Abstract

Previous research on green innovation sought to comprehend the antecedents and outcomes of environmental regulations. However, how these antecedents translate into outcomes may vary depending on different types of environmental regulations, such as environmental subsidies and pollution charges. We propose and test the effects of different environmental regulations on enterprises’ green innovation preferences. Moreover, we analyze how ownership type moderates the observed effects. The fundamental results reveal that: (1) Environmental subsidies and pollution charges positively affect energy conservation innovation. (2) Environmental subsidies and pollution charges positively affect emission reduction innovation. (3) Pollution charges are not as effective as environmental subsidies in promoting energy conservation innovation. However, pollution charges have a greater implementation effect than environmental subsidies in encouraging emission reduction innovation. (4) The types of enterprise ownership only play a positive moderating role in the relationship between pollution charges and emission reduction innovation. Accordingly, this paper provides auxiliary decision-making for the government to motivate the energy conservation and emission reduction of enterprises.

Keywords

Introduction

With the development of industrialization and urbanization, the energy consumption and pollution produced by manufacturing enterprises are increasing. Environmental pollution and ecological imbalance have become critical issues that seriously threaten the survival of humankind (Y. Guo et al., 2020). Green innovation is a crucial ingredient for achieving environmental protection and economic development (Huang & Li, 2017). Therefore, countries around the world have issued a series of environmental regulations to promote firms’ green innovation. Porter pointed out that properly designed environmental regulations can stimulate enterprises to trigger innovation activities. Although companies may increase costs in the short term, they can increase production efficiency and competitiveness in the long term (Porter & Van der Linde, 1995a). In comparison with enterprises, the government has sufficient information on green technology innovation. At present, the government encourages firms to reduce natural resources and minimize the emission of harmful substances through different types of environmental regulations, such as environmental subsidy, pollution charge, and emission trading. The government controls and optimizes overall pollution through the above mentioned measures (J. Y. Lee & Podsakoff, 2003).

Environmental subsidies and pollution charges are two primary environmental regulations, and myriad scholars have studied their impact on green innovation (J. Liu et al., 2020; Ma & Li, 2021). However, there is so much debate in the academic literature on the effects of environmental regulations on green innovation. On the one hand, most studies focusing on the impact of environmental subsidies on green innovation are still inconsistent (Gramkow & Anger-Kraavi, 2018). Enterprises need to invest a lot of resources in the long-term to promote green innovation, so they face the main problems of financing constraints and insufficient incentives (Bigerna et al., 2019; Joo et al., 2018). Environmental subsidies not only help companies enhance green innovation R&D funds, but also reduce excessive R&D costs caused by external factors (Bellucci et al., 2019; S. H. Lee & Park, 2021). Furthermore, environmental subsidies reduce managers’ concerns about the uncertainty of innovation activities and increase firms’ risk-taking capacity for green innovation. However, contrary views of some studies suggest that government subsidies have negative effects on green innovation, such as crowding out and substitution effects. Enterprises will squeeze innovation funds and increase environmental protection costs to meet standards, which results in reducing technological innovation capabilities (Howell, 2017; C. Wang et al., 2017).

On the other hand, scholars have focused on the impact of pollution charges on green innovation. Although paying pollution charges increases the cost of enterprises in the short term, for example, enterprises must import anti-pollution equipment, which takes time and money away from production management (Lanoie et al., 2011). However, enterprises will actively carry out green innovation activities, such as retrofitting existing equipment, upgrading technology, reducing external costs caused by pollution charges, to eliminate the negative impact of pollution charges and reduce pollutants in the production process (J. Lee et al., 2010; Shen et al., 2020). However, some scholars indicate that pollution charges will increase the squeeze on innovation input and the risk of technological innovation, thereby increasing operating pressure (Conrad & Wastl, 1995; Lanoie et al., 2011). As a result, even if companies pay pollution charges, they are reluctant to carry out green innovation easily.

In general, extant literature has not yet shown definitive conclusions about the impact of various types of environmental regulations on green innovation. There some gaps in the prior literature that need to be filled with more empirical research. First, previous researches frequently focused on a single type of environmental regulation rather than comparing the effects of different types of environmental regulations on green innovation. Second, few studies have subdivided green innovations, such as energy conservation innovation and emission reduction innovation, further to consider the strategic preferences of environmental regulations on different types of green innovations. Third, existing research on green innovation focuses on the backgrounds of developed countries while paying less attention to developing and emerging economies. Energy conservation and emission reduction have been the government’s top priority in most industrialized countries. However, energy conservation and emission reduction have not received sufficient attention in some developing countries. Fourth, many scholars have denoted that the structure of ownership significantly affects corporate innovation activities (Wu, 2017). Faced with the different environmental regulatory policies, enterprises may choose different green innovation strategic preferences (K. Wang & Jiang, 2021). However, this analysis seldom extends to the relationship between environmental regulation and green innovation. Fifth, previous studies mainly used a scale based on subjective perception to measure green innovation. Therefore, the reliability of the results may have certain deviations (J. Y. Lee & Podsakoff, 2003; Zhao et al., 2021).

To address the issues raised above, this paper mainly contributes to prior research from the following aspects. First, we divide environmental regulations into two categories: environmental subsidies and pollution charges. This paper studies the impact of the implementation effects of different policy tools on the strategic preference of green innovation. Our empirical research responds to the debate surrounding the relationship between different policy environment tools and green innovation. This paper provides fresh insights into environmental regulations and green innovation. Second, we divide green innovation into energy conservation innovation and emission reduction innovation. Because energy conservation/emission reduction innovation have different technical characteristics as well as investment requirements, risks, R&D processes. Contrastingly, according to the research gaps mentioned above, the empirical results answer whether different types of environmental regulations have an impact on companies’ choice of energy conservation innovation or emission reduction innovation, which enrich the results relating to energy conservation innovation and emission reduction innovation. Third, as the largest developing country, China has become the world’s largest emitter of greenhouse gases since 2006 and faces increasingly severe environmental challenges (M. H. Li et al., 2014). Therefore, the evidence in this paper comes from Chinese manufacturing companies, which can expand energy conservation and emission-reduction practices in developing countries. Fourth, this study expands the measurement of energy conservation/emission reduction innovation to compensate for the existing literature’s subjectivity in measurement. Finally, given firm heterogeneity, this study regards firm ownership type as moderating variables. Further, we explore whether state-owned enterprises and non-state-owned enterprises have green innovation preferences in the face of different environmental regulations. Following above, this paper offers a realistic point of reference for the government to promote energy conservation and emission reduction.

The remainder of this paper is organized as follows: In the next section, we review the literature. We propose research hypothesis in Section 3. Section 4 describes the research design. Section 5 presents the empirical results and robustness test and we provide discussion in Section 6.

Literature Review

Environmental Regulations

Environmental regulations are an important measure to limit the harmful effects of economic activity on the natural environment (Du et al., 2021; Shao et al., 2020). Environmental regulation was initially seen as a series of actions that government intervened or restrained market economic activities (Kemp & Pontoglio, 2011). The government enacts primary environmental management policies, such as prohibitions and non-transferable licenses, to prevent and control pollution discharge, protect the ecological environment, and control the environment. With the development of the market economy, the definition of environmental regulation has been gradually revised, and the role of the market mechanism has been emphasized (Tang et al., 2020). Since the 1990s, a new type of environmental regulation has gradually emerged, such as voluntary environmental regulation, which mainly includes voluntary agreements, voluntary standards, and voluntary norms (Blackman et al., 2010; Bu et al., 2020). Therefore, scholars have further expanded the meaning of environmental regulation. At present, environmental regulation includes a variety of tools, such as command-and-control environmental regulation, market-based environmental regulation and voluntary environmental regulation (Ren et al., 2018). Different environmental regulations may address different environmental problems due to differences in political and economic backgrounds (Stavins, 1996). Environmental subsidies are government financial incentives given to enterprises whose pollution control costs rise as a result of environmental standards (Bai et al., 2018). Pollution charges refer to the government’ use of a certain fee standard to define the degree of pollution caused by enterprises to the environment, which is mandatory and fixed (Chiroleu-Assouline & Fodha, 2014).

Energy Conservation and Emission Reduction

Braun and Wield (1994) first denote that green innovation is a technological innovation activity that reduces environmental pollution and improves the ecological environment. Following that, theoretical and empirical researches on green innovation emerged rapidly. After more than three decades of research, green innovation refers to activities related to the development of innovative products and processes that reduce harmful impacts on the environment (Kemp et al., 2000), which includes the use of green Raw materials, adhere to the principles of ecological product design, reduce material use, reduce pollutant emissions, and reduce consumption of water, electricity, and other raw materials (Albort-Morant et al., 2016).

Regarding the category of green innovation, many scholars divide green innovation into green process innovation and green product innovation (Andersén, 2021; M. Wang et al., 2021). Green innovation has been divided into three categories by some researchers: green product innovation, green process innovation, and terminal governance technology innovation. Furthermore, some scholars divide green innovation into energy conservation innovation and emission reduction innovation. Energy conservation innovation refers to a series of innovative activities carried out by enterprises to minimize energy consumption and resource consumption in the production process. Emission reduction innovation refers to an enterprise’s innovative change operation of the primary production or main process with the goal of minimizing or eliminating production in the production process. They evaluate energy conservation in the Chinese heating industry.

The majority of the energy conservation and emission reduction focus on measuring their efficiency, potential, and emissions in a region or industry. Lin and Lin (2017) evaluate energy conservation in China’s heating industry. Wen et al. (2021) examine the effects of financial structure on regional energy conservation and emission reduction. Kong et al. (2017) indicate that Chinese pulp and paper industry has potential for energy conservation and CO2 mitigation. Raggio et al. (2020) address the current logical gap of service firms on energy conservation. They create a conservation metric that enables service firms to measure their contributions to energy consumption relative to national economic growth.

Environmental Regulations, Energy Conservation Innovation, and Emission Reduction Innovation

According to the existing theoretical and empirical literature, environmental regulation tools have different effects on green technological innovation. Concretely, the relationship between them can be summarized as follows. First, environmental regulations negatively impact technological innovation (Christainsen & Haveman,1981; Shi et al., 2018). The implementation of environmental regulation policies has caused enterprises to increase the production cost of pollutant discharge and emission reduction. It is bound to invest in technological innovation funds of enterprises, thereby inhibiting technological innovation of enterprises. Second, environmental regulation can promote technological innovation. The Porter Hypothesis claims that in the face of pressure from environmental regulations, companies may accelerate technological innovation to address their current predicament (Albrizio et al., 2017; Porter & Van der Linde, 1995b). Although environmental regulation increases the cost of enterprises, it also promotes technological innovation. The benefits of innovation compensate for rising costs caused by environmental regulations. Third, there is a nonlinear relationship. The nonlinear relationships derived by scholars based on research samples include U-shapes (Cai & Li, 2018), inverted U-shapes (Johnstone et al., 2017), or other more complex threshold relationships (Y. Wang & Shen, 2016). Fourth, there is no significant relationship between environmental regulations and technological innovation (Becker, 2011; Jaffe & Palmer, 1997).

Based on the extant literature, the focuses of the existing research are as follows. First, most of the existing studies on the impact of environmental regulations on energy conservation and emission reduction are at the regional level, such as the impact of environmental policies on energy conservation and emission reduction in various regions (Dong et al., 2018). The environmental regulations have little influence on the preference of enterprises for energy conservation and emission reduction. Secondly, most of them generally choose carbon dioxide emissions as the measurement index when measuring the energy conservation and emission reduction of enterprises (Y. L. Liu et al., 2018; Q. Zhou et al., 2016). Few studies consider enterprise energy conservation and emission reduction from the perspective of technological innovation. Some scholars consider energy conservation and emission reduction innovation to be a subcategory of green process innovation, because both energy conservation technology and emission reduction technology contribute to the improvement of green processes.

Research Hypothesis

Environmental Subsidies and Green Innovation

Environment subsidies are net cash flow for firms, which can greatly reduce the cost pressure and risks of firms’ green innovation investments. First, enterprises must invest substantial initial capital and sufficient financial support when carrying out energy conservation innovation and emission reduction innovation activities. It will greatly increase the innovation cost of enterprises (Xu et al., 2012). Thus, the enthusiasm of enterprises to implement energy conservation innovation and emission reduction innovation will be weakened. Environmental subsidies provide enterprises with direct financial support, which can reduce their financing constraints and cost pressures. Therefore, the recipient enterprises are more willing to carry out energy conservation and emission reduction innovation activities. Second, green innovation, as a distinct type of innovation, must bear both the economic responsibility of generating potential excess profits for enterprises and the social responsibility of improving the effectiveness of the ecological environment. Therefore, the risk pressure caused by enterprises that innovate energy conservation and emission reduction is much higher than ordinary innovation. Government subsidies can send a positive signal, thus reducing information asymmetries and enhancing fund providers’ confidence, which helps minimize companies’ risk-taking capacity. Hence, those companies that perform poorly after receiving subsidies can effectively accelerate the progress and affordability of energy conservation innovation and emission reduction innovation. In general, government subsidies that refer to an important external capital and a direct government support, can reduce the cost pressure and risks of new technologies for energy conservation and emission reduction, thereby promoting technological innovation in energy conservation and emission reduction. Accordingly, we propose following hypothesis:

Pollution Charges and Green Innovation

Pollution charge refers to the government’s use of certain charging standards to define the degree of pollution caused by enterprises to the environment, which is mandatory and fixed. Since 2003, China has levied pollution charges on enterprises. In January 2018, the sewage charge was changed to an environmental tax. Both pollution charge and environmental tax are important regulatory tools for the government to protect the environment.

On the one hand, according to the stakeholder theory, stakeholders play a crucial role in the green development of enterprises (Freeman, 1984). They participate in corporate governance through formal or informal means to influence corporate decisions and goals (Freeman & Evan, 1990; Sharpe, 1996). The government is an important and special stakeholder that exerts pressure on corporate environmental protection behavior (Henriques & Sadorsky, 1999). The government restricts the use of corporate energy and waste resources in the production process by charging pollution charges. If a company’s pollution charges remain high, it could cause the company to go out of business or lose access to other government resources. As a result, companies will implement strict environmental regulations or improve pollution control technologies to reduce energy and pollution emissions. It will rise pollution control costs for businesses. As the pursuit of profit maximization, enterprises often improve energy-intensive and polluting production processes and reduce pollution charges through energy conservation innovation and emission reduction innovation. In addition, external stakeholders such as suppliers and customers will also assess the legitimacy of corporate pollution charges. When companies pay more for emissions, these external stakeholders reassess corporate risks, such as whether to continue investing in companies or provide companies with raw materials and loans. Therefore, enterprises will be forced to carry out innovative activities for energy conservation and emission reduction, and reduce pollution charges in order to obtain resources as well as support from external stakeholders. For example, enterprises reduce waste water, waste gas, waste, and other resources by improving certain energy conservation and emission-reduction processes or technologies.

On the other hand, in terms of internal incentives, energy conservation, and pollutant emissions are undoubtedly the embodiment of corporate social benefits. Although pollution charges increase the cost of the business in the short term and reduce the profit directly realized in the short term. However, pollution charges can raise awareness of corporate green development among managers (Grossman & Helpman, 2018). In order to gain new green market shares and cultivate unique green competitive advantages, enterprises will actively innovate energy conservation or emission-reduction technologies, such as improving waste water discharge or energy consumption in the production process. Hence, under the pressure of pollution charges, both the pressure from external stakeholders and the need for internal incentives will prompt enterprises to carry out energy conservation and emission reduction innovation activities.

Moreover, pollution charges include exhaust gas fees, sewage discharge fees, solid waste and hazardous waste fees, excessive noise fees, and so on. Energy conservation activities mainly focus on the conservation and utilization of energy and resources in the production process of enterprises, which cannot directly reduce exhaust gas, waste water, and waste. Therefore, the lag effects of energy conservation/emission reduction innovation on corporate environmental governance are not the same due to different technological processes. Compared with energy conservation innovation, emission reduction innovation can significantly improve the pollution control ability of enterprises, thereby slowing down or offsetting pollution charges. Therefore, when faced with pollution charges, enterprises are more likely to innovate in emission reduction. Based on the above analysis, we propose the following assumptions:

The Moderating Effect of SOE Types

Because state-owned enterprises and non-state-owned enterprises have different resource channels, production efficiency and operational capabilities. Therefore, companies with different ownership structures will adopt different green innovation strategies when they are faced with different regulations. First, compared with non-state-owned enterprises, state-owned enterprises have more obvious resource endowment advantages due to their political resource advantages. Therefore, it is not necessary for state-owned enterprises to obtain subsidized resources through green transformation, resulting in their lower willingness to innovate in energy conservation and emission reduction than non-state-owned enterprises. Second, although state-owned enterprises have less financing constraints than non-state-owned enterprises. However, state-owned enterprises are highly concentrated and have redundant organizational structures. Therefore, the innovation efficiency of energy conservation and emission reduction of state-owned enterprises is lower than that of non-state-owned enterprises, which is not conducive to the transformation of green innovation achievements (Hering & Poncet, 2014). Therefore, we propose the following hypothesis:

Compared with non-state-owned enterprises, state-owned enterprises have both a public welfare mission and a profit mission (Kemp et al., 2000). State-owned enterprises and non-state-owned enterprises have different goals. State-owned enterprises and non-state-owned enterprises have different goals. State-owned enterprises consider comprehensive benefits including economic, environmental, and social benefits, while non-state-owned enterprises pay more attention to economic goals. First, from the perspective of stakeholders, the government and the public have higher expectations for state-owned enterprises to fulfill their social responsibilities, which will bring greater external regulatory pressure on state-owned enterprises. Therefore, when state-owned enterprises are charged a lot of pollution fees due to excessive energy consumption or polluting emissions, it may cause dissatisfaction with the government and the public. In order to meet the requirements of the government and the public, state-owned enterprises will have more incentives to avoid pollution charges, thereby increasing the input and output of energy conservation and emission reduction innovation. Second, from the perspective of political relevance, pollution charges reflect the level of excess pollution charges of enterprises, which is not suitable for managers to achieve government goals and shape their image. Consequently, pollution charges have more significant incentives for state-owned enterprises. Therefore, we propose the following hypothesis:

The research framework of this paper is shown in Figure 1, where the type of enterprise ownership moderates the interaction between environmental regulations and green innovation.

Research framework.

Research Design

Samples and Data Sources

This paper uses the data of China’s A-share Shanghai and Shenzhen listed manufacturing companies from 2011 to 2019 to empirically test the effects of different types of environmental regulations on companies’ preference for green innovation activities. The data sources of this article are as follows: (1) The data on environmental subsidies and pollution charges are from the notes of listed companies’ annual reports, which are collected manually by us. (2) The data on green innovation of listed companies comes from the State Intellectual Property Office (SIPO), The corresponding data are collected manually by us. (3) The data of the remaining variables come from the CSMAR database, WIND database, and Chinese Research Data Services (CNRDS) database.

Concerning the primary data that we gathered, we: (1)exclude the enterprises with ST and *ST during the sample period. (2) Delete the samples with missing variable observation values. (3) Exclude samples that have not been disclosed for environmental subsidies and pollution charges to reduce the number of enterprises affected by information disclosure as much as possible. (4) Winsorize the continuous variables at the 1% and 99% levels to avoid the influence of abnormal data on the test results. Finally, we obtain 205 publicly listed manufacturing firms in China, resulting in an unbalanced panel.

Variable Selection and Measurement

Dependent variables

Energy conservation innovation (SepaRatio) and emission reduction innovation (EdpaRatio)

Regarding the definition of green patents, this research uses the “Green List of International Patent Classifications” launched by the World Intellectual Property Organization (WIPO) in 2010. We screened out patent information related to environmentally friendly technologies and conducted a conditional search in the State Intellectual Property Office. Because the number of patent applications can reflect the actual innovation level of an enterprise more than the number of patent grants. According to the standards mentioned above, we identify the number of green patent applications for listed companies in the Shanghai and Shenzhen A-share manufacturing industries. We have further identified energy conservation green patents based on “energy conservation” and “energy conservation,” and identified emission reduction green patents with the keywords of “emission reduction,” “exhaust gas,” and “wastewater.” This paper uses the ratio of the number of energy conservation green patent applications to the number of enterprise patent applications as an index to measure energy conservation innovation, expressed as SepaRatio. We use the ratio of the number of emission reduction green patent applications to the number of enterprise patent applications as an indicator to measure emission reduction innovation, expressed as EdpaRatio.

Explanatory variables and moderator variable

Environmental subsidy (Lnsubsidy)

The relevant information on environmental subsidies received by listed companies is disclosed in the “Details of Government Subsidies” under the “Non-Operating Income” item in the company’s annual report. However, this data does not form a unified disclosure form. At present, the measurement of environmental protection subsidies in academia is mainly based on the method of text analysis to search for the key words of the government subsidy details, in order to determine the items that fall under the environmental protection subsidy. Then the subsidy amount is summarized to represent the amount of environmental protection subsidy. This method can provide a more accurate representation of the environmental subsidies received by companies. This article uses the logarithm of the environmental protection subsidy amount as the proxy indicator of the environmental subsidies, denoted by Lnsubsidy.

Pollution charges (Lncharge)

The relevant information on the pollution charges obtained by listed companies is disclosed in the “Pollution charges” under the “Taxes and Surcharges” item in the company's annual report financial statements. The new environmental tax law officially implemented in 2018 changed the “pollutant discharge fee” to the “environmental tax,” and it is stricter than the “Regulations on the Collection and Use of Pollutant Discharge Fees” in terms of collection standards, collection and management measures, and pollution areas. Hence, we select the amount of “environmental tax” to represent the number of pollution charges in 2018 to 2019. However, it should be noted that whether it is an environmental tax or pollution charges, their nature is to charge for the enterprise’s economic activities of negative externalities. Because the tax object and nature of environmental taxes have fewer changes than pollution charges, they have no effect on the article’s conclusions and policy implications. We use the logarithm of the amount of pollution charges and environmental taxes as the proxy indicator of pollution charges, denoted by Lncharge.

Type of ownership (SOE)

The proportion of state-owned assets reflects the characteristics of the ownership structure of the enterprise. We set two dummy variables to measure the ownership type. Referring to the division of ownership in the CSMAR database, private enterprise = 0 means that an enterprise is a privately owned; otherwise, its value is 1.

Control variables

In order to control the impact of other variables on the company’s green innovation, this paper selects five indicators that may affect the company’s green innovation as the control variables: (1) Enterprise size (Size): Size represents the natural logarithm of the company’s total assets. (2) Asset-liability Ratio (Lev): Lev is expressed as the ratio of total liabilities to total assets of listed manufacturing companies. (3) R&D investment (Lnrd): In innovation activities, R&D can be regarded as the investment of innovation, expressed by the natural logarithm of the amount of enterprise R&D investment. (4) Growth of the firm: The growth represents the growth rate of the company’s operating income this year. (5) Age of establishment of the firm (Fage): Fage represents the time from the establishment of the listed manufacturing company to the statistical year. Table 1 displays the variables definition, in which CONTROLS uniformly represents the control variables.

Variable Definition Table.

Empirical Model Design

In order to avoid the influence of potential endogenous problems on the research conclusions, we use

Empirical Results

Descriptive Statistics and Correlation Analysis

Table 2 reports the descriptive statistics and correlation analysis of the variables, respectively. A descriptive statistical analysis of all variables shows that the standard deviation of environmental subsidies and pollution charges is relatively large, indicating that each firm’s environmental subsidies and pollution charges are quite different. This is due to the stringent policies of the companies themselves and the government. They are caused by different degrees. Secondly, the minimum number of patent applications for energy conservation/emission reduction innovation of enterprises is 0, and the average values are 0.06 and 0.08, respectively. The data shows that the green innovation level of listed companies in China’s manufacturing industry is generally low. To ensure that the model does not have a severe multicollinearity problem, we calculated the VIF value of the variance expansion factor of each primary variable of the model. The VIF value of all variables is within 3, and the average VIF value is less than 1.5, which implies that the model does not have serious multicollinearity problems. The pearson correlation coefficients for the main variables are shown in Table 2. As demonstrated, there is a significant positive correlation between environmental subsidies and all types of green innovations. Additionally, pollution charges have a significant positive correlation with all types of green innovations. The findings initially supported the central hypothesis of this paper.

Descriptive Statistics and Correlation Matrices.

p < .1. **p < .05. ***p < 0.01.

Regression Analysis Results

Main effect test

Before verifying the hypothesis, we explored different lagging structures in the empirical analysis. The findings indicate that the current environmental subsidies and pollution charges failed the significance test; the lagging one-period environmental subsidies and pollution charges are significant at the 1% significance level. The results show that the impact of environmental subsidies mainly occurs within a 1-year time interval (Lach, 2002). Pollution charges also show a lagging feature. The current pollution charges significantly increase the level of energy conservation innovation and level of emission reduction innovation of the enterprise in the next period. After the one-period lagging hypothesis test, the p-value of the model after the Hausman test is less than .05. The null hypothesis is rejected at the 95% level, so the fixed effects model is selected in this paper. Models (1) and (2) are used to test the impact of environmental subsidies on energy conservation/emission reduction innovation in hypotheses H1a and H1b, respectively. Models (3) and (4) are used to test the impact of hypothetical pollution charges on energy conservation/emission reduction innovation, respectively. Models (5) and (6) are used to test Hypothesis H3a, the moderating role of ownership types between environmental subsidies and green innovation. Models (7) and (8) are used to test Hypothesis H3b, the moderating role ownership types on the relationship between pollution charges and green innovation.

From the regression results in Table 3, the main effect of environmental subsidies on energy conservation innovation is strongly positive and significant (model 1: β = .007, p < .01) and is strongly positive and significant emission reduction innovation (model 2: β = .007, p < .01). Thus, the results in Models 1 and 2 support hypotheses H1a and H1b. In addition, the main effect of pollution charges on energy conservation innovation is strongly positive and significant (model 3: β = .006, p < .01) and is strongly positive and significant emission reduction innovation (model 4: β = .008, p < .01). By comparing model (1) and model (3), it can be seen that environmental subsidies can promote energy conservation innovation more than pollution charges. By comparing model (2) and model (4), the results show that pollution charges can promote emission reduction innovation more than environmental subsidies. Thus, the results in Models 3 and 4 support hypotheses H2a and H2b.

Results for Testing Hypotheses.

p < .1. **p < .05. ***p < .01.

Moderating effect

To verify the moderating effect of ownership types, we add a two-way interaction to test the moderating role of ownership types between independent variables and moderating variables. Models (5) and (6) add the interaction between Lnsubsidy and SOE to test H3a. Models (7) and (8) add the interaction between Lncharge and SOE to test H3b. To eliminate the multicollinearity between the interaction term of the moderating variable and the independent variable and other variables, this article will standardize the interaction term and then test moderating effect of ownership types. It can be seen from Table 4 that the regression results of models (5) and (6) reveal that the types of ownership have no significant effect on the relationship between environmental subsidies, energy conservation innovation, and emission reduction innovation. Therefore, the results of models (5) and (6) do not support H3a. The regression results of model (7) show that the corporate ownership types do not significantly affect the relationship between pollution charges and energy conservation innovation. The regression result of model (8) shows that the interaction term between pollution charges and ownership types is positive. The result is significant at the .05 level, which implies that state-owned enterprises can promote emission reduction more than non-state-owned enterprises when facing pollution charges. Therefore, the results of models (7) and (8) partially support H3b (Figure 2).

Results for Testing Hypotheses.

p < .1. **p < .05. ***p < .01.

The moderating effect of ownership types on pollution charges and emission reduction innovation.

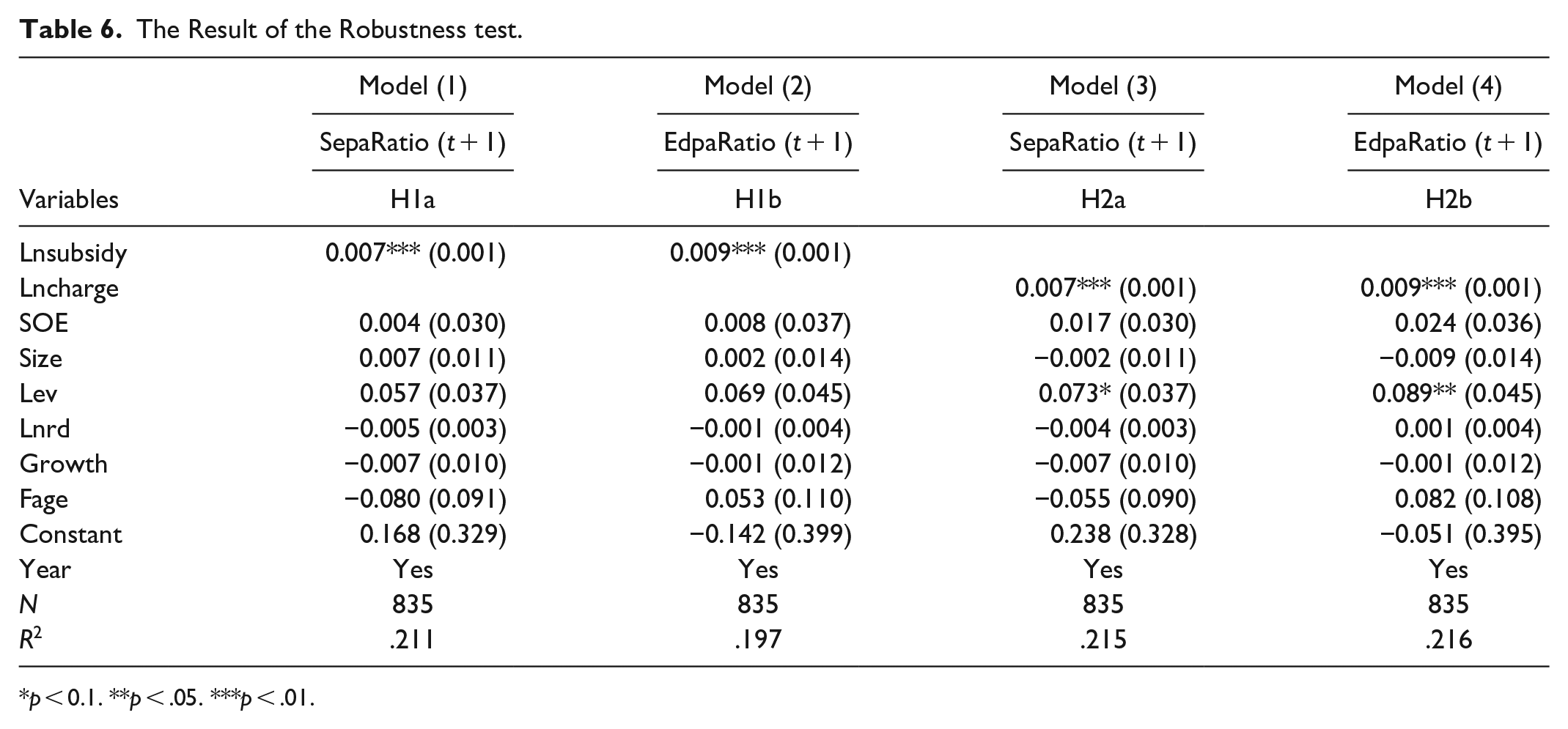

Robustness Test

We conducted additional analyses to ensure the robustness of the regression results. First, we use the method of reducing the sample size for robustness testing. Since the sample in this article is from the manufacturing industry, a large portion of the manufacturing industry is from the heavy pollution industry, which is better suited to promoting green innovation. Therefore, this paper selects heavily polluting enterprises as a sub-sample. According to the code of heavy pollution industry, we further screened the heavily polluting enterprises in the sample. Tables 5 to 7 are the regression results of the heavily polluting enterprises. There is no significant difference between the regression results and the previous comparison, indicating that the conclusions of this paper still have high explanatory power for the research hypotheses. It can be seen from the moderating effect diagram that enterprises in heavy pollution industries have a more apparent positive effect on pollution charges. Second, this paper adopts the standardized calculation method of operating income and business tax on environmental subsidies and pollution charges, which are defined as the percentage of environmental subsidies in non-operating income (Subsidyratio) and the percentage of pollution charges in business tax (Chargeratio). Then we use models (1) to (8) to re-run the regression test hypothesis. The results show that the results did not change the main research conclusions of this article (Figure 3; Table 5).

Heavy Pollution Industry Code.

The Result of the Robustness test.

p < 0.1. **p < .05. ***p < .01.

The Result of Robustness test.

p < .05. ***p < .01.

The moderating effect of ownership on pollution charges and emission reduction innovation.

Discussion

Main Conclusions

This paper mainly focuses on the effects of different types of environmental regulations on green innovation preferences. We use panel data of Chinese listed firms over the period 2011 to 2019 to empirically test the effects of different types of environmental regulations on enterprises’ green innovation strategic preference. The empirical results support most of our hypotheses. First, the research findings reveal that two environmental regulations both facilitate conservation innovation and emission reduction innovation. This finding basically matches up with viewpoints proposed by Porter and Van der Linde (1995b), Ye et al. (2018), Peng et al. (2021), and Zhong and Peng (2022). As for those conclusions in some studies, they appear to be similar to the conclusion in this paper. For example, Ye et al. (2018) claim that the market-based environment regulation had a significant positive impact on the energy conservation and emissions reduction innovation of the first-lag phase. Our findings validate this empirical result. Moreover, we further find that environmental subsidies can significantly promote energy conservation innovation more than pollution charges. Compared with environmental subsidies, pollution charges have a more significant positive effect on emission reduction innovation. Second, we take into account the effect of heterogeneity of results. This paper proposes and examines how ownership types moderate the relationship between environmental regulations and green innovation preference. According to the empirical results, at the enterprise level, only pollution has a stronger emission reduction innovation on state-owned enterprises. The findings of the study are consistent with the research conclusions of Zhong and Peng (2022), J. Liu et al. (2020), and K. Wang and Jiang (2021). That is, due to the difference in the firm’s ownership, environmental regulation has different promotion effects on green innovation of enterprises.

Theoretical Contributions

This paper provides valuable theoretical contributions in three aspects:

Firstly, our paper contributes to the environmental regulation literature by revealing the different roles of environmental regulations in green technological innovation. We divide market environmental regulation tools into two categories: pollution charges and environmental subsidies. Several studies only unified pollution charges and environmental subsidies as market-based environmental regulation tools, and only explored the impact of market-based environmental regulation tools on firms’ preference for technological progress (Ye et al., 2018; X. Zhou et al., 2020). X. Zhou et al. (2020) empirically detect the effects of three regulations (command-and-control regulation, market-based regulation, and informal environmental regulation) on energy- and environment-biased technological progress. Ye et al. (2018) how market-oriented policy tools impact technological innovation of energy conservation and emission reduction. Different with them, we further explore whether enterprises choose energy conservation or emission reduction in the face of different environmental regulation tools. The literature, however, has yet to identify whether a ’firm’s Energy Conservation/Emission Reduction innovation is primarily associated with different market-based environmental regulations. This is a preliminary study exploring their relationship. Our research not only provides empirical evidence for the “Porter Hypothesis,” but also enriches the studies on the effect evaluation of environmental regulations.

Secondly, our research contributes to energy conservation/emission reduction innovation research by conducting the relationship based on the micro-level of firms. Despite that many scholars talk about the relationship, most of which are based on the regional level (X. Guo et al., 2017; Ye et al., 2018). X. Guo et al. (2017) applied a modified slacks-based model to measure the performance of energy conservation and emission reduction in 30 provincial-level regions in China. Ye et al. (2018) studied the relationship between environmental regulations and energy conservation/emission reduction innovation based on Chinese city-scale data. Compared with macro-level data, corporate data can mitigate aggregation bias by controlling for heterogeneity not observed in panel data (Dechezleprêtre & Sato, 2017). We use panel data of Chinese listed firms to examine the hypothesis. Our study provides some insights for future researchers exploring corporate energy conservation and emission reduction activities, thereby enriching related research on the micro level.

Thirdly, the paper contributes to the green innovation literature by revealing the moderating effect of enterprise ownership type on the relationship between environmental regulation and green technological innovation. Prior literature emphasizes the interaction of energy conservation and emission reduction innovation orientation mainly caused by external regulatory agencies, which leads to neglect of the influence of corporate ownership characteristics. Some scholars have noticed that corporate ownership structure can impact a firm’s green innovation (J. Liu et al., 2020; K. Wang & Jiang, 2021). J. Liu et al. (2020) examine the moderating role of ownership types between innovation subsidies and green/nongreen innovation. K. Wang and Jiang (2021) indicate that state ownership positively affects a firm’s green innovation. They further found that positive effects increase when SOEs are in regions with advanced legal development, for firms with adequate resources, or when a board chair possesses functional experience. This paper further confirms that ownership type regulates the relationship between pollution charges and energy conservation innovation. Therefore, this paper fills the gap of previous research and expands the research on the impact of ownership structure on green innovation.

Policy Implications

Based on the preceding conclusions, our findings carry essential ethical and practical implications in China. First, the government should establish a comprehensive and scientific environmental supervision system. Enterprises will make different green innovation preferences when they are faced with different policy tools. Therefore, the government needs to further improve the regulatory system, such as paying attention to the public and the media, so that companies have more choices. It can be seen that environmental subsidies are more effective in promoting energy conservation innovation, while pollution charges are more effective in stimulating emission reduction innovation. Therefore, the government requires to formulate a more detailed and reasonable regulatory system based on environmental protection goals. It can ensure that the energy conservation and emission reduction benefits of local enterprises are maximized through a reasonable supervisory system. Second, when implementing environmental regulations and policies, the government should fully consider the ownership structure of enterprises. From the results mentioned above, ownership type does not moderate the relationship between environmental subsidies and energy conservation and emission reduction innovation, as well as the relationship between pollution charges and emission reduction innovation. The empirical results show that pollution charges are less effective in supporting non-state-owned enterprises. Therefore, the government can consider weakening the penalties for non-state-owned enterprises. The government can strengthen the intensity of emission reduction subsidies and increase support for non-state-owned enterprises in emission reduction innovation. Meanwhile, the government needs to strengthen the supervision of environmental subsidies and improve the review mechanism for obtaining subsidies, thereby reducing the “crowding-out effect” caused by the behavior of enterprises only to obtain support funds.

Limitations and Future Research

This paper has several inevitable limitations as well. First, we tested the hypotheses in a single industry. Thus, the conclusion may not be general, which may be limited in other industries. We encourage future research to be extended to other industries, especially those with high potential risks of environmental pollution. Second, we only divide green innovation into energy conservation innovation and emission reduction innovation. Most existing research divides green innovation into green process innovation and green product innovation. Future research can further divide energy conservation innovation into energy conservation products and energy conservation processes to explore the impact of different types of green innovation. Third, although we have selected the number of patent applications to measure green innovation, the number of invention patents may reflect the ability of green innovation. Fourth, we only divide enterprises ownership into state-owned enterprises and non-state-owned enterprises. Considering the Chinese context, central state-owned enterprises and local state-owned enterprises may have different green innovation preferences. Thus, we may consider further subdividing state-owned enterprises into central state-owned enterprises and local state-owned enterprises in future research.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by Hebei Social Science Foundation major project, grant number (HB19ZD03); Hebei Province Innovation Capacity Enhancement Project, grant number (19457678D); Hebei Provincial Department of Education Humanities and Social Science Research Major Project (ZD202004); Natural Science Foundation of Hebei Province, grant number (G2021202001); Philosophy Science Foundation of Xiongan, grant number (XASK20200003).