Abstract

This paper evaluates the impact of local and external economic uncertainty shocks on China’s exchange market pressure from a time-varying perspective. We first construct a simple behavioral model to provide some economic background for our empirical analysis. The model identifies two channels, namely market sentiment and market demand, through which economic uncertainty has a time-varying impact on exchange market pressure. Notably, we calculate a new exchange market pressure index for China by considering China’s practice. Using the economic policy uncertainty index as a proxy for economic uncertainty and our new estimates of China’s exchange market pressure, we employ a novel TVP-VAR model controlling for over-parameterization to a monthly dataset from January 2001 to October 2020 to analyze the impact of China’s and U.S. economic policy uncertainties on China’s exchange market pressure. Our empirical findings robustly show that an upsurge in U.S. EPU is followed by appreciation pressure of the RMB against the dollar, while a hike in China’s EPU triggers devaluation pressure on the RMB. In addition, the impact of economic policy uncertainty has considerable time variation in magnitude, especially after mid-2011, showing a trade-off mechanism between the effects of domestic and foreign economic uncertainties on China’s exchange market pressure. Moreover, we attribute the time-varying features to the changes in China’s dependence on the U.S. and in the exchange rate flexibility. Finally, China should further improve the exchange rate flexibility, reduce its dependence on the U.S. and develop a more diversified currency basket in the exchange rate formation mechanism.

Introduction

There is an anecdotal story about globalization that economic activity in an open economy is primarily driven by foreign shocks, while domestic shocks are reflected in its currency value (Nilavongse et al., 2020). Since economic uncertainty is a representative shock that conveys information about overall economic conditions, various attempts have been made to assess the impact of economic uncertainty on the exchange rate, see Kido (2016), Simo-Kengne et al. (2018), Nasir and Morgan (2018), Nilavongse et al. (2020), among others. Granted that most of the literature argues that the exchange rate is affected by local and external uncertainties, but Simo-Kengne et al. (2018) and Nasir and Morgan (2018) highlight that foreign uncertainty plays a small role in driving the exchange rate.

Theoretically, economic uncertainty is the primary source of risk of holding a currency (Hu, 1997). Elevated economic uncertainty can make it challenging to predict the exchange rates (Beckmann & Czudaj, 2017a, 2017b), leading agents to reduce their demand for the currency or raise the risk premium (Taylor, 1989), thereby putting pressures on the exchange rate to depreciate or appreciate. Ideally, these pressures will be fully reflected in the exchange rate movements for the countries with floating exchange rate regimes. However, this would not happen in the economies like China and Japan, where the central banks are known for intervening in the foreign exchange market (hereafter FX market).

In China, government intervention in the FX market is a stylized fact (Das, 2019; Wang et al., 2020). Accordingly, since the exchange rate is managed to change, depreciation or appreciation pressures on the renminbi against other currencies cannot be manifested totally in the exchange rate movements. Thus, uncertainty shocks may have a negligible impact on the realized exchange rate in China owing to central bank intervention, although it has been argued that market expectations are affected by the uncertainty shocks (Beckmann & Czudaj, 2017a, 2017b; Ter Ellen et al., 2013).

Naturally, when analyzing the impact of uncertainty for the economies that resort to FX intervention, the realized exchange rate needs to be restored to incorporate government intervention. A well-known measure of such an exchange rate recovery is the exchange market pressure (hereafter EMP) index. While most previous studies have focused on the realized exchange rates and exchange rate expectations, the impact of economic uncertainty on EMP has been less touched upon, except for two path-breaking works by Olanipekun, Güngör et al. (2019) and Olanipekun, Olasehinde-Williams et al. (2019). They, however, only aim at the causal relationships between economic uncertainty and EMP. Two recent studies by Olasehinde-Williams and Olanipekun (2020) and Olanipekun and Olasehinde-Williams (2021) provide empirical evidence that U.S. uncertainty affects EMP in some emerging market countries and African economies, respectively. Nonetheless, these two studies do not consider the impact of domestic uncertainty on EMP, which may be jointly motivated by local and external factors, as derived from the theory of exchange rate determination (Mussa, 1984). A similar issue also exists in the study by Liu (2020), who explores the impact of domestic uncertainty shocks on China’s EMP, overlooking the potential effects exerted by foreign uncertainty. However, because of China’s high dependence on the United States, China’s financial markets may endure the significant impact of uncertainty shocks from the United States (Gupta et al., 2020; Liu, 2021). Against this backdrop, we attempt to fill this gap by inspecting China’s EMP dynamics following unexpected rises in domestic and foreign economic uncertainties.

In this paper, we explicitly assess the role of economic uncertainty in governing EMP with China’s monthly data. China has been pursuing the globalization of the renminbi and building a responsible national image. Hence, maintaining the exchange rate stability is a pressing concern for China. As the exchange rate stability is critical to the macroeconomy and plays a crucial part in the Chinese government’s objectives (Das, 2019), evaluating the impact of economic uncertainty on EMP would benefit the Chinese policymakers to better understand the underlying causes of exchange rate fluctuations.

Specifically, as documented in Pástor and Veronesi (2013) and Krol (2014), the impact of economic uncertainty on EMP might be state-dependent, and thus motivated by Bartsch (2019), we construct a simple behavioral model with heterogeneous agents to demonstrate that the impact of economic uncertainty on EMP, mainly through the market sentiment and market demand channels, evolves over time.

Importantly, as our analytical result indicates, it is necessary to consider nonlinearity when modeling EMP and economic uncertainty. First, since the FX market has been surveyed as dominated by heterogeneous agents using different trading strategies (de Jong et al., 2010; Ter Ellen et al., 2013), exchange rate dynamics are often interpreted as nonlinear processes in the literature; see Sengupta and Sfeir (1998), Mahajan and Wagner (1999), Imbs et al. (2003), Nakagawa (2010), among others. Second, the impact of economic uncertainty shocks may be nonlinear due to changing dynamics, policy regimes, and economic shocks (Mumtaz & Theodoridis, 2018). Third, China has undergone many dramatic phases over the past decades (Chang et al., 2016) and has substantially reformed its exchange rate system, raising the possibility of potential nonlinearities and multi-equilibria (Liu, 2021). Therefore, it is reasonable and desirable to apply a nonlinear model when exploring the relationship between the foreign exchange market and the macroeconomy.

Theoretically, any nonlinear model can be approximated by a time-varying parameter (TVP) model (Granger, 2008). Given the appeal of TVP models, a few studies regarding exchange rate dynamics have utilized TVP-VAR models to examine the effects and causes of exchange rate movements; see Choi et al. (2018), Nasir and Morgan (2018), Zheng et al. (2019), Nasir and Vo (2020), and others. However, assuming that all model parameters are time-dependent increases model complexity and may suffer from the “curse of dimensionality” of over-parameterization, which would eventually bias the estimates. Recent studies have shown their concerns over this issue; see, for example, Koop and Korobilis (2013), Eisenstat et al. (2016), Huber et al. (2019), Chan et al. (2020). On this account, using a monthly dataset running from January 2001 to October 2020, we conduct our empirical study with a TVP-VAR model by combing the approach developed by Eisenstat et al. (2016) to control for over-parameterization.

Nevertheless, an essential issue that setting a proper proxy for economic uncertainty arises in our empirical study. Currently, there are three optional proxies for economic uncertainty in the literature; the news or reports-based economic policy uncertainty index (EPU) (Baker et al., 2016), the real data-based macroeconomic uncertainty index (Jurado et al., 2015), and the survey-based uncertainty index (Bachmann et al., 2013). Comparatively, the news-based uncertainty index is computed by text-mining newspaper reports available equally to every market participant. Therefore, the EPU index would catch more the uncertainty caused by specific events (Shin et al., 2018), as these events tend to evoke public or political concerns about the economic consequences, leading to an increase in the frequency of economic-relevant news and thus a higher EPU. In addition, the news reports used to construct EPU are usually easy to understand for market participants and may sometimes signal policy stance, especially for countries where the government controls public media in some way. Davis et al. (2019) construct an EPU index for China by retrieving news reports from two influential newspapers circulating in mainland China, namely the People’s Daily and the Guangming Daily. Since these two government-run newspapers are the foremost government mouthpieces in China (Qin et al., 2018), market participants may translate an upsurge in the frequency of economic-relevant coverage into a rise in economic uncertainty and policy concerns. Therefore, in this paper, we use EPU as a proxy for economic uncertainty.

Additionally, as the largest member holding dollar assets, China has been witnessed as a dollar-pegged country for a long time (Tervala, 2019), even though moving toward a more flexible exchange rate regime after the reform initiated in July 2005. Moreover, trading of the renminbi against the U.S. dollar dominates China’s onshore spot FX market, accounting for more than 95% of the overall FX transactions on average. Therefore, in our empirical section, we estimate a new EMP index of the RMB against the dollar by considering the contingent spending of FX reserves and the intervention through the counter-cyclical adjustment factor, which have been overlooked in most previous related studies, see, for example, Olanipekun, Güngör et al. (2019), Olanipekun, Olasehinde-Williams et al. (2019), and Liu (2020). To this end, we estimate a new EMP index for China using daily exchange rate data from August 11, 2015, when China authority announced adopting a new regime for formulating the central parity of the RMB/USD exchange rate, to October 30, 2020, the last trading day of our sample.

The empirical findings based on a monthly dataset for China from January 2001 to October 2020 show that a rising shock in U.S. EPU would trigger the appreciation pressure on the RMB against the dollar, while a hike in China’s EPU is followed by the devaluation pressure of the RMB against the dollar. Moreover, the magnitude of the EPU impact on EMP is found to be time-dependent. Specifically, the effect is relatively stable until mid-2011 but more volatile thereafter. As for the rationale for this time-varying impact, we attribute it to changes in China’s dependence on the U.S. and increased exchange rate flexibility. Further, the empirical evidence indicates a trade-off mechanism between the effects of China’s and U.S. economic policy uncertainties on China’s EMP.

Our marginal contribution to the growing literature is that we focus on the time-varying impact of local and external economic uncertainties on China’s exchange market pressure. Our work reaches a step closer to an understanding of how the FX market responds to the shocks originating from domestic and foreign economic uncertainties. First, unlike Kido (2016), Nasir and Morgan (2018), Huynh et al. (2020), Nasir (2020), Chen et al. (2020), among others, who center on the roles of uncertainty in the exchange rate dynamics, we attempt to explore the impact of uncertainty on China’s EMP. Since the RMB exchange rate remains under control, its fluctuations are less informative in revealing market pressures.

Second, as documented in The Economist (2020), China’s intervention in the FX market has become less pronounced in recent years, keeping FX reserves fairly intact. Therefore, a better index capturing exchange market pressure should consider the changes in FX reserves and the veiled measures as well. Consequently, we estimate a new and more accurate index representing China’s exchange market pressure by considering the occasional expenditure of FX reserves and the intervention implemented in recent years via the counter-cyclical adjustment factor. Doing so distinguishes our paper in a significant way from several previous studies, for example, Olanipekun, Güngör et al. (2019), Olanipekun, Olasehinde-Williams et al. (2019), and Liu (2020), who all use slightly biased EMP estimates for China.

Third, in line with the theory of exchange rate determination, an exchange rate is determined concomitantly by domestic and foreign fundamentals, which have been well-documented to be affected by the uncertainty shocks (Bloom, 2009, 2014). Moreover, the uncertainty has been found to spill over globally, especially from advanced economies to less developed countries (Liu, 2021). Hence, in this paper, unlike Liu (2020), Huynh et al. (2020) and others who only consider the impact of local (or external) uncertainty, we assess the impact of China’s and U.S. uncertainties on China’s EMP in a consistent model.

Finally, as outlined above, we resort our analysis to a novel TVP-VAR model to incorporate potential nonlinearities. Liu (2020) also uses a classic TVP-VAR model to evaluate the impact of macroeconomic and financial uncertainties on EMP for China. Differently, considering the over-parameterization problem arisen from the time-varying specifications, we apply a typical TVP-VAR model with the stochastic model specification (SMSS) framework proposed by Eisenstat et al. (2016) to implement our empirical analysis.

The rest of our paper is arranged in the following manner. The next section briefly reviews the current literature relevant to this paper. Section 3 illustrates the economic intuition that economic uncertainty affects exchange market pressure through a simple behavioral exchange rate model. Section 4 describes the empirical methodology and the data we use. The empirical results and discussions, as well as robustness checks, are analyzed in Section 5. The last section concludes the whole paper and highlights the policy implications.

Related Literature

Overall, our work is related to two strands of the existing literature. One of these strands has been devoted to uncovering the link between economic uncertainty and exchange rate movements, whereby the focus, however, has been primarily on exchange rate returns. Another direction of the literature, which is the closest to our work, has been to assess the role of economic uncertainty in provoking pressures on the exchange rate.

The impact of economic uncertainty on exchange rate movements (both returns and volatilities) is increasingly well documented. Earlier studies find pricing effects of uncertainty on the currency risk premium; see, for example, Taylor (1989) and Hu (1997). Recently, there has been evidence for the roles of home and foreign uncertainties in explaining exchange rate movements in industrial and emerging economies, albeit analyzing mainly the spillovers of U.S. EPU. However, while the impact of home-grown uncertainty on exchange rate stability is well understood, the findings on the influence of foreign uncertainty are mixed. Compared to developed countries, Krol (2014) finds that exchange rate volatilities in emerging economies are less affected by U.S. EPU during recessions. The author attributes the explanation to the low level of financial openness of these economies to the United States. However, Huynh et al. (2020) offer empirical findings that exchange rate returns and volatilities of nine international currencies against the U.S. dollar are associated with U.S. trade policy uncertainty and global economic policy uncertainty. Chen et al. (2020) show that the EPU shocks resulting from the United States, Europe, and Japan have significant and asymmetric effects on the Chinese onshore RMB/USD exchange rate volatility. Nevertheless, the exchange rate volatilities of developed countries may be less exposed to U.S. uncertainty shocks. Nasir and Morgan (2018) and Nilavongse et al. (2020) highlight the significant devaluation effect of uncertainty locally from the UK on the sterling exchange rate. Notably, the latter and Simo-Kengne et al. (2018) reckon that foreign EPU is not a determinant of the exchange rate. In addition, Bartsch (2019) documents that UK EPU rather than U.S. EPU impairs the stability of the USD/GBP exchange rate.

However, a growing literature demonstrates the salient impact of foreign uncertainty on the exchange rate returns. Kido (2016) finds that the real effective exchange rate is negatively correlated with U.S. EPU for Australia, Brazil, Korea, and Mexico except for Japan, which exhibits a positive pattern, indicating that the yen plays as a safe-haven currency in the face of the U.S. uncertainty. Beckmann and Czudaj (2017a) further corroborate the yen’s safe-haven standing, though they concentrate on the aftermath of uncertainty on the exchange rate expectations. Addressing the spread between the onshore and offshore RMB/USD exchange rates, a recent paper by Li et al. (2020) documents a finding that a rise in their constructed composite EPU (extracted from the EPU indices of China and G7) widens the spread. In addition, a closely related literature in this line of research centers on the impact of relative uncertainty. Focusing on the relative value of difference or ratio of domestic EPU to external EPU, Balcilar et al. (2016), Christou et al. (2018), and Zhou et al. (2020) show that the relative EPU has much power in predicting exchange rate movements.

Another strand of the literature has attempted to dissect the relation between economic uncertainty and EMP. Olanipekun, Güngör et al. (2019) study a case of four BRIC countries but give somewhat puzzling results. In the paper, Olanipekun, Güngör et al. (2019) find the one-way causation from global EPU to EMP and mutual interplays between domestic EPU and EMP in all four countries, which is inconsistent with the results of the country-specific analysis. In particular, a bidirectional relation between global EPU and EMP and a one-way causality from EMP to EPU were found for China. Further, Olanipekun, Olasehinde-Williams et al. (2019) expand the sample to 20 countries and use four EMP measures as in Aizenman and Binici (2016) to conclude that domestic EPU and EMP are cointegrated in the long run. Most recently, Olasehinde-Williams and Olanipekun (2020) and Olanipekun and Olasehinde-Williams (2021) report more evidence about the causality from uncertainty to EMP for African economies and emerging market countries, respectively. Moreover, based on China’s data, Liu (2020) finds that macroeconomic uncertainty and financial uncertainty weaken (strengthen) EMP in a state of RMB appreciation (depreciation).

The recent study by Liu (2020) is undoubtedly the closest to ours. As we will do in our paper, Liu (2020) uses a TVP-VAR model to investigate the impact of China’s domestic uncertainty on EMP and the jump risk of the RMB/USD exchange rate. However, there are several differences. First, Liu (2020) jointly estimates the effects of macroeconomic uncertainty and financial uncertainty measures, estimated using the methodology developed by Jurado et al. (2015). Moreover, Liu (2020) models the impact of domestic uncertainty only, but it is necessary to incorporate foreign uncertainty since, in theory, the exchange rate is determined by domestic economic conditions and foreign counterparts simultaneously. Second, Liu (2020) directly uses the EMP measure estimated by Patnaik et al. (2017). A closer scrutiny of Patnaik et al. (2017)’s EMP estimates for China reveals that they have overlooked China’s intervention through adjusting the central parity rate in recent years and the irregular spending of FX reserves. However, we estimate a new Chinese EMP index by considering these practices. Third, Liu (2020) relies on a four-variable TVP-VAR model of uncertainty and market stability to achieve an empirical analysis. Nevertheless, as documented in Aizenman and Binici (2016), variables regarding market sentiment and market demand, as well as macroeconomic fundamentals, which might change in the light of economic uncertainty, could be important factors affecting EMP. Therefore, we will consider these variables to assess the impact of economic uncertainty on EMP. In doing so, we can better explore the underlying mechanism of how economic uncertainty shapes EMP. Finally, we differ markedly from previous studies in that we illustrate some economic background for our empirical study through a simple behavioral exchange rate model with heterogeneous agents.

A Simple Behavioral Exchange Rate Model

We extend the FX market model in Dieci and Westerhoff (2010) to incorporate economic uncertainty. Specifically, we consider a world consisting of two-country and a domestic FX market in which two currencies are traded. Two types of traders, namely fundamentalists and chartists, invest in the market. Moreover, investors switch between these two trading strategies depending on market conditions. To conveniently describe exchange market pressure, we assume no trading restrictions in the market (e.g., capital controls and FX intervention).

Fundamentalists

Following Dieci and Westerhoff (2010), fundamentalists are usually assumed to formalize their demand as,

where

It is indicated in (1) that if the exchange rate is overvalued (undervalued), fundamentalists would expect the exchange rate to move toward its underlying fundamental price, promoting them to reduce (increase) their demand for the local currency against the foreign one.

Chartists

For simplicity, follow Dieci and Westerhoff (2010), we define the chartists’ demand as follows,

where parameter

Evolution of the Exchange Rate

As in Dieci and Westerhoff (2010, 2013), the exchange rate at time t + 1 is determined by the excess demand formed by heterogeneous investors in period t. Thus, the exchange rate is developed by,

where parameter

In addition, following Dieci and Westerhoff (2010), we define the proportion

where parameter

Recall that the FX market is supposed to be perfect and free of intervention, so following the EMP definition in Girton and Roper (1977), we can define exchange market pressure in our context as,

Using (6), we can obtain EMP from (3),

Clearly, (7) provides a theoretical basis for an intuition that EMP is jointly determined by market sentiment and currency demand.

Role of Economic Uncertainty

Our model suggests that investors’ demands for currency partially depend on the fundamental exchange rate, which is determined by domestic and foreign macroeconomic variables in traditional theory. Since economic uncertainty has detrimental effects on the macroeconomy (Bloom, 2009, 2014; Jurado et al., 2015), investors’ demands

where the assumptions on the first-order partial derivative that

For simplicity, let

We hence can derive the impact of economic uncertainty on EMP by taking partial derivatives based on equation (9),

Similarly,

From (10)–(11), the impact is straightforwardly decomposed into two components, that is,

By inspecting (10) and (11), the effect of economic uncertainty on market sentiment is certain that an unexpected increase in domestic (foreign) uncertainty would induce a negative (positive) response in market sentiment, making fewer (more) traders using fundamental trading rule. However, the effect on market demand essentially lies in market sentiment

Remarkably, as shown in (10) and (11), the impact of economic uncertainty on EMP would be time-dependent due to the variabilities in the exchange rate misalignments and the share of chartists, as well as market sentiment. Moreover, as analyzed by Chiarella et al. (2017), traders’ beliefs and sensitivity to price misalignments, which we have assumed to be constant, may also change over time, bringing additional sources to the time variability of the impact.

Empirical Methodology and Data

Empirical Model

We work with a VAR framework to allow for potential endogeneity generated by the self-filling mechanism and the autocorrelations. Since a large body of evidence indicates various nonlinearities in the macroeconomic time series, it is quite desirable to take these nonlinearities into account when studying the behavior of the macroeconomy. While many studies have contributed to nonlinear modeling, the results obtained from nonlinear models may conflict with economic theory. However, Granger (2008) demonstrates that any nonlinear model can be approximated by a time-varying parameter model, which is generally linear but still has sufficient power to capture nonlinearities. Consequentially, during the past decade, time-varying parameter vector autoregressions (TVP-VARs) have gained widespread popularity among applied macroeconomists and have become a standard framework for analyzing macroeconomic time series in the last decade due to their charm of tracking processes subject to structural breaks or regime shifts (Baumeister & Peersman, 2013). While time variations in coefficients and conditional higher moments have been separately well documented in the literature, a TVP-VAR model unites time variations jointly and concomitantly in coefficients and variances, allowing the data to speak freely and capturing a wide range of time variation and nonlinearity (Lubik & Matthes, 2016; Nasir et al., 2018; Nasir & Simpson, 2018; Nasir & Vo, 2020).

Although a TVP-VAR model is very flexible and can model nearly all nonlinear relationships among the variables of interest, it is highly parameterized and may risk overfitting, leading to inaccurate estimation of impulse response functions. Recently, a growing literature has developed several methods to mitigate these over-parameterization concerns, see, for example, Koop and Korobilis (2013), Eisenstat et al. (2016), Huber et al. (2019), Chan et al. (2020). In this part of the literature, a widely used method is to use global-local shrinkage priors to reduce estimation bias and improve model performance. However, applying shrinkage to time-varying parameter models cannot wholly eliminate estimation errors (Huber et al., 2021). Moreover, incorporating shrinkage is less straightforward, and it often requires computationally demanding algorithms or approximate inference (Eisenstat et al., 2016). Eisenstat et al. (2016) propose a new approach that combines the stochastic model specification search (SMSS) framework developed in Frühwirth-Schnatter and Wagner (2010) with a typical TVP-VAR to ensure model parsimony. Comparatively, the methodology in Eisenstat et al. (2016) is more flexible and efficient in that it allows the model to automatically and endogenously choose between a time-varying parameter against a constant parameter for each VAR coefficient.

A typical TVP-VAR model

The generic state-space form of a typical structural TVP-VAR with stochastic volatility can be written as,

where

The residual

where

This setup is motivated by the well-documented evidence of allowing variance-covariance of residuals to vary over time in modeling macroeconomic data, see Fernández-Villaverde et al. (2015), for instance. Following Eisenstat et al. (2016), we assume that

As the matrix

Let

where

The SMSS framework

To alleviate the over-parameterization worries around

and relate

In addition, in order to incorporate the Lasso structure, it is assumed that

It is clear to see that the Tobit prior automatically restricts

Model estimation

Following Eisenstat et al. (2016), the MCMC Gibbs sampler is adopted for estimation and computing the posterior distributions for the parameters and hyper-parameters. Generally, the MCMC Gibbs sampler is distinctively straightforward and efficient since it samples from the full conditional probability distribution. Crucially, the MCMC is a smoothing method that produces smoothed estimates (Nasir & Morgan, 2018). Most importantly, the MCMC Gibbs sampler is suitable for our case. As discussed earlier, introducing the Tobit prior to shrink model dimensionality would lead to a computationally feasible and fast Gibbs sampler. In addition, the posterior computations using MCMC are outlined to deliver an overview of the sampling procedure. First, for

Prior settings

The priors are set in line with Eisenstat et al. (2016), as all sample data will be standardized before estimation, making the priors standard to some extent. As shown above, the priors for the hyper-parameters,

Finally, the above empirical model and framework will be applied to a Chinese monthly dataset to exploring the roles of economic uncertainty in China’s exchange market pressure.

Data

We conduct our empirical investigation with a monthly dataset from January 2001 to October 2020, primarily based on data availability. Additionally, a principal consideration in our decision to start our sample from January 2001 is that China’s macroeconomic data prior to 2001, during which China underwent profound institutional and economic transitions, were less reflective of the transmission dynamics among economic variables (Fernald et al., 2014).

Our baseline model centers on five main variables indicated by our behavioral model presented in Section 3, that is, EMP, domestic and foreign economic uncertainties, market sentiment, and market demand in the FX market.

Estimates of China’s EMP

Girton and Roper (1977) theorize that EMP is the sum of exchange rate fluctuations and official intervention. For the former, as discussed earlier, we focus on the onshore RMB exchange rate against the dollar since this trading pair dominates China’s FX market. For the latter, the growth of FX reserves has been primarily considered in the literature, as the government usually intervenes through transactions on FX reserves. In addition, underpinned by the assumption that the central banks can intervene by adjusting short-term interest rates, Klaassen and Jager (2011) include interest rate differentials in calculating EMP. However, we do not include interest rate differentials because China rarely utilizes interest rate instruments to intervene in the FX market (Das, 2019; Li et al., 2017).

Moreover, the intervention might not be fully reflected in changes in China’s FX reserves, especially after the complete abolition of the mandatory FX settlement regime in April 2012. As documented in Li et al. (2017) and Das (2019), and more recently in The Economist (2020), China has many tools to intervene in the FX market and prefers to do so by adjusting the central parity rate and other non-transparent measures rather than intervening directly, especially after 2015. The central parity rate has been a usual tool since the People’s Bank of China (PBoC), China’s central bank, first announced it on August 11, 2015. Since the reform on July 21, 2005, the PBoC has been operating a system that allows the daily exchange rate to fluctuate within a narrow band, which was expanded from the initial 0.3% to 2% in March 2014, around a target called the central parity rate. This central parity rate was based on the closing price on the last trading day before August 11, 2015, and thereafter, is based on the last trading day’s closing price plus the needed changes, which refer to the needed adjustment of the RMB/USD exchange rate to offset the overall impact of the fluctuations of the currencies in the currency basket against the dollar on the last trading day and overnight. In addition, a counter-cyclical adjustment factor (hereafter CCAF), initiated on May 26, 2017, to mitigate irrational market sentiment, has been added to the regime since then. The PBoC has occasionally intervened in the market through the CCAF afterward. In this sense, the CCAF is viewed as an instrument for FX intervention (Das, 2019). Therefore, it is necessary to include this CCAF in the estimation of China’s EMP. Further, the PBoC had directly capitalized four big state-controlled banks with FX reserves between 2003 and 2008. Ignoring these expenditures for non-intervention purposes would bias the EMP estimates. Hence, we differ from previous studies in that we take these non-intervention purpose expenditures back and accordingly recover the reserves.

Thus, the formula for calculating China’s EMP is defined as follows,

where

However, since the PBoC does not make public the CCAF, we need to estimate it first. To this end, based on the formation regime of the central parity rate, we regress the differential between the central parity rate and the last closing price of the RMB/USD exchange rate (denoted by

where a constant term

Notably, to prepare

Additionally, to provide some insights into the reasonableness of our calculation of the composite growth, we also regress

The closing exchange rates are collected from Investing.com, while the central parity rate and the U.S. dollar index are retrieved from the WIND database.

We estimate the equation using the OLS method and sum the daily CCAFs to produce the monthly CCAFs. The resulting CCAFs are shown in Figure 1. As we have the CCAF, we compute the monthly EMP index from January 2001 to October 2020, with the (recovered) FX reserves retrieved from the WIND database. Our calculated EMP indices are also reported in Figure 1. Moreover, the EMP index computed by Patnaik et al. (2017), downloaded from https://macrofinance.nipfp.org.in/releases/exchange_market_pressure.html, is also presented for comparison.

Estimated EMP and CCAF. EMP: exchange market pressure, CCAF: counter cyclical adjustment factor, USD base: the U.S. dollar index base, CFETS base: the Chinese currency basket designed by China Foreign Exchange Trade System.

As shown in Figure 1, the estimated CCAF and the EMP index based on the CFETS currency basket are highly consistent with those based on the U.S. dollar index in terms of magnitude and pattern, where the correlation between the two CCAFs exceeds 0.9. Centering on the estimated CCAF yields an intuitively consistent result that the PBoC acts counter-cyclically when encountering significant exchange market pressure.

Compared to our EMP index, there are many outliers in the Patnaik et al. (2017)’s measure. Moreover, our EMP index is less volatile and generally smaller than Patnaik et al. (2017)’s. In the following section, we use the CFETS currency basket-based EMP to fulfill our empirical study.

Proxy for economic uncertainty

As stated in the introduction section, we use the news-based EPU index to proxy economic uncertainty. Motivated by Christou et al. (2018), Bartsch (2019), and Zhou et al. (2020), U.S. EPU is also included. Accordingly, since we focus on the RMB/USD exchange rate pressure, we use the U.S. EPU constructed by Baker et al. (2016) and China’s EPU computed by Davis et al. (2019), downloaded from policyuncertainty.com .

Proxies for market sentiment and market demand

Following Das (2019), we proxy market sentiment with the one-year-ahead forward premium on the exchange rate. Specifically, we compute the log-difference (multiplied by 100) between the one-year-ahead non-deliverable forwards on the RMB/USD exchange rate and its onshore spot counterpart, yielding a market sentiment index that reveals an expectation of devaluation (appreciation) when it has a positive (negative) value.

To approximate changes in currency demand, as investors would trade according to their expectations (Cornell & Dietrich, 1978), mainly through banks in China (Lin & Schramm, 2003), we use customers’ net sell of foreign currency against the RMB calculated by the log-difference between customers’ sell and purchase of FX through the commercial banks. We believe that the overall trading volume could disclose the changes in market demand of the RMB against the dollar since trading on this pair accounts for more than 95% of the overall trading volume on average.

Finally, all the data, except for the EPU measures, are retrieved from the WIND database and seasonally adjusted (if necessary), while the EPU measures were taken logarithm.

Results

Baseline Model

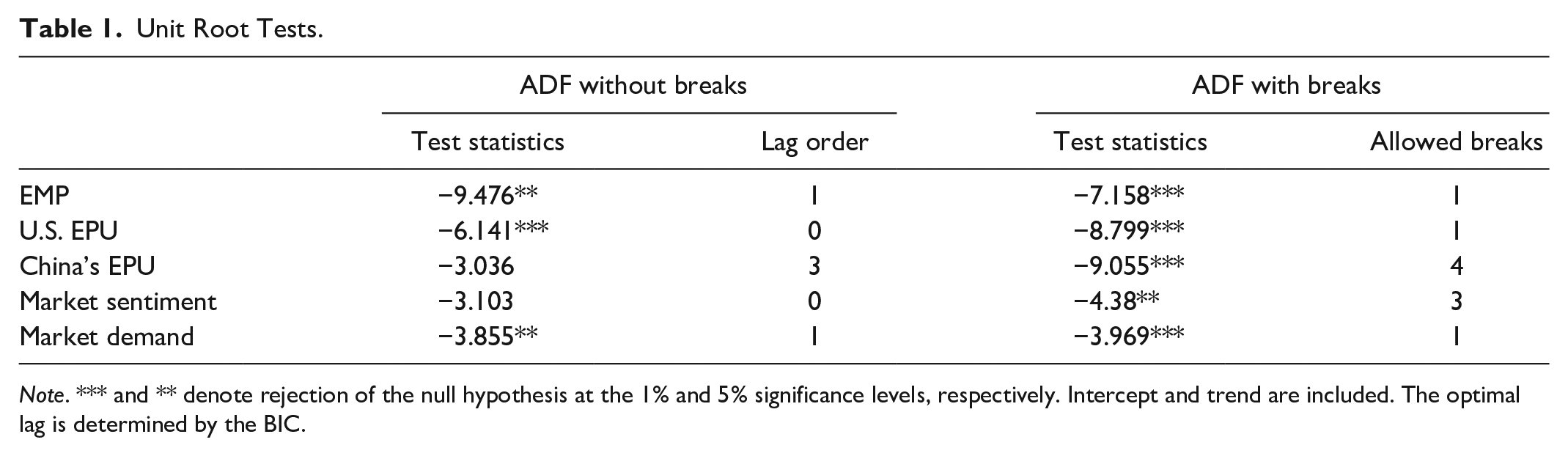

First of all, we perform unit root tests to elucidate some statistical properties of our variables. Following Jebabli et al. (2014), we employ the conventional ADF unit root testing approach to validate the stationarity of our variables. However, the conventional ADF test may be underpowered, given that the macroeconomic indicators may have multiple potential structural breaks (Check & Piger, 2021). Therefore, similar to Nasir (2021), we further apply the GLS-based ADF test proposed by Carrion-i-Silvestre et al. (2009), which allows for multiple structural breaks in both the null and alternative hypotheses. The corresponding results of unit root testing are reported in Table 1.

Unit Root Tests.

Note. *** and ** denote rejection of the null hypothesis at the 1% and 5% significance levels, respectively. Intercept and trend are included. The optimal lag is determined by the BIC.

As shown in Table 1, allowing for structural breaks in the variables improves the significance of the ADF test. It is suggested that EMP, U.S. EPU, and market demand are stationary regardless of whether structural breaks are considered. While the conventional ADF test detects that China’s EPU and market sentiment are non-stationary, the ADF test incorporating breaks signifies a high significance of stationarity of these two variables. Thus, all variables can be viewed as statistically stationary in a general sense. Moreover, this finding highlights the importance of applying the TVP-VAR model that incorporates structural breaks and regime shifts.

We set a lag length of six to ensure no serial autocorrelation and estimate the model by the procedure documented in Eisenstat et al. (2016). The MCMC Gibbs sampler in Eisenstat et al. (2016) is applied to attain 45,000 replicates with the first 15,000 draws as burn-in, obtaining 3,000 effective posterior draws by recording every ten replicates. Our estimation incorporates three potentially beneficial Generalized Gibbs steps, which can produce the lowest inefficiency factors plotted in Figure 2. Clearly, most of the inefficiency factors are less than 10, though the majority for

Inefficiency factors of the estimated parameters.

Next, based on the effective MCMC draws, we estimate the impulse response functions using the Cholesky decomposition to identify structural shocks. Notably, all impulse response functions (IRFs) are rescaled to match the original series. To evaluate the total impact of EPU, we compute cumulative impulse response functions at each time point of 1% shocks in U.S. EPU and China’s EPU, respectively.

We perform a preliminary analysis with the time-averaged IRFs for a horizon of 12 months to provide an overall picture of the EPU’s impact, see Figure 3: The 68% highest posterior density (HPD) intervals (shaded areas) are constructed with 16% and 84% percentiles of the posterior estimates, while the estimated IRFs (solid lines) are the posterior medians. As expected, a rising shock in U.S. EPU would generally increase the relative demand for the renminbi against the dollar, exerting appreciation pressure on the RMB. However, this market demand channel does not hold for the shocks originating from China’s EPU that it has a positive but imprecise effect on market demand. The counter-intuitive results are also presented in the response of market sentiment. While it exhibits a slightly negative response following a hike in U.S. EPU, market sentiment responds with a more significant negative pattern after an upsurge in China’s EPU, signifying that a higher China’s EPU may be associated with the expectations of RMB appreciation and increased demand for the RMB. Notably, this finding is likely relevant to our proxy for market sentiment, namely the spread between the one-year-ahead NDF exchange rate and the onshore spot exchange rate. As the NDF exchange rate is the expected exchange rate 1 year later, if the uncertainty shocks cause the spot exchange rate to depreciate in the short run, the market would expect the exchange rate to revert, inducing appreciation expectations. In addition, China’s asymmetric FX regulations, where selling FX is less controlled than buying, may also contribute to the preposterous response in market demand. Nevertheless, an increase in China’s EPU is still followed by an approximate positive response in EMP, corroborating roughly the findings in Liu (2020).

Time-averaged dynamics of market sentiment, market demand, and EMP, following a 1% increase in U.S. EPU and China’s EPU, respectively.

To dissect how the impact of EPU evolves over our sample period, we turn to an analysis based on the time-varying IRFs. Since the FX market operates daily, it is unlikely that the market consumes a long time to respond to an external shock. Accordingly, we accentuate our analysis on inspecting the market’s reactions in 3 months after the shock. Further, we detect the responses at 6-month after the shock as the time-averaged IRFs shown in Figure 3 almost all converge after then. More specifically, we look into the impulse response functions at each time point at horizons of 0 to 3 months and 6 months after the shock, where 0-month means the moment when the shock occurs. Figures 4 and 5 paint the time-varying market responses at these horizons after a 1% shock in U.S. EPU and China’s EPU, respectively.

Time-varying market responses at horizons of 0-month to 3-month, and 6 months following a 1% increase in U.S. EPU. The solid lines are posterior medians, while the shaded regions are the corresponding 68% HPD intervals.

Time-varying market responses at horizons of 0 to 3, and 6 months following a 1% increase in China’s EPU. The solid lines are posterior medians, while the shaded regions are the corresponding 68% HPD intervals.

At first glance, the IRFs in Figures 3 and 4 provide strong evidence of the time-varying impact of EPU on China’s FX market, particularly on EMP. Relatively, the IRFs are more volatile at longer horizons. One possible explanation is that since China’s FX market may not be fully efficient (Gupta & Plakandaras, 2019), the market may need time to recognize the shock, waiting to see the impact it will cause and responding accordingly afterward. Consequentially, the IRFs at the horizons of 0-month and 1-month are more stable and less precise, indicating market inefficiency. However, the IRFs at longer horizons generally depend on market conditions, such as institutional and market regimes, which have dramatically changed in China over the past decades, resulting in the high volatility of these IRFs. Therefore, we scrutinize and discuss the rationale of the time variability revealed by these IRFs in the following section.

As shown in the top panels in Figures 4 and 5, an increase in either U.S. EPU or China’s EPU would trigger appreciation sentiment on the renminbi against the dollar, which is consistent with the findings by Li et al. (2020). Moreover, the response of market sentiment to a U.S. EPU shock is consistent with the common wisdom that a rise in U.S. EPU has a detrimental impact on the U.S. macroeconomy and provokes devaluation expectations on the dollar. However, the response to the China’s EPU shocks contradicts the uncertainty theory. As noted earlier, this could be explained by China’s FX regulations, which might cause the market to expect the renminbi to appreciate against the dollar. Relatively, the response to China’s EPU shocks is more stable than that to U.S. EPU shocks, though the latter’s corresponding HPD intervals are wide to contain zero, indicating insignificant responses of market sentiment to the U.S. EPU shocks. By contrast, following a hike in China’s EPU, there would be a significant appreciation expectation on the renminbi against the dollar from 3 months onward, especially in the post-2005 period. Before 2005, China carried out a de facto pegged exchange rate regime, causing market sentiment to be less responsive to China’s EPU shocks. However, following the reform in July 2005, China implemented a gradual appreciation path for the renminbi against the dollar, leading to the widespread market expectations of the RMB appreciation. In addition, the exchange rate stability has been one of China’s principal objectives. Thus, the negative building impact of China’s EPU on the renminbi would stimulate an expectation that the government will intervene in the market, inducing the appreciation expectations on the renminbi. Further, the response of market sentiment to the U.S. EPU shocks swells progressively after mid-2015, which could be ascribed to the increased exchange rate flexibility after introducing the quoting regime of the central parity rate in August 2015 (Das, 2019).

It is noteworthy that market demand expresses a significant response following a rise in U.S. EPU, as shown in the middle panel in Figure 4. In the first month after the shock, the relative demand for the renminbi increases significantly, mirroring the dollar devaluation expectations caused by the U.S. EPU shocks. By contrast, market demand responds counter-intuitively and insignificantly to China’s EPU shocks. As displayed in Figure 5, after a rising shock in China’s EPU, we can see an increase in market demand for the renminbi in the first month, but it shows a preference for the dollar 2 months after the shock. Therefore, it may take about 2 months for China’s EPU shocks to have the supposed impact on market demand. Notwithstanding, China’s EPU exerts a less precise effect on market demand when compared with U.S. EPU. One explanation for this is that China’s FX regulations make it much easier to sell foreign currencies than to buy them. Importantly, as shown in Figure 5, the response also has a downward trend after mid-2015, probably due to an increasingly flexible exchange rate regime. This result supports the findings by Kozhan and Salmon (2009) that agents in the foreign exchange market are uncertainty averse.

While the responses of market sentiment and market demand to China’s EPU shocks are somewhat at odds with the theory, the response of EMP is consistent with our expectations. As shown in the last panels in Figures 4 and 5, respectively, a hike in U.S. EPU (China’s EPU) would systematically prompt appreciating (deprecating) pressure on the renminbi against the dollar, leading to a negative (positive) response of EMP. Comparatively, China’s EPU shocks take a longer time than U.S. EPU shocks to generate an impact on China’s EMP. Moreover, the IRFs at horizons of 2, 3, and 6 months after the shock exhibit noticeable time variations. Specifically, the impact of EPU on EMP is stable until mid-2011 but then enlarges till the end of 2017. Accordingly, our results provide little evidence to support the findings by Kido (2016), who finds that the real effective exchange rate returns and U.S. EPU were intensively correlated during the global financial crisis. The explanation is straightforward. Albeit, indeed, the unconventional monetary policy undertaken by the U.S. Federal Reserve during the financial crisis reduced the dollar’s value (Neely, 2015), China had pegged the renminbi to the dollar again during this period. Further, China had experienced large capital outflows during the crisis (Broner et al., 2013) due to the need to relieve the value-at-risk of U.S. domestic assets caused by the crisis (Schmidt & Zwick, 2015). Thus, the impact of U.S. EPU on China’s EMP could retain its past pattern without being altered by the crisis.

Intuitively, this time-varying property shown in the impact of U.S. EPU on China’s EMP may be associated with the evolution of China’s dependence on the United States. Over the last decades, China has developed a high degree of trade and financial linkages with the United States. Taking the foreign trade as an example, Figure 6 displays the geographical Gini coefficient of China’s international trade and the share of trade with the United States in China’s total trade from 1992 to 2019. Generally, the dependence on the U.S. is high, especially for exports, although the geographical concentration of China’s trade is relatively low. The overall dependence on the U.S. has declined gradually, but slightly, from 2001 to 2011, resulting in a relatively small and stable impact of U.S. EPU during this period. Subsequently, from 2012 to 2017, China’s dependence on the U.S. has been fueled up, associated with the strengthening impact of U.S. EPU on China’s EMP. However, since 2018, the trade dependence has plummeted because of the U.S.-China trade dispute, making China’s EMP less responsive to the U.S. EPU shocks. In addition, the recently heightened response of EMP to the U.S. EPU shocks may be attributed to the easing of the trade dispute and the outbreak of COVID-19.

Gini coefficients of China’s trade and trade dependence on the United States. Following Liu et al. (2020), we measure the geographical concentration of trade with the Gini coefficients, calculated by

As shown in Figures 4 and 5, it is discernible that the responses of China’s EMP to the shocks originating from domestic EPU and U.S. EPU are similar in dynamics but opposite in evolutionary path. Since EMP could be influenced by local and external uncertainties concurrently, we find a trade-off mechanism between them, where the impact of domestic EPU prevails when the impact of foreign EPU fades and vice visa, corroborating the effect of the EPU differentials on the exchange rate reported in Balcilar et al. (2016), Christou et al. (2018), and Zhou et al. (2020).

Further, the time-varying nature of EMP response to the EPU shocks may also be related to the transmission through market sentiment and demand. To explore the roles of market sentiment and demand, we estimate the time-varying IRFs of EMP to the shocks in these two variables and plot the results in Figure 7.

Time-varying responses of EMP to 1% shocks in market sentiment and market demand, respectively. The solid lines are posterior medians, while the shaded regions denote the corresponding 68% HPD intervals.

Obviously, more time variation is detected in EMP responses to the market sentiment and demand shocks. An increase in market sentiment (i.e., devaluation expectations on the renminbi against the dollar) would substantially coerce the RMB to devaluate, while a rise in market demand would trigger appreciation pressure on the RMB. Additionally, after August 2015, increasingly enhanced exchange rate flexibility raises investors’ risk exposure, causing the impact of market sentiment and market demand to reduce sharply.

Robustness Check

We consider the following two alternative specifications to implement robustness checks. (1) [

Time-averaged responses of EMP to 1% shocks to U.S. EPU and China’s EPU. The solid lines are posterior medians, while the shaded regions are the 68% HPD intervals.

Time-varying responses of EMP to 1% shocks in China’s EPU and U.S. EPU, respectively. The solid lines are posterior medians, while the shaded regions denote the 68% HPD intervals.

As we can see in Figures 8 and 9, Rmodel1 and Rmodel2 produce similar results to our baseline model. However, Rmodel1 derives a more precise estimate of the EMP response to China’s EPU shocks, particularly after 2010, during which an upsurge in China’s EPU would cause significant devaluation pressure on the onshore exchange rate. This result may suggest that the EPU index constructed by Huang and Luk (2020) is a more credible indicator of economic uncertainty as it is less prone to media bias (Huang & Luk, 2020). In addition, Rmodel2 renders a more remarkable but more stable response of EMP to U.S. EPU shocks.

Conclusion and Policy Implications

Our empirical findings show that an upsurge in U.S. economic policy uncertainty triggers appreciation pressures on the RMB/USD exchange rate, while a hike in China’s economic policy uncertainty tends to exert devaluation pressures on the exchange rate. Moreover, the magnitude of the impact of economic policy uncertainty on exchange market pressure is time-dependent. Specifically, the impact is relatively stable until mid-2011 but more volatile thereafter. In addition, we find a trade-off mechanism between the impact on EMP of domestic and foreign economic policy uncertainties.

Our results have the following policy implications. First, to stabilize the exchange rate, China should enhance its management of market expectations and market demand, reducing the unfavorable impact on the exchange rate of irrational market sentiment to cope with spikes in domestic and foreign economic uncertainties. In addition, a foreign exchange derivatives market should be established and advanced to provide functional risk hedging tools and attain a better understanding of market sentiment. Second, further liberalization of the capital account should be proceeded prudently and sequenced with prerequisite reforms, including a solid and sound financial system and an appropriate macroeconomic regulatory framework. Third, China should further improve the flexibility of the RMB exchange rate and make the exchange rate formation mechanism transparent, sending clear signals of two-way exchange rate fluctuations to avoid irrational market sentiment toward one-way movements. Finally, China should further diversify the basket currency structure and increase RMB transactions against non-USD currencies. Furthermore, China could lower its dependence on the United States in trade and finance to a certain extent to reduce the detrimental impact on China’s real economy and financial markets of economic uncertainty shocks originating from the United States.

However, our study still has some limitations. First, because of the lack of statistics on market agents, our proxy for market sentiment in the empirical section is not entirely consistent with that illustrated in the theoretical model, resulting in a rough understanding of market sentiment in a broad sense. Second, our proxy for market demand is not a pure index reflecting demand for the RMB/USD pair but also includes other trading pairs, despite the dominance of the RMB/USD pair in the market. Third, since China still adopts a managed floating exchange rate regime, we note that China’s monetary authority releases scant interventions in the foreign exchange market and intervenes the market by other hidden levers recently keeping the reserves unmoved, limiting us to obtain a highly accurate estimate of China’s exchange market pressure.

As for the future research, since capital flows are sensitive to economic uncertainty and exchange rate fluctuations, one possible direction is to dissect the roles of capital flows in the relationships between economic uncertainty and exchange market pressure. Moreover, in recent years, China’s authority has attempted to manage the foreign exchange market by adjusting the foreign exchange reserve requirement ratio, opening a topic that how and whether this policy affects market sentiment and market demand, and thereby the exchange rates.