Abstract

This study aims to examine the impacts of ownership and innovation on the sustainable development of micro and small enterprises (MSEs). Using the dataset from the 2015 China Micro and Small Enterprise Survey, this study divides the ownership of MSEs into state ownership, collective ownership, private ownership, and foreign ownership. In this study, the sustainable development of MSEs is measured by four sets of variables, sustainable operation, sustainable profitability from operations, sustainable profit input, and sustainable production or operation input. The Result suggests negative associations between the ownership of state-owned enterprises as well as collective-owned enterprises and MSEs’ sustainable development. Furthermore, public ownership also negatively contributes to MSEs’ sustainable development. Concerning the ownership of non-public-owned enterprises, while private ownership enables MSEs to develop sustainably, foreign ownership is not conducive to MSEs’ sustainable development. Besides, the result also indicates that innovation positively contributes to the sustainable development of MSEs. Moreover, this study offers implications for policymakers to take measures in promoting reform of mixed ownership as well as innovation to enhance MSEs’ sustainable development.

Keywords

Introduction

There is a burgeoning literature dealing with ownership, innovation, and enterprises’ sustainable development although this literature is not without conflict (Chege & Wang, 2020; Lin & Luan, 2020; Liu et al., 2020; Prashar & Sunder, 2020). Specifically, an increasingly prevalent topic on the sustainable development of the micro and small enterprise (MSE) has been highly highlighted since it plays a vital role in creating job opportunities, decreasing poverty, and accelerating economic growth (Asada et al., 2016; Xu et al., 2019). MSEs refer to enterprises with relatively small scales of economic activities, which are classified according to the number of employees, tax payment, and operating revenue. According to Word Trade Report 2016, the annual turnover of micro-enterprises is less than 2 million euros and the number of employees is no more than 10, while these of small businesses are less than 10 million euros as well as no more than 50 employees (WTO, 2016). Regarded as the backbone of developing economies, MSEs have played crucial roles in social stability and contributed positively to helping increase employment, alleviate poverty, and improve the rate of economic growth (Bischoff & Wood, 2013; Nursini, 2020). Data from the International Council for Small Business (ICSB, 2019) shows that small businesses contribute about 50% of GDP, and account on average for 70% of total employment. Therefore, as the most extensive production and management group among micro, small and medium enterprises, MSEs have played a pivotal role in promoting the development of the entire social economy (Faherty & Stephens, 2016).

Although MSEs have made outstanding contributions to economic development, their development has suffered enormous difficulties, with high failure rates and bankruptcy rates. In terms of the U.S. Small Business Administration (SBA, 2018), more than 20% of small businesses went bankrupt in the first year, 50% of the enterprises survived the first 5 years, and only one-third of establishments have continuously operated for 10 years or longer. Unlike large companies that can rely on their solid financial and abundant resources, MSEs face many difficulties in their development, such as political instability, limited financing channels, lack of coordination, the crisis of energy consumption, high costs of tax, limited resources, and asymmetric inter-institutional information exchange (Y. Wang, 2016). Despite the huge potential of MSEs, their operating performance is deteriorating, and thereby their sustainable development is challenged. Thus, there is an urgent need for policymakers to formulate specific policies to create a sound development environment for MSEs and provide strong motivation for their sustainable development in the long term.

In 1987, the World Economic Development Commission (WEDC) put forward the term of sustainable development for the first time in its report entitled Our Common Future (Brundtland, 1987). According to WEDC, sustainable development is defined as a development pattern that enables contemporary generations to satisfy their needs as well as sustains the capability of future generations to reach their requirements to the environment and resources. Notwithstanding, the notion of sustainable development has expanded into domains of business and management over time (López-Pérez et al., 2018), and many companies strive to achieve a balance between sustainable development and operational performance (Kuhl et al., 2016). Meanwhile, more and more studies switch to focus on the field of corporate sustainable development. For instance, some studies have examined the factors affecting sustainable development from the perspective of resources and systems (Klassen & Whybark, 1999; Kraus et al., 2020). Utilizing data from enterprises in several sub-sectors of the Canadian secondary industry, Bansal (2005) examined the organizational antecedents of corporate sustainable development, and the result suggests vital roles from resources and institutional systems. Under a highly competitive environment, most professional managers are supposed to maintain sustained profit growth and improve their management capabilities to enable companies to prosper in the long run. However, prior research has not, to the best of our knowledge, focused on the sustainable development of MSEs, and this study enriches the literature specific to the effects of ownership and innovation on the sustainable development of MSEs, which also provides novel perspectives and future research directions.

Innovation is considered to be one of the crucial means to urge corporate sustainable development and maintain a competitive advantage (Scherer & Voegtlin, 2020). To achieve a foothold in drastic competitions, MSEs are urged to constantly innovate in business practice, and thereby to overcome barriers to development through innovation and produce sustainable competitive advantages. Besides, innovation enables MSEs to maximize the utility of their available resources to make up for their deficiencies in capital and scale. The forms of innovation are diverse, not limited to the innovation in products and process, but also incorporate marketing and organizational innovation. Results suggest that innovation plays a crucial role in improving the productivity and GDP growth of countries, and is conducive to increasing market share and providing a competitive advantage in drastic competitions (Quaye & Mensah, 2019). However, innovation may also have different effects on the sustainable development of enterprises with different ownership. There are four types of corporate ownership, including state ownership, collective ownership, foreign ownership, and private ownership. Accordingly, different ownership types of MSEs have various impacts on their sustainable development. The ownership structure of the enterprise will determine a series of issues of corporate governance such as internal resource allocation, cooperation between owners and operators, and internal collaborative control (Jensen & Meckling, 1976). Several studies have shown that different types of corporate ownership may have differentiated effects on corporate technological innovation and operating performance. State-owned enterprises have low profitability and operating performance due to inefficiency, while privatization is significantly positive to enhance the profitability, operational performance, and efficiency of capital input (Boubakri et al., 2009). Besides, Megginson and Netter (2001) also found evidence that privatization is more likely to improve the operating performance of transitional enterprises. These results also imply that it is urgent to examine the effects of different ownership on the sustainable development of MSEs since despite their smaller size and weaker risk resistance, they are crucial for increasing employment and promoting overall economic growth. Unlike previous studies, this study combines the various ownership categories and innovation to further investigate their possible differential effects on MSEs’ sustainable development.

This study contributes to the literature on corporate sustainable development by exploring the roles of ownership and innovation. This study also enriches the literature on the sustainable development of MSEs by constructing a comprehensive variable to measure MSEs’ sustainable development appropriately. This can be informative for policymakers to formulate effective policies to help promote the mixed-ownership reform of public-owned MSEs and establish a sound external environment, which is positive to urge MSEs to develop more sustainably. The rest of this paper is arranged as follows. In Section 2, the literature on ownership, innovation, and MSEs’ sustainable development are reviewed in detail, and hypotheses concerning the effects of ownership and innovation on the sustainable development of MSEs are displayed respectively. Section 3 introduces the data, empirical model specification, definitions of variables, and estimation methods as well as offers descriptive statistics. In Section 4, the empirical results are appropriately presented, and the robustness, endogeneity, and heterogeneity are further discussed. Section 5 concludes and offers policy implications as well as future research directions.

Literature Review and Hypotheses

Prior Research on Sustainable Development of MSEs

As an important engine for increasing employment and promoting economic growth, the sustainable development of small and micro enterprises has been highlighted in recent studies. To be more specific, previous studies have indicated that small businesses with fewer than 50 employees are the growth drivers of a lot of countries, and they also provide a large number of employment opportunities for society. For instance, Beck et al. (2005) showed that MSEs accounted for more than 60% of the total manufacturing employment in most developing countries. MSEs are primary labor-intensive enterprises that provide employment opportunities for almost 78% of the labor force in low-income countries. Since a large number of MSEs are excluded when calculating employment data, Li and Rama (2015) re-examined the corporate dynamic development, productivity growth, and job opportunities in developing countries, proving that traditional views indeed seriously underestimated MSEs’ employment contribution. Therefore, there is an urgent need to address the importance of the sustainable development of MSEs.

The concept of sustainable development has been widely recognized, and achieving the balance between sustainable development and economic development has become the development goal of most modern enterprises. Martínez-Alonso et al. (2019) suggested that having sustainable competitive advantages is one of the key antecedents to achieving corporate sustainable development. Nevertheless, MSEs face huge challenges in their daily operations and long-term development. For instance, due to MSEs’ small size and high risks, they are more likely to be rejected when applying for loans from banks, which in turn leads to their lack of stable and reliable financing channels, thus plunging them into a shortage of funds (Seker & Correa, 2010). Besides, the results show that an excessive tax burden also hinders the sustainable development of small businesses (Hou & Lei, 2017). It is evident that small businesses specific to various types of ownership have faced different difficulties and challenges, and enterprises with state and private ownership have different financing channels (Nguyen, 2019). Compared with private-owned MSEs, enterprises with state ownership are easier and more likely to borrow operational funds from banks. Unlike extant studies, this study distinguishes the nature of ownership, and thereby focuses on the effects of different ownership categories together with innovation on the sustainable development of MSEs, which will fill the research gap in related fields.

The Ownership and Sustainable Developmentof MSEs

An enterprise’s ownership refers to the possession form of production means (Hansmann, 2000). According to types of ownership, Chinese enterprises can be broadly categorized as public-owned and non-public-owned enterprises, of which the former include state-owned and collective-owned enterprises, and the latter incorporate foreign-owned and private-owned enterprises (Choe & Yin, 2000; Pyke et al., 2000; Yang, 2015). Due to differences in property rights and the operating environment, most enterprises also perform variously in promoting economic development. Shibia and Barako (2017) argued that the structure of property rights specific to an enterprise determines a series of governance structure issues, such as internal resource allocation, cooperation between owners and operators, and internal collaborative control. Utilizing data from Kenya’s 42 listed companies, Ongore (2011) indicated that ownership concentration is negatively associated with corporate performance, while there is a positive contribution that originates from foreign capital and decentralized ownership. In the same vein, Rustam et al. (2019) collected data from the Pakistan Stock Exchange from 2016 to 2018 and explored the impact of foreign ownership on the sustainable disclosure of Pakistani non-financial enterprises. They concluded that foreign investment has significant impacts on sustainable information disclosure, in other words, foreign ownership has effectively improved the corporate governance mechanism, which enables enterprises to achieve sustainable development. Utilizing the dataset from 1989 to 1994, Conyon et al. (2002) conducted an experimental study, and the results show that the labor productivity of those local enterprises acquired from foreign companies has been improved significantly. Furthermore, Ferris and Park (2005) verified the nexus between Japanese corporate performance and the share of foreign ownership, and they revealed that foreign ownership is positively associated with corporate performance. Notwithstanding, the result also shows that there is an optimal value for this effect, that is, when the foreign shareholding ratio is on the left side of 40%, the corporate performance increases with the augment of the shareholding ratio, but if the foreign shareholding ratio is on the right side of 40%, the corporate performance decreases as the shareholding ratio increases.

The enterprises with state and private ownership have unique structures of property rights, which are highlighted in exploring the impacts of differentiated ownership on corporate performance. Recent evidence indicates that state-owned enterprises are “too big to fail,” and in the long run, these enterprises face fewer difficulties and challenges in sustainable development, so their financial and sales performance is significantly better than that of private-owned enterprises. Utilizing the data from Vietnam’s listed companies, Kubo and Phan (2019) suggested that state ownership enables these listed companies to improve their performance. Nonetheless, some studies have shown that the opposite conclusion has been reached. Based on the data of the 500 largest non-US industrial enterprises, Boardman and Vining (1989)investigated the impacts of various ownership on corporate economic performance through four profit margins and two X-efficiency indicators, and they proved that the profitability and productivity of the enterprises with state ownership, as well as enterprises with mixed ownership, are significantly lower than these of private-owned enterprises. Moreover, the result also indicates no significant difference in profitability between mixed-owned and state-owned enterprises, which reveals that only complete private control rather than partial private ownership can improve performance. Furthermore, Vining and Boardman (1992) took Canadian companies as samples and empirically examined the effect of state and private ownership on enterprises’ sustainable development. They reached a conclusion that was partially consistent with their previous research, but in the latter study, they also found that mixed-owned enterprises have higher profitability than enterprises with state ownership, but are still far below the profitability of private companies. Nevertheless, regarding the impact of ownership on the sustainable development of enterprises, most of the extant studies are only limited to large enterprises. This study attempts to explore the effects of ownership on MSEs’ sustainable development. Thus, hypotheses are proposed as follows:

Hypothesis 1 (H1): The state and collective ownerships negatively contribute to the sustainable development of MSEs.

Hypothesis 2 (H2): The ownership of foreign-owned and private-owned enterprises plays a positive role in promoting MSEs’ sustainable development.

The Innovation and Sustainable Development of MSEs

In recent decades, there has been a surge of interest in the impacts of innovation on corporate sustainable development. Concerning the definition of innovation, a large number of researchers have given different views. Thornhill (2006) suggested that innovation is a process that incurs the emergence of new products, new processes, and new services through proposing novel thoughts and finally brings these new things to the market. Ahmad (2010) defined innovation as taking advantage of new opportunities to develop a business and ultimately achieve the improvement of sustainable performance. In terms of Schumpeter’s innovation theory, continuous innovation activities are a powerful weapon for enterprises’ success in the long term, which is consistent with the general economic intuition and is also considered to be the mainstream view (Schumpeter, 1934). Also, innovation is considered to be a vital factor for enhancing sustainable competitive advantages as well as enabling an enterprise to survive and develop in a rapidly changing environment (Fischer & Sawczyn, 2013). Therefore, to obtain and maintain a competitive advantage, enterprises of any size must continue innovating, and those that do not continue innovating will put themselves in danger or even be replaced. Due to the continuous improvement of the current level of competition and the shortening of the product life cycle, enterprises are urgent to rely on innovation more than ever to improve corporate performance and maintain a competitive advantage (Cardinal, 2010). Innovation enables enterprises to develop sustainably and realize the full use of limited resources, so it is considered to be one of the most valuable sources of the sustainable competitive advantage (Gomes et al., 2011). Moreover, in the process of innovation, enterprises can obtain absorption capacity, resource utilization experience, and standard-setting ability through the effect of learning by doing. To be successful in drastic competitions, small businesses need to apply innovative advantages to compete with larger competitors. Compared with large enterprises, small enterprises have greater flexibility to make decisions and reconfigure their resources in the short term, and thereby innovation is also conducive to MSEs’ sustainable development (Malagueño et al., 2018). Besides, prior research also provides evidence that small and young enterprises are more likely to invest in innovation than that of more mature ones (Coad et al., 2016).

However, results from earlier studies suspect the positive effect of innovation on enterprise development and put forward very different views. Veugelers et al. (2019) claimed that innovation will consume a lot of resources, and for small businesses that are inherently under-resourced, the resources consumed by innovation can limit the sustainable development of small businesses. Moreover, Roper and Tapinos (2016) suggested that innovation is of uncertainty, which increases enterprises’ risk of financial cost and thereby decreases the investment in innovation. Large enterprises can bear the losses caused by innovation failure, while which will cause small enterprises to be in financial troubles or even bankrupt (Nohria & Gulati, 1996). Besides, compared with small businesses, large enterprises may have more successful experiences in innovation (Rosenbusch et al., 2011). Based on the above points, the empirical results of innovation on corporate sustainable performance are mixed as well. DeCarolis and Deeds (1999) showed a positive nexus between innovation and corporate performance, while the results of Birley and Westhead proved that innovation negatively affects corporate performance (Birley & Westhead, 1990). There is also evidence that innovation does not affect corporate external operational performance (Duhaylongsod & De Giovanni, 2019). However, these empirical studies all took large enterprises as research samples but excluded MSEs. Thus, the following hypothesis is put forward as follows:

Hypothesis 3 (H3): Innovation is conducive to the sustainable development of MSEs.

Research Design

Data Source

In this study, the data is collected from the 2015 China Micro and Small Enterprise Survey (CMSES). All the surveyed small businesses are domestic MSEs with an independent legal personality as well as family workshop enterprises, covering 28 provincial-level administrative regions across China. Besides, the sample size is 5,489.

Econometric Specification and Variables

This study seeks to explore the impacts of ownership and innovation on the sustainable development of MSEs. In terms of the hypotheses, this study specifies the baseline econometric model as follows:

In equation (1), the sampling enterprise is indicated by the subscript i. Besides,

The independent variables incorporate the state, collective, private, and foreign ownership. More specifically, the first two types of enterprises are designated as enterprises with public ownership, and the latter two types of enterprises are re-defined as enterprises with non-public ownership. The independent variable to measure enterprises’ innovation (having innovation) is measured by the question “Does your enterprise currently or ever have innovation activities in products or technology?” Accordingly, if the answer is “Yes,” the variable is coded 1, and 0 otherwise. As for control variables, following the specifications of Chen et al. (2020), the enterprise owner’s age, management experience, and educational status are incorporated. Besides, the enterprise’s operating length, current employee size, high-tech enterprise or not, and total assets are included. Also, province dummies, GDP per capita, and marketization index are entered. Additionally, all continuous variables are taken in natural logarithmic form. The marketization index comes from the research of X. Wang et al. (2017). Table 1 exhibits the variable definitions.

Definitions of Variables.

Note. The data of GDP per capita comes from the National Bureau of Statistics of China.

Estimation Method

In terms of the survey data, MSEs’ sustainable development is a discrete, categorical, and ordered variable, ranging from 0 to 4. Thus, using the method of Ordinary Least Squares (OLS) for categorical ordered data may produce misleading results and biased estimates, and thereby causing inaccurate test of the hypothesis. Due to the ordinal characteristics of the data of the dependent variable, this study utilizes the method of ordered probit regression to improve the estimates. According to the method of ordered probit regression, this study estimates the underlying score of the sustainable development of MSEs (

In equation (2), the vector of independent and control variables

In equation (3),

Furthermore,

Through the method of ordered probit regression, the probability function of MSEs’ sustainable development is more appropriate with the data features of the dependent variable, which enables estimation results to be more accurate. During the multivariate estimation, the effects of province regions and forms of enterprise organization are controlled. To produce more robust and accurate estimates, this study also constructs a new variable of the sustainable development index. The newly constructed dependent variable, namely the sustainable development index, is continuous, so the approach of OLS estimation is adequate. However, this study also utilizes the absolute values of the estimated residual as the weights to perform a robustness check through the approaches of Weighted Least Squares (WLS) estimation and ordered logistic regression. Specifically, the method of Instrumental Variable (IV) is applied to deal with endogeneity concerns. To capture the differentiated effects on the estimates from various subgroups, this study also conducts adequate discussion concerning heterogeneity in terms of the levels of economic development and marketization.

Descriptive Statistics

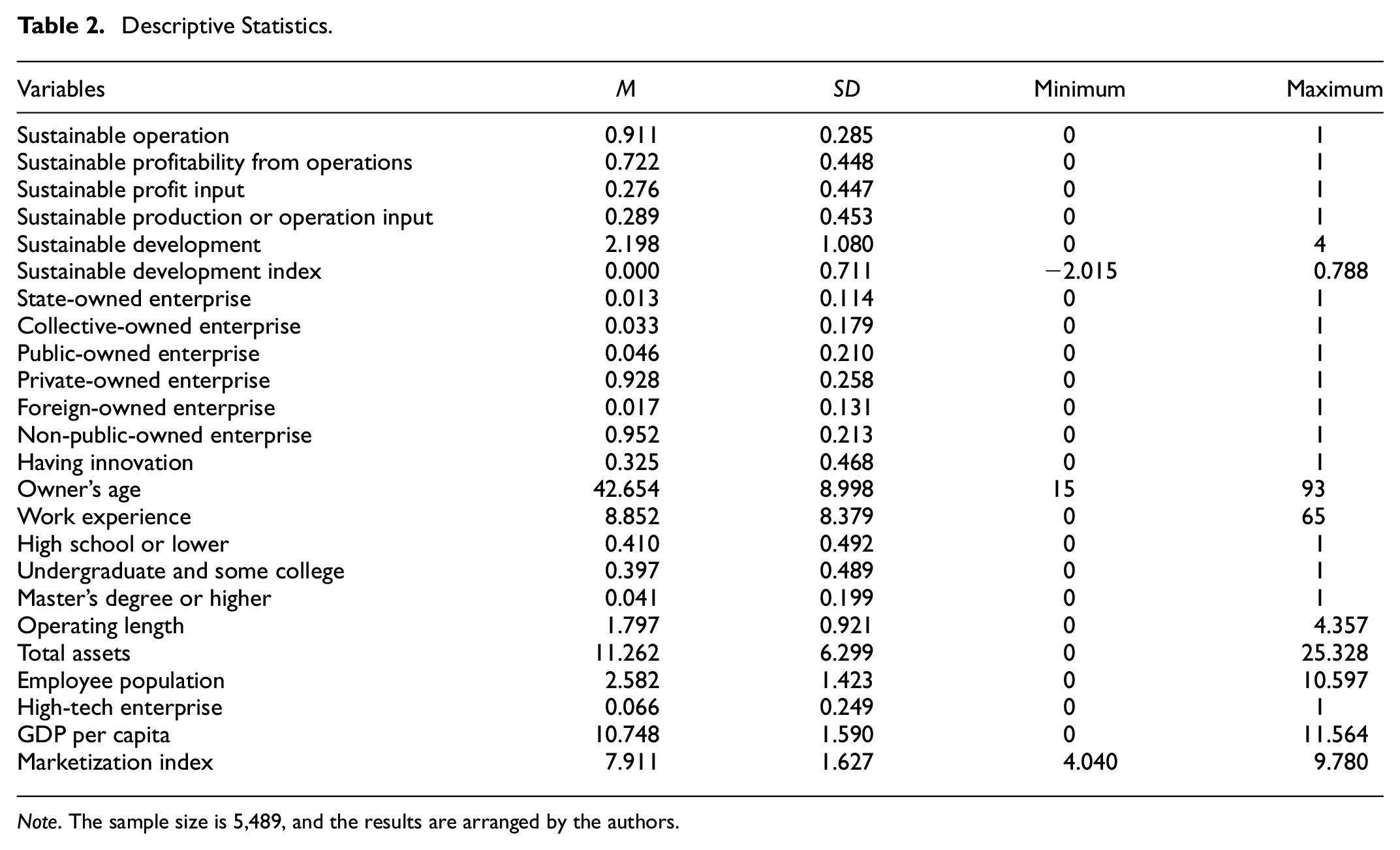

In Table 2, the result of the statistical description is displayed. The related variables of the sustainable development of MSEs are encoded as binary variables, where 0 stands for performing no activity and 1 otherwise. For the dependent variable of sustainable operation, more than 90% of the enterprises have been normally operated. The variable of sustainable profitability from operations with a mean value of 0.722 implies that more than 70% of the MSEs made profits in the year 2014. For the variables of sustainable profit input, and sustainable production or operation input, their mean values are 0.276 and 0.289, respectively, which indicates that more than a quarter of the MSEs have invested their profits in processes of production or operation. Moreover, the mean value of the variable of sustainable development is 2.198, which means that approximately 55% of MSEs perform well in sustainable development. For the independent variable of innovation, the mean value is 0.325 with a standard deviation of 0.468. Besides, the average value of age is 42.654, suggesting that most enterprise owners are middle-aged. In terms of work experience, the mean value is 8.852, indicating that most enterprise owners’ management experience is less than 9 years.

Descriptive Statistics.

Note. The sample size is 5,489, and the results are arranged by the authors.

Table 3 displays the results of the frequency and percentage of categorical and dummy variables. The proportion of state-owned and collective-owned enterprises is 1.3% and 3.3%, respectively. Together with state-owned enterprises, it accounts for 4.6% of the total number of public-owned enterprises. The proportion of private-owned and foreign-owned enterprises is 92.8% and1.8%, respectively. In terms of educational background, less than 45.0% of the main owners educate undergraduate and some college as the highest degree. Besides, high-tech companies only account for 6.7%, suggesting a small proportion of the total sample.

Frequency and Percentage of Categorical and Dummy Variables.

Empirical Results

Results of the Impacts of Ownership on Sustainable Development of MSEs

Table 4 presents the regression results of the ownership and innovation on MSEs’ sustainable development. Column (1) only incorporates the control variables. In Columns (2) to (7), the ownership-related variables are added. To eliminate the estimation bias caused by differences in provinces and enterprise organization forms, their dummies are controlled in all estimates. More specifically, the provinces in the reference group are Guizhou, Yunnan, and Gansu, all of which have the lowest GDP per capita. Additionally, clustered and robust standard errors at the industry level are employed to produce more accurate estimates.

Results of Regressions of the Ownership and Innovation on MSEs’ Sustainable Development.

Note. In this study, the reference education category is a high school or lower, and the reference province group incorporates Guizhou, Yunnan, and Gansu. Besides, ***, **, and * stand for the significant level of 1%, 5%, and 10%, respectively.

In Column (1), most coefficients of the control variables are as expected. The coefficient for the enterprise owner’s age is statistically negative, indicating that young owners are more conducive to the sustainable development of MSEs. Besides, the enterprise owner’s educational background is significantly negative to the sustainable development of MSEs. The total assets and employee size positively contribute to the sustainable development of MSEs. The results are aligned with Skrynkovskyy et al. (2018). Besides, industry and business scope affect enterprises’ sustainable development as well, as is statistically highly significant, high-tech enterprises are more likely to develop sustainably.

In Column (3), the state ownership is significantly negative to the sustainable development of MSEs, and so does the collective-owned enterprises in Column (4), although its coefficient is not statistically significant. Thus, the results are partly consistent with H1. The results are consistent with the investigation of Kubo and Phan (2019), in which state ownership negatively contributes to corporate performance. To further investigate the nexus between public ownership and the sustainable development of MSEs, Column (7) exhibits the estimation results. The result suggests that enterprises owned by the public sector are less likely to develop sustainably. In Column (5), it is evident that private ownership positively enhances the sustainable development of MSEs. Besides, Column (6) reports the foreign-owned enterprises’ significantly negative impact on MSEs’ sustainable development. Therefore, the result also provides strong evidence that the participation of foreign capital in the production and operation of MSEs cannot promote them to develop sustainably. Thus, the result of foreign ownership is not identical to H2. Compared with the prior study conducted by Rustam et al. (2019), they argued that foreign ownership enables enterprises to achieve sustainable development. The difference in results may be explained by differences in the selected samples, which were from Pakistan. In Column (8), the result shows that non-public ownership is vital to the sustainable development of MSEs, as the coefficient is significantly positive.

Furthermore, this study also constructs a sustainable development index to replace the prior dependent variable of sustainable development and performs corresponding estimations of the above-mentioned models. Table 5 exhibits the regression results of the ownership and innovation on MSEs’ sustainable development index. In Column (1), the results of most coefficients specific to control variables are as expected. Similarly, the variable of state ownership is statistically negative to the variable of sustainable development index at the significance of 1%. Nevertheless, compared with the result in Table 4, the ownership of collective-owned enterprises significantly and negatively contributes to MSEs’ sustainable development. In Table 4, although the corresponding coefficient is negative, it is insignificant. Therefore, together these results in Tables 4 and 5 provide important and strong evidence to support H1. In Columns (5) and (6), the results suggest that private ownership is conducive for MSEs to develop sustainably, while foreign ownership negatively contributes to the sustainable development of MSEs. Thus, only the estimates of private ownership are consistent with H2, and those estimates of foreign ownership do not support H2 as well. Concerning the public and non-public ownership, the results remain unchanged. To be more specific, in Column (7), the coefficient of the ownership of public-owned enterprises equals −0.142 at a significance of 1%. Besides, in Column (8), the coefficient specific to the ownership of non-public-owned enterprises is statistically positive at a significance of 1%. Although non-public capital enables MSEs to promote their sustainable development, the introduction of foreign capital may still mean a negative impact.

Results of Regressions of the Ownership, Innovation, and MSEs’ Sustainable Development Index.

Note. The reference education category is a high school or lower, and the reference province group incorporates Guizhou, Yunnan, and Gansu. Besides, ***, ** and * stand for the significant level of 1%, 5%, and 10%, respectively.

Results of the Impacts of the Innovation on Sustainable Development of MSEs

Table 4 also reports the results of the impacts of the innovation on MSEs’ sustainable development. In Table 4, the dependent variable is the sustainable development of MSEs. According to the estimated results in Column (2), the coefficient of the variable specific to having innovation is statistically positive at a significance of 1%. Moreover, after entering ownership-related variables, the positive impact of having innovation on MSEs’ sustainable development remains unchanged [see Columns (3) to (8)]. Thus, the results are consistent with H3, which implies that MSEs that engage in innovation to ameliorate related products or technology are more likely to develop sustainably. For MSEs, innovation has played a crucial role in urging corporate sustainable development and maintaining a competitive advantage in the future (Scherer & Voegtlin, 2020)

In Table 5, the impacts of the innovation on the sustainable development of MSEs are presented in detail as well. Meanwhile, the dependent variable is replaced by an index of MSEs’ sustainable development. In Column (2), the coefficient specific to the variable of having innovation is statistically positive at a significance of 1%. Moreover, in Columns (3) to (8), all coefficients related to the variables of having innovation are positive and significant. The results are still as hypothesized in H3. Furthermore, together with these results presented in Tables 4 and 5, the coefficients specific to the variable of having innovation suggest that regardless of the various ownership-related variables added, the coefficients’ size of MSEs innovation-related variable remains partially unchanged, and the significance is still at the 1% level. The results indicate that innovation in products and technology has a positive effect on the sustainable development of MSEs. Thus, it provides robust evidence to support H3.

Robustness and Endogeneity Check

To produce more robust and accurate estimates, this study conducts an adequate robustness check in detail. First, ordered logistic regression is applied to re-estimate the impacts of the ownership and innovation on MSEs’ sustainable development since the dependent variable used to measure the sustainable development level of MSEs is a discontinuous categorical variable. Second, the approach of WLS estimation is utilized to verify the robustness of the estimation results when a discontinuous categorical dependent variable is replaced by a continuous variable constructed as the sustainable development index. To be more specific, public and non-public ownerships as well as having innovation are considered as the main independent variables in the estimates of robustness check.

The results of the robustness check are displayed in Columns (1) to (4) of Table 6. Columns (1) and (2) report the regression results by replacing ordered probit regression with ordered logistic regression. The results concerning the coefficient of the ownership specific to public-owned enterprises and that of non-public-owned enterprises are consistent with the previous estimates, incorporating the signs and significance. Moreover, the estimates also suggest a consistent role of having innovation in promoting MSEs’ sustainable development. In Columns (3) and (4), WLS estimation is performed. The results still indicate negative associations between public ownership and the sustainable development of MSEs, but positive nexus for non-public ownership. Simultaneously, having innovation positively contributes to MSEs developing sustainably. Thus, together these results in Columns (1) to (4) provide robust evidence to support H3 as well.

Robustness and Endogeneity Check.

Note.The reference education category is a high school or lower, and the reference province group incorporates Guizhou, Yunnan, and Gansu. Besides, ***, ** and * stand for the significant level of 1%, 5%, and 10%, respectively. In Columns (3) and (4), WLS regression is utilized, and in Columns (7) and (8), OLS regression is used, and the statistics of Adjusted R2 and constant items are reported. Also, in Columns (1) and (2), ordered logistic regression is performed, and in Columns (5) and (6), ordered probit regression is conducted, so only the statistics of Pseudo R2 are reported. Besides, in Columns (1), (2), (5), and (6), the dependent variable is the sustainable development of MSEs, and in Columns (3), (4), (7), and (8), the dependent variable is sustainable development index of MSEs.

In this study, the ownership is considered to be an exogenous factor for the sustainable development of MSEs, since it can be determined when MSEs were established. However, to eliminate the likely estimation bias that might arise from endogeneity, this study also recognizes the endogenous problem that may occur in the regression models mentioned above because these coefficients cannot determine the causal relationships between having innovation and MSEs’ sustainable development. For instance, some enterprises may increase investments in product or technology innovation, because the implementation of the sustainable development strategy makes their profits increase enough to cover the cost of innovation. Therefore, it is necessary to carefully deal with the potential endogeneity of innovation in products or technology in this study. Accordingly, whether an enterprise recruits new professional technicians is applied as an IV since the variable is related to the innovation in products or technology but nearly exogenous to MSEs’ sustainable development in the future. Specifically, the IV is measured as the response to the question “In the past year, namely from June 2014 to June 2015, whether your enterprise newly recruited professional technicians?” And the variable (the recruitment of new professional technicians) is coded as a binary one, with 1 referring to employing technical staff and 0 otherwise. Besides, this study utilizes the approach of 2SLS to eliminate the disturbance of the endogenous problem on the estimated results. This study first conducts a regression analysis of having innovation on the variable specific to the recruitment of new professional technicians. In light of the regression results of the first stage, all coefficients of the IV are positively significant. Also, the F statistics specific to the independent variable of having innovation is 29.610, which is much larger than the critical value. The result shows that the disturbance from the weak IV may be negligible.

Accordingly, Columns (5) to (8) in Table 6 present the results of the endogeneity check in the second stage of 2SLS estimation, respectively. In Columns (5) and (6), MSEs’ sustainable development works as the dependent variable, which has been replaced with the index of MSEs’ sustainable development in Columns (7) and (8). Similarly, ordered probit regression is conducted in Columns (5) and (6), while in Columns (7) and (8), OLS regression is performed. The results of the 2SLS estimation indicate that the estimates of the coefficients are all unchanged, incorporating the signs and the levels of significance concerning the related variables of the ownership and having innovation. In detail, the results suggest that public ownership is positive to MSEs’ sustainable development, while non-public ownership has negative effects on MSEs developing sustainably. Thus, after controlling endogeneity, the results remain unchanged. Moreover, the coefficients of having innovation in Columns (5) to (8) are greater than those in Columns (1) to (4). It implies that the endogenous problem indeed matters, and the IV is vital to eliminate the disturbance of endogeneity in estimation. Therefore, the estimation results concerning MSEs’ innovation are as expected in H3.

Test for Heterogeneity

This study also notes that the effects of ownership and innovation may depend on the regional economic development and marketization level. Therefore, this study verifies further the heterogeneous effects of ownership and innovation on the sustainable development of MSEs. First, this study divides the sample into two sub-samples in terms of levels of economic development, namely developed regions and developing regions. More specifically, a province is classified as developed if its GDP per capita is greater than the average, otherwise, it is developing. Second, this study further considers regional marketization level as a possible source of heterogeneity. Similarly, high and low marketization are demarcated by the average value of the marketization index.

Table 7 exhibits the results of the heterogeneity test to levels of economic development. In Columns (1) to (4), the dependent variable is the sustainable development of MSEs, and that in Columns (5) to (8) is MSEs’ sustainable development index. In Columns (1) to (4), as public ownership is negatively associated with MSEs’ sustainable development, with the highly significant coefficients [except for that in Column (2)], the coefficients of non-public-owned enterprises are still statistically positive. However, the coefficients of non-public ownership are insignificant in developing provinces. Hence, the results keep unchanged. Meanwhile, the coefficient for public ownership in Column (3) and that for non-public ownership in Column (4) are statistically insignificant with unchanged signs. Moreover, in Columns (5) to (8), after the former dependent variable is replaced by MSEs’ sustainable development index, the coefficients for public ownership in Columns (5) and (7) are statistically negative at a significance of 5%, while the coefficients for non-public ownership in Columns (6) and (8) are statistically positive. Regardless of the heterogeneity of developed or developing provinces, the estimated results are unchanged. Besides, all the coefficients of the variable of having innovation are statistically positive at a significance of 1%, which is as hypothesized in H3 as well.

Heterogeneity Test With Respect to Levels of Economic Development.

Note. The reference education category is a high school or lower, and the reference province group incorporates Guizhou, Yunnan, and Gansu. Besides, ***, ** and * stand for the significant level of 1%, 5%, and 10%, respectively. In Columns (1) to (4), ordered probit regression is used, so Pseudo R2 is reported. In Columns (5) to (8), OLS regression is performed, so Adjusted R2 is reported. In Columns (1) to (4), the dependent variable is the sustainable development of MSEs, and that in Columns (5) to (8) is the sustainable development index of MSEs.

Table 8 displays the results of the heterogeneity test concerning levels of marketization. Similarly, in Columns (1) to (4), this study performs ordered probit regression with the dependent variable of the sustainable development of MSEs, and in Columns (5) to (8), the estimation method and dependent variable are replaced by OLS and MSEs’ sustainable development index, respectively. In Columns (3), (5), and (7), public ownership is negative to MSEs’ sustainable development, while that of non-public ownership is positive. However, in provinces with a high level of marketization [see Columns (1) and (2)], the public ownership is insignificantly negative to the sustainable development of MSEs, as well as the non-public ownership is insignificantly positive. A similar situation occurs in Columns (4), (6), and (8). All three coefficients of the non-public ownership are statistically positive and the significance of them is 5% or higher. Moreover, the results also indicate a positive association between the innovation and MSEs’ sustainable development regardless of the levels of marketization, estimation approaches, and dependent variables. Therefore, the disparity of the regional marketization level does not change the results, especially for provinces with a high level of marketization.

Heterogeneity Test With Respect to Levels of Marketization.

Note. The reference education category is a high school or lower, and the reference province group incorporates Guizhou, Yunnan, and Gansu. Besides, ***, ** and * stand for the significant level of 1%, 5%, and 10%, respectively. In Columns (1) to (4), ordered probit regression is used, so Pseudo R2 is reported. In Columns (5) to (8), OLS regression is performed, so Adjusted R2 is reported. In Columns (1) to (4), the dependent variable is the sustainable development of MSEs, and that in Columns (5) to (8) is the sustainable development index of MSEs.

Conclusions and Implications

MSEs are an important source of power to promote social and economic development, and innovation plays an essential role in enhancing an enterprise’s sustainable growth in the long term. This study aims to examine the effects of ownership and innovation on the sustainable development of MSEs. Using the dataset from 2015 CMSES, this study divides the ownership of MSEs into state ownership, collective ownership, private ownership, and foreign ownership. Simultaneously, the sustainable development of MSEs is measured by four sets of variables, sustainable operation, sustainable profitability from operations, sustainable profit input, and sustainable production or operation input. This study constructs a comprehensive variable, which is defined as a sum of the values of the four binary variables specific to the four aspects above, respectively. Moreover, to measure the MSEs’ sustainable development more appropriately, this study also utilizes the method of Principal Component Analysis to construct a sustainable development index by using the above variables that reflect the four aspects of sustainable development of MSEs. To produce more robust and accurate estimates, this study performs an adequate robustness check by replacing the approach of ordered probit regression with estimation methods of ordered logistic regression and WLS regression. Besides, the methods of IV and 2SLS are employed to eliminate estimation bias from endogeneity. Concerning the levels of economic development and marketization, the heterogeneous problems on estimates are comprehensively discussed.

Results indicate negative associations between the ownership of state-owned enterprises as well as collective-owned enterprises and MSEs’ sustainable development. Meanwhile, the results also suggest that public ownership is not conducive to MSEs’ sustainable development. Concerning the ownership of non-public-owned enterprises, private ownership enables MSEs to develop sustainably, while foreign ownership negatively contributes to MSEs’ sustainable development. Besides, the results indicate that innovation positively contributes to the sustainable development of MSEs.

The conclusions of this study pinpoint rich and crucial policy implications. First, measures should be taken to promote the mixed-ownership reform of public-owned MSEs, and further accelerate the sustainable development of MSEs. The results show that the ownership of state-owned and collective-owned MSEs is negative to their sustainable development, while private ownership positively contributes to the MSEs’ sustainable development. Second, policymakers should formulate specific policies to promote MSEs’ innovation. The results suggest that MSEs involving innovation in products or technology are more likely to develop sustainably. Hence, policymakers should encourage MSEs to conduct innovation activities through the measures of tax deduction or exemption for innovation. Third, urge the establishment of a development environment for private-owned MSEs. This study concludes that private ownership is positively associated with MSEs’ sustainable development, while foreign ownership has a negative effect. Thus, policymakers are advocated to formulate specific policies to build a good development environment for private MSEs, which will also be conducive to the overall development of the economy.

Limitations of this study also should be acknowledged, which is conducive to highlighting the directions of future research. First, this study employs cross-sectional data to examine the effects of ownership and innovation on MSEs’ sustainable development. Although the ownership is exogenous to the sustainable development of MSEs, there may still be causality between the innovation and MSEs’ sustainable development. In this study, only cross-sectional data is available, which makes it more difficult to investigate the bilateral causality. Nevertheless, there is currently no panel survey related to the topic of ownership, innovation, and the sustainable development of MSEs. To eliminate the estimation disturbance caused by endogeneity, this study utilizes approaches of IV and 2SLS estimation. To verify and produce appropriate results, this study has also offered a comprehensive robustness check as well as the heterogeneity test. The second limitation of this study is that only ordered probit regression is employed during the empirical analysis. It is difficult to capture the dynamic changes concerning the effects of ownership and innovation on MSEs’ sustainable development. For further study, more sophisticated methods, such as panel-ordered probit regression, can be employed when panel surveys under the topic in this study are available. The third limitation of this study is that only China’s samples of MSEs are selected. Since different countries have various development statuses, which may have a certain impact on the research conclusions. Therefore, in future studies, more samples from other developing countries can be incorporated to produce more accurate results. Additionally, more updated surveys need to be conducted to help offer timely policy recommendations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the General Research Fund of The Academy of China Open Economy Studies at the University of International Business and Economics (Grant No. 2022GK10), Research Project of the Center of Beijing Xi Jinping Thought of Socialism with Chinese Characteristics in the New Era (Grant No. 19LLLJB037), and Project for Young Excellent Talents at the University of International Business and Economics (Grant No. 18YQ07).