Abstract

This paper examines the hedge and safe-haven abilities of Bitcoin against U.S. aggregate and categorical economic policy uncertainty (EPU) via the application of quantile regression model augmented with a dummy and some control variables. Using monthly data from September 2011 to December 2019, empirical results indicate that Bitcoin does not act as a strong hedge against the aggregate U.S. EPU. However, it acts as a strong safe-haven for this aggregate measure of uncertainty when the Bitcoin market is bearish. Looking deeper into the disaggregated level of the U.S. EPU data, the analyses involving categorical EPU data indicate the ability of Bitcoin to act as a strong hedge and safe-haven against specific uncertainties related to fiscal policy, taxes, national security, and trade policy.

Introduction

Research interest in the effects of uncertainty and the economy in general on financial markets goes back to the theoretical models of Bernanke (1983) and Bloom (2009). However, since the 2008 global financial crisis, policy factors have gained ground in shaping the economic environment and financial markets. Lately, Baker et al. (2016) have proposed a news-based index of U.S. economic policy uncertainty (EPU), which has been widely used in academic literature. Accordingly, numerous studies try to understand the impact of the U.S. EPU on U.S. stock market returns and report evidence of a negative impact (e.g., Arouri et al., 2016). Other studies focus on the impact of the U.S. EPU on safe-haven assets such as gold, mostly showing that EPU has the ability to predict gold prices (Raza et al., 2018) and that gold prices and economic uncertainty are positively related (Bilgin et al., 2018). Such findings concur with previous evidence arguing that, during periods of economic and political uncertainties, investors switch their investments from risky assets to less risky or safe-haven assets such as gold (Baur & Lucey, 2010).

Remarkably, the most popular and largest cryptocurrency, Bitcoin, has emerged as a substitute instrument for the ineffectiveness of traditional economic and financial systems, especially during stress periods (Bouri et al., 2017a, 2017c), such as the European sovereign debt crisis (2010–2013) and the Cyprus banking crisis (2012–2013). Since its lunch, the value of this digital currency has soared from $0.09 in July 2010 to around $19,000 in December 2017. Bitcoin market capitalization surged from less than $1.6 Billion to about $316 billion during the same period, allowing Bitcoin to occupy more than 80% of the total market value of all cryptocurrencies. Accordingly, Bitcoin gained a large interest in the financial literature, given its beneficial proprieties. In fact, Bitcoin is almost isolated from the global financial system, making it a valuable addition to portfolios containing conventional assets (Corbet et al., 2018; Guesmi et al., 2019; Symitsi and Chalvatzis, 2019). In view of this, some academic literature examines the hedging and safe-haven properties of Bitcoin for equities (Bouri et al., 2017c; Klein et al., 2018; Shahzad et al., 2019, 2020), commodities (Bouri et al., 2017b; Klein et al., 2018), and currencies (Urquhart & Zhang, 2019). Other studies consider the effect of EPU on the Bitcoin market and make inferences regarding hedging and acting as a safe-haven (Cheng & Yen, 2019; Demir et al., 2018; Panagiotidis et al., 2019; Wang et al., 2019b; Wu et al., 2019). The findings are, however, mixed and inconclusive. Some studies show that the impact of the U.S. EPU is insignificant (Cheng & Yen, 2019; Wang et al., 2019b), while others find a positive impact (e.g., Panagiotidis et al., 2019) that varies across the lower, middle, and upper quantiles (Demir et al., 2018; Wu et al., 2019). Notably, related studies limit their focus to the aggregate EPU index, which would mask any potential heterogeneity in the impact of the categorical U.S. EPU on the Bitcoin market. Therefore, extending the above literature to the categorical level of the U.S. EPU data (Baker et al., 2016) would help uncover potential heterogeneity in the role of Bitcoin as a hedge and safe-haven against the various 11 components of U.S. economic uncertainty (monetary policy, fiscal policy, taxes, government spending, health care, national security, entitlement programs, regulation, financial regulation, trade policy, and sovereign debt and currency crises). This is important for at least two reasons. First, specific economic uncertainties and developments, such as those related to monetary, fiscal, political, and trade policies in the United States, have been in the financial news. For example, the trade war between the United States and China and the impeachment action in the United States have moved financial markets, and some press articles have tried to establish a link to Bitcoin. Second, a more nuanced analysis that accounts for the heterogeneity in the composition of the U.S. EPU helps investors make inferences regarding portfolio management. It also helps financial advisors make risk management and hedging decisions regarding the ability of Bitcoin to hedge various components of economic uncertainty, especially during market downturns.

In light of the above, we examine in this study the impact of categorical U.S. EPU indices on Bitcoin returns. Using monthly data from September 2011 to December 2019, we apply a quantile-based regression augmented with dummy variables and some other control variables to account for the heavy-tails of asset returns and various dependent variable distribution levels. Such an examination allows us to differentiate between the impact of categorical U.S. EPU indices at various quantiles of Bitcoin return distribution (i.e., bearish, normal, and bullish periods) (Wu et al., 2019).

Our contributions are on various fronts. First, we contribute to the strand of literature dealing with EPU and Bitcoin returns (Cheng & Yen, 2019; Demir et al., 2018; Panagiotidis et al., 2019; Wang et al., 2019b; Wu et al., 2019) by moving the debate to the categorical level of the U.S. EPU. In fact, our paper is the first to examine the impact of various components of the U.S. EPU on Bitcoin returns during bearish and bullish market states, which extends previous studies focusing only on trade policy uncertainty (e.g., Gozgor et al. (2019) apply wavelets methods and show that the relationship between trade uncertainty and Bitcoin prices is positive in general, with some exceptions.). Second, we contribute to the literature dealing with the debatable role of Bitcoin as a hedge and safe-haven against uncertainty (Bouri et al., 2017a; Cheng & Yen, 2019; Panagiotidis et al., 2019) during stress periods. Unlike previous studies (Cheng & Yen, 2019; Demir et al., 2018; Panagiotidis et al., 2019; Wang et al., 2019b; Wu et al., 2019), we find convincing evidence for Bitcoin being a hedge and safe-haven for specific categorical U.S. EPU indices such as fiscal policy, taxes, national security, and trade policy uncertainty. These findings are useful to a variety of economic players such as policymakers, financial advisors, and investors.

The rest of the paper is organized into four sections. Section 2 reviews the related literature dealing with Bitcoin. Section 3 describes the data and methodology. Section 4 reports the empirical results and offers a discussion in light of previous studies. Section 5 concludes and opens paths for further research.

Previous Studies

The release of Bitcoin as a genuine and fast payment mechanism has marked the last decade. Some studies examine the safety and legal aspects of the Bitcoin market (Anceaume et al., 2017; Teomete Yalabık & Yalabık, 2019). As the market for Bitcoin grows, Bitcoin becomes a leading digital asset, attracting the attention of many investors. Accordingly, numerous studies focus on the economic and financial implications of Bitcoin by considering price discovery (Baur & Dimpfl, 2019), volatility (Bouri et al., 2019), and speculative nature (Baur et al., 2018). Notably, Bitcoin is segmented from the global financial system, offering valuable diversification benefits (Bouri et al., 2017c, 2017b; Corbet et al., 2018; Guesmi et al., 2019; Klein et al., 2018; Selmi et al., 2018; Shahzad et al., 2019, 2020; Symitsi & Chalvatzis, 2019; Urquhart & Zhang, 2019). Bouri et al. (2017a) report that Bitcoin represents a hedging tool against stock market uncertainty. Other studies focus on the impact of EPU on the Bitcoin market. Demir et al. (2018) use a quantile-based approach to examine the prediction power of EPU on Bitcoin prices. They suggest that Bitcoin can be used as a hedging tool against EPU. Wu et al. (2019) employ a GARCH model and quantile regression to compare the hedge and safe-haven roles of gold and Bitcoin against EPU. They show the inefficacity of these two assets in acting as a hedge or safe haven against EPU. Fang et al. (2019) apply multivariate GARCH models to investigate the impact of aggregate EPU on Bitcoin and other assets. They report that Bitcoin can be considered a hedge under specific economic uncertainty conditions. Also, using a quantile-based approach and causality tests, Wang et al. (2019b) find that Bitcoin has the propriety of a safe-haven and a diversifier for the extreme shocks of economic uncertainty. Cheng and Yen (2019) investigate the relationship between cryptocurrency volatility and EPU. They indicate that Bitcoin and Litecoin are useful hedging tools against EPU.

Other studies focus on the hedging and safe haven proprieties of cryptocurrencies. For example, Wang et al. (2019a) investigate the spillover effects between Bitcoin and major financial assets based on the VAR-GARCH-BEKK framework. Their results show that Bitcoin can serve as a hedge against some assets, including stocks and bonds. Besides, Bitcoin can act as a safe haven against extreme changes in monetary markets. Shahzad et al. (2019) compare the hedging and the safe haven proprieties of Bitcoin compared to the commodities and gold against stock market investments during bear and bull market conditions. They report that Bitcoin, gold, and the commodity index can serve as weak safe-haven assets in some cases.

More recently, Wang et al. (2020) investigate the proprieties of stablecoins for traditional cryptocurrencies. They show the following. First, USD-pegged stablecoins have better risk-dispersion abilities for traditional cryptocurrencies than gold-pegged ones. Second, Tether plays the role of a strong hedge for traditional cryptocurrencies. Third, gold is a better hedge than stable coins, and the USD is a better hedge than two of the USD-pegged stablecoins. However, gold as a safe haven is not as good as the stablecoins it backs. Third, the gold-pegged stablecoin is less efficient than the USD-pegged stablecoins in terms of risk reduction. Bouri et al. (2020b) compare the safe-haven properties of Bitcoin, gold, and the commodity index against the world, developed, emerging, the United States, and Chinese stock market indices based on the wavelet coherency approach analysis. They indicate a weak dependence between Bitcoin/gold/commodities and the considered stock markets at various time scales. Regarding the diversification potential, the results report the dominance of Bitcoin over both gold and commodities.

In this paper, we contribute to the academic literature by investigating the potential hedging and safe-haven effects of Bitcoin with respect to various categories of U.S. EPU. To the best of our knowledge, no previous research has focused on various categories of EPU to address whether Bitcoin is a hedge or safe-haven against categorical U.S. EPU indices at various states of the Bitcoin market (i.e., bullish and bearish market periods). Methodologically, we use quantile regressions augmented with dummy variables to address various situations of markets and various lower and upper quantiles of Bitcoin return distributions.

Data and Methodology

The Dataset

In this study, we use a monthly dataset covering the closing prices of Bitcoin against the U.S. dollar and the U.S. EPU. To eliminate aggregation bias, we use 11 categorical uncertainty indices covering monetary policy, fiscal policy, taxes, government spending, health care, national security, entitlement programs, regulation, financial regulation, trade policy, and sovereign debt. Following Baker et al. (2016), these indices are solely based on news data and constructed using the Access World News (AWN) database of about 2000 U.S. newspapers. Each index is constructed with respect to the mention of categorical policy terms related to uncertainty terms. Table 1 presents the different terms used to construct each categorical EPU index, For more details, see Baker et al. (2016) and the website: https://www.policyuncertainty.com.)

Description of the Different EPU Categorical Uncertainty Indices.

Besides the availability of categorical U.S. EPU data, we focus on U.S. economic uncertainty for at least two other reasons. First, the United States is the country running most Bitcoin nodes in the world (21.49% in January 2020). Second, the Bitcoin price is mainly traded against the U.S. dollar. The dataset covers the period from September 2011 to December 2019, yielding 100 monthly observations Data for Bitcoin price are from DataStream and represent the price of Bitcoin against the U.S. dollar from Bitstamp, the leading exchange. Uncertainty indices are sourced from the website https://www.policyuncertainty.com/. Notably, the starting date depends on the availability of Bitcoin prices. We employ the logarithmic returns of Bitcoin and aggregate EPU (Demir et al., 2018), and categorical economic uncertainty indices, that is.,

(a) Bitcoin returns and (b) aggregate and categorical economic policy uncertainty changes.

Table 2 provides descriptive statistics and stationarity tests of Bitcoin returns and the returns of EPU and 11 categorical uncertainty indices. Bitcoin experiences the highest positive average return (10.203%). Conversely, all the uncertainty indices display negative average variations, except the trade policy uncertainty index. The standard deviation fluctuates between 25.529 and 103.345, the figures for the aggregate EPU index and the sovereign debt uncertainty index, respectively. Bitcoin and most of the U.S. categorical uncertainty indices have excess kurtosis and non-zero skewness. Based on the results of the Jarque-Bera test, the normality of Bitcoin returns is rejected. The normality hypothesis is rejected for the returns of the aggregate EPU index and three categorical uncertainty indices. Using both the augmented Dickey-Fuller (ADF) and Phillip-Perron (PP) tests, all return series are found to be stationary.

Descriptive Statistics and Stationarity Tests.

Note. The sample is September 2011—December 2019, covering the monthly returns series. STD (standard deviation) J-B denotes the p-value of the Jarque-Bera normality test. ADF and PP are test statistics for the augmented Dickey-Fuller (ADF) and Phillip-Perron, respectively. (***) indicates the statistical significance at 1% level. EPU = economic policy uncertainty.

The various categorical EPU indices capture policy uncertainty related to monetary and fiscal policies, taxation, financial regulation, trade policy, government spending, national security, debt and crises, and entitlement programs. In other words, information regarding categorical uncertainty indices comes from different terms and sources. Thus, an in-depth analysis of the association between categorical EPU and a global cryptocurrency currency such as Bitcoin helps identify the specific source of risk in the EPU that can be hedged by Bitcoin returns. Some of the source (e.g., trade uncertainty) is of global influence on financial markets and thus plays a more important role than others for the Bitcoin market (Bouri et al., 2020a). Conversely, other sources such as entitlement programs are of domestic influence and may be segmented from the Bitcoin market. This is also relevant as previous findings provide evidence on the adverse impact of some categorical policy uncertainties on stock market indices (Chiang, 2020). Accordingly, we conjecture that Bitcoin exhibits heterogeneity in its relationship with categorical EPU indices and thus in its hedging ability.

Methodology

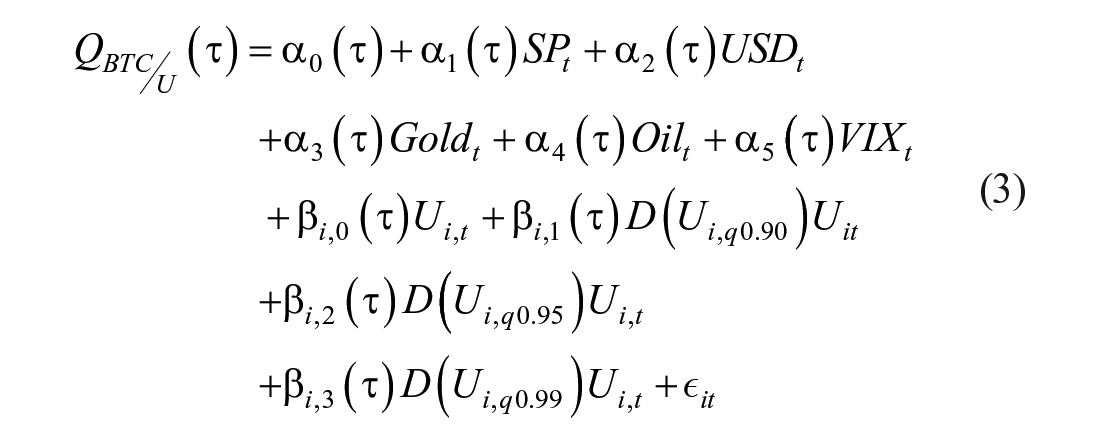

To determine the ability of Bitcoin to act as a hedge or safe-haven against aggregate and categorical EPU under Bitcoin’s various market conditions, we follow Wu et al. (2019) by considering a quantile regression augmented with dummy variables as follows:

where

To account for other factors affecting Bitcoin returns, we add some control variables, namely the S&P500 representing the effect of the U.S. stock market, the U.S. dollar index (USDX) to represent the currency market, and the gold price (Gold), and oil price (WTI) to account for commodity market effects. We also add the U.S. CBOE VIX index to take into account the volatility of the U.S. stock market. Then, the augmented Equation (1) becomes:

We run Equation (3) for the 5, 10-, 20-, 40-, 50-, 60-, 80-, 90-, and 95-th quantile. Following the line of previous studies (Baur & Lucey, 2010, who study the gold and stock market indices; Bouri et al., 2017a, 2017c, who study Bitcoin and conventional assets), especially Wu et al. (2019) who study gold/Bitcoin and aggregate EPU, we conjecture that Bitcoin is a strong (weak) hedge against categorical economic uncertainty

Results and Discussion

We present coefficient estimates from Equation (3) at 9 quantiles

Hedging Property Analysis

Table 3 provides the estimation of the hedging parameter

Estimation Results of the Bitcoin Hedging Parameter

Note. EPU = economic policy uncertainty. Numbers between parentheses denote the standard error. (*), (**), and (***) indicate the statistical significance at 10%, 5%, and 1% level, respectively.

To give a more comprehensive picture of the hedging ability of Bitcoin against U.S. economic uncertainty, we focus on the coefficient estimates of Equation (3) for the 11 categorical economic uncertainty indices. Notably, the estimates provide more mixed and nuanced results than those involving the aggregate EPU index. In fact, Table 3 shows that the parameter

On the other hand, under bullish market condition, the negative and significant parameter

Overall, it seems that Bitcoin is characterized by a strong ability to act as a hedging tool against some categorical uncertainty, mainly when it is Bullish. This result could be explained by the fact that during periods of price increases for Bitcoin, investors take more long positions in this digital asset, which makes it more attractive during high uncertainty (stress) periods (Bouri et al., 2017a, 2017c). In fact, Bitcoin acts as a hedging tool in the face of the inefficacity of traditional assets to hedge portfolios against economic and financial uncertainty conditions (Guesmi et al., 2019; Symitsi and Chalvatzis, 2019). Corbet et al. (2018) show that cryptocurrencies are somewhat segmented from stock market shocks and dissociated from popular financial assets, which points to the hedging ability of Bitcoin against uncertainty. Furthermore, our empirical results show that the hedging ability of Bitcoin is limited to financial (fiscal and taxes), national security, and trade uncertainty and not to regulatory uncertainty. This new finding could be explained by the fact that the cryptocurrency markets generally operate away from government regulation systems.

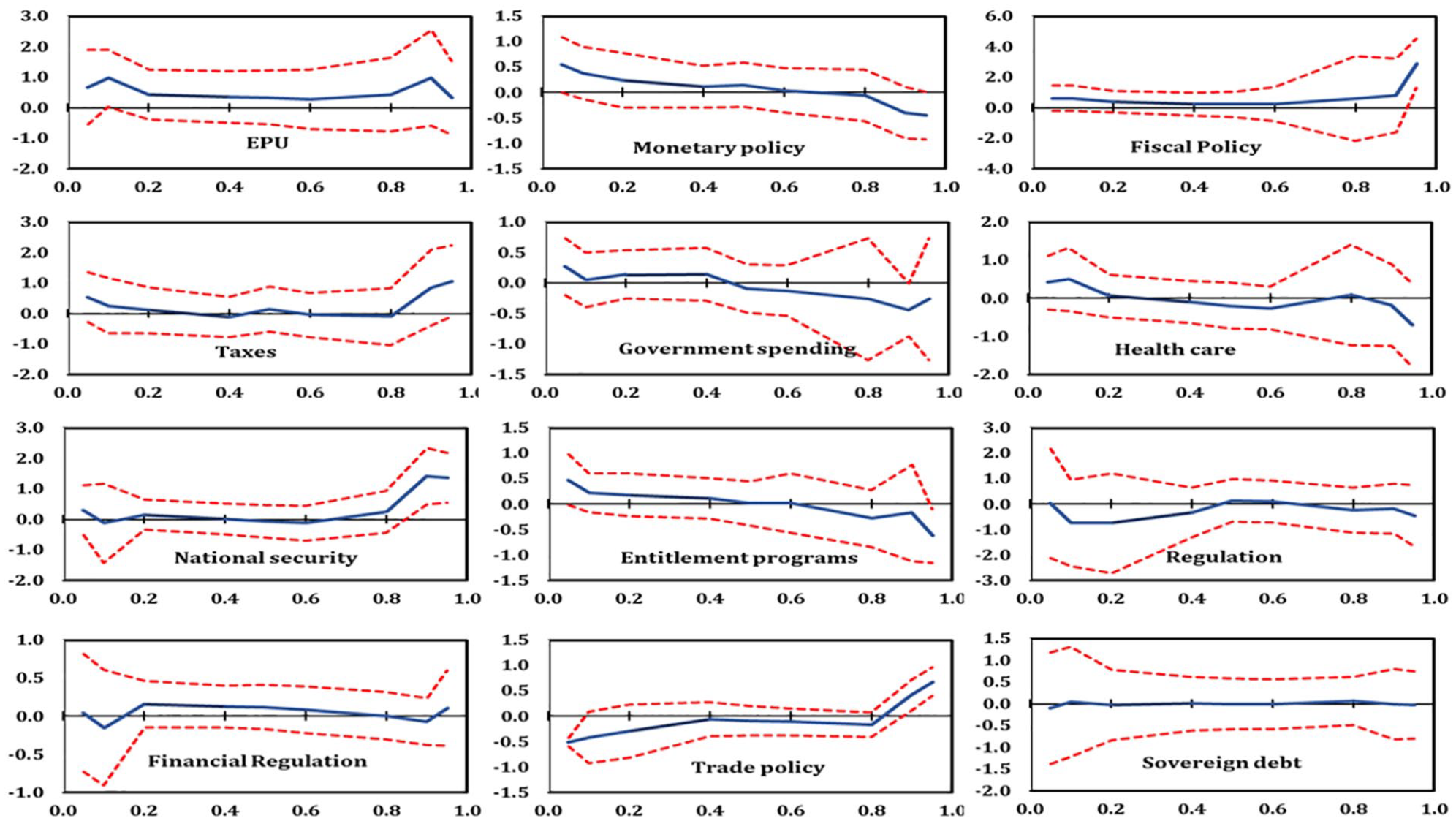

Figure 2 presents a graphical illustration of the estimated parameters, showing the shape of the parameter against the quantile order. Different forms and patterns of the hedging parameter are observed. The value of the parameter tends to increase with quantile order for financial policy uncertainty (fiscal and taxes), national security, and trade uncertainty. However, there is generally a decrease in the effect of the other categorical uncertainty indices on Bitcoin returns starting at positive values at lower quantiles and finishing at negative and insignificant values at high quantiles. This confirms Bitcoin’s ability to hedge uncertainty during Bitcoin’s bull market periods, while this ability is weak during Bitcoin’s bear markets.

Hedge coefficients of Bitcoin with 95% confidence bands.

Safe-haven Property Analysis

Here, we investigate the safe-haven ability of Bitcoin by focusing on the coefficients of the dummy parameters. Results are provided in Tables 4 to 6 at 90%, 95%, and 99% quantiles, respectively. Figures 3 to 5 graphically present the parameter estimations.

Estimation Results of the Safe-haven Parameter Sum at 90%

Note. EPU = economic policy uncertainty. Numbers between parentheses denote the standard error. (*), (**), and (***) indicate the statistical significance at 10%, 5%, and 1% level, respectively.

Estimation Results of the Safe-haven Parameter Sum at 95%

Note. EPU = economic policy uncertainty. Numbers between parentheses denote the standard error. (*), (**), and (***) indicate the statistical significance at 10%, 5%, and 1% level, respectively.

Estimation Results of the Safe-haven Parameter Sum at 99%

Note. EPU = economic policy uncertainty. Numbers between parentheses denote the standard error. (*), (**), and (***) denote indicate the statistical significance at 10%, 5%, and 1% level, respectively.

Safe-haven coefficients of Bitcoin with 95% confidence bands at the 90% quantile of the U.S. categorical uncertainty indices.

Safe-haven coefficients of Bitcoin with 95% confidence bands at the 95% quantile of the U.S. categorical uncertainty indices.

Safe-haven coefficients of Bitcoin with 95% confidence bands at the 99% quantile of the U.S. categorical uncertainty indices.

Table 4 shows that, at the 90% quantile, the parameter sum

Our above findings nicely complement the related literature dealing with Bitcoin and various measures of uncertainties (Bouri et al., 2017b), especially previous studies that consider the aggregate economic policy uncertainty index (Cheng & Yen, 2019; Demir et al., 2018; Panagiotidis et al., 2019; Wang et al., 2019b; Wu et al., 2019) by providing a more detailed and nuanced analysis of the hedging and safe-haven properties of Bitcoin against the disaggregated measures of U.S. economic uncertainties.

Conclusion

Previous studies consider the impact of U.S. aggregate economic policy uncertainty on Bitcoin returns to make a hedge and safe-haven inferences. However, they disregard the impact of categorical U.S. EPU data that covers disaggregated measures of uncertainties such as monetary, fiscal, regulatory, trade, and political uncertainties. To address this literature gap and account for the aggregation effect in the U.S. EPU, we examine the impact of categorical U.S. EPU indices on Bitcoin returns. Specifically, we employ quantile regressions augmented with dummy variables to take into account various states of the Bitcoin market.

The results indicate that Bitcoin is a weak hedge against all the uncertainty categories considered under bearish and normal market conditions. However, Bitcoin is a strong hedge and safe-haven against some categorical EPU, including fiscal policy, taxes, national security, and trade policy under bullish market conditions.

The policy implications concern the particularity of Bitcoin as a digital assets class that is very useful for investors, financial advisors, and risk managers making decisions involving the risk of specific measures of U.S. economic uncertainties. Furthermore, the findings could be useful to investors operating in conventional and cryptocurrency markets. They indicate that investors should monitor developments in taxes, fiscal policy, national security, and trade policy in order to be better prepared for uncertainty and hedge their conventional portfolios based on Bitcoin. Additionally, investors can benefit from our results by specifying more suitable portfolio design. During high uncertainty periods, investors can incorporate Bitcoin in their portfolios for hedging purposes. However, considering Bitcoin in such investment decisions would be most suitable when the Bitcoin market experiences a bullish state.

While our empirical analysis involves categorical data from the United States only, it would be interesting to extend the analysis by considering categorical EPU data from other countries and regions such as China and Europe. This might be done when such disaggregated data becomes available. Another potential path for future research could cover the role of other leading cryptocurrencies such as Ethereum and Ripple.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research and/or authorship of this article.