Abstract

This study investigates venture capital (VC) reputation impact on the pre-IPO performance of the entrepreneurial firms backed by three kinds of VCs. This study employs backward stepwise regression models following prior theoretical frameworks to examine the research question. Based on a database of the top 50 VC firms ranked during 2016 to 2020 and their portfolio firms. This study shows some contingent contribution to pre-IPO firm performance. Firstly, the reputation of the Chinese government-owned VCs is negatively associated with their portfolio firm performance. Still, there is a positive relationship between foreign and local private VCs. Secondly, entrepreneurial firm performance is significantly associated with industry policy and entrepreneur’s performance than VC reputation. This study has practical implications for entrepreneurs and limited partners regarding their corporation relationships with the Chinese VCs.

Introduction

Studies across countries demonstrate that VC reputation may contribute to the post-IPO performance of portfolio firms. Baker and Gompers (2003) and Nahata (2008) reveal a positive relation between VC reputation and post-IPO performance of portfolio companies because VC reputation may contribute to the market value of listed firms (Lee et al., 2011; Lin et al., 2017). Others support these findings (Barg et al., 2021; Krishnan et al., 2011).

However, research examining the relation between VC reputation and pre-IPO performance is few and far between, particularly from the Chinese evidence. These theories, mainly based on developed markets, cannot account for the Chinese context’s question. For instance, a new Sci-Tech Innovation Board (STAR Market), as a Chinese equivalent market to Nasdaq, was officially launched on the Shanghai Stock Exchange on July 22, 2019 (http://star.sse.com.cn/en/). It facilitates VC exist from their ventures. Noticeably, most of these VCs investing in IPO firms are emerging and unknown. This phenomenon attracts our study.

In addition, little literature addresses VC reputation based on different types of VCs because investment performance varies from other types of VCs (Bertoni et al., 2013). There are three types of VCs in China: foreign, government-owned, and local private VCs. Whether the portfolio firms backed by the three VCs perform differently is not investigated yet, which calls for this study.

This study aims to examine the pre-IPO performance as a dependent variable affected by VC reputation. Based on an analysis framework from Lin et al. (2017), this issue is discussed using the following steps: (1) Collecting a dataset of the top 50 VCs from league table rankings each year from 2016 to 2020 to measure VC reputation as a dependent variable, in line with Nahata (2008); (2) Employing backward stepwise regression models to test the extent to which VC reputation impacts on pre-IPO performance as an independent variable, along with other control variables.

The significance of this study is to examine the pre-IPO performance of entrepreneurial firms backed by three kinds of VCs (foreign, private, and government-owned), which is different from prior research. Due to the unique context of the VC market, VC as an emerging industry in China was introduced from overseas in the 2000s, so foreign VCs are experienced and more professional in investment than others (Park & LiPuma, 2020). However, because of the Chinese government-preferred business environment, the Chinese government-owned VCs, as policy funds, are the most favorable for local entrepreneurial firms because they have more access to business opportunities than others. Thus, entrepreneurs would like to have close relationships with the government. On this basis, reputation becomes less influential, and government-owned VCs may be favorable for entrepreneurial firms.

Although existing literature examines VC reputation impact on post-IPO market performance and suggests that VC reputation may contribute to their portfolio market performance (Barg et al., 2021; Woo, 2020), few studies shed light on pre-IPO operating performance. It is vital because VCs invest in pre-IPO firms and drive them to proliferate and consequently exist from their portfolios when they go public. Particularly in China, most VCs view an IPO as a saturation point for their returns. They are reluctant to hold their shares any longer because Chinese IPOs have the most profitable first-day returns in the global stock market (Que & Zhang, 2019). In addition, outstanding pre-IPO performance may increase post-IPO market value and draw new prospective investors, from which VCs may receive more returns (Wongsunwai, 2013). This study is expected to bridge this gap to investigate the connection between VC reputation and pre-IPO performance of their portfolios.

Therefore, this study reveals some different findings from prior research. VC reputation contributes less to firm performance when government-owned VCs are involved, and athletic performance is mainly determined by government industry orientation and strong founder performance. Secondly, despite the underperformance of their portfolio firms, the government-owned VCs have the highest reputation on average for entrepreneurs, followed by foreign and then local private VCs. However, the entrepreneurial firms backed by foreign VCs outperform the Chinese government and private VCs.

This paper is organized as follows: Section 2 provides a literature review and hypotheses. Section 3 outlines data. Section 4 discusses the analysis framework. Section 5 analyzes and presents results. Section 6 concludes the paper.

Literature Review and Hypotheses

A wide range of research documents that VC reputation may contribute to the post-IPO performance of their portfolio firms (Barg et al., 2021; Lin et al., 2017; Woo, 2020). Barg et al. (2021) suggest that firm valuation multiples are higher when more experienced investors are involved. Woo (2020) indicates that foreign VC is positively associated with the performance of portfolio firms that a foreign VC backs. Lin et al. (2017) suggest that VC reputation may significantly increase the market value of IPO firms backed by VCs. An extensive body of research attributes this blessing effect to resource inflow provided by VCs (Dutta & Folta, 2016; Park & LiPuma, 2020; Zhang, 2015).

However, research on VC reputation impact on the pre-IPO performance of their portfolio firms is minimal. There should be a connection between them because the vast majority of venture capitalists push their portfolios’ firms to go public prematurely to establish their reputations for the next round of fund-raising (Gompers, 1996). Meanwhile, as an IPO is the most profitable exit strategy relative to other exit options (Black & Gilson, 1998), VCs intend to establish their reputation through more successful IPOs.

In addition, the IPO approval system in the Chinese stock market is different from that in developed markets, where Stock exchanges approve IPOs according to some basic listing standards. IPOs in China have to satisfy higher listing standards on financial indicators and be approved by the China Securities Regulatory Commission (CSRC) to go public (Chen et al., 2016). According to the listing requirements on the official website (http://english.sse.com.cn/start/listing/overview/), the CSRC has rigorous IPO rules for issuers in terms of firm age (AGE), net profit (NPT), growth rate (NPTgr), cash flow (CFL), and net assets (NAT). Therefore, pre-IPO firms in China have strong incentives to grow fast to show their good pre-IPO performance to meet the listing requirements.

Venture capital plays an essential role in their firm portfolio growth; it provides financial support and managerial advice (Bottazzi et al., 2008). Research shows that VC-backed firms have significantly higher employment growth potentials (Bertoni et al., 2011) and higher profitability (Guo & Jiang, 2013) than non-VC-backed firms. As such, reputable VCs have more resources to improve and foster the pre-IPO operating performance of their portfolio firms to meet IPO requirements. Accordingly, a hypothesis is proposed.

Hypothesis 1a: VC reputation has significant contributions to pre-IPO firm performance in China.

On the other hand, the reality is far more complicated for the non-IPO firms backed by VCs. Firstly, portfolio firm performance is affected by the relationship between VCs and entrepreneurs. Due to conflicting interests, there are frequent conflicts between the venture capitalists and the entrepreneurial teams, which may potentially generate side effects on firm performance (Collewaert & Fassin, 2013; Higashide & Birley, 2002; Zacharakis et al., 2010), particularly for non-IPO portfolio firms. In addition, these kinds of conflicts are pretty often for non-listed firms. Hsu (2004) discusses further that fund-raising motivations drive VCs to shorten their ongoing incubation periods and drive portfolio firms to proliferate to meet listing standards as soon. As a result, these conflicting interests may lead to potential conflicts, leading to the firm’s underperformance.

Secondly, portfolio firm performance is associated with the motivations of both VCs and entrepreneurs. Reputable VCs are more powerful and have more external resources than others, but these characteristics can create an over-dependence on outside help for some opportunistic entrepreneurs. Resource over-dependence causes the curse effect (Brunnschweiler & Bulte, 2008; Gylfason & Zoega, 2010). Chinese research shows a situation that induces firms to satisfy present rather than long-term benefits and offers them an incentive to give up internal resources, thus hindering firm performance (Zhu & Li, 2011). As Seet et al. (2020) suggested, the internal value of entrepreneurial firms is positively related to entrepreneurial attitude. Indian evidence from Katti and Raithatha (2020) reveal a negative effect when opportunistic investors have a favorable exit option from their portfolios. Thus, possibly more optimistic entrepreneurs and VC investors are careless about firm performance in developing countries like China and India.

Thirdly, firm performance depends on development stages (Seet et al., 2020); previous literature suggesting a positive relationship between VC reputation and strong performance mainly investigates post-IPO performance because VC reputation may contribute to the market value of listed firms (Lee et al., 2011; Lin et al., 2017; Nahata, 2008). Comparably, IPO firms are likely to have more consistent interests with VC investors than non-IPO firms. They manage to improve post-IPO firm performance to maximize their returns. Accordingly, pre-IPO firm performance is less associated with VC reputation than post-IPO firm’s.

Last but not least, each nation’s venture capital industry is partially shaped by its institutional context (Çetindamar, 2003). In the Chinese business context, the fast-growing economy accelerates start-ups. These young entrepreneurs lack business experience and entrepreneurship, leading to frequent conflicts between them and eventually leading to firm under-performance. Additionally, China has some unique institutional context in financial markets. Long and Zhang (2014) demonstrate that the Chinese IPO assessment mechanism is determined by its institutional factors. Because of the Chinese government-preferred business environment, entrepreneurs would like to have close relationships with the government; they prefer to cooperate with government-owned VCs to facilitate their IPOs in the future. Even though reputable foreign VCs have higher levels of international integration (Park & LiPuma, 2020), the Chinese firms that plan to go public in the local stock markets prefer to cooperate with government VCs. In this China-specific context, VC’s government background becomes more favorable for entrepreneurial firms regardless of their reputation. As discussed above, a hypothesis comes out as below:

Hypothesis 1b: VC reputation has no significant contributions to pre-IPO firm performance in China.

Pre-IPO performance determines IPO probabilities. The Chinese IPO applications are assessed by the China Securities Regulatory Commission (CSRC) based on IPO candidates’ pre-IPO performance. Although few studies demonstrate an association of VC reputation with pre-IPO performance, existing research reveals that VC reputation connects to post-IPO market performance. Research shows that VC reputation is positively related to the IPO probability of a VC-backed firm (Nahata, 2008). Subsequently, VC reputation has positive associations with post-IPO performance (Krishnan et al., 2011).

Based on this argument, it may be inferred that VC reputation has associations with pre-IPO performance because reputable VCs have access to invest in firms with better pre-IPO performance (Sorensen, 2007), which facilitates IPOs, and eventually increases post-IPO market value for profitable returns. For instance, Miller et al. (2013) document that high profitability means high returns. Chakravarthy (1986) documents that good financial performance satisfies investors. Outstanding historical profitability and growth rates, along with future expectations, minimize investment risks and maximize returns (Lingaraja et al., 2015). Once this kind of over-performance information is revealed to a stock market, it drives listed firms’ stock prices upward, increasing their market value accordingly (Tian, 2012).

Gompers and Lerner (1999) suggest that IPOs are the most successful exit options and fetch the highest returns to the VCs. Venture capitalists aim to invest in start-ups with good pre-IPO performance to achieve IPOs for their venture exit. On this basis, reputable VCs than the non-reputable have more access to outside resources and add more values to support future growth and achieve IPOs. Meanwhile, Sorensen (2007) demonstrates that reputable VCs have the experience to select firms with superior pre-IPO performance and add incremental value to their portfolios. Thus, to preserve and enhance their reputation, reputable VCs, to a certain extent, prefer to invest in companies with outstanding pre-IPO performance for future IPOs, because taking portfolio firms public is critical for VCs’ next round of fund-raising and their reputation promotion (Gompers, 1996). Therefore, a hypothesis is proposed below:

Hypothesis 2a: VC reputation is associated with pre-IPO performance and facilitates IPOs consequently.

Each nation’s venture capital industry is partially shaped by its institutional context (Çetindamar, 2003), and China has some unique institutional context in financial markets. Long and Zhang (2014) demonstrate that the Chinese IPO examination mechanism is associated with its institutional factors. In this Chinese institutional context, post-IPO operating performance decreases (Long et al., 2021), and IPO contributions to firm performance varies (Gao et al., 2021). Moreover, Chinese IPOs have the most profitable first-day returns in the global stock market, and Chinese VCs view an IPO as a saturation point for their returns, such that they are reluctant to hold their shares any longer (Que & Zhang, 2019). There might be a different situation in the Chinese context for three reasons.

First, as a relationship-based market, Chinese VCs manage to address many kinds of relationships (so-called Guan Xi in Chinese Pinyin) to expand the pre-IPO performance of their portfolio firms. VCs have strong motivations to manipulate the firm’s accounting for high growth records (Gompers & Lerner, 1999). Regardless of their reputations, some opportunistic VCs even conduct fraud to meet the listing standards as soon (Chen et al., 2016; Szwajkowski, 1985).

Second, the existing studies demonstrate that macro factors significantly impact the exit options of venture capital (Cumming et al., 2010; Espenlaub et al., 2015; Nahata et al., 2014). Yang (2018) suggests that macro factors, such as legal rights and GDP growth, can potentially facilitate successful exits in the Chinese stock market. Therefore, the Chinese VCs have successful exits via IPOs, attributed to China’s fast-growing GDP rather than the VCs’ reputation.

Third, a very Chinese characteristic is government-oriented policies for entrepreneurs. It is the so-called “Mass Entrepreneurship and Innovation,” saying the government encourages the Chinese adults to run a business as an entrepreneur or innovators. Meanwhile, various policies and numerous funds are provided each year to support their start-up business. Consequently, firm performance is even more attributable to policy and capital supports from local governments. Que and Zhang (2019) show that VC-backed firms have a good performance on these factors. Accordingly, the second hypothesis is proposed below:

Hypothesis 2b: VC reputation is not related to the probability of IPOs, and the successful IPOs backed by VCs are attributed to external factors.

Data

Our sample includes two groups of databases: VC reputation data and firm performance-specific data. The data on VC reputation were sourced from league table rankings by Zero2IPO (www.zero2ipo.com.cn), the most well-known PE/VC data provider in China, and its database has been used by prior research (Lin et al., 2017; Que & Zhang, 2019). This database institution has released various league table rankings on VC reputation since 2009. We sampled the top 50 VC firms ranked from 2016 to 2020 and 310 portfolio firms.

For the data regarding pre-IPO performance, we collected their IPO prospectuses from the China Securities Regulatory Commission (www.csrc.cn), covering a variety of firm performance-related data in the last 3 years before their IPOs. All firm performance data, including healthy age, net profit, growth rate, cash flow, and net assets, were collected from the IPO prospectuses.

Variables and Model Development

In terms of the theoretical grounds of this study, reputable VCs than the non-reputable have more access to invest in the firms with outstanding pre-IPO performance and then add incremental value to them for potential IPOs (Sorensen, 2007). IPO probabilities are significantly associated with the determinants of pre-IPO performance because pre-IPO financial factors influence IPO success (Long, 2014). More portfolio firms go public; more reputation is promoted for VCs (Gompers, 1996) while establishing the reputation is critical for the next round of fundraising. Therefore, the pre-IPO performance of portfolio firms directly connects to their IPO success, consequently effects VC reputation.

For a reputable VC-backed firm, its pre-IPO performance (P) is mainly determined by VC reputation, firm-specific indicators, and macro factors (Espenlaub et al., 2015; Nahata et al., 2014), which are functionally denoted as

VC reputation as an independent variable is assessed through the Top50 league table rankings during 2016 to 2020. Using a rolling window facilitates capturing the often fluctuations in a VC’s reputation over the course of the study. Previous research adopted this approach (Lee et al., 2011; Pollock et al., 2015). Following investment procedures, VC investment consists of four significant steps: fund-raising (FA), investment (INV), management or supervision (MA), and exit (IPO). VC performance in each stage is viewed as a reputation index by literature (Pollock et al., 2015), such as the total amount fundraised, the total amount of money invested, the total amount of funds under management, and the total amount of cash returned from IPOs. For instance, Gompers and Lerner (1999) argue capital under management is a proxy for VC reputation; Lee and Wahal (2004) discuss the amount of raised capital and the number of VC-backed IPOs as proxies.

Chen et al. (2016) show that IPO applicants in China have to meet listing standards of financial indicators and be approved by the China Securities Regulatory Commission (CSRC). The CSRC has rigorous IPO rules for issuers in terms of firm age (AGE), net profit (NPT), growth rate (NPTgr), cash flow (CFL), and net assets (NAT), which are nominated as control variables to account for firm performance.

Apart from these, some non-financial determinants have been proposed to measure pre-IPO firm performance, such as employee satisfaction (Harter et al., 2002), customer satisfaction (Fornell et al., 1996), and government connection (Waddock & Graves, 1997).

Industrial orientation (IND) has been viewed as a critical variable by several pieces of literature (Brush et al., 1999; McNamara et al., 2005), which argues that industry orientation is positively associated with firm performance. Schmalensee (1985) suggests that industry effects determine firm profitability; moreover, Gao et al. (2021) argue that IPO’s significance to operating performance varies on an industry-adjusted basis. IND is measured by its industrial price-earnings (PE) on average, given by the IPO assessment committee nominated by the CSRC.

The geographical location (LOC) has significant contributions to firm development around the world (Becker et al., 2011; Behrens, 2005; Krugman, 1991), particularly for the business success of entrepreneurial firms (Sridhar & Wan, 2010).

It is particularly essential in China. First, there is a trendy slang within the Chinese investment industry, “Investments never reach Shanhaiguan,” saying no investors would like to invest in the place of Shanhaiguan located in Northeast China. Second, firm development varies because of uneven economic strength across the Chinese provinces. Entrepreneurs prefer to explore their business opportunities in pretty developed cities, such as Shanghai, Beijing, Shenzhen, etc., where more business sources and capital are more achievable than others.

GDP is included due to two reasons. First, China has been the world’s second-largest economy as of 2010. IMF data shows that China still dominates a fast-growing economy by 2018. Second, macro factors significantly impact venture capital exit (Espenlaub et al., 2015; Nahata et al., 2014). Additionally, China’s macro factors may facilitate successful entries into the Chinese stock market (Yang, 2018). In practice, fast-growing GDP signals more capital inflow for investment, which drives more firms to go public. It is expected that GDP has a significant association with firm performance, even more than VC reputation. It is measured by the amount of GDP in the last year of pre-IPO.

Researchers have frequently studied founder performance (FDR). Each firm founder is an engine to push startups forward. Studies show that high individual expectations of wealth growth and social status are solid motivators for founders (Amit et al., 2001; Carter et al., 2003). Cragg and King (1989) document that a founder’s personal ambitions dominate small firms’ strategy and performance accounting for 35.5% of firm outcomes by CEOs. Thus, the individual performance of a firm founder impacts its outputs (Hambrick & Quigley, 2014).

Founder performance has been measured based on various factors, such as founder personality (Gow et al., 2016), CEO managerial attributes, and background (Benmelech & Frydman, 2015; Kaplan et al., 2012). We use a general approach, measuring founders’ performance based on media coverage.

This study conducts stepwise regression methods to investigate VC reputation impact on the pre-IPO performance of their portfolio firms, so a series of models, generated by removing the relatively non-significant variables, will detect the extent to which VC reputation and other proposed variables affect firm performance. Employing an analysis framework from Lin et al. (2017) and Krishnan et al. (2011), this study suggests a regression model below to test the contribution of VC reputation to their portfolio firm performance.

Where, VcRep represents VC reputation; lnNPT, lnCFL, and lnNAT measure firm net profit, cash flow, and net assets respectively; lnAGE means firm age; FDR stands by firm founder performance; lnIND, lnLOC, and lnGDP refer to the macro-related factors: industry sectors, geographical location, and gross domestic product respectively.

Analysis and Results

Descriptive Statistics

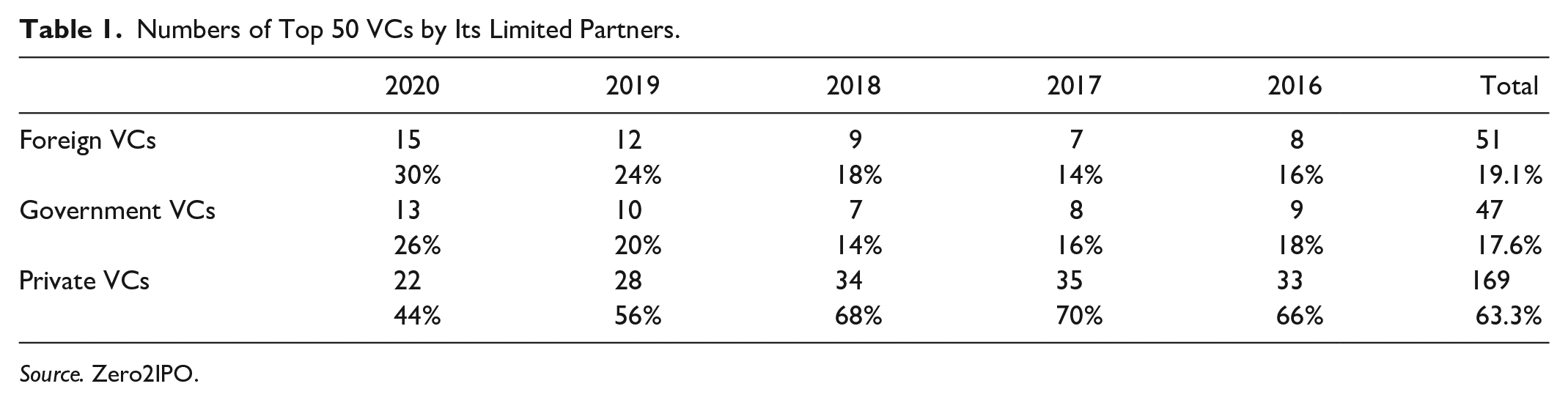

According to their limited partnership, VC firms are classified into foreign, local private, and Chinese government funds. As Table 1 shows, the local VCs dominate the top50 league table ranking in ranked firm numbers. It indicates that foreign VCs, as the former leaders, develop less, while local Chinese VCs are booming.

Numbers of Top 50 VCs by Its Limited Partners.

Source. Zero2IPO.

Table 2 indicates the reputation scores of VCs and their portfolio firm performance. Government-owned VCs (VCRep 12.82) have the highest reputation, but their portfolio firms have the lowest performance (P 4.955). This result is partially attributed to the Chinese institutional context that the government is more credible than others. On the contrary, the private VCs (VCRep 5.82) have the lowest reputation. Foreign VCs also have a high reputation (VCRep11.187) and the highest firm performance (5.620); as pioneer investors, they are well known by entrepreneurs.

Mean Report of Performance of VC-backed Firms.

Foreign VCs.

Government VCs.

Local VCs.

In terms of firm performance backed by the VCs, foreign VCs outperformed in lnNPT (18.467), lnNPTgr (0.794), lnCFL (19.200), and lnIND (5.509). Comparably, local private VCs performed well in lnINC (20.387) and lnNAT (20.11). However, government funds underperformed in these aspects.

There are three interesting Chinese-specific phenomena. The first is the vast differences with FDR. Foreign VC-backed firms outperformed (1.88), but private VC-backed firms performed poorly (−0.05). Understandably, foreign VCs are better at corporate governance than privates because they have just emerged in recent decades and lack experience in corporate governance.

The second issue concerns lnLOC: both foreign and private VCs have preferences in the locations of their portfolio firms, but the government, as a policy-oriented fund, does not (lnLOC 5.357) because it is responsible for some government-oriented industries and firms and has to offer funds to these firms regardless of their locations. Another piece of evidence to support this statement is the lowest lnIND (4.651) of government funds; due to some political policies, this kind of fund offers priority to some policy-oriented industries regardless of their returns.

The last one with lnAGE (2.239) shows that the private VCs have more motivations to push their portfolio firms to IPOs earlier. To raise funds for the next round, they are expected to exit soon. Relatively, both foreign and government-owned VCs have less pressure from their limited partners. These findings reject hypothesis 1a, but accept hypothesis 1b that VC reputation has no significant contributions to pre-IPO performance.

Model Analysis

We use the developed regression models to test VC reputation effects on firm performance. A stepwise regression method is utilized to investigate to what extent they are determined. The most significant factors affecting performance eventually appear.

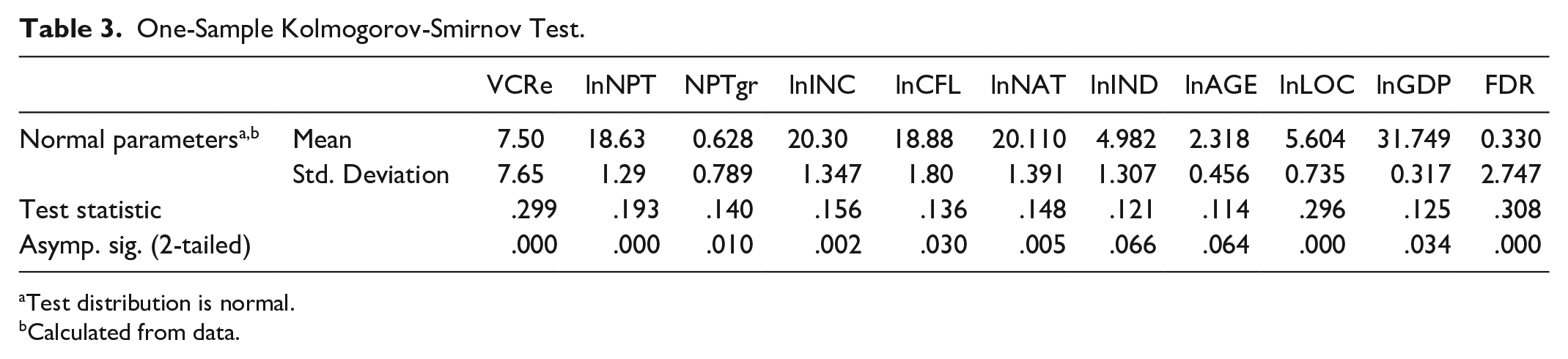

Before model analysis, we conducted a one-sample Kolmogorov-Smirnov test to examine the distribution. As Table 3 shows, the data for each variable is distributed on average, and the most sig. values are under .005, which means statistical significance.

One-Sample Kolmogorov-Smirnov Test.

Test distribution is normal.

Calculated from data.

Table 4 presents the developed models with R2 = .688 to .489, showing very significant goodness of fit. Therefore, the models are effective in testing the research question. The significance of each model is overwhelmingly 0, which means that the sampling data are representative and effective for this study.

Model Summary.

Table 5 shows each coefficient of the variables tested by 10 models. It gradually removes the less significant factors from the model and each coefficient changes accordingly. To do so, it presents the extent to which firm performance is determined by VC reputation and what exactly impacts firm performance.

Each Model Variable Coefficients.

Referring to the first model, all the variables are included. Initially, VCRep has a weak Sig. value at .446 but is not the weakest one. Its beta coefficient is .006, which means a minor impact on the dependent variable of firm performance. Both lnNPT and lnIND at a very significant level (Sig. <.005) have outstanding beta coefficients of 1.163 and 1.131, which means that firm net profit (NPT) and industry characteristics (IND) have the most significant contributions to firm performance. However, firm age (lnAGE) has less Sig. at .724 and is removed from model 2.

In the following models, the weakness of the VCRep Sig. value fluctuates between .446 in model 1 and .396 in model 7, and its beta coefficient stably remains at .006 to .007. Additionally, its t value remains under 1, which means its beta value has limitations in interpreting its contribution to the models.

This table presents these influential factors in descending order, which are organized as:

To sum up, firm performance is affected by the firm-specific variable of net profit and macro factors, such as industry orientation, but less so by VC reputation. Both variables FDR and NPTgr, have positive effects on firm performance. In contrast, the IPO-required variables, such as NAT, INC, and AGE, have less relationship with firm performance.

Further Robustness Checks

As Table 1 indicates, 15.7% and 16.6% of VC samples are from overseas investors and government-owned VCs, respectively, and the remaining 67.7% of the samples are from private VCs. These two data groups are not representative and even interfere with the results. Thus, we corroborate the results by removing these two types of data and using the same method to report the results in Table 6. Referring to Table 6, this group of R2 values is slightly lower than previous values, but it is still significant (Sig. value .000 < .005).

Model Summary.

According to model 1 in Table 7, VC reputation has weak Sig. .738 in model 1. In contrast, its beta values are negative (−.035 and −.030) in both models 1 and 2, and this factor is removed from model 3 and the following. This result shows no positive relationship between VC reputation and the performance of their portfolio firms.

Each Model Variable Coefficients.

As model 6 indicates, another different result is that GDP (Sig. .060, Beta 1.11) is the most significant factor contributing to firm performance rather than net profit, demonstrating that the macro-economy is more likely to determine micro-performance, such as athletic performance. This outcome could be understood as entrepreneurs having more access to external resources and no assistance from VCs. The only similar result to the one above is a unique positive relationship between industry orientation and firm performance.

These findings reject hypothesis 2a, but accept hypothesis 2b that VC reputation is not related to the probability of IPOs, and the successful IPOs backed by VCs are attributed to external factors, such as the fast-growing GDP, rather than VC reputation.

Conclusions

As the Chinese VC market has a different context from the developed ones, it has relationship-dominated and government-involved characteristics. This study investigates the pre-IPO performance of entrepreneurial firms backed by three VCs, including foreign VCs, government funds, and private partners. Sampling the top 50 VCs in the latest years and their portfolios, this study employs stepwise regression models to test the research question and presents four new findings.

The most significant finding is that VC reputation has little contribution to pre-IPO firm performance (see Table 5). There is a negative relationship between VC reputation and their portfolio firm’s performance (see Table 7). This finding is different from other studies investigating VC reputation influence on post-IPO performance (Baker & Gompers, 2003; Krishnan et al., 2011; Lin et al., 2017); they reveal strong positive relationships between VC reputation and post-IPO performance of their portfolio firms. We suppose that entrepreneurs have more access to fund-raising (such as IPOs) and other external resources; when the macro-economy performs well, they no longer rely on VCs; sometimes, reputable VCs have rigorous investment rules.

Although the Chinese private VCs have more successful IPOs, this success is attributed to external factors, such as China’s fast-growing economy, industrial policy supports from the government, and GDP performance (see model 6 in Table 7), because China’s GDP may increase the likelihood of successful exits in the Chinese stock market (Yang, 2018). This finding accounts for hypothesis 2b: VC reputation is not related to the probability of IPOs, and the successful IPOs backed by VCs are attributed to external factors.

Due to the unique Chinese context, the second finding has not been revealed by prior research. The Chinese government-owned VCs with the lowest firm performance obtain the highest reputation, followed by experienced foreign VCs with the highest firm performance (see Table 2). This finding responds to hypothesis 1b: VC reputation has no significant contributions to the pre-IPO performance of entrepreneurial firms in the Chinese context. It is consistent with the point of view that the venture capital industry of each nation is shaped in part by its institutional context (Çetindamar, 2003).

Third, firm performance is significantly determined by both net profit and industry orientation, followed by entrepreneurial performance and the growth potential of net profit (see model 8–10 in Table 6). This outcome lines up with prior literature. Previous research has revealed the same result (Brush et al., 1999), which documents that industry effects play a central role in determining profitability while firm factors are insignificant.

Last but not least, the founders of private VC-backed firms underperform more than those of firms backed by overseas VCs (see Table 2). This under-performance occurs partly because emerging private VCs, as sole opportunistic investors, have strong incentives to push their portfolio firms to go public and then exit quickly from these firms once they have an IPO, regardless of the performance of the firm founders, even some VCs encourage their portfolio firms to engage in accounting fraud for IPOs as earlier (Que & Zhang, 2019). The majority of the private VCs view an IPO as a saturation point for their returns, and they are reluctant to hold their shares longer.

These findings may account for the phenomenon mentioned initially. The first batch of entrepreneurial firms listed on the STAR market is backed by the Chinese emerging and unknown VC firms rather than experienced foreign VCs.

The results have some important practical implications for investors and stakeholders. First, the role of VCs’ reputation can’t be overvalued in China, as the entrepreneurs may have more external resources when the macro-economy goes well. Second, for the foreign investors, cooperating with the government-owned VCs is a better strategy to explore their business in the Chinese financial market. Third, the international VCs are suggested to understand that the Chinese private VCs have different investment philosophies on the portfolio firm performance.

The research limitations of this study are threefold. First, the sample data from foreign and government-owned VCs is minimal. Further research is suggested to investigate the performance differentials of the different firms backed by the foreign, government, and local VCs. Secondly, if data is available, further research is expected to investigate this question by sorts of portfolio firms that have different financing purposes, such as expanding client base, diversifying capital structure, and financing R&D. Lastly but not least, a further study is expected to examine this question through other methodologies, such as the two-sided matching method to investigate the interaction between VCs and entrepreneurs.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The author(s) received financial support from the Science Research Fund of University Scheme by Anhui Educational Bureau (grant number: KJ2021ZD0143). The Excellent Research Team Fund from Anhui International Studies University (grant number: Awkytd1908). The Ph.D Researcher Fund from Anhui International Studies University (grant number: Awbsjj2021001).