Abstract

This article investigates the investment cash flow sensitivity (ICFS) and the effect of leverage on the firms’ ICFS by using data from 66 non-financial companies from Muscat Securities Market, Oman for a 7-year period from 2013 to 2019. We used a dynamic panel investment model based on the Euler equation approach and ran dynamic panel regressions using the dynamic panel system generalized method of moments (GMM). We run two regressions: first, testing the sensitivity of investment to the availability of the internal funds; second, testing the effect of firms’ leverage levels on the sensitivity of investment to cash flows. The results showed a significant sensitivity of investment to cash flows for the sample companies. The positive coefficient for the cash flow variable indicates the presence of financing constraints. The results showed that leverage has a significant effect on the ICFS of the companies, indicating that the companies with higher leverage have ICFS.

Introduction

It is commonly accepted in the finance literature that the primary responsibility, therefore the primary objective of the management is to maximize shareholders’ wealth, which depends on long-term and sustainable profitability. To this end, the company must maintain and/or improve its productive capacity by making investments. Investing and financing decisions are two important issues in financial management; choosing the project with higher returns and finding the financing sources with minimum cost. Even though investing and financing decisions are considered separate decisions from a project management perspective and in corporate finance, they are closely related. The separation of investing and financing decisions goes back to Modigliani and Miller (1958) claiming that there is no difference in the costs of internal and external sources of finance, though this proposition is based on unrealistic assumptions. From a practical point of view, the separation can be justified due to the economic return of the investment projects, and it should not be considered according to accounting profit. The availability of alternative financing options to the company is an important factor, whether the company has enough internal capital or whether it can raise external capital at a reasonable cost. The sensitivity of investments to the availability of internal capital and cash flows has attracted attention in academic and practical studies. The level of investments over periods is affected by the firm’s cash flows, which is known as investment-cash flow sensitivity (ICFS). There is extant literature about the factors affecting ICFS, including financial constraints, corporate governance, ownership structure, corporate social responsibility, and so on. Fazzari et al. (1988) conducted a study on ICFS, which marked a milestone in the discussion of investment sensitivities and internal capital sources. By using dividend payout as the proxy of financial constraints, they concluded that the firms with higher financial constraints have a stronger ICSF. In this study, we aim to investigate both ICFS and the effect of leverage on ICFS, by raising two research questions; the first question is about the significance of investment cash flow sensitivity for Omani companies, and the second question is about the effect of leverage levels of the companies on their investment cash flow sensitivities. The level of leverage has important implications having pros and cons. On one hand, a high level of leverage may increase the risk of bankruptcy and in turn, this may increase the investments’ sensitivity to the cash flows. On the other hand, the inclusion of debt in the capital structure plays a disciplining role for the firm’s management (Jensen, 1986). In addition, the level of leverage has an implication on ICSF regarding the firm’s ownership structure, which relates to agency theory and corporate governance. Therefore, the leverage is expected to have a moderating role on ICSF. The article attempts to investigate the relationship between cash flow and investments in a developing country, Oman. Previous studies mostly presented positive relationship by examining the cases in developed countries. Therefore it is important to contribute by using the data from a developing country. The article aims to explore whether Omani companies’ investments are sensitive to the availability of internal funds and whether leverage has a significant effect on this sensitivity. It has important practical implications for company managers in designing the short-term financial management policies by considering the impact of leverage level on investments. Since the development level of financial markets in emerging countries is different from that of developed countries, the evidence from an emerging market makes an important contribution to the literature.

The rest of the article is organized as follows; the next section provides a review of prior related literature. Section 3 gives the details about the methodology, data, and estimation method used. Section 4 presents the results of the analyses, including descriptive statistics and dynamic panel regression results. The last section presents findings and concludes.

Literature Review

One of the most important decisions faced by managers is investment decisions. Investments are of immense significance for the long-term sustainability and survival of the firm because the firm must maintain its productive capacity, even it must grow to increase and maximize the value. Two important topics in corporate finance literature relate to those decisions; capital budgeting and capital structure. Capital budgeting deals with the evaluation of potential projects to increase or renew the capacity. Capital structure is about the financing of the investments, more clearly about the composition of debt and equity on the right-hand side of the statement of financial position. It is commonly accepted in project evaluation methodologies that the investing and financing decisions are separate and independent of each other. However, the relationship between investment decisions and the availability of internal capital and/or the firm’s access to external sources of finance has attracted great attention in academic studies. In their irrelevance theory, Modigliani and Miller (1958) propose that costs of external and internal finance sources are identical and consequently capital structure does not have any effect on the valuation. The other theories developed later presented different explanations; pecking order theory claimed the internal capital should be of priority; trade-off theory emphasized the benefits and risks of external financing and claimed that the firm should target an optimum level of capital structure by considering the tax advantages and bankruptcy risks. In this context, it can be claimed that the availability of internal capital may affect the firm’s investment decisions, due to the several factors affecting the firm’s access to external finance. This is reasonable because external financing has some costs and the availability of internal resources may affect investment decisions (Shin & Stulz, 1998). In other words, the availability of internal cash flows affects both investing and financing decisions, an increase in internal cash flows results in higher capital expenditures or vice versa (J. Kim et al., 2013; Li & Tang, 2008). Fazzari et al. (1988) used the concept of investment-cash flow sensitivity referring to the dependence of investment on the internal capital. They found a stronger sensitivity for the firms with higher financial constraints by using the dividend payout ratio as the proxy. Many studies reported similar results in different contexts (Aggarwal & Zong, 2006; El Gaied, 2018; Lewellen & Lewellen, 2016; Mizen & Vermeulan, 2005; Mulier et al., 2016; Rashid & Jabeen, 2018; Schaller, 1993). The underlying reasons for the sensitivity could be based on agency problems (Jensen, 1986; Jensen & Meckling, 1976) or information asymmetries (Myers & Majluf, 1984). Degryse and De Jong (2006) examined the investment cash flow sensitivities for the public companies in the Netherlands, by pointing out two factors to which ICFS could be attributed as the abuse of managerial discretion and asymmetric information. They reported that high debt is associated with lower ICFS for the firms facing managerial discretion problem. A. A. Chen et al. (2013) emphasized the role of corporate governance mechanisms and the lack of effective monitoring of managerial discretion may lead to the significant relationship between investments and cash flow. Vengesai and Kwenda (2018) investigated the impact of leverage on discretionary investment by using the panel data of non-financial firms in Africa. The results of their study revealed that leverage constraints investment with a disciplinary role avoiding over-investment.

Kaplan and Zingales (1997) presented a conclusion that is the opposite of Fazzari et al. (1998), by reporting that the firms with financial constraints face lower ICFS by using different criteria to categorize firms as constrained and unconstrained. Some other studies also found similar results (Bhabra et al., 2018; H. Chen & Chen, 2012; Dasgupta et al., 2011; Hadlock & Pierce, 2010; Lyandres, 2007). Cleary (1999) concluded that the firms with high creditworthiness have more sensitivity of investment decisions to the internal fund availability. Further, Cleary (2006) showed that ICFS is higher for firms with stronger financial position and higher dividend payout ratio. T. N. Kim (2014) found a negative relationship that financially constrained firms to have lower ICFS, one of the determinants partially explaining this relationship is corporate cash holdings with a negative impact on ICFS. The author also finds that the high level of external financing is another determinant of low ICFS for financially constrained firms.

There might be several reasons for finding opposite results for the relationship between ICFS and financial constraints such as the disagreement on the criteria used to categorize firms as financially constraint or not (Bhabra et al., 2016; Mulier et al., 2016), measurement errors (Erickson & Whited, 2000), omitted variables that are potentially correlated (Moyen, 2004), firms with negative cash flows (Allayannis & Mozumdar, 2004).

As the debate has been going on about the determinants of ICFS, it is observed and reported by some studies that ICFS has a declining trend over the recent decades globally, especially in developed countries. Brown and Petersen (2009) observed a declining trend in ICFS over a long period from 1970 to 2006 and attributed it to the changes in the pattern of investments from physical investments to research & development (R&D) investments and development of equity markets. Some other studies found decreases in ICFS in different contexts and attributed to different factors such as decreases in agency costs (Pawlina & Renneboog, 2005), increases in cash holdings (Andrén & Jankensgård, 2015).

There are significant differences between developed countries and emerging countries at the firm level in terms of the investment behavior, asset tangibility (Ameer, 2014, Moshirian et al., 2017), and corporate governance mechanisms which may lower the dependence of the firms in emerging countries on internal funds (Francis et al., 2013). Country-level factors play a role in the relationship between ICFS and financial constraints, especially macroeconomic conditions. Those conditions may alter the debt-equity composition on the statement of financial position, by limiting the access to the financial markets (Levy, 2007), a tightening monetary policy may increase the liquidity constraints (Masuda, 2015), changes in exchange rates, credit demand, prices of assets, financial development level may affect financial constraints which in turn affect the firms’ investment decisions (Gupta & Mahakud, 2019). Danso et al. (2019) investigated the relationship between financial leverage and firm investment by considering the effect of information asymmetry level and growth by using the data of Indian firms. They found a negatively significant relationship for firms with high information asymmetry and with low-growth levels. Poursoleiman et al. (2020) examined the moderating role of short-term debt and financial constraints in the relationship between financial leverage and future investment by using the data of Iranian companies from 2006 to 2018. They found short-term debt moderates the relation between financial leverage and future investment negatively. Short-term debt decreases this relation by increasing default and maturity risk and mitigating agency conflict. Vo (2019) examined the relationship between financial leverage and corporate investment by using Vietnam companies’ data and found a negative relationship that is stronger for firms with high growth opportunities.

Firms having relatively high levels of leverage face an under-investment problem because they may encounter difficulties in finding new finance sources to undertake new projects. From the trade-off theory perspective, at low levels of leverage, the firm may benefit from tax advantages, however as the level of leverage increases, its costs including bankruptcy costs increase. In line with this, the increased leverage makes any incremental external finance more and more expensive. Therefore, the firms with higher (lower) leverage have higher (lower) investment cash flow sensitivities.

Hypotheses

Based on the discussion above, we develop two hypotheses:

Firstly, we aim to find out whether there is an investment cash flow sensitivity for the firms included in the sample.

H1: There is a significant investment cash flow sensitivity for sample firms.

Second, we aim to find out the effect of leverage on investment cash flow sensitivity.

H2: There is a significantly positive relationship between a firm’s leverage and its investment cash flow sensitivity.

Methodology

Data and Sample

The sample is composed of 66 non-financial companies traded at Muscat Securities Market of Oman. The details of sampling are given in Table 1. The data covers the 7-year period from 2013 to 2019 and is a balanced panel. The source of data is company reports which are obtained from Muscat Securities Market website.

Sampling Details.

Variables and Measurement

The variables used in the empirical model are defined in Table 2:

Variable Descriptions.

Model

There are several models which have been used to test the relationship between the firms’ investment and cash flows. The most commonly used of those models are the Euler equation model and the Q model. Both methods have been employed in many previous studies (Aggarwal & Zong, 2006; Allayannis & Mozumdar, 2004; Perotti & Gelfer, 2001; Shen & Wang, 2005). In this study, we use the Euler equation model; however, for comparison purposes, we provide a short overview of both models.

The Q model is based on Tobin’s Q ratio which is defined as the market value of a firm divided by the replacement cost of the firm’s assets. In other words, it is a ratio between the market value of the firm’s capital stock and the current replacement cost of that capital stock. (Tobin, 1969; Tobin & Brainard, 1968). The Q model of investment states that the investments of firms are essentially determined by the expectations about future profitable opportunities. Any investment project adding value to the firm’s market value more than its cost is considered as profitable. The Q ratio reflects the view of equity market participants who have a forward-looking perspective. Therefore, the firm’s investments are expected to be higher when the markets value the firm’s capital than the replacement cost of the capital (Bond & Meghir, 1994). This point of view reflects the valuation of a firm’s capital by current and potential investors; if the market’s valuation is higher than replacement cost, the investments will be higher. The Q model is based on the assumption of perfect markets, however, in the presence of imperfect markets with financing frictions, the investments are sensitive to internal cash flows (Hoshi et al., 1991). The Q model has been adjusted by the addition of the availability of internal funds which is an additional determinant of investment (Agca and Mozumdar, 2008; George et al., 2011). One of the drawbacks of the Q model is the fact that it reflects the evaluations by the parties outside the firm, and in the presence of information asymmetries in financial markets, those parties cannot evaluate the future investment opportunities as the insiders can do (Carpenter & Guariglia, 2008). Another issue with the Q model relates to the measurement problems. Marginal q, which is the marginal value of capital, is considered as a sufficient statistic that can explain the firm investment behavior (Hayashi, 1982), however, it is not directly observable.

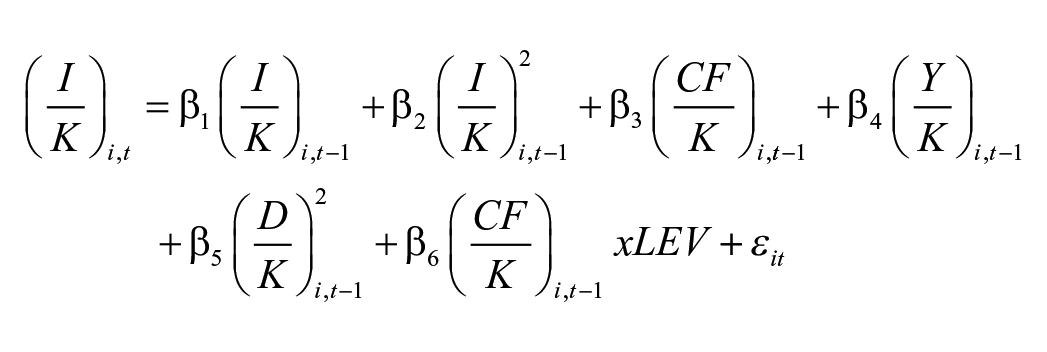

Due to the critics given above, some alternatives to Q model have been developed; the most important one is the Euler equation model. Since this model provides some advantages over Q model, it has been used in many previous studies (Gupta & Mahakud, 2019; Laeven, 2003; Tran & Le, 2017). It does not require the use of share prices and also linear homogeneity assumption for the net revenue function can be relaxed. Moreover, it exploits the relationship between investments in successive periods and does not require the explicit use of future values. The determinants of the firm’s investments are output (total sales), cash flows, investments in previous periods, and total debt. The Euler equation can be stated in linear form as follows (Bond & Meghir, 1994) and this is the first equation we test for ICSF.

Where I is net investment, K is capital stock at the beginning of the period, CF is cash flows Y is sales, and D is debt. Investment, cash flow, sales, and debt are stated relative to the capital stock (K).

The second equation aims to test the effect of leverage on ICSF.

LEV refers to leverage and is calculated as total debt divided by the sum of total debt and total equity. In the regressions, we worked on two alternatives ways; in one of them we used leverage as a ratio and in the other way, we used it as a dummy variable which takes a value of 1 if a firm’s average leverage ratio over the sample period is equal or greater than the median of all firms in the sample, otherwise takes a value of zero. We found more significant results for the alternative in which we used the median approach; therefore, we reported the results for that alternative.

All variables in the equations are scaled by the period’s capital stock, this acts as a control for heteroscedasticity arising from size differences.

Estimation Method

In this study, we employed a dynamic panel data model. Such models are better in the case of endogeneity. As explained in the methodology section, our model includes the first lag dependent variable and this makes the model a dynamic one but also causes endogeneity problem. Ordinary least squares (OLS) does not produce unbiased results due to its exogeneity assumptions. Another model used for panel data is fixed effects model, but in such models, those fixed effects may have a high correlation with the independent variables. Specifically, we used the generalized method of moments (GMM) system of estimators developed by Arellano and Bover (1995) and Blundell and Bond (2000). GMM estimators solve those problems, namely, they control for fixed effects by taking the first differences of the variables, and they also solve the problems heteroskedasticity and autocorrelation. GMM estimators handle the endogeneity problem. There are several types of GMM estimators, difference GMM and system GMM, both can be run as one-step or two-step estimation. In this study, we used system GMM with two-step estimation, which increases the efficiency of the results and the standard covariance matrix is robust to panel-specific autocorrelation and heteroskedasticity (Mileva, 2007). As a specification test, we performed Arellona-Bond AR(1) test and AR(2) test for the serial correlation in error terms. To test the validity of instruments, we used Sargan test of over-identifying restriction.

The Results of Analyses

Descriptive Statistics

Table 3 reports the descriptive statistics for all variables over the sample period including mean, standard deviation, minimum and maximum values.

Descriptive Statistics.

New investments as a percentage of current period capital stock (I/K) have an average of 11.8% overall, while 12.6% for the lagged variable. Compared to previous studies, the mean value of investments can be considered as low, Cleary (2006) reported a mean of 44% for French companies, A. A. Chen et al. (2013) reported a mean of 22% for Chinese companies, and D’Espallier and Guariglia (2015) reported a mean value of 18% for Belgian SMEs. Relatively low level of investments can be attributed to the fact that Oman is a developing country with newly developing financial markets. The overall mean value of Sales per current period’s capital stock (Y/K) is 15.3 times, and the overall mean value of Debt per current period’s capital stock (D/K) is 2.9 times. The leverage ratio has a mean of 29.1%. Mean leverage ratio can be considered as low compared to overall averages of non-financial companies around the world, this can be due to the development level of the financial system and also to the risk attitude of the managers.

Table 4 reports the mean values of investment-related variables and leverage ratio per year for the sample period. The mean of investments to capital stock (I/K) has a minimum of 9.7% in 2016 and a maximum of 12.8% in 2014; the overall trend can be described as stable. The mean of sales to capital (Y/K) stock has a minimum of 9.9 times in 2014 and a maximum of 25.8 times in 2016. The mean of debt to capital stock (D/K) has a minimum of 0.89 times in 2016 and a maximum of 7.07 times in 2017. Considering the overall mean of 2.9 in Table 3, the value in 2017 was a surge in the ratio, apart from these 2 years, the trend is stable. The mean of cash flow to capital stock (CF/K) has a minimum of 1.35 times and a maximum of 3.6 times. The mean value of leverage ratio has a minimum of 23.6% and a maximum of 33.4%, the sample companies have a moderate leverage ratio overall.

Mean Values of Investment Related Variables and Leverage per Year.

Regression Results

Table 5 presents the results for regression of investments on cash flows, which is according to Equation 1. The Wald statistics is significant indicating the overall, joint significance of all included variables in the model. AR(1) test shows that there is a first-order autocorrelation, but AR(2) test shows that there is no second-order autocorrelation. Sargan test shows that instruments are valid. The results showed that the coefficient of the lagged dependent variable is positive and significant; however, the coefficient of the squared lagged dependent variable is negative and significant. The significance of lagged investment implies a persistency in the companies’ investment decisions. The coefficient of sales variable is negative and significant. The coefficient of debt variable is positive and significant. The positive significant relationship between debt variable and investments implies that the companies increase borrowing to finance new investments. The coefficient of cash flow variable is positive and significant, implying some financing or liquidity constraints (Fazzari et al., 1988). This result may also suggest optimization problems regarding the use of free cash flows (Degryse & De Jong, 2006; Hines & Thaler, 1995). Except for the positive coefficient for debt variable and the negative coefficient for sales variable, the findings are consistent with those of previous studies (Bond & Meghir 1994; A. A. Chen et al., 2013, George et al., 2011). The negative coefficient for sales variable is an interesting result because it is normally expected that sales of the company is a source for the investments.

Regression of Investments on Cash Flows.

***: Significant at 1% level.

Table 6 reports the regression results based on Equation 2, created to find out the effect of leverage on ICFS. The Wald statistics shows that the overall model is fit and all included variables have joint significance. AR(1) test shows that there is a first-order autocorrelation, but AR(2) test shows that there is no second-order autocorrelation. Sargan test shows that instruments are valid. The effect of leverage is reflected by multiplying the lagged cash flow with a dummy variable based on the median of leverage ratios. The coefficient for this variable is positive and significant. This result indicates a higher ICFS for the companies with higher levels of leverage. From the perspective of classical trade-off theory, leverage has pros and cons. It increases risks such as bankruptcy risk; also it has advantages such as tax shields. However, when considered altogether, high levels of leverage make external finance riskier and more costly. The companies lacking sufficient amounts of internal funds may face under-investment or even zero investment. Thus, internal cash flow is critically important for companies with higher levels of leverage to continue a stable investment policy.

Regression for the Effect of Leverage on ICFS.

***: Significant at 1% level.

Conclusion

In this article, we aimed to investigate two questions by using the data of 66 Omani companies traded at Muscat Securities Market for a 7-year period from 2013 to 2019. The first question is whether there is significant investment cash flow sensitivity for the sample companies or not. The second question is whether the leverage levels of the companies have a significant effect on investment cash flow sensitivities. We employed a dynamic investment model based on the Euler equation and used the dynamic panel system GMM as the estimation method. The results showed that there is a significant sensitivity of investment to cash flows for the sample companies. The positive coefficient for the cash flow variable indicates financing constraints; this result is consistent with the findings of Fazzari et al. (1988). Guizani and Ajmi (2020) reported a similar result for the firms in Saudi Arabia and found that investment is strongly cash-sensitive, which reflects market imperfections in the stock exchange. Riaz et al. (2016) found significant investment cash-flow sensitivities for Pakistani firms, among others Makina and Wale (2016) in South Africa, and Gupta and Makahud (2019) in India. The results also showed that leverage has a significant effect on the investment cash flow sensitivities of the companies, indicating that the companies with higher levels of leverage have higher investment cash flow sensitivities. High leverage has some advantages and disadvantages for the companies, it may provide tax shields but also it increases bankruptcy risks. However, considering the pros and cons, high leverage may cause higher costs of external finance and decrease financial flexibility. Thus, such companies may face cases of under-investment or even zero investment.

The study has important practical and policy implications. Oman is a developing country with relatively less developed financial markets, which implies potential difficulties in firms’ access to external finance. In such contexts, high under-investment costs may arise as a result of those difficulties. This may have some policy implications for governments, especially for the economies with a significant portion of small and medium-sized companies in their non-financial sector. Government authorities may consider those factors in shaping their taxation policies, and for the incentives and supports given to the businesses. Significant investment-cash flow sensitivity implies that companies will experience a decrease in their investments in case they face problems in accessing external finance, consequently, this will affect the country’s economic growth. Therefore, policymakers must develop and implement policies that improve the firms’ efficiency and strengthen their capital at the micro level and the policies which improve the financial markets at the macro level.

The study has some limitations. It is conducted for a specific country for the 6-year period, future studies can be conducted by using data from multiples countries and for a longer period. In addition, we used yearly financial statement data, using quarterly data may increase the number of observations and may produce more robust results. In addition, our study used the data of non-financial companies from several sectors, and we did not focus on sectoral details, future research may consider sectoral characteristics and conduct analyses accordingly.

To the best of our knowledge, this is the first study investigating the effect of leverage on investment cash flow sensitivity for Oman companies. The study presents empirical evidence of the topic from an emerging country. The future research may investigate the topic on a regional basis such as GCC countries or MENA countries.

Footnotes

Acknowledgements

Not Applicable

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

An Ethics Statement

Not Applicable