Abstract

While shocks driven by exchange rate volatility and its impact on growth have been investigated in the extant literature, the recent exchange depreciation of major currencies has reignited interest among scholars. This study scrutinizes a novel Bootstrap Autoregressive Distributed Lag (BARDL) model for the effect of exchange rate shocks on the growth of the Nigerian economy. The results reveal several key findings. First, the finding from the bootstrap bound test revealed the presence of a cointegration relation between exchange rate and economic growth, indicating that exchange rate is a key indicator of inducing growth performance in Nigeria in the long-run horizon. Second, the results also show an inverted U-shaped effect of exchange rate on growth performance in the short-run horizon. This finding indicates that the coexistent positive effect of exchange rate shock on growth metamorphosed into a negative effect within a second lag. Third, while exchange rate depreciation retards economic growth in the short-run, the pattern demonstrates a strong potential for currency devaluation on external trade competitiveness of Nigeria. Fourth, the finding from the nonlinear model reveals the existence of strong asymmetries in exchange rate and economic growth nexus which validate the J-curve effect in Nigeria. The shocks driven from trade, particularly the import shocks are exacerbating the instability in the exchange market. Thus, controlling the asymmetric effects of exchange rate and import shocks is key to the sustainable growth of the Nigerian economy.

Plain language summary

The study explores the asymmetric effect of exchange rate and economic growth. The finding shows strong asymmetries in the growth-exchange rate relation in Nigeria.

Introduction

The fall of the Berlin Wall and post-Bretton Wood’s agreement era has attracted so much attention from policymakers, monetary authorities, and researchers to make frantic efforts aimed at investigating the dynamics of exchange rate fluctuations within the framework of growth performance (Bahmani-Oskooee et al., 2016; Bahmani-Oskooee & Gelan, 2018; Lawal et al., 2022; Tunc et al., 2018). While the exchange rate determines the exchange value between two or more currencies, the strategic choice of selecting the exchange rate regime(s) and its management is a serious challenge for policy makers if macroeconomic stability, competitiveness, and sustainable development are to be achieved because different regimes were accompanied by instability and uncertainties (Lawal et al., 2022). Thus, shocks from exchange rate add burdens to countries characterized by a weak level of financial system (Bahmani-Oskooee & Gelan, 2018). Worthy of note, the Bretton Wood’s time was the implementation of floating-exchange rate policies in the currency management (Lawal et al., 2022), triggering instability and volatility in bilateral exchange rates (Bahmani-Oskooee et al., 2016; Ibrahim, 2014).

The African continent is a developing frontier in comparison with its European and Asian counterparts, though some economies in Africa have begun exhibiting signs of growth potential (Iliyasu et al., 2024; Lawal et al., 2022). There are major dichotomy regarding exchange regimes: fixed and floating. while fixed exchange rate requires pegging the exchange value of currency with the best foreign currencies, whereas in floating (flexible) regime connotes allowing market forces to determine the exchange rates (Shagali et al., 2019). In Nigeria for instance, the management of exchange rate has started with fixed rate regime between independence in 1960 until 1986 when Structural Adjustment Programme (SAP) was implemented. Series of problems such as unrealistic exchange value, trade deficit, debt overhung, and depletion foreign reserve characterized the fixed exchange regimes (CBN, 2021). To resolve these pitfalls, a floating exchange rate was implemented under the comprehensive market reforms in the guise of SAP (Adeniran et al., 2014). A mounting body of empirical literature have explored the roles of SAP-induced exchange rate on the performance of Nigerian economy (Aliero & Ibrahim, 2010; Adeniyi & Olasunkanmi, 2019; Ehikioya, 2019; Onafowora & Owoye, 2008).

Despite the multiplicity of exchange regimes and various reforms implemented in the context of growth agenda, the performance in Nigeria in terms real growth is far below the expected average (Aliyu et al., 2021; Lawal et al., 2022). This lends credence to the fact that the most common insight on currency value is the “bilateral-exchange rate” which is often quoted in the FOREX market as a nominal exchange rate (Levich, 1985). For instance, the dual exchange rate at a point in time is partly driven by currency protection due to negative net-export, the dominance of the informal sector, and perennials oil price volatility (Aliyu et al., 2021; Lawal et al., 2022).

Currency appreciation could mean an improvement in the productive based in the country in the tenet of the market-driven exchange rate (Adeniyi & Olasunkanmi, 2019; Ehikioya, 2019). Depreciation of exchange rate can also lead to a growth in output since import will be costlier and export will become cheaper. This is premised on the capacity on the local producer to respond rapidly filling trade deficit. Currency will then appreciate due to favorable external trade competitiveness (Aliyu et al., 2021; Shuaibu et al., 2021). However, a mounting body of empirical pieces of evidence have shown that the devaluation of the Nigerian currency has a minimal impact on growth and trade competitiveness (Adeyemi & Ajibola, 2019; Omojimite & Akpokodje, 2010) due to production rigidities (Iliyasu et al., 2024). As such, exchange rate volatility could shape the patterns of well-being and economic growth in Nigeria (Aliyu et al., 2021; Usman & Ibrahim, 2021).

It remains plausible whether shocks associated with exchange rate can significantly influence output, particularly in a resource-dependence country like Nigeria. This study explores the impact of exchange rate volatility on economic growth in Nigeria. The study further examines the asymmetries in the growth- exchange rate nexus using the novel Guris (2019) asymmetric unit root and the Shin et al. (2014) nonlinear autoregressive distributed lag (NARDL). The study built on extant studies and made significant contribution to the literature on three grounds: first, extant studies investigated the nexus between exchange rate, and growth (Adjei, 2019; Iqbal et al., 2023). These studies have failed to bring into context the asymmetries net-trade, particularly the roles of import shocks on exacerbating the instability in the exchange market. Second, this study is among the first studies that employed a novel bootstrap model, particularly on exchange rate volatility in Nigeria which is a key driver of inflation and economic growth. Unlike extant studies that applied static models (such as Aliyu et al., 2021; Ibrahim, 2014; Lawal et al., 2022) and traditional distributed models (Shuaibu et al., 2018; Shuaibu et al., 2021) the current study adopted the BARDL which was characterized by a robust standard error, asymptotic for small sample, flexible with mixed order integer and controls for endogeneity. Third, the study draws a theoretical guide from the Marshall-Learner theory which captured import quotas and export subsidies, the J-curve theory which is concerned exchange rate asymmetry and trade balance, and the market theory of exchange rate determination concerned with free market mechanism.

The remainder of the paper is organized as follows; section “Stylized Facts” provides some stylized facts about exchange rate and trade, Section “Literature Review” covers the literature review, the empirical methodology is described in section “Methodology,” section “Empirical Results and Discussion” is the result and discussions, and section “Conclusion” concludes.

Stylized Facts

Nigeria is one of the developing countries struggling to stabilize its currency against international currencies. Since independence in 1960, exchange rate targeting framework was used as a strategy of enhancing the international value Naira legal tender, ensure price stability, maintain a robust external reserve and reduce exchange change rate volatility. Under this fixed exchange regime, monetary authority was empowered to pegged the Naira against the strongest currency at the foreign exchange market (Iliyasu et al., 2024). Aftermath the oil boom of 1970s, the currency support through exchange rate targeting became unstainable. As such, Naira became over-valued with attendant macroeconomic pitfalls such as external debt overhung, massive imports, uncompetitive exports, worsening terms of trade (Ibrahim et al., 2019) and depletion of external reserves (CBN, 2021). A stylized statistical data points a stationary export value of $ 0.40 billion from 1960 to 1964 whereas import rose from $ 0.7 billion to $ 0.85 billion over the period. The widened disparity between export and import has posed a daunting challenge of meeting up the legitimate demand for foreign exchange (Adetayo et al., 2004; Usman & Ibrahim, 2021).

To ameliorate the pitfalls associated with fixed exchange regime, a Second-tier Foreign Exchange Market (SFEM) was implemented under the broader framework of Structural Adjustment Programme (SAP) in 1986. This reform was aimed at providing enable environment for the full implementation of floating exchange rate as both invisible hand and other prevailing economic condition were key determinants of exchange rate (CBN, 2021). The SFEM is characterized with dual exchange window consisting of the first-tier (window for government official) and second-tier (a market-driven window for commercial activities) foreign exchange market. This dualist exchange rate has encouraged a round-tripping, speculation and fictitious bidding in the dual windows. Under the transitional period, 1986 to 2006, various reforms were implemented in the management of exchange rate in Nigeria. The salient policy reforms to fine-tune foreign exchange including the implementations of the Dutch Auction, Autonomous Foreign Exchange Market and Interbank Foreign Exchange Market (CBN, 2021; Ibrahim, 2014). However, these policy reforms have grossly failed to address the volatility in the exchange rate market due to lack of transparency, bureaucratic delay, mono-cultural economy, inflated demand and round-tripping (Campbell, 2010; Hanna et al., 2023).

With earnings majorly from oil export, Nigeria was able to generate an average export value at tune of $18.08 billion and import value at $10.89 billion from 1986 to 2006 (Wowo et al. 2023). Aftermath the global economic meltdown in 2007 which led to sharp decline of oil export, foreign exchange market was liberalized (AlGhazali et al., 2023; Ibrahim & Tanimu, 2016). Yet, concessionary rate was retained for government officials, investors and exporters. This has led disparity in exchange rate between the official window and parallel market (dominated by the unregulated bureau de change). In response to the declined in export from $67.48 billion in 2019 to $35.09 billion in 2020 triggered by COVID-19 pandemic, an exchange unification policy was implemented in May 2023, with aim of allowing market forces to determine the effective exchange (Iliyasu et al., 2024). However, the currency is still susceptible to speculative attacks exacerbated by the excess liquidity in the banking system, increased shadow economic activities and crude oil price volatility (AlGhazali et al., 2023).

Literature Review

This section discusses the theoretical settings and the empirical literature in which this study bases it arguments, contributions and findings.

Theoretical Settings

Several theories were advanced in explaining the determinants of exchange rate volatility, particularly in the context of stimulating growth. The Marshall-Lerner (ML) theory argued that the exchange rate and growth nexus can best be measured based on the interaction of the restrictive import quota-tariff and expanding exports’ subsidies (Iliyasu et al., 2024). In this way, the theory stipulated that when a country imposes quota and tariff to regulate the economy’s imports and simultaneously offer export subsidies, the value of the national currency appreciates since the demand for costly imported commodities will fall relative to domestic substitutes. At the same time, the export will become cheaper and in turn induce a rise in the in demand for domestic goods at the international markets (Lawal et al., 2022). However, this view has long been criticized by economists who argued that the global trade partners might also impose counter-tariffs and quotas which will inevitably induce increases in global prices of commodities, reduces aggregate demand, slows growth, and decreases employment (Aliero & Ibrahim, 2010; Bahmani-Oskooee & Gelan, 2018) which could possibly trigger a currency war similar to recent China-United States debacles (Lawal et al., 2022). However, the theory posit that currency depreciation improves a trade balance only if and only if the total trade is elastic (Bahmani-Oskooee & Gelan, 2018). A plethora of empirical studies have tested the validity of ML theory and found conflicting findings. For instance, controlling for simultaneity in export and import flow, Sastre (2012) found that devaluation exhibits a tendency for the improvement of balance of trade in Spain. Thorbecke (2022) demonstrates that while the net-export elasticities are insufficient to meet the ML condition, yet, depreciation raises the aggregate stock return. In this way, exchange rate has made a dramatic impact on the performance of Japanese economy. However, using structural VECM, Ibrahim and Tanimu (2016) documented a significant positive nexus between economic globalization and exchange rate depreciation of Nigerian currency. Dong (2017) discovers that high depreciation of real exchange rate does not boomerang into better bilateral trade balance between the US and other G7 member countries. Cavusoglu et al. (2019) assert that price elasticities for imports and export hardly conform with the ML condition. The economic usufruct related to the currency undervaluation is nearly zero regardless of the exchange rate regime in Sub-Saharan Africa (Iliyasu et al., 2024; Owoundi, 2016; Shagali et al., 2019; Usman & Ibrahim, 2021).

On the other hand, the J-curve theory highlights the asymmetric short and long-term effects of the devaluation on trade balance (Bahmani-Oskooee et al., 2016; Lawal et al., 2022). The theory advocates that at the initial stage, devaluation will lead to an upsurge in expenditure on imports, considering that consumers buy more imported goods with their domestic currency at a price much higher (Bahmani-Oskooee & Gelan, 2018; Lawal et al., 2022). However, the export prices will become cheaper aftermath the devaluation, since domestic firms will receive relatively less payment. Therefore, these apparently conflicting conditions only happen in the short run, given the fact that demand for foreign goods will eventually reduce, whereas demand for domestically exported goods will rise significantly (Bahmani-Oskooee & Gelan, 2018). On empirical ground, Alessandria and Choi (2021) validated the J-curve effect for the US and found it effect largely depends on whether trade policies have induced a trade war. A condensed body of literature demonstrates heterogeneity in exchange rate volatility as trade balance responds more to depreciation shocks than appreciation shocks (Antonio & Luis, 2022; Bosupeng et al., 2024; Vural, 2016).

The market theory of exchange rate determination applies the tenet of demand and supply consistent with the conditions of a free market (Ibrahim & Tanimu, 2016). This theory argued that the exchange rate is determined by the price of a commodity (CBN, 2021; Levich, 1985) which will influence the dynamism of market forces in foreign exchange market. A higher price reduces the demand for foreign goods through import reduction (Iliyasu et al., 2024; Shagali et al. 2019). Lowering import signifies lowering demand for foreign exchange. On the other hand, when exchange rate decreases, imported commodities become less expensive which will lead to increase in import. The increasing imports will lead to a greater demand for foreign exchange (Campbell, 2010; Ibrahim & Shagali, 2019). The applicability of these theories has often verified by employing empirical datasets from several countries but the findings were contradictory (Alessandria & Choi, 2021; Doojav et al., 2024; Fisera, 2024; Truong & Van Vo, 2023). As such, this study contributes in re-assessing these theories using a novel bootstrap ARDL which dis addresses the weaknesses of other known analytical techniques.

Empirical Literature

Various empirical studies have been conducted to explore the dynamics of exchange rate volatility, its determinants and exchange rate-growth. However, there is no unanimity in the findings of the extant studies regarding how exchange rate affects the output growth. For instance, Ozata (2020) employs an ARDL while exploring impact of exchange rate shocks on Turkey’s growth performance. The result shows a strong inverse effect of exchange rate volatility on Turkey’s growth performance. The striking findings particularly in the long-run dynamics indicated that investment and export have strong positive effects on economic growth, whereas import and exchange rate asymmetries have strong negative impact on growth. Similarly, Ehikioya (2019) scrutinizes the asymmetry effects of exchange rate on growth of the Nigerian economy using GARCH and GMM techniques. The results reveal that volatilities in the exchange rate induce strong negative effects on growth dynamics. A mounting body of empirical studies have further examined the shocks driven from volatility of the exchange rate on growth performance (see for instance, Adeniyi & Olasunkanmi, 2019; Okorontah & Odoemena, 2016). The results of these investigations revealed the existence positive nexus between economic growth and exchange rate volatility in developing economies. Moreover, Adjei (2019) uses an Autoregressive Conditional Heteroscedasticity (ARCH) and GARCH Models in modeling the exchange rate shocks and economic growth nexus in Ghana. The findings confirm that exchange rate shocks exerted a significant hostile effect on growth performance both in the short term and long term horizons. In addition, Umaru et al. (2018) utilized the POLS in examining the impact of volatility of exchange rate on key macroeconomic performance of West African countries and concludes that the real effective exchange rate has a significant negative impact on GDP.

Using Bai and Perron structural breaks, Cavusoglu et al. (2019) discovered a strong negative impact of appreciated exchange regime on economic growth in North Cyprus. They further found that financial shock served as a mediating factor through which exchange rate is stifling output growth. Moreover, Nor et al. (2020) utilized exponential generalized autoregressive conditional heteroskedastic on Somalian data and found that exchange rate volatility is accounted for by the dynamic of macroeconomic factors (such as import, export, and inflation). Moreover, Shingil et al. (2022) examines the balance of payment constrained growth model (BPCG) by moderating the impact of export, capital flows and exchange rate on economic growth. The result shows that capital flows, relative prices and exchange rate have strong impact on shaping the patterns of output.

Plethora of empirical studies have supported the assertion that macroeconomic fundamentals have mediating effect in exchange rate and output growth relation. Olanipekun et al. (2019) employed a rich quarterly data covering 20 countries and found that economic policy uncertainty is intensifying the exchange market pressure. Olanipekun et al. (2019) have explored the causality between exchange market pressure and economic policy uncertainty in BRIC using a bootstrap panel causality. The finding indicates that global economic uncertainty is greatly influencing the exchange market pressure. Using a combination of ARCH, bootstrap bound test, and Granger causality, Iliyasu et al. (2024) explore the effect of monetary policy and exchange rate volatility in Nigeria. Finding reveals that exchange rate volatility is accounted for by the asymmetries in the monetary policy tools, particularly the variability of money supply in Nigeria. Furthermore, the study documented a feedback causality between exchange rate volatility, interest rate, and money supply both in the short and long run.

A mounting body of empirical studies have captured the linear and nonlinear dichotomy in modelling the nexus between exchange rate and economic growth. For instance, Ahmed and Mazlan (2021) adopted the linear and linear models while exploring the impact of interest rate on exchange rate in ASEAN countries. The results of NARDL indicate the short and long run symmetric effect of interest rate on exchange rate for Cambodia, Malaysia, Thailand, Singapore and Vietnam. However, asymmetric effect was documented for Indonesia and Philippines. Bao and Le (2022) examine the asymmetric impact of vehicle currency (VCER) USD’s exchange rates, on trade balance in 10 ASEAN countries. The result of NARDL indicates that VCER exchange rate has a significant effect on trade balance. Moreover, Zakaria et al. (2023) validated the traditional purchasing power parity using monthly data from Pakistan. The result of wavelet coherence technique shows that inflation differential has a strong positive effect on exchange rate. Rate misalignment was further considered as a salient factor in explaining exchange-growth relation. Using non-linear ARDL, Iqbal et al. (2023) examine the nonlinear effects of exchange rate on economic growth in India. The result of the linear model reveal that exchange rate has adverse effect on economic growth. However, the result of non-linear model shows a strong evidence of asymmetric impact. Ren and Sakouba (2024) investigate the exchange rate movement and China-East Africa trade balance. While finding shows that exchange rate movement has a slight effect on trade balance, evidence does not support the J-curve hypothesis in the context of China and East African trade balance. Asymmetric effect may shape the patterns of the J-curve effect. In this sense, Parray et al. (2023) examine the exchange rate changes and the J-curve effect in emerging economies. While the result of asymmetric model reveals no evidence of J-curve effect, However, currency appreciation is found to have strong negative effect on trade balance. In the sense, appreciation is key to trade deterioration by a greater magnitude.

Discerning closely the existing investigations, the nexus between exchange rate and economic growth has been well explored. However, there is no unanimity among the scholars on the impact of exchange rate on economic growth, with some strands of studies pointed the positive effect of exchange rate on growth (Ibrahim & Sanusi, 2022; Iliyasu et al., 2024) whereas other studies found the retarding effect of exchange rate on growth (Adjei, 2019; Ibrahim, 2014; Iqbal et al., 2023). These conflicting evidences are partly explained by the failure in the extant studies to utilize a bootstrap technique that simultaneously control for the effect of exogenous variables and regressand in shaping the pattern of long run equilibrium. Moreover, previous studies related to connection between exchange rate and growth in the case of Nigeria were based on symmetric framework of cointegration without controlling for the breaks in data. The restricted hypothesis of symmetry couple with assumption of no regime shift in the data may prevent unraveling true nature of the relationship between exchange rate and economic growth. In light of these inconsistencies in the extant studies, there is a strong need to re-examine the growth-exchange rate nexus using more robust such as Bootstrap ARDL and Gurus (2019) will help in addressing the debates of whether exchange depreciation is beneficial to growth or not, particularly in the direction of external trade competitiveness which has not been covered by the existing investigations.

Methodology

This study utilizes time series data spanning from 1980 until 2020 which covered the period where major economic reforms were pursued which changed Nigeria’s exchange rate policy from a fixed to a flexible exchange rate regime (Okorontah & Odoemena, 2016). The study’s data for relevant variables were obtained from the Central Bank of Nigeria (CBN) and the world development indicator database. Figure 1 presents the time series graphical plot of the study variables.

Time series properties of the study variables.

The preceding discussion of the theories have hypothesized that elasticities of net-trade have mediating impact in the asymmetries of exchange rate and economic growth nexus. As such, the functional form of the mathematical model of the variable is specified in equation (1) as

where

where γ0 is constant, γ1 to γ5 are the parameters to be estimated with respect to the variables of the study.

Interestingly equation (2) can be extended to provide information about the presence of cointegration in both the short and long run within the framework of ARDL. The unrestricted error correction mechanism with each variable being estimated independently via the least square to establish its coefficient as given in equation (3):

the coefficients from β1 to β6 express the long run symmetry convergence among the coefficients and the variables. Thus, from γ1 to γ6 exhibit the dynamics of the short run associations amongst the considered variables, along with the first difference operator indicated by Δ, γ0 is the constant and ε t is the white noise error term.

As estimation procedures, the study scrutinized Bootstrap test statistics to the ARDL test frameworks. It appears that the Bootstrap-ARDL is preferred over the traditional ARDL cointegration test because of its predicting power and size weakness (Goh et al., 2017; Khan et al., 2018; McNown et al., 2018; Olasehinde-Williams et al., 2021; Pesaran et al., 2001; Yurtkuran, 2021). Thus, a recently advanced Bootstrap ARDL test includes other t-test

Accordingly, the newly developed bootstrap ARDL has Critical Values (CV) that are developed upon on the combination and integration features of every time-series employed in the procedures of ARDL bootstrap, Hence, the procedures would basically succeed in dealing with the volatility problem inherent in ARDL bounds test approach (Ibrahim & Sanusi, 2022). However, bootstrap-ARDL testing approach by McNown et al. (2018) used a robust Critical Value (CV) table derived from bootstrap ARDL simulation. These new CV are efficient, flexible and reliable compared with the traditional ARDL bounds test (Pata, 2019). Specifically, the Pesaran et al. (2001) CV permits the use of one endogenous variable, whereas the CV produced with a bootstrap method permits the dependent variable, endogenous explanatory variable and the sets of exogenous variables. Similarly, this method is also appropriate for data that comprises two or more independent variable (Goh et al., 2017). For instance, it was found that the co-integration between RGDP, EXRT, INFR, IMPO, EXPO, and NR will be established when the values of

As hypothesized by the J-curve, it is plausible that effect of exchange rate on economic growth to exhibit asymmetries driven by the appreciation and depreciation in the value of currency. To test the nonlinearity relation between exchange rate and growth in the context of Nigeria, this study employs the Shin et al. (2014) nonlinear autoregressive distributed lag (NARDL). This technique requires that exogenous variable(s) that are established to possessed asymmetries from non-linear unit root be decomposed be decomposed into negative and positive components based on equation (4):

The negative and positive components of the decomposed asymmetric series are specified into NARDL model as shown in equation (5):

The parameters

Thus, before estimating the model, the series were tested for their characteristics using Augmented Dickey–Fuller (ADF) and Phillips Perron (PP) tests for the linear model. These techniques are efficient in small sample when the data has no element of negative moving average and a regime shift (structural break). With break(s) in the series, the traditional unit root techniques often confuse break in data with unit root (AlGhazali et al., 2023) leading to false inference. As such, Perron and Vogelsang (PV) unit root test that account for break in data is employed in the study. The test is robust in differentiating the break in data and unit root issues. With respect to nonlinear unit, the study applied the novel Gurus (2019) asymmetric stationary test to validate the variable that exhibit the nonlinear effect.

Empirical Results and Discussion

Unit Root Test

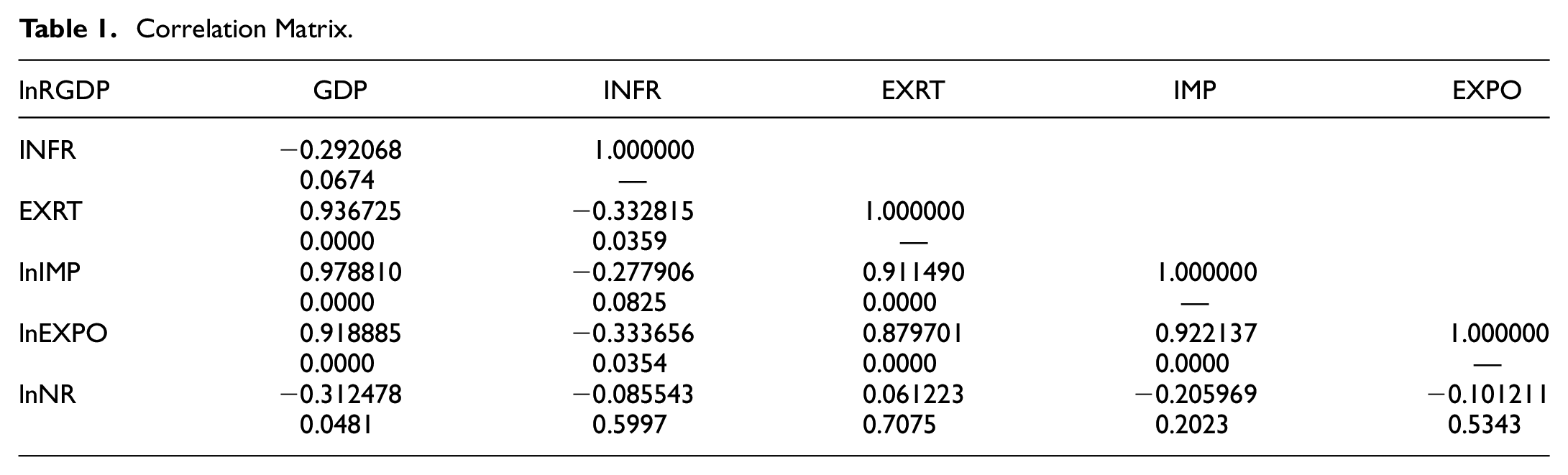

The correlation analysis of the variables was presented in Table 1. The results reveal a significant pairwise correlation between GDP, EXRT, INFR, IMPO, EXPO, and NR. Notwithstanding the strong relationship between the variables, a long span time series may yet contain bogus characteristics in it its covariate along a varied timeframe (Aliyu et al., 2021; Iliyasu et al., 2024; Yurtkuran, 2021). Thus, to avoid the spurious relationship, a unit root test is employed to determine the order of integration of the variables. ADF and PP unit root tests were used for all the series to serve as a guide for the choice of an acceptable model of cointegration. The results of unit roots are presented in Table 2.

Correlation Matrix.

Stationary Tests Results.

Notes.**, ***indicates statistical significance at 5%, and 1% level respectively.

As Table 2 shows, the log of real GDP, exchange rate, imports and exports do not have a constant mean and variance at their levels. However, they become stable when we take their first differences, which means they are I (1) series. In contrast, inflation rate is stable at its level, which means it is I (0).

The validity of ADF and PP unit root test is determined using PV. The results, as highlighted in Table 3, illustrate that null hypotheses are rejected, indicating that all the series are not significantly stationary after controlling for the structural break. This affirmed that the variables are I (1) and since none of the variables appeared I (2), we can estimate the short run, long run and error correction coefficients of the ARDL model. With respect to asymmetric properties of the series, the result of Gurus (2019) shows that only exchange rate and import have I (0) null hypotheses not rejected. These two series possessed asymmetric effects and are decomposed into negative and positive components in the estimation of NARDL.

Outcome of PV and GNUR Tests.

Notes. Gurus (2019) Nonlinear Unit Root, respectively.

, **, ***indicates statistical significance at 10%, 5%, and 1% level respectively.

Moreover, estimation of BARDL is sensitive selection of appropriate lag that minimize error and resolve autocorrelation (Aliyu et al., 2021; Goh et al., 2017; Ibrahim et al. 2024). Accordingly, Table 4 presents the lag order criterion and it suggests four lags for the estimation.

Lag Criteria.

Shows the recommended lag order criteria.

Following Aliyu et al. (2021), Lawal et al. (2022), and McNown et al. (2018) an ARDL (4, 3, 4, 4, 4, 1) model which determines co-movement of variables is selected according to Akaike Information.

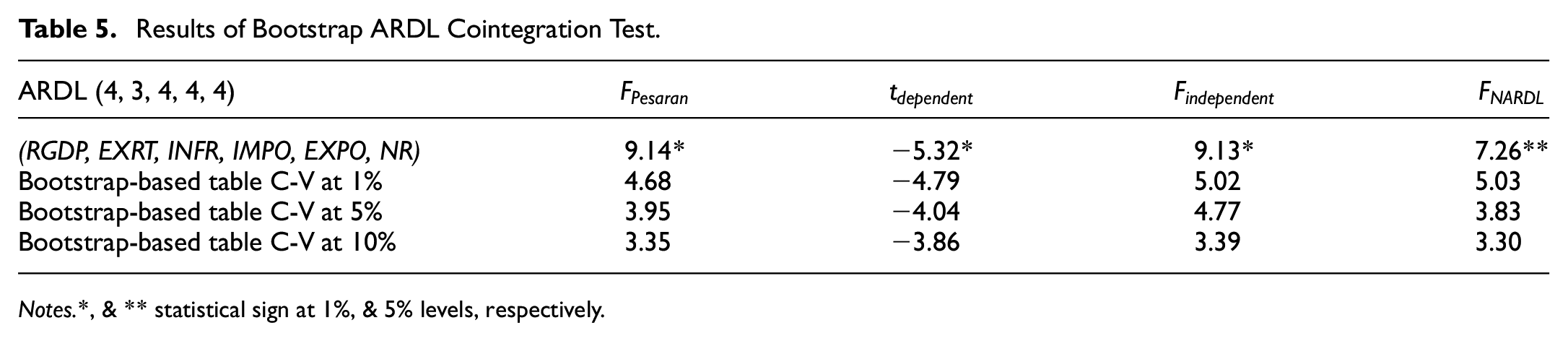

Bootstrap ARDL Testing of Cointegration

The results of BARDL bounds testing of cointegration approach are provided in Table 5. The findings show that the

Results of Bootstrap ARDL Cointegration Test.

Notes.*, & ** statistical sign at 1%, & 5% levels, respectively.

The results as shown in Table 5 indicate that the null hypothesis of no cointegration is rejected on the grounds of having a calculated F-statistic of 9.14 which is greater than the Bootstrap-based table C-V at even 1% (4.68). Turning to nonlinear cointegration, the result of asymmetric model presented in Table 5 shows the evidence of cointegration relation among the variables (F-value 7.26 > 5.03). This supported the findings of Ibrahim and Sanusi (2022) as well as Iliyasu et al. (2024) which reveal a nonlinear co-movement between key macroeconomic variables and economic growth in Nigeria.

ARDL Short Run Estimates and Error Correction Model

The dynamic relationship between exchange rate and economic growth of Nigeria is presented in Table 6. The results show that the outcome of the impact of the EXRT, INFR, lnIMPO, lnEXPO, and lnNR on lnRGDP in Nigeria through the short run horizon and the results are statistically significant at 1%. Thus, the null hypotheses of no short run association for the coefficient of ECT and short run dynamics were rejected because the ARDL result reveals that, the coefficient of error correction term

Short Run and Error Correction Model.

The results further indicated that the speed of adjustment (i.e., the errors) from the short run disequilibrium toward the long run equilibrium horizon can be corrected by 3.1% annually. Moreover, the coefficients of lag 2 and 3 values of exchange rate are statistically significant at 1% level with negative and positive effect on LRGDP, respectively. Thus, there is conformity of results on the effect of exchange rate on economic growth in the short run. Hence, we can establish that in the immediate short run exchange rate has a positive effect on RGDP but through time it will have a negative and statically significant effect on RGDP in short run, particularly when looking at the perspective of external trade competitiveness of the economy (Aliyu et al., 2021). This means that LRGDP fall with the depreciation of exchange rate in the short run all things being equal and this has a strong impact on the external trade competitiveness of Nigeria. This is in line with the findings of these condensed literature (Aliyu et al., 2021; Ehikioya, 2019; Ozata, 2020; Shuaibu et al., 2021).

Similarly, the result also reveals that inflation rate is found to have a statistically negative significant impact on LRGDP in the short-run at a 1% level. This is supported these condensed previous findings (Bahmani-Oskooee et al., 2016; Bahmani-Oskooee & Gelan, 2018; Okafor et al., 2018; Ren & Sakouba, 2024; Zakaria et al., 2023). Moreover, the coefficient values of LIMPO are positive from lag 1 to 3 are also statistically significant. This affirms that Nigeria has an import-dependent production structure for manufactured goods. This suggests that trade restrictive strategies such as tariff and quota, may hamper the growth in the country. Additionally, the coefficients of LEXPO are also statistically significant with only lag 2 which is statistically significant at 5% effect on LRGDP and this is supported previous findings (Fisera, 2024; Shingil et al., 2022; Shuaibu et al., 2021; Umaru et al., 2018). The results show the strong positive effect of natural resources on economic growth. This finding reinforces the tenet of the resources beneficial hypothesis where exchange earnings from resource rent are used to support the performance of local currency (Iliyasu et al., 2024).

ARDL Long Run Estimation Results

The results of estimated long run model are contained in Table 7 and it shows that the estimated coefficient of exchange rate has a significant negative impact on economic growth in Nigeria. Thus, LRGDP rises in the long run sequel to depreciation of exchange rate. In this sense, exchange rate can be used to predict the long run economic growth in Nigeria. This finding supported the findings of Adeniyi and Olasunkanmi (2019), Adjei (2019), Barguellil and Review (2021), and Doojav et al. (2024). Similarly, LINFR and LIMPO were found to have significant impacts on LRGDP in the long run at 1% and 5% level revels, respectively. This is supported by the findings of extant studies (Bahmani-Oskooee & Gelan, 2018; Iliyasu et al., 2024; Ren & Sakouba, 2024).

Result of ARDL Long-Run Estimation.

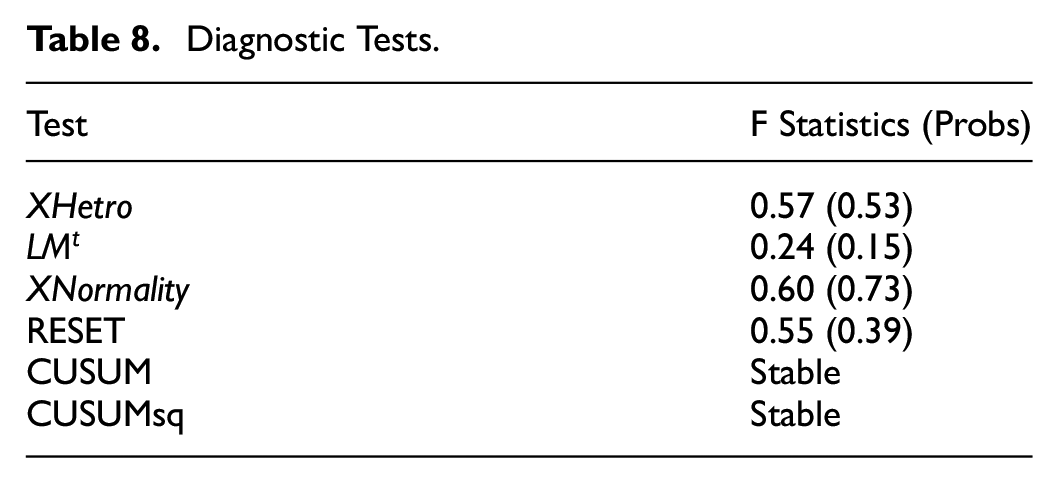

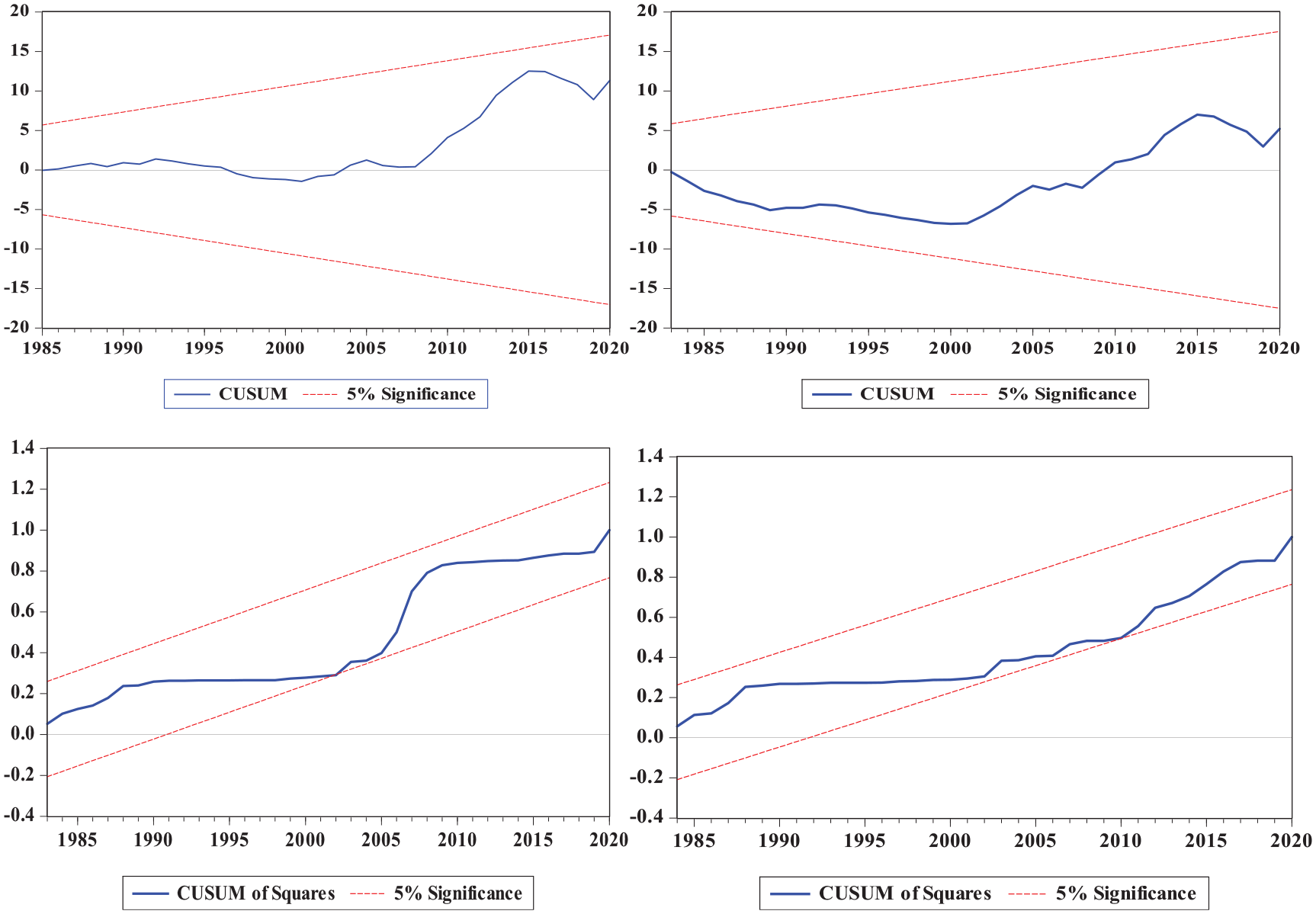

Table 8 shows that the results of heteroscedasticity, serial correlation, and normality as revealed by the P-value of the F-statistics J.B statistics are all greater than 5%, respectively. Consequently, the null hypotheses of no problems of heteroscedasticity, serial correlation, and not normally distributed residual have been rejected. In addition, the model is correctly specified within the acceptable and stable thresholds in the CUSUM and CUSUM of squares test as presented in Figure 2.

Diagnostic Tests.

ARDL CUSUM and CUSUM squares.

Asymmetric Effect of Exchange Rate on Growth

The asymmetric short run results, as depicted in Table 9, reveal that negative exchange rate has a strong positive effect on economic growth in the short run. This is consistent with result of linear model presented in the preceding section. Similarly, the positive exchange rate is enhancing the performance of the Nigeria economy. However, negative exchange rate has a significant negative effect on growth in the long run since decrease in exchange rate will make import cheaper and export expensive.

NARDL Short and Long Run Results.

Notes.**, & *** indicates statistical significance at 5% and 1% level respectively.

The results further demonstrate that positive exchange rate has a significant positive nexus with economic growth in long run. The finding supported the result of Iliyasu et al. (2024) which documented exchange appreciation is stippling the illegal cross-border in Nigeria. This asymmetry in the growth-exchange relation is consistent with the J-curve phenomenon. The heterogeneity is exacerbated by the structure of net-trade that respond more to depreciation shocks than appreciation (Antonio & Luis, 2022; Bosupeng et al., 2024). On the other hand, the negative import has a strong negative effect on growth, indicating that local producers lacked capacity to bridge the import deficit in the short run. However, the result demonstrates a positive effect of negative import in the long run. The negative import pattern of the result is indicating the potentials of local produce to utilize their excess production capacity to augment the import deficit. The positive import has a significant deteriorating effect on output growth in the long run. This result supported the findings documented in plethora of literature which found that increase in import led to increase in demand for foreign currency (Alessandria & Choi, 2021; Fisera, 2024; Truong & Van Vo, 2023).

Moreover, inflation rate can be a growth beneficial as it has shown a significant positive effect on economic growth in the short run. However, the results reveal a significant negative nexus between inflation and growth in Nigeria. On the other hand, natural resources have strong positive effect on growth both in the short and long run. The finding posits that a 1% increase in resource use will promote the performance of the Nigeria by 3.3% and 2.3%, in the short run and long run, respectively. These outcomes are in line with findings of Usman and Ibrahim (2021) and Zakaria et al. (2023) who suggested positive effect growth-exchange nexus in resource abundance countries.

To validate the overall asymmetric of short run and long run models, the results of Wald test as presented in Table 9 indicate that a short run asymmetry Wald test value of 6.233(p < .05). As such the null hypothesis of no asymmetries in the short run rejected. Similarly, the long run asymmetry Wald test statistics is 5.142 (p < .05) which points the rejection of null hypothesis. These outcomes implied the controlling the asymmetric effects of exchange rate and import shocks are key to the sustainable growth of Nigerian economy.

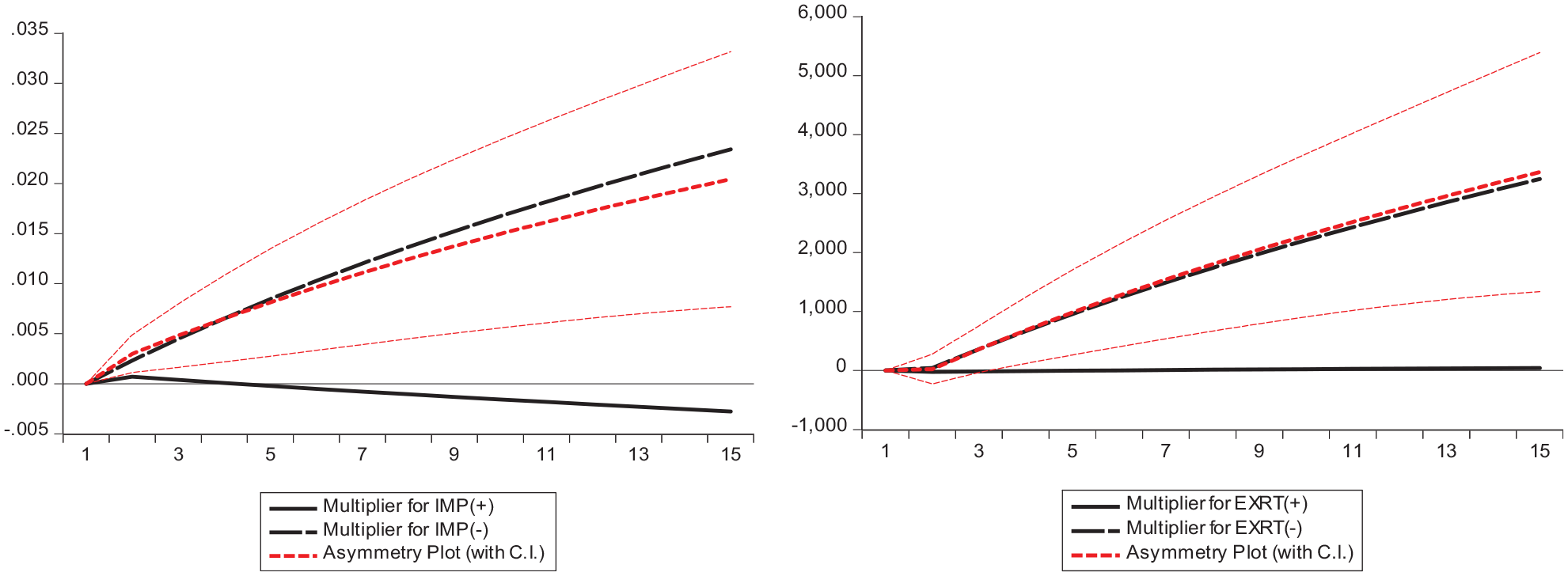

The plots of dynamic multipliers are presented in Figure 3. The asymmetry plots in the two panels displayed patterns similar to negative import and negative exchange rate. The negative import converged with the asymmetry plot and then rose higher after the 5th period. However, the convergence of the negative exchange rate with the asymmetry plot stretches longer up to the 9th period and then recorded a slight divergence thereafter. Whereas the positive asymmetry of import is greater than the positive change rate. These plots suggest that exchange rate depreciation may enhance economic growth if it is accompanied with favorable trade policies.

Dynamic multipliers.

The diagnostic test of NARDL as highlighted in the last segment of Table 9 shows that the estimated model is adequate and passed the fitness test. Similarly, the model is stable as Figure 4 shows that CUSUM and CUSUM of squares test falls within stable bands.

Robustness Checks and Causality Model

As for the robustness checks, the study validates the cointegration results using the Bayer-Hanck (B-H) combined cointegration model. This model used Fisher statistics on Engle-Granger (EG), Johansen (JOH), Boswijk (BO), and Banerjee-Dolado-Mestre (BDM) to analyze the joint cointegration on purely I (1) variables.

The results of B-H model, as highlighted in Table 10, reveal that the computed

The Results of the B-H Test.

Findings of Cointegration Regression Models.

Notes. DOLS and CCR denotes Dynamic ordinary least squares and canonical cointegrating regression, respectively.

,**, *** shows statistical significance at 10%, 5%, and 1% level, respectively.

The outcomes of DOLS and CCR as robustness check for long-run model are presented in Table 11. The findings are consistent with long-run results reported in Table 7 which reveal a significant negative impact of exchange rate and import on economic growth. On the other hand, inflation rate, export and natural resource have strong positive effect on economic growth in Nigeria.

The nonlinear causal nexus among the EXRT, INFR, IMPO, EXPO, NNR, and RGDP was examined via the Diks and Panchenko (DP) asymmetric model. The results as reported in Table 12 show that INFR, EXPO, and NNR have bidirectional causality with RGDP. However, unidirectional causality that runs from EXRT and IMPO on RGDP was equally unraveled. These findings confirm the strong nonlinear nexus among EXRT, INFR, IMPO, EXPO, NNR, and RGDP in Nigeria.

Outcomes of Diks and Panchenko Asymmetric Causality.

Notes.

, **&***demotes significance at 10%, 5%, & 1% level, respectively.

Conclusion

This study investigates the impact of exchange rate on economic growth in Nigeria within the framework of BARDL approach using annual time series data covering from 1980 to 2020. The finding from bootstrap bound test reveals the existence of cointegration among the variables, indicating that exchange rate is a key to the real growth of Nigerian economy in the long-run. The results also show an inverted U-shaped effect of exchange rate on economic growth in short run exchange. This finding indicates that the contemporaneous positive effect of exchange rate on growth metamorphosed into a negative effect within a second lag. While exchange rate depreciation retards economic growth in the short-run, the pattern demonstrates a strong potentials of currency devaluation on external trade competitiveness of Nigeria. However, the import-dependent structure of the Nigerian economy must be addressed through concerted efforts that would boost export diversification. The extant net-export elasticities are insufficient to meet the ML condition in Nigeria which partly explain why the usufruct of devaluation has been minimal.

Given that the null hypothesis of no short run association for the coefficient of error correction term is rejected because the ARDL result reveals that, the coefficient of ECT-1 is statistically significant at 1% level. It can be inferred that about 31% is needed for equilibrium convergence if stability is to be restored in the subsequent period after some shock in the system. This means that LRGDP fall with the depreciation of exchange rate in the short run which has a strong impact on the external trade competitiveness of Nigeria. In the long run, the finding shows that exchange rate has a significant impact on LRGDP. In this way, it can be argued that asymmetries in exchange rate must be taken into consideration while perusing sustainable economic growth drive policies. The stability of exchange rate will help the country to minimize the detrimental effect on welfare and purchasing power of the citizenry. In this regard, inflation targeting shall be closely scrutinized to ensure inflationary pressure does not reach a level that will become detrimental to growth.

Further policies are required to sustain exchange regime that will spur growth. In this sense, it is salient to navigate the effective exchange that will enhance the performance of the economy via a managed floating. As a result, the selection and administration of an effective exchange rate regime is a vital part of economic policy and management decisions to ensure competitiveness, macroeconomic stability, and long-term growth because differing regimes are associated with insecurity and uncertainty. The implication of exchange rate volatility imposes additional difficulties on the economy given its growing financial development. Future studies are expected to take into account of seasonality in the estimation of effective exchange rate and growth relation which cannot be addressed in this study.

Footnotes

Acknowledgements

Data, codes and DO-files used in this article are available from the author upon request.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data and codes are available upon request