Abstract

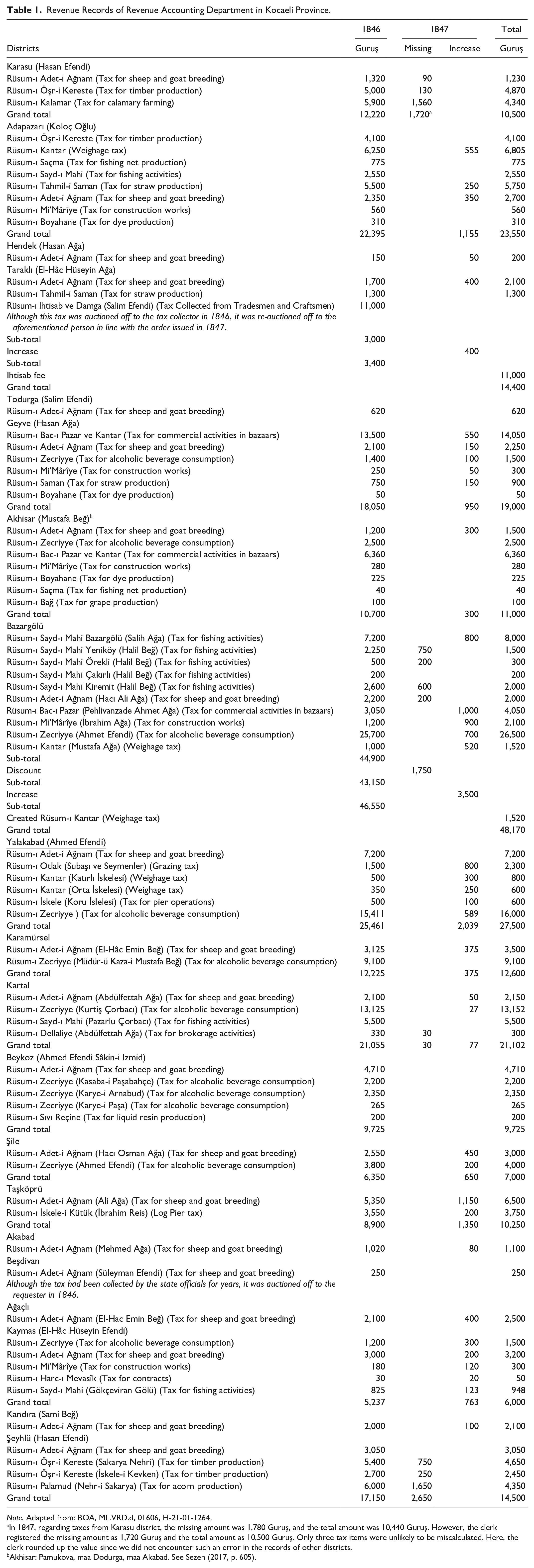

Unlike the European nations that shifted from privatized tax collection to a centralized government control system, the Ottoman Empire successfully maintained its tax farming system. Yet, there is ample evidence against the views that such a system was backward and wasteful are not entirely correct, but that the Ottoman tax collection method was successful in its own historical context. Therefore, the aim of this study was to reveal evidence of whether the Ottoman Empire implemented a successful tax farming system in the 19th century based on the accounting records of tax farming revenues considering the Ottoman public finances, institutional infrastructure, and administrative practices in a broader European context. Accordingly, the present study utilized the Prime Minister’s Ottoman Archives, the records of Revenue (Varidat) Accounting Administration, and the tax farming auctions in the Central Council (Majlis-i Val’a). The economic and financial conditions of the period were also considered in the analysis of the data. Evaluation of the tax collected by tax collectors in Kocaeli Province (Sancak) revealed the nature of economic activities in the empire. It can be stated that tax collectors in Kocaeli Province paid the total amount of 395,612 Guruş (Ottoman currency) tax revenue in five installments in 3 months and that the highest tax was collected from the sales of alcoholic beverages. Adet-i Ağnam (the tax collected for sheep and goat breeding) collected from each district was auctioned for tax farming price of 51,610 Guruş. In addition to these taxes, taxes from trade, forestry, maritime, and industrial production were included in the tax farming revenues. Overall, considering the adverse political and economic conditions in the historical process, the Ottoman Empire’s tax farming system was successful in collecting taxes and was a part of the formation of the modern Ottoman public finance system.

Introduction

Although tax farming, referring to the granting tax collection task to profit-seeking individuals, was common in most European countries before the 19th century, this method of privatization disappeared thanks to the French Revolution and the Napoleonic Wars. However, the Ottoman Empire maintained tax farming as an effective means of generating revenues from customs procedures, domestic and foreign trade, and agricultural production. In the Ottoman case, tax farming was not only related to the fact that it continued throughout the century as an essential mechanism of an extensive revenue collection system but also mainly related to direct taxes on agricultural production as well as indirect taxes such as customs duties (Özbek, 2018).

In recent years, European economic historians have compared the relationship between nations’ financial performances and institutional environments, exploring historical trends in the financing of liberal states and the different paths to modern public finance systems. While clustering is evident in Europe regarding the formation and consolidation of modern fiscal states, a closer examination of situations in each nation highlights their differences. Differences in national experiences require broad and flexible concepts about an exemplary fiscal state and its public finance system. Alongside such conceptual needs, the increasingly privatized governmental technologies of the neoliberal era have also encouraged a critical rethinking of our approaches and concepts (Özbek, 2018). In this context, this study aimed to reveal evidence of whether the Ottoman Empire implemented a successful tax farming system in the 19th century based on the accounting records of tax farming revenues considering the Ottoman public finances, institutional infrastructure, and administrative practices in a broader European context. Tax farming is a system in which the right to collect certain taxes is awarded to the highest bidder. The tax collector then retained the collected revenue. A winning bidder seeking to maximize profits would operate when private marginal revenue equals marginal cost. Tax farming represents a private finance solution to the tax collection problem of the states (Stella, 1993).

The previous research points out that about two-thirds of the net tax revenues, in other words, after deducting the expenses from the gross tax revenue, was distributed to tax collectors in the provinces, money changers, and high-level bureaucrats participating in the tax farming auctions in the capital city and sharing all tax resources among themselves in the 18th-century Ottoman Empire (Karaman & Pamuk, 2009). In the 19th century, while only 24% of the remaining revenue after deducting the tax collection costs, 30% was granted to the collectors, and the guarantors received the rest (Buluş, 2010).

Reaching consistent, homogeneous, and reliable data about the Ottoman economy becomes possible upon examining the document collections of the bureaucracy. A significant part of the revenues, which is the fundamental need of a centralized state, is obtained from the taxes for various economic activities. “Mukataas” (a kind of tax resource) in different regions of the empire were registered in a very systematic way by the offices registered under the Revenue Office. These records allow one to construct quantitative series and correctly interpret specific characteristics of the Ottoman economy (Genç, 2010).

As expected, keeping and closing the budget accounts in the empire accounting were different from contemporary methods. The realized revenues and expenses were started to be recorded on an accrual basis from 1846 to track the revenues and expenses of the state in a more systematic and institutional manner. Accordingly, if revenue or expense was collected in the current year but accrued in previous years, it was used to be recorded in the account of the year in which it was accrued, not in the current year’s account. Therefore, although the fiscal year was over, a year’s budget was not closed at the end of that year thanks to the exercise method; the administration could track the account movements of each year in the following periods. While the Ottoman accounting was based on the ladder or subtraction method, in which the expenses were subtracted from the revenues, the state accounting records began to be kept according to the double-entry method as of March 1882, as in Schneider’s System. However, this system was not settled in the entire public sector even at the beginning of the 20th century (Akkuş, 2013).

Recent years have witnessed a search for a novel and more efficient public administration with approaches for reforming the conventional understanding of public administration. Some of these approaches do not hold public finance separate from the proposals for the autonomy of the public administration. Therefore, there are ongoing debates on establishing more efficient tax administrations with relative autonomy. However, acting as if these proposals were put forward for the first time or there were no autonomous local administrations before is in need of correction. In this sense, tax farming as a kind of public administration may present robust historical evidence for the abovementioned efficient tax administration reform. Not only do contemporary states always have a desire to elevate tax revenues upon enhancing tax-collecting efficiency but deceased empires also had the same financial concern. As an example, historical practice-based changes in the tax collection methods in the Ottoman Empire depending on the severity of the financing need of the empire actually emerged from the following question: “What method can the administration collect the most tax from the state’s production capacity?” The Timar system emerged first as a response to this question. Later, there were efforts to establish the Iltizam and Malikane systems and a central financial organization in the 19th century (Buluş, 2010).

Modern finance has practices similar to the tax farming system. In this sense, financing products by some public institutions and organizations may become prominent. Such financing products, generally exported as capital market products, can find a place in western countries, particularly in the USA. Revenue Bond or Municipal Bond is a product of public finance exported mainly for financing the urban development projects of local governments in the USA. These bonds are paid upon the tax and operating revenues from related project investments. However, neither of the said financing systems (taxation increase and revenue bonds) has generally no risk-sharing similar to the tax farming system (Varlı, 2014).

The present study would make significant contributions to the literature on the bureaucratic efficiency of Ottoman public finance and the accounting methods of tax farming revenues. To the best of our knowledge, this study is the first to scrutinize the accounting of tax farming revenues and shed light on the economic history of the said region through taxation types. Tax collection procedures and principles of public finance constitute an essential source for accounting history. On the other hand, tax farming auctions were the control mechanism of the Ottoman financial bureaucracy over the tax farming system. Therefore, the present study is also deemed seminal with its contributions to the literature on the Ottoman bureaucracy.

Tax Farming System in the Ottoman Empire

One of the most noteworthy characteristics of the transformation at the end of the 16th century was the increasing role of local elements in the state’s financial structure. In this context, the Ottoman Empire changed its understanding of local government. The most fundamental element of this process was those who were local notables. The fact that the notables were able to obtain tax farms from time to time enabled the spread of the tax farming system and their social power and material gains to increase (Pamuk, 1999; Salzmann, 1993).

The tax farming method was implemented for tax resources that could not be classified in the Timar system in the Ottoman order (Genç, 2010). Consequently, the duty of collecting the taxes from the obliged and delivering them to the central treasury was granted to a group called tax collectors (mültezim) by auction (Cezar, 1986).

Prospective tax collectors would offer the government the price they would undertake to pay annually by estimating the revenue promised by mukataas and collection cost. The one, whose proposal was accepted, would have assumed the taxation rights and powers of mukataas for 3 years (Çizakça, 1999; Genç, 2010).

The entrustment of tax collecting duty to tax collectors for 3 years within the tax farming system led them to act for greedy and excessive returns quickly. Especially, peasants felt under pressure due to such behaviors of tax collectors, which caused the decline of agricultural production, which was the basis of the state’s economy and finance (Pamuk, 2007, p. 149). Harming resources in this way required the central government to take some measures, and the way was paved for the conversion of tax farming to its upgraded form: the Malikane system.

The Malikane system, which appeared in the 13th century, was the system in which mukataas were granted to tax collectors as long as they were alive (kayd-ı hayat). An edict published in 1695 made it possible to convert mukataas into manorial units (Tabakoğlu, 1985). Following the establishment of the system, the auction of mukataas started in Istanbul. The one who made the highest bid for the cash price, which is called muaccele (due and payable) in the auction, was granted a certificate recognizing his rights and responsibilities as the manor owner (Genç, 2010).

Yet, the Malikane system was not able to be a definitive remedy for the financial crisis of the state. The lack of competition conditions in the Malikane market became a factor preventing its effective functioning. Due to the high muaccele prices, some auctioneers engaged in an implicit alliance; thus, the expected revenue could not be achieved from the sums paid to the treasury (Pamuk, 2007). As a distinctive feature of the system, notables did not attempt to own mukataas but used their powers in the regions through sub-tax farming (alt mültezimlik). Consequently, over time, they became a significant social force in the functioning of the tax system as partners to the state and the manor owners (Pamuk, 2007). The transfer of tax collection privilege to others by the tax collectors made it difficult for the central government to control which tax collector had how much right on mukataa units (Kasaba, 1987).

In the system, which maintained its formation for a certain period of time, tax collectors had some economic, administrative, and disciplinary rights over manors. One of these rights was the freedom of mukataa sales. Such features of the system also brought with it the conditions strengthening the local elements. In addition, the fact that taxes were collected by intermediaries, not the tax collectors themselves, led to the formation of a social hierarchy (Bay, 2007). The Malikane system, introduced to ensure the transition of the Ottoman economy from in-kind to in-cash, caused a change in the understanding of private property and, in turn, a social transformation. The new class, which was between the public (reaya) and the state in the Ottoman financial system, became stronger during the 19th century and was positioned against the central elements.

The issue of financing the tax farming system also highlighted a different social group. Money changers gained significant importance in financing advance payments arising from tax farming contracts. They gave loans to the winners of the tax farming and manor auctions and organized the tax collection system by dividing a manor into sub-units. They specialized in financing trade and tax collection, especially in rural areas. The money changers, who made connections between countries and borrowed from the European markets to the central treasury when needed, formed the basis of the financial bourgeoisie class in Istanbul (Pamuk, 2007). Prospective tax collectors were expected to participate in the tenders held by the central treasury with the surety and commitment of money changers. The offers of those without such commitment were not accepted even if they offered high prices (N. Koyuncu, 2014).

Notables, whose social significance elevated after the 16th century, doubled their wealth and power not only through tax farming but also by leasing Miri lands (demesnes). In particular, lifelong leasing affairs made them privileged because of their influence on and cooperation with local authorities. From time to time, notables had conflicts of interest with each other. In line with the power struggles, they forced the government to grant them titles, such as vizier and pasha, to approach the authority of the Sultan, which allowed the rise of a robust, semi-feudal aristocracy in the Anatolian and Balkan provinces in the 18th and 19th centuries (İnalcık, 2019). This semi-feudal social group stood against any social innovation that might harm its entrenched interests (İnalcık, 2019).

Despite such an emergent issue, Anatolia remained only a geographical region hosting small farms. The existence of tax collectors, who owned lands from the 17th and 18th centuries and were known as the notables of their regions, could not change this picture (Faroqhi, 2010). The traditional structures of the social and economic sphere in the empire were maintained in the 17th and 18th centuries without any major differentiation. In a century-long period from the first years of the 19th century to the First World War, the state faced military, political, and economic powers of the West, which mandated the integration into a new Western-centered economic order (Pamuk, 2007). Fortunately, a series of changes in the 19th century enabled the balance of power to shift to the center.

On the other hand, tax collectors’ corruption within the tax farming system became a major complaint among peasants. The Tanzimat Fermanı (Imperial Edict of Reorganization) aimed to eliminate tax corruption and abolished the tax farming system. It was attempted to transfer tax revenues to the central treasury through the implementation of the state-based tax collection system (muhasıllık; Uzun, 2001). The edict adopted the principle of rearranging taxes and regular tax collection. In the edict, the tax farming system was interpreted as leaving the political and financial issues of the homeland to the will and conscience of a person. Henceforward, taxes would be collected according to the ability-to-pay principle, and no more would be demanded. It was recognized that a tax collector acting in favor of his own interests could be unfair and oppressive (Karal, 1975).

In the Tanzimat period, some opposition movements emerged due to the introduction of new taxes. Those who did not want to pay taxes attempted to rebel and plunder with partial support from the public. It is understood that mistaken attitudes and behaviors of those authorized to implement new decisions contributed to the initiation of such events (Çakır, 2001).

The abolition of tax farming created a significant loss of revenue and dissatisfaction among tax collectors and money changers. However, tax collecting costs immediately increased as tax officials employed a large number of people during the harvest periods. There were also losses in the conversion of in-kind taxes into cash. Such problems reduced the revenue expected by the state, which forced the state to restore the tax farming system in 1842 (Şener, 1990).

Before the First World War, tax revenues of the central treasury reached 11% of the annual total production and revenue (Pamuk, 2007). However, historians often draw a pessimistic picture regarding the production and trade activities in the Ottoman Empire during the 19th century. It is undeniable that the accepted customs regime and capitulations limited the economic field of action of the Ottoman administration. Although Ottoman trade and production adapted to the changing conditions for the sake of survival and European integration brought the increasing weight of foreign capital and an increase in production quality, the limited tax revenues could not be avoided (Faroqhi, 2010).

Methods

We utilized the document analysis technique in this study and obtained all relevant documents from the Ottoman Archives of the Prime Minister’s Office upon permission from the relevant bodies. The primary source of the study was the revenue accounting book belonging to Kocaeli province. The book issued tax farming revenues of the districts of Kocaeli in the years 1846 to 1847. Yet, the review of the archival records did not end up with any other documents issued other than these years. Thus, it was not possible to generate a time series on the data, which is the primary limitation to the study. Besides, budget statistics, allowing to address the composition of state revenues, were prepared in the fiscal years 1849 to 1850, 1862 to 1863, 1875 to 1876, and 1887 to 1888 (Güran, 2017). Thus, there was also a lack of data on tax revenues in the period we investigated. We also reviewed the documents related to the tax farming auctions in the same period to extend the main source. The documents of the auctions held by the Central Council (Majlis-i Val’a) for Aşar (tithe) cover helpful information on the procedures and rules of the tax farming system in the region. Overall, the relevant records may provide remarkable clues regarding accounting history and ample evidence for the sensitivity of the bureaucracy on taxation.

Accounting of Tax Farming Revenues From Kocaeli Province

It is well-known the eastern coast of the Sea of Marmara between Kocaeli and Istanbul increased its economic and social significance in the 18th and 19th centuries (see Map). Kocaeli was the province of primary importance in satisfying the basic food needs of the capital city. The reasons for the population density in the region during the specified period can be listed as follows: (1) Kocaeli was a region where the state could ensure life and property security at a higher level than other regions; (2) the state granted priorities in satisfying the basic needs of local citizens; (3) thanks to the importance of the region between Uskudar and Izmit for Istanbul, Kocaeli was always considered a zone of supplies, initiating the encouragement of its economic vitality; (4) the locals had high expectations of getting a share of prosperity as the surplus-value flowed to Kocaeli from Istanbul (Çelik, 2014). For further information, see Annex 1.

The establishment of a state-based tax collection system (muhassıllık) after the Tanzimat led to some changes to the administrative structure of Kocaeli province. In Kocaeli province, four tax collection offices were established. The first was responsible for taxes from the districts of Izmid, Kaymas, Şeyhler, Kandıra, Ağaçlı, and Gençler. The second was authorized to collect taxes from the districts of Hendek, Adapazarı, Akyazı, Karasu, Absafi, and Sarıçayır. Tax-related affairs of Karamürsel, Yalova, Pazarköy, and İznik were performed by the third office. Finally, the fourth was responsible for taxes from the districts of Geyve, Beşdivan, Akabad, and Gümüşabad.

Nevertheless, the expected benefit in tax collection could not be achieved; thus, the administrative structure was downsized in 1841. While the tax collection office responsible for Izmid was reauthorized outside the border, the districts of Kartal, Şile, Taşköprü, Beykoz, and Gebze were included in the administrative structure of Kocaeli province (Erken, 2016).

Public Tax Administration (Varidat-ı Umumiye) was affiliated with Finance Accounting Administration, established in 1840 to replace the Chief Accounting Administration. This state body supervised tax records and collections in the districts and audited the accounts by fiscal years (Pakalın, 1977).

Revenue Accounting Department (functioning under Public Tax Administration) was divided into Anatolian and Rumelian revenue accounting offices. Anatolian accounting office covered the regions of Arabia, Anatolia, Crete, and Tripoli. Rumelian accounting office regulated the accounts of Rumelia, Istanbul, and the Mediterranean islands (Güran, 1989).

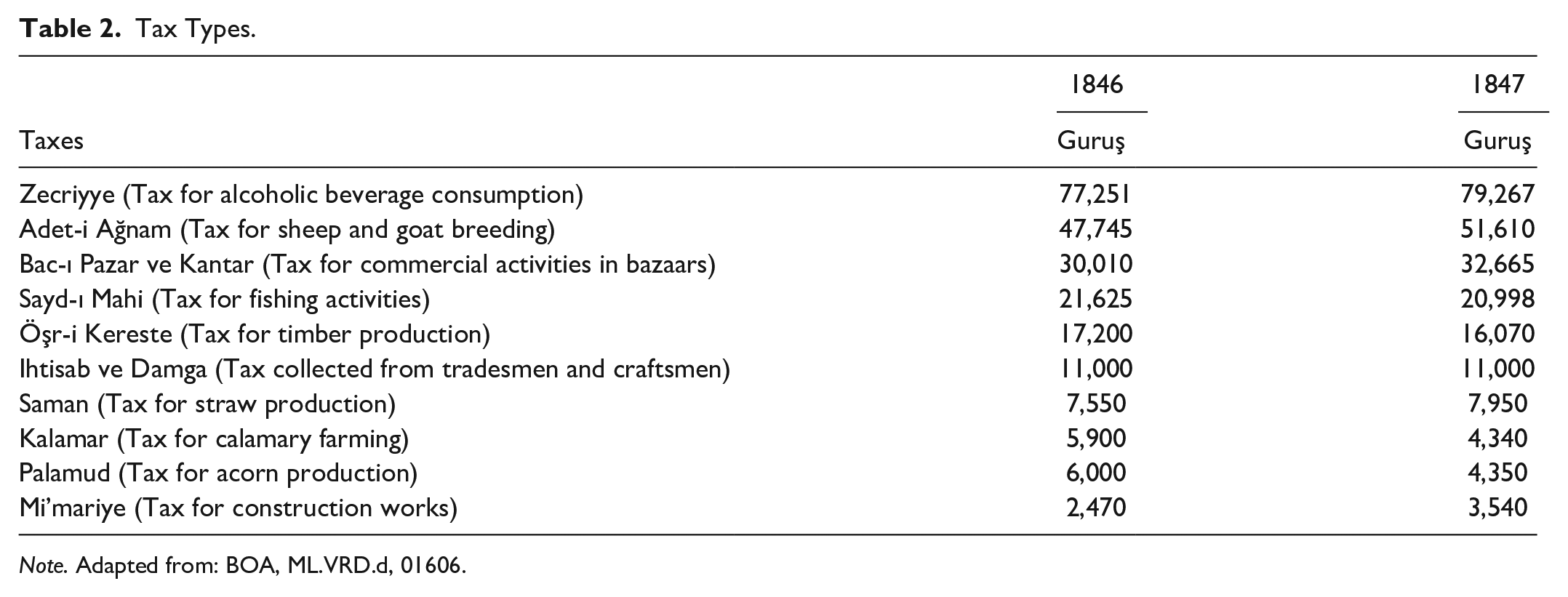

The revenue accounting book issued on December 29, 1847 arranged taxes to be paid by the tax collectors. Following the accounting of tax revenues collected in 1846, the reduced tax revenue in 1847 was deducted from the taxes as the missing amount. Then, the increased amount was added to the total tax amount, and the revenue paid by the tax collectors was recorded. There were also districts where the tax amount did not change during a 1-year period. Taxes were reduced in the districts of Karasu, Bazargölü, Kartal, and Şeyhlü. In other districts, taxes were increased compared to the previous year.

The tax farming price of Izmid district was 61,000 Guruş. Its share in the total tax farming price was 25%; this amount was not included in the accounting account but only shown in the abstract section. Following Izmid district, the highest tax farming price belonged to Bazargölü district (48,170 Guruş), where there were seven tax collectors. Tax collector Ahmet Efendi paid 27,500 tax farming price with an annual increase of 8% in Yalakabad district, while tax collector Koloç Oğlu undertook 23,550 Guruş tax farming price with a yearly increase of 5% in Adapazarı district. The lowest tax farming prices belonged to the districts of Hendek and Başdivan with 200 and 250 Guruş, respectively, which included only the Adet-i Ağnam as in Table 1 (See Annex 2).

Revenue Records of Revenue Accounting Department in Kocaeli Province.

| Districts | 1846 | 1847 | Total | |

|---|---|---|---|---|

| Guruş | Missing | Increase | Guruş | |

| Karasu (Hasan Efendi) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 1,320 | 90 | 1,230 | |

| Rüsum-ı Öşr-i Kereste (Tax for timber production) | 5,000 | 130 | 4,870 | |

| Rüsum-ı Kalamar (Tax for calamary farming) | 5,900 | 1,560 | 4,340 | |

| Grand total | 12,220 | 1,720 a | 10,500 | |

| Adapazarı (Koloç Oğlu) | ||||

| Rüsum-ı Öşr-i Kereste (Tax for timber production) | 4,100 | 4,100 | ||

| Rüsum-ı Kantar (Weighage tax) | 6,250 | 555 | 6,805 | |

| Rüsum-ı Saçma (Tax for fishing net production) | 775 | 775 | ||

| Rüsum-ı Sayd-ı Mahi (Tax for fishing activities) | 2,550 | 2,550 | ||

| Rüsum-ı Tahmil-i Saman (Tax for straw production) | 5,500 | 250 | 5,750 | |

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 2,350 | 350 | 2,700 | |

| Rüsum-ı Mi’Mârîye (Tax for construction works) | 560 | 560 | ||

| Rüsum-ı Boyahane (Tax for dye production) | 310 | 310 | ||

| Grand total | 22,395 | 1,155 | 23,550 | |

| Hendek (Hasan Ağa) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 150 | 50 | 200 | |

| Taraklı (El-Hâc Hüseyin Ağa) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 1,700 | 400 | 2,100 | |

| Rüsum-ı Tahmil-i Saman (Tax for straw production) | 1,300 | 1,300 | ||

| Rüsum-ı Ihtisab ve Damga (Salim Efendi) (Tax Collected from Tradesmen and Craftsmen)

|

11,000 | |||

| Sub-total | 3,000 | |||

| Increase | 400 | |||

| Sub-total | 3,400 | |||

| Ihtisab fee | 11,000 | |||

| Grand total | 14,400 | |||

| Todurga (Salim Efendi) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 620 | 620 | ||

| Geyve (Hasan Ağa) | ||||

| Rüsum-ı Bac-ı Pazar ve Kantar (Tax for commercial activities in bazaars) | 13,500 | 550 | 14,050 | |

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 2,100 | 150 | 2,250 | |

| Rüsum-ı Zecriyye (Tax for alcoholic beverage consumption) | 1,400 | 100 | 1,500 | |

| Rüsum-ı Mi’Mârîye (Tax for construction works) | 250 | 50 | 300 | |

| Rüsum-ı Saman (Tax for straw production) | 750 | 150 | 900 | |

| Rüsum-ı Boyahane (Tax for dye production) | 50 | 50 | ||

| Grand total | 18,050 | 950 | 19,000 | |

| Akhisar (Mustafa Beğ) b | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 1,200 | 300 | 1,500 | |

| Rüsum-ı Zecriyye (Tax for alcoholic beverage consumption) | 2,500 | 2,500 | ||

| Rüsum-ı Bac-ı Pazar ve Kantar (Tax for commercial activities in bazaars) | 6,360 | 6,360 | ||

| Rüsum-ı Mi’Mârîye (Tax for construction works) | 280 | 280 | ||

| Rüsum-ı Boyahane (Tax for dye production) | 225 | 225 | ||

| Rüsum-ı Saçma (Tax for fishing net production) | 40 | 40 | ||

| Rüsum-ı Bağ (Tax for grape production) | 100 | 100 | ||

| Grand total | 10,700 | 300 | 11,000 | |

| Bazargölü | ||||

| Rüsum-ı Sayd-ı Mahi Bazargölü (Salih Ağa) (Tax for fishing activities) | 7,200 | 800 | 8,000 | |

| Rüsum-ı Sayd-ı Mahi Yeniköy (Halil Beğ) (Tax for fishing activities) | 2,250 | 750 | 1,500 | |

| Rüsum-ı Sayd-ı Mahi Örekli (Halil Beğ) (Tax for fishing activities) | 500 | 200 | 300 | |

| Rüsum-ı Sayd-ı Mahi Çakırlı (Halil Beğ) (Tax for fishing activities) | 200 | 200 | ||

| Rüsum-ı Sayd-ı Mahi Kiremit (Halil Beğ) (Tax for fishing activities) | 2,600 | 600 | 2,000 | |

| Rüsum-ı Adet-i Ağnam (Hacı Ali Ağa) (Tax for sheep and goat breeding) | 2,200 | 200 | 2,000 | |

| Rüsum-ı Bac-ı Pazar (Pehlivanzade Ahmet Ağa) (Tax for commercial activities in bazaars) | 3,050 | 1,000 | 4,050 | |

| Rüsum-ı Mi’Mârîye (İbrahim Ağa) (Tax for construction works) | 1,200 | 900 | 2,100 | |

| Rüsum-ı Zecriyye (Ahmet Efendi) (Tax for alcoholic beverage consumption) | 25,700 | 700 | 26,500 | |

| Rüsum-ı Kantar (Mustafa Ağa) (Weighage tax) | 1,000 | 520 | 1,520 | |

| Sub-total | 44,900 | |||

| Discount | 1,750 | |||

| Sub-total | 43,150 | |||

| Increase | 3,500 | |||

| Sub-total | 46,550 | |||

| Created Rüsum-ı Kantar (Weighage tax) | 1,520 | |||

| Grand total | 48,170 | |||

|

|

||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 7,200 | 7,200 | ||

| Rüsum-ı Otlak (Subaşı ve Seymenler) (Grazing tax) | 1,500 | 800 | 2,300 | |

| Rüsum-ı Kantar (Katırlı İskelesi) (Weighage tax) | 500 | 300 | 800 | |

| Rüsum-ı Kantar (Orta İskelesi) (Weighage tax) | 350 | 250 | 600 | |

| Rüsum-ı İskele (Koru İslelesi) (Tax for pier operations) | 500 | 100 | 600 | |

| Rüsum-ı Zecriyye ) (Tax for alcoholic beverage consumption) | 15,411 | 589 | 16,000 | |

| Grand total | 25,461 | 2,039 | 27,500 | |

| Karamürsel | ||||

| Rüsum-ı Adet-i Ağnam (El-Hâc Emin Beğ) (Tax for sheep and goat breeding) | 3,125 | 375 | 3,500 | |

| Rüsum-ı Zecriyye (Müdür-ü Kaza-i Mustafa Beğ) (Tax for alcoholic beverage consumption) | 9,100 | 9,100 | ||

| Grand total | 12,225 | 375 | 12,600 | |

| Kartal | ||||

| Rüsum-ı Adet-i Ağnam (Abdülfettah Ağa) (Tax for sheep and goat breeding) | 2,100 | 50 | 2,150 | |

| Rüsum-ı Zecriyye (Kurtiş Çorbacı) (Tax for alcoholic beverage consumption) | 13,125 | 27 | 13,152 | |

| Rüsum-ı Sayd-ı Mahi (Pazarlu Çorbacı) (Tax for fishing activities) | 5,500 | 5,500 | ||

| Rüsum-ı Dellaliye (Abdülfettah Ağa) (Tax for brokerage activities) | 330 | 30 | 300 | |

| Grand total | 21,055 | 30 | 77 | 21,102 |

| Beykoz (Ahmed Efendi Sâkin-i Izmid) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 4,710 | 4,710 | ||

| Rüsum-ı Zecriyye (Kasaba-i Paşabahçe) (Tax for alcoholic beverage consumption) | 2,200 | 2,200 | ||

| Rüsum-ı Zecriyye (Karye-i Arnabud) (Tax for alcoholic beverage consumption) | 2,350 | 2,350 | ||

| Rüsum-ı Zecriyye (Karye-i Paşa) (Tax for alcoholic beverage consumption) | 265 | 265 | ||

| Rüsum-ı Sıvı Reçine (Tax for liquid resin production) | 200 | 200 | ||

| Grand total | 9,725 | 9,725 | ||

| Şile | ||||

| Rüsum-ı Adet-i Ağnam (Hacı Osman Ağa) (Tax for sheep and goat breeding) | 2,550 | 450 | 3,000 | |

| Rüsum-ı Zecriyye (Ahmed Efendi) (Tax for alcoholic beverage consumption) | 3,800 | 200 | 4,000 | |

| Grand total | 6,350 | 650 | 7,000 | |

| Taşköprü | ||||

| Rüsum-ı Adet-i Ağnam (Ali Ağa) (Tax for sheep and goat breeding) | 5,350 | 1,150 | 6,500 | |

| Rüsum-ı İskele-i Kütük (İbrahim Reis) (Log Pier tax) | 3,550 | 200 | 3,750 | |

| Grand total | 8,900 | 1,350 | 10,250 | |

| Akabad | ||||

| Rüsum-ı Adet-i Ağnam (Mehmed Ağa) (Tax for sheep and goat breeding) | 1,020 | 80 | 1,100 | |

| Beşdivan | ||||

| Rüsum-ı Adet-i Ağnam (Süleyman Efendi) (Tax for sheep and goat breeding)

|

250 | 250 | ||

| Ağaçlı | ||||

| Rüsum-ı Adet-i Ağnam (El-Hac Emin Beğ) (Tax for sheep and goat breeding) | 2,100 | 400 | 2,500 | |

| Kaymas (El-Hâc Hüseyin Efendi) | ||||

| Rüsum-ı Zecriyye (Tax for alcoholic beverage consumption) | 1,200 | 300 | 1,500 | |

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 3,000 | 200 | 3,200 | |

| Rüsum-ı Mi’Mârîye (Tax for construction works) | 180 | 120 | 300 | |

| Rüsum-ı Harc-ı Mevasîk (Tax for contracts) | 30 | 20 | 50 | |

| Rüsum-ı Sayd-ı Mahi (Gökçeviran Gölü) (Tax for fishing activities) | 825 | 123 | 948 | |

| Grand total | 5,237 | 763 | 6,000 | |

| Kandıra (Sami Beğ) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 2,000 | 100 | 2,100 | |

| Şeyhlü (Hasan Efendi) | ||||

| Rüsum-ı Adet-i Ağnam (Tax for sheep and goat breeding) | 3,050 | 3,050 | ||

| Rüsum-ı Öşr-i Kereste (Sakarya Nehri) (Tax for timber production) | 5,400 | 750 | 4,650 | |

| Rüsum-ı Öşr-i Kereste (İskele-i Kevken) (Tax for timber production) | 2,700 | 250 | 2,450 | |

| Rüsum-ı Palamud (Nehr-i Sakarya) (Tax for acorn production) | 6,000 | 1,650 | 4,350 | |

| Grand total | 17,150 | 2,650 | 14,500 | |