Abstract

The study examines the relationship between doing business factors and tax evasion in Asian countries. To this end, Ordinary Least Square (OLS), along with a fixed and random effect model, was used to analyze the 5-year data (2011–2015) of 35 Asian countries obtained from the global competitiveness report and World Development Indicators. The findings indicated that a high level of corruption, a high tax rate, limited access to finance, strict tax regulation, government instability, and poor ethics promote tax evasion. Extending the socio-economic theory, the findings of the study provide the tax administration and governments of Asian countries with insights into the mechanism by which certain business factors influence tax evasion. Moreover, the study offers some valuable guidelines for formulating suitable economic policies that engender a reduction in tax evasion.

Keywords

Introduction

Tax evasion provokes financial instability in almost all developed and developing countries (Epaphra, 2015; Yamen et al., 2018) and is said to occur when taxpayers intentionally fail to file tax returns, misreport income, overstate expenses, or pay less than the actual tax amount (Rashid, 2020). In addition, tax evasion is the deliberate use of illicit means by taxpayers to avoid paying their legal taxes (Alm, 2019; Alm et al., 2019; Rashid, 2020; Rashid & Morshed, 2021). Most theoretical and empirical work on tax evasion has focused on individual income tax. Individuals can reduce income taxes liability by underreporting income, failing to file applicable tax returns, or placing items in barter to forgo taxes (Alm, 2019; Alm et al., 2019; Rashid & Ahmad, 2020). Over the decades, tax evasion has been a debatable issue among policymakers, thus requiring effective solutions to tackle the burgeoning economic threat. The taxpayers’ decisions to evade tax highly depend on how they perceive the business environment within which the individuals and firms operate their businesses. They comply with tax obligations properly only if they find the business environment favorable across the national boundary (Reynolds, 1980). According to Arruñada (2007), commerce allows the development of the relationship between a government and business organizations. It facilitates the establishment of a business by simplifying its formal rules and regulations. Doing business focuses on the rules imposed on small and medium-sized domestic companies in each country (Doing Business, 2016). While developing nations, including those in Asia, are working to improve their tax systems and combat tax evasion, the stakes are higher in these countries because they cannot afford to build hospitals and schools, pay for social security systems needed as the population ages, or pay for basic infrastructure without higher tax revenues. It also involves developing a tax system that supports inclusion, good governance, investments, job development, and social justice while aligning with society’s beliefs on lowering inequality (Rashid et al., 2022).

The rationale behind the investigation of tax evasion from the perspective of Asian countries is the December 2015 report of Global Financial Integrity (Miyaki, 2016), which asserted that despite being the fastest growing economy region-wise,

“Asian developing nations accounted for 38.8% of the estimated $7.8 trillion that developing countries lost due to illicit financial outflows in 2004-2013, and as a whole region, Asia’s ratio of national tax revenue to GDP is among the lowest in the world–about half of that in Europe and lower than in Africa and Latin America.”

Moreover, as per the critical indicators for Asia and the Pacific 2017, the worldwide Gross Domestic Product (GDP) based on Purchasing Power Parity (PPP) has risen to 40.9% from 29.4% in 2000 (Araki & Nakabayashi, 2018). Meanwhile, the size of the economy in the South Asian region has increased to around 7% of global GDP (PPP), which is nearly twice the amount recorded in 1980 (Bhattarai, 2016). Despite the region’s financial prosperity, the statistics indicated that approximately 330 million individuals still earn less than $1.90 a day in Asia and the Pacific (PPP in 2011) region. It accounted for roughly 9% of the region’s total population living below the poverty line, and three-quarters of the region’s countries had a fiscal deficit in 2016 (World Bank, 2019a). Regarding the tax-to-GDP ratio, the Asia Pacific economy remains considerably smaller than that of member nations of the Organization for Economic Co-operation and Development (OECD) (Araki & Nakabayashi, 2018). Moreover, tax evasion causes underinvestment in the private sector and a low rate of private consumption (World Bank, 2019b). As a result, the expected level of growth in this region remains uncertain. Also, tax evasion incites domestic vulnerabilities, which could be heightened by huge fiscal deficits, a high level of inflation, scarcity of foods and other necessities, political uncertainty, and weak structural financial and non-financial institutions. In addition, Asia’s economy is also marked by a high level of corruption, bad governance, a high inflation rate, and a huge tax burden (Islam et al., 2020). In the emerging economies of Asia, the large informal sector, weak economic base, and inept tax administration have led to a traditionally lower percentage of GDP subject to tax (World Bank, 2019a), which in turn limits the capacity of the government to fund infrastructural and social growth.

In Asian countries, research on tax evasion is still limited, creating a significant gap in the existing literature. To the best of our knowledge, no study to date has investigated the impact of doing business factors on tax evasion. Consequently, it motivates to examine whether the factors of business dealings influence taxpayers to evade tax in Asian countries. Specifically, the study investigates the impact of doing business factors such as inflation, tax rate, access to finance, corruption, crime, poor work ethic, policy instability, government instability, government rules and regulations, foreign currency regulations, etc., on tax evasion.

The study will contribute to the existing literature in the following ways. First, it estimates the extent to which challenges in business activities in Asian countries influence tax evasion. Second, the study provides a new avenue for researchers and academics to explore the relationship between business dealings and tax evasion, in line with the socio-economic theory. Finally, this study is expected to provide tax authorities and governments of the respective countries with insights on business factors promoting tax evasion, thus enabling them to develop proper strategies to significantly reduce the level of tax evasion.

Literature Review and Hypotheses Development

Among many theories in relation to tax evasion, the psychological contract theory is viewed as crucial in understanding the relationship between taxpayers and the government, where taxpayers reciprocate government services by contributing to government revenue (Pickhardt & Prinz, 2014). Feld and Frey (2007) developed the concept of a psychological tax contract to establish a fair and reciprocal obligation between the government and taxpayers, where one party grants favor to another in exchange for something—a quid pro quo situation. Based on this theory, taxpayers feel discouraged about paying taxes if they perceive poor government institutional quality (Rashid et al., 2022). However, this theory considers only an aspect (individual norm) of tax evasion, neglecting other elements (economic freedom and institutional norm).

Considering the limitations of the existing theories of tax evasion, Nurunnabi (2018) proposes the socio-economic theory, explaining tax evasion practices based on “institutional infrastructure” (Pickhardt & Prinz, 2014) presented in Figure 1. He considered tax evasion to be a complex process involving multiple factors, including institutions, entities, individuals, and tax-paying behavior. The theory classifies both the economic and non-economic factors of tax evasion into three broad categories: taxpayers’ behavior, state structure, and the behavior of the tax authorities. In this circular model of tax evasion, the state sits at the top of the model. As a major player, the state acts as a legislator in providing a suitable environment for both taxpayers and the tax authority. The state’s role is to provide different types of freedom to the taxpayers: government tax regulation, labor regulation, as well as business, monetary, and fiscal freedom. The tax authority is the central body that collects the tax; its objective is to provide good administration (good governance) in taxation. Finally, individuals’ tax-paying behavior will be determined by their interaction with the state and tax authorities and their culture and ethical beliefs (Rashid et al., 2021). Therefore, successful tax planning must go beyond the narrow measures of the government to provide laws and benefits to the taxpayers, and it also includes the interactive force of all three parties involved.

The socio-economic theoretical model of tax evasion (Nurunnabi, 2018).

Moreover, the theory implies that people do not behave in the same way as the public policies—laws, economic and social actions of the government, funding priorities, and legislation representing the given positions, beliefs, cultural values, or accepted rules—are obligated by the state (Bishop, 2009). Mason et al. (2020) claimed that firms’ compliance with tax laws is reduced when they perceive an unfavorable impact from their government or an unfair policymaking process. Androniceanu et al. (2019) found an interdependence between tax evasion and government policies and identified the degree of economic, social, and cultural development as the major determinants of tax evasion. Besides, if taxpayers perceive restrictions in doing business due to high tax rates, complex rules and regulations, and poor governance qualities, they might feel unsupported and consequently express disregard for government rules and regulations, including tax obligations. Hence, it is necessary to identify which factors discourage entrepreneurs from paying taxes to their government. To this end, this study considers the socio-economic theoretical model of tax evasion as the basis for developing the hypotheses.

Prior studies have investigated many factors that demotivate taxpayers from paying taxes (Abdixhiku et al., 2018; Alm, 2019; Alm et al., 2019; Epaphra, 2015; Nurunnabi, 2018; Rashid et al., 2021) and have identified either economic or non-economic factors of tax evasion (Alm et al., 2019; Epaphra, 2015; Nurunnabi, 2018). Some scholars consider corruption and crime as the major determinants of tax evasion (Alm et al., 2016). They commented that corruption could lead to tax evasion by underreporting taxes, which is only possible when an illegal contract exists between taxpayers and tax officials. Similarly, McGillivray (2019) presented a high correlation between financial crime and tax evasion faced by the present world. Riahi-Belkaoui (2004) and Abdixhiku et al. (2018) conducted a cross-country investigation on the impact of the barriers to business, market structure, and economic freedom on tax evasion and identified crime as a major determinant. The tax rate also plays an influential role in tax evasion (Epaphra, 2015). A high corporate tax rate was observed to promote firm tax evasion (Do & White, 2018), while others documented inflation as a crucial factor in tax evasion (Abdixhiku et al., 2018; Cerqueti & Coppier, 2011; Gupta & Ziramba, 2010). Also, the complexity of tax regulation was found to impede taxpayers’ compliance with tax rules, thus raising their chances of tax evasion (Feld & Frey, 2007; Rashid, 2020). Generally, prior researchers have found a significant effect of corruption, crime, tax rates, tax regulation inflation, access to financing, government instability, etc., on tax evasion in their separate studies.

Social Norms and Tax Evasion

Social norms indicate cultural values and ethics, including corruption, crime and theft, and poor work ethics. As per the socio-economic theory, a significant relationship exists between social norms and tax evasion (Nurunnabi, 2018).

Corruption

Corruption and tax evasion are the most common forms of illegal behavior; these exercises have both harmful economic and social externalities. Many researchers, including Dimant and Tosato (2018), have found a significant positive relationship between corruption and tax evasion. Corruption enables tax evasion by facilitating taxpayers’ concealment of their income, while tax evasion promotes corruption by creating additional opportunities for corruption to thrive (Alm et al., 2016). In other words, an increase in corruption leads to a rise in tax evasion. To avoid tax liability, taxpayers offer bribery to the tax officer, and, depending on their mutual agreement, taxpayers underreport their taxable income. Political connections are positively amalgamated with tax evasion, and this interconnection becomes stronger in highly corrupted countries (Khlif & Amara, 2019). Rashid (2020) found a significant positive relationship between corruption and tax evasion. Therefore, the study posits the following hypothesis:

Crime and theft

According to the study by McGillivray (2019), the world is facing a great problem of financial crime, including tax evasion. His study also found that tax evasion increases proportionally with financial crime. Conducting a cross-country investigation, Riahi-Belkaoui (2004) found that the country with more economic freedom, a developed equity market, effective competition laws, and a short series of crimes faces the lowest tax evasion problem. Richardson (2006) identified income sources as another influential factor in tax evasion, highlighting that people who earn legally are more likely to pay tax than those with questionable income. Both Richardson (2006) and Riahi-Belkaoui (2004) found a positive relationship between crime and theft, and tax evasion. Hence, we propose the following hypothesis:

Poor Work Ethics

Ethics is a concerning issue in the case of tax evasion, as many previous studies have shown that only 1% of taxpayers pay their taxes voluntarily (Alm et al., 2012). When the labor force is unethical, they try to work as little as possible and embezzle cash, goods, and products, reducing the firms’ productivity. Consequently, firms are demotivated from paying their tax. Previous studies have found a negative relationship between poor ethical behavior and tax evasion, which indicates that tax evasion increases with the decline of staff ethics (Alm et al., 2012; Drogalas et al., 2018; McGee et al., 2011). Therefore, the study assumes that poor work ethics increases the level of tax evasion positively and summarizes the hypothesis as follows:

Regulations and Enforcement and Tax Evasion

As per the socio-economic theory, there is a significant relationship between enforcement and tax evasion (Islam et al., 2020). Therefore, this study attempts to develop hypotheses on the effects of government tax regulations, restrictive labor regulations, and monetary, fiscal, and business freedom on tax evasion.

Government tax regulation

Many researchers mentioned that tax compliance is based on the psychological contract between taxpayers and tax authorities (Feld & Frey, 2007; Umar et al., 2017). They suggested that for a contract to be supported, incentives such as rewards or punishments need to be provided (Feld & Frey, 2007). Besides, tax rules and regulations should be rational and motivated and should not be too rigid. On the other hand, it should not be too loose to allow taxpayers to evade tax (Feld & Frey, 2007). According to Kirchler et al. (2008), a lack of audits and fines may inspire taxpayers to evade more taxes when they perceive that monitoring by regulatory bodies is insufficient to get them accused of tax evasion. Tax officers who think that the crowding-out effect will be stronger with a high level of tax-paying mentality should focus less on incentives and treat taxpayers more respectfully (Feld & Frey, 2007). The relationship between taxpayers and tax authorities can be considered an implicit or relational contract (Akerlof, 1982). Akerlof (1982) and Feld and Frey (2007) found a negative relationship between tax regulation and tax evasion up to a certain level, after which the relationship turns positive. Rashid et al. (2022) stated that people comply with tax rules and regulations only when they perceive that their government is efficient and ensures their rights. Prior research documented a positive relationship between the higher level of enforcement and tax evasion (Feld & Frey, 2007; Richardson, 2006). Taxpayers feel discouraged from paying taxes if the government tax regulations are complex to understand and tight. Hence, evidence from prior studies on the relationship between tax regulations and tax evasion indicates that a lack of inferior and stringent tax rules and regulations increases tax evasion.

Restrictive labor regulation

Restrictive labor regulations refer to rules and regulations enforced by the government of a country concerning the recruitment of employees in a company. Sometimes, firms appoint children or women for some activities, which may not be permitted due to the country’s restrictions on employees’ age, gender, nationality, etc. However, labor regulation increases the cost of firms significantly. For example, Amirapu and Gechter (2020) estimated that such regulation increases firms’ costs by 35%, affecting tax evasion positively. Furthermore, Neck et al. (2012) found an ambiguous effect of labor supply on tax evasion due to the wage rate effect. Therefore, this study supposes a positive effect of restrictive labor regulation on tax evasion.

Inflation (monetary freedom)

Inflation, also known as monetary freedom, positively increases tax evasion (Abdixhiku et al., 2018; Nurunnabi, 2018). In addition to fiscal policy, penalty rates, probability of being detected, and degree of corruption, inflation influences the degree of tax evasion (Cerqueti & Coppier, 2011). Notably, they discovered a positive relationship between inflation and tax evasion. Two conflicting parties summarize opinions on the influence of inflation on tax evasion. Some scholars argue that inflation positively affects tax evasion, as the decision to evade tax can be affected by the attempt of taxpayers to restore their purchasing power (Fishburn, 1981). Other scholars argued that taxpayers delay tax payments till future periods of high inflation, creating an overall negative relationship between inflation and tax evasion (Tanzi, 1980). The present study posits a positive relationship between inflation and tax evasion.

Tax rate (Fiscal Freedom)

Based on data from the United Republic of Tanzania, the Republic of South Africa, and China, Epaphra (2015) found a positive relationship between tax rate and tax evasion. Similarly, while conducting a study in Muslim countries, Nurunnabi (2018) observed a positive effect of fiscal freedom on tax evasion. It is argued that if the state increases the tax rate, taxpayers underreport their income and underprice their products during imports and exports to evade tax duty (Levin & Widell, 2014). Moreover, Mahangila and Anderson (2017) documented that the tax burden enhances tax evasion significantly. Another study by Mpango (1996) stated that the spread of voluntary under-invoicing of imports is about 20% inaugurated by high scheduled tariff rates, exchange rate adjustments, low salaries, and minimum incentives offered to the customs staff. Alm (2019) documented that people negatively respond to a higher tax rate.

Constrained access to finance (Business freedom)

A country with high financial constraints exhibits a higher level of tax evasion. By evading tax, firms can augment their funding insufficiency created by financial constraints. Alm et al. (2019) argued that there is a strong positive relationship between financial constraints and tax evasion. Firms with a severe financial crisis are more likely to avoid tax payments for two main reasons. First, financial constraints hinder firms from getting full access to external finance, thereby instigating them to hold onto their internal funds (Rashid & Morshed, 2021). In perfect capital markets, there is a difference between internal and external funds in financing investment and other activities. Second, financial constraints a firm faces are, to a large extent, reflective of underdeveloped financial markets to the economy, which creates incentives for the firm to operate in the informal rather than the formal and legal sectors. In an economy with underdeveloped financial markets, a firm may defraud tax liability and other official rules by operating in the informal sector. Based on the aforementioned discussion of prior studies, this study advances the following hypothesis.

Public Sector Governance and Tax Evasion

Islam et al. (2020) documented that the higher the quality of a country’s public sector governance (institutional quality), the lower the occurrence of tax evasion. On the other hand, if citizens perceive the poor quality of government services, they tend to evade more taxes (Yamen et al., 2018). Therefore, the study would like to examine the impact of policy instability, government instability, and insufficient bureaucracy on tax evasion.

Policy instability, government instability, and government insufficient bureaucracy

According to previous studies, developing countries are generally unable to generate an adequate amount of tax revenue from taxation due to various institutional problems, including administrative corruption (Ajaz & Ahmad, 2010). As per the prior literature, there are two important components of revenue generation: tax administration and tax system reforms (Brondolo et al., 2008). However, increasing the efficiency of tax administration is the core objective, which is possible by reducing corruption and tax evasion. Government instability in a country refers to its political instability and is considered a significant threat to the generation of tax revenue. Unstable governments and the resulting frequent policy changes result in constant changes in the tax structure and system, which raises the chances of tax evasion. Bureaucracy is another important issue affecting tax evasion. Like Picur and Riahi-Belkaoui (2006), some scholars demonstrated that strong bureaucracy could reduce tax evasion. They further explained that poor bureaucracy could be associated with bureaucratic corruption, which makes the government inefficient and ultimately increases tax evasion. Therefore, this study posits the positive effects of policy instability, government instability, and insufficient bureaucracy on tax evasion.

Research Design and Methodology

Sample Size and Data Sources

For this study, we have utilized a sample size of 175 observations from 35 Asian countries, covering a period of 5 years from 2011 to 2015. Although there are almost 48 countries in Asia, a list of 35 Asian countries (presented in Appendix A) was selected based on the availability of data. We have used the shadow economy data as a proxy for tax evasion, which is available only up to 2015 (Medina & Schneider, 2018). The factors affecting business activities have been extracted from “The Global Competitiveness Report” surveyed by the World Economic Forum (WEF). The WEF’s Executive Opinion Survey estimates a score for each of the doing business factors by asking the respondents to select the five most critical factors hindering business activities in their country and rank them between 1 (most problematic) and 5 (less problematic) (World Economic Forum, 2016). The score corresponds to the responses weighted according to their rankings. Other data, including GDP, inflation, and tax rate, were collected from the World Bank Indicators.

Variables Measurement

As there is no perfect measure of tax evasion and it is not possible to capture tax evasion data directly, this study used the shadow economy as a proxy of tax evasion for the dependent variable, in line with the prior studies (Islam et al., 2020; Rashid et al., 2022; Schneider, 2012, 2022; Yamen et al., 2018). The shadow economy is also referred to as the hidden economy, cash economy, informal economy, black economy, gray economy, and lack economy. As agents involved in the shadow economy activities to avoid detection, it is, by its nature, very difficult to measure the shadow economy. The relevance of the shadow economy for politics and the economy drives the demand for information and changes over time. Additionally, the formulation of economic policies that react to changes in the economy over time and across space must take into account all aspects of economic activity, including official and unofficial production of goods and services. The magnitude of the shadow economy is also a crucial factor in determining how much tax evasion is occurring and, consequently, how much should be controlled.

Therefore, Medina and Schneider (2018) justified the use of the shadow economy as a proxy for tax evasion as follows.

“The shadow economy includes all economic activities which are hidden from official authorities for monetary, regulatory, and institutional reasons. Monetary reasons include avoiding paying taxes and all social security contributions; regulatory reasons include avoiding governmental bureaucracy or the burden of the regulatory framework; while institutional reasons include corruption law, the quality of political institutions, and the weak rule of law.”

Medina and Schneider (2018) described the shadow economy as economic operations and income that evade government regulations, taxation, or scrutiny. More specifically, the shadow economy covers all legal transactions involving money and non-money, which includes all productive economic activity that would typically be subject to taxation if they were disclosed to the state’s (tax) authorities. These actions are purposefully kept hidden from public authorities in order to avoid paying income taxes, value added taxes, other taxes, social security contributions, or to avoid adhering to specific legal labor market requirements like minimum wages, maximum working hours, safety standards, and administrative procedures. The shadow economy thus focuses on productive economic activities that would typically be recorded in national accounts but are instead carried out clandestinely as a result of tax or regulatory burdens.

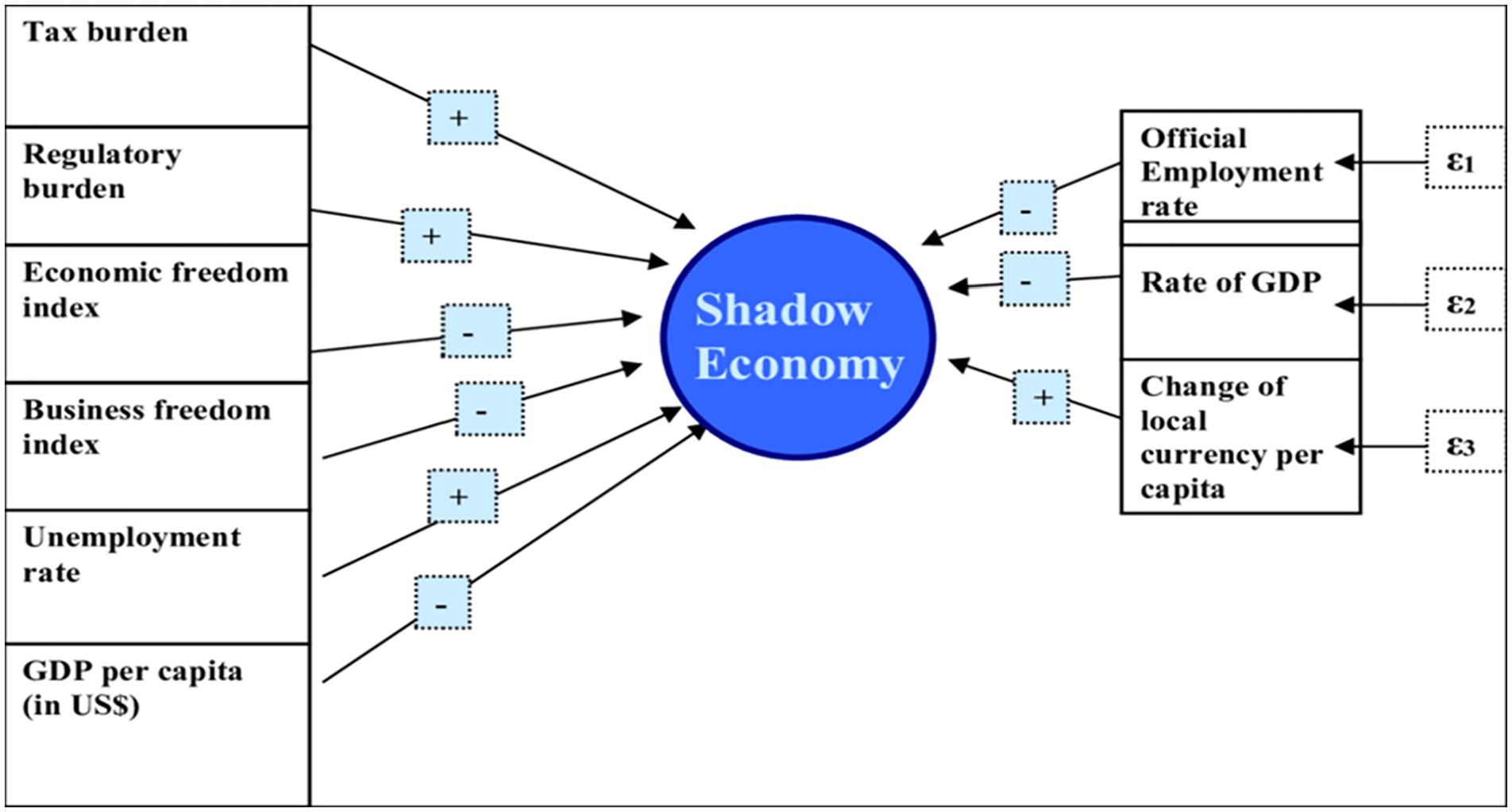

This research considers the macroeconomic measure of the shadow economy based on the MIMIC model (Multiple Causes Multiple Indicators) (Schneider & Buehn, 2012). The MIMIC approach is based on the idea that while the size of the shadow economy is not directly observed, it is possible to estimate it using quantitatively measurable factors that reflect the shadow economy (Schneider, 2022). Schneider et al. (2010) take into account various factors for the MIMIC model, such as tax burden, regulatory burden, economic freedom index, business freedom index, unemployment rate, and GDP per capita, shown in Figure 2, all of which directly affect the dimensions of the shadow economy over time.

MIMIC estimation procedure (adapted from Schneider et al., 2010).

This study has included the most problematic factors affecting businesses, like corruption, crime and theft, access to financing, tax rate, tax regulation, inflation, poor work ethics, policy instability, government instability, restrictive labor regulation, and inefficient government bureaucracy as independent variables. As per the socio-economic theory, we categorized those variables under three groups: culture and ethics, regulations and economic freedom, and public sector governance. Moreover, it is essential to include some variables in a panel study to control the social and economic differences between the countries. Therefore, this study has considered GDP per capita, foreign currency regulation, an inadequately educated workforce, and insufficient innovation capacity as control variables. The measurement of the variables is set out in Appendix B.

Data Estimation Method and Model

Since the study contains both economic and non-economic variables, the data is static (Islam et al., 2020). Under the static model, three alternative linear estimation techniques are available to handle panel data (Asteriou & Hall, 2007): (a) the pooled OLS method, (b) the fixed-effect model, and (c) the random effect model.

First, we used the pooled Ordinary Least Square (OLS) method as a standard constant technique. Under OLS, the prevalent assumption is that there is no variability between cross-sectional units; more specifically, all cross-sectional units are considered a single unit. On the other hand, the Fixed-Effect Model (FEM) introduces heterogeneity among cross-sections via the constant regression function. This approach provides a separate intercept for each cross-section, called a one-way fixed-effect, as it can capture only time-invariant features within the individual cross-section. However, this FEM has several limitations. For instance, because FEM needs to include too many dummy variables in the model, it reduces the degree of freedom and causes the multicollinearity problem in the regression function. The Random Effect Model (REM) considers the constants of the regression function for each cross country, as random parameters are not fixed. Therefore, the REM addresses a cross-sectional effect to a greater extent, as it assumes the differences across the country as random and uncorrelated with other dependent variables in the model.

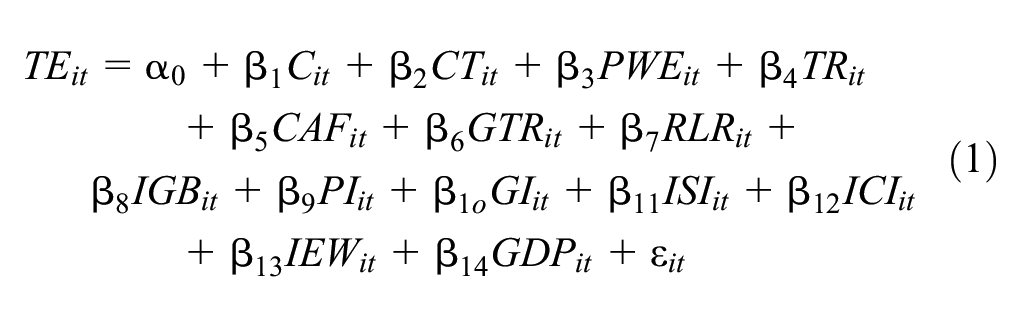

The model used in this study for OLS1 is as follows:

Where,

To check the robustness, we have run the OLS2 model, using

Where,

Furthermore, the study runs the fixed and random effect models (Fixed 1 and Random 1), including

Where,

Results and Discussion

Descriptive Statistics

Table 1 shows the descriptive statistics of the sample of 35 Asian countries for the 5 years based on the 175 observations of factors affecting business. The dependent variable, tax evasion (TE), ranges between 8.19% and 60.86% and has mean and standard deviation (Std.) values of 25.20% and 11.08%, respectively. This indicates a significant variation in tax evasion across the countries over the study period. Also, there is a considerable variation in the independent variables, with the standard deviation ranging from 1% to 8%.

Descriptive Statistics.

Source. Authors’ calculation.

Correlation Matrix

Furthermore, Table 2 presents the pairwise correlation among the variables. The results revealed many important correlations between TE and the doing business factors. For example, tax evasion has a positive correlation with corruption (C) (r = .46), government tax regulation (GTR) (r = .23), crime and theft (CT) (r = .21), and government instability (GI) (r = .25). On the other hand, tax evasion has a negative correlation with insufficient innovative capacity (ICI) (r = −.20), inflation (I) (r = −.27), restrictive labor regulation (RLR) (r = −.48) and GDP (r = −.42).

Pearson Pairwise Correlation.

Source. Authors’ calculation.

Source. Authors’ calculation.

p < .10. **p < .05. ***p < .01.

Multicollinearity Issue

However, prior to further analysis, the issue of multicollinearity was checked. Multicollinearity is a problem that occurs among the independent variables and can produce a biased result. If the value of the Pearson correlation matrix (r) is above .90, then a multicollinearity problem exists (Black et al., 2010). The highest correlation coefficient between corporate tax rate and government tax regulation is .68, which is less than the threshold of .90. Therefore, there is no collinearity issue in the study. Furthermore, the Variance Inflation Factor (VIF) was conducted to confirm the absence of collinearity in the model (see Table 3). The results showed that all the values were less than the threshold value of 10 (Hair et al., 1984), indicating the absence of multicollinearity among the variables used in the study.

Regression Analysis of Doing Business on Tax Evasion,

Source. Authors’ calculation.

p < .10. **p < .05. ***p < .01.

Hausman Test

We conducted the Hausman test to choose an efficient estimator between fixed and random effects. The test reports that the p-value for the chi-square statistic (Prob > χ2) is .0037, which is less than 5%, indicating the inconsistency of REM. Hence, the study considered FEM as an efficient and consistent estimator in explaining the variables.

Regression Results and Analysis

Table 3 represents the regression results of business factors and tax evasion. The study ran OLS, fixed, and random effect models to investigate the relationship between doing business factors and tax evasion. In the OLS regression results, the study found a significant and positive relationship between tax evasion (TE) and corruption (C) under all models at a 1% level of significance. This implies that an economy’s high level of corruption exacerbates tax evasion. Previous studies have also found a similar relationship between corruption and tax evasion (Alm et al., 2019). Taxpayers’ and tax officers’ involvement in corruption is considered a major determinant of tax evasion (Nyamwanza et al., 2014). Rashid (2020) argued that taxpayers might justify tax evasion if they perceive corruption by the government and its officials. On the contrary, our study documented an insignificant relationship between crime and theft, and tax evasion. The results did not support the findings of Richardson (2006). Crime and theft have no impact on tax evasion, as there may be higher economic freedom, effective competition laws, and a low rate of crime in some Asian countries. Therefore, the study advises the governments of Asian countries to control corruption, and crime and theft to reduce tax evasion and consequently boost the economy.

However, the finding of a significant positive relationship between poor work ethics and tax evasion suggests that ethically poor taxpayers evade more tax than those who are morally upright. The finding is supported by McGee et al. (2011) who documented that the poor ethics of taxpayers increase tax evasion. Many entrepreneurs exhibit a poor commitment to the tax rules and regulations of the country due to their low morality and lack of guilt (Drogalas et al., 2018). Therefore, the study suggests that firms and taxpayers should morally educate their workers to improve their commitment to tax payments.

While investigating the impact of regulations and enforcement on tax evasion, the study found a significant and positive relationship between government tax regulation (GTR) and tax evasion.

It means that if the government’s tax regulations become complex and stringent, tax evasion will be higher. The result implies that the higher the level of enforcement, the higher the level of tax evasion. This observation agrees with the result of prior research (Feld & Frey, 2007; Richardson, 2006) and suggests that taxpayers may feel discouraged from paying taxes if the government rules and regulations are very tight and complicated. Similarly, the study found a significant positive relationship between restrictive labor regulation (RLR) and tax evasion in both fixed and random effect models, in line with the study of Feld and Frey (2007). The results imply that the higher the government tax regulations and labor regulations, the greater the level of tax evasion. Therefore, the study suggests that the government of the Asian region should relax the tax rules and labor regulations; otherwise, the taxpayers’ perception of the complexity of the tax regulations may demotivate them from complying with their tax obligations.

Additionally, the study observed a positive and significant relationship between constrained access to finance (CAF) and tax evasion in all the models. When firms face constraints in managing credits or bank loans due to either high-interest rates or restrictive collateral, they consider tax evasion as a source of financing. Moreover, financial constraints hinder the smooth operation of firms and push them toward tax evasion. The findings support the studies of Alm et al. (2019) and Rashid and Morshed (2021), who observed that firms experiencing financial difficulties are more likely to be involved in tax evasion. Financially constrained firms tend toward tax evasion to increase their revenue, albeit with limited access to external finance. Firms struggle to manage or access external funds in an imperfect capital market, forcing them to depend on internal funds, including tax funds. Therefore, governments should take necessary actions to ensure the availability of funds for businesses to abate tax evasion to a significant extent.

While examining the effect of the corporate tax rate on tax evasion, the study found a significant and positive impact in both fixed effect and random effect models, confirming the finding of Epaphra (2015). The result indicates that the higher the tax rate, the greater the level of tax evasion. The findings suggest that the government should keep the tax rate as minimum as possible to reduce tax evasion. Similarly, the significant and positive impact of inflation on tax evasion in both fixed and random effect models implies that a lack of monetary freedom has a substantial influence on tax evasion. Supporting the prior research, the study outcome implies that a higher level of inflation increases tax evasion to a great extent (Abdixhiku et al., 2018; Gupta & Ziramba, 2010). Therefore, we suggest a reduction in the level of inflation in this region to curb the tendency of tax evasion.

Furthermore, in investigating the role of public sector governance on tax evasion, the study found a positive and significant association between government instability (GI) and tax evasion in all models. The result is consistent with the observations from prior studies by Nurunnabi (2018) and Islam et al. (2020). The findings imply that frequent government changes may impact policymakers’ decision-making process, which may, in turn, increase the level of tax evasion. In addition, the frequent changes in tax policy may discourage taxpayers from paying the tax due to the difficulties associated with adapting to a new government system. Also, tax payments may become costly for taxpayers, as they have to obtain services from lawyers to understand the changing tax policy. Furthermore, political instability generates inconsistent rules and regulations, as newly appointed political leaders tend to conduct the economy in their way. Moreover, different political parties promote different policies to pilot the internal affairs of the country, which may significantly encourage tax evasion (Ajaz & Ahmad, 2010).

Despite the insignificant effect of policy instability (PI) and inefficient government bureaucracy (IGB) on tax evasion in the OLS model, the significant impact in the REM supports the findings of prior research (Picur & Riahi-Belkaoui, 2006). Policy instability and insufficient government bureaucracy increase tax evasion, as unstable policies and weak bureaucracy, may lead to bureaucratic corruption and an unstable tax system, which induces taxpayers to neglect tax duty. Therefore, the study suggests that the government should strengthen its policy and bureaucratic systems since stable policies and bureaucratic efficiency play a crucial role in reducing tax evasion. However, among the control variables, insufficient capacity to innovate (ICI) and inadequate workforce (IWF) show a significant and positive effect on tax evasion, while GDP shows a negative association with tax evasion in both fixed and random effects.

Additional Tests

Furthermore, the study runs an additional model of OLS presented in column 4 of Table 3, exchanging the control variable GDP with foreign currency regulations (FCR). The results remain unchanged, indicating that our results are robust. Moreover, the study runs fixed and random effect models, and the results are consistent with OLS results except for PWE, TR, and RLR. Overall, the results of these models are consistent with the baseline model, which proves the robustness of the findings of our study.

Conclusion, Implications, and Future Directions for Research

Tax is one of the major sources of government revenue, which is often called the lifeblood of a government. For a government, it is essential to collect enough tax revenue to support government expenditures on health, education, social infrastructure, security, public goods, and so on. Tax revenue also plays a vital role in reducing a country’s poverty level. Nowadays, this vital source of government revenue has dwindled due to higher tax evasion, particularly in emerging countries like the Asian region. Therefore, the study aimed to investigate the relationship between business factors and tax evasion. The study found a positive and significant impact of corruption, poor work ethics, tax rate, constrained access to finance, government tax regulations, labor regulations, government instability, and policy instability on tax evasion.

The result of this study is expected to help the governments, tax regulatory authorities, tax lawmakers, and tax collection authorities of the respective countries build up a proper taxation system. The findings of the study provide the tax administration and governments of Asian countries with some valuable guidelines for the development of successful tax policies to reduce tax evasion. First, the government and regulatory bodies should decisively control corruption, and crime and theft, as these encourage taxpayers to disobey tax laws. Second, firms should improve the work ethics of their employees by providing them with proper education and training to motivate their tax compliance. Third, the government should relax the tax regulations and restrictive labor regulations as it encourages businessmen to contribute more to the state, thereby minimizing the level of tax evasion. Fourth, the government should reduce both the corporate tax rate and inflation rate, as higher monetary freedom and fiscal freedom cause greater tax evasion. Moreover, governments and funding agencies should take the necessary initiatives to relax the collateral conditions so that firms and individuals can easily manage their necessary funds at a cheap rate, significantly reducing tax evasion. Fifth, the study informs the governments and policymakers of Asian countries to improve institutional qualities such as political stability, policy stability, and the bureaucratic system, as they play an influential role in reducing tax evasion.

In a nutshell, the study offers some specific insights to governments and policymakers to gain a better understanding of the critical factors affecting businesses and their significant association with tax evasion. By designing and implementing sound strategies, the governments and tax authorities will be able to reduce tax evasion and consequently improve their tax collection capacity. Moreover, the study contributes new insights into the existing knowledge on taxation and tax evasion, thus extending the socio-economic theory. The study will also guide researchers and tax practitioners interested in extensive research on effective tax planning and implementation. Finally, it also creates an avenue for future researchers to explore other business factors that may induce tax evasion and offer possible solutions.

This study is not free from limitations. First, the study uses shadow economy data as a proxy for tax evasion, as it is challenging to measure. Hence, the outcome of this study might not depict an accurate picture of tax evasion. Secondly, the study was conducted in Asian countries, most of which are developing; therefore, the results may not be generalized to developed countries. Future studies may include all other parts of the world to get more robust results. Finally, the study considers only factors hindering business activities while excluding other factors, such as economic freedoms, institutional qualities, and religiosity. Therefore, future research can explore other economic and non-economic factors of tax evasion and consider a cross-regional investigation.

Footnotes

Appendix

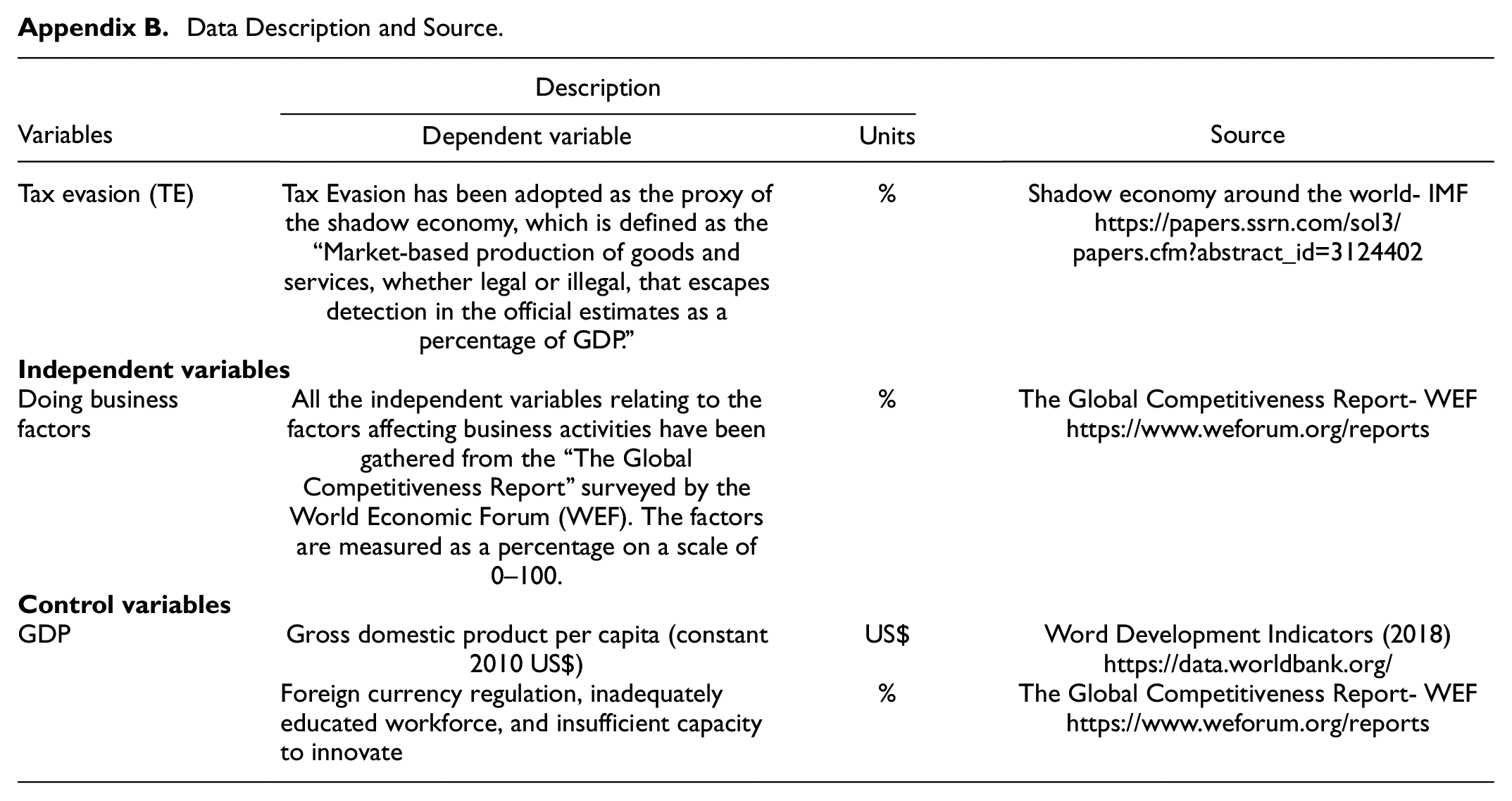

Data Description and Source.

| Variables | Description | Source | |

|---|---|---|---|

| Dependent variable | Units | ||

| Tax evasion (TE) | Tax Evasion has been adopted as the proxy of the shadow economy, which is defined as the “Market-based production of goods and services, whether legal or illegal, that escapes detection in the official estimates as a percentage of GDP.” | % | Shadow economy around the world- IMF https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3124402 |

|

|

|||

| Doing business factors |

All the independent variables relating to the factors affecting business activities have been gathered from the “The Global Competitiveness Report” surveyed by the World Economic Forum (WEF). The factors are measured as a percentage on a scale of 0–100. | % | The Global Competitiveness Report- WEF https://www.weforum.org/reports |

|

|

|||

| GDP | Gross domestic product per capita (constant 2010 US$) | US$ | Word Development Indicators (2018) https://data.worldbank.org/ |

| Foreign currency regulation, inadequately educated workforce, and insufficient capacity to innovate | % | The Global Competitiveness Report- WEF https://www.weforum.org/reports | |

Acknowledgements

The authors are grateful to the editors and anonymous referees of the journal for useful suggestions to improve the quality of the paper. Usual disclaimers apply.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.