Abstract

Export is an important macroeconomic factor that can elevate a country’s output performance and raise employment opportunities, in any economy. Any country may expand the number of its allies through exports. Foundation trade theories, like absolute advantage and comparative advantage, suggest that a country should export the product with greater absolute or comparative advantage. This sheds light on allocating the optimal resources for producing low-price products and flouting the idea of specialization among the countries of the world. The present study explores the factors that may influence the export performance of a developed economy like Canada from 1979 to 2019. The study findings provide evidence of the absence of multicollinearity and that the data series for the selected functional form of the study is stationary at mixed order. The results of the ARDL bounds test confirm long-run cointegrating relations between exports and its determinants for Canada. The results further reveal that per capita energy consumption and government final consumption expenditures significantly elevate export performance in both the long and short run, while population size significantly elevates exports performance only in the long run in Canada. Moreover, the findings also expose that real effective exchange rate significantly reduces exports in both the long and short run in Canada: This means that by depreciating Canadian currency, Canadian exports will be boosted. The real interest rate reports a negative but insignificant impact on the Canadian export function in both the long and short run. Finally, the CUSUM and CUSUM Square graphs confirm the stability of the estimated coefficients for the Canadian export function for the selected sample of the study.

Keywords

Introduction

The wellbeing of any society depends solely on its economic development, and the goal of sustainable development cannot be achieved without persistent economic growth. This relationship has already been explored, tested, and applied in many countries with the primary objective of each country making its entrance into the global market. Canada’s economy is an exceedingly advanced market economy. Canada’s total exports are over CA$585 billion while its imports are over CA $607 billion and its GDP rank is nine globally (SKVMES, 2020).

Government executives, policymakers, and academics worldwide are concerned with the almost austere results of appreciation of a currency on domestic production and exports (Liu et al., 2013). If there is an increase in the real exchange rate, domestic products are more costly compared to goods produced and sold internationally and therefore not economical. Other things being equal, an appreciation of the domestic currency will increase the domestic real exchange rate, in turn lowering effectiveness and ultimately distressing export volumes. An increased exchange rate will also change exporters from profitable to less profitable. Haddad and Pancaro (2010) and Eichengreen and Gupta (2013) assert that exchange rate depreciation can be used as a policy instrument to spur export and economic growth in the short run, since a country cannot indefinitely sustain a depreciated real exchange rate. According to Huang et al. (2014), fluctuations in the exchange rate affected the Canadian economy under the flexible exchange rate system. Appreciation of the Canadian dollar shows a significant effect on the exports weighted exchange rate, but not on the imports weighted exchange rate.

The main idea of this research is to explore important factors that may impact export performance for a developed economy like Canada. In this context, the present study takes into account the role of the real effective exchange rate, the real interest rate, government final consumption expenditures, energy consumption per capita and total population for testing the export performance.

There is plenty of research (see, e.g., Bostan et al., 2018; M. S. Hassan et al., 2017; Lupu et al., 2018; Thuy & Thuy, 2019) available to explore the conventional determinants of exports. This study contributes in existing literature by adding public spending as one of the major determinants behind export performance in the context of Canada. Furthermore, the study provides country specific insight to see long-run as well as short-run relationship.

The research paper is organized as follows. The next section offers a literature review, then data sources, model, and estimation technique are discussed in section 3. The fourth section presents detail on the results and provides comments. The last section consists of a conclusion and possible policy implications.

Literature Review

Economic theory postulates exports as surplus between domestic supplies and domestic demand. There are many factors from both demand and supply sides that affect export performance of an economy. Along with these factors, macroeconomic and social determinants are also equally important to enhance the export performance of a country. Cost of capital and relative domestic prices can boost/hinder the export performance of an economy. High cost of capital leads to lower the investment expenditures which in turn fall the supplies and vice versa. Relative domestic prices also generate incentives to enhance production and export to international market. Moreover, higher energy consumption also leads to raise the output of economy. As a result, greater domestic supply creates a surplus to be exported to other economies. Labor force in economy also enhances output in a similar fashion. Public spending provides producers greater external benefits lead to lower the cost of doing business. This further enhances the profitability of businesses.

The Impact of Exchange Rate on Exports

Kiprono (2019) investigated the exports performance of coffee in Kenya from 1980 to 2018 by using the Error Correction Model (ECM) and by considering indicators such as the World’s real gross domestic product in time t; the real effective exchange rate; FDI inflows; trade openness; institutional quality by rule of law; and exporting capacity by capital formation. The real effective exchange rate, FDI inflows, and institutional quality are significant and positively related to exports. The devaluation of Kenyan currency favors coffee exports, so the government should consider competitive exchange rate regimes through monetary institutions and give subsidy to agricultural services. Thuy and Thuy (2019) used the bound testing approach to analyze outcomes of instability of the real exchange rate on exports in Vietnam, consuming quarterly data for 4 years from 2000 to 2014. The results revealed that in the short run, there is a negative consequence of exchange rate instability and devaluation on exports, but in the long run, as consistent with a J-curve, depreciation has a positive impact on exports volume.

M. S. Hassan et al. (2017) assessed the role of the real effective exchange rate on the trade deficit of Pakistan, India, and Bangladesh. Three separate ARDL models demonstrated that exchange rate devaluation showed a positive effect on the exports of Pakistan and Bangladesh, while it proved insignificant in India. Fugazza and Molina (2016) identified the major determinants of patterns and duration of trade relationships across three country groups by empirically using the Probit random effects model from 1995 to 2004. The results in 96 countries at first revealed three different findings, where export value is absolutely correlated with export existence. Secondly, the affiliation among the export period and the kind of the product explains the competition pattern. Thirdly, fixed costs to export in emerging southern economies rise at the time of export, whereas in developing southern and northern countries, those costs diminish. Epaphra (2016) examined the factors distressing export performance in Tanzania for the period 1966 to 2015 by using Johansen’s cointegration and Granger causality. Error correction modeling is also used to empirically estimate the stable long-run association amongst the determinants of exports; results suggested that real per capita GDP, trade liberalization, and the exchange rate are positively related to exports of Tanzania, while official development assistance is negatively related to exports. Granger causality also proved a trend of causality among exports and economic evolution. Malhotra and Kumari (2016) examined export determinants of designated Asian economies (East Asia, Southeast Asia, and South Asia) during years 1980 to 2012 by using the Ordinary Least Square (OLS) method to evaluate the influence of export performance. Beside with conventional demand and supply as real effective exchange rate, world demand, capacity or production level, and relative prices, it also includes foreign direct investment invasions and trade on exports performance. It has been observed that volatility in the exchange rate can increase export volume. Gupta et al. (2015) explored the exports determinants of IT companies in India from 2000 to 2012, using company-level data with the help of ordinary panel data regression; the study found that world demand and the real effective exchange rate have an anticipated relation to exports of a country. Unexpectedly, foreign capital has an inverse coefficient, emphasizing the relationship between domestic demands and exports. Research and development is insignificant. The reason for this may be that these companies’ expenditure on research and development was low in the early 2000s.

Panda and Mohanty (2015) examined the effects of real exchange rate volatility by using Johansen cointegration on India’s exports for the period 1970 to 2012. Their study used a simple rolling standard deviation as a measure of exchange rate volatility and found that there exists a co-integrating relationship among exports, world GDP, and real exchange rate volatility. World GDP is positively related to export volume in India, and real exchange rate volatility negatively affects export volume. That moderation in the exchange rate is required was empirically proven in the results. Nyeadi et al. (2014) empirically tested that the growth rate of exports is considerably robust and evaluated the increase in exports due to changes in the real exchange rate in Ethiopia and Tanzania. Their results suggested that undervaluation enhances export supply and export modification, as observed in Tanzania with a high interest rate. That same study reported opposite results regarding that exchange rate movement shows no significant impression on the exports of goods in Tanzania. Butt (2013) examined the relationship of exchange rate volatility and exports of eight developed states, including Canada, to determine a positive association, especially using Pooled Ordinary Least Square, Fixed Effect Model, and Random Effect Model from 1991Q3 to 2011Q4. Gross Domestic Product, volatility in exchange rate, and the Consumer Price Index are independent variables, while total exports are the dependent variable. The “Moving Average Standard Deviation” method is used to measure exchange rate volatility that shows a positive association amongst volatility in exchange rate and exports. The strong financial sector of advanced nations helps the traders survive in ambiguous situations formed by a volatile exchange rate. M. U. Hassan et al. (2013) assessed the role of exchange rates on the exports of Pakistan. Using the ARDL model, their results showed that exchange rate devaluation had a positive effect on exports.

Anagaw and Demissie (2012) determined the export performance of Ethiopia by using Johansen’s Cointegration Methodology and their Vector Error Correction modeling for the years 1970 to 2010. Variables included real GDP at home, exports plus imports, official development assistance, the real exchange rate, public expenditure, and private sector credit. The real exchange rate, private sector credit and trade have a positive and significant association, showing a long-run relationship with export performance. To improve export performance and economic growth in Ethiopia, infrastructural facilities and credit to the private sector should increase. Majeed and Ahmad (2006) found the core factors for export determination in developing nations by using a sample of panel data for 75 developing nations for years 1970 to 2004. The fixed effects method is used to assess the association of exports with its possible factors founded on the panel data. Gross Domestic Product, exchange rate, the effect of labor force growth, and industrialization for economic growth have a positive and significant association. It is suggested that a stable exchange rate policy and sustainable growth patterns promote exports. Choudhry (2005) compared the impact of exchange rate volatility in the US to Japan and Canada’s exports, during a flexible exchange rate time period between 1974 and 1998, by using the Johansen Multivariate Cointegration Technique and Error Correction Model to observe the relationship among exports determinants. Conditional variance from the GARCH model was used as exchange rate volatility. Results showed a significant and negative impact of exchange rate volatility on real exports, and a long-run relationship was observed between real exports from the US to Canada.

Hypothesis # 1: Appreciation or depreciation of exchange rate has positive effect on exports.

The Impact of Interest Rate on Exports

Bostan et al. (2018) evaluated the continuous exchange rate influence on Roman worldwide commercial trade effectiveness from 2007 to 2014. The study found how the exchange rate and interest rate negatively influence Romanian exports and imports by using the OLS method. The Consumer Prices Index, imports, portfolio investments, and foreign direct investments show a significant and positive impact on exports of OIC countries. The focal point of their study is to evaluate the effect of the exchange rate on global trade effectiveness and its relations among factors. Sonaglio et al. (2016) evaluated the effect of fluctuations in the monetary and exchange rate strategy and in the configuration of the total exports on the enactment of Brazil by using a structuralist model. The results strengthen the significance of the manufacturing sector to economic development, specifically in a reasonable exchange rate environment. This exchange rate valuation may be taking place due to changes among local and global interest rates. In another study, Oo et al. (2019) found negative long-run as well as short-run relationship between interest rate and exports. They used the panel ARDL technique by using data from ASEAN countries for the period 2000 to 2015. They concluded that stability in interest rate enhance the export performance of the economies.

Hypothesis # 2: Interest rate has negative effect on exports.

The Impact of Energy Consumption on Exports

Ahmed et al. (2017) empirically identified energy-to-export and energy-to-agricultural relationships by using time series analysis and causality and cointegration tests for the time period between 1967 and 2015. Unidirectional causality was observed from energy consumption to agricultural progress, although energy consumption and export showed no connection. To avoid its hostile impacts on sector growth, steady liberalization of energy prices for agricultural usage is suggested. Molina and Roa (2014) followed the reverse causality approach to test the association between the demand for domestic credit and export presentation of Colombian exports. The authors found a positive effect of credit on exporter’s revenue, and their study further analyzed the impact of credit on the size of the manufacturer to show that medium and large manufacturers tend to use credit for exploring market destinations and reach. At the same time, Molina and Roa (2014) observed no significant gain of credit for small manufacturers. Erkan et al. (2010) determined the effect of internal energy consumption on exports in Turkey for the period 1970 to 2006 by using cointegration and Granger causality tests and impulse response functions. Results showed a significant association in the long run among domestic energy consumption and exports, along with a unidirectional relationship between them. Impulse-response functions specify the positive impact of energy consumption shocks on exports. Consequently, energy is a vital aspect for economic progress in Turkish economy. Sami (2011) discussed the relationship among exports, income per capita and energy consumption for 1960 to 2007. By applying the bound-testing approach, the results of Sami’s analysis revealed co-integration among energy consumption, exports, and economic growth.

Hypothesis # 3: Energy consumption has positive effect on exports.

The Impact of Population on Exports

Mdanat et al. (2018) identified the factors distressing exports in small open economies by using the panel data technique and the gravity model, targeting 2001 to 2014. Their findings are appropriate for policy makers in small economies that are involved in free-trade agreements (FTA) and trade liberalization. This same study established mixed results toward the direction of the affiliation among FTA and exports; income boosts exports, so a positive relationship results, whereas distance and cost have an inverse relationship on exports. It is suggested that policies aiming to take full advantage of trade agreements and reduced costs may be supportive in endorsing exports. Oliveira et al. (2020) explored export divergence and its determinants for different sectors of the Brazilian economy between 2003 and 2013 by using general methods of moments. Results found that the Southeastern states and the southern region have much more diversified exports than the Northeastern states, and in the Central-West region diversification started in 2006. They count all Brazilian federations, previous divergence performances, patents per capita, education, public investments, and credits established as significant factors of Brazilian export divergence. Nuroglu (2010) investigated bilateral trade movements and their determining factors between six large OIC economies by using the panel data technique for 2007 to 2014. This study also encompasses the gravity model of bilateral trade with exchange rates volatility and population to use in panel studies; Noroglu highlighted in particular the positive impact of population on a country’s trade flows and methodologies to the subject of population size from a controlled perception, whereas its impact is adverse for the importer country. The positive impact of population is a good sign in bilateral trade for an OIC, specialization opportunities in production enhancement and the opportunity to export more goods and services.

Hypothesis # 4: Population has positive effect on exports.

Based on the above discussion, the present study attempts to justify export function for Canadian economy using various empirical studies of the scholars and this discussion is presented as below:

Theoretical Justification for Selecting the Export Function for Canadian Economy

For the assessment of the exports of any country, the determinants are generated from the theory of firms. This study has proposed two indicators which hinder the process of goods production and movement abroad. The indicators like the real interest rate and the real effective exchange rate are taken to assess the effect of cost of capital and relative prices of domestic goods. While other indicators like energy input utilization, labor force available, and government expenditures are proposed indicators that promote exports as they help make production more competitive compared to foreign countries. We initiate by referring the contribution of Bostan et al. (2018) and Oo et al. (2019) who guided us for considering interest rate as determinant of export function. Besides them we find Thuy and Thuy (2019) who provided positive impact of the real effective exchange on exports for the long run but a negative impact of the real effective exchange rate on exports is also reported in the short run in the case of Vietnam. On the other hand, Ahmed et al. (2017) have reported a negative but insignificant impact of the exchange rate on export performance in Pakistan. In another study, M. S. Hassan et al. (2017) reported that real effective exchange rate helped in improving trade balance and hence export performance in Pakistan and Bangladesh cases while it remained insignificant in case of Indian economy. By considering these studies, we feel motivated for taking real effective exchange rate as determinant of exports for Canadian economy. Besides this, the studies by Sami (2011) and Nnaji et al. (2013) found unidirectional causal relations running from energy consumption to exports, while Li (2014) and Erkan et al. (2010) disclosed a positive impact of energy consumption on exports. We therefore incorporated the role of per capita energy consumption in export function to see how it will impact Canadian export function.

Afterwards, the contributions of Joshua (2019) and Oluwafemi and Laseinde (2019) for the Nigerian economy and Kunwar (2019) for Nepal have found a positive impact of government expenditures on economic growth. Besides this, M. S. Hassan and Kalim (2012) exposed bidirectional causal relation between government expenditures on education and economic growth in both long and short run while government expenditures on health had bidirectional causality with economic growth only in long run. In another study we found Maryam and Hassan (2013) who disclosed positive and significant impact of public spending on education on trade openness in long and short run in Pakistan while health expenditures left insignificant impact on trade openness. Besides them, we see Kalim and Hassan (2014) who reported that public development spending was helpful in controlling poverty in Pakistan. The study by Dalango (2020), however, reported a positive impact of per capita GDP on the export performance of Ethiopia. Based on these studies, the present study concludes that there is hardly any study in the literature that directly captures the impact of government expenditures upon export performance and therefore this study is going to contribute in the literature on the relation between public spending and export performance by inspect the impact of government spending on export performance of Canada. This is the motivation for considering public spending as part of export function into the present research. Moreover, in one of the researches, M. S. Hassan et al. (2012) took urbanization and unemployment as determinant of trade openness for Pakistan economy and reported that urbanization significantly curtailed trade openness in the long run while it encouraged it in the short run. The unemployment appeared as elevating force for trade related activities in both long and short run in Pakistan. Besides this, Ali et al. (2013) considered population growth as a determinant of economic growth and found a positive impact in the long run, which negatively impacted the short run on economic growth in Pakistan’s case. M. U. Hassan et al. (2013) considered labor force as a determinant of export performance and found a negative impact on export performance in the long run but in the short run, their study revealed a positive impact. We then see M. S. Hassan et al. (2014) who found positive and significant effects of real effective exchange rate and both rural and urban population on import function in long and short run in Pakistan. From these findings, the present study considered population growth as an important determinant of exports function in Canada.

Afterwards, we see M. S. Hassan et al. (2022) who disclosed significantly positive impact of gross fixed capital formation on economic growth in short run in France, Finland, and Portugal while Wang et al. (2022) reported the positive impact of gross fixed capital formation on economic growth in both long and short run in Pakistan. These studies set the base for taking capital as determinant of our export function for Canadian economy. The entire discussion has set up a base for conceptualizing export function for the Canadian economy.

This section has actually provided us the rationale for empirically testing export function for the Canadian economy. The entire discussion presented above provides assistance in extracting various determinants of exports for Canadian economy. The literature on exports determinants is rich for the case developing economies but for the case developed economies such as Canada, not enough research has been carried out. The present study seeks to fill this gap by identifying the impact of various export determinants. We use similar hypotheses for our analysis, using the variables that provide significant relationships for other countries.

Methods

Sources of Data Collection

This study collected data for exports of goods and services, real interest rate, government final consumption expenditures, total population, and real effective exchange rate from World Bank (2020). The unit of the data is constant in local currency units. However, we have the selected the data range from 1979 to 2019. The selection for the period of study is purely based on data availability. This range has data for all variables.

Functional Form of the Study

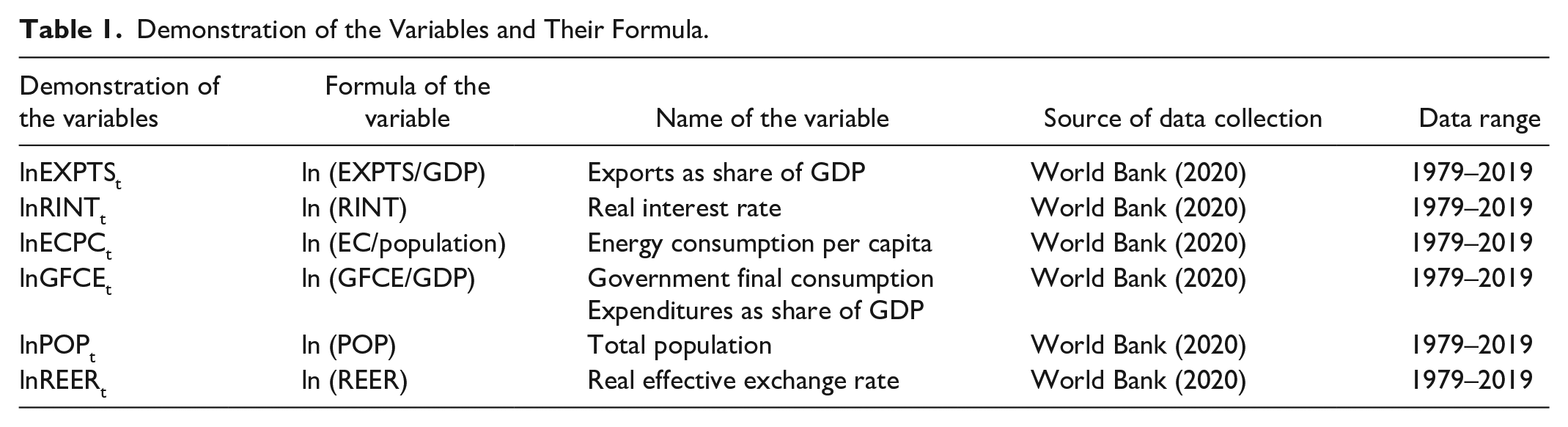

In this research, double log form approach is considered for estimating robust results as exposed by many scholars like M. S. Hassan et al. (2012, 2015, 2016, 2018, 2021), Mamoon et al. (2017), Iftekhar et al. (2016a, 2016b), Kalim and Hassan (2014), Satti et al. (2014), Ehrlich (1977), Layson (1983), Bowers and Pierce (1975), Cameron (1994), and Ehrlich (1996) in their researches. They were of the view that the results are robust, efficient, and consistent if these are calculated by using double log transformation approach. Based on their conclusion, in the present research, we will follow the following function for further estimation procedure (Table 1):

Whereas:

Demonstration of the Variables and Their Formula.

Results Estimation Method

Testing for unit root

In this study, we will use Ng and Perron (2001) unit root test for testing whether there is evidence of unit root in the data series or not? In the null hypothesis, the test suggests “series is nonstationary” and in the alternate hypothesis it proposes “series is stationary.” The decision about the test is made on the basis of the value of MZa test. If the calculated value of MZa would be find less than its corresponding critical value at 10% level of significance then we will fall in the critical region where we would reject null hypothesis and conclude that series is stationary and vice versa. This process will allow us to conclude about the order of integration of the data series. This unit root test is relatively more efficient as compared to the earlier versions of unit root tests like Phillips and Perron (1988) and Augmented Dickey and Fuller (1981) tests. In the below given equations (2) to (4), the Ng–Perron unit root test procedure is provided.

Testing for long run cointegrating relation

In the present research, we would be applying the renowned method developed by Pesaran et al. (2001) for testing long run cointegrating relation between dependent and its independent variables in the presence of mixed order of integrated data series. It is also known as ARDL bounds testing Approach. The null hypothesis of “No Cointegration” will be rejected if the calculated value of “F-Statistic” would be found greater than the corresponding 5% or 10% critical value of “Upper Critical Bound.” If the long run cointegrating relation between dependent and its corresponding independent variables is confirmed for the selected ARDL model, we will find long run and short run coefficients for explaining the impact of independent variables on dependent variables. For finding long and short run coefficients for this research, we would use the following equations:

Error correction model

Once we would be finished with the long run coefficients, we would calculate error correction representation for the selected ARDL model. This would also be called as short run coefficients. In the short run equation, one period lagged term in addition to first differenced terms of all the selected variables will be presented. The one period lagged term of error term should be negative and significant to provide evidence that the proposed functional form in this research has the strength to converge to long run and stable equilibrium if any of the macroeconomic shock converts the long run equilibrium into disequilibrium. The coefficient of one period lagged term of error term will signify the speed of adjustment. If we may divide one upon the one period lagged term of error term, we would be able to identify the required time to achieve long run and stable equilibrium again. For estimating coefficients for short run we would use the following equation (6):

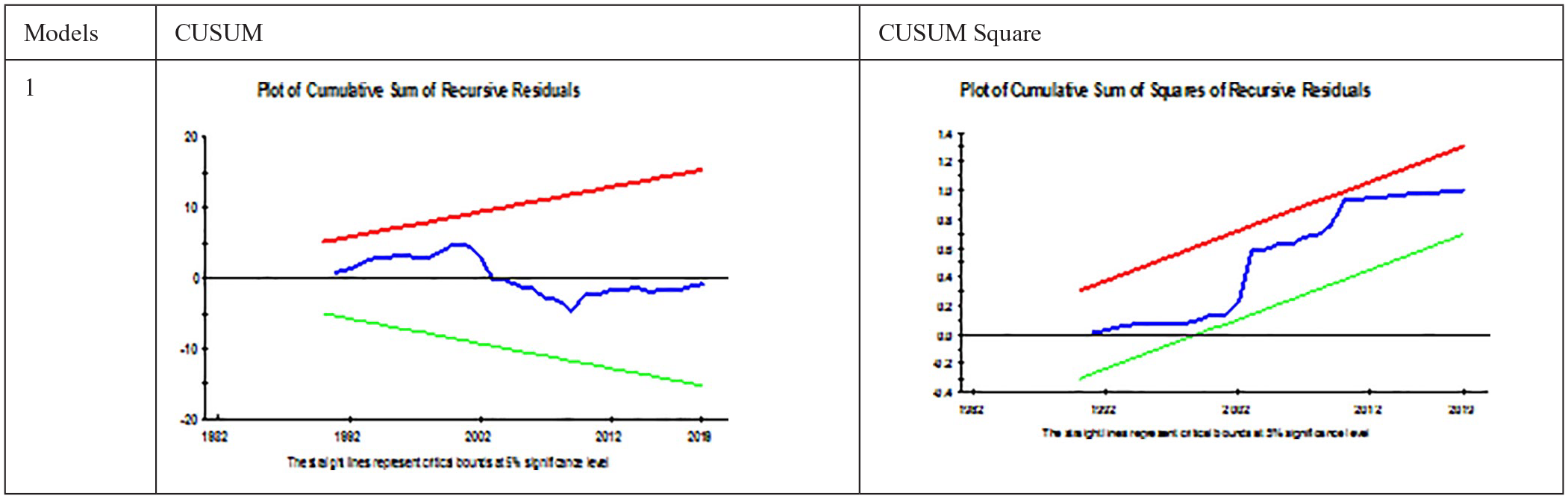

Besides finding short run coefficients for this research, we would also use stability diagnostic for confirming that the mean and variance of error term are stable or instable. If they are stable then the estimated coefficients of the proposed model of this study would not have any evidence of structural instability. If the mean and variance of error term will be found instable, then the estimated coefficients will be instable. This would be confirmed by looking at the diagrammatical portion of the study in the result section where we would be reporting Cumulative Sum (CUSUM) and Cumulative sum of Square (CUSUMSQ) graphs. If the mean and variance of the error term will be found within their critical bounds, we would conclude about structural stability.

Estimated Results and Interpretation

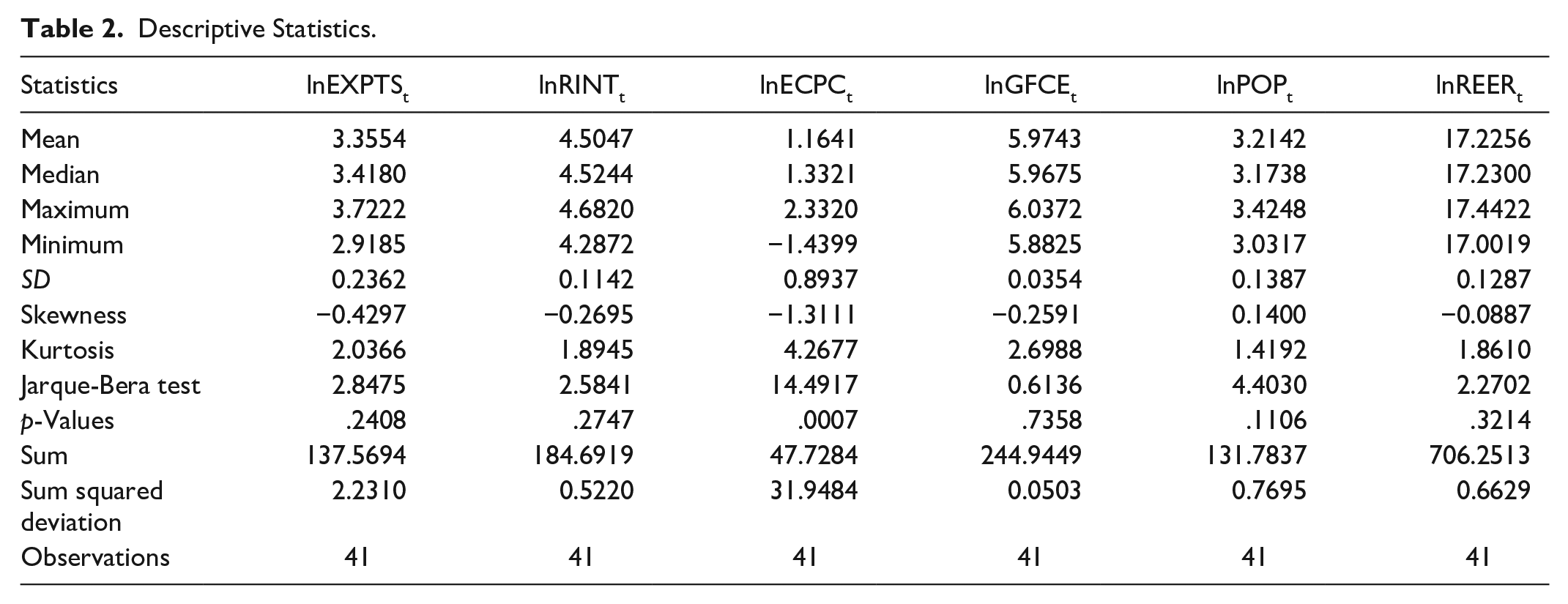

The present section is designed to present estimated results for the proposed functional form in the study. The results are estimated in a series of steps from the Descriptive Statistics to the Stability Test. We will begin by sharing and interpreting results for the descriptive statistics. The results shared in Table 2 show that the probability values of all selected variables for the study, except the natural log of energy consumption per capita, are insignificant, hence they follow the properties of normal distribution. The findings regarding the descriptive statistics are presented in Table 2.

Descriptive Statistics.

Besides explaining the descriptive statistics results, we may now shed light on the coefficient of correlation matrix and the variance inflation factor (VIF) matrix. The coefficient of correlation matrix is calculated only for the determinants of exports to diagnose whether or not any pair of determinants of exports are significantly correlated. For this purpose, we further calculated the matrix of variance inflation factor by using the formula VIF = [1/ 1 − r2]. This would provide us evidence of the presence or absence of multicollinearity issues. If the calculated value of the “VIF” measures at 10 or above, we may conclude the presence of multicollinearity, and vice versa otherwise. Table 3 shows that no pair of independent variables was found at the value of “VIF” 10 or above, leading us to conclude that the multicollinearity issue is absent in the present research. Table 3 exposes all the results regarding both the correlation and VIF matrices:

Coefficient of Correlation and Variance Inflation Factor Matrix.

I. Variables represents independent variables.

The estimated results for testing stationarity by using Ng–Perron’s unit root test are presented in Table 4. The findings show that the natural log of exports, the natural log of real interest rate, the natural log of government final consumption expenditures and the natural log of total population are nonstationary at level specification because the calculated values of the MZa test was found to be greater than their corresponding critical value for all these highlighted variables at 10% significance level; thus, we accept a null hypothesis for all the mentioned variables and conclude that these are nonstationary at level. As far as the natural log of real effective exchange rate and the natural log of energy consumption per capita are concerned, both are stationary at level because the calculated values of MZa for both real effective exchange rate and energy consumption per capita remain less than the 10% critical value, so both factors fall in the critical region. Therefore, we reject a null hypothesis for both factors at level specification and conclude that both are stationary or I (0) variables.

Ng–Perron Unit Root Test.

Source. Ng and Perron (2001).

Note. Asymptotic critical value at various levels of significance for MZa statistic are −13.8 (1%), −8.1 (5%), and −5.7 (10%).

Besides this, all variables were tested for first difference, and we found that the calculated value for all the variables falls in the critical region; therefore, we accept an alternate hypothesis for all the variables and conclude that all variables are stationary at first difference. The entire discussion regarding the reported results in Table 4 concludes that the real effective exchange rate and energy consumption per capita are I (0) variables, while exports, real interest rate, government final consumption expenditures, and total population are I (1) variables. This provides evidence of a mixed order integration regarding the selected variables in the study. When there is evidence of nonstationarity about the data series, then the findings of an ordinary least square technique become redundant. Econometrics experts suggest applying an alternate technique to account for the nonstationarity issue, that is, the cointegration method. Pessaran et al. (2001) provided a cointegration technique that is efficient for a data series integrated at mixed order. This method is known as the ARDL bounds testing approach.

The results presented in Table 5 disclose that the calculated value of F-statistic (6.3322) is greater than its corresponding Upper Critical Bound (4.3447) at a 5% level of significance. This allows us to reject a null hypothesis of “No cointegration” and conclude that exports have long-run cointegrating relation with determinants such as the real effective exchange rate, real interest rate, energy consumption per capita, government final consumption expenditures and total population of the selected study sample. Moreover, the results also expose that the variance of the error term is homoskedastic, the error term is not serially correlated, the error term follows attributes of normal distribution and the functional form of the study is correctly specified for the selected sample of the study. This concludes that the results about cointegration are robust as per diagnostic tests. The results are reported in Table 5.

ARDL Bounds Testing Approach.

Note. Also the values within() represents probability values.

and ** Demonstrates significance level at 10% and 5%, respectively.

Table 5 confirms that exports and their determinants have a long-run cointegrating relation with one another; therefore, there is a need for interpreting long and short-run coefficients for the selected ARDL model. The results are reported in Table 6.

Long Run Coefficients for the selected ARDL Model.

The estimates regarding long-run coefficients for the selected ARDL model are reported in Table 6, which demonstrates that the real effective exchange rate has both negative and significant impacts, while the real interest rate has a negative but insignificant impact on Canadian exports. An increase in the real effective exchange rate allows the Canadian currency to appreciate, which raises the prices for Canadian exports; therefore, Canadian exports fall and this confirms the negative relation between the real effective exchange rate and exports. An increase in the real interest rate reduces the banks’ ability to advance credit and the flow of money into the hands of investors falls, all of which reduces production and in turn reduces exports. This confirms the inverse relation between the real interest rate and exports. The third variable is energy consumption per capita, which has both a positive and significant impact on Canadian exports.

An increase in per capita energy consumption also means that energy usage is increased in the manufacturing sector, which means that more production is taking place in the country and this ultimately encourages exports. This establishes a positive relation between per capita energy consumption and exports in the country. The study also provides evidence of the positive and significant impact of government final consumption expenditures and total population on exports. The coefficient of government final consumption expenditures is 0.1549, which shows that a 1% increase in government expenditures increases exports by 0.1549% in the long run in Canada. The results also expose that the increase in population increases demand for goods and services in the country, in turn motivating manufacturers to raise their level of production; after meeting domestic demand for consumption, the rest will be exported. This ensures a positive relation between population and exports in the long run in Canada as it relates to the selected sample and time period.

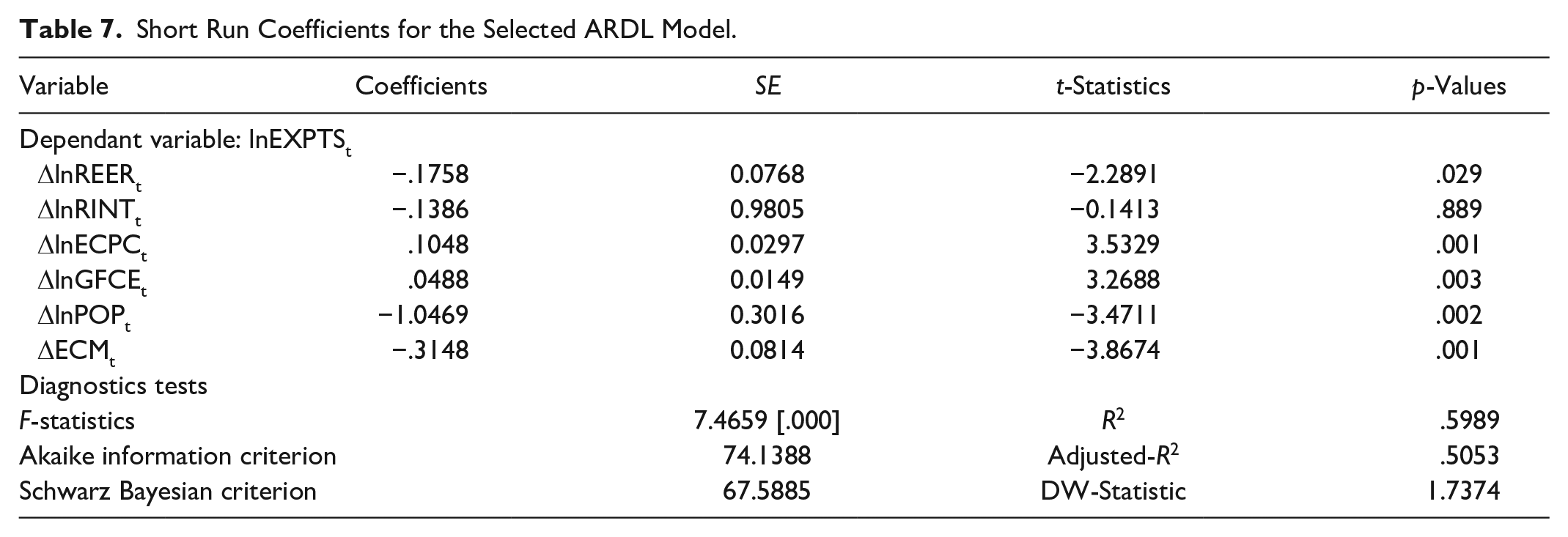

Unlike long-run coefficients, the short-run coefficients are almost similar in terms of signs and significance, except for total population case. The coefficient of the real effective exchange rate and real interest rates are negative. By contrast, the real effective exchange rate has a significant impact on exports. In contrast, the real interest rate has an insignificant impact on exports in the short run in Canada. Moreover, the coefficients of per capita energy consumption and final government consumption expenditures are found to be positive and significant in the short run in Canada, as witnessed in the long run. The coefficient of the total population in the short run is not similar to its coefficient in the long run; this may confirm that in the short run, the increased demand by increased population immediately puts pressure on consumption more than on production. The results for the short run are provided in Table 7.

Short Run Coefficients for the Selected ARDL Model.

Therefore, exports fall rather than increase. The results further demonstrate that the proposed model of this research has the power to converge toward the long run and stable equilibrium point if it is changed into disequilibrium in response to any macroeconomic shock in the short run. This is confirmed because of the negative and significant coefficient of the one period lagged error term. The result shows that the long run and stable equilibrium will be achieved in about 3.18 years by correcting almost 31.48% of errors each year. The results are robust to all the diagnostics used for testing validity. After discussing the short-run coefficients, the stability of the estimated coefficients for the proposed functional form for Canadian Export Function was also tested by looking at the CUSUM and CUSUM squared graphs. The graphs provide evidence that the mean of error term and variance of error term do fall into their critical boundaries, confirming that mean and variance of error terms are stable, so the estimated coefficient for Canadian Export Function is stable. There is no evidence of structural instability. This can be confirmed in Figure 1.

Stability test for the selected ARDL model.

Conclusion and Policy Implications

Discussion and Conclusion

This study was carried out to explore the important factors which may impact export performance in a developed economy like Canada. Among many factors, the present study extracts the real effective exchange rate, real interest rate, per capita energy consumption, government final consumption expenditures and population size as important factors of export performance. In order to propose country specific policies, this study takes time series data for Canada between 1979 and 2019. For testing the unit root issue, we use the Ng–Perron unit root test while investigating long-run cointegrating relations between exports and their factors. Pessaran et al. (2001) is used. Besides identifying long-run cointegration, the study finds long and short-run coefficients for the selected ARDL model and in the end, CUSUM and CUSUM Square graphs are considered for finding stable coefficients for the proposed functionality of this study during the selected time period.

The estimated results confirm the absence of a multicollinearity issue between all the explanatory variables of export function, while the data series provide evidence of a mixed order of integration. The results of Pessaran et al. (2001) disclose evidence of a long-run relationship between export performance and its contributing factors. Moreover, per capita energy consumption and government final consumption expenditures are found to significantly elevate export performance in the long and short run in Canada, while the real effective exchange rate is evident in significantly reducing exports during the same periods for Canada. This confirms that the depreciation of Canadian currency will expand Canadian exports. This finding is in line with studies of Sidheswar and Ranjan (2015), Thuy and Thuy (2019), and M. S. Hassan et al. (2017). The real interest rate is negatively related with exports of Canada. Some other studies also reported similar findings like Boston et al. (2018) and Oo et al. (2019). Increase in energy consumption also leads to enhance exports of Canada. This study supports the results of Erkan (2010) and Sami (2011) but Ahmed et al. (2017) found no connection between energy consumption and exports. The findings also shed light on the role of population size for expanding exports in Canada; therefore, that is taken as a part of export function in the study. The results demonstrate that an increase in population in Canada means that exports will significantly increase, but only in the long run. This is because due to an increase in population in Canada, the labor force will increase, which lowers the earnings of the labor class and in turn lowers labor costs. This will raise demand for labor, so production will increase. In turn, exports will improve in Canada but only in the long run. Similar types of findings were reported by Nuroglu (2010). Finally, the CUSUM and CUSUM Square graphs confirm the stability of the estimated coefficients for the Canadian export function for the selected sample of the study.

Policy Implications

In this study, the impact of various macroeconomic factors on the export performance of Canada is tested by using the famous method developed by Pesaran et al. (2001). The results allow us to propose certain policy implications, presented below:

The negative coefficient of the real effective exchange rate suggests that it is an important factor that may improve Canada’s export performance. Depreciating it on a required time may deliver fruitful results. Policy makers may get some input from these findings while deliberating the policy related to exchange rate.

The other important factor for boosting exports in Canada is seen as per capita energy consumption. The more energy per person would increase the use of energy per manufacturer, which may further translate to an increase in production level. This will allow manufacturers to export the excess after meeting domestic demand. Therefore, energy consumption per person can also help boost exports in Canada. If the government provides energy at the lower cost. This will create an incentive for investors by reducing cost of doing business in Canada.

We have come across only a few studies that capture the direct impact of government final consumption expenditures on exports; that is one unique factor of the present work. The results are supportive in terms of expanding exports in Canada; therefore, policy advisors may also consider this factor for targeting exports in Canada.

The variable of population size is taken into consideration by maintaining Canada’s policy of encouraging people around the world to move to Canada. This would increase the population in Canada, which in turn lowers the cost of labor; this then raises demand for labor and hence raises the level of production in Canada. The increase in production will increase exports in Canada. Increasing the population size could be monitored in such a way that it may help to elevate exports in Canada.