Abstract

This study investigates calendar anomalies in eight Islamic frontier markets. Our sample consists of the daily closing prices of their stock indices for the period of January 2006 to September 2019. The data are categorized with respect to day-of-the-week and month-of-the-year according to both the Gregorian and Islamic calendars. We control for time-varying systematic risk using Morgan Stanley Capital International (MSCI) index as the proxy for the market portfolio and apply Bonferroni correction to reduce the occurrence of false-positive results. We find little support for the proposition that any of the Islamic calendar months generate abnormal returns, bar a slight negative abnormal return during the holy month of Rajab for Kuwait. We find evidence of a small negative Monday effect for the stock markets of Bangladesh and Pakistan and a small positive January effect for the stock market of Morocco. The results support weak-form market efficiency, suggesting that investors in frontier stock markets should not expect to outperform the market on a consistent basis when trading on particular days of the week or months of the year according to the Islamic or Gregorian calendar.

Introduction

The term anomaly can be traced back to Kuhn (1970) who labeled it as “any discovery that despite repeated effort cannot be aligned with expectations that govern normal science” (p. 53). Indeed, financial market anomalies imply stock market returns are predictable, in stark contrast to Fama’s (1970) weak-form efficient market hypothesis (EMH), also known as the random walk hypothesis. The theory states that all information contained in historical price data is completely reflected in current stock prices. As such an analysis of this data alone cannot aid market participants in predicting future price movements. One of the most documented financial market anomalies are calendar seasonalities, that is, predictable market returns related to the days or months of the calendar year (Ikenberry & Lakonishok, 1989; Lakonishok & Smidt, 1988). In terms of day-of-the-week effects, many studies document that stock market returns tend to be negative on Monday and positive on Friday (French, 1980; Gibbons & Hess, 1981; Jaffe & Westerfield, 1985; Kato, 1990; Rogalski, 1984; Solnik & Bousquet, 1990). The January (turn of the year) effect is one of the most well-documented stock market anomalies, with stock market returns in this month significantly higher than in other months of the year (Patel, 2016; Rozeff & Kinney, 1976; Wachtel, 1942). Calendar anomalies have been documented in other financial markets as well, including futures markets (Cornett et al., 1995; Truong & Friday, 2021), currency markets (Berument et al., 2007; Corhay et al., 1995; Ke et al., 2007; McFarland et al., 1982; Yamori & Kurihara, 2004), and crude oil and gold markets (Yu & Shin, 2011).

In this paper we examine week-of-the-day and month-of-the-year calendar anomalies in the returns of the stock markets of several Islamic frontier markets. The underlying motivation for our selection of frontier markets is that these markets have attracted considerable attention from investors ever since they have been designated as a separate category of developing markets by the International Finance Corporation (IFC) in 1996. Frontier markets are a subset of emerging markets that remain relatively local in character, primarily shaped by internal economic and political dynamics. These markets are characterized by their low correlation with other markets, low liquidity and small market capitalization, and thus are thought to exhibit substantial weak-form market inefficiencies. We focus on Islamic markets to establish whether Islamic religious activity results in calendar anomalies that investors may be able to exploit. So far, researchers have been rather careful in claiming a link between religious activities and economic outcomes (Weber & Kalberg, 2013).

We contribute to the literature on calendar anomalies in two main ways. We are the first to test for the presence of day-of-the-week and month-of-the year effects according to both the Gregorian and Islamic calendar in frontier markets. Islamic calendar effects have been studied substantially less than their Gregorian equivalent. In the Islamic calendar, 4 months are especially sacred and important where the spiritual reflection and special attention is emphasized: Muharram, Rajab, Dhul Qa’dah, and Dhul Hijjah. Muharram is the first month of the Islamic calendar and the first of the four sanctified months with which the Muslims begin their Hijri calendar. It has certain characteristics peculiar to fasting during this Islamic month. The 10th day of Muharram (the day of Aashurah) is the most sacred among all its days. Rajab is the seventh month of the Islamic calendar, meaning “to respect.” It is when Muslims should start preparing for the coming month of Ramadhan. Rajab is derived from the word forbidden as fighting is forbidden in this month. Dhul Qa’dah is the 11th month of the Islamic calendar and the first of the four sanctified months in which battles were prohibited in the days of the Prophet. Dhul Hijjah is the 12th and last month of the Islamic calendar, which means the month of Hajj (Pilgrimage). The Hajj is the fifth “Pillar” of Islam. The first 10 days are the most virtuous in this whole month, with a fast on any of these days equivalent to fasting throughout the year. Ramadhan, the ninth month of the Islamic calendar, has specific significance in the Islamic calendar, widely known for the full month of fasting. The month of Ramadhan is when the Quran was revealed, providing a special opportunity for every Muslim to strengthen his/her faith, to purify the heart and to remove the evil effects of the sins committed. The least sacred months in the Islamic calendar are the second month (Safar), the fourth month (Rabi’ul Akhir), the fifth month (Jumaad al Oola), and the sixth month (Jumaad al Thani).

Our second contribution is that we apply robustness to our research by controlling both for time-varying systematic risk and applying Bonferroni correction, which should substantially reduce the chances of obtaining false-positive results (type I errors) for calendar anomalies.

Our analysis provides support for weak-form market efficiency in frontier markets, revealing no substantial evidence that religious activity leads to potential profit opportunities for investors. We find a negative abnormal return during the Islamic month of Rajab for Kuwait only. In terms of Gregorian calendar effects, the results reveal a small negative Monday effect for the stock markets of Bangladesh and Pakistan, and a small positive January effect in the stock market of Morocco. In sum, our results suggest that investors in frontier markets should not expect to outperform the market on a consistent basis when trading on a particular day of the week or month of the year.

The rest of our paper is organized as follows. We review the extant literature on calendar anomalies in Section 2. In Section 3 we present the data and method used to test for market anomalies. We discuss the empirical results in Section 4, followed by a summary and conclusion in Section 5.

Review of the Literature

There is an extensive literature on seasonality in stock market returns both for developed and emerging countries. Day-of-the-week effects in developed markets have been documented by Osborne (1962), Cross (1973), Jaffe and Westerfield (1985), and Mbululu and Chipeta (2012), amongst many others. Generally, low mean returns are observed on Monday relative to other days of week, whilst mean returns on Friday tend to be positive and abnormally high. Aggarwal and Rivoli (1989) examine seasonal and daily patterns in equity returns of four emerging markets: Hong Kong, Singapore, Malaysia, and the Philippines. They find support for a weekend effect in the form of low Monday returns. In addition, they find a strong Tuesday effect, which they argue may be related to the time difference between New York and emerging markets. Anwar et al. (2021) find a significant negative Monday effect and a positive Thursday effect across many of the developing countries they examined. Gkillas et al. (2021) show a positive return on Wednesdays for the majority of the 17 international equity markets they examined. Khan et al. (forthcoming) show a significant day-of-the-week effect in the returns in China, South Korea, Taiwan, Thailand, Indonesia, and Pakistan. Wuthisatian (2021) reports a negative Monday effect for the Thai stock market. In contrast, for China positive Monday returns are reported by. Ali and Ülkü (2020).

Like day-of-the-week effects, there has also been extensive work on month-of-the-year calendar anomalies. Most studies focus on return-based patterns without adjusting for systematic risk. Rozeff and Kinney (1976) present the first formal evidence of seasonality in the monthly returns on the New York Stock Exchange from 1904 to 1974. With the exception of the 1929 to 1940 period, they find statistically significant differences in mean returns across the months due primarily to large January returns. Similar results were reported by many others (Agrawal & Tondon, 1994; Barone, 1990; Gultekin & Gultekin, 1983; Ziemba, 1999). For emerging markets, Aggarwal and Rivoli (1989) show higher returns in January compared to any of the other months. Ignatius (1998) provides evidence for seasonality in the monthly prices of the Bombay stock exchange with large returns in December relative to other months, questioning the random walk hypothesis. Wong and Ho (1986) find higher returns in the month of January for the Singapore stock market. Using the stochastic dominance (SD) approach, Lean et al. (2007) confirm the presence of significant month-of-the-year effects for several Asian markets. However, they note that the first-order SD of the January effect appears to have largely disappeared over time.

While the calendar anomalies in stock markets have been explored in a large body of the literature, Islamic calendar anomalies have received considerably less attention. Arguably, religious practice during the Islamic calendar months could affect the economic activities in the Islamic world, creating seasonal patterns in stock market returns. Several studies have examined Islamic calendar anomalies in stock markets across the Islamic world (Al-Hajieh et al., 2011; Al-Ississ, 2010; Al-Khazali, 2014; Al-Khazali et al., 2017; Białkowski et al., 2012; Halari et al., 2019; Oğuzsoy & Güven, 2004; Seyyed et al., 2005; Wasiuzzaman & Al-Musehel, 2018). For the Istanbul stock exchange, Oğuzsoy and Güven (2004) find a significant positive return during the month of Ramadhan only. Similar findings of a Ramadhan effect have been reported by others (Al-Hajieh et al., 2011; Al-Ississ, 2010; Al-Khazali’s, 2014; Białkowski et al., 2012; Wasiuzzaman & Al-Musehel, 2018). Nevertheless, a number of studies that explicitly investigate the existence of a link between Islamic religious activity and stock market returns find no evidence such a link exists. For example, Seyyed et al. (2005) find no evidence that the month of Ramadhan impacts the stock market returns of Saudi Arabia. Whilst Mustafa (2008) finds evidence for significant positive returns in the months of Shawwal and ZilQad, he finds no evidence for abnormal returns during the most significant month of the Islamic calendar (Ramadhan). Wasiuzzaman (2017) finds no evidence for abnormal returns in the month of Hajj for Saudi Arabia. Most recently, Ali et al. (2017) reveal small positive abnormal returns for the holy day of Eid-ul-Fitr for Pakistan, Bahrain, Saudi Arabia, and Turkey, but no significant abnormal returns for all other holy days in the Islamic calendar (including Ramadhan). Since Islamic calendar effects could not be replicated in a number of recent studies, more research is in order to resolve whether religious activity poses a challenge to the weak-form efficient market hypothesis.

Data and Method

Data

For our empirical analysis we obtain the closing prices of eight Islamic frontier markets (Table 1) together with Morgan Stanley Capital International Frontier Markets (MSCI-FM) index from DataStream database for the period January 2006 to September 2019 (a total of 3,584 observations). The MSCI Frontier Markets Index captures large and midcap representation across 28 frontier market countries. The index includes 95 constituents, covering 85% of the free float-adjusted market capitalization in each country. MSCI divides financial markets into three main categories: developed, developing, and frontier markets based on economic development, size, and liquidity requirements and market accessibility criteria. Whilst what constitutes a frontier market remains open to interpretation, at the time of data collection, 21 markets were classified as frontier markets. Our sample consists of eight Islamic countries (see Table 1) included in their classification of frontier markets.

Selection of Islamic Frontier Markets.

We compute the daily continuously compounded market returns

where

We apply the Augmented Dickey-Fuller (ADF), Phillips-Perron (PP), and Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test of stationarity in returns. The results in Table 2 show that for all stock markets and MSCI-FM, both the ADF and PP test reject (p < .01) the null of unit root in returns. Likewise, the KPSS test shows that the null of stationarity in returns cannot be rejected at the 1% significance level for these markets. Thus, we conclude that the data are stationary.

ADF, PP, and KPSS Test for Unit Root.

Note. Dickey-Fuller (ADF), Phillips-Perron (PP), and Kwiatkowski-Phillips-Schmidt-Shin (KPSS) test of stationarity in returns.

and *** shows significance at the 10% and 1% levels respectively.

Method

Day-of-the-week effects

To test for difference in mean returns across the various days in a week, we estimate equation (2):

where

Equation (2) does not include the systematic risk factor. The possibility of low/high returns on certain days might be explained by corresponding variation in systematic risk across the days. To estimate the risk-adjusted market return, in equation (3) we include the return on the MSCI-FM price index as our proxy for the market portfolio:

If any of the dummy variables in equation (2) become insignificant in equation (3), this would suggest that the mean return on that day can be accounted for by the systematic risk-return relationship and cannot be considered a day-of-the-week return anomaly.

To control for time-varying systematic risk across each day of the week, we include interaction variables in the regression specification, that is, we multiply each of the day-of-the-week dummies with MSCI-FM index return. Thus, the following time-varying risk equation is estimated:

If any of the α-coefficients remain significant we have a day-of-the-week return anomaly which is not accounted for by seasonality in the systematic risk premium.

Gregorian month-of-the-year effects

To test for month-of-the-year anomalies according to the Gregorian calendar, we use a similar strategy. To test for the difference in mean returns across the months of the year, we regress the returns on the market index on 12 dummy variables as follows:

where Mi are the dummy variables representing January to December, respectively (Mi = 1 if month t is January, and 0 otherwise). Just like in the case of testing for day-of-the-week effects, we control for the risk-adjusted market return, where market risk is captured by the MSCI-FM index return. This relationship is written as follows:

We compare equations (5) and (6) for a change in the significance of the α-coefficients. In equation (7) we use interaction terms, where we multiply each of the month-of-the-year dummies with the MSCI-FM index return, to control for seasonality in the risk-return relationship. Thus, the returns equation can be written as follows:

On the same grounds, the α-coefficients in equation (7) will be compared with the corresponding ones in equations (5) and (6) to find out whether the month-of-the-year effect can in indeed be considered a return anomaly.

Islamic month-of-the-year effects

We use a similar strategy as for the Gregorian months to test for Islamic month-of-the year effects. Instead of Gregorian months being represented by Mi, the dummy variables represent the 12 Islamic calendar months, that is, Muharram, Safar, Rabi-ul-Awal, Rabi-Uthani, Jumadi-ul-Awal, Jumadi-Uthani, Rajab, Shaban, Ramadhan, Shawwal, Dhu_al_Qi_dah, and Dhu_al_Hijjah.

Bonferroni correction

To reduce the chances of false-positive results (type I errors) when multiple pair-wise statistical tests are performed on a single set of data, we adjust the significance of the estimated coefficients using the Bonferroni correction (Bonferroni, 1935), also known as the Bonferroni type adjustment. The critical values are computed as follows:

where k is the number of comparisons on the same dependent variable.

Results

Day-of-the-Week Effects

In Table 3, we report the α-coefficients of equation (2) that estimates the average stock market returns on the 5 days of the week. We find evidence of significant day-of-the-week effects for seven out of the eight Islamic frontier markets. Consistent with the prevailing literature, we find a negative Monday effect for the majority of the countries examined: Bangladesh (−0.35%), Pakistan (−0.15%), Jordan (−0.11%), and Kuwait (−0.10%). The odd one out is Palestine, showing a large positive (0.68%) Monday effect. On Tuesday, Bangladesh and Pakistan have positive mean returns of 0.21% and 0.10%, respectively, whilst Palestine has a large negative mean return of −0.79%. Further, we find a positive Wednesday effect for Pakistan (0.15%), and a positive Thursday effect for Jordan (0.08%) and Oman (0.07%). Finally, only for Pakistans’ stock market do we find a significant positive Friday effect (0.11%).

Day-of-the-Week Effects in Islamic Frontier Markets.

Note. The model estimated is

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

Table 4 shows that after inclusion of MSCI-FM price index as a proxy for the market portfolio, the only evidence of a negative Monday effect is for the stock market of Bangladesh and Pakistan. The statistical significance of the large positive Monday effect for Palestine disappears. Whilst the evidence of the Tuesday and Wednesday effect remain intact, no evidence remains for a Thursday or Friday day-of-the-week effect. The results show that the beta coefficient (MSCI-FM Index) is statistically significant (after Bonferroni type adjustment) for all countries, except Bangladesh and Palestine.

Day-of-the-Week Effects With the Inclusion of a Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

In Table 5 we find that the evidence for day-of-the-week effects, except for Monday, disappears after controlling for day-of-the-week seasonality in systematic risk. Only the negative Monday effect remains for Bangladesh and Pakistan. The results shows that the average systematic risk level varies throughout the days of the week. For instance, the beta coefficient for Oman’s stock market ranges from .31 on Friday to .63 on Thursday. Similar variations are noted on different days of the week in the other Islamic frontier markets.

Day-of-the-Week Effects With the Inclusion of Interactive Dummy Variables With the Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

In sum, the results show no substantial evidence for the presence of day-of-the-week anomalies in Islamic frontier markets, except for a negative Monday effect for Bangladesh and Pakistan.

Gregorian Month-of-the-Year Effects

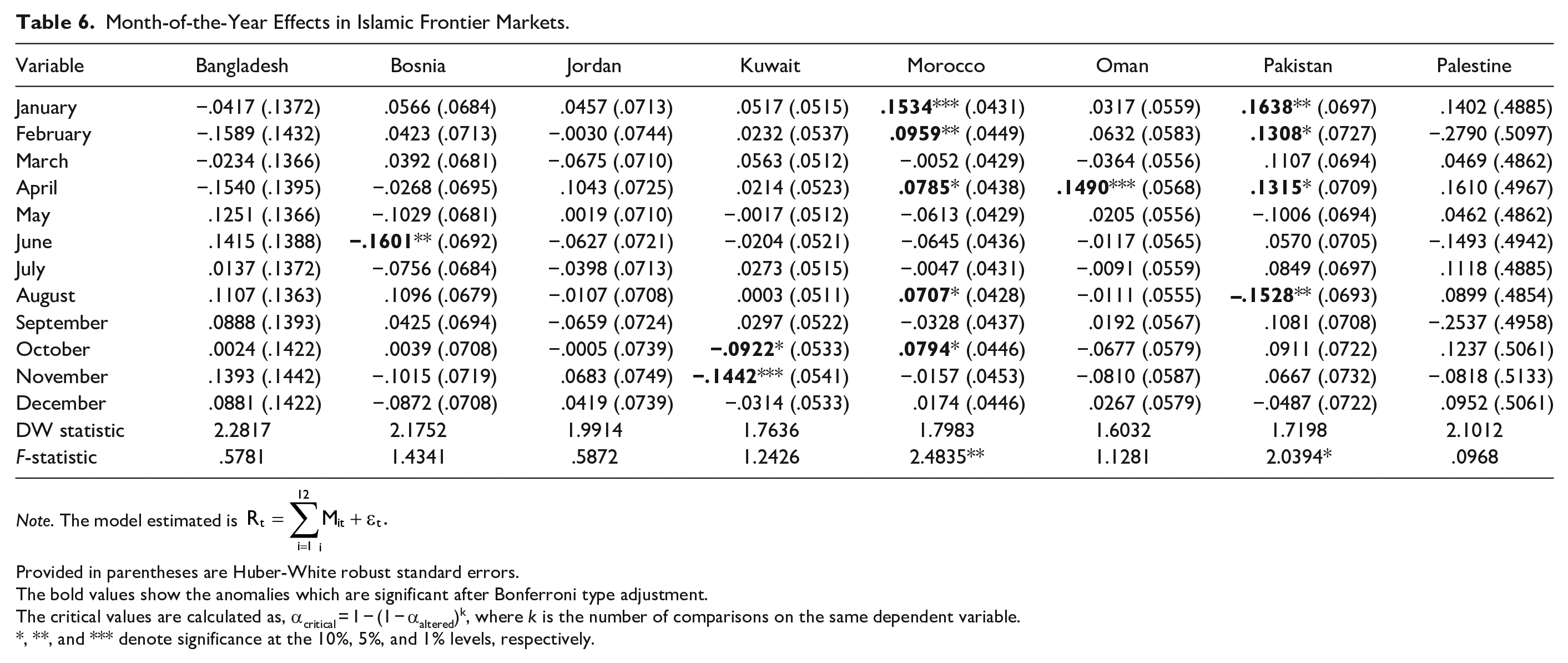

Table 6 presents the results of equation (5) for month-of-the-year effect as per the Gregorian calendar. The evidence for month-of-the-year anomalies (after Bonferroni adjustment) is much weaker than for day-of-the-week anomalies. We only find evidence for a positive January effect (0.15%) for Morocco, a positive April effect (0.14%) for Oman, and a negative November effect (−0.14%) for Kuwait.

Month-of-the-Year Effects in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

We place the estimates of equation (6) in Table 7 which shows that the evidence of the month-of-the-year effect becomes even weaker after controlling for systematic risk. Only the modest positive January effect for Morocco remains intact.

Month-of-the-Year Effects With the Inclusion of a Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

Table 8 reports the results of equation (7). Again, only the positive January effect for Morocco remains intact after taking account of month-of-the-year seasonality in systematic risk.

Month-of-the-Year Effects With the Inclusion of Interactive Dummy Variables With the Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

Islamic Month-of-the-Year Effects

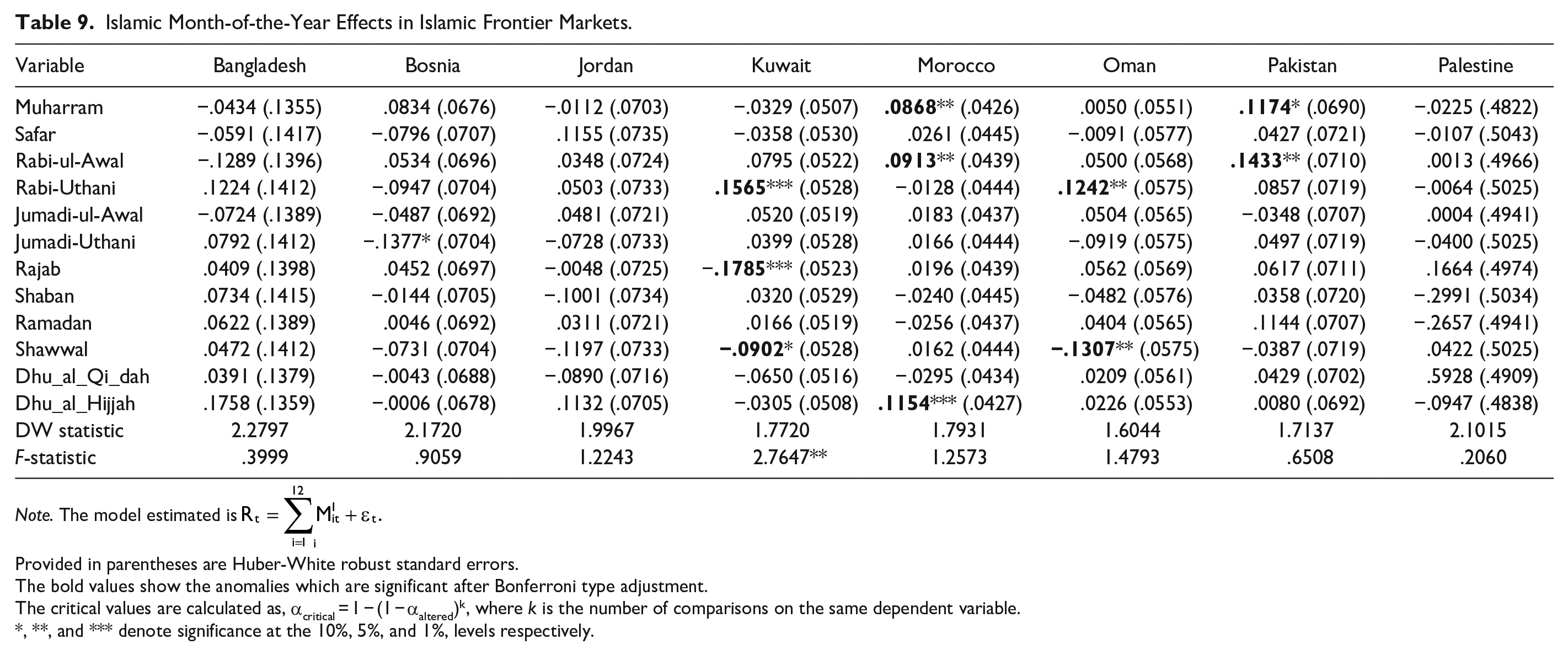

Next, we examine the impact of religious practice on financial markets. The estimates (after Bonferroni correction) from equation (5) of month-of-the-year effects according to the Islamic calendar are placed in Table 9. The results show Islamic month-of-the-year effects for two of the eight Islamic frontier markets examined. Kuwait’s stock market exhibits a significant positive mean return of .15% in the month of Rabi-Uthani and a significant negative mean return −.17% in the month of Rajab, whilst Morocco exhibits a positive mean return of .11% in the month of Dhu_al_Hijjah. In short, we find no significant month-of-the-year effects for the religious important months of Dhul Qa’dah, Muharram, and Ramadhan.

Islamic Month-of-the-Year Effects in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1%, levels respectively.

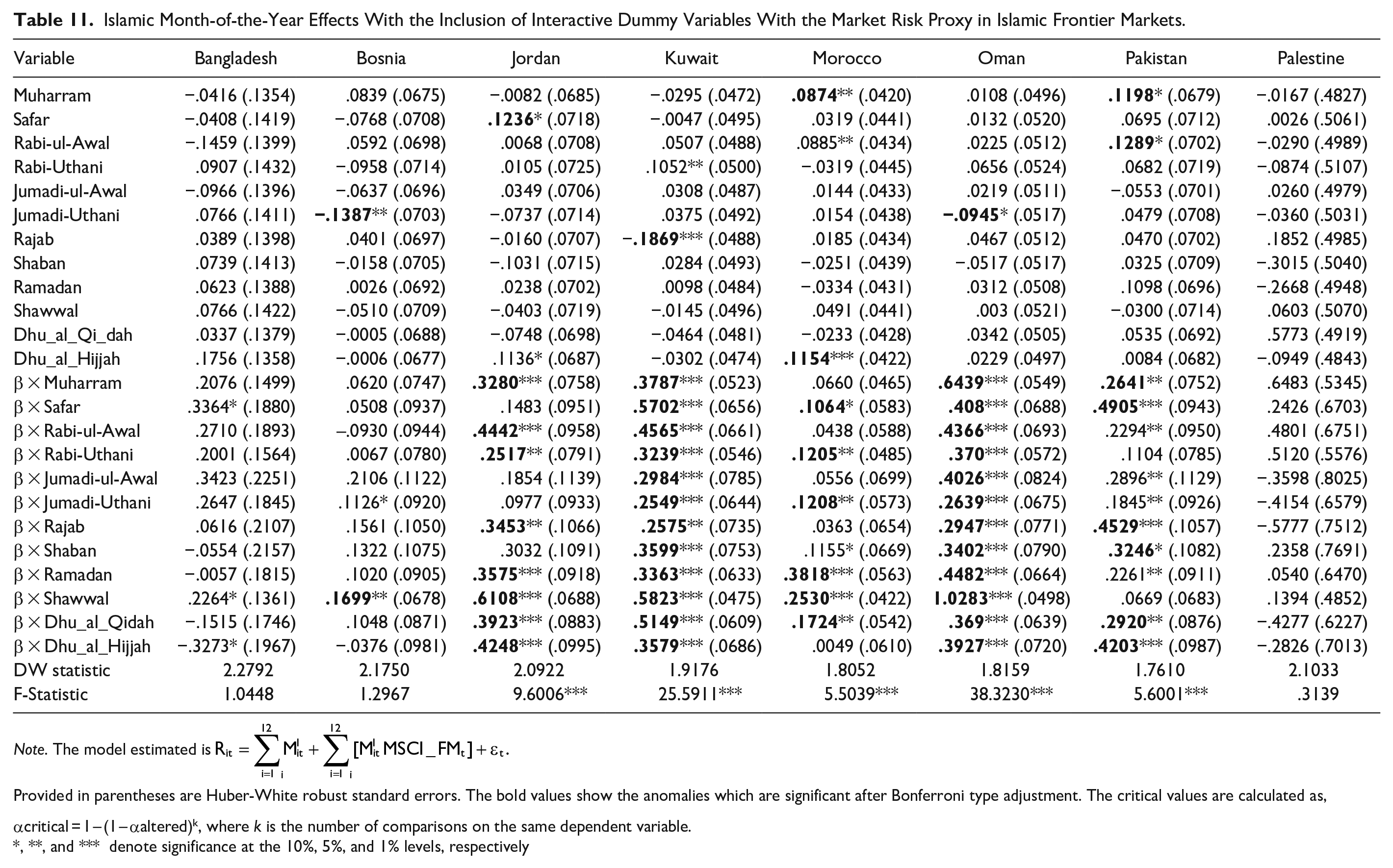

Table 10 presents the results from equation (6), controlling for systematic risk. We find the evidence for Islamic month-of-the-year effect weakens further when systematic risk is accounted for. The only significant effect that remains is the negative mean return (−0.17%) in the month of Rajab for Kuwait’s stock market. Table 11 presents the results from equation (7) which takes into account time-varying systematic risk. Again, the negative mean return in the month of Rajab remains intact for Kuwait. Further, we find that the systematic risk level varies across Islamic months for all countries, with the exception of Bangladesh, Bosnia, and Palestine. For instance, the beta for Oman varies from 0.26 in Jumadi-Uthani to 1.02 in Shawwal.

Islamic Month-of-the-Year Effects With the Inclusion of a Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors.

The bold values show the anomalies which are significant after Bonferroni type adjustment.

The critical values are calculated as, αcritical = 1 − (1 − αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively.

Islamic Month-of-the-Year Effects With the Inclusion of Interactive Dummy Variables With the Market Risk Proxy in Islamic Frontier Markets.

Note. The model estimated is

Provided in parentheses are Huber-White robust standard errors. The bold values show the anomalies which are significant after Bonferroni type adjustment. The critical values are calculated as, αcritical = 1 – (1 – αaltered)k, where k is the number of comparisons on the same dependent variable.

, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively

The absence of any significant evidence of an Islamic month-of-the-year effect in the Islamic frontier markets is in line with the results of Syed and Khan (2017) who also fail to provide any evidence of Islamic calendar effects for Pakistan, suggesting that religious activity may not be linked to economic activity and market returns.

Conclusion

When looking for quick profits, money managers search extesively for market anomalies. In this study we explore the presence of day-of-the-week and month-of-the-year market anomalies, and the impact of religious activity on financial markets. Our sample consist of eight Islamic frontier markets over a 14-year period from January 2006 to September 2019. We control for time-varying systemic risk and apply Bonferroni-type adjustment to reduce the occurrence of false-positive results (type I errors).

Our analysis reveals no substantial evidence for the presence of calendar anomalies in the stock market returns of Islamic frontier countries, supporting weak-form market efficiency. We only find evidence of a small negative abnormal return during the Islamic month of Rajab for Kuwait. This seventh month of the Islamic calendar is especially sacred and important, with the Muslims preparing for the coming month of Ramadhan. Further, our analysis reveals a small negative Monday effect for the stock markets of Bangladesh and Pakistan and a small positive January effect for Morocco. Additionally, we find that systematic risk varies with respect to day-of-the-week and month-of-the-year, confirming the findings of Brooks and Persand (2001). Our findings have key implications for mutual funds in America, Europe, and other parts of Asia which offer investors direct exposure to frontier market indices. Such institutional investors often have large pool of funds with flexible investment decisions allowing them to postpone or accelerate their buying and selling decisions. The results imply that investor in frontier markets should not expect to outperform the market on a consistent basis when trading on particular days of the week or months of the year according to the Gregorian or Islamic calendars.

Our research is not without limitations. With respect to religious effects, rather then focussing on entire months, future studies could focus more narrowly on only the most holy days within Islamic months when the religious experience is most intense. To add further robustness to our results, future studies could employ non-parametric methods and/or include a larger pool of Islamic/frontier markets over a longer period of time to increase the power of the statistical tests. We will leave these suggestions for others to explore.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.