Abstract

The aim of alleviating poverty has a necessary implication on rural households’ economic development. The study investigates the mediating role of access to financial services (AFS) in the effect of financial literacy (FL) on household income using survey data collected from four regions in Ghana. Using the multi-stage sampling technique, 572 respondents were randomly selected for the study. The findings of this study reveal that financial literacy has a robust, increasing effect on household income. Again, the results depict that AFS mediates the positive effect of FL on household income. An interesting moderating effect of social networks is also revealed in the study. This study adds to the existing literature on rural development by exploring how financial education and inclusions contribute to poverty alleviation and provides policy implications to improve rural households’ well-being.

Introduction

Improving rural households’ income opportunities is vital to help rural dwellers alleviate poverty, affecting economic development (Atkinson, 2017). An increase in disposable income affects households’ savings and consumption patterns, which literally leads to growth in consumption; that is, there is an increase in households’ demand for goods and services. When households’ goods and services demand increases, the profit share of suppliers (companies) is also positively affected, all other things being equal, thereby enabling the expansion of those companies (e.g., creating new jobs and hiring new workers), hence, affecting economic growth. Also, the welfare of most households is positively affected by improved household per capita income (Kikulwe et al., 2014; van Den Berg, 2010). For example, the wealthy rural household health conditions, educational investment, risk management, and entrepreneurial enhancement can be attributed to improved income (Case et al., 2002; Thomas, 1990). However, the number of people living in poverty continues to rise in rural Ghana (Ghana Statistical Service [GSS], 2015). The poverty gap between rural and urban dwellers is broad; thus, urban residents are now four times richer than their rural counterparts (Cooke et al., 2016). While many factors may contribute to this menace, prior studies (Andoh et al., 2015; Ankrah Twumasi, 2020; Atakora, 2016; Koomson et al., 2020) have shown that promoting financial inclusion and literacy are critical factors to increase rural household welfare in Ghana.

The ability to understand key financial concepts and demonstrate good financial management skills through appropriate and sound financial decision-making to improve his/her economic conditions is termed financial literacy (Remund, 2010). From these explanations, it can be argued that without proper financial management skills, that is, being financially illiterate, financial decisions and utilizing financial services, which is most advantageous to increase households’ income, becomes a challenge; hence affecting households’ well-being (Gallery et al., 2011; Lusardi & Tufano, 2015).

In most developing countries like Ghana, savings, borrowing, and investment decisions have direct effect on income. However, individuals’ lack of technical know-how of financial management reduces household income generation power through poor or wrong investment and borrowing decisions (Atakora, 2016; Mishkin, 2008). For example, Atakora (2016) argues that microcredit, an income booster, has no significant effect on Ghanaian rural households’ income development due to the misappropriation of funds (credit received) caused by financial mismanagement. The study also showed that most farmers could not improve their revenue even after selling their harvested products due to huge debts resulting from poor financial management.

Also, financial and economic risks related to investment, savings, and borrowing, which are likely to reduce household income, can be curtailed through the acquisition of better financial skills, leading to better financial decisions (Banks et al., 2020; Boekhold, 2016; Lusardi & Mitchell, 2017). According to Banks et al. (2020), people who are able to mitigate financial risk are less likely to lose money during investment or ruin in debt after securing credit. In the same manner, gaining much financial knowledge and skills can help individuals minimize financial market transaction costs, such as financial expertise consultation costs (Sabana, 2014). Escaping these costs are relevant because those funds could be used in income generating activity. From this background, it can be deduced that financial literacy can help improve household income. In other words, financial literacy has a direct effect on household income.

Moreover, compared with financially illiterate households, financially literate households are more likely to participate in the financial market that creates avenues for them to invest in economic activities advantageous to their livelihoods. A financially illiterate person may find it worrisome to patronize financial services such as holding savings account, accessing credit and participating in the stock market (Andoh et al., 2015; Ankrah Twumasi, Jiang, & Danquah, 2019; Frost et al., 2018; van Rooij et al., 2011; Xu et al., 2020). For example, Andoh et al. (2015) showed that most people, especially rural dwellers, refused to hold a saving account or borrow because of the complex nature of accessing financial services and misunderstanding of most financial terminologies such as interest rate, treasury bills, fixed deposit and many others. Also, formal access to credit was also positively associated with financially literate business owners in China (Xu et al., 2020). The study of van Rooij et al. (2011) identified that stock market participation is prevalent among financially literate individuals. Against this backdrop, we argued that financial literacy is essential to access and optimally use available financial services. In other words, financial literacy has a direct effect on access to financial services.

Generally, the need of being financially literate is essential because households or individuals financial and investment decisions in the financial market, such as where to invest or save, type of investment or financial assets to deal in, and how to invest, all require a certain degree of financial knowledge (Lusardi, 2008; Miller et al., 2009). This implies that financial literacy boosts individual confidence to patronize the financial market; thus, individuals’ access and optimally use of financial services is highly linked to their financial literacy level. As financial services are properly utilized, income is positively affected at large, all other things being equal. The reason is that access and optimally use of financial services improve household income. For instance, Ankrah Twumasi, Jiang, Ameyaw, et al. (2020) and Koomson et al. (2020) identified that access to financial services and products (e.g., credit and savings) among rural households, predominantly farmers, can increase farm revenue through enhanced farm productivity. Thus, the credit received can be used to purchase farm inputs, strengthen farmers’ ability to adapt or cope with climatic conditions and adopt new technologies to improve production. Even though mobilized savings can be used as collateral to secure formal loans in most developing countries, it also serves as a wealth creation instrument (Ankrah Twumasi, Jiang, Ameyaw, et al., 2020). People who invest in financial services such as treasury bills and fixed deposits can generate some income through dividends. Based on this scenario, we argued that financial literacy affects access to and appropriate use of financial services, which, in turn, affects income access. Therefore, this study explores the mediating role of access to financial services in the effect of financial literacy on household income. Theoretically, in this study, the authors argues that financial literacy positively affects both access to financial services and household income. Furthermore, social network (i.e., whether a household has a member working in a financial institution), is believed to moderate the core relationship between financial literacy and financial service participation (Ankrah Twumasi, Jiang, Osei Danquah, et al., 2020).

Household income is generally accepted in literature as a sustainable tool for improving household livelihood, but how financial literacy affects it has been less explored. This study adds to rural development and rural finance literature using data collected from four regions in Ghana. Ghana, a developing country, is interesting to examine because the nation is initiating several interventions to improve rural household welfare by ensuring that access to financial services becomes universal. For example, Ghana has seen a tremendous financial system progression through financial sector reforms such as the Structural Adjustment Program (SAP) and the Financial Sector Structural Adjustment Program (FINSAP). Also, to support the growth of the private sector and entrepreneurs, the Bank of Ghana, together with the Danish International Development Agency (Danida) and the German Agency of International Cooperation (GIZ) launched the Support Program of Enterprise Empowerment Development (SPEED). The program aims to propagate loan acquisition, investment, and insurance cover education for the people of the nation. All these programs and reforms aim is to enhance household living standard. Although 54% of females have a transaction account compared to 62% of males, the nation can boast of 29% improvement in Financial institutions (FIs) from 2011 to 2017 (Demirgüç-Kunt et al., 2018).

The study’s contributions are as follows. First, the study expands research on how financial literacy influences household welfare. Researchers on financial literacy mainly focus on urban households, students, entrepreneurs, and teachers; however, this study considers rural households, which have received less attention.

Similarly, we expand research on rural household development by indicating the significance of financial literacy as an essential tool in the financial market that affects rural households’ decision to utilize financial services. Rural dwellers, predominately farmers, due to inadequate capital, rely on credit, remittances, and other forms of financial aids to build their income; hence, improving household well-being. Without proper financial management skills, these dwellers participation in the financial market is likely to be a failure (Han & Melecky, 2013), which will affect their financial service patronization, thereby causing a detrimental effect on their welfare.

Also, the study measured access to financial services status by a more comprehensive definition. Specifically, the study defined access to financial services as the services that meet the needs of transactions and payment, credit, savings, and insurance rather than taking only one aspect of these services, which happens in most literature.

Finally, from the theory of social networking, the author tries to test social networks (whether a household has a link with a FI official) as a moderator for the financial literacy-AFS relationship. It is believed that individuals take precautional measures when dealing in the financial market to be successful in their financial decision (Ankrah Twumasi et al., 2021; Bucher-Koenen et al., 2017). Therefore, knowing an expert or relating to someone already an official in the financial market becomes a plus for the individual willing to participate in the market.

The remainder of the paper is organized as follows: Section 2 provides a literature review and hypotheses of the study. Section 3 presents the methodology of the study, which includes data sources and measurement of key variables. Section 4 presents the findings and discussions of the results. Section 5 concludes the study, provides policy implications and limitations of the study.

Literature Review and Hypothesis

Financial Literacy and Household Income Relationship

In this study, the author argues that there is a positive relationship between financial literacy and household income based on available literature (Figure 1). Thus, individuals with high financial education are more likely to increase their household income. According to van Rooij et al. (2011) and Brown and Graf (2013), financial illiteracy among individuals prevents them from exercising investment choice decisions, which affects their income negatively. An indication that with proper financial knowledge, better choices of investments are made to promote income. Again, Agyei (2018) reported that proper financial management (financial literacy) positively affect individuals and households wealth accumulation and financial well-being. To acquire wealth, one needs to be endowed with financial management skills. The decision to invest in a profitable venture or activities does not happen easily, that is, it comes with critical thinking that will enable the investor to weigh the cost and benefit of that particular investment (Guiso & Jappelli, 2005). For example, a farmer who borrows from a formal FI to increase productivity must understand why that loan is needed and how to apportion the loan to escape the huge loan burden lost after selling out his or her harvest. Also, the act of committing financial mistakes unknowingly, abandoning recommended financial practices, and sticking to less risky but inefficient financial practices are as a result of being less financially literate (Lusardi & Mitchell, 2013). This simply implies that household income, which is affected by household financial management skills or choice of investment, is influenced by the financial literacy level of the household members. The hypothesis underlying the above discussion is:

H1: Household financial literacy positively relates to household income

The Mediation Effect of Access to Financial Services (AFS)

Access to financial services is an essential variable capable of explaining the effect of financial literacy on households’ income levels. Thus, when describing the relationship between financial literacy and income, AFS can serve as a mediator. Financial literacy is understood as a determinant of access to financial service participation. For example, Andoh et al. (2015) revealed that being financially literate can boost individuals’ confidence to participate in the financial market (e.g., receiving credit and mobilizing savings for future predicaments). Most people battle with huge sums of debt (unable to pay back loans) because of financial illiteracy, which affects their ability to accurately calculate interest rate charges on loans demanded and misappropriation of fund (loans received). Therefore, causing them not to borrow again (Stango & Zinman, 2007).

Similarly, concerning household welfare, several studies have found a positive relationship between access to financial services and household income (Dong et al., 2012; Khandker & Koolwal, 2016; Saifullahi & Haruna, 2012). For example, Dong et al. (2012) found that farmers with access to credit and savings tend to increase farm productivity and household income. There is much enhancement in rural farm households’ livelihood if they are not financially excluded (Khandker & Koolwal, 2016). The positive effect of financial service participation on incomes cannot be concealed. AFS has elevated most farmers from small scale farming to commercial one (Dimova & Adebowale, 2018). For instance, patronizing financial service products (e.g., securing credit) is expected to affect rural farm households’ agriculture technology adoption and the purchasing power of inputs needed to increase productivity; hence, increasing household income (Inoue & Hamori, 2012; Lin et al., 2019). Most households’ welfare outcomes such as income, expenditures, food security, and health are all impacted by the services provided by financial institutions (FIs). From the above discussions, we can argue that AFS serves as an underlying mechanism through which financial literacy affects household income. Thus, the author expects a financial literacy household to patronize financial service products, which will, in turn, affect household income. The hypothesis in this section is as follows:

H2: Access to financial services mediates the positive relationship between financial literacy and household income

Social Network as a Moderator

In this study, the variable social network is selected as a moderator linking the relationship between FL and AFS. Here, social network means knowing someone, being it a relative or a friend, who works in a financial institution. It is expected that those with such connections are more likely to be active in the financial market. Thus, social networks may moderate the relationship between FL and AFS. The study of Ankrah Twumasi, Jiang, Ameyaw, et al. (2020) explored credit accessibility impact on energy consumption by controlling social networks. The study revealed that social network positively and significantly affects households’ access to credit in the financial market. For example, when an individual is connected with FI officials, the trust and confidence of patronizing financial services and products increase. Also, such a person is abreast with financial market concepts through interaction with the FI official he/she knows, thereby affecting their decision to patronize financial service products (Ankrah Twumasi, Jiang, & Owusu Acheampong, 2019). Thus, FL is expected to substantially affect AFS for those with social networks with FI officials in a financial institution. In this era where banks are collapsing in Ghana, and people are being exploited by FIs (Baidoo et al., 2018), knowing someone in the financial market may increase the confidence level of a financial literacy person to participate in the financial market. Thus, social network provides a stronger effect of FL on AFS. The study proposes this hypothesis for the moderator.

H3: Social network moderates the positive nexus between households’ FL and AFS such that the nexus is stronger when social network is high.

However, the study proposed a hypothesis depicting the connectivity of the mediation effects to the moderating effects of social network as:

H4: Social network moderates the positive relationship between FL and household income through AFS such that the nexus is stronger when social network is high.

Theoretical model.

Measurement of Key Variables

This study explores the effect of FL on household income using AFS and social networks as a mediator and moderator, respectively. This study’s financial literacy measurement was calculated using seven quiz-like questions employed by many scholars (Andoh et al., 2015; Ankrah Twumasi et al., 2021; Lusardi & Mitchell, 2007; Niu & Zhou, 2018). We assigned the value of 1 to a correct answer and 0 to an incorrect answer, suggesting that the FL score will range from 0 to 7. Thus, a respondent is assigned the value of 7 in getting all the questions right and 0 otherwise. Table 1 depicts the seven financial literacy questions of the study.

Financial Literacy Questions and Responses.

In the same manner, AFS is measured using three questions. These questions included whether the respondent has access to (1) savings account, (2) credit/loan, and (3) insurance. Here, access to financial services means that the respondents own these financial services or products. Thus, the respondent is a savings account holder or insurance policy account holder or has received a loan within the last 12 months. The insurance variable includes agriculture (e.g., weather index insurance), and property (e.g., house and vehicle/car). These two types of insurance were found common among the rural dwellers; therefore, they were selected. The respondents were asked to respond “yes” or “no” to the following questions. Did you hold a savings account in the last 12 months? Did you receive credit from any financial institution in the last 12 months? Did you own any of these insurance policies in the last 12 months? A value of three (3) is assigned to a respondent who enjoys all three financial services and 0 to those who do not enjoy any of these services. According to the World Bank, this measurement is adopted because a person is considered financially inclusive if he/she has access to a savings account, credit, and insurance (World Bank, 2018).

Concerning household income measurement, the author followed previous studies, that is, Ma et al. (2018, 2020). Thus, household income equals each household’s total net annual income in 2019, including farm income, off-farm income (e.g., wages/salaries), and other income sources (e.g., remittances, pension, rents, and dividends), which is measured in 1,000 cedis (GH¢)/capita.

In addition, other variables that could help achieve the study’s goal are controlled in the study. Thus, following previous literature (Andoh et al., 2015; Browning & Lusardi, 1996; Xu et al., 2020) and data available, householders/households’ characteristics (e.g., age, sex, education, and household size) and other factors (e.g., farm size, access to the Internet, off-farm work and NFA) are taken into consideration in this study. The definitions of these variables can be seen in Table 2.

The Definition and Data Description of the Variables in the Model.

Source. Survey results, 2020.

Note. Cedis (Gh¢) is Ghanaian currency ($1 = Gh¢5.5).

Data Source

We conducted this study in Ghana from April to June in the year 2020. Data collection was done through the use of interview schedules and questionnaires. To clear all doubts and make the questions simple and understandable for our respondents, we had an in-depth interview and carried a pilot survey. The questionnaires used for data collection covered information relating to socioeconomic characteristics, financial literacy, and alternative variables necessary to help us achieve the aim of the study.

We employed the multi-stage sampling method. Four regions, including Northern, Central, Eastern, and Brong Ahafo, were selected at stage one (Figure 2). The reason of selecting these regions is that they have more rural dwellers compared with the other regions (GSS, 2019). In the next two, we randomly chose a district from each of the four regions. Thus, Northern (East Gonja), Central (Ekumfi District), Eastern (Kwahu Afram Plains District), and Brong Ahafo (Atebubu Amantin District). The random selection of three communities/villages from each selected district was done in the third stage. The East Gonja, Ekumfi, Kwahu Afram Plains, and Atebubu Amantin districts had the following villages respectively selected (Yankanjia, Akyenteteyi and Salaga), (Essarkyir, Otuam, and Kontankore), (Tease, Bumpata, and Ahiatroga), and (Asempanye, Dobidi Nkwanta, and Atebubu). Based on the information gathered from the Ghana Living Standard Survey 7 (GLSS 7) report, about 44% of the people living in rural areas have access to financial services (GSS, 2019). We, therefore, estimated our sample size based on the report by following Kotrlik et al. (2001) estimation method. Thus, assuming a 95% confidence level and 5% margin of error, the total number of respondents was estimated as follows.

where

A map of Ghana and study areas.

Results

Descriptive Analysis

Table 2 depicts the definitions, means, and the variables standard deviations applied in this study’s model. The table displays an average of 2.63 financial literacy scores, a mean of 1.68 for AFS (47%, 38%, and 19% of the respondents with access to savings, credit, and insurance, respectively), an average household income of GH¢3,970, and a percentage of 43 for respondents who relate with financial institution officials (social network). The respondents’ average age is approximately 42 years. Meanwhile, about 27% of the respondents have a high school or higher education, and 14 years is recorded as the average years of the respondents’ farming experience. About 41% to 59% of the respondents have NFA access and off-farm job, respectively. On average, a household consists of seven people and a farm size of 4.34 acres. About 33% of the households reported that they have at least a member who has a chronic disease, 78% are risk-averse, and 69% are males.

Hypothesis Testing

The mediation path model test

Using observed variables was preferred to latent variables when testing for the study’s hypotheses, hence implementing the PROCESS-macro model in the study. Moreover, the mediator and the outcome variable are regressed on the control variables, and the results are presented in Tables 3 and 4. Table 2 estimates that only the mediation model is displayed, while Table 4 considers a moderated mediation model by including the moderating effects of social networks. The direct and indirect impact of FL on household income through AFS can be seen in the mediation model. The results in Table 3 provide evidence to support H1. Thus, the results show that there is a significant and positive relationship between FL and household income. In the same manner, the positive relationship between FL and household income is mediated by AFS, a finding that supports H2. This can be seen from Table 5 where the indirect effect of the mediator is positive (0.162) and with an acceptable range, that is, 95% Bias-corrected confidence intervals ((BC CI) = [lower = 0.101, upper = 0.213]). Using 5,000 bootstrap samples, we calculated the BC CI.

The Mediation Path Model Estimates (Model 1).

Source. Survey results, 2020.

Note. Robust standard errors are in parentheses. The reference region is Northern.

, **, ***Represent significant levels at 10%, 5%, and 1% respectively.

The Moderated Mediation Path Model Estimates (Standard Error).

Source. Survey results, 2020.

Note. Robust standard errors are in parentheses. The reference region is Northern.

, **, ***Represent significant levels at 10%, 5%, and 1% respectively.

The Mediation and Moderated Mediation Effect Results (Standard Error).

Source. Survey results, 2020.

Note. Robust standard errors are in parentheses.

Test of the moderated mediation path model

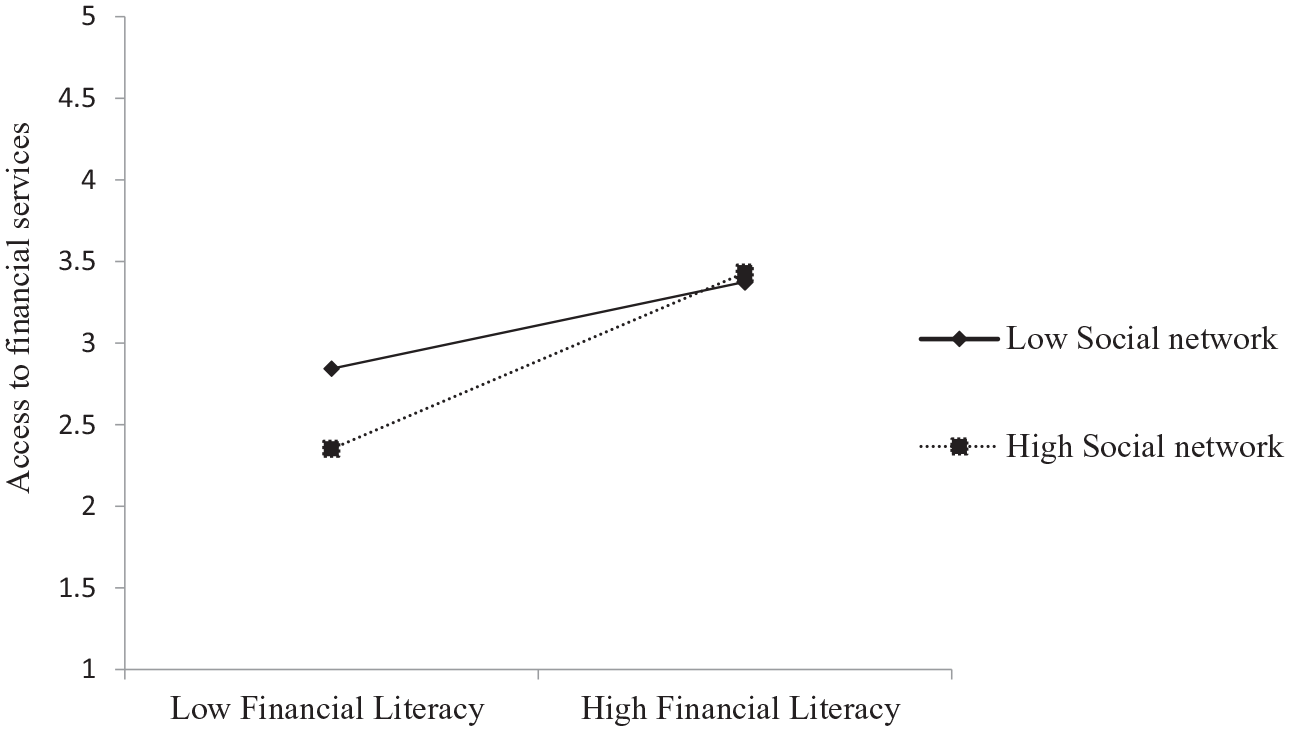

In Table 4, we depicted the moderated mediation path model analysis. At this stage, the social network is included as a moderator. To predict AFS, the author introduced an interaction term between FL and social networks. The interacting variables of FL and social networks are centered prior to being interacted. The results reveal that H3 is supported. Thus, the interaction between FL and social networks on AFS is statistically significant, at 5% (coefficient = .137). The tests of the simple slope for both household heads with high social network (simple slope = 0.417, p < .01) and those with low social network (simple slope = 0.145, p < .05) are positive and significant. However, the magnitude of the household head with a high social network slope is profound compared with their counterparts with a low social network.

To give a further insight into the interaction patterns, the FL and AFS nexus is plotted at high and low values of social network (see Figure 3), defined as one standard deviation above and below the mean value, respectively (Cohen, 2014). The analyses again provide evidence that supports H4. From Table 5, the interaction effect product term between FL-social network nexus on AFS and the direct effect between FL and AFS, that is, moderated mediation index is statistically significant (index = 0.083, p < .05) (Hayes, 2015). In Table 5, further explanation to support H4 is shown. Here the FL conditional indirect effects on household income through AFS is not significant for household heads with low social network (coefficient = .061, and the 95% BC CI = [lower = −0.043, upper = 0.122]). However, household heads with high social network depict a significant conditional indirect effect (B = 0.194, and the 95% BC CI = [lower = 0.061, upper = 0.152]).

The interaction effect between financial literacy and social network on access to financial services.

Discussions

This study explores how household income is affected by FL through AFS (mediator) and social network (moderator). The study is explored by employing survey data from four regions in Ghana. The study’s contributions compared to previous works are the following: first, this study constructs a theoretical framework of “financial literacy → Access to financial services → household income”; second, the mechanism at which FL positively influences household income is affected by the mediating role of AFS. Third, social network moderates the direct relationship between FL and AFS and the positive FL indirect effect on household income. This study helps in understanding the mediating role of AFS in the impact of FL on household income as well as how social networks as a moderator could improve financially literate individual’s financial services participation. The study will be of high benefit to policymakers through the provision of measures or policies highlighted in this study to enhance rural farm households’ income through AFS and FL.

The results reveal that household income is likely to increase as individuals become financially literate; thus, a positive relationship exists between these two variables. However, the mediating role of AFS in the FL and income positive nexus is profound. This is possible because people who tend to be financially literate will be more likely to access financial services since they have enough knowledge and understanding of the financial market services and products; hence, affecting household income. These findings have similarities with prior studies which reported that being financially literate improve one’s understanding of the financial market; hence, empowering financial services and products patronization (Andoh et al., 2015; Thomas & Spataro, 2018; Xu et al., 2020), which in turn, affects household well-being positively (Churchill & Marisetty, 2020; Kim et al., 2018; Kumari & Ferdous Azam, 2019). For instance, Kumari and Ferdous Azam (2019) found out that financially literate women can improve their economic status through access to financial services and products. Also, Andoh et al. (2015) showed financial literacy together with access to credit increase the growth level of Small and Medium Enterprises (SMEs) drastically. Thus, access to financial services mediates the positive relationship between financially literate women and their improved economic status. The study also revealed that the positive relationships among these variables are moderated by social networks (whether the respondent has a link with someone who works in a financial institution). In Ghana, many people have lost trust and confidence in the banking sector due to the collapse of many local financial institutions (e.g., banks, microfinance) by the central bank to strengthen the banking sector (Owusu-Antwi, 2011). Again, the probability of facing credit constraints in rural areas, that is, rejection or rationing of credit application, is reduced through social networks (having a connection with FI officials or opinion leaders) (Ankrah Twumasi, Jiang, Ameyaw, et al., 2020; Chandio & Jiang, 2018). Therefore, social networks can serve as a tool to enhance individual financial services patronization.

Several policy implications are provided in this study to help formulate better policies to enhance rural dwellers’ living standards in Ghana and the other developing countries. First, the results have revealed that designing policies to enhance financial inclusion and education should be prioritized. For instance, the government, NGOs, and other policy stakeholders should consider organizing financial literacy training for rural dwellers at least once a month to improve their financial literacy. Again, initiatives to increase the establishment of microfinance in rural communities should be considered. The reason is that household incomes are improved should the household gain financial education and access financial services.

Second, the moderating role of having a high social network in the positive relationship between FL and AFS, as well as FL and household income positive indirect relationships through AFS, has some implications. This mechanism implies that it is essential for rural dwellers to establish a good relationship with financial institution officials to gain much knowledge on financial services, which in turn, enhance financial service participation; hence, improving household income.

Conclusion

With the help of household survey data from four regions, this study explored the mediating role of AFS in the effect of FL on household income. This study contributes to rural household development or welfare enhancement literature by indicating the significance of financial literacy as an essential tool in the financial market that affects rural households’ decision to utilize financial services. Based on the above analysis, the research mainly draws the following three conclusions:

The results of the current study showed that financially literate individuals and also with access to financial services are more likely to improve their household income. Also, the positive nexus between FL and household income was attained through the mediating role of AFS. The variable, social network moderated these mechanisms. This study explains how financial education and inclusions contribute to poverty alleviation.

The study employed a mediation effect model to examine FL impact on household income using AFS as a mediator and social network as a moderator. The mediation effect model depicts a clear picture of the mechanism among these variables, which allows testing all hypotheses in one model. However, in this study, several limitations still exist and need to be critical attention by readers and other researchers. First, the study focused on rural areas in only four (4) out of (10) regions in Ghana because of financial constraints. Targeting a more than 4 regions or the entire nation can be a priority for future researchers. Second, the measurement of the mediating variable, AFS, was based on three financial services concepts, transaction service (savings), credit service (access to credit), and insurance. However, financial services go beyond these three. Future researchers can formulate more advanced scales or indexes to measure financial service participation by including other services such as the capital market (e.g., stock exchange market). Third, the outcome variable was limited to household income level. However, considering household welfare (which includes household expenditure, income, and other household possession) rather than only household income will deepen the mediating role of AFS in the effect of FL on household well-being. Thus, future studies are encouraged to extend the analysis to household welfare. Finally, we acknowledge the existence of reverse causality between access to financial services and financial literacy which has important implications on our finding. Although the study has demonstrated the direct effect of financial literacy on access to financial services, financial literacy can also be influenced by financial services accessibility. Therefore, caution is need when interpreting the result of the study. In spite of these caveats, we are not expecting a systematic bias in our assessment.

Footnotes

Appendix

Acknowledgements

We would also like to thank the anonymous reviewers for their valuable comments and suggestions. Finally, thanks to the Associate Editor for his/her generous corrections, patience, and support during the review process.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors gratefully acknowledge the financial supports from the Soft Science Program of Sichuan Department of Sci-technology (Grant No. 18RKX0773). Martinson Ankrah Twumasi and Zhao Ding acknowledge the financial support from the National Social Science Fund of China (No. 21CGL026).