Abstract

Steered by the resource-based view theory, this study scrutinizes the impact of the dimensions of Intellectual Capital (IC)—human capital, structural capital, and relational capital (RC)—on sustainable growth (SG) with the mediating role of Sustainable Competitive Advantage (SCA). We gathered data from 2010 to 2017 of 90 listed firms of China and Pakistan, respectively, and applied EVIEWS. The results indicate that IC plays a significant role in the SG of Chinese and Pakistani firms. IC has a significant influence on differentiation strategy (DS) in Chinese firms whereas only RC has an insignificant influence on DS in Pakistani firms. IC has a significant influence on cost leadership strategy (CLS) in Pakistani firms whereas structural and RC have an insignificant influence on the SG of Chinese firms. In terms of the mediating role, DS partially mediates the relationship between IC and SG in Pakistani firms while it only fully mediates the path between RC and SG in Chinese firms. CLS partially mediates the relationship between IC and SG in Chinese firms while it fully mediates the association between human capital and SG in Pakistani firms. This study recommends Chinese and Pakistani firms to encourage investment in IC to gain SCA and SG in the turbulent markets. To concise, this research advises Chinese firms to invest a satisfactory amount in human capital as compared with structural and RC. However, Pakistani firms should focus on IC to gain SCA and SG.

Keywords

Introduction

Securing a sustainable competitive position (SCP) in a turbulent market has become a requisite of the day for business and nonbusiness organizations across the globe. For the last several decades, business firms across the globe have been competing for Sustainable Competitive Advantage (SCA) and sustainable growth (SG; Lee & Lee, 2019; Maury, 2018; Xu & Wang, 2018). Some firms invest in intangible resources such as machinery (Shirodkar & Mohr, 2015), land and equipment (Mitra et al., 2016), and technology (Khallaf et al., 2017), whereas other firms prefer investment in intangible resources such as Intellectual Capital (IC), Corporate Social Responsibility (CSR; Sampong et al., 2018), knowledge (Dženopoljac et al., 2019; Ying et al., 2019), and entrepreneurial activities (Kiyabo & Isaga, 2020). In other words, previous studies have suggested several determinants that can spur firms’ SCA and SG (Lee & Lee, 2019; Maury, 2018; Xu & Wang, 2018). Resource-Based View (RBV) theory demonstrates that a firm’s tangible and intangible resources and capabilities configure its survival and superior performance (Barney, 1991). The theory has given more importance in this context to intangible resources over tangible resources (Sallah & Caesar, 2020; Salvi et al., 2020). This claim (e.g., supposed by RBV theory) is supported by several recent studies (Haji & Mohd Ghazali, 2018; S. Z. Khan, Yang, & Waheed, 2019). However, the question is still elusive whether the tangible resources or intangible resources are more useful for a firm’s success. Considering business firms in China and Pakistan, studies have reported a high failure ratio because of poor support, lack of managerial skills, and deficiency of resources (Alkahtani et al., 2020; S. Z. Khan, Yang, & Waheed, 2019). Moreover, they have a lack of technological and financial capacity to respond to external pressure and competition (Motta & Sharma, 2020). Therefore, firms in China and Pakistan need intangible skills and capability to boost their performance (Ali et al., 2020).

Due to a high cost and poor convenience, firms in emerging economies such as China and Pakistan prefer intangible skills—specifically IC—to spur their competitiveness and performance. However, it is not yet acknowledged how Chinese and Pakistani firms use their IC to secure a competitive position—resulting in superior performance in the market. This research fills the gap and contributes to the existing body of knowledge using the mediating role of competitive advantage (CA; differentiation-based CA and cost leadership-based CA) between the dimensions of IC—human capital, structural capital (SC), and relational capital (RC)—and SG. The model of this research is tested on empirical evidence collected from Chinese and Pakistani listed firms.

Studying the relationships among IC, SCA, and growth are not new. Since the last two decades, many studies have claimed a significant positive relationship in emerging markets (Khalique et al., 2020; S. Z. Khan, Yang, & Waheed, 2019) and developed economies (Nadeem et al., 2018; Tonial et al., 2019; Xu & Wang, 2018). However, some constraints exist in the results of prior studies. For instance, Z. Wang et al. (2018) claimed no significant direct relationship between all the dimensions of IC and firm performance. Similarly, previous studies have considered different dimensions of IC including customer capital (Inkinen, 2015) and organizational capital (Andreeva & Garanina, 2016). However, we used the most used dimensions named human capital, SC, and RC. A study conducted by Deloitte (2015) indicates that 75% of the companies believe in human capital for superior performance whereas only 8% prefer other types of organizational capabilities.

The novelty of this research is described in two ways. First, previous studies have broadly discussed the relationship between IC and firm performance (Asiaei et al., 2018; Smriti & Das, 2018) as well as the mediating role of SCA (S. Z. Khan, Yang, & Waheed, 2019).

These studies further warrant the examination of the role of the CA as a mediating factor in explaining the direct effect from IC to the organizational performance. However, the mediating role of each strategy namely differentiation and cost leadership between each dimension of IC and SG has been untouched. Second, the existing studies have either focused on developed or emerging markets. Most studies in the context of SCA have focused on small firms whereas listed firms have received very minor attention in China and Pakistan. This study collected evidence from two emerging economies: China and Pakistan to test the model. We argue that the evidence from both firms will enhance the validity of the results and will generate significant implications for practicing managers. This research helps CEOs, top managers of the listed firms to enhance the most remarkable dimensions of IC that can spur growth and SCA. This research also encourages responsible managers to invest money in intangible factors such as IC rather than focusing on tangible resources. In other words, intangible resources are less risky and require less amount of money as compared with tangible resources such as technology and machinery. Therefore, it is a good opportunity for investment managers to acquire maximum benefits through investment in intangible resources. Furthermore, this study helps top managers of Chinese and Pakistani firms in building their strategies for SCA, SG, and performance. For instance, the findings help which strategy either differentiation or cost is better to configure growth performance in the market.

This research contributes to the RBV theory (Barney, 1991) that states the prevalence of tangible and intangible resources in superior performance and SCA. However, RBV theory gives more weight to intangible resources over tangible means (Alkahtani et al., 2020; S. Z. Khan, Yang, & Waheed, 2019). Therefore, considering intangible resources for SCA and SG is a worthy attempt for research in the current era of globalization. Hence, our study examines how intangible factors facilitate firms in gaining SCA and superior growth. It clears the concept and claim of the RBV theory through empirical evidence gathered from Chinese and Pakistani firms.

This article has significant contributions to current strategic literature of dimensions of IC, cost leadership strategy (CLS), differentiation strategy (DS), and SG in the RBV theory prospective. For instance, the RBV theory (Barney, 1991) has been tested by several studies in emerging and developed markets. However, this research tested the theory with separate dimensions of IC, SG, and SCA. This research supports and adds new insight into RBV theory via empirical evidence gathered from China and Pakistan. For example, RBV theory scrutinized that enterprises’ internal capabilities have a significantly high impact on enterprises’ success in contrast to external capabilities concerning RBV theory. IC dimensions may be deemed as distinctive intangible internal capabilities that every firm embeds regularly for the sake of superior growth and SCA. This article assesses the significance of IC dimensions in SG and CA to improve our knowledge in respect to RBV theory in the context of China and Pakistan.

Theoretical Underpinning

The quest of the organizations for scarce organizational resources is more volatile with globalization. Organizations ensure their survival and increase their profitability through their available resources, which is only by effective utilization of these resources (Chang et al., 2016). According to the RBV, there are two types of resources available in the organizational field (Barney, 1991). These two are characterized by their intrinsic nature, such as the form of the resources, whether they are unique or common in the organizational field. The common resources are those which are equally available for all the organizations operating in the organizational field. However, the unique resources are those which are rare, valuable, and hard to imitate and obtain (Barney, 1991). However, the resourceful an organization is, its ultimate survival and competitiveness rely on the availability and control over scarce resources. Every organization is different as far as their resourcefulness is concerned; some rely on the common stock of resources and perform innovatively to make their common resources more effective, whereas the others who are bestowed with the unique resources may enjoy reasonable competitiveness, as long as their resources remain unique. These variations in the levels of their access to the resources force the lagging organizations to strive hard either for the scarce resources or to increase their competitiveness through increasing their innovativeness (Kozlenkova et al., 2014). These characteristics of competitiveness make the smaller organization more vulnerable in the hyper turbulent environment. The small organizations are constrained by their proximal zone, which can determine their access to the available scarce resources (Porter, 1985).

Literature Review and Hypotheses Development

Dimensions of IC and SG

IC refers to access to the unique knowledge, experiences, and professional knowledge which improves the organizational performances, and also includes the technological advancements which give an organization a better position as compared with their competitors (Sofian et al., 2004). IC is considered to be a very important resource for an organization; however, it is sometimes undermined by the organizational inability to capitalize on it, or sometimes simply ignored to protect it legally (Rossi et al., 2016). It is agreed that human capital is the driver of these secondary resources, such as they are the sources who are the custodians of these capitals, such as the experiences of the employees, their knowledge, and their innovative capabilities.

Articulating these sources, Barney (1991) argued in the RBV of the firms that the CA of the organizations is determined by the availability of the unique and rare resources, which are hard to imitate by the competitors, and purely internal to the organization, such as it is not relying on any other external sources for these stocks (Stiles & Kulvisaechana, 2004). The existing literature is lacking in providing the empirical pieces of evidence for ascertaining the causal relationship between the IC, on one hand, and the organizational performance and the CA, on the other hand. In addition to that, it is still not clear that what is the generating mechanism through which the effects of the IC are transferred to the organizational performance? In this backdrop, the CA is one of the important factors which could be used to explain the generating mechanism through which the IC affects the organizational performance of the firms.

Oppong and Pattanayak (2019) claimed that all the dimensions of IC significantly spur firm efficiency and growth in emerging markets. In a similar vein, Khattak and Shah (2020) concluded that IC is deemed an essential driver of enterprises’ growth and success. S. Z. Khan, Yang, and Waheed (2019) suggested that in turbulent market firm give more preferences to IC because it is less expense source and help the firm to achieve higher profitability. Supporting this notion, Ying et al. (2019) scrutinized that intangible capabilities significantly spur firm growth and contribute to SCA. Besides, IC is a source of novel activities, innovation, and helps the firm to gain valuable resources which in turn enhances firm growth and success (Cabrilo et al., 2018; Mukherjee & Sen, 2019b; Xu & Wang, 2018). It is claimed that those enterprises which are technology-intensive should focus on IC to improve their innovativeness and creative work (Y. Liu et al., 2019; Sardo & Serrasqueiro, 2021).

Enterprise productivity can be enhanced by numerous variables but IC can spur productivity more efficiently as compared with other variables (Oppong et al., 2019; Yao et al., 2019).

Furthermore, IC can be a prominent factor for high innovation (Agostini et al., 2017; McDowell et al., 2018) and competitiveness (Ślusarczyk & Dziura, 2017). However, some scholar’s concluded that all the proxies of IC do not significantly influence firm growth and success. For example, Yaseen et al. (2016) scrutinized that two proxies of IC such as RC and SC have a significant influence on enterprise performance. Besides, in developed economies, scholars argue that those firms which invest a huge amount in intangible resources (e.g., IC) are growing faster than other firms (Nadeem et al., 2018) and enhance enterprise performance (Nadeem et al., 2016). Therefore, the hypotheses are as follows:

Dimensions of IC and SCA

Different studies examined the relationship between the IC and the CA and demonstrated that they are strong predictors of the CA an organization enjoys, particularly, the dimensional-level analysis of the IC exhibited that RC is strong predictor among the three dimensions of the IC (Dyer & Singh, 1998; Jadallah, 2012). This strong relationship is due to the instrumentality of the RC and the human capital which are the driving forces in achieving the other sources of capital. The RC is the source, which interacts with other forms of the resources in creating the overall IC for the organization and serves as instrumental in achieving the CA for the organizations. Besides, human capital is also considered to be an important source of the CA due to its capabilities to interact with other sources and the internal skills, knowledge, and experiences in dealing with the diverse nature of problem-solving and other forms of organizational innovativeness (Auw, 2009).

Taking the first dimension of the IC, which is human capital, it is the accumulation of the human capabilities, their experiences, their knowledge base, their relevant skills, and other individualist attributes that make them different from them both within the organization and outside the organization. Finally, the third dimension of the IC is RC, which is both internal as well as external and is associated with the relationship of the organization with the internal stakeholders such as their employees. They may need to capitalize on the opportunities available in the external environment of the organizations such as the feedback from the customers, the financial support opportunities available for the research and development programs, development of their organizational identities through engagement in the CSR programs of the social societies for the betterment of the society, and also to attract more efficient workforce from the external environment, these factors holistically define the RC of the organizations (Bontis, 1998; Roos & Roos, 1997).

All dimensions of IC are a source of innovation, novel activities, and effective SCP (Duodu & Rowlinson, 2019; Radjenović & Krstić, 2017). Novel business events permit firms to manufacture goods at a low cost and different from the well-known competitors in the industry. As highlighted by Sardo and Serrasqueiro (2018), IC not only assists enterprises to gain useful resources but also facilitates growth. Intangible resources (i.e., IC) are considered very essential for enterprises’ success and SCA (Ginting, 2020). In a turbulent market, the high growth and SCP of enterprises are strongly affected by IC (2020). IC dimensions are considered important drivers for technological innovation in high tech firms (Elia et al., 2017), which in turn spur small and medium-sized enterprises’ (SMEs) innovative performance and SCP (Agostini et al., 2017). A study of Verbano and Crema (2016) stipulates that the basic intention of IC is to improve the innovativeness in the manufacturing business, which in turn can enhance SCA (Xu & Wang, 2018). A satisfactory level of IC is essential for enterprises to survive long-term in the dynamic market (Bontis et al., 2018). In recent waves, several studies recommended that IC significantly influence SCA in emerging market (Kanaan et al., 2020; Yusliza et al., 2020). Drawing on these arguments and having empirical pieces of evidence, we develop our hypotheses as follows:

SCA and SG

There are ample pieces of evidence that claimed a significant positive influence of CA on superior performance and firm growth (S. Z. Khan, Yang, & Waheed, 2019). For instance, Porter and Strategy claimed, when a firm differentiating and producing unique kinds of products and services other than competitors, customers intend to purchase the products. In turn, the company’s sales performance improves and secures its sustainable position. Similarly, when a firm produces a low-price product, cost-conscious customers purchase the products in bulk which enhances SG. Therefore, both the strategy of either differentiating products or producing products at a lower price enhances SG (Acquaah & Agyapong, 2015).

An enterprise in an emerging market can achieve the SCA via producing unique goods, having lower manufacturing costs and new features as compared with their competitors (Vinayachandran & Ambily, 2020). For instance, scholars have argued that those enterprises having sufficient intangible resources and capabilities can easily acquire SCP over other enterprises having insufficient resources in the turbulent market (Ferreira et al., 2020; Khalique et al., 2020). SCA has two main dimensions namely DS and CLS (2020). Both the dimensions significantly spur financial performance (FP; (C.-Y. Chen et al., 2017; Kharub et al., 2019).

Manufacturing distinctive and dissimilar goods enable enterprises to grab a sustainable position in the dynamic market which in turn enhances FP (Bayraktar et al., 2017). In a similar vein, lessening several costs using CLS—such as acquire raw material at a lower cost—upsurges enterprises’ growth (Bayraktar et al., 2017). In recent waves, scholars found positive significant nexus between SCA—such as DS and CLS—and sustainable performance (Grahovac & Miller, 2009; Sigalas & Papadakis, 2018).

The Mediating Role of SCA Between IC and SG

The CA is not un-ambiguously defined in the literature, as the definition varies from industry to industry and profession to profession; however, generally speaking, the CA is the capability of the organizations to survive in a long run and become more profitable in the longer viz-a-viz the competitors and other organizations operating in the same organizational field (Porter & Millar, 1985). Similarly, the variant definition of the CA is also available, such as if an organization successfully devises a strategy for the value creation for its stakeholders it gains the edge of being competitive viz-a-viz their competitors (Barney, 1991). The later views focus more on the intellectual capacity of the organization which helps them achieve an advantage over its competitors through the implementation of the cutting edge technologies for the performance of the organization, which other organizations failed to implement.

IC is considered to be an important antecedent of the sustained CA and the value creation, particularly, in the context of SMEs which are characterized as having limited resources (Ayuso et al., 2018; Ling, 2013). Collectively, IC comprises the talents of the employees, the intellectual capabilities, the knowledge they possess, and the prevalence of the requisite skills and the number of patents registered both by individuals as well as by the organizations (Ayuso et al., 2018; Djuric & Filipovic, 2015), which are also significantly associated with the performance of the SMEs in the developing countries (Cleary & Quinn, 2016). In this context, Pakistan, being a developing country, the SMEs also experienced a high level of returns from the IC (Khalique et al., 2015). Besides, the evidence also supports the relationship between the IC and the CA while considering the former as a multidimensional construct (Ling, 2013; Zakery & Afrazeh, 2017).

According to S. Z. Khan, Yang, and Waheed (2019), IC is considered a less expensive intangible resource in emerging economies such as Pakistan and China. Hence, those enterprises gain an SCP in such turbulent markets that have a satisfactory level of IC (Z. Wang et al., 2016). IC is a less expensive source that supports enterprises in costs reduction (e.g., gain CLS; Zakery & Saremi, 2020), and IC is distinctive knowledge and skills which are inimitable and cannot be copied easily by other enterprises and become a source of differentiation advantage that in turn spur enterprises growth (Xu & Wang, 2018). Firms need to gain a CA as they can in turn significantly improve performance (S. Z. Khan, Yang, & Waheed, 2019). For instance, Jain et al. (2017) claimed that IC significantly contributes to SCA and firm’s return on assets (ROA). However, Khattak and Shah (2020) argued that IC indirectly contributes to performance while significantly and directly contributing to CA. They further concluded that SCA significantly and partially mediates the nexus between IC and small firm performance. In a similar vein, S. Z. Khan, Yang, and Waheed (2019) also confirmed the partial mediating role of SCA between IC and FP.

SCA (CLS and DS) does not come inevitably by offering distinctive goods but it emanates from the capabilities (e.g., IC) that harvest them to improve firm competitiveness and success (Mubarik et al., 2019). The intangible capabilities of a manager (e.g., IC) facilitate the firm to acquire resources that contribute positively to CLS and DS (Wahyuni et al., 2020). To summarize, Torres et al. (2018) scrutinized that the paths between the dimensions of IC and organizational performance are mediated by CA, endorsing the claim of the mediating role of SCA between IC and SG. Therefore, drawing on these studies, we develop our hypotheses as follows:

The research model is shown in Figure 1.

Research model.

Method

Research Design, Sample, and Population

This research assesses the importance of IC dimensions—human capital, SC, and RC in SCA—differentiation and cost leadership based and in SG. Furthermore, the mediating role of each CA between IC and SG is also tested in this study. The nature of the research is quantitative and a deductive approach is followed. Using a simple random sampling technique, we selected 90 listed firms from China and 90 listed firms from Pakistan for a period of 6 years from 2013 to 2018. We used the sample size of 90 companies because of the unbalance data of other firms. In other words, we only found 90 firms whose data relevant to the model are available as balance. Chinese firms’ data were obtained from China Stock Market and Accounting Research and Shanghai Stock Exchange, and Pakistani firms’ data were gathered from the Pakistan Stock Exchange (PSE) and State Bank of Pakistan (SBP). The data are shown in a million figures.

Measurement of the Variables

IC

In this study, we used three dimensions of the IC that are explained below.

In general, the most used measure is the Value Added Intellectual Coefficient (VAIC) Model (Maji & Goswami, 2016; Pulic, 2000). VAIC model is used to measure the IC and its components. The model tells about the sum of Intellectual Capital Efficiency (ICE) and Capital Employed Efficiency (CEE). In general, ICE contains Human Capital Efficiency (HCE) and Structure Capital Efficiency (SCE).

VAIC model is discussed below:

The model first needs Value Added (VA) which can be got from the difference between OUT and IN.

OUT demonstrates total revenue produced by a company in a year. IN is the sum of all operating expenses incurred by the business in generating revenue (except employee cost which is considered as a value-creating entity).

So, VA algebraically presented as,

Here, EBIT = Earnings Before Interest and Tax, D = Depreciation, A = Amortization (if any) and EC = Employee Cost.

Therefore, HCE, SCE, and CEE can be calculated through the following equation:

HC = Overall salary expenditure of a firm (Bontis et al., 2007).

Here again, SC = VA – HC.

CE = the book value of net assets of a firm.

However, for clarity and description of each variable, we followed Sardo. Serrasqueiro and Alves (Sardo et al., 2018) used the following proxies for each dimension of IC:

HC measured with the natural logarithm of staff costs.

SC measured with working capital turnover.

RC measured with revenues growth.

SCA

This study used two CA that are differentiation based and cost leadership based. These two strategies that are suggested by Porter (Porter & Strategy, 1980) are mostly used in the existing literature.

Differentiation-based CA

To measure the DS, we used the following components based on existing studies (Balsam et al., 2011; Banker et al., 2014). The main theme of this study is to invest in such types of activities that help firms in differentiating their products and services from their competitors and industry rivals.

SG&A/sales: Investment in expensive activities such as selling, general, and administrative expense (marketing, advertising, product distribution, customer services etc.) to total sales.

R&D/sales: Investment in R&D activities to total sales.

Sales/COGS: Total sales to cost of goods sold.

Cost-based CA

SALES/CAPEX: Total sales to capital expenditures.

SALES/P&E: Total sale ratio to book value of plant and equipment.

EMPL/ASSETS: No. of employees to total assets.

SG performance

The SG rate changes in equity scaled by beginning-of-period equity. The most used formula for the SG is discussed.

P denotes the profit margin (profit scaled by total sales), A denotes the asset turnover ratio (total sales scaled by total assets), T denotes the leverage factor (total assets scaled by end-of-period equity), and R denotes the retention ratio (retained earnings scaled by profit).

Econometric Equations/Algebraic Model

The algebraic model of the research is discussed below:

β0 is slope-intercept and β1, β2, β3, β4, and β5 symbolize expected coefficients.

Data Analysis and Results

We analyzed data through EVIEWS 9. However, first, we performed the statistical tests: descriptive statistics, normality, multicollinearity, and correlation through SPSS.

Descriptive Statistics

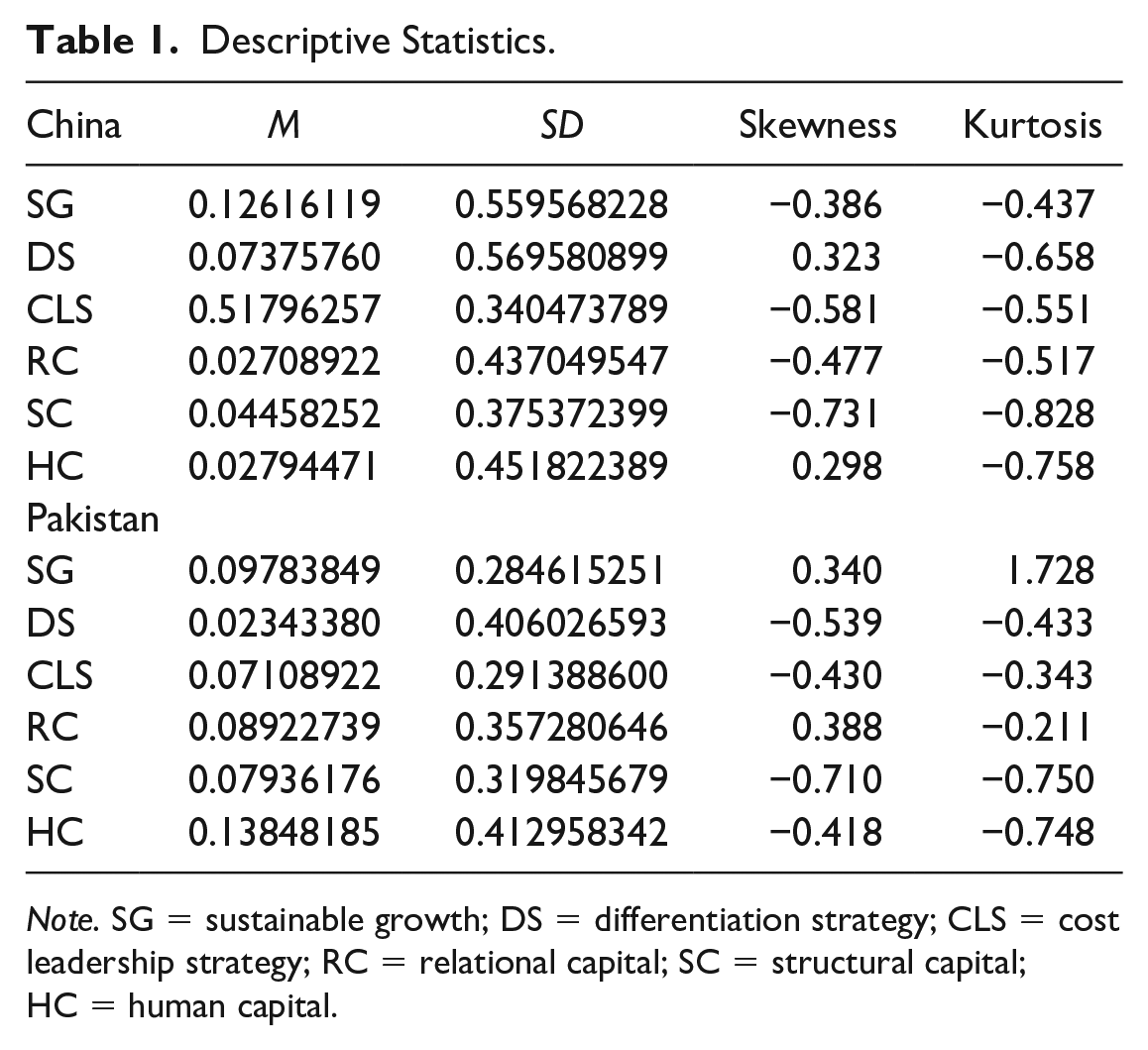

Table 1 illustrates the descriptive statistics of the variables where mean, standard deviation (SD), and normality of both data set have been discussed. It displays that in the data set of Chinese firms, CLS has the highest M value 0.52 and the lowest M value is of RC 0.027. In Pakistani firms, human capital has the highest M value 0.14 whereas DS has the lowest M value 0.023. SD of both countries move in a normal direction, and a minor significance difference is reported. Both data sets are normal as none of the factors has its skewness and Kurtosis values greater than the cutoff ±1 (George, 2011).

Descriptive Statistics.

Note. SG = sustainable growth; DS = differentiation strategy; CLS = cost leadership strategy; RC = relational capital; SC = structural capital; HC = human capital.

Multicollinearity

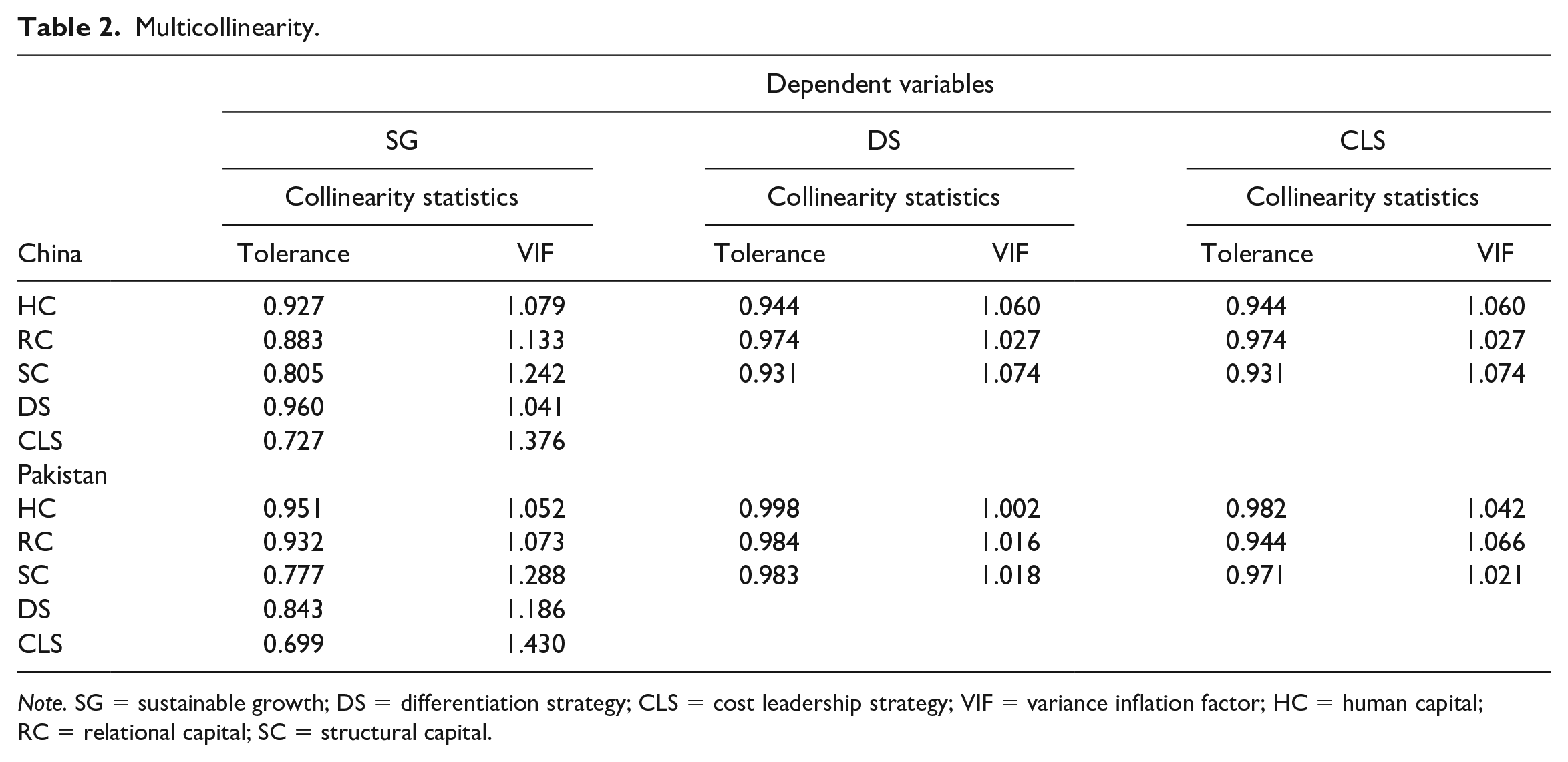

To check the problem of multicollinearity in the data set, we executed the Variance Inflation Factor (VIF) in SPSS that have been described in Table 2. We checked the influence of IC dimensions—human capital, SC, and RC—on SG, DS, and CLS and also the influence of DS and CLS on SG. We confirmed the absence of multicollinearity in both data sets as none of the factors has a VIF value above 3, and all the factors have their tolerance values greater than 0.10.

Multicollinearity.

Note. SG = sustainable growth; DS = differentiation strategy; CLS = cost leadership strategy; VIF = variance inflation factor; HC = human capital; RC = relational capital; SC = structural capital.

Correlation

Pearson’s correlation coefficient has been used to examine the relationship between constructs of the study. The correlation coefficient values of all constructs for both China and Pakistan are present in Table 3. The correlation results for China indicates that human capital (r = .462, p < .01), RC (r = .235, p < .01), SC (r = .242, p < .01), DS (r = .177, p < .01), and CLS (r = .282, p < .01) are significantly associated with SG. Similarly, human capital (r = .110, p < .01), RC (r = .106, p < .01), and SC (r = .093, p < .05) are significantly related with DS. In addition, human capital (r = .209, p < .01), RC (r = .339, p < .01), and SC (r = .417, p < .01) are significantly linked with CLS.

Correlations.

Note. HC = human capital; RC = relational capital; SC = structural capital; DS = differentiation strategy; CLS = cost leadership strategy; SG = sustainable growth.

Significant at p value .05.

Significant at p value .01.

In case of Pakistan, the correlation coefficient values indicate human capital (r = .102, p < .01), RC (r = .519, p < .01), SC (r = .196, p < .05), DS (r = .228, p < .01), and CLS (r = .363, p < .01) are also significantly related with SG. In similar vein, human capital (r = .087, p < .05), RC (r = .143, p < .01), and SC (r = .311, p < .05) are significantly related with DS. In addition, human capital (r = .205, p < .01), RC (r = .246, p < .01), and SC (r = .439, p < .01) are significantly linked with CLS.

Testing Hypotheses

To examine the mediating role of CLS and DS between IC dimensions (human capital, SC, and RC) and SG, panel regression was applied. Panel data regression has been used because the nature of data is a combination of time series and cross-section data. To test the hypotheses through panel regression, first, the data were scrutinized for the selection of an appropriate model (common-effect model, fixed-effect model, or random-effect model). The F-statistics value (p < .05) indicates that the fixed-effect model was appropriate for data analysis instead of the common-effect model as recommended by Gujarati (Gujarati & Porter, 2004). Furthermore, the significant results of the Housman test (chi-square statistic > 2, p < .05) also suggested that the fixed-effect model is appropriate instead of the random-effect model. Hence, the fixed-effect model was considered for data analysis and testing the hypotheses.

To substantiate the hypothesis of the study, Baron and Kenny’s (1986) method has been used. Baron and Kenny (1986) suggested performing mediation analysis in four separate steps to obtain more accurate results. To follow the Baron and Kenny (1986) procedure of mediation in the first step, the influence of interdependent variables (IVs) on the dependent variable (DV) has been examined. In the second step, the influence of IVs was regressed on mediators. In the third step, the mediators were regressed on DV. In the fourth step, the influence of IVs on DV was checked after controlling for the effect of a mediator.

The results of first step are reported in Table 4 for both countries such as China and Pakistan. The result of the first step indicates that for China all the three dimensions of IC such as human capital (β = .502, t = 14.6, p < .05), SC (β = .159, t = 3.95, p < .05), and RC (β = .105, t = 3.14, p < .05) have significant influence on SG. Similarly in Pakistan context, all the three dimensions of IC namely human capital (β = .075, t = 3.26, p < .05), SC (β = .153, t = 5.18, p < .05), and RC (β = .395, t = 14.27, p < .05) significantly contribute to the SG of Pakistani firms. This result favored H1, H2, and H3 for both nations.

The results of second step are reported in Tables 5 and 6. In this step, all the dimensions of IC were regressed on DS and CLS. The results of Table 5 revels that IC dimensions namely human capital (β = .592, t = 2.08, p < .05), SC (β = .345, t = 1.39, p < .05), and RC (β = .223, t = 8.05, p < .05) of Chinese firms have significant influence on DS. As compared with China in the context of Pakistan, two dimensions of IC namely human capital (β = .111, t = 3.61, p < .05) and SC (β = .347, t = 8.80, p < .05) have significant influence on DS, whereas RC (β = .058, t = 1.59, p > .05) has insignificant influence sales on DS. This result supports H4 and H5 for both nations (China and Pakistan). In addition, this result supports H6 in Chinese context and does not support H6 in Pakistani context.

The Impact of IC Dimensions on SG.

Note. IC = intellectual capital; SG = sustainable growth; RC = relational capital; HC = human capital; SC = structural capital.

The Impact of IC Dimensions on DS.

Note. IC = intellectual capital; DS = differentiation strategy; HC = human capital; RC = relational capital; SC = structural capital.

IC Dimensions on CLS.

Note. IC = intellectual capital; CLS = cost leadership strategy; HC = human capital; RC = relational capital; SC = structural capital.

The results of Table 6 depict that only human capital (β = .142, t = 3.47, p < .05) significantly influence CLS whereas the SC (β = .061, t = 1.29, p > .05) and RC (β = .054, t = 1.37, p > .05) have insignificant impact on DS of Chinese firms. However, in case of Pakistan, human capital (β = .176, t = 7.07, p < .05), SC (β = .372, t = 11.60, p < .05), and RC (β = .129, t = 4.31, p < .05) significantly contribute to the CLS. These results substantiate H7 for both nations (China and Pakistan). In addition, this result also substantiates H8 and H9 for Pakistan but does not substantiate H8 and H9 in the context of China.

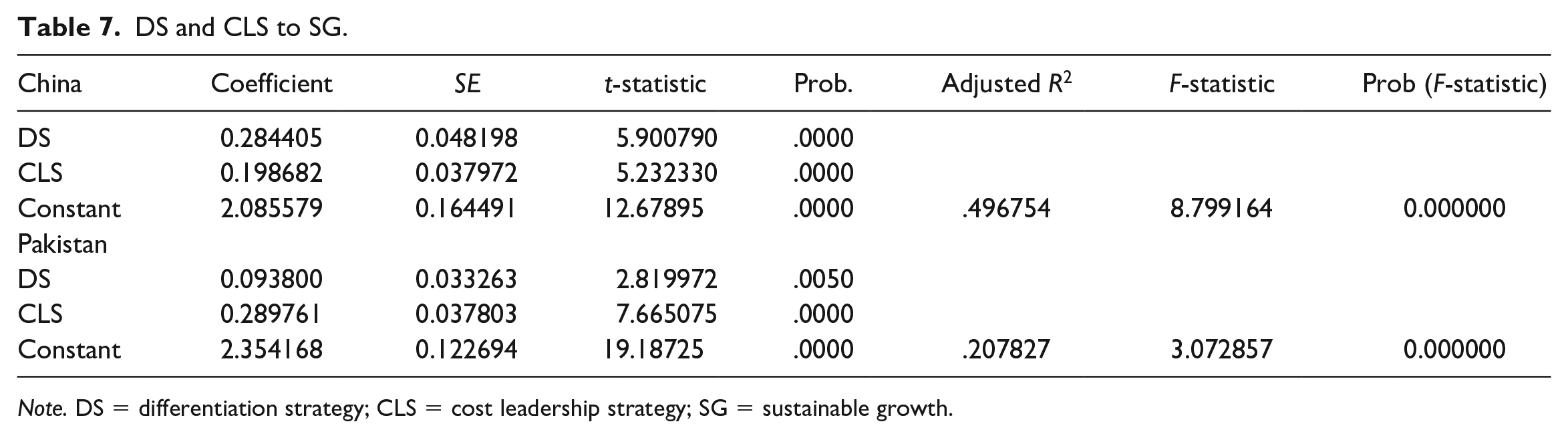

The results of third step of mediation were reported in Table 7. The results show that both DS (β = .284, t = 5.90, p < .05) and CLS (β = .198, t = 5.23, p < .05) strategy significantly contributes to SG of Chinese firms. In similar vein, DS (β = .093, t = 2.81, p < .05) and CLS (β = .289, t = 7.66, p < .05) have significant influence on SG of Pakistan firms. This result favored H10 and H11 for both nations (China and Pakistan).

DS and CLS to SG.

Note. DS = differentiation strategy; CLS = cost leadership strategy; SG = sustainable growth.

The results of the fourth step were presented in Tables 8 and 9. First, the mediating role of DS has been investigated between IC dimensions and SG for both nations (China and Pakistan). The results of Table 8 reveals that in presence of DS, human capital (β = .490, t = 2.10, p < .05) and SC (β = .090, t = 14.39, p < .05) significantly influence SG whereas RC (β = .061, t = 1.75, p > .05) insignificantly contributes to SG in the context of China. However, for Pakistan firms, human capital (β = .093, t = 2.81, p < .05), SC (β = .093, t = 2.81, p < .05), and RC (β = .093, t = 2.81, p < .05) have significant influence on SG in presence of DS. These results partially support H12 and H13 for both nations (China and Pakistan). Furthermore, these results partially support H13 in Pakistani content and did not support H13 in China’s context. Second, in the fourth step, the mediating role of CLS has been examined between all the dimensions of IC and SG for both nations (China and Pakistan). The result of Table 9 indicates that human capital (β = .479, t = 14.05, p < .05), SC (β = .149, t = 3.76, p < .05), and RC (β = 2.92, t = 2.81, p < .05) have significant impact on SG after controlling for the effect of CLS. These results suggested that CLS partially mediates the relationship between IC dimensions and SG in the context of China. Whereas in case of Pakistani firms, SC (β = .079, t = 2.48, p < .05) and RC (β = 13.45, t = 2.81, p < .05) significantly contribute to SG in presence of CLS whereas human capital (β = .040, t = 1.70, p < .05) insignificantly contributes to SG. These results suggested that CLS partially mediates the relationship between SC and RC with SG. Whereas CLS does not mediate the relationship between human capital and SG of Pakistani firms. These results partially support H15 and H16 for both nations, but H14 was not substantiated in the Pakistani context. The summarized results of the research are shown in Table 10.

Mediating Role of DS Between All the Dimensions of IC and SG.

Note. DS = differentiation strategy; IC = intellectual capital; SG = sustainable growth; RC = relational capital; SC = structural capital; HC = human capital.

Mediating Role of CLS Between All the Dimensions of IC and SG.

Note. CLS = cost leadership strategy; IC = intellectual capital; SG = sustainable growth; RC = relational capital; HC = human capital; SC = structural capital.

Hypotheses Remarks.

Note. SG = sustainable growth; DS = differentiation strategy; CLS = cost leadership strategy.

Robustness Checks

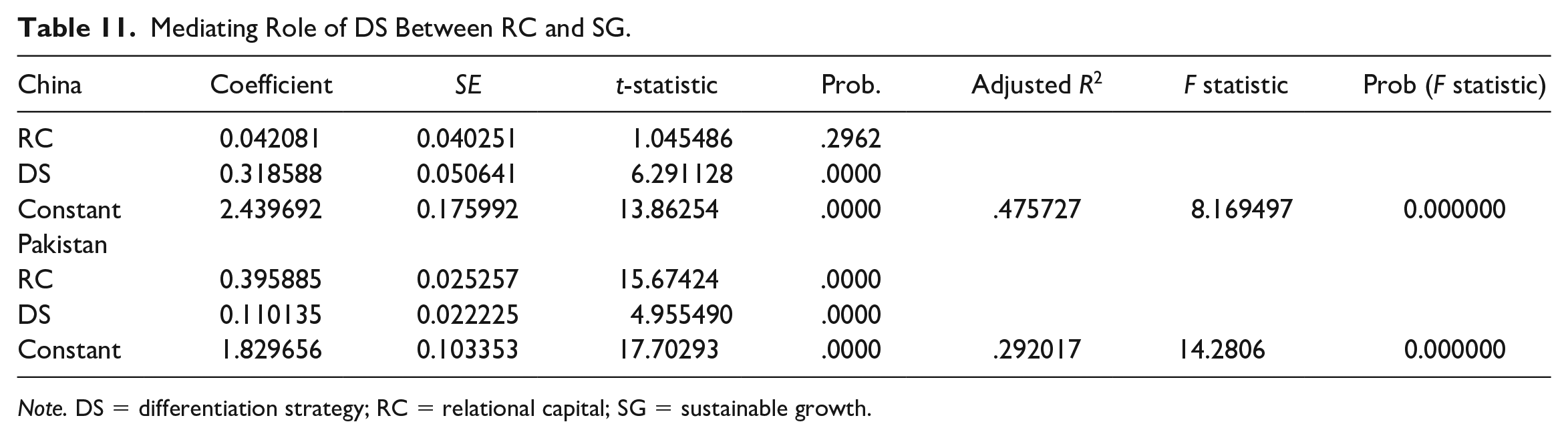

To authenticate the results first, we test the mediating role of DS between each dimension of IC and SG, and separate regression analysis was performed for each dimension. The results of Table 11 shows that the direct effect of RC on SG is insignificant (β = .042, t = 1.45, p > .05) for Chinese firms, whereas in the case of Pakistan, the direct effect of RC on SG becomes significant (β = .39, t = 15.67, p < .05) and which indicates that DS fully mediate the relationship between RC and SG in China while partially mediate the above relationship in Pakistan.

Mediating Role of DS Between RC and SG.

Note. DS = differentiation strategy; RC = relational capital; SG = sustainable growth.

The results of Table 12 reveal that both the direct effect and indirect effect of human capital on SG is significant for both nations (China and Pakistan), which shows that DS partially mediates the nexus of RC and SG in both nations.

Mediating Role of DS Between HC and SG.

Note. DS = differentiation strategy; HC = human capital; SG = sustainable growth.

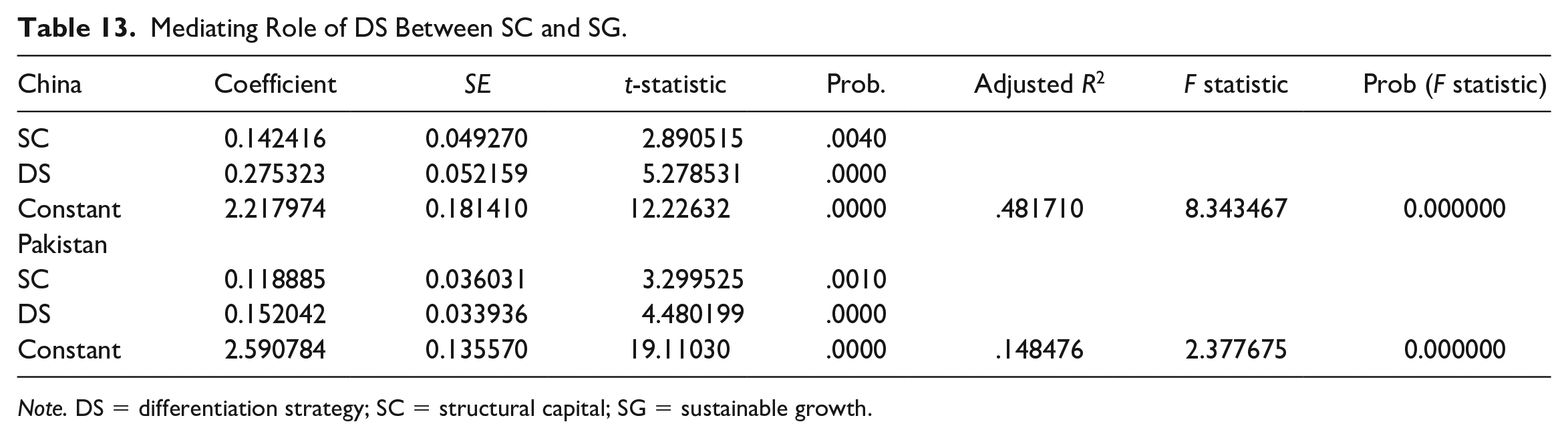

The results of Table 13 also depict that SC significantly influences SG both through the direct path and indirect path for both nations. This result indicates that DS partially mediates the relationship between SC and SG in both nations.

Mediating Role of DS Between SC and SG.

Note. DS = differentiation strategy; SC = structural capital; SG = sustainable growth.

Second, we examined the mediating role of CLS in each dimension of IC and SG, and separate regression analysis was performed for each dimension. The results of Table 14 portrayed that RC has a significant impact on SG both via direct path and indirect path for both nations. This result indicates that CLS partially mediates the relationship of RC with SG for both nations.

Mediating Role of CLS Between RC and SG.

Note. CLS = cost leadership strategy; RC = relational capital; SG = sustainable growth.

The results of Table 15 depict that both the direct path and indirect path of human capital on SG are significant which portrayed that CLS partially mediates the nexus of human capital and SG of both nations.

Mediating Role of CLS Between HC and SG.

Note. CLS = cost leadership strategy; HC = human capital; SG = sustainable growth.

The results of Table 16 shows that direct effect of SC on SG (β = 0.224, t = 4.98, p < .05) is significant for Chinese firms, whereas in case of Pakistan, the direct effect of SC (β = .053, t = 1.49, p > .05) become insignificant. These results portrayed that CLS partially mediates the relationship between SC and SG for China, whereas CLS fully mediates the relationship between SC and SG of Pakistani firms.

Mediating Role of CLS Between SC and SG.

Note. CLS = cost leadership strategy; SC = structural capital; SG = sustainable growth.

Discussion and Conclusion

This study tested the influence of each dimension of IC on SG with the mediating role of each competitive strategy named CLS and DS. Although the relationship between IC and performance as well as between IC and SCA has been tested in the literature, the venture growth has been missed from the literature. Moreover, in particular, the mediating role of each strategy between each dimension of IC and SG has been neglected especially in emerging economies. The present study has focused on the missing zone and aims to contribute to the RBV theory in this way. For instance, the RBV theory (Barney, 1991) has been tested by several studies in emerging and developed markets. However, this research tested the theory with separate dimensions of IC, SG, and SCA. We revealed that all the dimensions of IC are very important for SG and both of the strategies in emerging markets. To put it another way, this research favors the theme of RBV theory and confirms that intangible factors, for example, the dimensions of IC are very useful SCA and superior performance. Hence, the factors can be significant predictors of RBV theory. Our model is related to previous studies but in fact, the relationships tested in this research are unique and new as compared with other studies. For instance, this research advances our understanding of the RBV theory concerning each dimension of IC and CA for profitability and performance.

We found that all the dimensions of IC are very important for high SG which favored the posited H1 to H3. Our findings are in line with several other studies such as Kadir et al. (2018) and McDowell et al. (2018), who revealed a significant positive association between the dimensions of IC and performance. In addition, a recent study conducted by Mukherjee and Sen (2019a) confirms that IC is a significant driver of SG in emerging firms. Favoring this notion, Sardo and Serrasqueiro (2018) tested the relationship among IC, growth opportunities, and financial performance in 14 Western countries and revealed that ventures having a high level of IC have a greater chance of growth opportunities. Our findings strongly favor Xu and Wang (2018), who concluded that physical capital, human capital, and RC significantly contribute to SG of Korean companies.

Our findings revealed that all the dimensions of IC—human capital, SC, and RC—significantly influence DS in both nations except RC which does not significantly impact DS in Pakistan. Our findings relate to Y.-S. Chen (2008), who claimed that human capital and SC provide CA to Chinese firms. The findings oppose the notion of C.-H. Wang (2014), who revealed that RC has a significant positive influence on CA. They suggested that RC is attractive and enables the firm to sustain itself in the market for a longer period. However, our findings do not fully support the results of Ahmad and Ahmed (2016), who revealed that IC is a significant driver of CA in Pakistani firms. Considering the importance of IC in CLS, we found that all the dimensions of IC have a significant influence on CLS in Pakistani firms, whereas only human capital plays a significant role in Chinese firms. It describes that CLS in Chinese firms can be gained only through human capital. Unlike Y.-S. Chen (2008) who claimed a significant relationship between all the dimensions of IC—human capital, RC, and SC—and CA in Chinese firms, our findings show slightly inverse results. These findings contradict the study of Yaseen et al. (2016), who demonstrate that RC and SC significantly explain variation in CA as compared with human capital. However, in general, the relationship between IC and CA is discussed as significant and positive in the existing studies (S. Z. Khan, Yang, & Waheed, 2019).

Our findings revealed that both the strategies—DS and CLS—have a significant positive influence on SG of firms in both nations that supported H10 and H11. Our findings are similar to W. Liu and Atuahene-Gima (2018) and Zehir et al. (2015), who scrutinized that both DS and CLS are very vital for superior performance. Although the exact relationship between competitive strategy and SG is not yet tested, similar findings claim that both the strategies are very important for superior performance (e.g., Sigalas & Papadakis, 2018). We reveal that both the strategies—DS and CLS—play a significant role in the enhancement of SG of firms in China and Pakistan.

Our study revealed that DS partially mediates the relationship between all the dimensions of IC and SG in Pakistani firms, whereas it only plays a full mediation role between RC and SG of Chinese firms. It argues that Chinese firms first build their differentiation-based advantage through RC, which in turn contributes to their SG. However, all the dimensions play a similar role in the creation of CA and enhancement of SG in Pakistani firms. On the other hand, CLS plays a partial mediating role between all the dimensions of IC and SG in Chinese firms, whereas it fully mediates only the relationship between human capital and SG in Pakistani firms. It can be argued that human capital is very crucial for creating low-price products in Pakistan that can help firms in gaining SG. Similarly, in the context of Pakistani firms, our findings match the results of Khattak and Shah (2020), who claimed a mediating role of CA between IC and SMEs performance. However, overall, our findings favor Kamukama et al. (2011), who scrutinized a partial mediating role of CA between IC and firm performance. These findings are parallel with the outcomes of S. Z. Khan, Yang, and Waheed (2019), who found that SCA partially mediates the nexus of IC and firm performance. Similarly, the results of this study are consistent with Khattak and Shah (2020), who concluded that CA partially mediates the relationship between IC and SMEs performance. However, our results are partially related to Rochmadhona et al. (2018), who revealed the fully mediating role of CA between IC and financial performance in five Association of Southeast Asian Nations (ASEAN) economies.

Implications for Practices

This research suggests several significant implications for CEOs, executives, managers, and policymakers. We confirmed that IC is vital for SG of firms operating in both nations: China and Pakistan. Therefore, top managers and CEOs need to focus on IC to enjoy SG in the turbulent markets. However, considering the importance of each dimension of IC in DS, our findings reveal that all the dimensions of IC are important for DS in Chinese firms but only RC is not a significant driver of DS in Pakistani firms. Hence, top managers need to care for the RC to gain the advantage of differentiation in products and services. In terms of CLS, we found that all the dimensions of IC are useful for CLS in Pakistani firms, whereas only human capital plays a significant role in Chinese firms. Hence, top managers of Chinese firms need to give enough attention to the human capital to reduce their operational, material, and administrative costs (e.g., to gain CLS). Both the strategies—DS and CLS—are very advantageous for SG in Chinese and Pakistani firms. As pointed by the researchers (Chung & Kuo, 2018; Lechner & Gudmundsson, 2014), DS and CLS are the significant drivers of superior financial performance in emerging and developed economies. Favoring the notion, studies from China (e.g., Ge & Ding, 2005; K. U. Khan, Xuehe, Atlas, & Khan, 2019) and Pakistan (S. Z. Khan, Yang, & Waheed, 2019; Khattak & Shah, 2020; Shah & Ahmad, 2019) have confirmed the significant positive relationship between CA and performance. We scrutinized a significant relationship between SCA and SG in both firms that gives worthy implications to policymakers. For instance, managers planning for high SG should focus on SCA. However, SCA does not come directly, managers need to merge adequate resources for it. This research suggests firms spend time on IC as compared with other drivers. Because as pointed out by Ying et al. (2019), intangible resources are better than tangible resources for SCA in emerging economies such as Pakistan. We also recommend a similar suggestion for both Chinese and Pakistani firms to focus on IC. Another reason for emphasizing IC is that firms in emerging economies have a lack of resources to invest in tangible means (S. Z. Khan, Yang, & Waheed, 2019). Hence, it shifts their attention toward intangible factors over tangible ones. To put the implications in further detail, Pakistani firms should improve their RC to gain DS. Chinese firms should emphasize the betterment of structural and RC to seize a cost leadership position in the market. The implications are not only useful for emerging firms but also other developing economies in Asia and Europe can replicate the implications to secure SCA and high SG.

Limitations and Roadmap to Future Research

Despite having several limitations, this research is having several limitations that can be addressed in future studies. For instance, we compared the firms operating in two emerging economies named China and Pakistan but have ignored to collect evidence related to other emerging economies and developed economies. We did not analyze and distinguish between the industries such as oil, sugar, textile, and imports if the IC dimensions play a different role in SG in these firms. Hence, we recommend to test and compare the importance of IC dimensions in various industries. Moreover, we test the mediating role of the two strategies between IC dimensions and SG. We recommend considering ROA, return on owner’s equity (ROE), and return on investment (ROI) as DVs to clear the significance of the factors. We considered only three dimensions of IC named human capital, SC, and RC in this study. However, the existing literature (e.g., Andreeva & Garanina, 2016; Inkinen, 2015) has suggested five dimensions with additions of organizational capital and customer capital. Hence, testing all these dimensions can give articulated insights. In addition, we only tested the mediating role of SCA in this study. However, recent studies have claimed that other factors can influence the relationship between IC and performance. For instance, Li et al. (2019) claimed that IC is significantly related to knowledge sharing and innovative performance. We recommend testing the mediating role of innovative performance if it can mediate the relationship between the dimensions of IC and SG in both nations. Indeed, IC and its dimensions have been tested in many studies. However, considering the claim of Demartini and Trucco (2016), IC is associated with audit risk in business industries. Hence, we suggest testing if the dimensions of IC influence risk management practices in business industries that in turn can influence their performance.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.