Abstract

The aim of this research is to investigate the relationship between family involvement and innovative capability in Chinese family small-medium sized enterprises (SMEs). Although previous studies based on the behavior agency model have investigated how financial factors could influence the relationship between family involvement and innovative capability, there is a dearth of studies with an emphasis on the impact of non-financial factors. Notably, the moderating role played by family firms’ human resource (HR) redundancy in this relationship has not been sufficiently explored in the literature. Our research analyzed secondary data of Chinese family SMEs listed in the China Stock Market and Accounting Research (CSMAR) database. Standard multiple regression and moderated multiple regressions were conducted to test the main and moderating effects, respectively. According to the results of our study, the three dimensions of family involvement (ownership, management, and governance) have a negative influence on Chinese SMEs innovative capability, but this influence can be partially moderated by HR redundancy. Based on the socio-emotional wealth (SEW) perspective, this research contributes to family business literature by addressing previously noted research gaps in related studies.

Keywords

Introduction

According to estimates, family-owned or operated businesses account for between 65% and 80% of companies worldwide (Bent & Seaman, 2017; Ye & Li, 2021). Family small and medium-sized enterprises (SMEs) have played an important role in supporting the economic stability of many countries and regions, especially in the emerging markets (Ahmad & Yaseen, 2018). In China, the success of SMEs is becoming increasingly important for the country’s economy (Yan et al., 2018). However, like the situation in many other countries, the rate of failure among Chinese family SMEs is notably high. According to latest statistics, 68% of Chinese family SMEs fail within their first 5 years of operations, and only 13% of these firms have a lifespan that exceeds 10 years (Huang et al., 2020). With intensifying competition in the global markets, innovative capability has received much attention as one of the core factors that could assist family firms in maintaining their competitiveness against rival firms (Fuetsch & Suess-Reyes, 2017). Empirical studies show that a firm’s high level of innovative capability (such as higher R&D intensity) could positively influence its performance as well as its sustainable competitive advantage (Purwati et al., 2021; Yousefi et al., 2022). Thus, it is crucial for family SMEs to place an emphasis on their innovative capability within the competitive business landscape.

To improve innovative capability, the introduction of discontinuous/innovative technology in family firms may require the retrenchment of a proportion of redundant family employees who are no longer qualified professionals in their positions (König et al., 2013). In this situation, the firms may face a dilemma in their HR strategy, having to decide whether to retrench the corresponding section of employees to save costs or to retain them as part of their strategy in promoting socio-emotional wealth (SEW; Gomez-Mejia et al., 2007). To address this dilemma, this study aims to explore the potential value of family firms’ HR redundancy in affecting their innovative capability.

The impact of family involvement on innovative capability has received much interest in prior research studies (Alayo et al., 2021; Jocic et al., 2021; Matzler et al., 2015). However, a notable limitation in these studies is that they tend to focus on the main effects of family involvement on research and development (R&D) investment and/or R&D output, such as investigating the impact of family ownership on firms’ innovative capability (Chen et al., 2013; Chirico et al., 2022). The moderating variables, especially those internal organizational factors that could affect the relationship between family involvement and innovative capability have not received sufficient research attention. This potentially limits scholars and practitioners’ ability to better understand the relationship between family involvement and innovative capability.

Although previous studies based on the Behavioral Agency Model (BAM; Chrisman & Patel, 2012; Kotlar et al., 2014) have investigated a number of situational factors that can be used as moderating variables, such as the performance dilemma of firms (Chrisman & Patel, 2012) and external suppliers’ bargaining power (Kotlar et al., 2014), these moderating variables are generally not closely aligned with family firms’ unique attributes (e.g., their distinct HR policy for preserving family emotional attachment). Thus, these moderators that are commonly explored in non-family business studies may not be appropriate in addressing the current research context, which seeks to better understand the relationship between family involvement and innovative strategy in family businesses.

Furthermore, previous family business studies tended to consider only a firm’s economic pursuit as the decision-making referencing point, and these studies did not sufficiently explore family firms’ non-economic pursuits. For instance, Chrisman and Patel’s (2012) study noted that family firms would tend to conduct more R&D investment when they face a dilemma related to financial performance, and this may imply that financial performance dilemma could potentially moderate the negative relationship between family involvement and R&D investment. Although valid, this argument does not sufficiently consider the duality of goal objectives in family firms. For example, from the SEW perspective, the focal point of family-firm decision-making is in preserving their non-financial/socioemotional wealth rather than financial wealth (Gomez-Mejia et al., 2007). To address this research gap, our study aims to explore how family firms’ unique non-economic/socioemotional pursuits can potentially affect the relationship between family involvement and innovative strategies. The level of HR redundancy is considered as a focal point for emotional attachment (one of the SEW dimensions) between family business employees and their firms. The moderating influence of HR redundancy in a family business is analyzed to better understand its potential role in affecting the relationship between family involvement and innovative capability. The objectives of this article are as follows: (a) to capture and summarize the studies regarding the relationship between family involvement and innovative capability; (b) to predict/analyze the moderating role of HR redundancy based on SEW perspective; (c) to present the findings after regression analysis; and (d) to provide a discussion on the results and to conclude with considerations on potential limitations and future research directions.

Theory Development and Hypotheses

Family Involvement and Innovative Capability

As the cornerstone of corporate governance, agency theory focuses on the problems caused by the divergent interests between agents and principals. Agency theory has played a leading role in many previous studies that have attempted to explore and explain the effect of family involvement on family firms’ innovative capability (Ashwin et al., 2015; Matzler et al., 2015; Rondi et al., 2021; Tan et al., 2021). These studies highlight two types of agency relationships that are unique to family businesses: the relationship among family members (Memili et al., 2015) and the relationship between family and non-family members (Madison et al., 2018). Researchers have argued that the agency relationship among internal family members will result in excessive company-paid private consumption (Fan et al., 2021), which may reduce the cash flow that should have been applied to more important technological projects.

In terms of the agency relationship between family employees and non-family employees, nepotism is a unique feature of family businesses that can lead to non-family employees’ perceptions of injustice and unfair treatment (Waterwall & Alipour, 2021). Nepotism within family firms could also limit their human resource quality and talent pool (Hayajenh et al., 1994) as the hiring and promotion of less-educated family members could cause resentment among more qualified non-family employees who have better skills and talents (Sciascia & Mazzola, 2008). This resentment may impact negatively on non-family employees, reducing their enthusiasm and motivation to assist family firms in pursuing longer-term innovative strategies.

From the SEW perspective, this paper notes that family enterprises tend to carry out less innovative activities in comparison with non-family-oriented firms. The SEW perspective emphasizes the non-financial pursuits of a firm, such as family identity, emotional attachment, family control, family social networks, and perpetuation of the family dynasty (Berrone et al., 2012; Gomez-Mejia et al., 2007). Family members tend to regard potentially risky decisions as threats to family control and inheritance, thus reflecting a conservative attitude in the decision-making process (Ceipek et al., 2021), which may lead to family businesses’ aversion to pursue activities that may improve their innovative strategies and investments in the long term.

Emotional Attachment and HR Redundancy

This study supports the view that family firms’ human resources considerations cannot be neglected when it comes to their innovative strategies. In line with the SEW perspective, the stronger the employees’ emotional attachment, the more painful it would be for family firms’ decision-makers to accept discontinuous technologies since doing so would require the firm to reconfigure their human resources and divest older assets (König et al., 2013). The success of innovative strategies can make family businesses achieve better financial performance (Lee, 2021). However, it is often unrealistic for some older family employees to be qualified for newer positions since they may have difficulty adapting newer technological trends and developments (Vandekerkhof et al., 2015). In this situation, family firms’ innovative activities could put some of these employees at risk of being retrenched, thus disrupting the emotional attachment/ties within the family firm. König et al.’s (2013) study noted that a part of family firms’ employees who are less-qualified in their positions are often retained in a company in order to preserve the firm’s unique socio-emotional pursuit (emotional attachment dimension). This study aims to provide an empirical analysis to evaluate the role that those redundant employees may play in influencing family firms’ innovative capability.

Adapting and Reframing Existing Research

Chrisman and Patel’s (2012) research applied the BAM to investigate family firms’ R&D intensity, and the results suggest that a family firm may increase its R&D investments when it is impacted by a lower financial performance. This implies that financial factors like financial performance dilemma could be a trigger in stimulating family firms’ R&D intensity. This finding is consistent with the standard BAM which suggests that an enterprise’s decision-makers would tend to adjust their firms’ risk-taking strategies due to their egocentric and economic concerns (Wiseman & Gomez-Mejia, 1998). However, it should be emphasized that the preceding assumption may not apply completely in the context of family businesses because family firms’ non-economic/social-emotional pursuits have been overlooked in the model.

In contrast with decision-makers’ egocentric motivations in non-family businesses, some studies have noted that the altruism motivation of a family firm’s decision-maker could also affect the firm’s behaviors (Bendell, 2022). How those altruistic behaviors (e.g., job security for family firm employees) could affect family firms’ risk-taking preferences (e.g., employing innovative strategies) deserves further exploration, and it is an issue that will be investigated in this study. Due to altruism, it is often difficult for family decision-makers to deal with employment-related issues such as the promotion and retrenchment of their internal members (Reid et al., 2002). Because of this, some older employees who are not competent enough are still appointed and retained in key positions in family firms even though there might be external employees available who are better qualified and more efficient for these positions (Gibb Dyer, 2006).

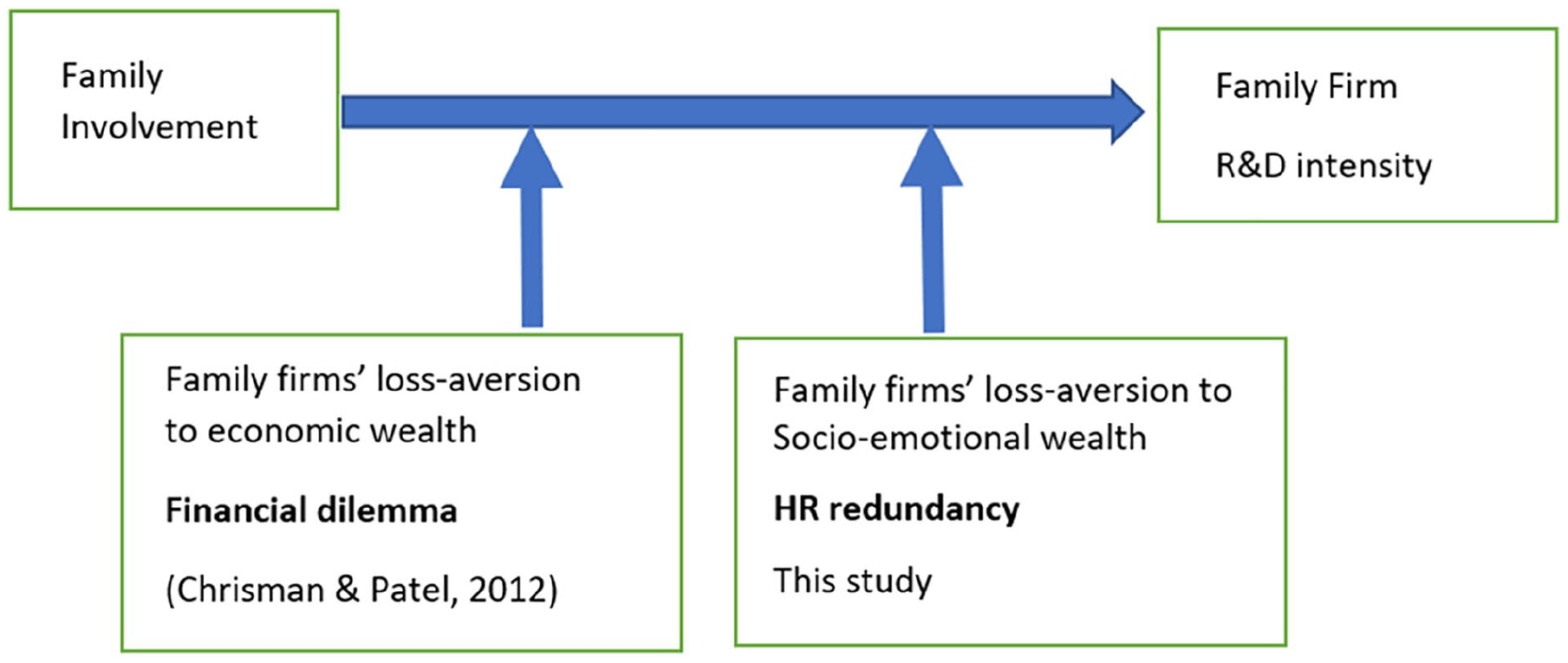

The high level of HR redundancy noted in this study represents family firms’ loss-aversion to their socio-emotional wealth (rather than loss-aversion to financial wealth as noted in other studies). Although Chrisman and Patel’s (2012) study has applied the BAM in a family businesses context, it was still focused on using an economic indicator (performance dilemma) as the reference point while investigating a family firm’s R&D intensity, which potentially overlooks the fact that preserving socio-emotional wealth could be a family firm’s reference point in the decision-making process (Gomez-Mejia et al., 2007). This study proposes that the level of HR redundancy in family businesses could be more suitably investigated as a moderating variable that is unique to the circumstances of family businesses. As such, this study will adapt and reframe Chrisman and Patel (2012) model as shown below in Figure 1. The duality of family firms’ reference points (both socio-emotional and financial pursuit) is considered in this model so that a family firm’s innovative capability could be investigated from both a financial and a non-financial perspective.

Adapting the research model of Chrisman and Patel’s (2012) study.

Although it is generally understood that HR redundancy in a firm may waste a firm’s resources and funding that could have been invested in potentially more rewarding R&D projects, this study argues that it is still worthwhile for a family-owned business to retain redundant employees as part of preserving its socio-emotional wealth. According to Jones (1980), retaining/absorbing redundant employees is a good strategy for a firm not only in fulfilling its social responsibility but also in fostering a positive reputation within the local community. This may potentially assist the firm in gaining extra resources from the external society to conduct more innovative projects. Although some family firm employees may not have the necessary skills or knowledges to directly assist their enterprises in achieving beneficial strategies and outcomes, they could still provide a set of external social capitals to family firms, such as in the building of solid networks with suppliers, clients, and the local government (Niehm et al., 2008). Based on the social capital theory, Leenders and Dolfsma’s (2016) study noted that these stable social capitals/networks could assist firms in gaining easier access to financing that are required for their innovative strategies. Based on this understanding, it can be proposed that HR redundancy in family firms could be potentially positive in enhancing its innovation.

Hypotheses Development

In the following section, we hypothesize a series of relationships between family involvement and innovative capability and how these relationships could be influenced by HR redundancy in family businesses.

Family ownership and innovative capability

Most family owners are often reluctant to transfer their equity in exchange for financial support from external investors (Ahmad et al., 2020; Gomez-Mejia et al., 2010; Tan et al., 2021). The reasons can be attributed to the possibility that: (a) external financing will potentially reduce a family’s control over the family firm, (b) the selling of family owners’ holdings may hurt their firms’ reputation as trustworthy business partners, and (c) the selling would also reduce the shares that their offspring could inherit in the future (Ahmad et al., 2020; Casson, 1999). Therefore, the behavior of selling off family owners’ holdings in exchange for external funding could potentially hurt family firms’ SEW because the family’s control, reputation, and inheritance are very significant dimensions of their SEW (Berrone et al., 2012). In other words, family owners’ reluctance to sell off shareholdings in exchange for financial support can significantly block the development of technological innovation activities. Based on the above discussion, the first hypothesis of this research is proposed:

Family management and innovative capability

Family management involvement could potentially exacerbate the nepotism phenomenon within family enterprises (Yeon et al., 2021). To preserve family SEW, family enterprises may hire more family members as senior managers, which could, in turn, lead to a limitation in sourcing the required managerial capabilities and characteristics (Liang et al., 2014). Chrisman et al. (2014) found that non-economical and family-centered goals often result in the implementation of HR policies that would severely restrict a family enterprise’s management talent pool. Innovative/R&D activities often have a higher requirement for R&D managers who can exhibit professional knowledge and comprehensive expertise (Hagel & Singer, 1999). A policy of limiting top management positions solely to family members is harmful to a family business since it could likely increase the firm’s risk of hiring low-quality managers (Schepers et al., 2014), and this could eventually have a negative influence on a firm’s innovative capability. Based on the above discussion, the second hypothesis of this study is proposed:

Family governance and innovative capability

The misuse of firm resources is more likely to occur if internal family members dominate the board (Matzler et al., 2015), which may negatively influence the implementation of R&D projects. Thus, having independent directors would play an important role in combating family opportunism and in preserving the benefits of all shareholders rather than focusing on the protection of only the major family shareholders’ rights (Anderson & Reeb, 2004). If family members have enough power to pursue their own interests, they are more likely to emphasize SEW (like family identification and reputation) when considering business strategies (Deephouse & Jaskiewicz, 2013), and, thus, may neglect important needs that may be more in line with the business economic/financial interests of its shareholders. Miller et al. (2011) found that having family members in any position on the company board could influence the corporate decision-making process, making it beneficial for achieving family-oriented goals rather than economic goals for a business. In order to preserve a family’s SEW, extra company-paid private consumption could occur when more family members are involved as participants on the board of directors (Deephouse & Jaskiewicz, 2013). This means that family enterprises may sometimes sacrifice their economic performance in order to avoid the loss of family SEW, and this may lead to insufficient investment in important R&D projects. Based on the above discussion, the third hypothesis is proposed:

Moderating role of HR redundancy

This study aims to investigate an alternative perspective that has not been sufficiently addressed in previous research. Most prior studies hold the view that labor redundancy would bring about negative effects on a firm (Marek et al., 2020; Xie et al., 2019), For instance, Marek et al. (2020) proposed that minimizing labor redundancy could help foster greater efficiency within a firm, and a firm’s employment policies should be aimed at reducing redundant staff. Rather than adhering strictly to this viewpoint, this study considers the argument highlighted in some family business studies that a family firm’s labor redundancy phenomenon need not always be viewed negatively; within the family business context, due to the influence of an internal network, nepotism, and the effort to maintain emotional ties, some redundant employees are retained in the corporation despite not having the required skills and knowledge (Madison et al., 2021).

As the creation of employment opportunities for society is one key objective of a country’s government (Liao et al., 2009), a family firm’s policy of keeping a high level of HR redundancy could be seen as a form of assistance to the local government and communities. Prior studies have found that a firm’s reputation may be positively enhanced if it is seen to be assisting local communities, especially in relieving employment-related problems (Jones, 1980). A positive corporate reputation could further improve customers’ and investors’ evaluations of a firm (Srivastava et al., 1997), and, thus, family enterprises with a good reputation could potentially receive more opportunities in relation to external investments for pursuing innovative strategies. This may alleviate most family firms’ ongoing financial dilemma of having to restrict R&D activities due to their reluctance to fund such activities through the selling of equity.

This study notes that family shareholders’ aversion to the loss of SEW could be relieved through their firm’s HR policies. The introduction of external capital could harm a family’s control over a family business to some extent, and this control is one of the key dimensions of family SEW (Hauck et al., 2016). An adjustment to HR policy to improve a firm’s reputation could potentially make up for the loss of SEW caused by the introduction of external capital (Leitterstorf & Rau, 2014). By doing this, family firms’ unique HR policy could weaken shareholders’ aversion to the use of external capital to conduct innovative activities.

In terms of management and governance in family businesses, some managers and directors could be selected based on their status and identification and they may not have the required professional skills/knowledge unlike externally recruited talents (Gallo & Sveen, 1991). It is especially difficult for some older managers and directors to embrace discontinuous technology as they may either feel threatened by the change or may resist the change due to their strong emotional attachment to existing tangible and intangible resources within the enterprise (König et al., 2013). In order to preserve their current status and authority, these managers and directors are often reluctant to allocate resources to conduct innovative activities that may introduce discontinuous technology (Matzler et al., 2015). In such a situation, if the family firm owners have a strong motivation or commitment to retain redundant employees in the firm (including redundant managers and board directors), the potential aversion to the innovative strategies/investments could be relieved. Although such a HR policy may mean that some potentially talented external employees would be turned away, the potential agency conflicts and costs between internal and external employees could be accordingly reduced since majority of the employees come from the same family network (Dawson, 2011). These saved agency costs may alleviate the shortage of family enterprises’ innovation investment to some extent. Based on above discussion, the following hypotheses regarding the moderating effects of HR redundancy on the relationship between family involvement (including ownership, management, and control) and innovative capability are proposed:

Data Collection and Methodology

Data Source and Sample

This study analyzed data from Chinese family SMEs listed in the Chinese Stock Market & Accounting Research (CSMAR) database. This database consolidates a comprehensive collection of statistics on Chinese listed companies and has been widely used in past research studies that have focused on Chinese businesses (Krause et al., 2019; Li et al., 2019). In China, listed family SMEs are concentrated in the Chinese SME board, and these firms are required to disclose detailed and comprehensive information regarding the actual family control as well as to declare all associated family members in their firms’ prospectus (Zhou et al., 2015).

For this study, companies listed in the 2011 to 2019 SME board were sampled. The study population of this research included 1,129 listed firms in the Chinese SME board. The sampling process followed these procedures: (a) selection of enterprises whose actual controllers are families (Campopiano et al., 2014); (b) exclusion of firms where the controlling shareholder holds less than 5% equity (Peng & Jiang, 2010); (c) screening of listed family firms across divergent industries according to the established classification of SMEs in China (e.g., in the manufacturing industry, the number of employees in each chosen company should be between 20 and 1,000; Prange & Zhao, 2018); and (d) since R&D investment and patent counts are not mandatory data for public disclosure, those companies with insufficient data required for this study were omitted during the sampling process (Kong, 2019). Following these procedures, we obtained a sample size of 504 firm-year observations.

Measurement Variables

Independent variables

Consistent with prior research (Matzler et al., 2015), this study utilizes the following three dimensions of family involvement as the independent variables: family involvement in ownership, family involvement in management, and family involvement in governance. First, family involvement in ownership is measured by the equity ratio owned by the family, which should be higher than 5% (Chen et al., 2008). Second, family management is calculated by dividing the number of family members in the top management team, with the total number of management positions in the company. Finally, family governance refers to the ratio of the number of family members sitting on the company’s board of directors against the total number of board members. For this study, the required data on family involvement was manually collected and consolidated through the prospectus of the sampled companies. The prospectuses are open to the public and can be accessed through the China Securities Regulatory Commission website (http://www.csrc.gov.cn). In China, this is the only government agency responsible for regulating securities instruments and overseeing market regulations in the country (Rousseau & Xiao, 2007; Tondkar et al., 2003).

Dependent variables

In this paper, the innovative input of family SMEs is measured through R&D intensity, which is the ratio of a company’s R&D expenditure to total sales. This is a widely accepted method in prior research for measuring corporation innovation input (Barker & Mueller, 2002; Chen & Hsu, 2009). R&D spending can be an appropriate indicator of measuring innovation input since the firm’s R&D expenditure enables it to accumulate strong technological/market capabilities for developing its innovative capability (Matzler et al., 2015). In contrast with the absolute value of R&D expenditure, R&D expenditure as a percentage of total sales is a more appropriate measure as it permits relative comparison between different companies (Chen & Hsu, 2009) and could better reflect a company’s commitment to innovative activities (Hoskisson & Hitt, 1988).

As R&D intensity does not sufficiently reflect the quality of a firm’s innovation, this study relies on another measure for innovation output through the utilizing of patent data, which is a similar approach adopted in prior studies on innovation output (Leten et al., 2007; Matzler et al., 2015). Past researchers have proposed that the application year is a better proxy for the actual time of innovation (Tan et al., 2020). This study focuses on the number of patent applications filed by each sample enterprise within each year. Unlike using R&D intensity as a dependent variable, patent data represents another approach in which a company’s radical, innovative capability can be measured since it could better reflect how effectively a company has utilized its R&D expenditure (Gao et al., 2016).

Moderating variables

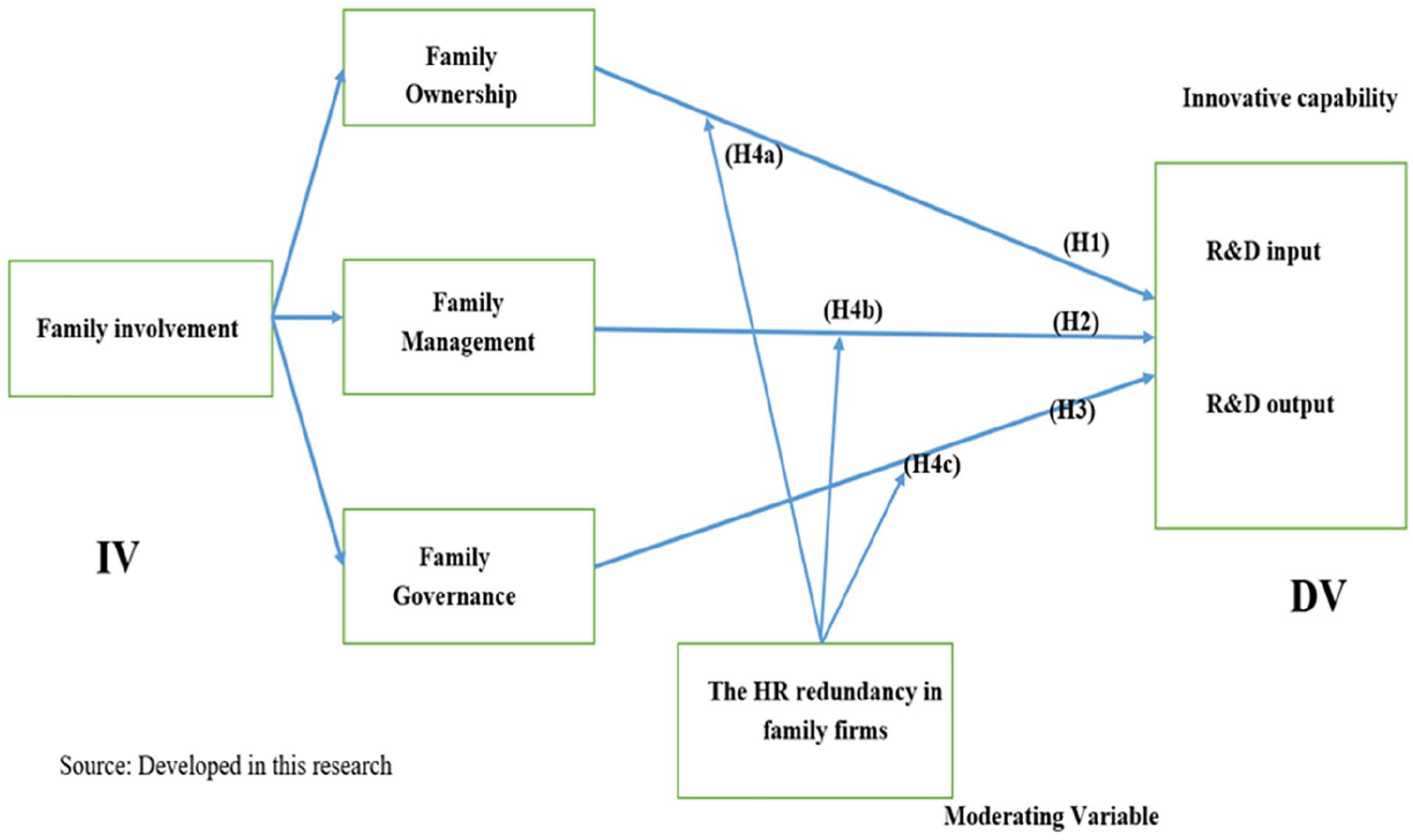

In this paper, we take into consideration that the level of HR redundancy in family businesses is an important indicator for measuring family firms’ motivation to preserve their SEW (emotional attachment dimension). As mentioned in the theoretical model (see Figure 2) of this paper, the HR redundancy level is the moderating variable of this research study.

Theoretical model of this study.

Our study adopts Zhang et al. (2013) method of measuring a firm’s HR redundancy level. The process is as follow: equation (1) is applied to derive the coefficients (α, β, γ, θ) needed to measure sample firms’ expected employment size (full-time equivalent) based on firms’ total assets, growth rate, and fixed assets. In mainland China, a firm’s total assets, revenue growth rate, and fixed assets are the three most important factors which could influence the firm’s employment size (Zeng & Chen, 2006).

Specifically, the dependent variable “Y” in equation (1) is a firm’s actual number of employees divided by the total assets and then multiplied by the scaling factor 1,000,000, used to represent the actual employment size of a sample firm (Zhang et al., 2013). The first independent variable, “size,” is the natural logarithm of the total assets of the enterprises (Zhang et al., 2013). The log transformation could effectively reduce the effect of outliers (Van Caneghem & Van Campenhout, 2012). The second independent variable, “growth,” is the sample firms’ revenue growth rate (Zeng & Chen, 2006; Zhang et al., 2013), used to measure firm growth. The third independent variable, “capital,” represents a sample firm’s fixed assets, measured by the ratio of the firm’s fixed assets to total assets (Avery, 1956; Cheng & Lin, 2009). The redundancy level of human resources is not suitable for horizontal comparison between different industries in mainland China (such as between labor-intensive and capital-intensive enterprises). Thus, following Zhang et al.’s (2013) study, the sub-industry regression was carried out for all the sample firms through equation (1) to derive the sub-industry coefficient (α1, β1, γ1, θ1) used to measure the expected employment size Y1 (the employment size purely based on a sample firm’s total assets, fixed assets, and revenue growth rate). Specifically, the expected employment size Y1 of each sample firm can be calculated through the below equation (2):

Through the above steps, this study obtained both actual employment size, Y, and the expected employment size, Y1, of the sample firms, and then used equation (3) to obtain the HR redundancy index of each sample firm:

The factors mentioned above, including the sample firms’ actual number of employees, total assets, fixed assets, and revenue growth rate, could all be collected through the CSMAR database.

Control variables

In our study, we controlled the following variables that could influence the association between family involvement and innovative capability. We controlled firm size, computing the natural logarithm of the total assets of the sample companies because larger firms tend to conduct more R&D productivity relative to smaller firms (Revilla & Fernández, 2012). We controlled firm age, measured as the difference between the date of the recorded statistics in the database and the year when the enterprise was established because it has been shown to influence firms’ R&D innovation (Sørensen & Stuart, 2000). We controlled financial leverage, measured as the asset–liability ratio, because corporate debt may impact firms’ long-term investment (Singh & Faircloth, 2005). We controlled cash flow, measured as the difference between the amount of cash income and the amount of expenditure, because there is a significant relationship between firms’ cash flow and R&D expenditure (Bloch, 2005). In addition to the abovementioned control variables, our analysis also controlled the industry and year using dummy variables.

Analysis strategy

Standard multiple regression analysis is a technique frequently used by researchers to investigate the relationship between a set of dependent and independent variables (Jeon, 2015). As the technique is consistent with our requirement, we explored the main effects of the three dimensions of family involvement using standard multiple regression analysis. Besides detecting main effects, moderated multiple regression has been noted in prior research as an appropriate technique for identifying the effects of moderating variables (Anderson, 1986). Thus, the moderating effects of HR redundancy in this context could be unambiguously identified through the conducting of moderated regression analysis. The details of the data analysis are presented in the next section.

Results

Summary of Variables

Descriptive statistics and correlations of variables are provided in Tables 1 and 2. Table 1 gives a basic statistical summary of all variables, including mean value, minimum, and maximum value. The average share of equity held by families is 36%. The average ratio of family members on the board to all board members is 41%, and among managers, the average ratio of family managers to all managers is 37%.

Descriptive Statistics.

Correlation Coefficients Between Variables.

p < .05. **p < .01.

In Table 2, it can be observed that almost all correlations are less than .5, which indicates that multicollinearity is not a serious concern for this analysis (Aspelund et al., 2005). The results in Table 2 reveal that all three dimensions of family involvement (ownership, management, and governance) are significantly associated with both innovative investments and patent counts. Specifically, family ownership, management, and governance will negatively affect family firms’ innovative expenditure (r = −.46, p < .01, r = −.49, p < .01, and r = −.20, p < .01, respectively). In addition, these three dimensions of family involvement also have a negative influence on firms’ patent counts (r = −.39, p < .01, r = −.46, p < .01, and r = −.22, p < .01, respectively). This indicates that a higher degree of family participation in ownership, management, and governance will result in weakening a family firm’s innovative capability.

Regression Results

Regression results for family ownership and innovative capability

The results of the relationship between family ownership and innovative investment are presented in Table 3. The results show that the independent variable (family ownership) has a significant negative influence on firms’ innovative investments (β = −.44, p < .001). This is indicative that a higher level of family ownership could adversely affect family firms’ innovative investments. As for the effect of family ownership on innovative output, the results in Table 3 show that the independent variable (family ownership) has a significant negative effect on family firms’ patent counts, which is seen in the standardized coefficient (β = −.371, p < .001). It indicates that a higher level of family involvement in ownership is negatively related to family firms’ innovative output. Based on the above results, the proposal in H1 is supported.

Hierarchical Regression Analysis for the Effects of Family Ownership on Innovative Capability (H1).

p < .10. *p < .05. **p < .01. ***p < .001.

Regression results for family management and innovative capability

In terms of the effect of family management on innovative investment, Table 4 shows that the entering of the independent variable (family management) negatively impacted family firms’ innovative investments significantly (β = −.23, p < .001). This result indicates that a higher level of family involvement in the management team will lead to a lower level of firms’ innovative input. Similarly, by applying patent counts as the dependent variable, “family involvement in management” is shown to have a significant negative effect on family firms’ patents count (β = −.45, p < .001), which can be seen from the standardized coefficient value. The above results show that the deeper the level of family involvement in a management team, the fewer R&D outputs a family firm will likely have. Based on these results in the data analysis, the proposal in H2 of this study is fully supported.

Hierarchical Regression Analysis for the Effects of Family Management Involvement on Innovative Capability (H2).

p < .10. *p < .05. **p < .01. ***p < .001.

Regression results for family governance and innovative capability

It can be seen from Table 5 that family governance has a significant negative effect on family firms’ innovative investments (β = −.09, p < .001). In other words, higher levels of family involvement in the family firm’s board will lead to lower levels of family firms’ innovative expenditure. Furthermore, the results shown in Table 5 indicate that “family involvement in governance” has a significant negative influence on family firms’ patent counts, which can be seen from the standardized coefficient value (β = −.18, p < .001). The results verify that a higher level of family governance involvement in family corporations will lead to fewer innovative outputs. Based on the above results, H3 of this study is fully supported.

Hierarchical Regression Analysis for the Effects of Family Governance on Innovative Capability (H3).

p < .10. *p < .05. **p < .01. ***p < .001.

Moderating effect of HR redundancy on the relationship between family involvement and innovative capability

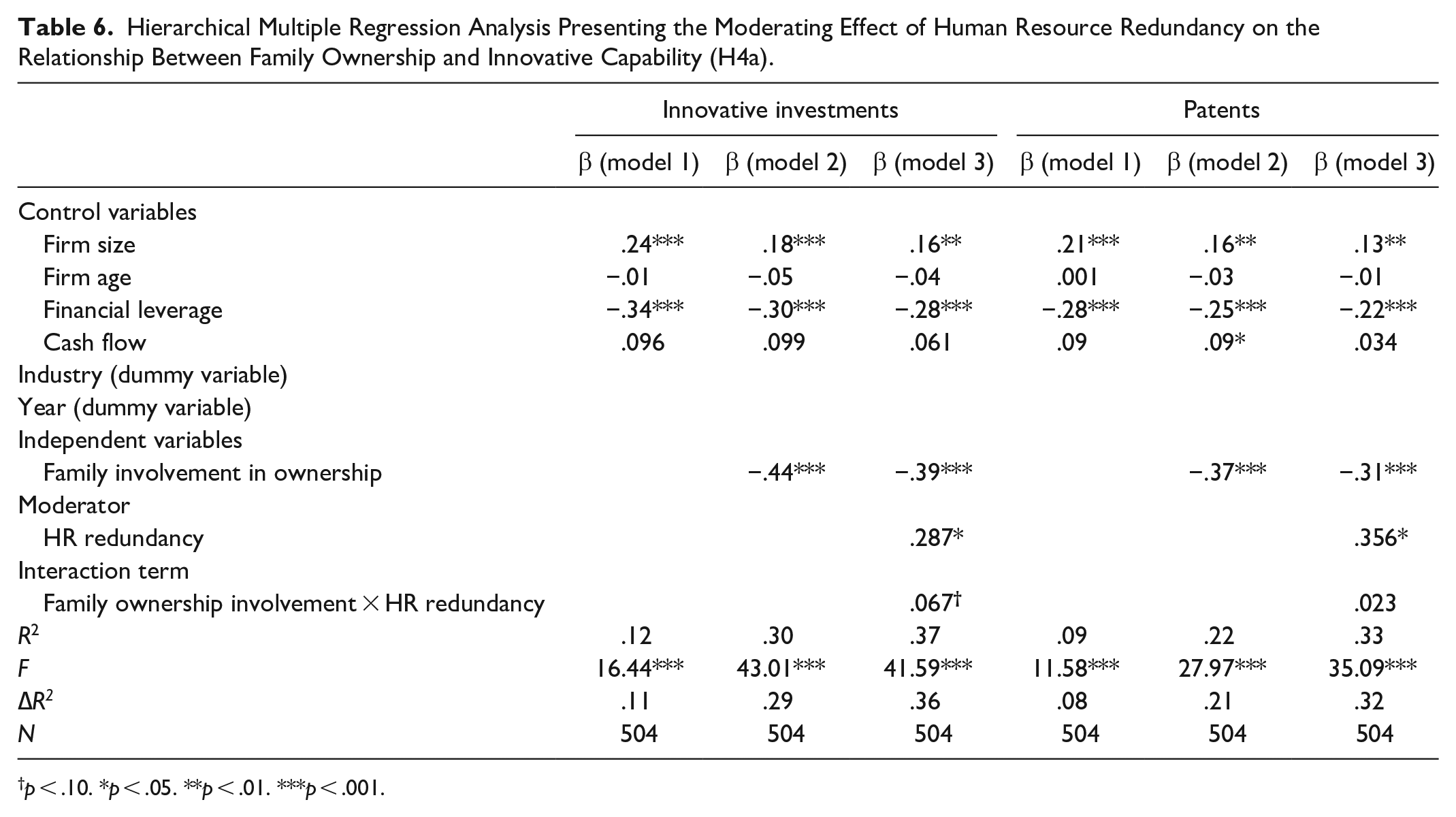

As shown from the regression results in Table 6, the interactive effects of “Family Ownership x HR Redundancy” have a significant and positive influence on family firms’ innovative investments (β = .003, p < .1) but not on firms’ patent counts (β = .023, ns). This result revealed that the negative relationship between family ownership involvement and firms’ innovative input will be weakened when the level of family firms’ HR redundancy is higher. However, the analysis also shows that the moderating variable “HR redundancy” did not have a significant effect on the relationship between family ownership and firms’ innovative output. Based on the results of this analysis, the proposal in H4a is partially supported.

Hierarchical Multiple Regression Analysis Presenting the Moderating Effect of Human Resource Redundancy on the Relationship Between Family Ownership and Innovative Capability (H4a).

p < .10. *p < .05. **p < .01. ***p < .001.

The analysis results in Table 7 show that the interaction term “Family Involvement in Management x HR Redundancy” did not have a significant influence on family SMEs’ innovative investments (β = .002, ns) or on patent counts (β = .09, ns). This result verifies that the moderating variable (HR redundancy in family SMEs) will not significantly affect the relationship between “family involvement in management” and “innovative capability.” Thus, the proposal in H4b of this study is not supported.

Hierarchical Multiple Regression Analysis Presenting the Moderating Effect of Human Resource Redundancy on the Relationship Between Family Management and Innovative Capability (H4b).

p < .10. *p < .05. **p < .01. ***p < .001.

Finally, the regression outcomes shown in Table 8 indicate that the interaction term “Family Involvement in Governance x HR Redundancy” had a significant influence on family SMEs’ innovative capability, including firms’ innovative investments (β = .004, p < .05) as well as firms’ patent counts (β = .10, p < .05), which indicates that the negative relationship between family governance involvement and a firm’s innovative capability will be significantly weakened when the level of family SMEs’ HR redundancy is relatively higher. Thus, the proposal in H4c is fully supported.

Hierarchical Multiple Regression Analysis Presenting the Moderating Effect of Human Resource Redundancy on the Relationship Between Family Governance and Innovative Capability (H4c).

p < .10. *p < .05. **p < .01. ***p < .001.

Discussion

The findings of this study confirm the proposed hypotheses that family involvement (ownership, management, and governance) has a negative influence on family firms’ innovative capability. From the perspective of family ownership, the data analysis results can be linked to prior scholars’ findings based on agency theory. For instance, Ahmad et al. (2020) noted that family-specific agency costs could have a negative impact on R&D investments since family owners always tend to inhibit innovative activities/investments for the purpose of preserving the existing business’s cash flow.

From the perspective of family management and governance, the results of this study confirm prior scholars’ findings. For example, Yeon et al. (2021) identified that having a greater proportion of family members within a company’s management team will result in a lower level of innovation output. Furthermore, prior research shows that internally sourced family managers are usually chosen from a smaller and less promising talent pool, and they may not have the necessary skills for fostering effective innovations within their companies (Mehrotra et al., 2011). Therefore, having a higher proportion of family members in a management team could negatively affect a family firm’s innovative capability.

In addition, the findings of this research support the SEW perspective. When considering their firms’ business strategies, family board directors are more likely to pursue activities that will increase the family firms’ SEW, such as reputation and identification (Deephouse & Jaskiewicz, 2013). Thus, when internal family members dominate the board, the likelihood of the misuse of firm resources is potentially higher (Matzler et al., 2015); when this occurs, vital resources that could have been invested in the development of innovative programs will be removed. In family firms, internal family members are often selected to be board members based on their status and power within the family, and these family members often lack the required professional abilities (Gallo & Sveen, 1991; Tan et al., 2021). As board directors need to play an important role in providing professional advice to a firm (Dalton & Daily, 1999), any lack of expertise will negatively influence the conduct of innovative strategies, including the creation of new patents and products. Based on this understanding, this study contributes to the existing literature (Kor, 2006; Su & Lee, 2013) by providing further evidence regarding the negative influence of family involvement on firms’ innovative capability.

This study also explored the moderating effect of HR redundancy. Notably, those redundant employees often do not have the necessary skills to directly assist their enterprise in achieving beneficial strategies and outcomes. However, these redundant employees could continuously provide stable external capital for their family firms, such as building stable and solid social networks with clients, suppliers, and the local community (Carney, 2005; Niehm et al., 2008). Prior research has revealed that these stable social networks could more easily assist family companies in accessing financial resources that are needed for successful innovations (Leenders & Dolfsma, 2016). Furthermore, the additional external investments that could be obtained due to an improved social reputation (enhanced through HR policy) could alleviate family owners’ difficulties with securing the required finances to conduct innovative investments. Also, an enhanced firm reputation (one dimension of SEW) could weaken the family owners’ aversion to the loss of SEW, and, thus, relieve their reluctance to conduct innovative investments.

The results from this research also show that this behavior of preserving SEW (through a special internally oriented HR policy) can reduce the negative impact of family governance involvement on innovation capability. Family businesses’ high motivation and commitment to the retention of redundant human resources may preserve these board members’ sense of job security, and thus, reduce their aversion to innovative strategies while also encouraging them to allocate more resources to innovative projects. This explains why a HR policy that supports redundancy in family firms could potentially reduce the negative relationship between family governance and innovative investment. Although some of the internal family members sitting on the board may not have the required professional or technical skills and cannot bring along technical counsel and guidance to help with a business’s innovations, it is still considered appropriate to retain them as board members.

It has been noted in the literature that even family board members who lack the required innovation skills may still play an important role in monitoring the company (Johannisson & Huse, 2000; Tan et al., 2021). According to agency theory (Fama & Jensen, 1983), the principal owners will choose a board of directors to supervise the management team (agent), and the information asymmetry or mistrust between internal members and externally hired employees is also a major component in the agency theory framework. An increase in the number of internal employees who are hired based on family relationships and network ties could alleviate the information asymmetry between internal and external employees, as this facilitates the board’s supervision over the entire family enterprise. This effectively reduces the leakage of innovative secrets, and the resulting reduction of information asymmetry may assist in fostering a higher level of internal social capital. Overall, the result of this study is consistent with Allameh’s (2018) study, which found that a high level of internal social capital (knowledge sharing in the firm) could be beneficial to enterprises’ radical innovation (innovative output). Based on the above discussion, it can be seen that the negative effect of family governance (caused by board members’ lack of professional skills) on family firms’ innovative capacity could be weakened through unique HR policies in family businesses.

Contributions to Theory and Practice

From a theoretical perspective, this study extends the BAM in a family business context on the basis of Chrisman and Patel’s (2012) model by additionally considering family firms’ unique pursuit on their socio-emotional wealth (see Figure 2). Both the standard BAM and the Chrisman and Patel (2012) models tend only to focus on how various economic indicators would impact a family firm’s risk-taking behaviors, thus neglecting the importance of non-economic factors and their potential influences to family businesses. This study attempts to address this gap and further explores the moderating influence of HR redundancy which has not been emphasized in this context by previous researchers. By considering the duality of family businesses in their pursuit of both financial and socio-economic wealth, this study delivers new insights that contribute to the literature on family firm research. This study also contributes to the HR literature by highlighting the positive aspects of family firms’ unique HR policy (the retention of redundant employees), noting that HR redundancy may partially reduce the negative effects of family involvement on innovative capability with the research results suggesting that family firms’ redundant employees could bring potential social capitals to their businesses that support innovative activities.

Next, this study contributes to the SEW literature, especially to the dimension of emotional attachment. Retaining redundant employees in their positions is an important way of preserving emotional ties within a family business, and the results of this study show that HR redundancy could potentially be advantageous to a family firm’s innovative capability. This offers a differing view to existing studies that have emphasized the negative impact of SEW on family firms’ risk-taking behaviors. This study extends the knowledge of how family firms’ HR redundancy could affect the relationships between each dimension of family involvement and family firms’ innovative capability and further shows that that the effects of HR redundancy on family firms’ innovation may differ depending on the different dimensions of family involvement.

The results from our study highlight some important practical implications for family firms. In the design and implementation of HR policy within family firms, one major dilemma often faced by decision-makers is the need to consider a trade-off between either retaining or retrenching redundant employees. This concern may arise as part of an organization’s need to streamline its staff size, for example, during the introduction of new technologies into the firm or when there is a need to retrench family employees whose skills and knowledge have become obsolete. The positive influence of HR redundancy as highlighted in this study could be important in assisting policy makers in evaluating whether redundant employees may have an indispensable role to play in fostering the innovative strategies of family firms. Although these redundant employees may not be able to assist their firms directly due to lack of required operational expertise, their continuing employment could present other unique advantages, for example, if they have the ability to enhance social capital/network that would benefit their firms’ business.

Limitations and Future Research Directions

There are some limitations to this study that should be noted. First, this study has utilized only family-owned SMEs as the research sample. Thus, the results may only apply to family firms in the SME category and may not be generalizable to larger-sized family enterprises. Future research can be conducted with larger-scale family businesses to explore whether the excessive size of HR redundancy will significantly strengthen the negative impact of family involvement on innovative capability. Second, this is a country-based study that has only focused on Chinese family-owned firms. As such, it should be noted that the results may only apply to family businesses located in China but may not be generalizable to family firms located in other countries. Future research may consider a similar investigation conducted in a different country or region. There is also potential for a cross-country comparison to identify similarities and differences between Chinese and non-Chinese family businesses. Finally, it should be noted that SEW includes multiple dimensions and HR redundancy highlights only the dimension of emotional attachment. How the other dimensions of SEW may potentially impact on the relationship between family involvement and innovative capability deserves to be further explored in future studies.

Conclusions

This study complements prior research that investigates the relationship between family involvement and innovative capability and attempts to addresses some of the existing gaps relating to the role of SEW and HR redundancy. The benefits of SEW in boosting family SMEs’ innovative capability is supported in our results. Specifically, this study confirms that HR redundancy can partially weaken the negative relationship between family involvement and innovative capability, which effectively challenges the traditional views regarding the negative influence of HR redundancy on an organization’s development. In addition, this study further extends the BAM in a family business context by considering family firms’ non-economic/socio-emotional pursuit in their decision-making process, which highlights a rich research area that has much potential for future studies that may further explore issues relating to the influence of non-economic factors on family businesses.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

We used secondary database while collecting all the data in this study. The data in the database is open to public thus ethical approval is not applicable for this study.