Abstract

International trade frictions have changed the business environment of enterprises. However, how do these changes influence the behavioral decisions of enterprises, and will this further affect enterprise competitiveness? Exploring these questions will help determine the influencing mechanism of external negative impacts, such as international trade frictions, on the competitiveness of entity enterprises. In this study, the influences of China-U.S. trade friction, which served as an exogenous research event, on the competitiveness of entity enterprises were empirically analyzed via a difference-in-difference (DID) model with semiannual report information of Chinese nonfinancial A-share listed companies in 2016 to 2020 as research samples. Research results show that the China-U.S. trade friction promotes enterprises to enlarge their financial asset investment by changing the business environment of enterprises. Moreover, this friction further weakens the enterprise competitiveness, an essential element of industrial investments. As revealed by further heterogeneity analysis, the China-U.S. trade friction has generated heterogenous influences on enterprise competitiveness in the aspects of investment motives, industry, competition status, and internal governance mechanism. In this study, two types of enterprise competitiveness elements—environment and resources—were included into the same research framework, and the category of theoretical research on the connotation of enterprise competitiveness was expanded. Moreover, this research provided new scenes and evidence for identifying the causal relationships of the impacts of exogenous negative events with the financial behaviors and competitiveness of entity enterprises, Furthermore, it rendered countermeasure paths and policy suggestions for scientifically coping with international trade frictions and enhancing the competitiveness of entity enterprises.

Plain Language Summary

This study empirically analyzes the influences of Sino-US trade friction, which served as an exogenous research event, on the competitiveness of entity enterprises via a difference-in-difference model with semiannual report of Chinese nonfinancial A-share listed companies in 2016–2020 as research samples. The results show that the Sino-US trade friction has weakened the competitiveness of entity enterprises. To be specific, such a trade friction promotes enterprises to enlarge their financial asset investment by changing the business environment of enterprises and further weakens the enterprise competitiveness element–industrial investments. On this basis, we also make further heterogeneity analysis test from the perspective of industries, companies’ behavioral motives, competitive status and internal governance mechanism. The study (1) enriches the research related to the economic consequences of international trade frictions, (2) expands the category of theoretical research on the connotation of enterprise competitiveness by integrating two types of enterprise competitiveness elements—environment and resources—into the same research framework, (3) expands the research scope of financialization studies of industrial companies, (4) provides new scenes and evidence for identifying the causal relationships of the impacts of exogenous negative events with the financial behaviors and competitiveness of entity enterprises, (5) renders countermeasure paths and policy suggestions for scientifically coping with international trade frictions and enhancing the competitiveness of entity enterprises. However, restricted by data sources and research perspectives, this study investigated the industrial competitiveness of enterprises on the basis of the presumption of their excessive attention to financial asset investments and neglect of industrial investments. And future research must further optimize the financialization measurement of entity enterprises.

Introduction

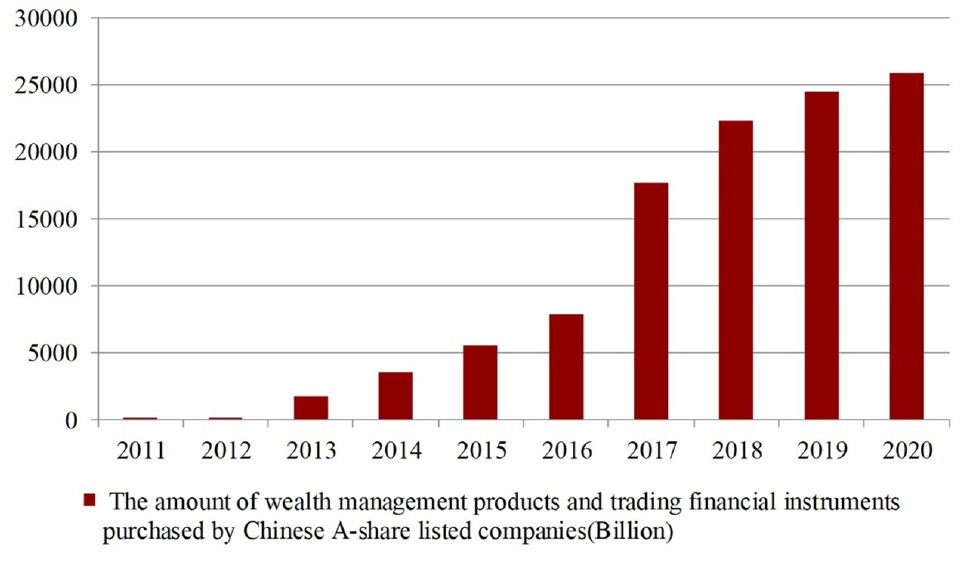

Amid the global economic integration, exchanges among countries have been rising. The number of international trade frictions has grown, thus influencing the economic well-being of bilateral trading countries. In the face of risks and challenges brought by international trade frictions, enterprises need to respond to the above problems by adjusting their investment strategies and enhancing industrial competitiveness (Faustenhammer & Gössler, 2011). For example, during the U.S.–Japan trade friction in the automobile industry in the 1980s, Japan posed voluntary restraint on exports to the United States and reversely forced domestic industrial upgrading and direct foreign investments, thus successfully coping with the trade friction between the two countries (Chu, 2014; Urata, 2020). The course and experience of Japan in dealing with this issue are applicable to the context of the largest-scale China–U.S. trade friction throughout world history. To achieve growth in this adversity, Chinese enterprises must implement scientific and technological innovation to drive industrial upgrading and cultivate emerging industries, all of which need additional industrial investments from enterprises (Xue et al., 2020). Different from the references from past experience, however, entity enterprises have not shown evident industrial upgrading trends after the outbreak and escalation of the China–U.S. trade friction. Instead, enterprises have been keen on financial activities, such as stock and real estate investments. Consequently, the amount of income from financial asset investments has stayed at a high level. Meanwhile, enterprises have extruded and neglected industrial asset investments. After the outbreak of the China–U.S. trade friction, the amount of wealth management products and trading financial instruments purchased by Chinese listed companies has grown accumulatively by 47.09% (Figure 1) compared with the amount before the trade friction. In 2020, the net investment income of A-share listed companies (financial companies excluded) accounted for 29.19% of the total profit of A-share listed companies (financial companies excluded) in the same year, thus creating a historical new high. In addition, the net investment income became a trump card for listed companies to boost profits. In sum, the financialization phenomenon of enterprises is more significant than that before the China–U.S. trade friction, which will influence the industrial competitiveness and long-term development of enterprises.

The amount of wealth management products and trading financial instruments purchased by Chinese A-share listed companies.

According to the theory of enterprise competitiveness, resource and environment are important factors influencing the competitiveness of an enterprise (Porter, 1990). The external business environment will trigger the endogenous strategic and behavioral reform of enterprises and further influence the combination mode and allocation efficiency of enterprises’ economic factors and interact with them, thereby realizing the change of enterprise competitiveness and industrial transformation (Geels, 2010, 2014). Practices have proven that companies that adapt to the ever-changing economic environment will gain more resources than those who do not, and their competitiveness will also be strengthened to some extent, and vice versa (Weitzel & Jonsson, 1989). Therefore, environmental factors to the exogenous event of China–U.S. trade friction have been further analyzed. On the one hand, the trade friction, an external impact, will change the past financial position of enterprises and their resource allocation in the supply chain (Peck, 2006). On the other hand, a general background of external negative impacts has been formed due to the trade friction, thus forcing enterprises to change their investment decision-making behaviors and seek for new profitability (Soener, 2015). However, the existing research regarding enterprise competitiveness has mainly concentrated on the evaluation and measurement of enterprise competitiveness (Almazroi et al., 2021; Chikán et al., 2022; Karabag et al., 2014). In a few analyzes on influencing factors, the focus has also been on single factors, such as resource or environment (Hermundsdottir et al., 2021; Rammer et al., 2017). However, environmental factors and resource input have been scarcely included into the same framework to answer the following question: how do external environmental factors, such as trade frictions, influence the effect of enterprises’ investment behaviors and factor allocation on the competitiveness of these enterprises? Hence, the main issues to be solved in this study are as follows: (a) whether the impacts of negative environmental events will trigger the financialization of entity enterprises and (b) how to identify the causal relationships between financial behaviors of entity enterprises and their competitiveness from the perspective of resources.

To explore the above issues, this study performed an empirical test using a difference-in-differences (DID) model with the semiannual report information on Chinese nonfinancial A-share listed companies in 2016 to 2020 as research objects and the China–U.S. trade friction as an exogenous event. Compared with the studies in the existing literature, the contributions and innovations of this study are summarized as follows. (a) The substitution effect between financial asset investment and industrial asset investment supplemented the research perspective and research framework regarding the influences of negative exogenous impacts on enterprises’ financial behaviors and competitiveness. (b) The differential influencing mechanisms of the impacts of external environmental negative events, such as trade frictions, on the enterprise competitiveness at levels of industry, enterprise, and internal governance were verified and deconstructed on the basis of empirical data. Meanwhile, this study lays a foundation for scientifically evaluating the influences of trade frictions on entity enterprises in emerging markets. Furthermore, it provides a new decision reference for enterprises to form and maintain their competitiveness and realize high-quality development under the superposed effect of “new normalcy” on the economy and international trade frictions.

The structure of this study was organized as follows. In Section “Literature Review,” the literature review is presented. Then, the research methods and research data are described in Section “Research Methods and Research Data.” Next, the main empirical results are analyzed in Section “Empirical Result Analysis and Discussion,” including the descriptive statistics, baseline regression analysis, placebo test, robustness test, and further analysis. Section “Discussion” is discussion. Conclusions and policy suggestions are provided in the last section.

Literature Review

Researchers have mainly theoretically explored enterprise competitiveness, which directly reflects the comprehensive national strength of a country. In particular, scholars have focused on theory tracing, conceptual frameworks, and natures and characteristics. The relevant empirical research has been carried out by measuring the level of competitiveness and analyzing influencing factors. All the above problems take the definition of enterprise competitiveness as the logistical starting point (Chikán et al., 2022). The typical definition frameworks for enterprise competitiveness are mainly divided into three major types: market, resource, and ability. As believed by market environmentalism scholars, the competitive advantages of an enterprise mainly depend on the profit potential of its industry and its market position in this industry (Porter, 1980). According to the resource-based view, the scarce, valuable, and differentiated resources possessed by an enterprise constitute its competitive advantages (Wernerfelt, 1984). Competency theory reveals that enterprise competitiveness refers to the core ability of an enterprise to organize and integrate various technologies and coordinate all kinds of production skills; such an ability leads to enterprise differences in efficiency and benefits (Prahalad & Hamel, 1990). Enterprise competitiveness is explained by the three theoretical perspectives with the emphasis on different sources of competitive advantages, which are mutually complementary. Under the “resource–ability–market” theoretical analysis framework of enterprise competitiveness, enterprise competitiveness can be expressed as the ability of an enterprise to provide customers continuously with products or services that are more effective than those that competitors provide by taking full advantage of the resources and environment and to win profits and development further (Chikán, 2008; Jin, 2001). Therefore, resources and abilities serve as the basis for enterprises to win competitive advantages (Sun et al., 2021). Moreover, the environment is a significant factor influencing enterprise competitiveness (Barney, 1991). To sustain competitiveness, enterprises must continuously input resources represented by industrial investments. Meanwhile, the formation and maintenance of enterprise competitiveness are also influenced by the environment to some extent.

From the angle of the resource input of enterprise competitiveness, industrial investment, which is a resource input approach, is one type of enterprise investment activity. In general, the investment activities of entity enterprises can be divided on the basis of the target field into industrial asset investment and financial asset investment, between which a substitution effect is manifested (Tobin, 1965). The financialization degree of entity enterprises is deepened at the price of reducing the enterprise investments on their own industrial projects (Barradas, 2017). Moreover, capitals that ought to flow into the industry are continuously retained by enterprises in the financial system, thus squeezing industrial investments (Tori & Onaran, 2020). On the premise of enterprise resource constraints, excessive financial asset investments may weaken the scale and impetus of enterprises’ industrial investments and further weaken the basis for enterprises to acquire and maintain their competitiveness. Therefore, the financialization degree can serve as a substitutive perspective to investigate enterprises’ industrial competitiveness, namely, a higher financialization degree of entity enterprises leads to their lower industrial competitiveness.

In terms of the environmental influencing factors of enterprise competitiveness, the China–U.S. trade friction has aggravated the uncertainties of enterprise business environment and has given rise to the changes in the operating environment of entity enterprises, thus promoting enterprises to change their decision-making behaviors, adjust resource allocation and asset structure, postpone their industrial investments, wait for opportunities, and seek new profit growth points by deepening the financialization (Akkemik & Oäzen, 2014; Baud & Durand, 2012). Meanwhile, enterprise financing constraints can be further aggravated by credit grudging and credit limit resulting from external environmental uncertainties. Enterprises show evidently increasing reliance upon financial asset investments to maintain a stable cash flow and hedge against risks (Akbar, 2017; Duchin et al., 2017). For the above reasons, enterprises are inclined to allocate resources, which are limited, into financial assets, thereby enhancing the financialization characteristic of enterprise investment management and weakening the industrial investment and competitiveness of enterprises.

According to the literature review, enterprise competitiveness is influenced by enterprise abilities, resources, and external environments. Under the structure–conduct–performance analysis paradigm (SCP model; Bain, 1959), if an industry or an enterprise is subjected to surface impacts or changes in external environments, such changed external environments will influence enterprise behaviors by changing the market structure and resources of the industry or the enterprise (Aldridge et al., 2014; Yoon et al., 2017), which finally spreads to the changes in enterprise competitiveness. Enterprise attractiveness and competitiveness has been expounded by scholars from ability and resource factors, such as social responsibility (Marín et al., 2012), strategic management and corporate governance (Paek et al., 2019; Y. Wang et al., 2020), management control and planning system (Laguir et al., 2022; Wacker & Sheu, 2006), R&D innovation and learning abilities (Sukumar et al., 2020), enterprise culture (Bibi et al., 2020; Kraśnicka et al., 2018), and business models (Koprivnjak & Peterka, 2020). Meanwhile, enterprise competitiveness has also been investigated from environmental factors, such as transport facilities (Z. Liu et al., 2022), environmental regulation (Ramanathan et al., 2017; Stavropoulos et al., 2018), and taxation and financial policies (Turner et al., 2021). Therefore, the previous literature mainly analyzes the impact of single component of the competitiveness of enterprises, and scarcely incorporates multiple components of enterprise competitiveness into the same research framework, not to mention to explore enterprise competitiveness on the basis of structure–conduct–performance causal logic. Moreover, the measurement of competitiveness mainly focuses on enterprise performance, firm-level markups, and construction of a competitiveness evaluation system, scarcely on substitute measurement indicators: enterprise financialization. In this study, the international trade frictions as environmental factor and the financial asset allocation of entity enterprises as resource factor were included into the same research framework. With the exogenous event—China–U.S. trade friction—as the surface impact on enterprises, whether the trade friction expedited the financialization degree of entity enterprises, which is a substitutive perspective, was empirically analyzed in an effort to explore accurately the influences of this trade friction on the industrial competitiveness of entity enterprises. The China–U.S. trade friction triggers the changes in enterprise behaviors by affecting the operation status and market characteristics of enterprises, that is, the microscopic subjects of national economy, thus influencing the enterprises’ comprehensive performance represented by industrial competitiveness. The research on the above problems can expand the scope of research on the China–U.S. trade friction, enterprises’ industrial competitiveness, and the financialization of entity enterprises. In addition, such research can provide a new perspective and new path for scientifically evaluating the impacts of the China–U.S. trade friction, thus improving enterprise competitiveness and breaking through the existing development bottlenecks faced by Chinese enterprises.

Research Methods and Research Data

Sample Selection and Data Sources

Generally, July 6, 2018, on which the first additional tariff list on Chinese imports was released by the United States, has been taken as the time point marking the outbreak of the China–U.S. trade friction in theoretical circles and practice circles. By reference to Zhang (2019) and Ye et al. (2018), nine periods before the China–U.S. trade friction and after the friction were selected as the sampling interval based on the semiannual report data of the Shanghai Stock Exchange and the Shenzhen Stock Exchange listed sampled companies in 2016 to 2020 (the data in 2020 were updated until 2020 semiannual reports), followed by screening as per the following criteria. (a) Financial, insurance, and real estate-type listed companies were excluded. (b) The observation values of initially listed samples during the observation period were excluded to avoid the influence of initial public offering (IPO). (c) Samples with extreme values or outliers, such as ST and *ST companies, were removed. (d) Samples with data missing in the sampling interval were excluded. (e) Samples with the asset-liability ratio >1 were excluded. Through screening and processing according to the above criteria, 23,425 samples were finally obtained. The financial data and characteristic data of enterprises adopted in this study were derived from the Wind database and the CSMAR database.

Definitions of Key Variables

Financialization level (Fin) of entity enterprises. By reference to the practices of Orhangazi (2008) and Duchin et al. (2017), this study uses the ratio of financial assets to total assets was used to measure the financialization level of enterprises. Notably, nonfinancial enterprises may hold monetary funds to meet the production needs of maintaining their normal operation or the investment needs of participating in financial activities; thus, the added value brought to enterprises is limited (Du et al., 2019). Similarly, the long-term equity investment cannot be completely normalized as a financialization behavior, as it usually includes stocks held by enterprises from joint ventures and allied companies to meet production needs, such as related technologies, products, or fixed assets (G. Liu, 2017). Hence, the above-mentioned assets were not considered in this study on for the financialization of entity enterprises according to predecessors’ research and the accounting standards of China. To obtain a steady financialization index and eliminate the heteroscedasticity, the natural logarithm was taken from the financialization index according to the research of several scholars, including Yu and Li (2015), Su and Mao (2019), and Geng and Yang (2019).

Sample group dummy variable (Qualified) of China–U.S. trade friction. The China–U.S. trade friction influenced export-oriented enterprises enjoying the income from exports to the United States with their industry and tariff-targeted products included into the bilateral tariff lists in the trade friction. Therefore, the above enterprises were selected into the experimental group (treatment group) with a value of 1. Non-export-oriented enterprises not influenced by the China–U.S. trade friction and export-oriented enterprises with their industry and products not included into the tariff list were selected into the control group with a value of 0.

Time dummy variable (Post) of China–U.S. trade friction. In this study, July 6, 2018, on which the first round of the tariff list for imported commodities from China had been released by the American government, was taken as a benchmark time point. The value of 1 was assigned to the time of July 2018 onward, and 0 was assigned to the time before July 2018.

Settings of Baseline Regression Model

To verify the above hypothesis, a DID model was used to test the influences of the China–U.S. trade friction on the financialization of entity enterprises for the following reasons. First, the occurrence of the China–U.S. trade friction, an exogenous event, depended on the negotiation and game between the two countries. Furthermore, the occurrence time was unpredictable and random. Second, the influences of the China–U.S. trade friction on enterprises could be divided into an experimental group and a control group according to the products in the tariff lists of the two countries. The commodities in tariff lists were not arbitrarily and blindly determined by China and the United States. Instead, they were determined out of strategic considerations. Consequently, the randomness of the experimental group and the control group might not be satisfied completely. Nevertheless, the randomness could be controlled through the industrial fixed effect. In this study, therefore, the following model was constructed via DID by reference to Goodman-Bacon (2021) and Callaway and Sant’ Anna (2021). Moreover, the annual effect (μ) and industrial effect (λ) were controlled to analyze the changes in the financialization of entity enterprises before and after the occurrence of the China–U.S. trade friction. Moreover, the analysis explores the effects of the trade friction—an exogenous event—on financial asset investment behaviors and further competitiveness of Chinese entity enterprises. The concrete variables and definitions listed in Table 1.

Variable Definitions.

Descriptive Statistics

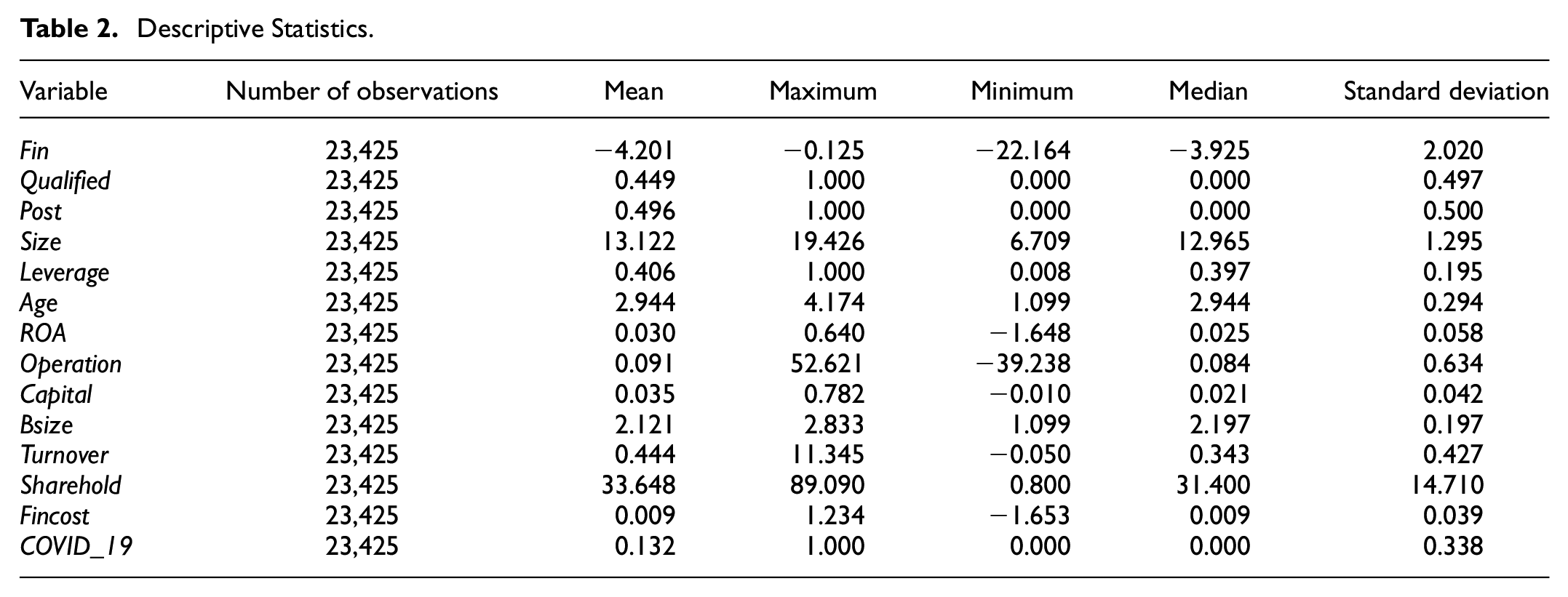

The descriptive statistical results of each variable in the standard regression model are listed in Table 2. The mean value, median, standard deviation, maximum value, and minimum value of the explained variable (Fin) were −4.201, −3.925, 2.020, −0.125, and −22.164, respectively. These values indicate that Chinese entity enterprises were generally financialized with an overall high financialization degree and the financialization degree varied greatly from enterprise to enterprise. The explanatory variable, namely, the sample group (Qualified) of the China–U.S. trade friction, was a dummy variable, with a median of 1. These variables manifested that over half of the entity enterprises were influenced by the China–U.S. trade friction. Compared with the previous research, the sampled data were mostly distributed in a relatively reasonable range.

Descriptive Statistics.

Empirical Result Analysis and Discussion

Parallel Trend Hypothesis Test

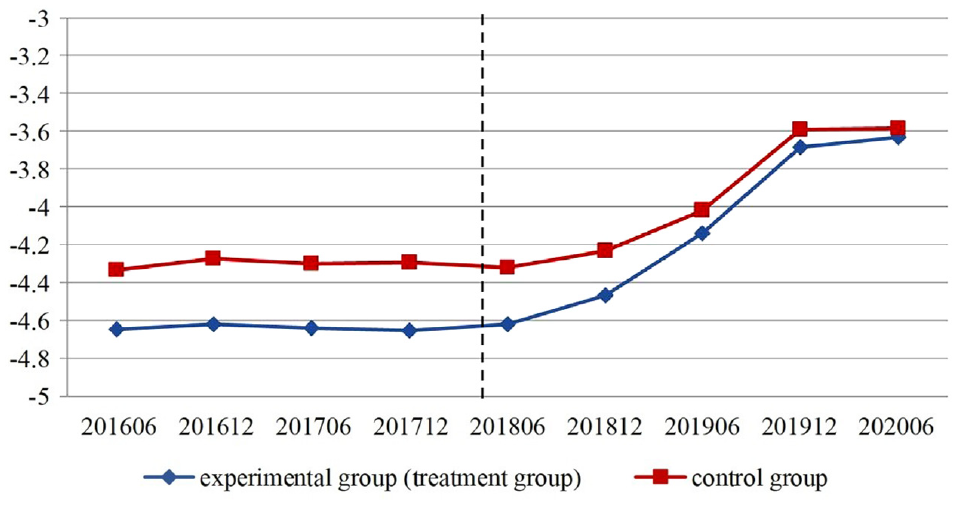

Parallel hypothesis is one of preconditions for the effectiveness of a DID model. The trend distribution diagram of the financialization degree of samples in the experimental group and control group within the same sampling interval is displayed in Figure 2. The dotted line denotes the financialization trend of the experimental group, and the solid line represents that of the control group. As observed from the figure, the enterprises in the two groups showed very different financialization trends from June 2016 to June 2018 (before the outbreak of the China–U.S. trade friction). Such a difference changed steadily. In addition, the financialization degree of enterprises in the control group was higher than that of enterprises in the experimental group. After July 2018 (after the outbreak of the China–U.S. trade friction), the financialization trends of enterprises in the two groups tended to be approximate. Specifically, the financialization trend of enterprises in the experimental group was more evident than and already approximate to that in the control group. Thus, the impact formed by the China–U.S. trade friction on the financialization of entity enterprises was manifested.

Financialization trend chart of entity enterprises.

Baseline regression test

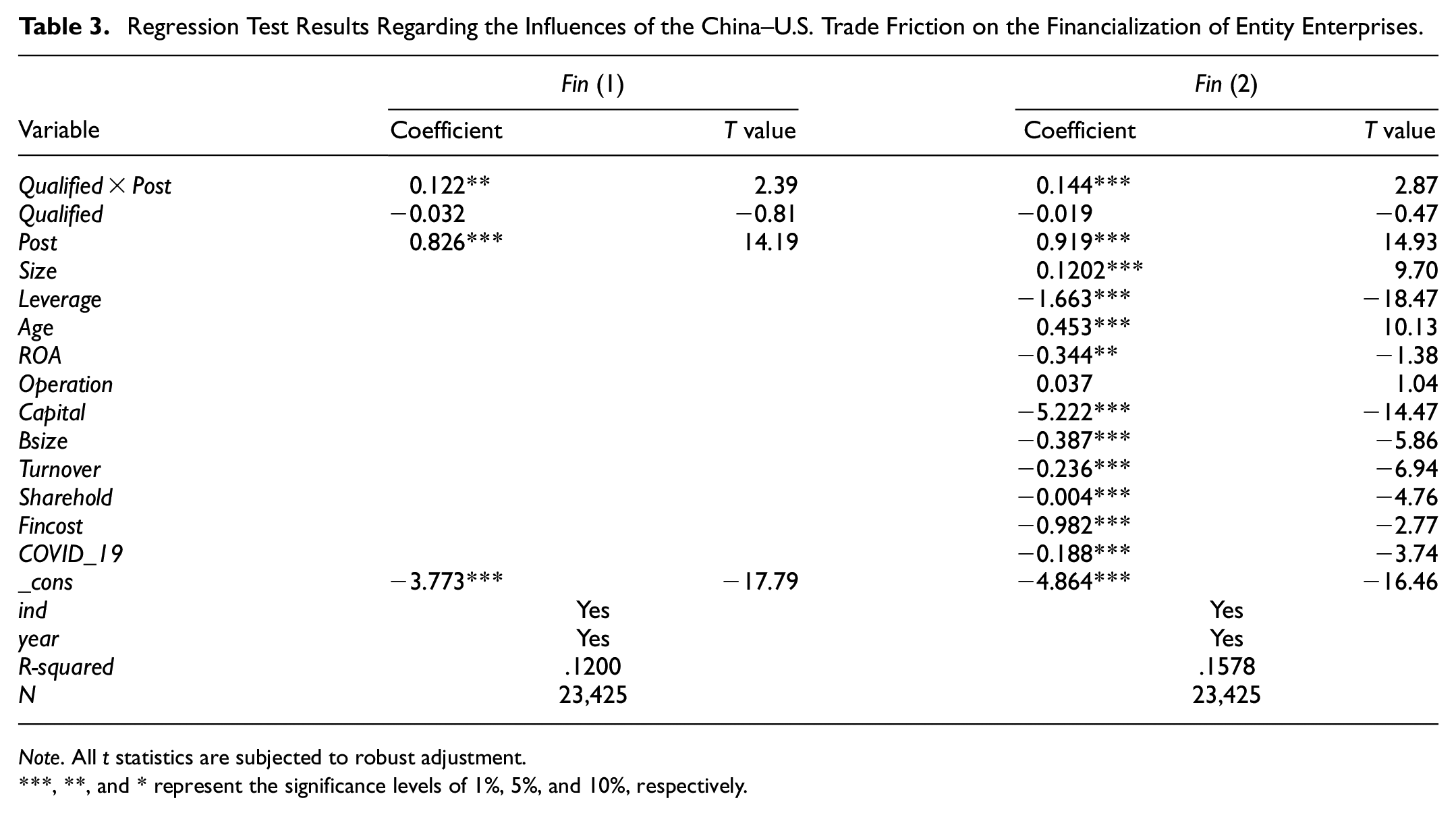

Table 3 lists the test results of the standard regression. Fin (1) and Fin (2) represent the influences of the China–U.S. trade friction on the financialization of Chinese entity enterprises without and with considering other control variables, respectively. The regression coefficients of the explained variable (Fin) and key explanatory variable (Qualified × Post) were significantly positive at levels of 5% and 1%, respectively. This outcome indicated that given the China–U.S. trade friction, entity enterprises tended to hold more financial assets, thus reducing their competitiveness.

Regression Test Results Regarding the Influences of the China–U.S. Trade Friction on the Financialization of Entity Enterprises.

Note. All t statistics are subjected to robust adjustment.

, **, and * represent the significance levels of 1%, 5%, and 10%, respectively.

Placebo Test

Time Resetting of Trade Friction Event

The connotation of the parallel trend referred to the treatment group and control group showing consistent operation trends before the treatment. The empirical results might sometimes be biased due to the disturbance of time variation trends or other uncontrollable factors. To exclude the above possibilities, a counterfactual test was performed, and the fictitious event impact time was reset.

By reference to R. Liu and Zhao (2015), the data after the comprehensive escalation of the China–U.S. trade friction were excluded. Meanwhile, only the samples from 2016 to the first half of 2018 were reserved. We assumed that the China–U.S. trade friction comprehensively escalated and broke out in the first half of 2016, the second half of 2016, the first half of 2017, and the second half of 2017. Then, whether the outbreak time of such hypotheses had any event influence was re-estimated according to the previous empirical test steps.

The above estimation results are listed in Table 4. Columns (1) to (4) present the test results when the China–U.S. trade friction was assumed to occur in the first half of 2016, the second half of 2016, the first half of 2017, and the second half of 2017, respectively. All coefficients of the cross-product term Qualified × Post were insignificant, thus indicating that no significant differences existed between the treatment group and the control group in the early outbreak of the China–U.S. trade friction. In other words, these outcomes confirmed that the China–U.S. trade friction escalated the financialization degree of entity enterprises.

Time Resetting of China-U.S. Trade Friction Event.

Note. All t statistics are subjected to robust adjustment.

, **, and * represent the significance levels of 1%, 5%, and 10%, respectively.

Correction of Samples in the Experimental Group

During the outbreak of the China–U.S. trade friction, other policies introduced in China might have also affected the changes in the financialization degree of enterprises in the treatment group and the control group. Therefore, the samples in the experimental group were corrected to eliminate the influences of policies in the same period on the research results. On September 24, 2018, the General Office of the State Council of China issued the Implementation Plan for Perfecting and Facilitating Consumption System and Mechanism (2018–2020) (the Implementation Plan), which aimed to release domestic demand potentials, promote economic transformation and upgrading, guarantee and improve people’s livelihood, and enhance the fundamental effect of consumption on economic development. The changes of the experimental group and the control group in this study might also be affected by this policy. According to Chen et al. (2019), the industries and enterprises tightly connected to people’s livelihood and consumption, such as medical treatment and communication, in the samples were excluded in the placebo test for regression.

Table 5 displays the regression results after correcting samples in the experimental group. After samples in the experimental group were corrected, the regression coefficient of the interaction term Qualified × Post between core indexes was .155, which was significantly positive at the level of 1%. The result revealed that after the industries and enterprises that might be influenced within the sampling period were excluded, the regression results were largely consistent with the baseline regression results. This outcome proved that the China–U.S. trade friction induced the financialization of entity enterprises and further influenced enterprise competitiveness.

Test After Sample Correction of Experimental Group.

Note. All t statistics are subjected to robust adjustment.

, **, and * represent the significance levels of 1%, 5%, and 10%, respectively.

Robustness test

Selection of Annual Report Data as Sample Data

In this study, the robustness of baseline regression was tested using annual report data to avoid the possible information differences in the transformation of annual report data into comparable semiannual report data.

Table A1 in the Appendix A lists the regression test results of sampled enterprises using annual report data. The test results showed that the coefficient of the cross-product term Qualified × Post was .228, which was significantly positive at the 1% level. The test result of the baseline regression model using annual report data supported the aforementioned baseline regression conclusion. Thus, the model was robust. In addition, COVID-19 did not break out during the sampling period. Hence, the control variable, COVID_19, in the model was deleted.

Propensity Score Matching (PSM) Test

The precondition for using DID was that the samples in the experimental group and the control group were randomly selected in addition to the parallel trend. However, great individual heterogeneity was observed among the sampled enterprises. Moreover, such enterprises were significantly different in the aspects of size, nature, capital volume, and management level, accompanied by a certain self-selection problem. Hence, the comparable control group was acquired through the nearest-neighbor propensity score matching (PSM) to facilitate balanced comparisons between the treatment group and the control group.

Table A2 in the Appendix A presents the regression results obtained through the baseline regression model under nearest-neighbor matching subsamples at proportions of 1:1 and 1:3. The cross-product term (Qualified × Post) of core variables was always significantly positive, which was consistent with the baseline regression test conclusion.

Winsorization Test

In this study, samples were not winsorized in the baseline test. All continuous variables were subjected to 1% and 2% winsorization to avoid the influences of the extreme value processing mode on the research conclusion. Thus, the hypothesis in this study was retested. From the regression results in Table A3 of Appendix A, the coef

Further Analysis

The influences of the China–U.S. trade friction on the financial asset investment behaviors of entity enterprises and their competitiveness were theoretically and empirically analyzed in the previous section. However, the influences of the China–U.S. trade friction on enterprise competitiveness via the financialization of entity enterprises might vary with the industry and enterprise characteristics. On the one hand, different industries might differ in decision making due to the differences in the variety of tax-related commodities and the threshold for industrial upgrading. On the other hand, the trade friction might lead to changes in the enterprises’ internal interests and further affect their investment decision-making behaviors by influencing the internal and external environments. Hence, further analysis was conducted from three levels—industry, enterprise, and senior management—to investigate the concrete influences of the China–U.S. trade friction on the financialization and competitiveness of entity enterprises considering the heterogeneity. This examination aimed to provide some directions for follow-up policy suggestions.

Specifically, labor-intensive industries were distinguished from capital-intensive industries in terms of industrial level to test the influences of the China–U.S. trade friction on the financialization degree of enterprises in different industries. At the enterprise level, the precautionary saving motivation was differentiated from the speculative arbitrage motivation from the angle of motivation to explore which motivation the China–U.S. trade friction deepened the financialization of entity enterprises. From the level of competition, enterprises under high competition status were differentiated from those at low competition status to test the influence of the China–U.S. trade friction on enterprise financialization with different levels of competition. At the level of managers, executive compensations were differentiated to investigate the various influences of the China–U.S. trade friction on the financial asset investment decisions of senior managers with different compensations.

In sum, the research framework for further analyzing the influence of the China–U.S. trade friction on the financialization of Chinese entity enterprises conformed to the following idea (Figure A1 of Appendix A).

Consideration of the Influences of Industrial Differences

Industries are subjected to different influences of trade friction. Thus, these industries make heterogeneous decisions, which are ascribed to the differences in the variety of tariff-targeted commodities, and upgrade the threshold and the demand elasticity for resource elements. Influenced by the China–U.S. trade friction, the cost of labor-intensive enterprises increases. Hence, will they increase enterprise profits through financial asset speculation? Will capital-intensive enterprises increase financial asset investments in the face of the current difficulties or reduce financial asset investments and expand industrial investments to gain more potential competitive advantages? To test different influences of the trade friction between different industries on enterprise financialization, the experience of scholars such as H. Wang and Wang (2019) was referenced in this study, that is, the capital intensity was measured using the ratio of the net value of the fixed assets of sampled enterprises to the total number of enterprise employees. The enterprises with the capital intensity greater than the median or 75 quantiles were classified into capital-intensive enterprises, while others were classified into labor-intensive enterprises. Next, the relationship between the trade friction and the financialization degree of labor-intensive and capital-intensive enterprises was tested in the two groups.

Table A4 in the Appendix A presents the influencing degree of the China–U.S. trade friction on the financialization of Chinese capital-intensive and labor-intensive enterprises. In this study, the partition criteria for the median and the 25 and 75 quantiles were tested. The results under the two circumstances were consistent. Furthermore, the table demonstrates that in both groups, the China–U.S. trade friction exerted significant effects on the financialization degree of capital-intensive enterprises, while the influence on labor-intensive enterprises was insignificant. In other words, the China–U.S. trade friction significantly elevated the financialization degree of capital-intensive enterprises, which coincided with the expectation. Enterprises in capital-intensive industries have high technical thresholds, large inputs, and long investment periods. Under the trade friction, the sustained enterprise operation is affected. In addition, the substantive initial capital input has not been taken back yet. Given the double pressures, enterprises lack the additional technical and financing abilities for the next-round capital investment within a short term. Thus, the senior management layers tend to increase the financial asset investment to realize their own assessment goals or reach the goal of smoothing profits and maintaining stable stock prices within a short term, thus further weakening the competitiveness of capital-intensive industries compared with labor-intensive ones.

Consideration of the Influences of the Difference in Financialization Motivation

The enterprises can allocate financial assets out of different motivations. The financialization out of speculation motivation means that enterprises are subjected to a higher degree of information symmetry and agency problems or the senior management layer is more inclined to self-interest psychology. Driven by such motivations, enterprises always pay added attention to financial asset investments, while industrial investments are neglected. Enterprises holding financial assets out of precautionary motivation will conduct financial asset investments within a short term. However, they are likely to invest funds into the industry if industrial investment conditions permit. Therefore, the difference in the financialization motivation enterprises will influence their future development and competitiveness.

To determine the investment motivation of enterprises, we further decomposed the financialization index according to the findings of Du et al. (2019). Given the high requirements for the rate of return, we used trading financial assets and available-for-sale financial assets to reflect the enterprise motivation of pursing speculative profits and classified them into speculative financial assets. Then, we classified the assets with high hedging and precautionary motivations, such as derivative financial assets, net amount of loans granted and money advanced, held-to-maturity investments, and investment real estates, into hedging financial assets for regression. Then, we analyzed the main motivations for the financialization of entity enterprises.

Table A5 in the Appendix A presents the respective regression results of the speculative arbitrate-type financial asset and precautionary hedging-type financial asset investments of sampled enterprises. Under the arbitrate-type financial asset investment, the regression coefficient of the key explanatory variable (Qualified × Post) was significantly positively significant at the 1% level. In contrast, it was insignificant under the precautionary hedging-type financial asset investment. This outcome revealed that the financialization of entity enterprises induced by the China–U.S. trade friction was manifested more in the speculative arbitrage-type financial assets, which could further weaken the competitiveness of enterprise.

Consideration of the Influences of the Difference in Enterprises’ Competition Status

After the China–U.S. international trade friction escalated, enterprises leading the market as well as those following the market at low competition status all faced major uncertainties. Under this circumstance, will the investment decisions of leading enterprises and enterprises at low competition status be different? Will they continuously expand financial asset investments to overcome the current difficulty or expand industrial investments to gain more pioneering advantages in the future?

By reference to Peress (2010), the approximate value of the enterprise competition status index—Lerner index—was calculated to group the sampled enterprises. A greater Lerner index indicates a stronger product pricing ability of enterprises, a stronger market power of their products, and a higher competition status. We calculated the approximate value of Lerner index through the following formula: Operating revenue—operating cost—selling cost—administrative expense/operating revenue.

Table A6 in the Appendix A lists the grouping regression results of the financial asset investments of sampled enterprises at different competition status under two circumstances: the median partition criterion and the 25 and 75 quantile partition criteria. Under the two partition criteria, the regression coefficient of the key explanatory variable (Qualified × Post) in the group of high competition status was significantly positive, whereas that in the group of low competition status under the two partition criteria was insignificant. The results reflected that the trade friction significantly influenced the investment behaviors of enterprises at high competition status, thus diving such enterprises to invest more in financial assets. Meanwhile, the influence on the investment behaviors in the group of low competition status was insignificant. The enterprises at high competition status still showed a strong market-controlling force under the China–U.S. trade friction, accompanied by smaller impacts and more abundant resources relative to other enterprises. The highlighted market-leading position of enterprises weakened their motivation for industrial investments and laid a foundation for expanding financial asset investments.

Consideration of the Influences of the Differences in Management Compensation

Under the framework of principal-agent theory, the agency problem and information asymmetry allow enterprise managers to satisfy their personal interests through their rights of management and decision making. To explore the influence of compensation on the investment decisions of the enterprise management layer in the case of the China–U.S. trade friction, we used X. Wang and Wang (2016) as reference. Then, we selected the natural logarithm of the average compensation of the three senior managers with the highest compensation to measure the compensation of managers. Next, we analyzed the high-compensation and low-compensation groups of sampled enterprises.

Table A7 in the Appendix A presents the grouping regression results under the different compensation status of senior managers. The financialization degree of enterprises paying high compensation to management layers was high, whereas that of enterprises paying relatively lower compensation changed insignificantly in the face of the China–U.S. trade friction. This variation may be because of the link between the compensation for high-compensation management layers and business performance (Core et al., 1999). When the China–U.S. trade friction severely affects the business performance of an enterprise, the high-compensation management layer will make decisions of financialization, similar to what peer enterprises do to maintain their compensation and reputation and cover their insufficient personal ability. This move not only stabilizes and improves enterprise performance in a profitable case but also shifts the responsibility in investment losses. As a result, the financialization phenomenon is prominent in enterprises with high-compensation management layers, which, to some extent, indicates the universal presence of the management layer’s short-sighted behaviors.

Discussion

The previous empirical results reveal that the international trade friction can induce entity enterprises to allocate additional limited resources to financial assets. Thus, it reduces the cultivation of resources and abilities needed by the industrial development, which then weakens the enterprise competitiveness. This conclusion means that enterprises will not reversely force the industrial upgrading or increase industrial investments under the impacts of negative environments, such as international trade frictions. Thus, enterprise competitiveness will not be enhanced except under powerful policy intervention or consciousness guidance. This notion is evidenced by the previous research conclusion regarding the influence of environmental regulation on enterprise competitiveness. For instance, environmental regulation is one of the environmental factors that business operations face. According to the Porter hypothesis (Porter, 1991; Porter & Vanderlinde, 1995), environmental regulation can promote enterprise innovation, improve productivity, further enhance enterprise competitiveness, and realize economic growth. However, Hancevic (2016) and Stoever and Weche (2018) obtained an inconsistent conclusion with the Porter hypothesis by investigating the influences of environmental tax and water tax on the American power industry and German enterprise competitiveness. In addition, Arouri et al. (2012) and Albrizio et al. (2017) did not support the Porter hypothesis, as under environmental changes, enterprises need to spend additional costs in adjusting and adapting to the environment. Although enterprises can improve their productivity and competitiveness by industrial investment means, such as innovation, upgrading, and investment expansion, whether this approach can offset the cost expenditure brought by environmental changes to enterprises remains unclear (André et al., 2009; Feichtinger et al., 2005). In other words, enterprises will select the financial behavior—industrial investment—only when the additional cost brought by an environmental change to enterprises can be offset by the profits created by activities such as industrial investments. Thus, this outcome demonstrates that environmental change promotes the improvement of enterprise competitiveness. As such, the Porter hypothesis holds true on certain preconditions (Costantini & Mazzanti, 2012; Doganay et al., 2014; Ford et al., 2014). However, when an enterprise cannot judge whether expanding the industrial investment can compensate for the cost brought by adapting to the environment, making a judgment will become especially difficult if the enterprise is subjected to an external negative impact and the operating status is deteriorated. The enterprise, an economic subject of bounded rationality, and its managers cannot proactively step over such a psychological barrier to implement industrial investments, such as industrial upgrading. In the market economy, the primary task of an enterprise is to survive and make profits. Under the current double actions of the scissor difference between virtual economy and real economy and the external negative impact, enterprises can gain high profits through financial asset investments within a long term, thus causing difficulty in making the above scientific judgment. Investing in financial assets can bring higher profits to enterprises within a short term. Thus, enterprises have increased difficulty making scientific judgments. On this basis, the environmental changes, such as external negative impacts, can weaken the competitiveness of entity enterprises under normal circumstances.

Hence, appropriate policy orientation and flexible supervision are required to stimulate the enterprise motivation of industrial investments to change the above situation (Desrochers and Haight, 2014). For instance, government sectors should formulate some policies for guidance to reduce uncertainties to the greatest extent. The concept of innovating and rejuvenating the country through the industry should be formed at the whole social level. Moreover, necessary supporting measures should be equipped to reduce the short-sighted behavior—purely seeking profits—of enterprises. Related policies can be implemented and examined through pilot testing as soon as possible. The key to the above problems lies in flexibly guiding enterprises and helping them to overcome “inertia” and cultivate spontaneously the concept of rejuvenating the country through the industry.

Therefore, certain changes exist in the side effects of the external negative environment on enterprise competitiveness. For instance, in the research, industrial upgrading and foreign direct investment can be selected from the enterprises’ financial behaviors as the research objects to explore the effects of related systems and mechanisms on the abovementioned enterprise behaviors under external negative impacts. Alternatively, the influences of the international trade friction on entity enterprises can be probed from intermediary factors at the level of enterprise operation behaviors, such as financing, production, and profit distribution.

Conclusions and Policy Suggestions

Conclusions

With the realistic investment phenomenon of Chinese enterprises after the China–U.S. trade friction as the research object, a DID model was established to explore the influence of the external negative impact—international trade friction—on the competitiveness of entity enterprises from the perspective of financialization. Different from the previous main research, we included external environments and enterprise investment behaviors into the same research framework to explore enterprise competitiveness by following the structure–behavior–performance causal logic. Meanwhile, we considered the substitution effect of two investment types. When the other conditions are fixed, the China–U.S. trade friction promotes the financialization of Chinese entity enterprises, manifesting, from the perspective of substitutive index, that the China–U.S. trade friction influences and weakens the competitiveness of entity enterprises to some extent. Further analysis of the industrial differences and investment motivations demonstrate that capital-intensive enterprises show a higher financialization degree under the China–U.S. trade friction. In addition, the motivation mostly derives from their speculative behaviors, which reduces the industrial investment of enterprises and weakens their competitiveness. Meanwhile, the differences in enterprises’ competition status and senior management compensation also lead to changes in their resource allocation and further affect enterprise competitiveness. Enterprises with high competition status are more inclined to financialization than those with low competition status. Moreover, high-compensation senior managers are likely to conduct financial asset investments. The abovementioned financialization behaviors induce entity enterprises to pay excessive attention to the virtual economy while neglecting their main business, which weakens their industrial competitiveness to a certain degree.

Policy Suggestions

The above research conclusions provide a basis for scientifically evaluating the influences of the trade friction on the competitiveness of entity enterprises in emerging markets. Moreover, they are of great significance for enterprises to form and maintain competitiveness and realize high-quality development under the superposition of the new “economic normalcy” and international trade frictions. Therefore, we provide the following policy suggestions:

(1) Accelerate the mixed-ownership reform of enterprises and promote dual circular development.

The industrial difference analysis and the heterogeneity analysis of investment motivations show that the China–U.S. trade friction diminishes the industrial investment opportunities of enterprises and facilitates enterprises to reduce industrial investment reserves and increase speculative financial asset investments. Therefore, creating industrial investment opportunities is the key to attracting the attention of Chinese entity enterprises to industrial investments and improving enterprise competitiveness.

On the one hand, the various capitals introduced by state-owned enterprises through the mixed-ownership reform can create a competition mechanism to reduce resource misallocation, transform enterprise concepts, and enhance enterprise vitality and competitiveness. In doing so, state-owned enterprises become the real market subjects. On the other hand, private enterprises form a reasonable check-and-balance ownership structure and perfect corporate governance through “reversely mixed-ownership reform” (Wei & Song, 2020). Hence, they gain additional resources and opportunities for the industrial development via state-owned capitals (Song et al., 2014). Furthermore, the mixed-ownership reform can stimulate the vitality of social enterprises, further promote the realization of “dual circulation” goals, provide enterprises with broader market and investment opportunities to develop the industry, and enhance their competitiveness through multiple channels in an all-round way.

(2) Cultivate the entrepreneurship of enterprise managers and attach importance to the industrial development.

According to the research findings, speculative motivations under the China–U.S. trade friction mainly drive the financialization behaviors of entity enterprises. In particular, competitive enterprises are keener on financial asset investments in the case of relatively abundant resources, which are fundamentally ascribed to the short-sighted interest-oriented behaviors of enterprise decision makers and managers. Cultivating and recruiting responsible and far-sighted managers are indispensable in controlling the financialization behaviors of entity enterprises and promoting their industrial development. Hence, we should pay attention to the cultivation of entrepreneurship at the levels of enterprise and society.

Entrepreneurship is a concentrated reflection of superior traits and outstanding capabilities of enterprise senior managers. Furthermore, it is an intrinsic factor and important fountain influencing enterprise operating decisions and financial behaviors and stimulating enterprise vitality. Entrepreneurial managers can undertake the industry’s social responsibility of rejuvenating the country with a view of long-term development, promote enterprise R&D and upgrading, and master the core competitiveness of enterprises.

(3) Optimize the compensation structure and evaluation method and pay attention to the stimulation of an enterprise’s long-term value.

Given the impact of the China–U.S. trade friction, high-compensation senior managers are more inclined toward financial asset investments, as their compensation is mostly linked to their performance. The China–U.S. trade friction impacts business operation, further induces the self-interest mentality of senior managers, and facilitates senior managers to acquire short-term performance through financial asset investments.

Therefore, a reasonable mechanism and assessment method for senior management compensation incentives can guide the scientific decision-making behaviors of senior managers, which can help to attach importance to the improvement of enterprise long-term values, boost their industrial development, revitalize the real economy, and enhance their competitiveness. First, the assessment of senior managers’ performance should highlight the structure and continuity of corporate profits. Additionally, enterprises should pay much attention to the assessment of the sources of operation income. Second, senior management should establish a classified supervision scheme for the financial asset allocation of enterprises to link their financial asset allocation with their industrial investment ratio. This scheme can avoid the neglect of industrial investments due to the separation of enterprises’ financial asset investments from industrial investments. Third, managers should assess the long-term value growth of enterprises, for example, continuing to promote and popularize the quotation of indexes related to long-term value growth, such as EVA and R&D innovation. Finally, enterprises should elevate the proportion of equity incentives and encourage senior managers to attach importance to the long-term values of the enterprise. In doing so, they can inhibiting short-term interest-pursuing motivations and enhancing enterprise competitiveness.

Research Limitations and Future Expectations

This study utilized empirical data to investigate the influences of the trade friction on the industrial competitiveness of entity enterprises as well as the changes in such influences due to the differences in industry, investment motivation, competition status, and senior management compensation from the perspective of financialization. Restricted by data sources and research perspectives, however, the following problems need further improvement.

(1) This study investigated the industrial competitiveness of enterprises on the basis of the presumption of their excessive attention to financial asset investments and neglect of industrial investments. The industrial investment will be weakened, and the competitiveness will be damaged if financial assets are held excessively for a long time. However, enterprise competitiveness can be enhanced if far-sighted managers can master moderate financialization and back-feed the industry during the enterprise development. Therefore, research can explore enterprise investment behaviors by considering the financialization appropriateness of entity enterprises, which is expected to provide more accurate conclusions and suggestions.

(2) Future research must further optimize the financialization measurement of entity enterprises. Given the restriction of information disclosure, researchers have difficulty distinguishing enterprise demands for financial assets from their demands for industrial development. In addition, researchers also struggle to measure the financialization degree of entity enterprises accurately. In future research, as enterprise information disclosure improves, researchers can more precisely judge whether enterprises have financialization behaviors and observe their financialization degree according to the intentions of their capital expenditures. Doing so can help researchers increase the accuracy of their analysis on the investment behaviors of entity enterprises.

Footnotes

Appendix A

Regression Results (4) of Heterogeneity Analysis: Differences in Senior Management Compensation.

| Variable | (1) Enterprises with high-compensation senior managers | (2) Enterprises with low-compensation senior managers | ||

|---|---|---|---|---|

| Coefficient | T value | Coefficient | T value | |

| Qualified × Post | 0.188*** | 2.57 | 0.094 | 1.13 |

| Qualified | −0.034 | −0.60 | 0.048 | 0.84 |

| Post | 0.782*** | 9.07 | 0.999*** | 10.84 |

| _cons | −4.696*** | −13.72 | −4.728*** | −9.16 |

| Controls | Yes | Yes | ||

| Ind | Yes | Yes | ||

| Year | Yes | Yes | ||

| R-squared | .1676 | .1538 | ||

| N | 10,154 | 10,146 | ||

Note. All t statistics are subjected to robust adjustment.

, **, and * represent the significance levels of 1%, 5%, and 10%, respectively.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Natural Science Foundation of China (71861010, Regional Fund Project); Jiangxi Provincial Association of Social Sciences (19ZK36); Jiangxi Provincial Education Reform Project (JXJG-20-5-18); and Jiangxi University Humanities and Social Sciences Research Project (JJ2120).

Ethics Statement

No human or animal studies are presented in this manuscript.

Data Availability Statement

The data supporting this study’s findings are available from the corresponding author upon reasonable request.