performance. Unlike other papers that have focused on mobile phone use and impact on firm performance., the paper addresses this gap and uniquely analyzed the mediation role of the utilization of financial services. The high significance level of association of the utilization of technology and the utilization of financial services by SMEs in Africa implicate the importance of firms focusing on technology utilization for enhancing financial inclusion in Africa. The availability of technology-based solutions can play a great role in promoting financial inclusion in Africa.

On the other hand, the study observed a highly significant impact of the utilization of technology by firms in Africa on their innovation processes. The observation implies that for firms’ innovations to have an impact on their market share, integrating technology is inevitable. Tech-based innovations have had a taste of being loved by the current millennial generation, therefore, it is easier to capture the market share and in turn, may enhance firm performance and sustainability. The study also shows the partial meditation of utilization of financial services on tech-based innovations, which connote that tech-based innovation is more enhanced when firms can first access finances and optimally allocates finances on research for new technologies that will enhance firms’ introductions of new products and improve their production processes.

Further study on this aspect may focus on the interconnectivity of technology and financial issues at the firm level in the Africa environment. Either focusing on tech-based innovation is a progressive phenomenon that needs a constant watch, and more study will never quench such unfathomable opportunities. Also, further study may wish to widen the scope of analytical data not just focusing on the use but also the factors that attenuate the utilization of technology and financial services by SMEs in the African continent.

This study concentrated on the utilization of technology, the utilization of finance, and innovation variables that are obtained in the enterprise survey portal. Such other surveys could be undertaken, integrating many more variables of the phenomena. The technology and financial use variable are limited to those which are used by the enterprise survey. Surveys that may integrate more variables of the utilization of technology and financial services would provide more robust results.

Policy Implications

Government and specific institutions governing the operationalization of manufacturing and service firms in Africa, should recognize the booming connections between finance and technology, as they devise means to enhance the venture success, they should appreciate that their moves in tandem with aggregating the operationalization of technology and finance.

For enhancing firm innovation technology and financial thrust are inevitable. Policy makers sensitizing innovations at firm level may wish to tap into the potentiality of marriage of financial and technology. The connection has enabled the creation of hybridized products which can be customized to fit the particular challenge facing a firm in its locality.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.