Abstract

How macroeconomic risk affects asset prices is an important issue in the academic and industrial fields. This paper measures Chinese financial stress (CFSI) by constructing a new index, and empirically verifies the pricing relationship between financial stress and Chinese mutual fund returns. First, we use eight source variables, which are the driving forces of financial market risk and financial stability, from bank, security, and foreign exchange markets, to build a new index representing financial stress. In addition, we estimate mutual funds’ exposure to financial stress and find that the resulting financial stress betas explain a significant proportion of the cross-sectional dispersion in mutual fund returns. Moreover, this result also remains robust when we conduct tests using other macroeconomic indices or control for the Fama–French and Carhart four factors. Hence, we argue that financial stress is a powerful determinant of cross-sectional differences in Chinese mutual fund returns and plays an important role in the sustainable development of financial markets.

Introduction

Based on the close relationship between macroeconomic and asset pricing, a hot issue in academic research is to use macroeconomic conditions to predict asset returns. First, the existing literatures demonstrate that mutual funds’ investment strategies and performance are closely related to the macroeconomic changes in advanced countries (Bali et al., 2011; Ferson & Schadt, 1996; Racicot & Théoret, 2016a). In addition, macroeconomic factors related to asset returns involve a large amount of economic and financial data, such as the volatility index (VIX) and economic uncertainty index. Scholars have found that these indices constructed by using big data analysis have significant predictive abilities for stock and hedge fund returns in developed countries (Bali et al., 2014; Drechsler, 2013; Kang et al., 2011; Racicot and Théoret, 2019). However, these big data indices involve numerous data information and complex modeling methods, which are difficult to grasp and realize for microenterprises. Moreover, the current literature does not effectively simplify abundant data information. Therefore, a very important research topic of macrofinance and asset pricing is to extract more effective and important information from abundant market information to construct the investment vane of financial assets.

Second, the institutional, economic, and investment environment in emerging market is quite distinct from that of matured economies (Caglayan et al., 2021; Montiel, 2011). The Chinese mutual fund industry has been developing for more than 20 years since 1998 and has made great achievements. Looking back on the past development process, the Chinese mutual fund industry has become an important subindustry of the Chinese financial system. Moreover, the management of mutual funds in China is different from that in developed countries. Chinese funds are relatively more radical since Chinese fund managers pursue high or ultrahigh yields as the management goal and Chinese mutual fund returns nearly reach hedge fund returns in developed countries. Therefore, the Chinese mutual fund industry is developing rapidly. However, academic research on the Chinese mutual fund industry is still insufficient.

In addition, building a prevention system for financial risk, monitoring financial market risk, and predicting and preventing systemic events effectively are very important research topics to maintain national financial security. Since 2008, the world economy has entered a new stage, and the economic growth rate has changed substantially. Strengthening the prevention and control of financial risks and focusing on national financial stability have become important task for countries. For example, with the Chinese economy entering a new era, its financial operations have also experienced new changes. Ensuring that no financial crisis occurs in China has become the government’s main goal.

As financial stress can reflect important macroeconomic information, this raises a new question regarding whether financial stress can affect mutual funds’ returns in emerging markets, especially in China. Among the previous studies, there are only a few studies focusing on the relationship between mutual funds’ returns and macroeconomics. Therefore, in this paper, we focus on the relationship between mutual funds’ returns and Chinese financial stress. Namely, our paper seeks to answer the question of whether Chinese mutual funds’ exposure to financial stress can predict their future returns.

In this paper, we first choose eight indicators from the bank, security, and foreign exchange markets to construct a new financial stress index; and then we investigate whether mutual funds’ returns are associated with this financial stress proxy using Fama–MacBeth (Fama & MacBeth, 1973) cross-sectional regressions, namely, whether financial stress helps predict mutual funds’ future returns in China. Based on the IMF financial stress framework (Apostolakis et al., 2015; Cardarelli et al., 2011; Vašíček et al., 2017), the new Chinese financial stress index (CFSI) can be divided into three subgroups: the bank market stress index (

In order to empirically test our hypothesis, we run the Fama–MacBeth cross-sectional regressions following Bali et al. (2011, 2014), and we find that the cross-sectional relations between the Chinese mutual funds’ exposures to financial stress and their future returns are statistically positive and significant. In the first stage, we run time series regression to derive the monthly risk exposure

Using a sample of Chinese listed mutual funds over the period from 2004 to 2020, our main finding is that the Chinese financial stress index has a strong positive explanatory power for future mutual fund returns. Actually, in the Fama–MacBeth cross-sectional regressions, we can see that the coefficient is 1.4517, which is significant at the 99% confidence interval after controlling for fund characteristics. This result is consistent with classic asset pricing theory (Campell, 1993; Merton, 1973). Specifically, as financial stress exposure increases by one unit, investors need 1.4517 unit of monthly risk premium as compensation (Table 2 column 5). Furthermore, for the fund, the average monthly risk premium is nearly −0.0595%, and the annual risk loss is −0.714%. In additional, for the max

Furthermore, we compare our new financial stress index to other indices, such as the Chinese macroeconomic climate index, economic policy uncertainty index, volatility index, securities market stress index, foreign exchange market stress index and bank market stress index. The comparison indicates that the other indices’ pricing and forecasting relationship with Chinese mutual funds returns are not positively significant, but our new financial stress index is still the same for mutual funds. This finding remains robust when we control the Fama–French three factors and the momentum factor, namely, the positive relationship between financial stress betas and mutual fund returns remains economically and statistically significant.

Our study contributes to the literature in two ways. First, an easier realized and measured financial stress index is proposed to analyze or track the real-time financial market risk based on macroeconomic fluctuations. The existing research mostly adopts big data or high-order calculation methods involving every macro and micro detail of the economy to track macroeconomic fluctuations, which is difficult for most small and medium-sized financial institutions to use (Balakrishnan et al., 2011; Illing & Liu, 2003). The most famous index, which widely exploits huge data to provide direct econometric estimates of time-varying macroeconomic uncertainty, is constructed by Jurado et al. (2015). However, our new index is much easier to calculate and construct for policy makers or other researchers, especially because all the data for building the index can be obtained from public sources. Second, we can predict Chinese mutual funds’ returns from a new perspective. At present, the Fama–French three-factor model and momentum factor have better predictability for Chinese stock markets, but their impact on the return of Chinese mutual funds remains debatable (Huang, 2019; Kothari & Warner, 2001; Sha & Gao, 2019). Our index not only performs better than the Fama–French three-factor model, but it also captures most of the useful information on macroeconomic fluctuations compared to other indices, such as the Chinese macroeconomic climate index and economic policy uncertainty index. Our financial stress index newly constructed in this paper can predict macroeconomic trends and assist fund investors in correctly and easily predicting future mutual fund market trends.

The remainder of this paper is structured as follows. Section 2 contains the literature review. Section 3 introduces the theoretical analysis and research hypothesis. Section 4 introduces the financial stress index and econometric model design. Section 5 contains the data source and variable statistics. Section 6 gives the empirical results, comparative analysis and robustness tests. Section 7 gives the conclusions and policy advice.

Literature Review

Financial Stress and Economic Effects

In 2008, the world outlook report of the IMF adopted the research of Cardarelli et al. (2009); chose seven indicators including term spreads, TED spreads, the beta coefficient of the banking sector, corporate bond spreads, stock index returns, the time-varying volatility of stock returns, and the time-varying volatility of exchange rates; and constructed a financial stress index for 17 developed countries (Advanced Financial Stress Index, AE-FSI) to measure the risk of financial markets and identify corresponding stress events. The empirical results show that the financial stress index has a forecasting effect for the economy. Subsequently, Hakkio and Keeton (2009) chose more source indicators to measure financial stress in a single city, Kansas City. Balakrishnan et al. (2011) measured the Emerging Financial Stress Index (EM-FSI) of 25 emerging market countries by choosing six source indicators: the beta coefficient of the banking sector, the stock return index, the time-varying volatility of stock returns, sovereign debt spreads, the devaluation of the exchange rate, and the decline of foreign exchange reserves. The EM-FSI has been affirmed and quoted by the IMF, improving the framework of the IMF’s financial stress index.

The construction of the Financial Stress Index (FSI) is exactly in line with the measurement of macroeconomic risk. It selects forward-looking, real-time, and high-frequency data covering financial markets such as stock markets, bond markets, foreign exchange markets, and banking institutions as the data source. Thus, the FSI can dynamically trace the overall risk changes in financial markets from a macro perspective. It is also regarded as a synchronization index of the systematic risk, which can reflect the fluctuations of macroeconomic risks in a timely manner. Furthermore, from the perspective of asset pricing, a change in financial stress is closely related to macroeconomic risk, so it may significantly affect asset returns.

In recent years, scholars have continued to improve the FSI methodology and explore the mechanism by which financial stress affects economic development (Apostolakis and Papadopoulos, 2015; Cardarelli et al., 2011). Vermeulen et al. (2015) and Vašíček et al. (2017) develop a Financial Stress Index (FSI) for 28 OECD countries and examine its relationship to crises. Then, they examine which variables have predictive power for financial stress. Finally, they conclude that financial stress is hard to predict. Hubrich and Tetlow (2015) define a “stress event” as a period of adverse latent Markov states. These stress events line up well with historical events, and shifts to stress events are highly detrimental for the economy. Afonso et al. (2018) study the linkages between changes in the debt ratio, economic activity, and financial stress within different financial regimes. In the most recent related research, Duprey (2020) construct a new systematic financial market stress measure for Canada. This systematic financial market stress measure reached a peak during the COVID-19 outbreak, and the measure at that time was second only to the measure during the 2008 global financial crisis for Canada. Moreover, the latest empirical evidence shows that financial stress can affect the transmission mechanisms of macroeconomic policies. Zhu (2018) and Zhu et al. (2018) diagnosed the risk situation of China’s financial market from the perspective of financial stress and then verified the significant correlation between financial stress and economic policy uncertainty.

Asset Pricing and Macroeconomic Factors

Based on the asset pricing literature, the impacts of changes in economic indicators will affect asset returns through various channels, and macroeconomic factors can be mapped to the trend of financial asset prices directly or indirectly. Chen et al. (1986) and Chen (1991) argue that macroeconomic factors play an important role in the expected return equation of securities. Fama and Schwert (1977), Keim and Stambaugh (1986), Campbell (1987), Campbell and Shiller (1988), and Fama and French (1988, 1989) argue that basic macroeconomic factors (including short-term interest rates, inflation, term spreads, and default spreads) can influence the prices of stocks, bonds, foreign exchange, and financial derivatives through various channels. Following them, Torous et al. (2004) showed that basic macroeconomic variables are not only influencing factors, but they are also good predictors of asset prices. Based on the preliminary research, many studies have provided theoretical and empirical evidence for the relationship between macroeconomic changes and asset returns (Bali et al., 2012; Bloom, 2009; Drechsler, 2013; Jurado et al., 2015). In addition, Cenesizoglu and Timmermann (2012) and Pettenuzzo et al. (2014) made a breakthrough in the theoretical research. They found that the asset return prediction model considering economic variables and economic constraints could improve the performance of the prediction model, affirming the importance of macroeconomic variables to asset return prediction. Furthermore, Kang et al. (2011) and Bali et al. (2017) explored the relationship between financial markets and macroeconomics by combining multiple macroeconomic variables into an index and using multiple macroeconomic indexes. They demonstrated that the macroeconomic index they constructed can capture the stock premium and predict long-term and short-term stock prices well. Therefore, it is necessary to factor in macroeconomic changes when forecasting asset returns.

In recent years, hedge fund returns have become a hot spot in academic research. Fund managers actively seek new investment opportunities. When financial markets change, hedge fund managers will adjust their asset portfolios according to the uncertain information of the leading macroeconomic indicators. The earliest literature in this area is Ferson and Schadt (1996) who explored the investment performance of mutual funds with lagged economic information variables. Then, Avramov et al. (2011) believed that fund managers’ skills were related to the prediction of hedge fund returns, and the prediction ability based on macroeconomic variables can more effectively help managers form the optimal portfolio. Bali et al. (2011, 2014) found that the risk exposure

However, is the relationship the same between mutual funds and macroeconomic changes? The academic research remains controversial, and related references are rare at present. In terms of efficient markets, such as the US funds market, Bali et al. (2014) show that the risk exposure of mutual funds to macroeconomic uncertainty was not positively significant, and macroeconomic uncertainty could not predict cross-sectional differences in mutual fund returns. They argued that mutual funds in the US seemed to lack market timing abilities. Zheng et al. (2021) analyzes that mutual fund managers possess skill in timing stock market misvaluation. Caglayan et al. (2021) consider that mutual fund herding plays on the return comovement in Chinese equities. Therefore, this paper chooses the Chinese fund market as the research target and constructs a new financial stress index containing macroeconomic risks as the indicator, aiming to prove that the financial stress index can be a leading signal index of an economic cycle.

In addition, the latest literature focuses on the risk-price relationship between financial stress and various types of assets (including digital currency, commodities, and fixed assets) and suggests that governments should pay attention to the supervision of financial stress. Bouri et al. (2018) show that Bitcoin can act as a safe haven against global financial stress from a medium-term perspective. Lee et al. (2019) found that financial stress do have a significant impact on energy commodity returns of futures contracts with different maturities. Gkillas et al. (2020) find that financial stress does have predictive value for realized oil-price volatility with alternative types of investors benefiting from monitoring different regional sources of financial stress. Duprey (2020) studies housing market corrections and suggestions on the supervision of financial stress. Since the coronavirus disease pandemic has seriously affected various countries’ economic and social development, it also can affect financial market risk and assets prices (Zhu et al., 2021). Zhang and Wang (2021) consider that Bitcoin is greatly affected by financial stress in the U.S. exchange market. Although the relevant literature is limited, these literatures form strong support for the effects of “financial stress on fund return forecasts.”

Theoretical Framework and Hypothesis

The capital asset pricing model (CAPM) of Sharpe (1964) and Lintner (1965) marks the birth of asset pricing theory. The CAPM builds on the portfolio choice model developed by Markowitz (1959) that defined a mean-variance model for calculating optimal portfolios. Under the Markowitz framework, optimal investment decisions are represented in a two-dimensional space by the ex ante mean and standard deviation (

Then, the CAPM turns this algebraic statement into a testable prediction regarding the relation between risk and expected returns by identifying a portfolio that must be efficient if asset prices are to clear the market of all assets. Specifically, if there are

In this equation,

The arbitrage pricing theory (APT) proposed by Stephen (1976) is a plausible alternative to the simple one-factor CAPM. The appeal of the APT is likely its implication that compensation for bearing risk may be comprised of several risk premia rather than just one risk premium as in the CAPM. Roll and Ross (1980) claim to have empirically found at least three and probably four factors that are priced in the model.

Our paper builds a conditional asset pricing model with macroeconomic risk based on the Intertemporal Capital Asset Pricing Model (ICAPM) theory. The ICAPM proposed by Merton (1973) proved that there is an equilibrium relationship between the expected return and risk for any risky asset

A Conditional Asset Pricing Model With Macroeconomic Risk

The Intertemporal Capital Asset Pricing Model (ICAPM) proposed by Merton (1973) proved that there is an equilibrium relationship between the expected return and risk for any risky asset i:

where µi represents the unconditional excess return on risky assets i,

In the ICAPM, investors are assumed to be rational, and the parameters and covariance of the expected returns are regarded as constants. However, the expected returns and covariance in the model are time-varying, so their coefficients should be time-varying. Therefore, the model can be transformed as:

where

Following Bali et al. (2011, 2012), and Bali et al. (2014), conditional beta is used to replace conditional covariance, and the model changes to:

where

Macroeconomic risk is a state variable that represents the set of consumption and investment opportunities in the ICAPM framework. Therefore, the financial stress index constructed in this paper is regarded as the proxy index of state variable X in equations (4) and (5). The beta in equation (6) is referred to as the “risk factor beta,” and the beta in equation (7) is referred to as “uncertainty index beta.”

Hypothesis

The new hypothesis in the conditional asset pricing model replaces the traditional hypothesis that beta is a constant and defines

where

In the CAPM model, if investors are risk averse, they will choose the portfolio with the maximum expected returns under the given variance. The portfolio satisfies the efficient boundary minimum variance. At this point, the

Based on the theoretical analysis of the conditional asset pricing model with macroeconomic risk, this paper proposes the following hypothesis:

Chinese Financial Stress Index and Econometric Design

Chinese Financial Stress Index

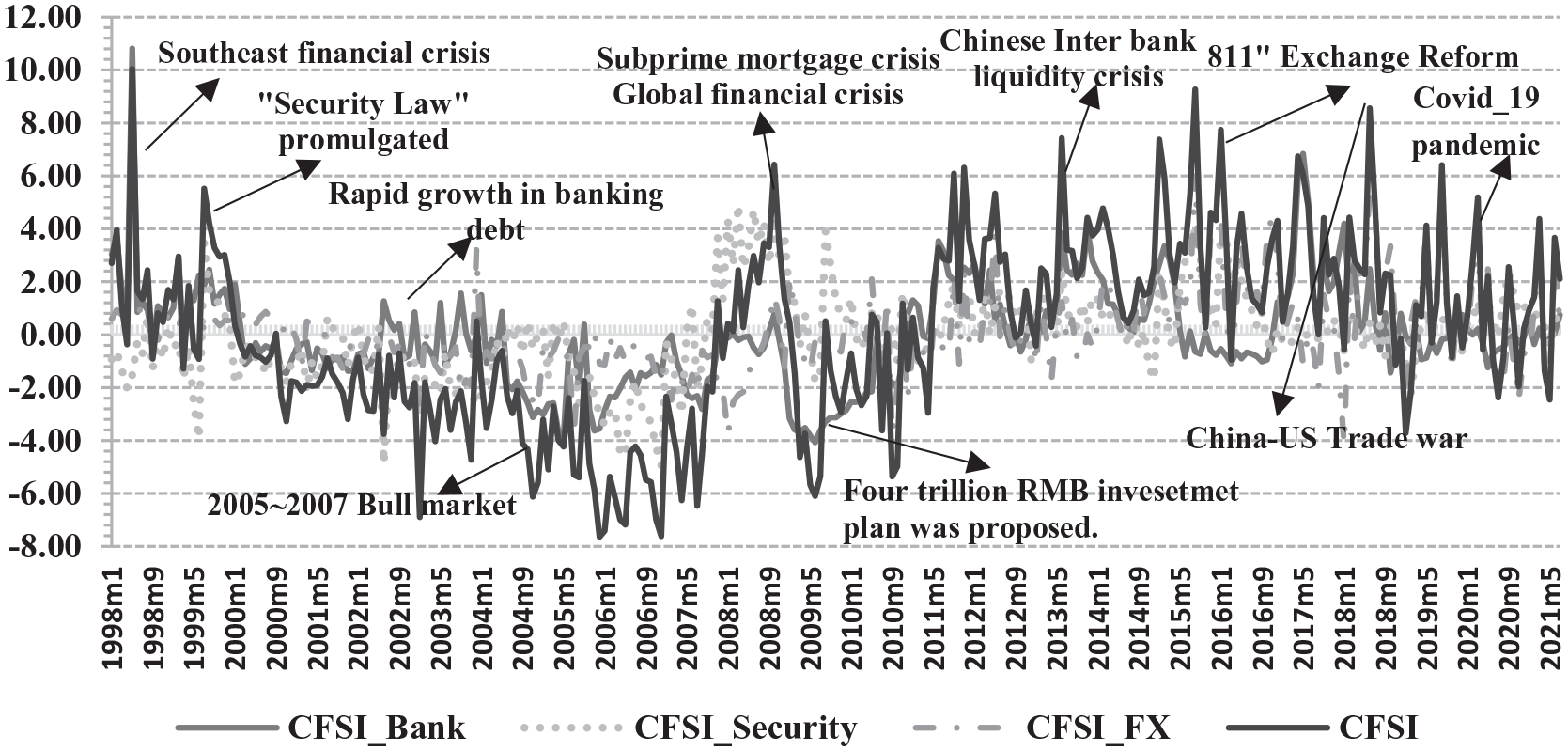

Before the econometric analysis, we need to build our new financial stress index. Our index is constructed using the following procedure. First, eight source indicators, including the banking sector

where

Chinese financial stress index.

In addition, the explanation of each source indicator is as follows, which can also be seen in Table 1.

The Construction of the Financial Stress Index in China.

The rolling

where

Econometric Design

In this section, we introduce the method used to test our hypothesis. The empirical method used by Bali et al. (2011, 2014) is applied in our paper to study the relationship between macroeconomic risks and fund returns. Following Bali et al. (2011, 2014), our benchmark model was used to estimate the financial stress betas. The time series regression over a 36-month rolling window period is used to estimate the monthly beta of fund exposures to the 1-month lagged CFSI. The model is as follows:

where

Then, we use Fama–MacBeth cross-sectional regressions to test the relationship between financial market risks and mutual fund returns. The specific equation is as follows:

where

To study the effectiveness of the CFSI further, we will also add another widely used macroeconomic index to the equation. Additionally, Kothari and Warner (2001) thought that the FF factor model is not suitable for the evaluation of mutual fund returns in China. As a robustness test, we will also consider the FF factors in our paper.

Data

The sample includes CFSI indicators, mutual fund data, and comparison indices (factors). The data samples of CFSI indicators and comparison indices are monthly data from January 1997 to August 2021 except for the Chinese volatility index data, which is from April 2011 to July 2021. The mutual fund data are monthly data from January 2004 to June 2020.

The CFSI indicators, which include the bank TED spread (subtracting the risk-free interest and the 3-month interbank rates),

The mutual fund data and the comparison factor data, such as the MKT, SMB, HML, and momentum factor, are from the RESSET database. The comparison indices, including the Chinese macroeconomic climate index, economic policy uncertainty index, and volatility index, are from Datastream. The mutual fund data include closed-end funds listed on the Shanghai Stock Exchange and Shenzhen Stock Exchange. The data include the fund share category, securities code, transaction date, funds return rate considering cash dividend reinvestment, total market value, management fee rate, trusteeship fee rate, establishment date, and the risk-free rate.

Empirical Results

Financial Stress Betas

In this part, we estimate the exposures of mutual fund returns to Chinese financial stress. The time series regressions over the 36-month rolling window period are used to estimate the monthly beta of mutual fund exposures to the 1-month lagged financial stress index. The empirical results show as follows:

According to the distribution chart in Figure 2, there are 14,574 resulting financial stress betas, ranging from (−0.6313, 0.6388). The mean value of

Monthly beta distribution of mutual funds.

Financial Stress Betas and Mutual Funds

This part constructs cross-sectional regressions of 1-month-ahead fund excess returns on mutual funds’ exposure to financial stress and a set of control variables. The empirical results are as follows:

Table 2 presents the average intercept and slope coefficients from the Fama–MacBeth cross-sectional regressions for the full sample period from January 2004 to June 2020. The Newey-West t-statistics are given in parentheses. First, we investigate the cross-sectional relationship between the financial stress betas and future fund returns after controlling for the momentum or reversal effect. The results of regression (1) provide evidence for a positive and highly significant relation between financial stress betas and future fund returns. The average slope from the 1-month-ahead returns on financial stress betas is 0.9190, and the Newey–West t-statistics is 1.9995. After determining a significantly positive correlation between financial stress betas and future fund returns using Fama–MacBeth regressions, we now control for other characteristics and risk factors simultaneously to test whether mutual fund exposure to financial stress remains a strong predictor of future returns. The results of regressions (2)–(5) show that the average slopes on the financial stress betas are 0.9064, 1.1978, 1.2165, and 1.4517, respectively, which are all positive and significant; and the the Newey–West t-statistics are 1.9047, 2.3155, 2.2002, and 2.6282, respectively. The empirical results show that after controlling for a series of characteristic variables and risk factors for funds, the relationship between financial stress betas and future fund returns is still positively significant. That is, the market risk premium of Chinese financial stress is economically and statistically positive. The hypothesis is true.

Fama–MacBeth Regression of Fund Returns on the Financial Stress Index and Control Variables (2004:01–2020:06).

Note. This table constructs a cross-sectional monthly Fama–MacBeth regression model of Chinese financial stress

It should be emphasized that in Table 2, after controlling the other characteristic variables of the funds, the regression results show that the average slope on the lagged fund returns

Thus, the Chinese financial stress index (CFSI) has strong positive explanatory power for future mutual fund returns. The economic explanation is that as financial stress exposure increases by one unit, investors need 1.4517 unit of monthly risk premium as compensation (Table 2 column 5). Furthermore, for the fund, the average monthly risk premium is nearly −0.0595% (i.e., −1.4517

Therefore, first, mutual funds’ exposure to financial stress predicts the cross-sectional variation in mutual fund returns. Second, the Chinese financial stress index can also be used as a macro-timing strategy for fund investment. Adopting such a financial stress investment strategy can bring more risk premium compensation to investors, thereby improving the investment value of mutual funds.

Bali et al. (2014) consider that since mutual funds do not use dynamic trading strategies, they do not expect mutual fund exposure to macroeconomic risk to explain cross-sectional differences in mutual fund returns. Mutual fund exposure to the broad index of economic uncertainty does not predict the cross-sectional variation in mutual fund returns. Compared with Bali et al. (2014), we find that the Chinese investors behave distinctively from American investors. The management of mutual funds in China is different from that in developed countries. Chinese fund managers pursue high or ultrahigh yields as the management goal and they are more sensitive to the macro financial risk. So, our paper verifies that the Chinese mutual funds’ exposure to financial stress predicts the cross-sectional variation in mutual fund returns.

Comparative Analysis

In this paper, the Chinese macroeconomic climate index, economic policy uncertainty index, volatility index, securities market stress index, foreign exchange market stress index, and bank market stress index are selected as the comparison indices. Among these indexes, the securities stress index, foreign exchange stress index, and bank stress index are the financial stress subindices we constructed, and the others are from Datastream.

The comparative test procedure is as follows:

The time series regression method of a 36-month rolling window is used to estimate the monthly uncertainty beta of each fund’s returns on the previous comparative index. The time series regression econometric model is as follows:

Then, aiming to determine the funds’ excess returns in the next month, a cross-sectional regression model with financial stress betas and control variables is constructed. The monthly cross-sectional regression econometric model is as follows:

where

The comparative empirical results in Table 3 show the following: (1) In Panel A, there is a significant negative correlation between beta

Comparative Tests (2004:01–2020:06).

Note. Panel A is the comparative test result of the macroeconomic climate index, Panel B is the comparative test result of the economic policy uncertainty index based on news, Panel C is the comparative test result of the volatility index, Panel D is the comparative test result of the security market stress index, and Panel E is the comparative test result of the foreign exchange market stress index. Panel F is the comparative test result of the bank market stress index. Regarding the panels, Panel C’s data sample period is from April 2011 to June 2020, and the periods of the other panels are from January 2004 to June 2020. The values in the brackets are the Newey–West t-statistics. ***, **, and * represent significance at the 1%, 5%, and 10% significance levels, respectively.

Robustness Analysis

In this part, the Fama–French three-factor and momentum factor are selected as the regression factors of the comparative tests model, and the robustness test model is introduced as follows:

where

The empirical results in Table 4 show that the dependent variable

Robustness Test (2004:01–2020:06).

Note. This table presents the results of the Fama–MacBeth regression among residual

Conclusion and Policy Recommendations

This paper constructs a more easily realized and measured financial stress index; analyzes its real-time tracking of macroeconomic fluctuations; and conducts the first study of the asset prediction puzzle from a new perspective, financial stress. Specifically, referring to the measurement methods in Bali et al. (2011, 2014), based on financial stress, this paper establishes a conditional asset pricing model with macroeconomic risk, explains the relevant analysis and hypothesis of this model theory, proposes an effective econometric method, and demonstrates that financial stress can help price Chinese mutual funds. Compared to the Chinese macroeconomic prosperity index, economic policy uncertainty index, volatility index (iVIX), securities market stress index, foreign exchange market stress index, banking industry stress index, and Fama–French market premium factor, this research found that financial stress contains economic cycle information, macroeconomic risk information and financial market stress information, which is more applicable to research on the pricing of mutual funds in China. The empirical results show that the risk exposure of financial stress has significant explanatory power for the cross-sectional difference in individual Chinese mutual fund returns. For every 1 unit increase in risk exposure of financial stress, investors need to be compensated with a risk premium of 1.4517 unit per month. For the max

The measurement and supervision of financial stress in China is a very important and urgent research field. This paper concludes that the original microprudential risk supervision method for individual financial institutions, financial markets, and financial products is no longer suitable for current risk supervision and is insufficient to ensure financial stability. Given Chinese national conditions, it is of great significance to design and improve a systematic risk index system and build a risk regulatory framework suitable for the Chinese combination of macro and micro prudence. Therefore, the following suggestions are proposed by this paper.

First, the government should establish a financial stress index for subfinancial markets. Besides the bank market and stock markets, more attention should be paid to the foreign exchange market, real estate market, financial derivatives market, etc. Take the real estate market as an example. The government should not only regulate real estate companies, but the government also needs to construct a real estate market risk monitoring system including real estate prices, real estate financing, real estate management, real estate policy, and other aspects.

Second, regulators should establish a financial market risk warning system and establish a financial market risk supervision mechanism, such as “market risk monitoring—risk identification—crisis warning—feedback.” This can help to identify financial market risks in a timely manner and report the measurements to address the risks. This can effectively prevent the contagion and spillover effects of systemic financial risks among different financial markets and countries.

Third, the government should promote collaborative supervision and improve regulatory efficiency. The government should strengthen the cooperation between the supervisory departments and macromanagement departments and strengthen the cooperation between financial departments and other departments. More attention should be paid to the coordination efficiency of macroprudential supervision, microprudential supervision, and behavioral supervision to effectively improve the supervisory efficiency.

Fourth, financial institutions should explore the application of regulatory technology and improve their digital supervision, technology supervision, and intelligent supervision capabilities. Financial technology supervision can use technologies such as artificial intelligence, big data, cloud computing, and the blockchain to effectively handle financial market risks.

In the future, the construction method of financial stress index needs to be improved, and the research on the financial stress index and asset return pricing needs to be further deepened. This paper only analyzes the impact of CFSI on mutual fund returns. Whether it can also affect other assets’ pricing should be further studied.

Footnotes

Author Note

Qian Wang is now affiliated to Shanghai Jiao Tong University, Shanghai, China.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by Scientific Research Fund Project of Yunnan Education Department (No. 2021J0586), and supported by the Scientific Research Foundation of Yunnan University of Finance and Economics (No. 2020B03).