Abstract

Smart wearable (SW) devices have attracted the users’ attention and their utility has been increasingly employed in different arenas of life. Of late, it is expected that wearable payments will be the norm of mobile payments soon. Recognizing the SW payments as an emerging innovation, this study investigates the consumers’ adoption of SW payments. A survey method was used to collect data from SW devices users in Saudi Arabia. For this purpose, online questionnaires were distributed and a total of 269 responses were received within that 243 operational cases were used for data analysis. Partial least squares structural equation modeling (PLS-SEM) technique was employed to analyze the data. The statistical tools employed for data analysis are SmartPLS 3.0 and SPSS23. The findings show that all hypothesized relationships were supported except the compatibility and perceived ease of use relationship which was found insignificant. Additionally, the moderating role of personal innovativeness on behavioral intention and actual use relationship was also confirmed. Although TAM is an established robust model of technology adoption, however, the integration of technological features like (perceived esthetics, compatibility, and convenience) make it a more vigorous model for adoption of the smart wearable device.

Introduction

With the worldwide availability of 4G and 5G broadband internet, users are attracted to use digital devices in every field of life. Due to the internet of things (IoT) and other distributed technologies, SW devices have pulled the users’ attention (Park, 2020). The swift proliferation of IoT provides the facility of digital payments beyond point-of-sale terminals, cards, and smartphones (Lee et al., 2020). The advancement of digital technologies has brought countless of SW devices such as smartwatches, fitness trackers, wristbands, rings, keychains, glasses, and jackets (Jee & Sohn, 2015). The SW devices have been increasingly employed in different fields of life like management, healthcare, communications, and sports (Park, 2020). According to CSS Insight (2018), shipments of SW devices will reach 9.6 million units in the year 2022 and its compound annual growth rate is 11% between 2017 and 2022.

The contactless payment method (made through smartwatches, wrist bands, or rings) that offer a faster, easier, and secure way for payment is referred to as wearable payment (Bezhovski, 2016). SW payment is like a mobile payment that allows the user to pay on the move (Lee et al., 2020). It is expected that soon SW payments will be the norm of mobile payments (Loh et al., 2019). The adoption of SW payments has been growing around the world (Infosys, 2018). SW payments will open avenues for new business prospects in many different products (Lee et al., 2020). However, the penetration rate of wearable payments in the market is still low (Jeong et al., 2017; Schumacher, 2018). The market of wearable payments was dominated by Europe in 2019 and it is expected that it would lead this position through 2020 to 2027 (Khan et al., 2020). Researchers’ attention is needed to focus on users’ adoption of wearable payments and explore the drivers of wearable payments adoption (Loh et al., 2019). Prior research in the context of wearable payments is limited and researchers have recommended further research to explore the factors that influence the users’ behavioral intention to use the SW payments and the actual use of SW payments (Lee et al., 2020; Loh et al., 2019).

To investigate the users’ adoption of SW payments, researchers have employed different models and theories like Unified Theory of Acceptance and Use of Technology (UTAUT), Technology Acceptance Model (TAM), fashion theory, technology readiness theory, and diffusion of innovation theory (Lee et al., 2020; Loh et al., 2019). The extant research in the context of wearable devices has examined the drivers of behavioral intention to use wearable technologies and have ignored the enclosure of actual use construct of TAM (Cheung et al., 2019; Hsiao & Chen, 2018; Lee et al., 2020; Li et al., 2019; Loh et al., 2019). To investigate the users’ adoption of SW payments, this study extends the TAM by incorporating the technological characteristics like perceived esthetics, compatibility, and convenience. Moreover, the moderating effects of personal innovativeness on the relationship between the behavioral intention and actual use are tested. The purpose of this study is to answer the following two research questions:

What are the important factors that affect the users’ adoption of SW payments?

What is the moderating role of personal innovativeness on the relationship between the behavioral intention and actual use of SW payments?

This research aims to examine the consumers’ adoption of SW payments. For this purpose, a sample of 269 respondents was collected from Saudi Arabia out of which 243 usable cases were used for data analysis.

This research contributes to SW technologies literature in many ways. First, this study integrates technological characteristics (perceived esthetics, compatibility, and convenience) to TAM and suggests a broader framework to describe the adoption of SW payments. According to Venkatesh et al. (2011), incorporating and testing different theories/models is vital for the advancement of science. Second, the validated model can help in determining the importance of determinants that can provide clear insights into the adoption of SW payments. Third, findings of the study present helpful insights to SW manufacturers to design more useful, pleasant, and successful SW payment solutions so that potential adopters can be attracted toward the use of SW payments. Fourth, the current study explored the moderating effects of personal innovativeness on the relationship between consumers’ behavioral intention and the actual use of SW payments. This contribution helps focus the less innovative individuals and prepare marketing strategies to convince them for acceptance of SW payments.

Rest of the paper is organized as follows. First, the background and development of the framework are discussed. A proposed model is presented and the corresponding hypotheses are developed based on a review of the prior research. Second, methodology, instrument development, sample collection, and data analysis are presented. Third, based on the results of data analysis, discussions, and conclusions are given. Fourth, theoretical and practical implications, limitations, and future research avenues are presented.

Background and Development of the Framework

SW Payments

The SW payments have added another layer of ease and convenience to mobile payments. SW device refers to any electronic device worn by the users that provides a specific service (Jeong et al., 2017). SW payment is referred to as the use of SW devices by users to buy products and services ubiquitously (Bezhovski, 2016; Lee et al., 2020). Technically, SW payments facilitate the users to pay on the move by using SW devices, thus making it similar to the notion of mobile payments (Liébana-Cabanillas et al., 2014). It is worthy to explore the emerging topic of SW payments which performs as the next generation of mobile payment (Lee et al., 2020). SW payments are becoming popular across Europe and there is eight times increase in wearable payments transactions in just 1 year and 10 countries (Netherlands, United Kingdom, Switzerland, Russia, Poland, Sweden, Czech Republic, Finland, Germany, and Ukraine) are the leaders in SW payments (Mastercard, 2019). Some popular payment systems which offer wearable payments are ApplePay, GooglePay, FitBit Pay, Garmin pay, and Samsung Pay (Borowski-Beszta & Polasik, 2020).

Researchers have investigated the users’ behaviors about the diffusion of SW devices and SW payments in numerous ways. Schmidthuber et al. (2020) investigated the acceptance of disruptive technologies like mobile payments by European customers and used an extended TAM. Their findings confirmed the significant effects of perceived risk, perceived usefulness, perceived compatibility, perceived personal innovativeness, and perceived social influence on intention to use mobile payments. Further, they have suggested to study digital payments in other cultural settings and other payment methods. Talwar et al. (2020) studied the continuance of mobile payments by collecting sample data from India and have posited that deeper research is needed to examine the reasons behind the surprising low acceptance of such digital payment methods. Yan et al. (2021) used an extended TAM model to explore the disruptive forces in retail specifically QR code and mobile payments in Malaysia. Their results showed the direct significant impacts of mobile usefulness, mobile ease of use, optimism, and personal innovativeness on behavioral intention. They recommended for future scholars to carry out research on NFC mobile payments. Loh et al. (2019) used mobile-TAM to investigate the role of wearable technology in a cashless society and confirmed that usefulness, ease of use, perceived financial cost, perceived risk, and mobile innovativeness are the direct antecedents of consumers’ intention to adopt wearable payments. Furthermore, mobile self-efficacy and mobile innovativeness are the predictors of perceived usefulness and perceived ease of use. Lee et al. (2020) investigated the consumers’ behavioral intention to use wearable payments by incorporating mobile-TAM and Technology Readiness Theory. Their findings confirmed the significant impacts of mobile usefulness, perceived esthetics, and technology readiness on behavioral intention to use wearable payments. Moreover, they have recommended that future research should investigate the actual usage of wearable payments.

Researchers have also employed extended versions of TAM namely TAM2 and TAM3. Jaradat and Faqih (2014) used TAM2 framework to study the mobile payment adoption in the context of Jordanian consumers. Their findings revealed that perceived usefulness, perceived ease of use, subjective norm, output quality, and result demonstrability are the direct antecedents of behavioral intention. In another similar study, Jaradat and Al-Mashaqba (2014) used TAM3 to study mobile payment services. They reported that subjective norm, perceived usefulness, perceived ease of use are the direct determinants of behavioral intention. Moreover, significant impacts of image and output quality were found on perceived usefulness while self-efficacy, and perceptions of external control exerted significant effects on perceived ease of use. Researchers have different approaches about the inclusion of the effects of trust and perceived risk on system use in the context of digital payments. Many studies have included these constructs in similar perspectives (de Kerviler et al., 2016; Loh et al., 2019; Schmidthuber et al., 2020) while others have not considered the inclusion of these variables (Elhajjar & Ouaida, 2019; Lee et al., 2020; Yan et al., 2021). In our study, we are of the view that the customers who intend to adopt SW payments have already tested other forms of digital payments (like mobile banking, etc.) due to which their trust has been established in the banking channel and the associated infrastructure due to which they are not worried about the security of their information, therefore, the trust and risk factors have not been incorporated.

Despite several revisions to TAM, still it is popular among the scholars due to its characteristics like rigorous, solid, and dominant model in the context of technology acceptance behavior (de Luna et al., 2019). The most important objective of TAM is to foresee the adoption behaviors of users regarding innovative technologies and ascertain the possible concerns regarding the design of information systems (Yi et al., 2006). One of the main criticism on TAM is that it provides very generic information about individuals’ perceptions and adoption of technology (Patil et al., 2020). In spite of having many strengths, TAM has certain limitations also. According to Chuttur (2009), TAM does not evaluate the causes that measure perceived usefulness and perceived ease of use. However, TAM is the most widely used model by scholars to examine the acceptance of innovative technologies in pre-adoption stage (Leong et al., 2013; Yi et al., 2006). Future studies will build models by exploiting the strengths of TAM and eliminating its limitations (Chuttur, 2009). Although, our model is mainly based on TAM, but for further improvement and to adapt the model more appropriate for SW payments context, it was crucial to incorporate additional constructs to make its explanation capacity more precise in the context of SW payments acceptance behavior (Zhong et al., 2021). Thus, after sufficient deliberation, this research employed TAM as the base model by incorporating some additional variables to overcome the shortcomings of TAM.

The SW payments are still in the infancy stage and previous studies on the adoption of SW payments are limited. Based on the above discussion and to fill the research gap, this study employs TAM as the core contributing theory and proposes a model for the adoption of SW payments by incorporating technological characteristics like perceived esthetics, compatibility, and convenience to TAM. The moderating effects of individual characteristic “Personal Innovativeness” are tested on the relationship between behavioral intention to use SW payments and actual use of SW Payments.

Technology Acceptance Model (TAM)

The TAM was proposed by Davis (1989) and it is the most extensively employed model to study the user acceptance of digital technologies. TAM posits that perceived usefulness and perceived ease of use determine the users’ attitudes toward system use which in turn influence their intentions to use a system. The intention to use the system mediates the relationship between the attitude toward systems use and the actual use (Davis, 1989). According to TAM, if an innovation improves the performance of users, it is believed useful, and it will be more likely adopted by the users (Le, 2021). TAM is an appropriate model for assessment of the consumers’ behaviors in the contexts of Fintech and digital payments (Daragmeh et al., 2021). To and Trinh (2021) has recommended to include more variables to TAM due to the lack of diversity of constructs to explain the users’ intention.

The explanatory power of TAM has been validated by several studies on user’s adoption of mobile technologies and services including mobile banking (Elhajjar & Ouaida, 2019; Koenig-Lewis et al., 2010), e-books reading (Jin, 2014), smartphones (Joo & Sang, 2013), mobile cloud computing (Park & Kim, 2014), and wearable technologies (Chau et al., 2019; Ho et al., 2020; Park, 2020; Schmidthuber et al., 2020). Elhajjar and Ouaida (2019) used TAM to explore the factors affecting adoption of mobile banking and integrated seven constructs namely digital literacy, resistance, perception of risk, compatibility, awareness, subjective norm, and personal innovativeness. Subjective norm and personal innovativeness were taken as moderators. The effects of compatibility on perceived ease of use, awareness on perceived usefulness, and perceived usefulness on attitude were found insignificant while all other paths were found significant. To examine the role of wearable technologies in a cashless society, Loh et al. (2019) incorporated mobile self-efficacy, mobile innovativeness, perceived financial cost, and perceived risk to TAM. They found direct impacts of perceived financial cost and perceived risk on intention to adopt wearable payments and indirect impacts of mobile self-efficacy and mobile innovativeness on intention to adopt wearable payments. Lee et al. (2020) also combined fashion theory and technology readiness theory to TAM to investigate wearable payments. Their findings confirmed insignificant impacts of mobile ease of use on behavioral intention which is contrary to the outcomes of other studies. Daragmeh et al. (2021) studied the factors to influence the behavioral intention to adopt Fintech payments in the COVID-19 era. They added subjective norm and perceived COVID-19 risk constructs to TAM. They found significant direct impacts of perceived COVID-19 risk on behavioral intention while direct and indirect impacts of subjective norm were found on behavioral intention. To investigate the behavioral intention to use mobile wallets in Vietnam, To and Trinh (2021) incorporated trust and enjoyment factors to TAM. They made slight changes to TAM relationships by omitting the relationship between perceived ease of use and perceived usefulness. They found direct and indirect impacts of trust and enjoyment on behavioral intention while direct effects of perceived usefulness and perceived ease of use on behavioral intention were confirmed. Based on the findings and arguments of these studies given above in section 2.1, this study considers the TAM as the base model and incorporates technological characteristics (perceived esthetics, compatibility, and convenience) to TAM as most of the prior studies have suggested that only the perceived usefulness and perceived ease of use are not sufficient to explain the users’ intention to use and the actual use of innovative technology (Daragmeh et al., 2021; Loh et al., 2019). The “Attitude toward Use” construct of TAM is excluded because this study is focusing on the adoption of SW payments for which the actual use is a more appropriate measure of the innovative technology adoption.

Conceptual Framework and Development of Hypotheses

Perceived ease of use

In the context of this study, the perceived ease of use (PEU) refers to the extent of ease perceived by the user in learning and using the SW payments (Loh et al., 2019). To study the role of wearable technology in a cashless society, Loh et al. (2019) employed TAM model and confirmed significant impacts of PEU on both PU and behavioral intention (BI) to adopt wearable payments. Giovanis et al. (2021) examined mobile payments and showed that PEU has significant impacts on both PU and BI. Similar results were corroborated by other scholars pertaining to digital payments (Williams, 2021). In this study, we assume if an SW payment will be easier to use and minimum effort will be needed to learn and use the SW payments, the users will perceive the device more useful and hence they will intend to use it. Hence, we propose the first hypothesis:

Perceived usefulness

Deriving from TAM, perceived usefulness (PU) refers to the extent a user believes that the use of a particular technology will enhance his/her job performance (Davis, 1989). In this study, PU means the degree that a user believes that using SW payments enhances his/her performance. The individual’s intention to use technology is influenced significantly by the individual’s perceptions of usefulness of the technology (Davis, 1989). In the context of wearable payments, Lee et al. (2020) ascertained that PU has significant relationship with BI. Daragmeh et al. (2021) investigated FinTech payments in the era of COVID-19 and reported that PU has significant influences on BI. Similar outcomes were presented by Yan et al. (2021). The users will critically evaluate the SW payments and if they find it more useful in comparison with the prevailing payment methods, they will intend to use it (Shankar & Datta, 2018). Hence, we frame the second hypothesis:

Behavioral intention (BI), actual use (AU)

In the TAM model, the combined impacts of users’ behavioral beliefs like the ease of use and perceived usefulness determine the users’ attitude toward technology (Davis, 1989). In UTAUT, the behavioral intention is the antecedent of “use behavior” (Venkatesh et al., 2003). Moreover, the Delone and McLean (2003) IS success model posits the “use behavior” as a measure of success of the system. Previous research has confirmed the significant impacts of behavioral intention on actual use (Dehghani et al., 2018). The collaborative responses of SW devices can be configured, changed, or controlled according to the intention of the user and this interaction enhances the experience and ability of the user to utilize the SW devices (Turhan, 2013). Penney et al. (2021) investigated the factors influencing consumers’ intention to use mobile money services and confirmed significant impacts of behavioral intention on use behavior. Based on these facts, this study assumes that a stronger behavioral intention to use SW devices leads the user toward the “actual use” behavior. Therefore, we frame the third hypothesis:

Perceived esthetics

Perceived esthetics (PA) refers to the extent of the user’s perceptions about fashion or style (Nam et al., 2007). In this study, PA refers to the user’s perceptions about the visual design and beauty of the SW device interface. The wearable devices are in the early stages of adoption, therefore, product design and esthetics can be important functions for acceptance (Chuah et al., 2016). Dehghani et al. (2018) explored the factors influencing the intention to use smart wearable technology. Their results confirmed that esthetic appeal is positively related to continuous intention and usage. Studying the effects of design esthetics on intention to use mobile banking, Chaouali et al. (2019) showed that design esthetics have significant relationships with perceived usefulness and trust. Lee et al. (2020) examined the factors influencing consumers’ behavioral intention to use wearable payment. They found that PA has significant effects on both perceived usefulness and perceived ease of use. Based on the above discussion, we assume the direct positive impacts of the PA on both perceived usefulness and perceived ease of use. Therefore, we frame the fourth hypothesis:

Compatibility (Comp)

The diffusion of Innovation Theory (DIT) proposed by Rogers (1995) posits that compatibility is one of the major factors of information systems (IS) adoption. According to DIT, compatibility refers to the users’ beliefs that the innovation is consistent with their lifestyle, beliefs, experience, existing values, and needs (Rogers, 1995). Higher levels of compatibility lead to the preferable espousal of innovation (Cheng, 2015). Giovanis et al. (2021) examined the adoption of mobile payments by employing decomposed theory of planned behavior and revealed significant relationship between compatibility and perceived usefulness. Li et al. (2019) investigated the health monitoring of older adults through wearable technologies and presented significant impacts of compatibility on perceived usefulness and perceived ease of use. Elhajjar and Ouaida (2019) analyzed the factors that affect the adoption of mobile banking and their findings exhibited significant relationship between compatibility and perceived usefulness while the relationship between compatibility and perceived ease of use was insignificant. In examining the factors affecting the intention to use smartwatches, Choi and Kim (2016) showed that compatibility has significant relationships with perceived usefulness and perceived ease of use. Keeping in view the above findings of prior research, we expect significant effects of compatibility on perceived usefulness and perceived ease of use in our proposed model. Thus, we hypothesize:

Convenience

Convenience refers to the extent to which the user perceives the innovative technology convenience and easy in terms of saving effort and time (Brown, 1990). Yoon and Kim (2007) defined convenience as the degree to which a user perceives that he/she can use the technology to complete his/her work in a convenient way, at a convenient time, and in a convenient place. A product or service is considered convenient if it lessens the physical, cognitive, and emotional burden of the user (Chang et al., 2012). Based on these definitions, this study defines convenience as the degree to which the users perceive that they can complete SW payments conveniently in terms of time and place and in a convenient way of execution. Williams (2021) studied the payment and security perception of users in the context of mobile platforms and revealed that convenience has direct significant impacts on intention to use. They also established that convenience moderates the relationship between PU and BI. Another study made by Mokhtar et al. (2018) in the context of learning management systems confirmed the significant effects of convenience both on PU and PEU. Similarly, Hidayat-ur-Rehman et al. (2020) established significant relationship between convenience and PU. Based on the above definitions and findings of the prior research, this study proposes that convenience has a positive influence on perceived usefulness and perceived ease of use. The user’s perceptions about usefulness and ease of use of the technology are enhanced if the user can use SW payments at any time and place and the way of SW payments is convenient. Thus, we hypothesize:

Moderating effects of personal innovativeness

Personal Innovativeness (PI) is a user-specific characteristic that refers to the extent an individual is willing to try out new technology (Agarwal & Prasad, 1998). Individuals having higher PI can deal with higher levels of challenges, and have a higher propensity to adopt the new technology even if they have little proficiency about the technology (Cheung et al., 2019; Schmidthuber et al., 2020). The higher is the innovative level of the consumer, the higher is the tendency to know the benefits of the innovation (Talukder et al., 2019). PI has been identified as a critical personal trait that affects the consumer’s intention to adopt new technology (Hirschman, 1980). Previous studies in the context of mobile payment and wearable technologies indicate that PI as one of the important determinants of consumers’ intention to use the technology or service (Cheung et al., 2019; Loh et al., 2019; Schmidthuber et al., 2020). Williams (2021) investigated the mobile payments and security perceptions of consumers and revealed that PI moderated the PU → BI and Trust → BI relationships. Since the SW payment is relatively new and the existing users are the early adopters, therefore the PI role may be significant in adoption and actual use of SW payments. Thus, this study proposes that PI moderates the relationship between behavioral intention to use SW payments and the actual use of SW payments such that the relationship is stronger for consumers with more PI and vice versa. Hence, we hypothesize:

Proposed model of the study is depicted in Figure 1 below.

Proposed model of the study.

Research Methodology

Instrument Development

To validate the proposed model, this study used a survey method to collect data. Measurement items of the survey were adapted from well-established prior researches in the context of wearable payments, mobile applications and mobile banking and minor modifications were made according to the context of this research. The survey contained a total of 27 items. Initially, a sample of 39 was used to carry out a pilot study. Upon satisfactory results of the pilot study, the questionnaires were distributed for data collection. The study employs the Likert scales (1–5) ranging from “Strongly Disagree” to “Strongly Agree” were used for all items. Appendix covers the measurement items of this study.

Data Collection and Sample

The survey was distributed online and data was collected from respondents in Saudi Arabia. Keeping in view the research objectives, a random sampling technique was used. First, four big cities of Saudi Arabia namely Riyadh, Dammam, Jeddah, and Madinah were selected keeping in view difficulties in access to all geographical areas within the country due to COVID-19 pandemic. Then the questionnaires were randomly administered to respondents in these cities. As the focus of this study is on the drivers of SW payments, therefore a screening question was asked at the beginning of the survey “Do you use any smart wearable device?” The purpose was to accept data from such respondents who are using any wearable device.

A total number of 269 filled questionnaires were received. During the data screening phase, 21 responses were discarded due to no experience of using wearable devices and 5 responses were deleted due to missing data. Thus the study carried out 243 responses for data analysis. Table 1 below lists demographic information of the respondents.

Demographic Information of the Sample.

Data Analysis and Results

The proposed model was tested through PLS-SEM method. SmartPLS 3.2.7 and SPSS 23 tools were used to analyze our data. To proceed PLS-SEM, measurement model’s reliability and validity were assessed followed by a structural model assessment.

Assessment of measurement model

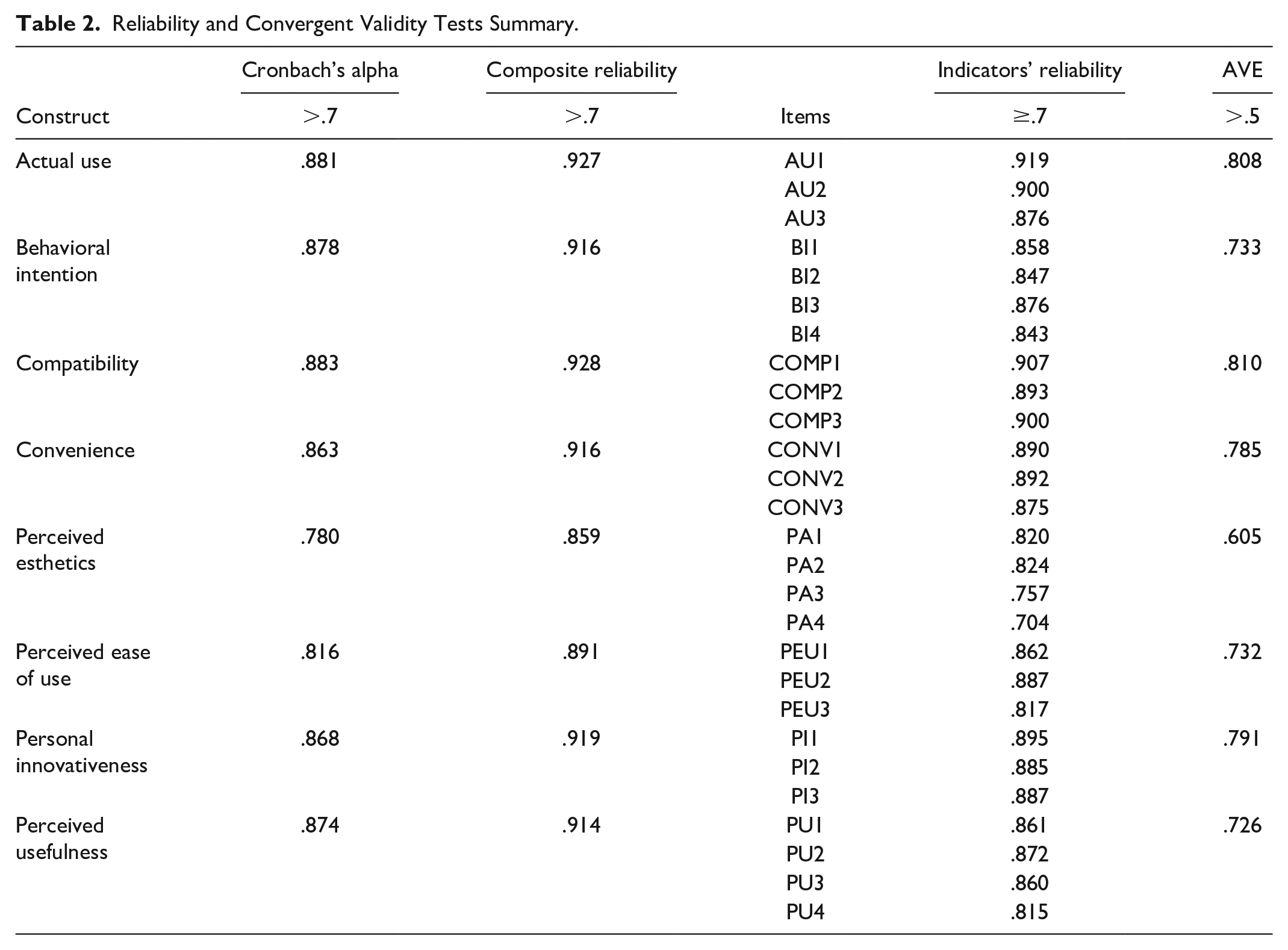

For assessment of the measurement model, the tests about reliability and validity were conducted as recommended by Hair et al. (2017). Internal Consistency Reliability, Composite Reliability and Indicator Reliability were examined to check the reliability while Convergent Validity and Discriminant Validity tests were examined to assess the validity. Cronbach’s alpha >.7 criteria was used to evaluate internal consistency reliability and the threshold value for composite reliability and indicators’ reliability is >.7. Table 2 lists the results of reliability and convergent validity. Values of internal consistency reliability (Cronbach’s alpha), composite reliability and indicator reliability are greater than the threshold values. For indicators’ reliability, the outer loadings were examined. One measurement item PA5 was removed for further analysis as its outer loading value was found 0.327 which was not fulfilling the indicators’ reliability criteria. The last column in Table 2 shows the AVE (average variance extracted) values. All AVE values are greater than .5 that indicates the existence of convergent validity.

Reliability and Convergent Validity Tests Summary.

To examine the discriminant validity, we assessed the Fornell-Lacker’s Criterion and Heterotrait-Monotrait Ratio (HTMT). Table 3 below lists results of Fornell-Lacker’s Criterion. The diagonal elements are the square roots of the AVEs of the constructs. It is evident from these findings that each diagonal element is greater than its corresponding correlations with other constructs. It shows the existence of discriminant validity. Table 4 depicts the HTMT results. All the HTMT value between any two constructs are less than 0.9 as suggested by Henseler et al. (2015). It also confirms that discriminant validity is established.

Discriminant Validity (Fornell-Lacker’s Criterion).

Discriminant Validity (HTMT).

Common method bias

The Common Method Bias (CMB) is a bias triggered due to the use of the same source (like a survey) to collect data about independent and dependent variables. According to Podsakoff et al. (2003), the CMB occurs if amongst the variables most of the variance is explained by a single factor. Harman’s single-factor test was conducted to assess the CMB. The test results exhibited that a single factor explains 37% of the variance, which is far below 50%, and thus the CMB does not exist. Furthermore, a full collinearity test was carried out to examine the CMB. All Variance Inflation Factor (VIF) values of the latent variables were found less than the threshold value 3.3 as recommended by Kock and Lynn (2012). These results indicate that CMB does not exist in our data.

Values of model fitness

To investigate the capability of the measurement model to portray the surveyed data, we assessed the model fit indices namely standard root means square residual (SRMR), the normed fit index (NFI), and the root mean squared residual covariance matrix of the outer model residuals (RMS_theta). The SRMR value is 0.055 which is less than 0.10 indicating a good model fit (Hair et al., 2017). The NFI value is 0.879 which is very near to the threshold value (>0.9). The RMS_theta is .131 which is slightly higher than then the threshold (<.12). Thus, these values indicate that the measurement model fits to the observed data.

Structural model analysis

Before the structural model assessment, to evaluate the Coefficient of Determination (R2), the PLS algorithm was administered with standard settings. The R2 value for Perceived Usefulness, Perceived Ease of Use, Behavioral Intention, and Actual Use are .459, .468, .484, and .405, respectively. The R2 values for behavioral intention to use and actual use are slightly less than .5. The main reason is that very few paths are pointing toward these variables due to which the R2 values of the two target variables are small (Hair et al., 2017, p. 199). These findings show that the conceptual model has a satisfactory explanatory power to describe the behavioral intention to use and the actual use of SW payments.

To assess the proposed hypotheses, 5,000 bootstrap subsamples were used by applying a bootstrapping procedure. Other settings set were “No Sign Change,” “Bias Corrected and Accelerated Bootstrap,” and “Two-Tailed Test Type.” The relevant path coefficients with corresponding p and t values were evaluated in order to appraise the significance of the relationships. Hypotheses testing results are presented in Table 5. Figure 2 below shows the results of hypotheses testing. According to Table 5 results, all the hypothesized paths excluding COMP → PEU (H5b) are supported with a minimum significance level of p < .1.

Summary of Structural Model Path Coefficients.

Note. NS = not significant.

p < .1. **p < .05. ***p < .01.

SEM analysis of conceptual model.

The PEU has significant effects on PU (β = .199, p < .05) and BI (β = .399, p < .01) thus supporting hypotheses H1a and H1b. The impacts of PU on BI are significant (β = .392, p < .01) which supports hypothesis H2. The relationship between BI and AU is significant that confirms hypothesis H3. The effects of PA on PU (β = .196, p < .05) and PEU (β = .388, p < .01) are significant and thus hypotheses H4a and H4b are sustained. The next significant relationship COMP → PU (β = .246, p < .01) supported hypothesis H5a while H5b (β = .067, p > .1) is not supported by our results. Our hypotheses H6a and H6b proposed significant impacts of convenience on both PU and PEU. Outcomes of analysis provided support for these hypotheses H6a (β = .219, p < .01) and H6b (β = .356, p < .01).

In brief, empirical results provided support for ten hypothesized relationships except for the path COMP → PEU and thus validated our proposed model. It indicates that the compatibility of SW payments affects the consumers’ perceptions about usefulness while their perceptions of ease of use are not affected even if they find the SW payments highly compatible. Moreover, the validated model has a reasonable depiction strength to describe the users’ intention to use the actual use of SW payments.

Predictive relevance (Q2)

Stone-Geisser’s Q2 value is estimated in order to find the predictive relevance of the model. This indicator helps in understanding whether the indicators in a reflective model correctly predict an endogenous construct. To evaluate Q2 value, we employed blindfolding procedure keeping an omission distance of 7. Q2 values for all endogenous constructs PU (0.326), PEU (0.333), BI (0.350), and AU (0.286) were found larger than zero which indicate the predictive relevance of the model (Hair et al., 2017).

Moderating effects

This study hypothesized in H7 that the BI → AU relationship is moderated by PI such that the relationship is stronger for higher values of PI and vice versa. Our findings indicate significant positive effects of PI on AU (β = .390, p < .01). The interaction effect of BI and PI on AU is (β = .393, p < .01) which indicate that the relationship BI → AU is dependent on the PI. The path coefficient between BI and AU is β = .482. It is inferred by the results that the strength of BI → AU relationship is .482 for an average value of PI. The BI → AU relationship is strengthened equal to the magnitude of the interaction term (.482 + .393) when PI has higher values. Thus, we conclude that higher values of PI strengthen the BI → AU relationship while lower values of PI weaken this relationship. Figure 3 depicts the interaction slope. The upper line has a steeper slope which shows the higher level of PI while the lower line has a flatter slope showing the lower level of PI. Since the interaction term is positive, so this is plausible. These findings reveal evidence for the moderating effect of PI and thus confirms our hypothesis H7.

Moderating effect of perceived innovativeness (PI) on the relationship between behavioral intention (BI) and actual use (AU).

Theoretical and Managerial Implications

The study has made a significant contribution to the research community, as wearable devices are gaining attention among global populace. The study explored the critical factors influencing the research outcome, recommended its role in users’ perceptions and experience, and emphasized consumers’ acceptance of technology.

The theoretical and practical contribution of the research has been corroborated scientifically. The scientific model has been formulated to discuss the consumers’ intention to adopt smart wearable payments R2 = .484 and actual use R2 = .405. The study has tested the moderating effects of personal innovativeness on the relationship between behavioral intention and actual use. The findings validated that personal innovativeness does not directly impact the actual use of smart wearable payments. Still, it strengthens the behavioral intention and actual use relationship for higher values of personal innovativeness and vice versa.

Theoretically, this study contributes in two main perspectives. First, although TAM is an established robust model of technology adoption, our findings indicate that only the PU and PEU are not enough to explain the adoption of wearable technologies and the integration of technological features like (perceived esthetics, compatibility, and convenience) make it a more vigorous model for adoption of the smart wearable device. Second, the personal innovativeness characteristic is an important antecedent of the actual use of the technology and it affects the relationship between intention and actual use. This result is according to expectations as it makes sense that consumers who are passionate towards new technologies are more likely to adopt SW payments. The uniqueness of this study lies in examining the actual use behavior in the context of SW payments and analyzing the moderating role of personal innovativeness on the relationship of behavioral intention and the actual use behavior.

The research findings have established perceived esthetics as a central factor to describe the use of technology and ease perceived by the user in learning and using the payments. The result indicates that the esthetic feature of payments is essential for users. It is proved in the research that users’ perceptions of usefulness and ease of use positively influence users’ behavioral intention if the interface of the payments is esthetically designed.

The study has scientifically proven that visual design, the beauty of the SW device, and fashion style have critical impacts on users’ perceptions. The manufacturers should pay special attention to the esthetic feature while manufacturing SW devices for payments. This study demonstrates compatibility as a salient factor influencing PU, but the study did not confirm its significant impacts on PEU. These findings are consistent with prior research (Elhajjar & Ouaida, 2019) while differing with (Choi & Kim, 2016; Li et al., 2019). Similarly, results confirmed significant impacts of convenience on PU and PEU as prior research supports these results (Zhang et al., 2017). Findings prove that if the users find the SW payments compatible and convenient, they perceive it valuable and easy to use and they intend to use. It implies that the SW devices should have compatibility with the lifestyle and existing values like other innovative communication technologies. Since the users are concerned about the compatibility and convenience features of SW devices, therefore the manufacturers should consider these features while manufacturing SW devices for payments. Our results also suggest that the wearable devices for payments should be prepared very easy to use so that users (even with little or no user experience) can easily use the SW payments. The boost in their perceptions about ease of use will enhance their perceptions about the usefulness of SW devices and will significantly impact their intention to use. These findings are supported by prior studies (Chuah et al., 2016; Lee et al., 2020; Loh et al., 2019). These findings suggest that practitioners emphasize design (esthetics), engineering (technological features), and cognitive features to provide a pleasant and valuable user experience.

The study has a significant contribution and plays a critical role in the existing knowledge. It reinforces the original Technology Acceptance Model, extends the depth of the literature on wearable technologies, and provides applied research references.

The findings addressed that the degree that a user believes that using smart wearable payments enhances their performance and the extent of ease perceived in learning and using the payments are not adequate to clarify the adoption of wearable technologies and the integration of technological features. For example, perceived esthetics, compatibility, and convenience make it a more vigorous model for adopting the smart wearable device.

The scientific findings validated that passionate consumers about new technologies are more likely to adopt smart wearable payments. The study added research value to the existing knowledge by exploring personal innovativeness characteristics as an imperative precursor of the authentic use of the technology and affects the relationship between intention and actual use. The study further provides thought-provoking to existing knowledge through examining the actual user behavior in the context of payments and analyzing the personal innovativeness on the relationship of behavioral intention and the actual user behavior.

Limitations and Future Research Avenues

This study contributes substantially to the theory and practice of the wearable technologies payments, yet some limitations are linked to this research. First, this research collected and analyzed data from wearable technologies consumers in Saudi Arabia. The findings cannot be generalized globally due to uneven facilitating conditions in different countries. Thus, future research may be conducted across countries that will broaden the scope of research on SW payments. Second, this study has employed a sample of 243 respondents. A comparatively larger sample is recommended for more robust results and generalization of findings. Third, this study has considered personal innovativeness as a moderator. In future, scholars can test other moderators like age, gender, perceived risk, social influence, facilitating conditions, and fashion behavior. Fourth, the quantitative technique has been employed to explore the consumers’ adoption of SW payments. Mixed method approaches may deliver deeper understandings about the phenomenon. Fifth, a cross-sectional survey was carried out by this study. Longitudinal studies may provide more insights about the subject matter as the behaviors of consumers are changing over different periods. Sixth, the current study has incorporated technological features with TAM framework. Future studies can integrate technological characteristics to UTAUT framework to examine the subject matter. Seventh, future research can use the model of the current study to compare the behaviors of users and non-users which may help understand the adoption of SW payments. Lastly, our research has explored the effects of perceived esthetics in SW payments context. Future research can explore the dimensions of perceived esthetics and its effects on technology adoption in other contexts of wearable technologies.

Research Data

sj-csv-1-sgo-10.1177_21582440221117796 – Research Data for Examining Consumers’ Adoption of Smart Wearable Payments

Research Data, sj-csv-1-sgo-10.1177_21582440221117796 for Examining Consumers’ Adoption of Smart Wearable Payments by Imdadullah Hidayat-ur-Rehman, Arshad Ahmad, Fahim Akhter and Mohd Ziaur Rehman in SAGE Open

Footnotes

Appendix

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

References

Supplementary Material

Please find the following supplemental material available below.

For Open Access articles published under a Creative Commons License, all supplemental material carries the same license as the article it is associated with.

For non-Open Access articles published, all supplemental material carries a non-exclusive license, and permission requests for re-use of supplemental material or any part of supplemental material shall be sent directly to the copyright owner as specified in the copyright notice associated with the article.