Abstract

Cross-border venture capitals (CBVCs) are increasingly prevailing in recent decades, inter alia in emerging markets like China. The venture capital (VC) firms investing outside their home countries are faced with foreignness which is broadly regarded as liability. The primary aim of this article is to contribute to our understanding how foreignness affects VC’s strategy when entering emerging markets, particularly with respect to the foreignness originated from cultural distance. The data consist of over 5,000 CBVC deals taking place in China mainland from 1988 to 2016. Our empirical study shows that, with foreignness growing, it turns from liability into advantage in the context of CBVCs. We find an inverse U-shape relationship between foreignness and syndication, with VC firm’s reputation as the moderator. Besides, foreign VC firms establish local subsidiary when faced with foreignness, which serves as alternative to syndication. The key contribution of this article is that foreignness turns from liability into advantage in emerging markets, which exerts a curvilinear impact on the entry strategy of VC firms. This study advances the knowledge of foreignness and VC strategy, and sheds new light on entrepreneurial activities in emerging markets.

Introduction

As start-ups and unicorns prevailing around the world, cross-border venture capital (CBVC) is a blooming phenomenon in the recent decades; its percentage over total venture capital (VC) deals grows from 15% in the early 1990s to around 40% by the 2008 crisis (Aizenman & Kendall, 2012). Such percentage in Asia was even once as high as 70% (Dai et al., 2012). Typically, VC firms tend to share geographical proximity with their (potential) portfolio start-ups to reduce transaction cost (H. Chen et al., 2010; Hochberg & Rauh, 2012). Then, why do VC firms finance portfolios overseas in spite of higher cost owing to the long distance?

To address this question, we need to look at the advantage of CBVC. CBVC is beneficial for both VC firms and start-ups. For VC firms, enhanced competition of domestic market drives more VC firms (inter alia those from advanced economies) to seek opportunities abroad, and portfolio diversification spreads risk across countries (Buchner et al., 2018). For the start-ups, finance and advisory services provided by the CBVCs are indispensable for not only its survival (Bertoni et al., 2015; Faria & Barbosa, 2014) but also its internationalization (Humphery-Jenner & Suchard, 2013). An interesting fact shown in prior research is that foreign VC firms outperform the local counterparts in terms of value-adding service (Bringmann et al., 2018). As a result, portfolio financed by CBVCs is more likely to succeed in Initial Public Offering (IPO) (H. Chen et al., 2010).

In spite of the above-mentioned advantages, liabilities are inevitable when investing as a foreigner, known as liability of foreignness (LOF). Information asymmetry remains salient in the context of CBVC (Wright & Robbie, 1998; Wuebker et al., 2015) and raises transaction cost (Portes & Rey, 2005). Moreover, such cost continues to rocket because of various social distinctions across countries. As suggested in prior literature, cultural distance is one of those distinctions that leads to LOF (Johanson & Vahlne, 2009; Vaara et al., 2012). The first question inspiring this article is whether foreignness brings CBVC firms only liability in emerging markets like China.

Syndication, which refers to two or more VC firms investing in the same portfolio in the same round, is widely used to mitigate LOF and we notice multinational syndication involving a bunch of VC firms (Jaaskelainen, 2012; Lockett & Wright, 2001). Figure 1 plots the development of VC (and CBVC) in China through the recent three decades. Line in Panel A represents the yearly ratio of syndication over total CBVC deals. Focused on the trend in this century, 1 the syndication ratio levels at around 40%. Notably, this ratio rises drastically since 2014 when the VC market in China became increasingly competitive with a huge number of domestic VC firms stepping in the industry. This trend reflects, to some extent, that foreign VC firms share experience as well as risk through syndication to mitigate the LOF. However, we notice that about half CBVC deals in China are solo investment to avert the transaction cost brought by syndication. The second question we intend to answer with this article is how the CBVC firms syndicate when faced with LOF.

VC deals and portfolios in China mainland (1988–2016).

To address these questions, we focus on the foreignness brought by cultural distance and estimate the effect of cultural distance on foreign VC firm’s strategy of entry. To be specific, we test whether foreign firms are more likely to syndicate than solo when faced with greater cultural distance. Furthermore, we find some other strategies to mitigate LOF: enlarging the syndication, syndicating with firm from the same home market, and setting subsidiary in the host market. Our estimation shows an inverse U-shape relationship between cultural distance and the above-mentioned strategies. Thus, we justify that foreignness turns from liability into advantage while it grows. In addition, we find that the reputation of foreign VC firms exerts a negative effect on the curvilinear relationship between cultural distance and syndication. In other words, reputation mitigates the LOF. One concern of our estimation lies in the measure of foreignness. We address this concern in the following manner. First, in the “Theory and Hypotheses” section, we interpret the causality between cultural difference and foreignness and justify the variable cultural distance as proxy of foreignness. Second, we alter the measures of cultural distance and re-estimate the relationship in the robustness test.

This contribution of this article is threefold. First, to the best of our knowledge, prior literature is more concentrated on the dark side of foreign identity and discusses the LOF (Buckley & Casson, 2016; Gaur et al., 2011; Sethi & Guisinger, 2002; Tykvova & Schertler, 2014). Instead, we notice the other side of foreignness and justify that foreignness can be an advantage in the VC market. We suggest that emerging markets are desirable destination for VC firms, especially those from faraway advanced economies. We recommend that VC firms take good advantage of their foreign identity and adjust entry strategy accordingly. Second, research on VC in emerging markets is handicapped for the lack of data. In this article, we fill this gap with evidence from China. Our findings shed some new lights on the entry strategy of CBVC inter alia in emerging markets. This article proposes that proper entry strategy of CBVCs brings a win–win between VC firms and the portfolio in host market. Thereby, a promising prospect awaits not only the entrepreneurial activities in emerging markets but also the global growth. Third, we enrich the theories of multinational operation. Prior literature on multinationals is almost focused on manufacturing firms (Ghemawat, 2007), while prior research on cross-culture is concentrated on individuals (Mathur, 2012). On one hand, VC firms are different from manufacturing firms. On the other hand, organizational decisions are made by individuals. Thus, this article enriches the theories of multinational operation by discussing the entry strategy of CBVC firms with a perspective of culture.

The rest of this article is organized as follows. We propose our hypotheses in the following section. In “A Brief of CBVCs in China” section, we describe the background of China’s CBVC market and characteristics of foreign VCs operating in China mainland. The “Method” section describes the methodology of empirical research, and the “Results” section interprets the results. Conclusion and discussion are presented in the last section.

Theory and Hypotheses

Foreignness as a Liability

Cross-border business is costly (Hymer, 1976), as foreign firms suffer from cost and barriers in terms of economy as well as society (Gaur et al., 2011; Luo et al., 2002; Petersen & Pedersen, 2002; Sethi & Guisinger, 2002; Tykvova & Schertler, 2014), known as the Liability of Foreignness in the host market (Buckley & Casson, 2016; Caves & Caves, 1996; Dunning, 1977). Cultural distance between home and host economies leads to the LOF in capital market (Bell et al., 2012).

In terms of business, culture affects behavior and outcomes (Barro & McCleary, 2003; Fernandez & Fogli, 2009; Guiso et al., 2006, 2008, 2009; Tabellini, 2008; Zingales, 2011). Share values and beliefs are the source of attractiveness and trust (Vaara et al., 2012), which increases the likelihood of successful contract (Y. J. Gu et al., 2019). The prior literature suggests that domestic investors enjoy advantage in terms of information, network, and knowledge (Grinblatt & Keloharju, 2001; Hau, 2001). On the contrary, their foreign counterparts suffer from higher information and transaction cost (Choe et al., 2001).

Communication is necessary in the VC business (Amit et al., 1998; Dai et al., 2012). However, communication in CBVC is less efficient because of cultural distance, which raises transaction cost for both sides and lowers the efficiency of the deal (Hofstede, 2001; Steensma et al., 2000). Furthermore, the LOF generated from cultural distance undermines mutual trust (Johanson & Vahlne, 2009; Vaara et al., 2012) and eventually the performance (Bottazzi et al., 2008; Li et al., 2014). To sum up, cultural distance between home and host market generates LOF of CBVC firms.

Syndication: Benefits and Costs

To overcome the LOF, inter alia in the process of portfolio selection (Wright et al., 2005) and monitoring (Cumming et al., 2006), CBVC firms tend to syndicate (Devigne et al., 2013; Makela & Maula, 2008). Syndication benefits VC firms in threefolds. First, knowledge is shared within syndication (de Clercq & Dimov, 2004), and the decision is more likely to be rational and wise (Sah & Stiglitz, 1986). Thus, the syndicated deal is more robust and profitable from the process of portfolio selection (Lerner, 1994). Second, as syndicated VC firms share risks (Lockett et al., 2002). Thus, syndication is widely used when financing start-ups with higher risks (Manigart et al., 2006). Third, syndication is effective in sharing financial burden across VC firms, which enables deals requiring large amount of capital (de Clercq & Dimov, 2004). Therefore, we propose the following hypothesis:

However, syndication is associated with transaction cost. Generally, a typical VC deal involves one or two leader VC firm(s) and several follower VC firms. The leader, with a good reputation and outstanding prior performance, contributes more in the deal. The followers, however, take advantage of leader’s contribution to improve their own performance (Bothner et al., 2015). Instead of “free-riders” (Wright et al., 2005), leaders desire a complement or at least an equal contributor (Manigart et al., 2006). To sum up, the disparity leads to a search of “better-than-me”—Every firm is seeking a partner with experience and reputation (Lerner, 1994). Thus, the process of partner selection is a costly process of signal screening. Furthermore, syndication is social network in essence, and VC firms are embedded in the network through sharing knowledge and consistent decision (Guler, 2007). Once syndicated, this embeddedness fetters the firm, inter alia when it desires to exit (Zheng & Xia, 2018). Therefore, transaction cost is inevitable through the process of establishing and maintaining a syndication.

Foreignness as an Advantage

Despite a huge body of literature focused on the LOF, some researchers notice the Advantage of Foreignness (AOF) in, inter alia, emerging markets. When cultural distance is great enough, foreignness would turn the table. First, foreignness improves the organizational performance by changing individual cognitive framework. Operating in a context with completely different culture, individuals in the multinational organization would develop a unique cognitive framework combining the cognition practice from both host and home market (Vora & Kostova, 2007). Thus, the multinational would reflect on (Mutch, 2007) or even break social taboos of the host market (Boxenbaum & Battilana, 2005; Edman, 2016; Regner & Edman, 2014; Siegel et al., 2019) and would become more creative (Shi & Hoskisson, 2012; Smets et al., 2015) and competent (Battilana et al., 2015).

Furthermore, the foreign identity builds a unique image for the multinational, which averts homogenization with the domestic competitors (Smith, 2011). A competent multinational enhances the image of its brand by adjusting strategy to the local conditions (Bhaumik & Co, 2011; Evans & Mavondo, 2002). In particular, pro-foreign bias prevails in emerging markets (Kostova & Zaheer, 1999) and multinationals turn the foreign identity and cultural distance into an “exotic halo” in the host market (Insch & Miller, 2005). In addition, Ghemawat (2007) suggests arbitrage as an entry strategy for multinationals, which exploits differences across locations rather than taking differences as constraints. The opportunities of cultural arbitrage lie in the country-of-origin advantages (Ghemawat, 2007). The United States (where VC is originated) and West Europe where VC has developed for decades enjoy such country-of-origin advantages against the emerging markets. Therefore, with the cultural distance increasing, foreign VC firms gain AOF, which offsets the LOF to some extent. We propose the following hypothesis:

Reputation as an Asset

A company’s reputation reflects public cognition of its prior behavior and performance (Rindova et al., 2005), and generates revenue as an intangible asset (Hall, 1992; Kreps & Wilson, 1982; Lange et al., 2011; Milgrom & Roberts, 1982; Rindova et al., 2005, 2007; Weigelt & Camerer, 1988). The prior literature shows that higher reputation of the VC firm improves the performance of portfolio. First, a higher reputation triples the likelihood that the VC is accepted (Hsu, 2004). Thus, a VC firm with better reputation is more likely to finance the portfolio with better potential (Sorensen, 2007). Second, once financing, better-reputed VC firms provide better value-adding service (Zacharakis et al., 2007). For example, VC firms with higher reputation perform more efficiently in terms of monitoring and signaling (Krishnan et al., 2011), and hire more professional advisors (T. H. Lin & Smith, 1998). Third, to maintain their reputation, better-reputed VC firms focus more on the IPO of portfolio (Bradley et al., 2015; Lee & Wahal, 2004) and therefore are more eager to enhance the portfolio’s performance (R. Lin et al., 2017). The prior study shows that start-ups backed by better-reputed VC firms are more successful in IPO and growth afterward (Gompers & Lerner, 2003; Krishnan et al., 2011; R. Lin et al., 2017; Nahata, 2008; Shu et al., 2011).

On the contrary, reputation of a company indicates its potential (Q. Gu & Lu, 2014). External investors find it difficult to assess a start-up due to its limited history (Bruton & Ahlstrom, 2003). In this case, finance from a prestigious VC firm positively indicates the potential of the start-up (P. M. Lee et al., 2011; Rindova et al., 2005). Thus, these start-ups would be valued higher in the rounds afterward, and the cumulative effect leads to better performance. Therefore, reputation plays a crucial role in the win–win relationship between VC firm and portfolio. Accordingly, we propose the following hypothesis:

A Brief of CBVCs in China

The VC industry in China was born from the sporadic inflow of foreign capitalists since the late 1980s, and the CBVCs were once dominant in China’s VC market while domestic VC firms were in their infancy. These foreign pioneers played an important role in the development of emerging industries. For instance, Alibaba was financed by a bunch of foreign VC firms like Softbank and Goldman Sachs and became the second largest internet giant in the world. It is obvious in Figure 1 that China became an attractive host market, and the number of CBVC deals increased significantly since marketization reform in 1992. Both the number of CBVC deals (see Panel A of Figure 1) and the number of portfolio start-ups (see Panel B of Figure 1) went up around 2000 when China won the membership of World Trade Organization (WTO). The Regulation of Foreigner Establishing Investment Company was enacted in November 2004 and CBVC deals grew dramatically afterward. Figure 1 depicts drastic reduction of CBVC after 2008 crisis, especially in the year of 2009. The market of VC as well as CBVC recovered in 2010 with the recovery of global economy then. Another dramatic plunge took place in 2012 when foreign investment reduced due to the Debt Crisis of Europe. Demand for VC was greatly encouraged when the slogan of “Mass entrepreneurship and innovation” put forward by China’s Prime Minister for the first time in September 2014. Both VC firms and portfolio start-ups took advantage of the favorable policies and enjoyed an immense growth over that period. On the other side, foreign VC firms are losing their role of dominance in an increasingly competitive market in China from 2016.

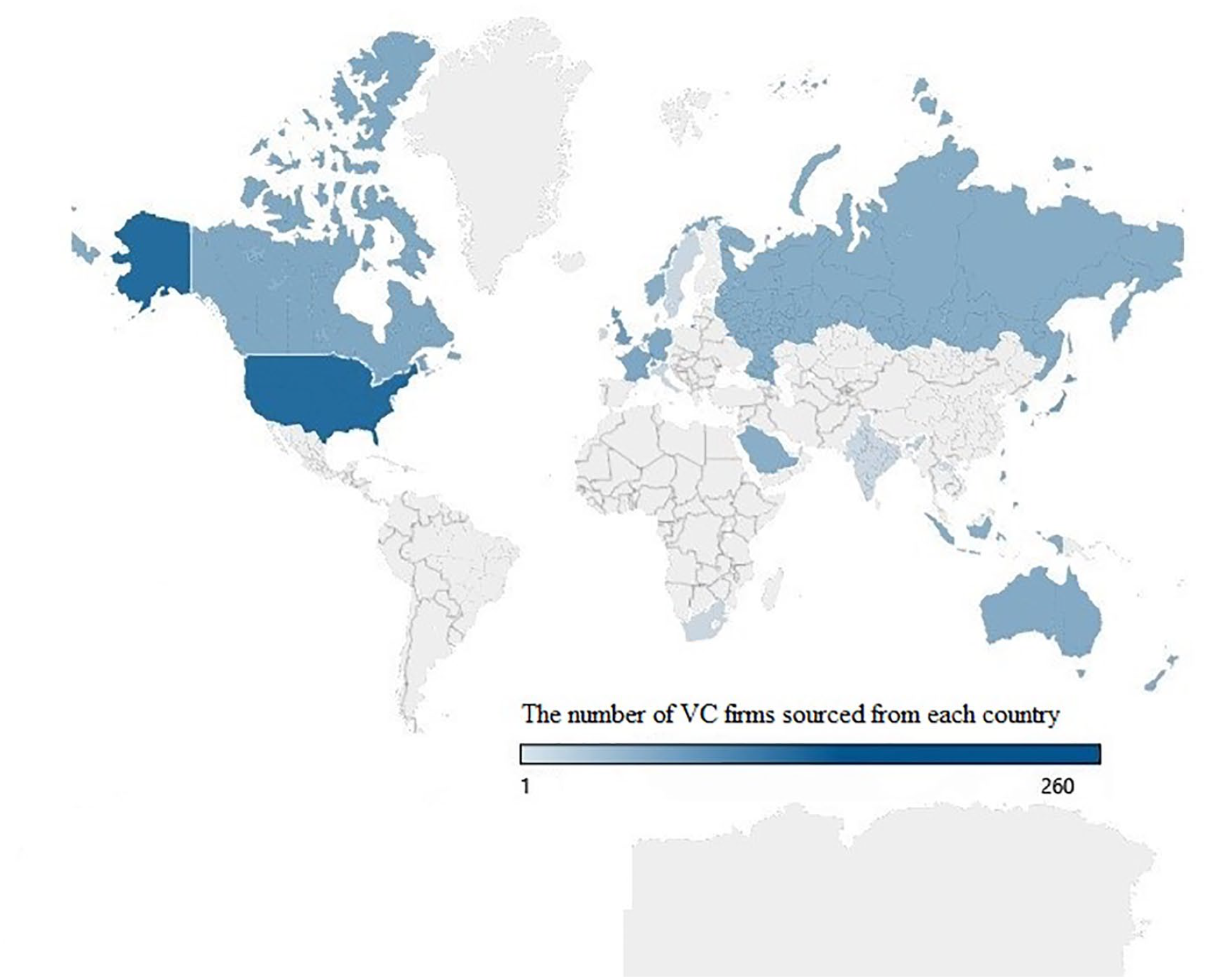

Where Do They Come From?

Figure 2 plots the home market of CBVCs in China mainland through 1988 to 2016. During the sample period, a total of 260 VC firms sourced from the United States (42% of the total foreign VC firms) and 134 firms from Hong Kong (21.65% of the total foreign VC firms) invested at least once in the market of China mainland; that is, Hong Kong and the United States are the largest sources of CBVCs in China mainland (while the number of VC firms from any other economies makes up no more than 7% of the total foreign VC firms). Sharing the context of Chinese culture, VC firms from Hong Kong are advantaged with short cultural distance when operating in China mainland. However, instead of other Confucian economies in Asia, the United States sources the largest CBVCs in China, which indicates the pro-foreign bias prevails in emerging markets (Kostova & Zaheer, 1999) and country-of-origin advantages (Ghemawat, 2007) to some extent. Hong Kong and the United States are two extremes in terms of cultural distance from China mainland and, as the largest sources, they suggest the LOF and AOF.

Home market of CBVCs in China mainland (1988–2016).

What Do They Finance?

Figure 3 shows the preference of domestic and foreign VC firms on portfolio selection. For both domestic and foreign VC firms, the top preferred industries are information technology (IT), manufacturing, and retailing, which depicts the whole body of booming online retailing in recent years. Furthermore, domestic VC firms seem more prone to finance manufacturing start-ups, for their local identity plays an important role in fixed investment. In addition, the lucrative industry of “culture, sports and entertainments” 2 is one of the four most attractive industries in Panel A. In Panel B, however, this industry stands out no more owing to the restrictive terms against foreign capital. By comparison, the advantage of domestic VC firms in terms of portfolio selection indicates the LOF of their foreign counterparts.

Portfolio industry for domestic and foreign VCs.

When Do They Finance?

Figure 4 shows the preference of domestic and foreign VC firms on stage selection. For both domestic and foreign VC firms, the stage of development is the most attractive. Furthermore, foreign firms in Panel B are more prone to finance portfolio in the late stage (i.e., expansion and maturity), where risk is relatively lower than that of earlier stages. In other words, foreign VC firms are more likely to invest in less risky stages, which mitigates the LOF to some extent.

Stage of VC deals for domestic and foreign VC firms.

Method

Sample and Data

We extract detailed description of VC deals from the databases CVSource (http://www.cvsource.com.cn) and Zero2IPO (https://www.pedata.cn/data/index.html). To be specific, we adopt the dataset framework of CVSource. For the data missing in CVSource, we attempt to search in Zero2IPO, if possible. Notably, CVSource provides data on deal level; that is, a syndication involving several VC firms is reported as ONE deal in CVSource, with no evidence showing who is leading. Panel A of Figure 1 plots number of deals on this same level. However, data used for regression in this article are pairwise; that is, every observation includes one VC firm vis-à-vis one portfolio start-up while details of other VC firms in the syndication are labeled as “partner data.” For example, three VC firms (Firms A, B, and C) syndicate to finance one start-up. This deal is divided into three equal pairwise observations: Observation 1 including Investor A with Partners B + C, Observation 2 including Investor B with Partners A + C, and Observation 3 including Investor C with Partners A + B.

In addition, data of ownership are gathered from official websites of the VC firms and start-ups and National Enterprise Credit Information Publicity System of China (http://www.gsxt.gov.cn/index.html). We extract data of cultural distance from the book Culture, Leadership and the Organizations: The GLOBE Study of 62 Societies (House et al., 2004). Reputation of VC firms is defined by the Zero2IPO annual ranking of VC firms (https://www.pedata.cn/topranking/index.html). Our sample period spans from January 1, 1988, to December 31, 2016.

Variables

To simplify, each observation includes the focal VC firm, its partners (if syndicated), and the portfolio start-up. For each observation, we introduce variables of four categories: (a) variables determined by the focal VC firm, like the age and experience of the focal VC firm, syndication, and stage; (b) variables determined by the focal VC firm and the portfolio start-up, like the cultural distance; (c) variables determined by the focal VC firm and its partners, like deal amount; and (d) variables determined by the portfolio start-up, like industry. With the pairwise (rather than firm-level) data, we address the multiple strategy of VC firms. For example, if a VC firm conducts different strategies in different deals (or even different rounds of the same portfolio), there would be different observations for each deal.

Dependent variable

The dependent variable describes the strategy of VC firms. In our baseline regression, the dependent variable is dummy

Independent variable

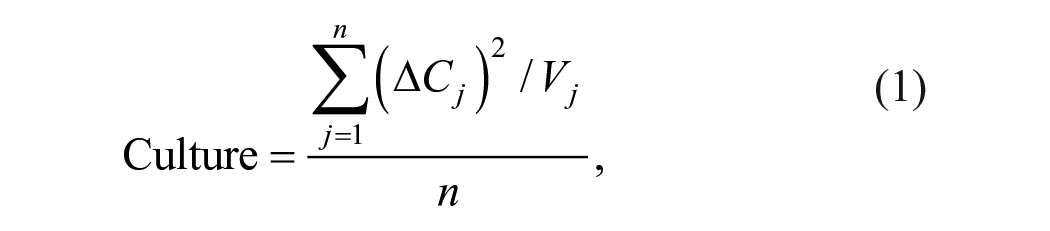

As the core independent variable, cultural distance between home and host countries measures to which extent customs and values in one region are different from those in another (Hofstede, 2001; Kogut & Singh, 1988). Cultural distance is one of the most important determinants of entry mode in the field of cross-border business (Harzing, 2002). The GLOBE distance, updated in this century, is much more suitable for discussion of recent business behavior and is selected as the core independent variable of this article. The GLOBE distance is the result of the international survey Global Leadership and Organizational Behavior Effectiveness Research Program (GLOBE) with 60 economies involved, which is dedicated to the impact of culture in corporate governance and performance. House et al. (2004) describe culture in the following dimensions: uncertainty avoidance, power distance, institutional collectivism, in-group collectivism, gender egalitarianism, assertiveness, future orientation, performance orientation, and humane orientation. House et al. (2004) define the distance on two basis: practice and values. Although multinationals start localization and adjust their practice after entry (Luo et al., 2002), values of the home market are imprinted for the long term. Thus, we use the GLOBE distance of values. Aggregating distance of nine dimensions in line with Kogut and Singh (1988), we have the independent variable:

where ∆

Moderator

We define the reputation of VC firms based on Annual Ranking of VC or Private Equity (PE) in China published by Zero2IPO, which is the most widely used ranking for VC firms in China (Q. Gu & Lu, 2014; R. Lin et al., 2017). This ranking, dating back to 2001, involves both domestic and foreign VC firms investing in China mainland with consideration of capital size, experience, exit in history, performance and profit, and so on. Although Zero2IPO publishes various number of VC firms as the “top echelon” each year, the Top 10 domestic/foreign VC firms are always included in the ranking list. Thus, we describe the reputation with a dummy variable

Control variables

As is proposed in prior literature, green hands are more likely to syndicate. On the contrary, a veteran with increasing experience is less prone to syndicate (Wang, 2017). Furthermore, experience inspires VC firms start business overseas, no matter whether they gain the experience from domestic or overseas market (Tykvova & Schertler, 2011). We describe VC firm’s experience with three alternative variables: (a) number of deals as investor in its history (Experience1), (b) number of exits as investor in its history (Experience2), and (c) number of deals in China mainland as investor in its history (Experience3). 3 These experience variables are logarithmic value of count. Considering most of the foreign firms have just started business in China mainland recently, it is unlikely to observe enough samples of exit from China market.

Imagine a VC firm who finances the start-up from the very beginning and keeps financing until IPO. The above-mentioned variable of experience may draw a biased picture of this far-sighted firm, for its experience grows despite few deals/exits taking place. In other words, the firm is gaining experience more or less, as long as it survives. Thus, we control the variable of VC firm’s age (Age). Notably, a considerable number of firms are registered for a predictable investment; that is, VC firms are quite active shortly after being founded. On the contrary, quite a few firms survive through the first 24 months after establishment. Therefore, we describe the age variable in a more detailed manner and count the age in month. 4 The age variable is logarithmic.

Manigart et al. (2006) point out that VC firms are more likely to syndicate when the deals require large amount of capital. Thus, we control the capital amount (trillion CNY) of each deal (Money). As is mentioned in the “Sample and Data” section, we identify the amount of each deal but not of each firm, if syndicated. This variable is deflated with gross domestic product (GDP) and exchange rate.

VC firms become more cautious in business overseas and the strategy of multistage financing prevails in CBVCs (Chemmanur et al., 2016). Owing to the implicit higher risk of early-stage portfolio, foreign VC firms tend to follow their domestic partners (Makela & Maula, 2008). Based on the financing round and the life cycle of start-up, CVSource identifies the stage of portfolio as infancy, development, expansion, and maturity. Accordingly, we control the stage with a dummy variable (Late). If the deal takes place in the stage of expansion or maturity, then Late equals one.

Generally, VC firms prefer high-tech portfolio start-up (Bassolino, 2002; Dossani & Kenney, 2002; Mayer et al., 2005), where syndication prevails because of higher risk. We extract the GB code 5 of portfolio start-ups and identify whether the industry is high-tech according to the Guidance for Identification and Management of High-Tech Enterprises (2016). We describe the industry of portfolio with a dummy variable (Hitech). If the start-up is identified as high-tech, then Hitech equals one.

Econometric Model

Equation 2 shows the econometric model of our empirical research:

where X represents control variables. Without loss of generality, we assume that cultural distance is positively related with foreignness. Thus, cultural distance is applied as proxy of Foreignness. According to the hypotheses above, we predict that

Results

Descriptive Statistics

Table 1 reports the descriptive statistics of main variables. We notice that the mean value of

Descriptive Statistics.

Note. This table reports the descriptive statistics of main variables. Panel A reports the statistics of full sample, while Panel B reports the sample of solo investment and Panel C reports the sample of syndications.

Curvilinear Effect of Foreignness on Syndication

Table 2 reports the baseline results. The coefficient of cultural distance remains significantly positive in both univariate and multivariate regressions. Thus, we test Hypothesis 1; that is, foreign VC firms bearing longer cultural distance between home and host markets are more likely to mitigate the LOF by syndication. Furthermore, the coefficient of squared cultural distance remains negative in Columns (2) to (6). Thus, we test Hypothesis 2 and find the inverse U-shape relationship between cultural distance and syndication. Specifically, foreign VC firms are more likely to syndicate while the cultural distance increasing but below the threshold. On the contrary, with the cultural distance above the threshold, the growing distance decreases the likelihood of syndication. Moreover, the negative coefficient of interaction between cultural distance and reputation tests Hypothesis 3; that is, foreign VC firm’s reputation mitigates the effect of cultural distance on syndication. In addition, the coefficient of control variables tests some above-mentioned predictions. For example, the negative coefficient on VC firm’s age and experience indicates that foreign VC firms equipped with either domestic or overseas experience are more likely to conduct solo investment. The significantly positive coefficient of deal amount shows that syndication is effective in terms of sharing financial burden (Manigart et al., 2006). The significantly positive coefficient of high-tech industry implies that greater industry risk leads to syndication.

Baseline Regression: Curvilinear Effect of Foreignness on Syndication.

Note. This table reports the baseline results of foreignness’ curvilinear effect on syndication, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. The dependent variable is the dummy variable of syndication (Syndication). All the columns report the result of logit regression.

More Hands Light the Fire: Syndication Size

Syndication shares not only the risk (Lockett & Wright, 2001; Manigart et al., 2006) but also the profit (Brander et al., 2002). Thus, syndication bears a trade-off between risk and profit. Similarly, the size of syndication (i.e., number of VC firms involved in one syndication) bears the same trade-off. Derived from Hypothesis 2, we propose the following hypothesis:

Figure 5 plots the size of syndication involving foreign VC firm(s) in China mainland through 1988 to 2016. Nearly half of the syndications involve only two VC firms. The number of deal halves while the size of syndication grows by one. More than 90% of the syndications involve no more than five firms. Thus, focusing on the syndication size between two and five, we construct a dummy variable to indicate whether the syndication is large: The variable equals one when the syndication involving more than two firms.

Size of syndication with foreign firm(s) involved.

Table 3 reports how the cultural distance affects the size of syndication. We replace the independent variable in Table 2 with the dummy variable indicating large syndication. The results in Table 3 show an inverse U-shape relationship between cultural distance and syndication size. Specifically, foreign VC firms are more likely to syndicate with more than one partner in a deal while the cultural distance growing but below the threshold. On the contrary, if the cultural distance is greater than the threshold, foreign VC firms are more likely to maintain a smaller syndication while the distance continues growing.

Effect of Cultural Distance on Syndication Size.

Note. This table reports the effect of cultural distance on syndication size with the sample of syndicated foreign VC firms, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. The dummy dependent variable equals one if the firm syndicates with more than one partner in the deal. Columns (1) to (3) report results of logit regression, while Columns (4) to (6) report results of OLS regression using linear probability model (LPM). We exclude syndications with six or more firms involved. We control the experience with variable Experience1, and the other control variables are same with Table 2. VC = venture capital; OLS = ordinary least squares.

Going Abroad With “Countrymen”: Syndication With Home Market

As tunnels of information, syndication mitigates the LOF caused by cultural difference. In other words, syndication alleviates the adversity of unfamiliarity. In this section, we test the relationship between familiarity within syndication and the unfamiliarity between home and host markets. Compared with a foreign partner, a “countryman partner” (i.e., VC firm from the same home market) increases the familiarity within the syndication and thereby reduces the organizational transaction cost. Derived from Hypothesis 2, we propose the following hypothesis:

We construct an alternative dependent variable describing partner selection: It equals one when the firm syndicates with at least one firm from its same home. Table 4 shows an inverse U-shape relationship between cultural distance and the probability of syndicating with “countrymen.” Specifically, VC firms are more likely to syndicate with partners from its home market when the foreignness growing with cultural distance below the threshold; VC firms are less likely to syndicate with partners from its home market when the foreignness growing with cultural distance above the threshold.

Effect of Cultural Distance on Partner Selection.

Note. This table reports the effect of cultural distance on partner selection of syndication, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. The dummy dependent variable equals one if the firm syndicates with at least one firm from its same home (i.e., countryman). All the columns report results of logit regression. Control variable are same with Table 2.

Learning From the Local: Subsidiary in Host Market

According to Uppsala model, information is the fundamental determinant of international operations (Johanson & Vahlne, 1977), whereas LOF is disadvantageous in terms of operation. Apart from the above-mentioned syndication, subsidiary in the host market channels information and mitigates the LOF (Hollensen, 2007). To be specific, subsidiaries embedded in local network (Porter, 1993) are adapted to the culture and institution of host market (London & Hart, 2004), especially in the context of emerging markets (Zhao et al., 2005). On the contrary, subsidiaries bring about transaction cost in terms of setting up and operation. Thus, setting subsidiary is a trade-off between cost and benefit. Derived from Hypothesis 2, we propose the following hypothesis:

To test Hypothesis 2-3, we alternate syndication with the variable of subsidiary location, and the results are presented in Table 4. Notably, as the location data for subsidiaries are cross-sectional; that is, we know whether the firm has a subsidiary in China by the end of 2016 but not when the subsidiary was initiated. Therefore, apart from the full-sample regression, we use the more recent subsample of period 2015–2016. The results in Table 5 test that foreignness of VC exerts a curvilinear effect on the probability of setting subsidiary in host market. Specifically, VCs are more likely to set a subsidiary in host market when the foreignness growing with cultural distance below the threshold; VCs are less likely to set a subsidiary in host market when the foreignness growing with cultural distance above the threshold.

Effect of Cultural Distance on Subsidiary Location.

Note. This table reports the effect of cultural distance on subsidiary location of foreign VC firms, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. The dummy dependent variable equals one if the firm establishes at least one subsidiary in the host market (i.e., China mainland). The cross-sectional data of subsidiary location are updated by January 1, 2017. Columns (1) and (2) report results of full sample, while Columns (3) to (6) report results of period 2015–2016. All the columns report results of logit regression. Control variables are same with Table 2. VC = venture capital.

Robustness

Despite the wide use of Kogut and Singh’s (1988) aggregation shown in Equation 1, it is criticized for the excessive and asymmetric simplification of index for each dimension (Shenkar, 2012). Thus, as is illustrated in Equation 3, we calculate cultural distance as is proposed in recent literature on CBVC (Li et al., 2014; Meuleman & Wright, 2011):

where the denotations are same with those of Equation 1.

We re-estimate baseline regression of Table 2 by replacing cultural distance with the variable calculated as Equation 3 and the results are presented in Table 6. Thus, our estimation remains robust across different measures of cultural distance.

Robustness Test.

Note. The table reports the results of robustness test, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. Columns (1) to (4) report results of logit regression, while Columns (5) to (8) report results of OLS regression using linear probability model (LPM). Independent variable (Culture) is calculated as Equation 3. We control the experience with variable Experience1, and the other control variables are same with Table 2. OLS = ordinary least squares.

Conclusion and Discussion

Conclusion

Foreignness is liability. Yet, foreignness is more than a liability. Although most of prior literature focuses on the fact that foreignness isolates multinationals by undermining their information tunnel, in this article we emphasize that excess foreignness turns into an “exotic halo,” which facilitates business in emerging markets with pro-foreign bias. Thus, the foreign VC firms operating in emerging markets need to fully understand their identity of foreignness and adjust entry strategy accordingly. This article investigates how the foreignness affects strategies of foreign VC firms in the emerging markets. To be specific, this article focuses on the entry strategy vis-à-vis syndication and subsidiary location. The entry strategy is the decision-making process when faced with trade-off between liability and AOF, between benefits and cost of syndication, and between benefits and cost of establishing local subsidiaries in the host market.

First, we detect a threshold of foreignness in terms of cultural distance between home and host markets. When the cultural distance remains below the threshold, with the distance growing, a foreign VC firm is more likely to syndicate. In other words, the identity of foreignness is liability-dominant in this phase and the foreign VC firm relies on the information tunnel provided by cooperation and needs to spread risk through syndication. Thus, syndication is the entry strategy of foreign VC firms in this phase. However, once the cultural distance passes the threshold, foreign VC firms behave in the opposite manner; that is, they are less likely to syndicate with the distance continues growing. In this phase, the identity of foreignness becomes advantage-dominant. Considering the cost of syndication, foreign VC firms in this phase tend to operate solo with their exotic halo. In addition, our finding shows that reputation works as a negative moderator on the inverse U-shape relationship between foreignness and the entry strategy of syndication, which implies that reputation as an intangible asset brings firm sustainable advantage and mitigates the LOF.

Second, we test a similar threshold of foreignness affecting the strategy of those firms in syndication. As to the syndication size, when the cultural distance remains below the threshold, with the distance growing, a foreign VC firm is more likely to stay in a larger syndication (i.e., syndicating with more than one partner in the same deal); however, once the distance passes the threshold, such inclination declines with the distance growing. It is explicable in terms of benefits (e.g., risk-spreading and knowledge-sharing) and costs (e.g., free-rider exploit and embeddedness) of enlarging the syndication. As to the syndication partner selection, when the cultural distance grows but remains below the threshold, the foreign VC firm is more likely to syndicate with “countrymen” (i.e., VC firms sharing the same home country with it); yet, with the threshold passed, the foreign VC firm operates in the opposite while the distance continues growing. This curvilinear relationship indicates that foreign VC firms rely on the information tunnel based on familiarity in the syndication when their foreign identity is liability-dominant, but the “countrymen” syndication brings more redundancy than familiarity when foreignness becomes advantage-dominant.

Third, we notice local subsidiary in host market as alternative entry strategy to syndication and find a similar threshold of foreignness therein. To be specific, the foreign VC firm is more likely to establish a local subsidiary in the host market when the cultural distance grows but under the threshold—but the inclination decreases while the distance continues growing over the threshold. It indicates that, when the foreignness is liability-dominant, foreign VC firms acquire knowledge of the host market by entering and staying in it in the form of a subsidiary. Nevertheless, once the foreignness becomes advantage more than liability, the operational cost of local subsidiary in host market outweighs the knowledge-acquiring capability.

Discussion and Future Directions

LOF and liability of outsidership (LOO)

Notably, when investing in a foreign market, the VC firm might suffer from not only LOF but also LOO. The LOF is caused by the lack of “institutional market knowledge” (e.g., culture and legislation) while the LOO is resulted from the lack of “business market knowledge” (e.g., relationship with other firms on the same market), according to Johanson and Vahlne (2009) who pioneered a comparison between the two terms. In this sense, prior syndication in the host market channels business market knowledge and mitigates the LOO.

The term “centrality” describes the density of syndication links that a firm maintains with different partners (cf. R. Chen & Qiu, 2019). We employ a 3-year window to build the syndication network and a VC firm with high centrality means it has syndicated with a great number of partners in the previous 3 years. Thus, we construct eigenvector centrality in line with Burt (2000) as a solution to Equations 4 and 5:

where

We re-test Hypothesis 2 with centrality introduced, and Table 7 reports the results. The inverse U-shape relationship between cultural distance and syndication maintains while the mitigating effect of reputation stays significant, which indicates that syndication alleviates the LOF. Furthermore, we notice the significantly negative coefficient of centrality variable; that is, a foreign VC firm enjoying more relationship with other VC firms in the host market is less likely to syndicate. In other words, syndication is also a method to mitigate the LOO.

Curvilinear Effect of Foreignness on Syndication With Centrality.

Note. This table reports the results of foreignness’ curvilinear effect on syndication with centrality introduced, where *, **, and *** denote the significance on the levels of 10%, 5%, and 1%, respectively. The values in parentheses refer to t value. The dependent variable is the dummy variable of syndication (Syndication). All the columns report the result of logit regression. Culture in Columns (1) to (3) is calculated as Equation 1, while calculated as Equation 3 in Columns (4) to (6).

Methods to mitigate foreignness

Ghemawat (2007) proposes “AAA” strategies to mitigate foreignness, including adaptation (to adjust to cross-border differences through variation), aggregation (to overcome cross-border differences through regionalization), and arbitrage (to exploit cross-border differences).

The adaptation of a firm begins with the variation of its products, policies, positioning, metrics, and so on, which raises costs because of increasing fragmentation and complexity (Fayerweather, 1969). Thus, the process of adaptation is a series of cost–benefit trade-offs, and the focus is to reduce the need for variation (Ghemawat, 2007). Ghemawat (2007) suggests two methods for adaptation: (a) externalization to reduce the burden of variation (e.g., strategic alliances, networking) and (b) innovation to improve the effectiveness of variation (e.g., localization, transformation). In this sense, adaptation is used by VC firms when investing abroad. To be specific, syndication reflects the method of externalization while subsidiary in home market exemplifies the method of innovation.

As is mentioned in the “Foreignness as an Advantage” section, we suggest the country-of-origin advantages (Ghemawat, 2007) of VC firms from the United States and West Europe, which reflects the strategy of arbitrage employed by these VC firms. As to the strategy of aggregation, it refers to the vertical integration across locations (Ghemawat, 2007) and is more often discussed in manufacturing than consulting or financial industries. However, VC industry, different from consulting and traditional financial industries, involves on-site jobs like due diligence. Thus, the application of aggregation strategy would be an interesting topic for future research.

Besides, Gordon (1964) proposes the process of assimilation where immigrants replace cultural norms of their origin with the cultural norms of the host country, and such process might be influenced by demographic variables of immigrants (Gordon, 1964). Nevertheless, both overacculturation (i.e., immigrants assimilate to the mainstream culture of host country) and hyperidentification (i.e., immigrants insist the culture of their origin and refuse to assimilate) are perceived in a more recent study (Mathur, 2012). In the context of CBVC, acculturation or assimilation would mitigate or even eliminate not only the LOF but also the AOF. Empirical results in this article show no evidence of assimilation. Yet, it would be an interesting direction for future research to examine the balance between acculturation and identification of C-suite employees in the VC firms.

Measures of cultural distance

Apart from the GLOBE distance (House et al., 2004) employed in this article, the prior literature proposes two other measures of international cultural distance: Hofstede distance (Hofstede, 1998, 2001) and Schwartz distance (Schwartz, 1999). The former, focused on individual characters, includes six dimensions: power distance index, collectivism versus individualism, uncertainty avoidance index, femininity versus masculinity, short-term versus long-term orientation, and restraint versus indulgence (Hofstede, 1998, 2001). The latter, focused on values, includes seven dimensions: conservatism, intellectual autonomy, affective autonomy, hierarchy, egalitarian commitment, mastery, and harmony (Schwartz, 1999). Despite the wide use of Hofstede distance, it is criticized for the limited sample size and lack of update (Schwartz, 1999). In this sense, the GLOBE distance outperforms the other two measures, inter alia, in terms of up-to-dateness.

Notably, it is the individuals inside who make decision for the organization; that is, the decision of VC firms is the decision of those people in charge. As is specified in the GLOBE survey, the GLOBE distance is focused on human behavior in the context of business (House et al., 2004). Thus, this measure suits the context of CBVC. One of the limitations of this article is that cultural distance in both baseline and robust regression are calculated in an unweighted manner. Although all nine dimensions affect the decision maker to some extent, the impact of each dimension is not the same. Therefore, it would be useful to check the impact of each dimension and construct a weighted aggregation of cultural distance in the future research.

Two sides of reputation

The majority of prior literature focus on the process where the VC firm selects its portfolio actively and those with better reputation enjoy a louder voice (Sorensen, 2007) and stronger performance (Krishnan et al., 2011). Yet, the VC financing is a two-way process, where VC firms and start-ups match with each other. Hsu (2004) focused on the process where start-up selects a VC firm and his finding shows that start-ups are not always inclined to accept financing from a more reputable VC firm. Although a reputable VC firm may well bring greater business opportunities to its portfolio start-ups, the start-up needs to pay a premium to access such reputable financing (Hsu, 2004). Therefore, if a start-up has established its own reputation and network, it would unlikely pay the premium to the VC firm (Hsu, 2004). One of the limitations of this article is that few portfolio-level variables are controlled (due to the unavailability of dataset). In future research, we would gather more data to describe the portfolio start-ups and introduce the reputation variable of start-ups in regression.

Institutional environment

Prior literature underscores the role of institutional environments in overseas operation (Kostova & Zaheer, 1999). The institutional environment is complex in two aspects: (a) It is fragmented and involves different domains of institutions (Scott, 1995), and (b) multinationals are exposed to multiple environments (Galbraith, 1973; Lawrence & Lorsch, 1967; Thompson, 1967) in terms of authorities (Sundaram & Black, 1992), resource providers (Pfeffer & Salancik, 1978), and stakeholders (Evan & Freeman, 1988). Such complexity builds barrier to entry for the multinationals; Kostova and Zaheer (1999) define this barrier as “lack of legitimacy.”

Culture difference makes a part but not the whole of institutional difference. Also, cultural adaptation is “neither a necessary nor a sufficient condition for legitimacy” (Kostova & Zaheer, 1999, p.65). One of the limitations of this article is the absence of institutional distance. Prior empirical results show that both cultural and institutional distance and firm type exert an impact on the organizational identity of managers. As individual is the one who makes decision for the organization, a potential direction for future research is to introduce the institutional distance to the study of cultural distance.

Implications

Unlike the prior literature focused on the dark side of foreignness, we notice and test that foreign identity of VC firms could be an advantage in emerging market. This advantage is associated with the cognition of home market and is largely originated the expectation on the novel “guest” from diversified culture. Therefore, the VC firms from advanced but faraway countries are well accepted in emerging markets. We highly recommend that VC firms take good use of this advantage and operate in emerging markets far away, which is expected to stimulate knowledge spillover to the host markets and to complement the domestic VC firms.

As for the VC firms operating in markets where culture is not distinct enough from their home market, they might face liability rather than AOF. For these firms, syndication (especially with more VC firms and with other VC firm sharing the same home with them) and setting local subsidiaries are effective entry strategies. Besides, assimilation through adopting the host culture is another recommendation to these VC firms, given the learning cost is relatively low due to the similarity between the home and host cultures.

In addition, a good reputation plays a vital role in the operation of all VC firms. Better reputed VC firms are expected to take initiative to invest overseas while those with lower reputation are recommended to invest overseas through syndication in later stage.

Footnotes

Acknowledgements

The authors would like to extend gratitude to Prof. Yi Tan from Shanghai Jiaotong University, Prof. Jo-Ann Suchard from the University of New South Wales, and all the discussants on the 5th Annual Conference of Investment Academy (China) for the insightful comments that helped improve this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the National Natural Science Foundation of China (Grant Number: 71573163) and the Graduate Innovation Foundation of Shanghai University of Finance and Economics (Grant Number: CXJJ-2016-443).