Abstract

The aim of this research is twofold: establishing whether access to bank financing facilitates innovation in SMEs and whether such effect can be explained from a gender perspective. Using a sample of 310 Spanish SMEs, this study first examines the effect of alleviating financial constraints on both technological and management innovation through a structural equation model. Then, the moderating effect of gender is examined. Our results showed that (a) relaxing financial constraints helps SMEs to innovate in both technological and management innovation, (b) the effect of the relaxation of financial constraints is significantly greater in companies managed by women, and (c) the moderating effect of gender occurs from the double perspective of technological innovation and management innovation. Our empirical results suggest that the gender of the CEO plays a vital moderating role among innovation and financial constraints, providing new evidence about women’s contribution to innovation in SMEs, so these results have practical business and institutional implications as they point out the relevance to promote employment policies that favour the gender diversity of employees at all hierarchical levels of the company.

Introduction

Research on innovation is a persistent topic within the business sector. Thus, the literature on this subject is extensive with studies at business, industrial, and regional levels (Damanpour et al., 2009; McCann & Ortega-Argilés, 2015). In this context, it’s increasingly difficult to ignore the importance of women’s role in economic activities, as in recent years they have become more and more prominent in the professional sphere (Ojeda-López et al., 2019), as globalization has made them more visible in the world of work (Sarada Ramesh, 2013). Although women have made a great effort to grow their businesses in the labour market (Sarfaraz et al., 2014; Zeb & Ihsan, 2020), in general, they seem to be more risk-averse (Langowitz & Minniti, 2007; Nissan et al., 2012). However, the effect of risk aversion on female innovativeness has not been clearly analyzed in the previous literature, as most studies have focused on the innovation performed by men, and there is a systematic gap in the research on innovation activities performed by women (Kuschel & Lepeley, 2016).

Nevertheless, business innovation processes have been related to difficulties in accessing financing, showing that the existence of financial constraints affects companies’ innovation abilities. Moreover, empirical evidence has demonstrated that problems caused by financial constraints are even more obvious for businesswomen due to gender stereotypes (Godwin et al., 2006). Therefore, it seems that gender differences in accessing financing are considered an obstacle to business growth (Coleman et al., 2019).

The aim of this study is twofold: establishing whether access to bank financing facilitates innovation in SMEs and whether the effect of financial constraints on innovation can be explained from a gender perspective. For this purpose, we used questionnaires completed by SMEs Spanish managers about their innovation outputs and the difficulties encountered in accessing bank financing. The data obtained enabled us to build a structural equation model that provides an essential contribution to the understanding of this innovative field.

Hypotheses Development

Alleviating Financial Constraints and Innovation

Literature related to innovation in business is extensive and includes different approaches to the development of the concept of innovation. The first discussions and analyses of this subject were carried out by Schumpeter (1939), who introduced the concept of innovation understood as a new production function. However, this concept has recently been questioned by studies that have demonstrated that innovation is a fundamental tool in business management, as it generates competitive advantages for companies (Carboni & Russu, 2018). In addition, numerous studies have shown that innovative activities involve many aspects simultaneously in the business area, such as new products, new process technologies, and new organizational practices (Heredia Pérez et al., 2019; Johannessen et al., 2001). In this context, the concept of the innovation process is of great importance, as it is defined as a complex and dynamic system of external research, which includes not only an innovative model but also different innovation types (Bucherer et al., 2012; Laursen, 2012; Markides, 2006; Wang et al., 2015).

The classification of innovation has been widely studied in previous research by a large number of authors. One of the first approaches used to establish the types of innovation was that of authors Daft (1978) and Damanpour (1992) who argued that innovation has generally been classified into technological and management innovations to signify the differences among social structure and technology in organizations. Technological innovation refers to products, services, and production processes (Damanpour, 2010), and they refer to methodological changes that allow greater performance and efficiency (Antonucci & Pianta, 2002; Kahn, 2018; Terjesen & Patel, 2017; Trantopoulos et al., 2017). However, innovation in management can be defined as “the invention and implementation of a management practice, process, structure, or technique that is new to the state of the art and is intended to further organizational goals” (Birkinshaw et al., 2008; Gebauer et al., 2017, among others). Thus, while technological innovation is linked to the primary work activities of the organization, management innovation is associated with its management (Damanpour, 1991, 2010; Zahra & Covin, 1994).

Financial constraints refer to limited access to financial borrowing (Bigsten et al., 2003; Feder et al., 1990) and is a key factor for innovative development (Fombang & Adjasi, 2018). In this context, the previous literature shows some controversy about the effects of financial constraints on business innovation. The majority of previous studies provide evidence of the negative effects that financial constraints have on innovation (Efthyvoulou & Vahter, 2016; Fang et al., 2014; Gorodnichenko & Schnitzer, 2013; Hall, 2002; Hottenrott & Peters, 2012). These adverse effects explain why companies with fewer financial constraints are in a better position to increase their investments in innovation. Other studies question the effect of financial constraints on innovation in firms (Ayyagari et al., 2011; Bond et al., 2005; Harhoff, 1998). This effect would only happen if external finance had an essential role in the supply of capital to the innovating firm (Ayyagari et al., 2011).

In short, previous literature indicates that alleviating financial constraints is an important factor when explaining business innovation (García-Pérez-de-Lema et al., 2021). Furthermore, there is much more evidence of the negative effects caused by financial constraints on innovation, and these negative effects make businesses with fewer financial constraints more likely to increase their investments in innovation (Cornaggia et al., 2015; Efthyvoulou & Vahter, 2016). Hence, eliminating or alleviating financial constraints may produce higher innovation outputs in SMEs. Therefore, we propose the following research hypotheses as follows:

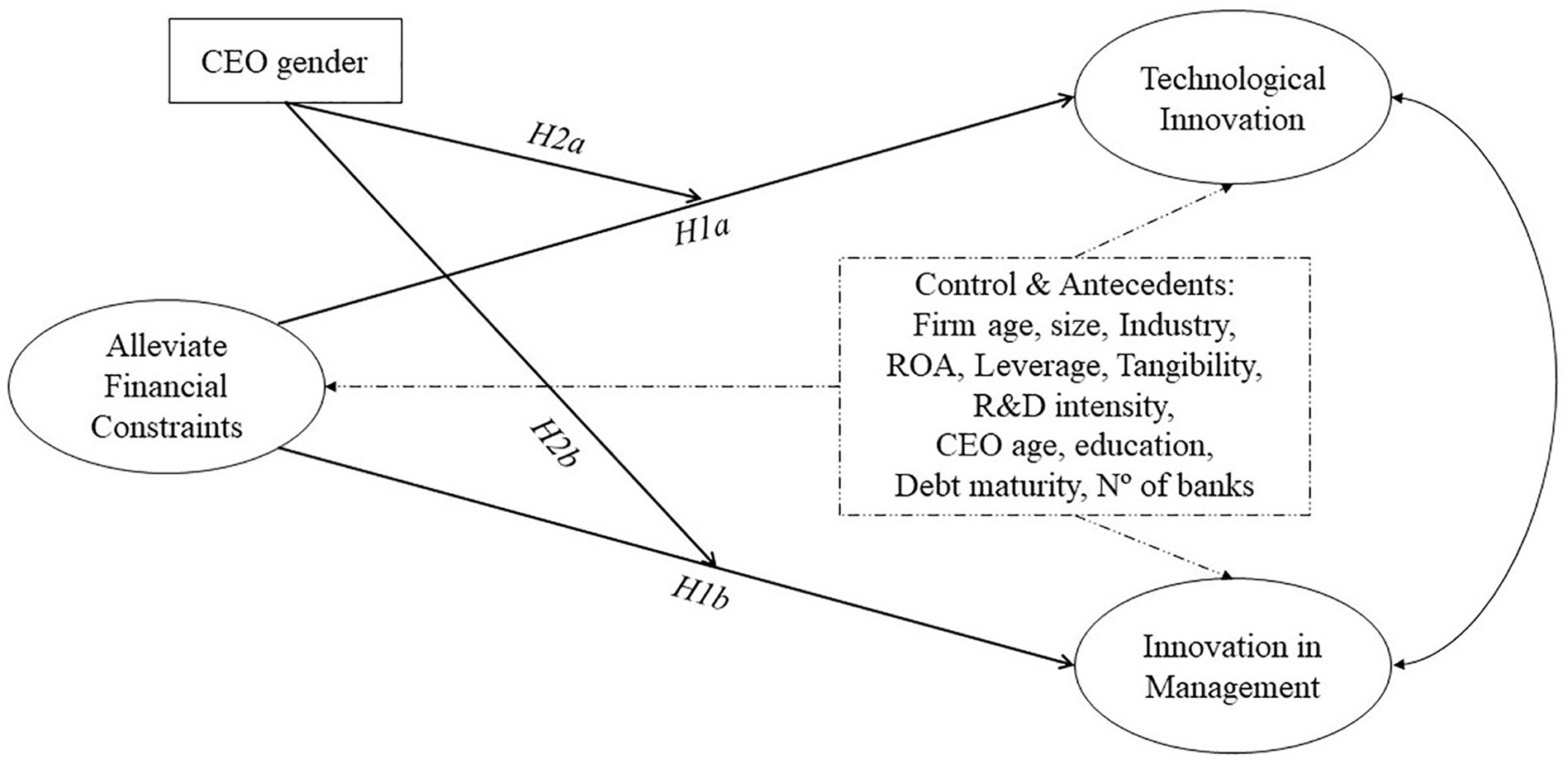

Hypothesis 1a (H1a): A reduction in financial constraints will increase technological innovation in SMEs.

Hypothesis 1b (H1b): A reduction in financial constraints will increase management innovation in SMEs.

The Moderating Role of Gender

The role of gender in business innovation has previously been analyzed by a large number of researchers. The generalization of the research published to date concludes that gender diversity among employees has a positive impact on the innovativeness of firms (Ritter-Hayashi et al., 2016). This is because gender diversity could increase the interaction between different types of skills and knowledge which would contribute to making the firm more open to new ideas and more creative (Østergaard et al., 2011). Thus, the establishment of policies and programs that encourage companies to hire a more gender-diverse workforce plays a key role in business innovation (Østergaard et al., 2011; Ritter-Hayashi et al., 2016).

On the other hand, the obstacle of financial constraints seems to be more pronounced in women due to gender-based stereotypes (Godwin et al., 2006). Hence, a growing literature on female entrepreneurship has examined gender differences in credit markets and the factors that can help female entrepreneurs access finance (Pham & Talavera, 2018). Previous studies show that female entrepreneurs face multiple obstacles caused by the lack of opportunities (Panda & Dash, 2014, 2016). However, the available evidence on discrimination against women when accessing bank financing is not conclusive either. Being a woman is not a disadvantage when obtaining bank loans, as both men and women receive equal treatment (Iakovleva et al., 2013; Lituchy & Reavley, 2004). But other studies have indicated that women entrepreneurs face many challenges, including gender discrimination, work-family conflicts, financial constraints, lack of infrastructural support, unfavourable business and political environments, lack of training, and limitations due to their personality (Cho et al., 2019; Kemppainen, 2019; Nählinder, 2010).

In addition, there is a great interest in studying the difficulties faced by women entrepreneurs when applying for bank credit (Halkias et al., 2011; Jamali, 2009; Maden, 2015; Naguib & Jamali, 2015; Ramadani et al., 2015). Research shows that this is due to the high-risk category of entrepreneurs (Thampy, 2010). Women entrepreneurs often have more difficulties accessing credit than men due to weaker credit history, lower remuneration, and inadequate savings (Carter et al., 2007; Sandhu et al., 2012; Thampy, 2010). As a consequence, Sexton and Bowman-Upton (1990) found that, in relation to the four facets of risk (monetary, physical, social, and ethical), women, in general, tend to be more averse to monetary risk. Then, men show a higher propensity for risk due to a greater preference for financial gains. Conversely, women accept less financial gain in exchange for less risk-taking with the firm (Brush et al., 2006). In addition, other researchers suggest that women entrepreneurs are more risk-averse than men because they are less confident in their ability to make financial decisions (Forlani, 2013; Lituchy & Reavley, 2004; Stefani & Vacca, 2015). Therefore, women owners are more likely to prefer low-risk businesses (Kepler & Shane, 2007, p. 53).

Available scientific literature also shows evidence that both the profile of the company and that of its owners influence the nature and extent of financial constraints (Bigsten et al., 2003; Rand, 2007; Tran & Santarelli, 2014). In general, women entrepreneurs tend to run smaller businesses, thus reducing the chances of accessing bank financing (Stefani & Vacca, 2015). It is clear to some authors that discrimination against women may arise from the fact that women-owned businesses tend to have fewer capital (Alesina et al., 2013; Treichel & Scott, 2006; Verheul & Thurik, 2001). Therefore, discrimination against women may arise from the fact that women-owned businesses tend to have a lower amount of equity capital (Pham & Talavera, 2018; Verheul & Thurik, 2001). Consequently, loan approval is problematic as banks are often reluctant to lend to low equity firms (Pham & Talavera, 2018).

In the end, the role of women in accessing credit has been extensively studied in the literature, where it has been shown that women entrepreneurs face a large number of obstacles in accessing bank credit (Halkias et al., 2011; Naguib & Jamali, 2015; Ramadani et al., 2015). On the other hand, the role of women has also been extensively analyzed in the framework of innovation, where it has been shown that, in general, women entrepreneurs innovate less because they are more risk-averse than men (Nissan et al., 2012; Stefani & Vacca, 2015). From these arguments, the following hypotheses are proposed:

Hypothesis 2a (H2a): Gender moderates the positive relationship among alleviating financial constraints and technological innovation, so that the relationship will be stronger for firms managed by women. That is, alleviating financial constraints might reduce the gender gap in SMEs technological innovation.

Hypothesis 2b (H2b): Gender moderates the positive relationship among alleviating financial constraints and management innovation, so that the relationship will be stronger for firms managed by women. That is, alleviating financial constraints might reduce the gender gap in SMEs innovation in management.

Figure 1 shows the research model and hypotheses.

Research model.

Methodology

Sample

This study uses a sample of 310 Spanish companies randomly selected from those that meet the SME criterion in accordance with European Commission Recommendation 2003/361/EC of 6th May 2003. SMEs are economically and socially important because of their contribution to the productive sector and their adaptability to technological changes. They contribute over 65% of GDP and are responsible for 53.3% of imports and 51.1% of exports in Spain (Eurostat, 2019). This sample size provides a sample error of 5.57% for a 95% confidence interval based on an infinite population. The smallest sample size for this model with 3 latent variables and 16 manifest variables is 296, defining an anticipated effect size of 0.2, a p-value of .05 and a power of 0.80 (Westland, 2010).

The contact details of the companies in the sample were obtained from the Bureau van Dijk’s Iberian Balance Sheet Analysis System (SABI) database, and the selection process was based on the principles of stratified random sampling for finite populations, with size and industry as segmentation variables. The size of each segment was implemented according to the information available in the official statistics of the National Institute of Statistics (INE, 2019). The information on the businesses in the sample comes from a telephone survey addressed to business managers, considering that managers are the most important decision-makers and their points of view and opinions have a significant impact on the company’s strategic behaviour (O’Regan & Sims, 2008; Van Gils, 2005). Respondents who chose not to answer were randomly replaced by others of similar size and sector.

The telephone surveys were conducted from November 2016 to January 2017. A structured interview with a set of Likert-scale questions was used, where the opinion of the respondent was asked about several questions related to the evolution of some aspects of financial constraints and innovation. When making the contact, the interviewer asked to talk to the manager of the company. On speaking to the manager, the interviewer introduced the purpose of the study and ensured the statistical confidentiality of the information.

Table 1 shows the composition of the selected sample. The presence of women is proportionally lower in medium-sized enterprises (6%) than in micro and small enterprises (around 15%). Concerning the sector, construction has the highest percentage of companies managed by women (18%). This ratio of female CEO is similar to those obtained in some previous works in Spanish companies (García Solarte et al., 2012; Herrera Madueño et al., 2016).

Sample Distribution.

Measurements

We measured the managers’ perceptions about the evolution of financial constraints and the innovation outputs related to their competitors through multi-item responses on 5-point Likert scales that were based on previous literature.

Regarding the reduction of financial constraints, we used a questionnaire since the utilization of account-based ratios as a proxy for the availability of bank financing do not always accurately measure the situation of the firm (García-Pérez-de-Lema et al., 2021), because it cannot be known if the firm has not applied for financing or if the lenders have refused it (e.g., Savignac, 2008). Hence, the degree of financial constraints was determined by costs, repayment terms, required guarantees, and the volume of bank financing (Amara et al., 2016; Blanchard et al., 2013; Savignac, 2008).

Regarding innovation, we followed a subjective approach to assess both technological and management innovation (Diéguez-Soto et al., 2016), since it seems to be particularly appropriate in SMEs (Hughes, 2003). First, we used six questions to measure technological innovation, three of them are questions related to product innovation and the other three related to the innovation in processes (García-Pérez-de-Lema et al., 2021; Ruiz-Palomo et al., 2019; Uhlaner et al., 2013). Management innovation was established using four items (Belderbos et al., 2018; Bubou & Amadi-Echendu, 2018).

In addition, the gender of business managers was associated with the gender of the CEO (Carter et al., 2007; Pham & Talavera, 2018).

Finally, 11 antecedent variables on relaxing financing constraints have been considered which have also been used as control variables in the innovation models. These variables are related to the company’s profile [age, size, industry, return on assets (ROA), debts, tangible assets, and R&D intensity], to the personal characteristics of the company’s CEO (age and educational level), and to the characteristics of the company’s banking relationships (debt maturity and the number of banks which the firms work with).

Table 2 shows the literal of the questionnaire used to measure these variables as well as the antecedent and control variables.

Variables Definition.

Results

Factor Analyses and Validation of Measures

Our analysis was carried out using Stata (v.14). We initially assessed the feasible effect of common method variance and the reliability and validity of scales through a double process. First, we perform an Exploratory Factor Analysis (EFA; Podsakoff et al., 2016) obtaining seven significant factors (eigenvalue > 1) that explain 61% of the variance (15%, 13%, 11%, 6%, 6%, 6%, and 5%, respectively), Cronbach’s α = .256. The first factor of the rotated solution corresponds to the financial constraint measures, the second factor to the technological innovation variables, and the third factor to the management innovation measures. The control variables are distributed among the four remaining factors. Afterwards, the factor analysis was repeated only with the measurement variables that compose the factor scales, and three significant factors were obtained that together explain 65% of the variance (24%, 22%, and 19%, respectively), Cronbach’s α = .874. Second, we executed a Confirmatory Factor Analysis (CFA) in which two SEM models were tested: one of them was a single factor model, and its results were not acceptable (χ2 = 1,378.6; RMSEA = 0.20; SRMR = 0.18; AVE = 0.31; CFI = 0.5; NNFI = 0.42). This model was significantly different from the second, which considers three factors separately (log-likelihood ratio test χ2 = 1134.4***). These results suggest that the common method bias was not a concern because the single factor did not comprise for most of the variance (Podsakoff et al., 2003) and because separate individual factors significantly improved the single-factor model (Podsakoff et al., 2012). In addition, possible collinearity issues between measurements were tested by estimating variance inflation factors of items (all below 2.78) and latent factors (all below 1.27).

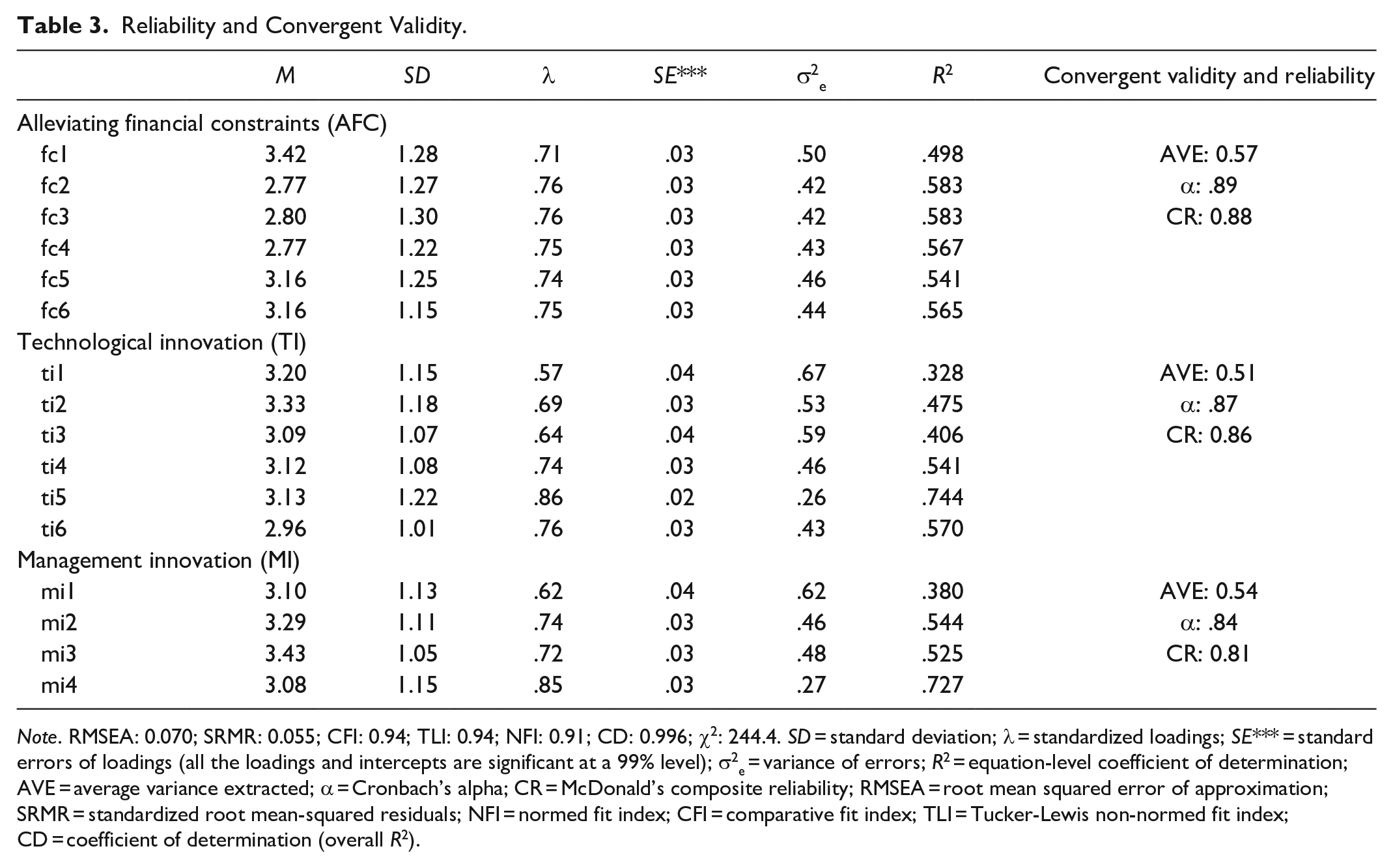

Table 3 lists the tests carried out to ensure the reliability and convergent validity of the second CFA model, which shows the goodness of fit, suggesting the reliability and convergent validity of the model (e.g., Boateng et al., 2018) because the main indices exceed their respective thresholds.

Reliability and Convergent Validity.

Note. RMSEA: 0.070; SRMR: 0.055; CFI: 0.94; TLI: 0.94; NFI: 0.91; CD: 0.996; χ2: 244.4. SD = standard deviation; λ = standardized loadings; SE*** = standard errors of loadings (all the loadings and intercepts are significant at a 99% level); σ2e = variance of errors; R2 = equation-level coefficient of determination; AVE = average variance extracted; α = Cronbach’s alpha; CR = McDonald’s composite reliability; RMSEA = root mean squared error of approximation; SRMR = standardized root mean-squared residuals; NFI = normed fit index; CFI = comparative fit index; TLI = Tucker-Lewis non-normed fit index; CD = coefficient of determination (overall R2).

Moreover, to check the discriminant validity of the model, Table 4 shows the HTMT ratios-all below 0.85—(Henseler et al., 2015), as well as inter-factor correlations -all of them lower than the squared root of AVE—(Fornell & Larcker, 1981). In addition, a slightly high inter-factor correlation between technological and management innovation suggests the existence of a close relationship between both types of innovation, which has been considered in the model specification facilitating the free covariance between them.

Discriminant Validity.

Note. Fornell-Larcker criterion: Inter-Factors Correlations below the diagonal (cursive); AVE2 in diagonal (bold). AFC = alleviating financial constraints; TI = technological innovation; MI = management innovation; HTMT ratio over the diagonal.

Finally, it is necessary to check that there are no significant differences in intercepts, loads, and error variances of the manifest variables as a requirement for comparing the results obtained for the two subsamples (Gregorich, 2006). To achieve this, four SEM models have been built to gradually relax the measurement invariance constraints and check if there are significant differences between them using the log-likelihood ratio test for the complete model, and the Wald test for each individual coefficient (Putnick & Bornstein, 2016). Table 5 summarizes the results obtained. As there are no significant differences between the models according to the constraints imposed on the external model and considering that only two error variances (afc5 and ips1) are significant at a p < .05 level, the model does not raise any doubts on the invariance of its measurements.

Measurement Invariance Assessment. Log-Likelihood Ratio Tests.

Note. Wald tests only were significant for one load (fc5*) and for three variances of item errors (fc5***, ti1**, and ti2*). Model A: Loads, intercepts, and error variances are set as invariant—strict invariance model. Model B: Loads and intercepts are set as invariant—strong invariance model. Model C: Loads are set as invariant—pattern invariance model. Model D: Neither load nor intercept nor variance of errors is set as an invariant-unrestricted model.

p < .1. **p < .05. ***p < .01.

Hypotheses Testing

To contrast the effect of the reduction of financial constraints on technological and management innovation (H1a and H1b), the significance of the internal model for the entire data set has been used. To contrast the moderating effect of the CEO’s gender (H2a and H2b), a multi-group analysis was carried out in two phases: initially, measurement invariance is ensured (see Table 5). Then, using Wald’s test, we check whether the difference in betas among the two groups considered is significant.

Once the reliability and validity of the model and the comparability of the results between both subsamples have been ensured, Table 6 and Figure 2 show the results obtained by the model for the whole sample, for companies managed by men, and for companies managed by women. They display the result of Wald’s test to identify which coefficients are significantly different for companies run by men and women. Only significant paths in at least one subsample are listed.

Inner Model Results.

Note. Antecedents and control variables only are reported whether they are significant at a 95% level at least in one model. β = standardized coefficients; z = z statistic (β/SE); e.TI↔e.MI = error covariance of Technological and Management Innovation.

p < .1. **p < .05. ***p < .01.

Results.

Our results suggest that relaxing financial constraints makes it easier for SMEs to adopt policies that allow them to innovate, which is reflected in higher innovation outputs, both in technology (β = .25***) and in management (β = .18**). Also, companies managed by women are significantly more likely to increase innovation achievements when they reduce their financial constraints (β = .79*** and β = .75***, respectively), compared to companies managed by men (β = .18*** and β = .13***, respectively), staging significant Wald tests (χ2 = 6.50** and χ2 = 4.31**, respectively). In short, the effect of relaxing financial constraints on innovation is significantly higher in women-led enterprises than in those managed by men. On the whole, this may be due to the fact that women entrepreneurs tend to run smaller businesses, thus diminishing the possibility of accessing bank financing (Stefani & Vacca, 2015). In addition, women entrepreneurs face multiple barriers regarding the lack of employment opportunities, since they have limited resources (Panda & Dash, 2016). This fact could mean that, once such restraints on resources are lifted, the effect generated is greater than in companies run by men, who seem to be less accustomed to overcoming such challenges.

As for the background that alleviates financial constraints, the size of the company, the sector, business profitability, the level and maturity of debts, and the number of banks with which the company operates are generally important. This suggests that the characteristics of the company, those of the owners, and those of the banking relationships influence the nature and the extent of the financial constraints. These results are in line with previous findings (Bigsten et al., 2003; Rand, 2007; Tran & Santarelli, 2014). However, their effects are not significantly different depending on the CEO’s gender, therefore there are no moderating effects for this variable.

Additionally, the study also found that none of the control variables in the general sample was significant at 95% for either TI or MI, although in companies managed by women the influence of company age and debt was indeed significant for both TI and MI. Furthermore, size also significantly affected management innovation in this segment. Moreover, the differences between companies managed by men and women were significant in terms of the company’s age on TI and MI. These findings are in line with previous studies and contribute to the empirical evidence that gender diversity among a company’s employees has a positive impact on innovation (Østergaard et al., 2011), especially in developed countries (Ritter-Hayashi et al., 2016).

Finally, Figure 3 illustrates the moderating role of gender on the relationship among the access to bank financing and innovation. These results indicate that companies run by women adopt a much more conservative position than those run by men in the presence of financial constraints. However, when these financial constraints are lowered, the propensity to innovate more is much higher in companies with a female CEO than in companies with a male CEO. In fact, when financial constraints are eased, the difference between the two segments is much smaller, suggesting that the gender gap in innovation could be significantly reduced thanks to facilitating access to bank financing for companies with female CEOs.

Moderation effects.

In this sense, our results confirm that financial constraints have a negative effect on business innovation, so reducing them will increase the innovativeness of firms. These results agree with those obtained in the previous studies of Efthyvoulou and Vahter (2016), Fang et al. (2014), and Gorodnichenko and Schnitzer (2013). Furthermore, these results have reinforced those proposed by the authors Sandhu et al. (2012) and Thampy (2010) by showing that gender has a moderating effect on the impact of financial constraints on innovation. However, these results contrast with those of the authors Iakovleva et al. (2013) and Lituchy and Reavley (2004) that ensure that there is no discrimination against women in accessing bank financing, and with those of Stefani and Vacca (2015) which show that women are more risk-averse than men. Our study then contributes to the existing literature by providing conclusive evidence that the gender gap in innovation could be significantly reduced thanks to facilitating access to bank financing for companies with female CEOs.

Conclusions

In the existing literature, innovation is considered as an important requirement for business development and growth. Similarly, this innovative progress has increased as women have been gradually joining business management. However, although the literature analyzing the factors that influence innovation is extensive, the impact of financial constraints and gender diversity has not been sufficiently studied. Therefore, this research aimed to provide new evidence to the study of the influence of gender diversity on innovation in Spanish SMEs.

Firstly, our results confirm that financial constraints have a negative impact on business innovation, as reducing them increases businesses’ innovation ability. Furthermore, this impact occurs in both technological and management innovation. Secondly, the presence of women in business management means that an improvement in finance access has a very positive effect on the innovation output, which would suggest that the gender of CEOs has a moderating effect in this field. Thirdly, the aforementioned moderating effect of women occurs in both innovation types, regardless of the line of business and other aspects of the company such as age or size.

Our empirical results provide new information about women’s contribution to innovation in SMEs, showing that the more involved in management women are, the greater the effect of relaxing financial constraints on innovation. Analogously, our findings have practical business and institutional implications as they point out the influence of gender, unveiling the convenience of promoting the access to bank financing for companies managed by women, as well as employment policies that favour the gender diversity of employees at all hierarchical levels of the company.

The study is regionally oriented within Spain, so it cannot provide evidence at the international level. Therefore, future research could compare our results with the business environment in other countries, including those that are under development. It is relevant that future lines of research might validate our findings in other regions or countries since we are discussing the role of gender in a heavily male-dominated organizational context, and this is a common characteristic of SMEs all around the world. However, the role of gender might look quite different from other regional contexts where this same question is still quite important. In this sense, generalizing our findings from a multicultural perspective might provide a deeper knowledge about women’s contribution to innovation in SMEs. Also, future research could further analyze the moderating effect of gender diversity in innovation through longitudinal studies of panel data to test the hypotheses raised in this work.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Universidad de Málaga.

Availability of Data and Materials

Ruiz-Palomo, Daniel; Fernández-Gámez, Manuel Ángel; León-Gómez, Ana (2020), “Database for gender moderating effects of financial constraints on business innovation,” Mendeley Data, V1, doi: 10.17632/zrkxwkfvzf.1.

Code Availability

Software application: Stata, v. 14. Statacorp.