Abstract

In an increasingly competitive market, customer retention is imperative for businesses in the services sector, particularly banks. This study aims to understand how relationship quality as second-order impacts repurchase intentions based on the Theory of Repurchase Decision Making (TRD). The switching cost moderating role is addressed. The model was validated using empirical data from Pakistan. A regression modeling was adopted to measure the research hypotheses that underpinned a proposed conceptual model. Results show that relationship quality positively and significantly influences the repurchase intentions. Switching cost determined to be a moderator between relationship quality and repurchase intentions. The implication is that services industry professionals should not overlook the importance of relationship quality and switching costs, as they have a significant impact on repurchase intentions.

Introduction

In a highly competitive environment, businesses are desired to keep the current customers (Antwi, 2021). The growing competition creates serious challenges specifically for the services industry, mainly retaining current customers. Customers retention becomes an important event for service providers to sustain market share (Darzi & Bhat, 2018). This is a phenomenon related to the individual (consumer or customer) that will repeat to buy products or services of a similar brand or company in the future (Parawansa, 2018). Therefore, individuals’ process to repeat the purchase is being considered an essential element in customers’ behaviors (Liang et al., 2018). In this case, customers behavior is opportune for companies to understand the value of customers satisfaction, as they cultivate trust-based on positive experiences, and remains committed to the brands or services providers (Boonlertvanich, 2019; Mahmoud et al., 2018).

Organizations are well aware of the cost incurred for attracting new customers than retaining existing customers (Pollack, 2015). Specifically, over time, service-providing firms are more focused on knowing about the relationship role in customer retention. The cultivation of high relationships with customers gains much weight (Brun et al., 2016). They realized the importance of relationship quality that cannot be easily replicated by rivals. Relationship quality provides a competitive edge to a service provider by sustaining customers (Chi et al., 2020). Furthermore, relationship quality strongly predicts customers’ behavioral intentions (Fernandes & Pinto, 2019; Roberts et al., 2003).

Relationship quality in investigating effective relationships considers essential for the services industry (Narteh, 2018; Walsh et al., 2010). It plays a significant role in continuing relationships with a service provider (Al-alak, 2014; Lam & Wong, 2020). In a few studies satisfaction (SAT), trust (TR), and commitment (COM) were studied as fundamental factors of relationship quality, which shapes the customer’s behavioral intentions (Foster & Cadogan, 2000; Petzer & van Tonder, 2019). These factors are also named pull-in forces to retain existing customers (Liu et al., 2011); this affects the customer and service provider relationship continuity (Huntley, 2006; Wisker, 2020). However, literature has revealed inconsistent opinions related to the roles of SAT, TR, COM, for example, some revealed as antecedents of relationship quality (Morgan & Hunt, 1994; Naudé & Buttle, 2000; Sperandio Milan et al., 2019), others explained SAT direct impact on relationship quality (Darzi & Bhat, 2018; Kaur & Soch, 2018), and few explores TR and COM roles as mediators under different research settings (Garbarino & Johnson, 1999; Morgan & Hunt, 1994). The first research gap concerns the combination of SAT, TR, and COM are considered to measure the second-order construct, that is, relationship quality, which impacts repurchase intentions in the services sector.

In the services industry, switching cost as a switching barrier also plays a more significant role in influencing repurchase intentions (Chebat et al., 2011). The intense rivalries put pressure on businesses to retain the existing customers by increasing switching costs (Koo et al., 2020; Pollack, 2015). In this situation, the high switching cost is more effective for customer retention (Chebat et al., 2011; de Matos et al., 2013; Li, 2015). The literature provides that switching cost as moderator has limited insights in services settings. Therefore, the second research gap focused on moderating the role of switching cost between relationship quality and repurchase intentions.

To address these gaps, this study has the two main objectives to understand customers retention in the services (banking) settings. To better comprehend the factors affecting customers’ repurchase intentions, we have drawn on relationship quality (second-order construct) literature that impacts repurchase intentions in the banking context. Further, this study makes clear that switching cost influence the relationship between relationship quality and repurchase intentions. The two most pressing issues researchers have dealt with are following:

How does relationship quality impact repurchase intentions in the services (banking) sector?

What role does switching cost play in moderating the relationship between relationship quality and repurchase intentions?

The rest of the paper presented the literature review on relationship quality, switching cost, and repurchase intentions that provides the basis for hypotheses development. The next section gives the details related to the methodology that includes sampling techniques and measures. Then we presented the results and discussions which explains the empirical model, regression assumptions measurements, and hypotheses results. The direct and moderation impacts between predictors of repurchase intentions measured through regression techniques. The last part explicates discussions, theoretical and practical implications, and concludes with potential limitations and future directions.

Theoretical Foundation and Hypotheses

Relationship Quality

Relationship quality can be explained as a tool that measures the customer intent and scope of relationships with their service providers (Athanasopoulou, 2009; Roberts et al., 2003; Su et al., 2016). Relationship quality plays a vital role in developing a good or bad relationship between buyers and sellers; their quality of relationship assessment consists of different dimensions. The most prominent dimensions are TR, need, power, integration, and profit (Naudé & Buttle, 2000). Moreover, relationship quality within the context of service selling was investigated by the relationship quality model that measures the nature and consequences. Customers perceived the salespersons’ previous interactions, expertise, and future interactions that affect sales performance. Despite the uncertainty, salespersons are tried to develop customers’ confidence (TR) by meeting their expectations (SAT) (Crosby et al., 1990). Relationship quality creates future sales opportunities to convert them into sales by relational interactions. And relational selling behaviors develop a robust buyer-seller relationship (Ryu & Lee, 2017).

Customers take their actions based on perceived service quality and SAT, which creates opportunities to develop a profitable long-term relationship (Antwi, 2021; Kant & Jaiswal, 2017; Kim & Kim, 2016). The relationship quality construct elements are related to each other, which consist of the following concepts customer SAT, relationship strength, relationship length, and customer relationship profitability (Santouridis & Veraki, 2017). In the services sector, relationship quality (TR and SAT) is significantly affected by the following antecedents: customer orientation, domain expertise, service recovery, and interpersonal relationship (Cheng et al., 2008).

Relationship quality consists of three factors, which are the SAT, TR, and COM. These factors play an essential role in generating repurchase intentions. Specifically, SAT and COM positively influence customers’ repurchase intentions (Rosenbaum et al., 2006; Wisker, 2020). Relationship quality elements SAT, and overall service quality is significantly impacting the repurchase intentions of customers. Also, overall quality, COM, and TR strongly affect attitudinal loyalty. Customer loyalty can be increased by improving the relationship quality (Rauyruen & Miller, 2007).

Relationship quality plays a crucial role in developing long-term relationships and influencing profitable customer relationships. The quality of relationships between buyer-seller is determined by the TR, COM, and goal congruity. The relationship quality strongly influences the promising outcomes (actual sales, recommendation intentions). Whereas TR, COM, and goal congruity positively affect relationship quality (Huntley, 2006; Wisker, 2020).

Impact of Relationship Quality on Repurchase Intentions

Relationship quality (SAT, TR, and COM) plays a crucial role in the services sector, positively affecting the customer’s loyalty (Abdul-Rahman & Kamarulzaman, 2012; Boonlertvanich, 2019). Another study describes that SAT and TR also significantly affect customer loyalty (Lin et al., 2008; Melián-Alzola & Martín-Santana, 2020). Furthermore, calculative COM significantly affects customer retention (Gustafsson et al., 2005; Moriuchi & Takahashi, 2016); and service quality affects the customers’ behavior intentions through SAT (Cronin et al., 2000). Additional study findings reveal that relationship quality positively and substantially influences the purchase intentions of customers. Moreover, vendor characteristics positively impact relationship quality, and distrust in vendor behavior harms the relationship quality (Zhang et al., 2011). The above discussion provides that relationship quality was measured with SAT, TR, and COM in different research settings like few consider TR and COM, and others mentioned SAT and TR. However, the relationship quality (second-order construct) has been ignored in the services sector like the banking industry of Pakistan. Not much work has been done on relationship quality impact on customer repurchase intentions. There is a need for additional research in this area. Hence, we proposed the hypothesis;

The Moderating Role of Switching Cost

Switching cost is stated as customers’ decision to remain connected in the future with service providers or products (Hume et al., 2007). Switching cost as a moderator plays a critical role, which affects the relationship between SAT and COM. The analysis results describe that switching cost significantly and positively moderates the relationship between SAT and COM. Moreover, switching cost can retain the existing customers with the service provider (De Matos et al., 2009; Kaur & Soch, 2018; Pollack, 2015). Switching cost considerably and positively influenced the relationship between SAT and COM (Chebat et al., 2011; Li, 2015). Furthermore, switching costs dimensions impact the association between SAT and customer COM. When the customers’ SAT level is low, the customer retains only by enhancing the switching barriers (Kim et al., 2004).

Switching cost moderates the relationship between customer loyalty and SAT. It is interesting to know that switching cost affects customer loyalty when customer perceived value and SAT are above the average. This state explained that customers did a cost-benefit analysis, and they get more benefit than cost. Averse to this condition, when customers are not much satisfied, then switching cost has no moderating effect on the association between customer SAT and customer loyalty (Koo et al., 2020; Yang & Peterson, 2004). Another study confirmed that customers are highly satisfied, switching barriers has no considerable moderation influence on repurchase intentions. However, low satisfied customers’ repurchase intentions are positively affected by the switching barriers. Moreover, as expected, switching cost and repurchase intentions vary according to the services industry (Jones et al., 2000, 2002; Kaur & Soch, 2018).

The above discussions provide that switching cost moderating role was explored with SAT, Loyalty, and COM, however, its impact on the association between relationship quality and repurchase intentions was overlooked in the banking sector context. This gap compels us to investigate the switching cost moderation effect. Therefore, we postulate the following hypothesis.

Empirical model

This empirical study model is developed to deepen our understanding of customers retention strategies in the banking context. The process of repurchase decision-making is based on several factors determined by the post-purchase and personal decision-making process. We mainly included the relationship quality factor in deciding the repurchase intentions. Additionally, the role of switching cost as a moderator between relationship quality and repurchase intentions is studied. The Theory of Repurchase Decision Making (TRD) is one of the most critical behavioral theories to understand customers underlying motives for repurchase behavior. Previous studies have empirically tested TRD to examine the role of different factors, that is, SAT, TR, and switching cost, significantly contributing to reshaping the behavioral intentions (Han & Ryu, 2012; Narteh, 2018; Petzer & van Tonder, 2019). Thus, our empirical study considered TRD a crucial theoretical model to determine the impacts of relationship quality (i.e., SAT, TR, and COM) and moderator switching cost on repurchase intentions (behavioral outcome). This empirical study model has deepened our understandings of constructs, as shown in Figure 1.

Empirical model.

Methodology

Sampling

In the first stage, the original construct elements (in English) were translated into Urdu (Pakistan native language) and then back-translated into the original construct with linguistics experts. Additionally, marketing professors’ services were hired to review the constructs critical. Furthermore, the psychometric properties of constructs were checked with five randomly selected audiences. The response shows that audience was able to understand the construct elements.

To collect the primary data, a personally administrated survey was conducted in metropolitan cities of Pakistan. The survey was conducted for approximately 3 weeks, from August 13 to September 03, 2019. A convenience sampling method was used to collect the data (Sohaib et al., 2019), and 300 research questionnaires were distributed to conveniently available customers from different banks. The respondents were requested to take 10 to 15 minutes to complete the questionnaire by considering their relationship with the bank, switching cost, and repurchase intentions about the current service-providing bank. A total of 260 questionnaires was returned, out of which 14 questionnaires were not included in the data analysis due to incomplete information. Finally, 225 questionnaires were included to study data because the box plot detected 21 responses as outliers, and these responses were deleted from the data file. The data cleaning process was adopted as reported by Hair et al. (2010). The response rate to the questionnaire was 87%. Hair et al. (2010) stated that ten observations should be taken against each measure of the construct. Therefore, this study sample size was acceptable.

Sample Profile

The demographics of the data were presented in Table 1. Our study’s significant proportion was based on male respondents, as Pakistan is a dominant male society, and it is not easy for a homemaker to deal with banks’ financial matters. However, the data collection team managed to collect the data from 65 females. The randomly selected respondents were from representative banks in Pakistan accounted for Bank Alfalah Limited (BAL) 16.4%, Habib Bank Limited (HBL) 14.7%, United Bank Limited (UBL) 13.8%, Muslim Commercial Bank (MCB) 12.9%, National Bank of Pakistan (NBP) 9.8%, and Allied Bank Limited (ABL) 8.4%.

Demographics.

Measures

A comprehensive questionnaire was designed for the collection of primary data. The empirical model involved SAT, TR, COM, switching cost, and repurchase intentions as measurement constructs. Specifically, SAT, TR, and COM are first-order constructs that measure relationship quality as a second-order construct. TR and COM were measured by five and seven items consecutively on a seven-point Likert scale “1 = strongly disagree” and “7 = strongly agree.” Measures of TR and COM were adapted from the previous studies (Brown et al., 2019; Brun et al., 2016; Morgan & Hunt, 1994). The one item of TR was negatively worded as “In our relationship, my bank cannot be trusted at times.” This item of TR was reverse coded for the accuracy of the results. SAT was evaluated with three items on a seven-point Likert scale with anchors like “1 = Very Low” and “7 = Very High,” which were initially taken from (Brun et al., 2016).

The overall concept of switching cost as a moderator is explained in the shape of time, value, and money. These were measured with three items on a five-point Likert scale given by Jones et al. (2002). The rating scale measures against the following anchors as “1 = strongly disagree” and “5 = strongly agree.” Lastly, repurchase intentions as a dependent variable were assessed with four items on a seven-point Likert scale developed by Garbarino and Johnson (1999). The rating scale consists of the following anchors, “1 = strongly disagree” and “7 = strongly agree.”

Previous studies miss the links with SAT, TR, and COM that measures relationship quality as second-order (Kaur & Soch, 2018; Morgan & Hunt, 1994; Petzer & van Tonder, 2019; Wisker, 2020). Switching cost is also considered an important element that influences customers’ loyalty and commitment in a few studies (Chebat et al., 2011; de Matos et al., 2013). It provides the basis that switching could retain the customers. Hence, switching cost moderating role was considered. We adopted 22 measures to test the empirical model.

Data Analysis and Results

Evaluation of Measurement Model

The data were analyzed using SPSS 22 (Fida et al., 2020). The reliability statistics explained that all the constructs’ values ranged from .682 to .883. See details in Table 2. The minimum requirements were met, ranging from .60 or .70 (Hair et al., 2010; Nunnally & Bernstein, 2010). Afterward, the factor analysis technique is used to measure the underlying structure among variables. The factors of variables were categorized by using principal component analysis through the extraction method. Bartlett’s test of Sphericity and Kaiser Meyer Olkin (KMO) measured the appropriateness of inter-item correlations. Bartlett’s test of sphericity value p = .000, p < .05 explains that all the independent variables that were loaded on the correlation matrix had good correlations to the factor analysis. The KMO value of .886 was more significant than the minimum acceptable range of .50. A value greater than .80 called meritorious value means inter-correlation among the variables was adequate, and factor analysis of factors was appropriate. The rotation results elucidate that one TR and SAT item were removed due to disassociation with constructs.

Reliability Statistics.

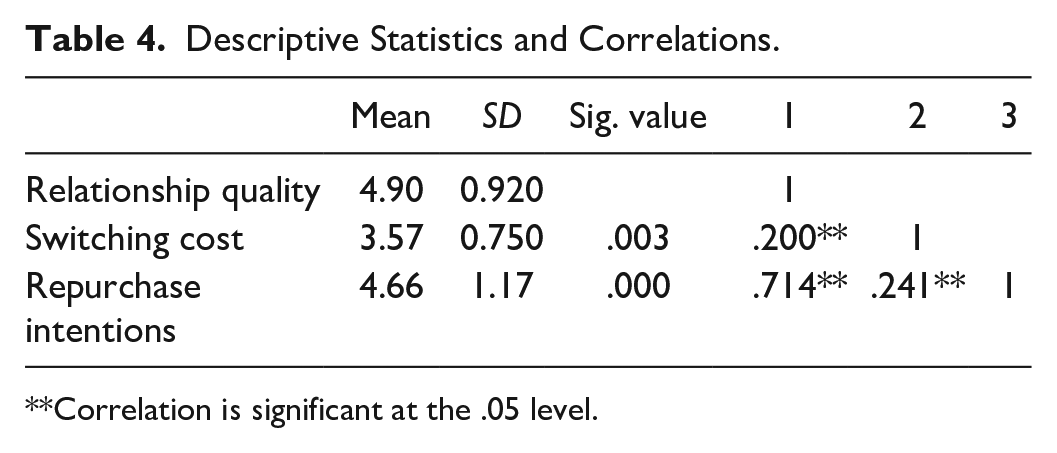

The Kaiser-Meyer-Olkin (KMO) test gives the results as, Chi-square = 1,609.77, KMO value = .886. Although, KMO value .886 was more significant than the minimum acceptance value of .50 for the measure of sampling adequacy (MSA). Also, this value was more excellent than the .80 value of MSA is called meritorious value. It means that inter-correlation among the variables was adequate, and factors for factor analysis were appropriate. Moreover, Bartlett’s test of Sphericity value p = .000, p < .05 explains that all the independent variables that were loaded on the correlation matrix had sufficient correlations among them to proceed for the factor analysis (Hair et al., 2010). The factor analysis outcomes are explained in Table 3. Furthermore, Table 4 reveals the descriptive statistics and partial correlation, which explains the correlations among the variables by controlling the Age, Gender, Income, Education, and Occupation.

Factor Analysis.

Note. TR and COM two items were deleted due to cross-loadings. TRS 5 = .790, COM 7 = −.847.

Descriptive Statistics and Correlations.

Correlation is significant at the .05 level.

Regression Assumptions Measures

The prerequisites of regression should be fulfilled before the analysis. Specifically, regression assumptions were taken into consideration to improve the predictive ability of predictors. The normal distribution of dependent, independent, and moderating variables was investigated by the Kolmogorov-Smirnov test and the Shapiro-Wilk test. These test values were explained that data were normally distributed over the variables. Furthermore, multicollinearity and autocorrelation among values were measured with tolerance value, variance inflation factor (VIF), and Durbin-Watson test. In linear regression model, Tolerance value = 1, 1 > 0.1 and VIF = 1, 1 < 10 make clear that there was no problem of Multicollinearity. Additionally, the Durbin-Watson test value 1.714 < 3 confirmed no autocorrelation problem, and error terms are independent. In multiple regression model, Tolerance value = 0.960, 0.960 > 0.1 and VIF = 1.042, 1.042 < 10 described that there was no issue of Multicollinearity. Moreover, the Durbin-Watson test value 1.757 < 3 clarified that the autocorrelation assumption was fulfilled. Table 5 shows the details about Kolmogorov-Smirnov and Shapiro-Wilk tests.

Normal Distribution Tests.

Hypotheses Testing

The linear and multiple regression equations are described in the following way.

Repurchase intentions = b0 + β 1 × relationship quality + єi

Repurchase intentions = b0 + β1 × relationship quality + β2 × switching cost + β3 × relationship quality × switching cost + єi

To test Hypothesis 1, we used linear regression analysis and analysis of variance (ANOVA). The results explained that the coefficient of determination value was R2 = .510; this shows a 51% variation of the dependent variable defined by the predictor. The model statistics were given as standardized coefficient β = .714, t = 15.235, and p < .005, which suggests that relationship quality significantly and positively affects the repurchase intentions.

The ANOVA results described the model predicting ability. Regression Sum of squares = 156.842 defines the variance explained by the relationship quality of repurchase intentions. Moreover, the residual sum of squares = 150.698 was an unexplained variance by the independent variable. The total degrees of freedom = 224, which was obtained by using N−1, N = 225. The regression degrees of freedom = 1 indicated that one independent variable relationship quality predicted the model and residual degrees of freedom = 223. The result was obtained by Total Degrees of Freedom minus Regression Degrees of Freedom. Hence, mean square of regression = 156.842 and residual mean square = 0.676. Furthermore, the p-value was calculated based on the F value, and both values were explaining the model predicting ability. The significance value p = .000, p < .05, describes that the independent variable had significant predicting ability and relationship with the dependent variable. Therefore, H1 is accepted. These results are consistent with previous studies. Relationship quality was considered as a higher-order construct that consists of SAT, TR, and COM. Although repurchase intentions are related to behavioral loyalty, and this is influenced by relationship quality. Accordingly, relationship quality and repurchase intentions have a significant relationship with each other (Rauyruen & Miller, 2007; Wisker, 2020).

Hypothesis 2 was tested with stepwise multiple regression. In the first step, relationship quality and switching cost were entered as predictors. The second step considered the interactive impact (relationship quality × switching cost) on the association between relationship quality and purchase intentions. The outcomes illustrate that switching cost positively and significantly moderates the relationship between relationship quality and repurchase intentions (β = .799, ΔR2 = .010, p < .05). The stepwise multiple regression results are shown in Table 6. Hence, H2 is supported. Previous studies found that switching cost impacts the relationship between SAT and COM under different research settings (Chebat et al., 2011; Kaur & Soch, 2018; Pollack, 2015; Yang & Peterson, 2004). The gap in the literature is clear that roles of switching cost as mediator and moderator were mostly explored with SAT, loyalty, and COM; however, its moderating role among relationship quality and repurchase intentions in the banking sector was overlooked. This provides a reason to gauge the switching cost role which is significant.

Moderation Analysis Statistics.

Predictors: relationship quality, switching cost.

Predictors: relationship quality, switching cost, interaction term (relationship quality × switching cost).

p < .05.

The interaction plot also explains the moderating variable impact. The field depicts the dependent variable on the y-axis, the independent variable on the x-axis, and moderating variable on the right-side legends. The low switching cost and high switching cost lines are interacting at the short relationship quality. The main effects of switching cost look at the stable line, and the dotted line is high or low. The solid line is a bit higher than the dotted line. Hence, the main effects of switching cost can be concluded as high switching cost could significantly affect the association between low relationship quality and repurchase intentions. The significant increase in switching cost can raise the repurchase intentions, see Figure 2.

Interaction plot.

Discussion and Conclusions

Customer retention in the banking sector is a significant concern. Hence, it is indispensable to find out ways to retain existing customers. This empirical study unveils the relative importance of relationship quality and switching cost through TRD, which can shape customers’ repurchase intentions. Accordingly, we highlighted that SAT, TR, and COM are first-order measures. It provides the basis to gauge the relationship quality as a second-order construct. The results discussions are provided below.

The H1 results showed that relationship quality significantly and positively influences customers’ repurchase intentions in the banking sector. The verdicts directed that quality of relationship with customers is essential to increase their loyalty with banks, ultimately enhancing their repurchase intentions. The retention of customers is the key to success in any business. Therefore, it is essential to retain the existing customers by enhancing relationship quality with them. Specifically, banks can improve the relationship’s quality by increasing customers’ SAT, TR, and COM, leading to increased repurchase intentions. The findings are consistent with previous studies explaining that relationship quality plays a leading role in the relationship between customers and service providers. It is constructed upon three first-order measures, that is, SAT, TR, and COM. Specifically, relationship quality significantly and positively influences the customer’s repurchase intentions, which ultimately affect the firm performance and business relationships (Fernandes & Pinto, 2019; Lam & Wong, 2020; Vieira et al., 2008). Relationship quality converts sales opportunities for future sales, which significantly affects customers’ intentions and sales opportunities (Ryu & Lee, 2017). Another study investigates that relationship quality plays a vital role in the services sector, and also this positively affects customer loyalty (Abdul-Rahman & Kamarulzaman, 2012; Petzer & van Tonder, 2019).

The outcomes revealed that switching cost significantly and positively moderates the relationship between relationship quality and repurchase intentions (H2). It is worth noting that if customers’ SAT level is low with the service provider, then an increase in switching cost could better retain the existing customers. This result has corresponded with previous studies, which elucidates that switching cost as moderator positively affects the customers’ repurchase intentions when the SAT level is low due to service providers. The high switching cost has much higher repurchase intentions (Chebat et al., 2011; Li, 2015). Another study confirmed that switching cost significantly and positively moderates the association between relationship quality and repurchase intentions in the services sector (de Matos et al., 2013; Koo et al., 2020; Tsai & Huang, 2007). Overall findings suggest that relationship quality and switching cost are essential elements that play a pivotal role in shaping the repurchase intentions in the banking sector settings. Therefore, we articulated that the utmost attention should be paid while developing an empirical customer retention model within the banking sector.

Theoretical Contributions

The findings of this study make substantial contributions to theoretical work. This research elicits a perceptive comprehension of customers’ relationship quality, switching cost, and repurchase intentions in the banking context. It primarily integrates the TRD to examine the role of switching cost in the relationship quality-repurchase intention association. This theoretical perspective adds new insights to the existing literature, laying the groundwork for comprehending the associations between relationship quality, switching costs, and repurchase intentions in the banking sector.

A second-order construct known as customer relationship quality was also included in the study, and it was derived from the first-order constructs, SAT, TR, and COM, which were used to calculate customer repurchase intentions. The results show that the relationship quality is crucial for determining the repurchase intentions of the customers. In addition, a more thorough understanding of behavioral intentions is provided by taking into account switching cost as a moderator between relationship quality and repurchase intentions. It provides insights that both switching cost and relationship quality are essentials for retaining existing customers. Overall, this study has attempted to extend the previous literature on the services industry through probing the roles of relationship quality and switching cost to retain the existing customers in the services industry context, that is, the banking sector.

Managerial Implications and Recommendations

In light of our research, service providers are not only required to adopt the strategies related to relationships but also to track and evaluate the development of relationship quality strategies over time. Evaluating the relationship strengths can identify the areas that need to be addressed. Therefore, managers in banking settings should monitor both relationship quality and switching cost components, such as relational and economic aspects, since only relationship quality is not enough to retain the customers.

The research findings demonstrate, relationship quality is comprised of three factors: SAT, TR, and COM, all of which play a critical role in enhancing relationship quality. To maintain or increase SAT levels, banks need to pay greater attention to the development of SAT and TR that promotes COM. These three elements are pivotal for improving relationship quality which influences customers’ behavioral intentions that are, repurchase intentions in the banking sector.

Fernandes and Pinto (2019) highlighted that service-providing sectors are more conscious about the relationship quality development to retain the existing customers. Since they are well aware of the value of relationship quality, they cannot be easily imitated by their competitors and provide a competitive edge in customer retention. Another study by Kim and Kim (2016) revealed that long-term relationships provide relational benefits to both customers and service providers. Customers perceived the relational value as a special treatment that ultimately influences the repurchase intention.

Moreover, Petzer and van Tonder (2019) revealed that relationship quality significantly affects behavioral intentions and creates the sales opportunities that convert into future sales by the service provider. The relationship quality minimizes the customers’ uncertainty and builds more TR in the service provider. Accordingly, the banking sector needs to develop long-term relationship strategies that reduce both customers’ and banks’ financial risk factors.

Bank managers should realize that switching cost is also a vibrant factor, which can significantly enhance the relationship quality of low satisfied customers and retain the existing customers. Wang (2010) described that short-term relationships can be shifted into long-term relationships by only amplifying the service provider perceived image and value and service quality. It provides the basis that switching cost is much imperious to retain the existing customers. For instance, bank managers can raise the switching cost by developing a long-term relationship with customers. It may influence customers’ behavioral intentions because switching banks could fear losing personalized services, financial loss, and required much effort to learn about the new system.

In light of our research, service providers are not only required to adopt the strategies related to relationships but also to track and evaluate the development of relationship quality strategies over time. Evaluating the relationship strengths can identify the areas that need to be addressed. Therefore, managers in banking settings should monitor both relationship quality and switching cost components, such as relational and economic aspects, since only relationship quality is not enough to retain the customers.

Limitations and Future Directions

This study makes significant contributions to marketing literature and concepts, despite its limitations. We measured the overall switching cost as a moderating variable between relationship quality and repurchase intentions. Further investigation should expand this issue in the banking context. The consideration of monetary and non-monetary types of switching cost could provide better information in comparison. In addition, this data was collected through a convenient sampling technique, which has the potential for biased responses or anomalous results due to the dissimilar nature of the subjects. The results variation should be revealed through comparison among different types of banks and using systematic sampling for data collection. For instance, in banking settings, corporate, commercial, and retail banking relationship quality effects on repurchase intentions can be compared and contrasted. Moreover, our study used repurchase intention as a dependent variable, which is an element of behavioral intentions. Future studies should incorporate the recommended intention that is also the dimension of behavioral intentions. A longitudinal design and experimental research should develop a better understanding related to behavioral intentions at different repurchase times, among other methods. In the last, this empirical study was conducted in only Pakistan banking context. A cross-cultural comparison should provide a much deeper understanding of consumer behaviors in future studies.

Footnotes

Appendix. Constructs

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The work is supported by the Xi’an Eurasia University.