Abstract

This study investigated the factors determining the behavioral intention of young Saudi entrepreneurs to use crowdfunding to finance their small enterprises. The capacity of behavioral intention to predict the use behavior of crowdfunding platforms was also assessed. Partial least squares-based structural equation modeling method (PLS-SEM) was used to analyze responses collected from 270 young Saudi entrepreneurs (qualified students) attending the Community College of Abqaiq in Saudi Arabia, which is affiliated with King Faisal University. The unified theory of acceptance and use of technology (UTAUT) with extensions of three constructs was employed. The findings revealed that performance expectancy, social influence, perceived trust and perceived risks predicted the behavioral intention of young Saudi entrepreneurs to use crowdfunding platforms to finance their small enterprises, whereas effort expectancy, facilitating conditions and trialability had no significant predictive effect on the same behavioral intention. It was further reported that behavioral intention could also predict the use behavior of young Saudi entrepreneurs on crowdfunding platforms. The overall results indicated that the model explained 55.4% of the variance in behavioral intention and 38.3% of the variance in use behavior of young Saudi entrepreneurs.

Introduction

The growth and development of economies depend on various factors, including engagement by small and medium-sized enterprises (SEMs) and the development of entrepreneurship. Both SMEs and entrepreneurship play a vital role in creating new job opportunities and reducing unemployment, particularly in developing countries (Alshebami, 2021; Audretsch, 2012; Chew et al., 2022), through the establishment of start-ups, small enterprises and other income-generating activities. However, these small investments may often be hindered by various challenges, including lack of experience, lack of technical knowledge, and deficient formal and informal institutions, information asymmetry, and many other obstacles that discourage entrepreneurs from launching their enterprises. In addition to the previously mentioned obstacles, lack of financial support represents the most critical challenge, as it can prevent the very establishment of the enterprise itself, prior to any considerations of work requirements or fixed capital.

Accessing the required capital is the most difficult challenge for business start-ups and small enterprises (Berger & Black, 2011; Lee & Brown, 2017). Most new entrepreneurs seek financing from conventional financial institutions, yet they often lack the required collateral and optimal credit history. Consequently, nearly half of all credit applications by entrepreneurs are rejected (Wahjono et al., 2016). Hence, it has become necessary for many entrepreneurs to search for alternative financing sources to meet their financial needs, such as crowdfunding platforms, venture capital and business angels. Accordingly, we sought to examine the perceptions of young entrepreneurs (qualified students) in Saudi Arabia concerning the use of crowdfunding platforms to finance their small enterprises. This is because it has been reported that crowdfunding platforms are a useful financial technology for supporting Middle Eastern start-ups (Abdeldayem & Aldulaimi, 2021). Furthermore, the concept of crowdfunding is linked to Fintech, which has exploded in popularity, affecting every aspect of the financial system. Fintech has benefited a significant number of people around the world while also improving the efficiency of the financial system (Allen et al., 2021).

As the concept and phenomenon of crowdfunding are relatively new, only a few studies have been conducted on them, mainly in developed countries, such as Australia (Ley & Weaven, 2011), China (Lee & Brown, 2017; Li et al., 2018), and Germany (Koch & Siering, 2015).

The majority of researchers who have investigated crowdfunding have agreed that it is an excellent alternative financing source for start-ups (Paschen, 2017). It has more potentiality of using it as a financing source, particularly in developing countries (InfoDev, 2013), as it does not require a good credit history nor any collateral, and it helps entrepreneurs secure the requisite funds to launch their enterprises (Hemer, 2011). Crowdfunding is also an attractive medium for those young entrepreneurs who seek to convert their innovative ideas into sustainable, feasible businesses (Stemler, 2013) but are unable to secure financing from conventional banks. Crowdfunding shares its origin with crowdsourcing, in which a group of people come together to communicate specific ideas about a particular topic. Crowdfunding allows entrepreneurs to acquire the funds needed to launch their nascent enterprises from anyone via the internet (InfoDev, 2013).

Among its many advantages, crowdfunding is less expensive than other funding sources, facilitates immediate feedback from funders about the proposed business model or plan, and permits unrestricted access to people from all over the globe. It is also considered a fundamental source of financial support for SMEs (Pazowski & Czudec, 2014). Further, the crowdfunding process allows small entrepreneurs to obtain the requisite funds for their ventures through increased flows of credit, ultimately creating more job opportunities, improving the economy and supporting financial inclusion (Achsien & Purnamasari, 2016; Coakley & Lazos, 2021).

Crowdfunding is typically donation-based, reward-based, equity-based, lending-based, or royalty-based (InfoDev, 2013), with greater emphasis placed on equity-based crowdfunding as an attractive financing source for graduate entrepreneurs (Amuna & Aburahma, 2019) and entrepreneurial activities (Talla et al., 2018).

However, despite the potential benefits and advantages of crowdfunding, and even though it can resolve funding issues for entrepreneurs, it must be carried out carefully and cautiously (Stemler, 2013). This is because online transactions between founders and funders can be risky (Belleflamme et al., 2014). Some such risks include—but are not limited to—defaulting, fraud, information asymmetry, poor product quality, inexperienced investors, and cyber-attacks. Minimizing these risks requires the relevant authorities to establish laws, rules and regulations that can effectively govern and control crowdfunding activities and discourage illegal activities, such as money laundering and the financing of terrorism. Accordingly, crowdfunding platforms that exercise due diligence with respect to minimizing risks and thwarting illicit activities are clearly more beneficial for both project founders and funders (Cumming et al., 2019).

Since crowdfunding in developing countries is still in its nascency (Turan, 2015), the economic and social circumstances of these countries must be fully understood before launching a crowdfunding endeavor in order to maximize benefits and ensure success (Steinberg & DeMaria, 2012). More specifically, the behavioral, cultural, technological, capital, and regulatory conditions of developing nations must be considered before commencing a crowdfunding project (InfoDev, 2013).

Like other oil-rich developing countries, Saudi Arabia is struggling with the sharp decline in oil prices, which has led to a massive deficit in the state budget, compelling the Saudi government to search for alternative income-generating activities to compensate for this deficit. Notably, the Saudi government has established a comprehensive long-term plan (Saudi Vision 2030) aimed at developing and implementing economic reforms throughout the country. These reforms are intended to diversify the Saudi economy, embrace globalization and support entrepreneurs in the country.

Saudi Vision 2030 considers SMEs as an engine for economic growth and development. Consequently, various initiatives have been launched to support SMEs. One such initiative, Monsha’at, was established in 2016 with the purpose of organizing, supporting, developing and sponsoring SMEs in line with global best practices to ensure their maximum productivity and thereby increase their contributions to the GDP, from 20% to 35% by 2030. To achieve this target, concerted efforts have been made to improve regulations concerning SMEs, facilitate easier financing and offer more international partnerships. In addition, a Saudi venture capital investment company was established to provide funding for SMEs. All of these actions have been undertaken to support entrepreneurship in Saudi Arabia as part of Saudi Vision 2030 (Coduras et al., 2019).

A vital objective of Saudi Vision 2030 is to maximize the contributions of SMEs to the national economy. Toward this end, funding facilities for entrepreneurs have been established to stimulate business development. The government-affiliated Capital Market Authority (CMA) has created a Fintech lab to allow financial innovators to examine their proposed innovative financial services, products and business models relevant to the capital market before launching them. The ultimate aim in this regard is to provide valuable financial products and services to entrepreneurs in the market.

The CMA has approved the establishment of two local, equity-based crowdfunding platforms—namely Scopeer and Manafa Capital (FintechSaudi, 2020). Manafa Capital, one of the market’s first and most well-known players, allows investors to search for and filter projects by specialty. When an attractive project is found, the investor can review the founders’ background information, including financial history, and contact them if interested. 1K SAR is the minimum investment amount. Scopeer, like Manafa Capital, is a pioneer in Saudi crowdfunding. Scopeer believes in an all-or-nothing approach. If a company fails to raise the required capital, contributions are returned to investors. Due diligence is performed by third-party vendors for the firm. They assist in determining a company’s management and system of laws before advertising a project (Reminskaya, 2020).

The approval of the two abovementioned crowdfunding platforms will facilitate the funding process of start-ups and other enterprises in Saudi Arabia. Thus, it is expected that these crowdfunding platforms will fill the financing gap and cover the minimum bank lending contribution, estimated at 2% in the SME sector in Saudi Arabia, which often compels young Saudi entrepreneurs to resort to their savings, friends and family to raise these funds (Alsaidlani, 2018). This has been confirmed by the Global Entrepreneurship Monitor (GEM, 2019), which has reported that about 35% of entrepreneurs in Saudi Arabia rely on their family to raise the required capital for their enterprises, underscoring the necessity of introducing new financing tools for young entrepreneurs.

To elaborate further, Figure 1 shows the different financing sources used by Saudi entrepreneurs to fund their enterprises (GEM, 2019).

Percentage of different financing sources in Saudi Arabia for entrepreneurs.

Figure 1 clearly shows that family members account for the highest percentage of entrepreneurial funding, confirming the dependence of young Saudi entrepreneurs on their family members more so than on other funding sources and therefore emphasizing the need for substitute financing sources, such as crowdfunding platforms.

Obtaining funding is challenging for entrepreneurs in general and for young entrepreneurs (qualified students) in particular regardless of how attractive their business idea is or the soundness of their business plan (Bernardino & Santos, 2020). Their difficulty accessing funds is primarily a consequence of a lack of required collateral or poor credit history, compelling them to rely on their social networks or family to obtain funding and preventing them from securing loans for their ventures (Jordan, 2018).

Therefore, allowing entrepreneurs in general and young entrepreneurs in particular to have easier access to funding through crowdfunding platforms reduces pressure on the Saudi government in offering them permanent jobs, stimulates economic growth, increases their trust and independence, and improves their standard of living. Young entrepreneurs, known collectively as millennials and Generation Z, are well positioned to take advantage of crowdfunding platforms and to play an important role in economic development by launching innovative ventures in specific markets (Bernardino & Santos, 2020). According to the GEM (2019), about 33% of entrepreneurs in Saudi Arabia have expressed their intention to start their businesses in the next 3 years, and 69.8% of early-stage entrepreneurs expect to create more job opportunities in the next 5 years.

The above discussion reveals the concerted efforts being made by the Saudi government and other official bodies to support SMEs and entrepreneurship. The discussion also highlighted the funding challenges being faced by young entrepreneurs in Saudi Arabia and the ways in which crowdfunding platforms can address these challenges. As a result, crowdfunding has been promoted as an alternative financing source for young Saudi entrepreneurs. Yet, the extant literature has only partially examined crowdfunding (e.g., Gazzaz, 2019) and has thus far not generated any empirical evidence concerning which factors are crucial to the success of crowdfunded ventures. In response, our study investigated the key factors responsible for influencing young Saudi entrepreneurs’ behavioral intention to use crowdfunding for fundraising.

This paper is organized into six sections. Following the introduction, the second section covers the theoretical background and hypotheses upon which the study was based. In the third section, the methodology for the study is described, while the following section covers the data analysis and interpretation. The last section of this work provides a discussion of the study findings and their implications and makes some general conclusions.

Theoretical Background

This study sought to examine the key factors responsible for influencing young Saudi entrepreneurs to raise funds for their venture via crowdfunding. Toward this end, the study applied the unified theory of acceptance and use of technology (UTAUT) model, originally developed by Venkatesh et al. (2003), and extended three other constructs—namely, trialability, perceived trust, and perceived risks—proposed by Islam and Khan (2021). The UTAUT was selected because it is considered one of the best technology acceptance models for thoroughly explaining user acceptance (Rosen, 2005).

Literature Review and Hypothesis Development

Performance Expectancy

Users of any system always expect it to provide a specific level of performance that will meet their needs—otherwise, they will be discouraged from using it. Concerning a crowdfunding platform, both users and investors expect a particular level of performance, one that will meet their requirements—if it fails to do so, then it will be rejected. Hence, in the context of the present study, performance expectancy refers to the degree to which a crowdfunding platform yields expected benefits in the view of those who use it (Venkatesh et al., 2003). Previous studies have reported conflicting results on the impact of performance expectancy on decisions made by investors to invest through crowdfunding platforms. For example, Kim and Jeon (2017), Lee et al. (2015), and Li et al. (2018) revealed a positive effect of performance expectancy on crowdfunding investors. However, Moon and Hwang (2018) observed opposite results. Generally speaking, performance expectancy determines whether one will decide to use a system (Venkatesh et al., 2003), such as entrepreneurs relying on crowdfunding platforms to fund their enterprises (Islam & Khan, 2021).

In our study, performance expectancy was employed to gage how quickly and effectively crowdfunding platforms generate funds for entrepreneurs. Therefore, we formulated the following hypothesis:

H1: Performance expectancy positively influences the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Effort Expectancy

The amount of effort needed to use any system is considered when deciding whether to use it. Users nearly always expect to expend less effort and achieve greater benefits from the use of a system. Effort expectancy is defined as the degree to which one is comfortable with using a system (Venkatesh et al., 2003) and involves the relative ease or difficulty of the system, its user-friendliness, its degree of simplicity or complexity, and its level of risk. In this study, the clarity and readability of instructions and the ease with which crowdfunding platforms can be used were considered effort expectancy. The extant literature has examined the role of effort expectancy in influencing one’s behavioral intention to use information technology systems and has reported significant positive findings (Aggelidis & Chatzoglou, 2009; Kim & Jeon, 2017; Li et al., 2018; Moon & Hwang, 2018). Systems that can be easily handled and managed can be expected to improve users’ performance, ultimately increasing their self-efficacy in using these systems (Bandura, 1982). Finally, Islam and Khan (2021) reported a significant positive connection between effort expectancy and the behavioral intention to use crowdfunding platforms in Pakistan. In view of this and based on the above discussion, we formulated the following hypothesis:

H2: Effort expectancy positively influences the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Social Influence

The concept of social influence is similar to that of subjective norms, which focus on the effects of others, such as friends, colleagues, relatives, and peers, on an individual’s behavior. Social influence is defined as how people believe others should use a new system (Venkatesh et al., 2003). In this research, social influence represented the extent to which young entrepreneurs were affected by other individuals when raising funds through crowdfunding platforms. Extant studies have reported that social networks and peers influence individuals to use information systems (Lu et al., 2005), as do acquaintances, family and friends (Mollick, 2014). Other studies that have specifically examined the effect of references on the use of crowdfunding also confirmed that friends play a crucial role in encouraging entrepreneurs to rely on crowdfunding to raise funds (Islam & Khan, 2021; Ordanini et al., 2011) and that peers influence backers to invest in crowdfunded projects (Kim & Jeon, 2017). It has thus been concluded that social influence should be considered when examining crowdfunding. Thus, we developed the following hypothesis:

H3: Social influence positively influences the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Facilitating Conditions

Venkatesh et al. (2003) defined facilitating conditions as the extent to which a person believes that an organizational and technical infrastructure exists to facilitate the system’s use. In this study, the facilitating conditions were represented by the available organizational and technological infrastructures necessary for enhancing crowdfunding platforms. Previous empirical studies have reported conflicting findings on this construct. For example, the study by Moon and Hwang (2018) reported no influence of facilitating conditions on the behavioral intention to use crowdfunding platforms. In contrast, the study by Islam and Khan (2021) revealed a significant effect on the same relationship. Other studies reported that social media could enhance the facilitating conditions of crowdfunding platforms by raising awareness among users (Gerber et al., 2012), while inadequate information about the fundraising process can hinder the development of crowdfunding (Kwon et al., 2014). The above review indicates an intriguing area in which to investigate the effect of facilitating conditions on the use of crowdfunding among young entrepreneurs in Saudi Arabia. Accordingly, we proposed the following hypothesis:

H4: Facilitating conditions positively influence the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Trialability

Trialability refers to attempts made to test existing or new processes, systems or ideas before deciding whether to use them. Those innovations that allow more opportunities to test them tend to be adopted more often (Moore & Benbasat, 1991). In our study, opportunities to use and become familiar with crowdfunding platforms were considered as their trialability. Previous research has demonstrated the significance of trialability in adopting new systems (Sahin & Thompson, 2006) and in determining the behavioral intention to use—and the actual use of—new information systems (Agarwal & Prasad, 1997). Still, Islam and Khan (2021) revealed that trialability has a negative relationship with behavioral intention. Therefore, and based on the above debate, the following hypothesis was developed:

H5: Trialability positively influences the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Perceived Trust

Perceived trust represents the level of faith an individual has in an entity when conducting an activity. From a crowdfunding point of view, perceived trust pertains to the beliefs entrepreneurs have about the reliability, integrity, appropriateness, and other characteristics of crowdfunding platforms. Those platforms possessing a high degree of integrity, security and stability positively influence entrepreneurs to use them (Lee & Brown, 2017; Lee et al., 2015; Li et al., 2018; Moon & Hwang, 2018). Platforms for which there is a lack trust in their operations tend to have a lower number of users (Gerber et al., 2012). Promoting trust on online platforms can be enhanced by installing firewalls, encrypting financial transactions and using authentication tools (Bhimani, 1996). Thus, investigating the relationship between perceived trust and the behavioral intention of young Saudi entrepreneurs is important, and the following hypothesis was formulated accordingly:

H6: Perceived trust positively influences the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Perceived Risks

Perceived risks refer to uncertainties among individuals about an item, product, process or technology before using it. In the domain of technology, perceived risks entail the possibility of loss in the pursuit of desired outcomes when using e-services (Featherman & Pavlou, 2003). These risks include financial risks, time risks, and privacy risks (Grewal et al., 1994). In our study, perceived risks included – but were not limited to—the imitation of a business plan and/or ideas, privacy risks, and the potential risk of disclosing financial transactions and related information. Previous studies have yielded divergent findings in this regard. For example, it has been found that perceived risks do not necessarily affect entrepreneurs’ behavioral intention (Islam & Khan, 2021), whereas negative influences of perceived risks on the behavioral intention to use crowdfunding have also been demonstrated (Lee & Brown, 2017; Moon & Hwang, 2018). In contrast, Kim and Jeon (2017) found that perceived risks did not have an adverse effect on investors’ intention to invest in crowdfunding projects, as such investments were minor. Therefore, it was considered valuable to investigate the connection between perceived risks and the behavioral intention of young entrepreneurs in Saudi Arabia. The following hypothesis was formulated accordingly:

H7: Perceived risks positively influence the behavioral intention of young entrepreneurs in Saudi Arabia to use crowdfunding platforms.

Behavioral Intention

According to Ajzen (2002), an individual develops the intention to perform a specific action based on three components: attitude toward the behavior, subjective norms and perceived behavioral control. In our study, behavioral intention was viewed in terms of the extent to which factors associated with crowdfunding affected young Saudi entrepreneurs’ intention to use crowdfunding platforms to raise funds for their enterprises, which in turn directly influenced their actual use of these platforms. The extant literature has reported that behavioral intention positively influences actual use of information technology (Oliveira et al., 2014). Hence, we formulated the following hypothesis:

H8: Young Saudi entrepreneurs’ behavioral intention to use crowdfunding platforms positively affects their actual use of crowdfunding platforms.

Methodology of the Study

Conceptual Model of the Study

Figure 2 depicts the study model and the constructs used in the study.

The hypothesized model.

Figure 2 also portrays factors that influence the behavioral intention of young Saudi entrepreneurs.

Participants and Data Collection

The study included a valid sample of 270 young entrepreneurs who were close to graduating from the Community College of Abqaiq, which is affiliated with King Faisal University, and who wished to start their small enterprises shortly thereafter with crowdfunding platforms as their funding source. The primary data were collected via a non-probability purposive sampling technique that employed an online questionnaire for data collection. Secondary information pertinent to the study was compiled from various sources. Before distributing the questionnaires, a pilot study was conducted with 15 young entrepreneurs to test the questionnaire’s validity and quality. As no issues arose from the pilot test, it was sent to the 270 young entrepreneurs constituting the sample and kept online for 1 month. The measurement items were scored with a 5-point Likert scale.

Measures of the Study

The questionnaire was adopted from the previous literature as it was considered suitable for meeting the current study objectives (see Table 1 for more details).

Sources for Measures Used in the Current Study.

Source. Author elaboration.

Table 1 also lists the sources for the measures used in the current study.

Data Analysis and Interpretation

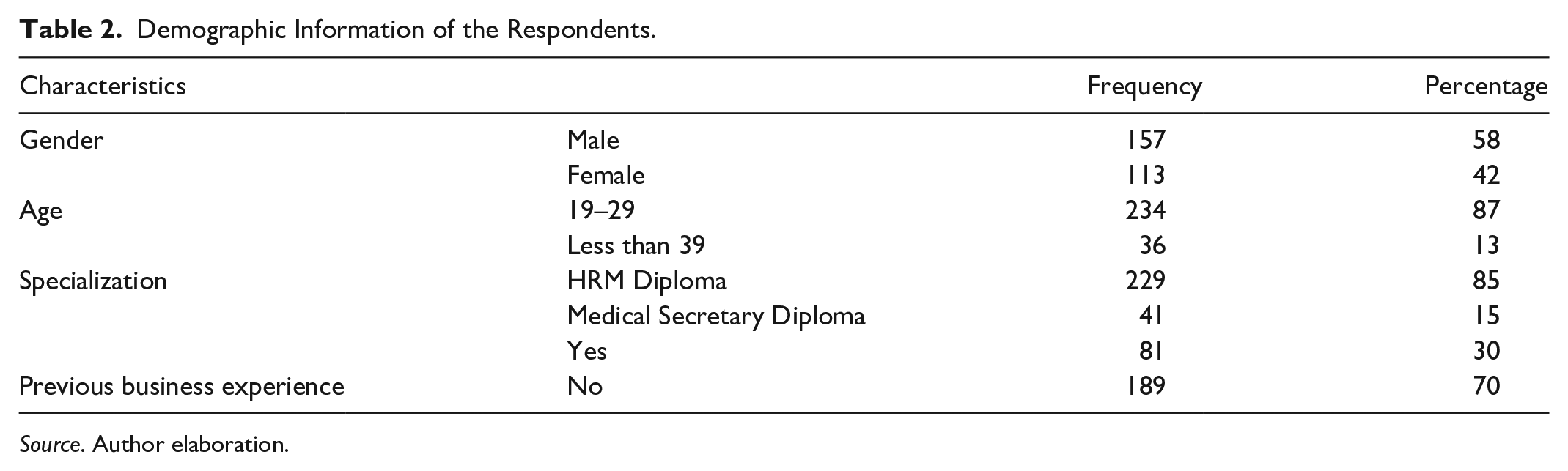

Table 2 provides the demographic information of the study respondents. Of the respondents, 58% were male, whereas 42% were female, indicating the inclination among women to start their own businesses in the future.

Demographic Information of the Respondents.

Source. Author elaboration.

Table 2 additionally shows that 87% of the respondents were between the age of 19 and 29, indicating that they were young enough to launch their business effectively. The respondents were also enrolled in one of two college programs: HRM and the medical secretary program. Finally, about 70% of the respondents did not have previous business experience.

Analysis of Measurement Model

The measurement model was employed to examine the reliability and validity of the constructs in order to ensure the accuracy of the items used in the study. Three tests were conducted to assess the study model, that is, its internal reliability, discriminant validity, and convergent validity (Hair et al., 2014). The outcomes of the three tests are provided in Table 3 below.

Measurement Model.

Source. Primary data.

Table 3 also gives the results for both the internal reliability and convergent validity of the study constructs.

Internal Reliability

Internal reliability was measured via Cronbach’s alpha and composite reliability (Fornell & Larcker, 1981). It has been recommended to have Cronbach’s alpha values and a composite reliability greater than .70 to demonstrate better reliability of the study constructs (Hair et al., 2017). As per the findings shown in Table 3 both Cronbach’s alpha and composite reliability met the recommended values, except for some constructs with a small number of items, as Cronbach’s alpha depends mainly on the number of items comprising the scale (Nunnally, 1978).

Convergent Validity

Convergent validity refers to the degree to which a measure relates to other measures of the same phenomenon or construct. The average variance extracted (AVE) and item loadings are two tests used to measure convergent validity. Each item used should have an outer loading value of at least 0.60 according to Chin (1998) and an AVE value of 0.50 or higher to ensure support for the study’s validity (Fornell & Larcker, 1981). Table 3 shows that the values of the item loadings and AVE corresponded to the recommended values.

Discriminant Validity

Discriminant validity was measured by two tests: cross-loadings and the square root of the AVE (Barclay et al., 1995). The recommended value for the square root of the AVE was greater than the correlation among the other constructs (Henseler et al., 2009). There is also another method for examining discriminant validity in a study, that is the Heterotrait-Monotrait Ratio (HTMT), which requires an acceptable number of research constructs to be smaller than 0.85 (Henseler et al., 2016). Table 4 lists the discriminant validity of the study items.

Cross-Loadings.

Source. Author elaboration depending on the primary data.

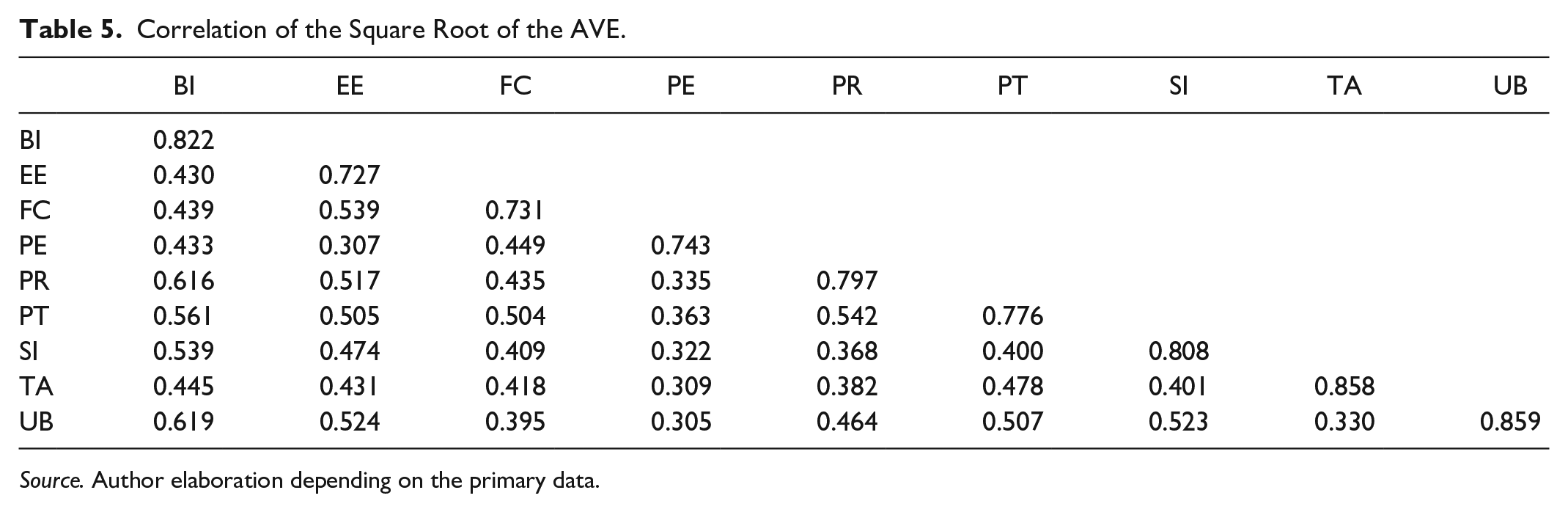

Table 4 specifically shows that the loadings of the items used in the study were more significant than their corresponding alternative correlations with other constructs. Hence, there was sufficient discriminant validity in the data. Furthermore, the second test used to measure discriminant validity was the square root of the AVE, the results of which are shown in Table 5 below.

Correlation of the Square Root of the AVE.

Source. Author elaboration depending on the primary data.

Table 5 indicates that the item loadings used in the study were higher than their corresponding alternative correlations with other constructs, thereby confirming suitable discriminant validity.

The third method used to examine discriminant validity was the HTMT, as shown in Table 6 below.

Correlation Matrix of the Heterotrait-Monotrait Ratio (HTMT).

Source. Author elaboration depending on the primary data.

According to Table 6, the ratios of all constructs employed in the study were less than the proposed value of 0.85, which also indicates sufficient discriminant validity of the study data.

Analysis of the Structural Model

The first step for analyzing the structural model involved conducting a lateral collinearity test, which applies in cases in which two variables measure the same construct. An examination of variance inflation factors (VIFs) is used to perform the test, and the results should be less than 5. Ideal values for not having collinearity should be about 3 or less. (Diamantopoulos & Siguaw, 2006).

According to Table 7, all of the values were less than 3, meaning there was no lateral multi-collinearity.

Collinearity Analysis.

Source. Primary data.

Results

Table 8 lists the results of the hypothesis testing of the study variables.

Hypothesis Testing.

Source. Primary data.

Table 8 shows that performance expectancy, social influence, perceived trust and perceived risks had a positive relationship with the behavioral intention of young Saudi entrepreneurs to use crowdfunding platforms to finance their enterprises. At the same time, effort expectancy, facilitating conditions and trialability had no significant impact on the behavioral intention of young Saudi entrepreneurs to use crowdfunding platforms. Further, Table 8 also indicates that the behavioral intention of the young Saudi entrepreneurs had a significant positive effect on their actual use of crowdfunding platforms. To summarize the results of the hypotheses, H1, H3, H6, H7, and H8 were supported, whereas H2, H4, and H5 were rejected. The model’s overall result indicated its ability to explain 55.4% of the variance in behavioral intention and 38.3% of the variance in use behavior. The model was considered substantive since it explained more than 10% of the variance in the endogenous variables (Falk & Miller, 1992). Figure 3 demonstrates the path coefficient of the study constructs.

The results of the path coefficients.

Discussion

This study investigated the key factors that influence young Saudi entrepreneurs’ behavioral intention to use crowdfunding platforms to finance their small enterprises. Therefore, the extended UTAUT model was used to achieve this objective. The findings of the study showed that some of the constructs and hypothesized relationships were accepted, whereas others were rejected, as elaborated below.

First,

Second,

The fourth construct,

Both

In conclusion, the relationship between the behavioral intention to use and the actual use, that is use behavior (H8), of crowdfunding platforms was confirmed to be both positive and significant (β = .619, p = .000), indicating that the behavioral intention to use crowdfunding platforms plays a crucial role in the actual use behavior of young Saudi entrepreneurs.

Implications of the Study

This research investigated crowdfunding platforms and their significance as an alternative financing source for young Saudi entrepreneurs. More precisely, the study examined the key factors that influence the behavioral intention of young Saudi entrepreneurs to use—and their actual use of—crowdfunding platforms. The results of the study have important implications for a variety of stakeholders. For example, the findings can be used to establish essential guidelines for future researchers in their investigations of different issues related to crowdfunding as well as other factors that may influence the decisions and intentions of entrepreneurs in Saudi Arabia with regard to crowdfunding. The study also provided an overview of the intentions of young Saudi entrepreneurs when using crowdfunding platforms to fund their enterprises.

The study also generated insights on the key factors that influence the behavioral intention to use and the actual use of crowdfunding platforms that could be of value to policymakers, entrepreneurs in general and young entrepreneurs in particular, as well as universities, research institutions, training programs and entrepreneurship centers. Accordingly, policymakers represented by the government of Saudi Arabia and the CMA are advised to focus on introducing and permitting various types of crowdfunding platforms to operate in the market after taking the necessary precautionary measures. Doing so will allow entrepreneurs to obtain funds from a pool of individuals worldwide instead of depending on traditional financial institutions, such as commercial banks, that demand collateral and entail lengthy procedures. Policymakers in Saudi Arabia should also direct their efforts toward addressing the factors identified in this study by ensuring that the available crowdfunding platforms deliver the expected results for entrepreneurs.

Policymakers should also ensure that the necessary infrastructure of the Fintech industry is publicly accessible in order to facilitate new crowdfunding platforms and other financing tools and for the purpose of raising awareness about the significance of crowdfunding for entrepreneurs. Universities should also introduce entrepreneurial education (Alshebami et al., 2020) and various financing sources into their syllabi and programs to cultivate the acquisition of knowledge of their benefits among young entrepreneurs. Universities should also coordinate with incubators to provide young entrepreneurs with the necessary training and knowledge about financing and small enterprises. Finally, existing crowdfunding platforms should consider the various factors presented in the current study to improve their processes and operations.

Conclusion

This study examined the key factors that affect the behavioral intention of young Saudi entrepreneurs to use crowdfunding platforms. The findings generated interesting results, particularly the confirmation that most of the constructs of the study model (crowdfunding model) predicted the behavioral intention of young entrepreneurs to use crowdfunding platforms. The findings also confirmed the validity of the UTAUT model in the context of Saudi Arabia. However, despite these compelling results, the study had some limitations, such as a limited sample size of students from a single university, which may limit its generalizability. Further, focus was placed on young entrepreneurs (qualified students), who often face more challenges and difficulties due to their limited business experience. Lastly, as the study employed an electronic questionnaire to collect data, it was not possible to address the individual concerns and perspectives of the respondents. As such, future research should include more constructs, a larger sample size and comparisons with other contexts, such as different countries or different institutions within a single country.

Footnotes

Author Contribution

The entire work is carried by the corresponding author only that is, Ali Saleh Alshebami.

Availability of Data and Materials

The datasets used during this study are available from the corresponding author on reasonable request. The data had been extracted from a questionnaires distributed to the students of community college of Abqaiq in king Faisal university. The sample totaled 270. It is available if needed in excel sheet.

Coding

SMART PLS.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by The Saudi Investment Bank Chair for Investment Awareness Studies, the Deanship of Scientific Research, The Vice Presidency for Graduate Studies and Scientific Research, King Faisal University, Saudi Arabia [Grant No. 58].

Ethical Approval

All procedures performed in studies involving human participants were under the institutional and national research committee’s ethical standards and the 1964 Helsinki declaration and its later amendments or comparable ethical standards.

Informed Consent

Informed consent was obtained from all individual participants included in the study.