Abstract

This study is aimed to conceptually engineer the effects of hot potatoes (bad loans) in the banking system. The study’s research design uses elementary concepts of graph theory comprising of mappings of systemic behavior of contemporary banking. Issues have been formally underpinned, described, and visualized through directed and linear graphs. Findings of the study show that it is an inherent feature of the banking system to generate hot potatoes and allow them to sit there. It creates heat in the system by way of latency, turgescence, propagation, and concurrent cyclicality. These predicaments of systemic crises of banking deteriorate the sustainability of the system. The pilot study (using classical t-Test) conducted as part of this research has validated the theoretical argument aforementioned. The study provides new insights into these die-hard issues. It helps refine the agenda of future research in banking.

Introduction

Economies of the World consist of different pseudo-natural systems, and financial development is a hallmark of economic growth (Asongu, 2015; Hassan et al., 2011; Kandil et al., 2017; Rahman et al., 2020; Shahbaz et al., 2015). The financial system is one of the significant systems in an economy that is considered equivalent to the blood circulatory system of the human body. There are various sub-systems within the financial system. Banking is one of the vital systems, major constituents of which are commercial banks. Banking system stability ensures economic and financial stability, as it is an important sector that plays a pivotal role in financial systems (López-Penabad et al., 2021; Salehi & Mansouri, 2016; Swamy, 2014). It is one of the core systems in economies, but no part of the economy misfunctions as banking (Tilly, 2012). Banking history witnesses that due to specific faults in the present system of banks, economies of the World have encountered severe problems (Dell’Ariccia et al., 2008; Demirgüç-Kunt & Detragiache, 2005; Demirgüç-Kunt et al., 2006; Demyanyk & van Hemert, 2011; Kroszner et al., 2007; Logojan, 2009;). Banks are considered intermediaries between individuals and firms because they collect deposits from individuals and give loans to firms. They accumulate funds from the general public and make them available to businesses; in the shape of loans. In this way, they ensure the supply of money needed (Chiappori et al., 1995). They provide loans in sizable chunks to support mass production in the industry. However, the contracts of loans embody a wide variety of ex-ante terms and conditions. Hoelzl et al. (2011) argued that loan repayments are a sequence of installments based on a presumption that processes of repayment of loan along with interest will necessarily recoil. This arrangement provides a lever to firms to pay interest even less than 0%. Default on bank loans is a common phenomenon in banking. It seems to be illogical to argue to conceptualize the interest rate as even less than 0%. Still, it is logical that the firms default on the payment of interests and the principal amount. In case of default on the principal loan amount, the return on loans will run into less than 0%. There is a wide variety of causes of defaults, namely: mismanagement of funds by an obligor, over/under-investment by the banks in a project, adverse effects of government policies, a dispute in management of firms, stiff marketing competition, outdated technology, lagging behind the change, strategic default, cash flow problem, etc. In addition to the cases mentioned above, clients become locked in with banks through loan and deposit contracts. The problem of volatility in working capital makes it difficult for them to honor debt obligations and leave bleak chances of resilience, that is, initiation of loan repayment process (de Guevara & Maudos, 2011; Odeh et al., 2011). Probst and Raisch (2005) asserted that organizations must strike a balance between the extremes of efficiency and resilience. Default in loans threatens the whole financial system that turns into crises. Governments spend trillions of taxpayers’ dollars to averse the crises and avoid financial systems collapse (Prorokowski, 2011; Thompson, 2010). The financial crisis turns into an economic recession, and there is little guidance to overcome this problem (Khashanah & Miao, 2011; Logojan, 2009). The bank default occurs due to some systemic faults, and they, in turn, ignite banking crises. It is transformed into worldwide financial and economic crises that are not limited to any specific country or region (Logojan, 2009; Raza & Karim, 2017). Crises have substantial negative impact on economies (Boyd et al., 2005; Fernández et al., 2013; Hoggarth et al., 2002; Serwa, 2010). The frequency of crises and density of severity of loss caused by them is increasing day by day, for example, the World Bank has identified more than 96 banking crises since the 1970s (Aikman et al., 2015; Bartoletto et al., 2019; da Rocha & Solomou, 2015; Lietaer et al., 2010; Schularick & Taylor, 2012). Marginean et al. (2011) and Clemente et al. (2020) argued that the financial crisis is considered one of the severe economic problems of today. One can find the following leading causes of crises in contemporary research:

(i) Difference/mismatch between actual payments and contractual commitments of interest (Allen & Gale, 2000; Amri et al., 2017; Borio, 2014; Chapra, 2007; Driga, 2004; Festić et al., 2009; Zarrouk & Ayachi, 2009).

(ii) Continuous focus on economic efficiency contradicting the principle of resilience (Lietaer et al., 2010).

(iii) Adverse selection problem (i.e., ex-ante verifying promises and intentions) is considered a seed of crises (Iqbal & Molyneux, 2005).

(iv) We are filling up inflatable balloons of banks (i.e., balance sheets) with subprime borrowers by compromising resilience with efficiency (Shin, 2009).

However, to cure the banking crises, it is imperative to fix the causes of crises inexact. It is not a partial or regional but a holistic international plan to fix them once for all.

Research Gap and Contribution of the Study

Admittedly, there is no dearth of research on the issue, but since the viable and universally acceptable solution has not been surfaced; therefore, banking issues need to be studied rather seriously (Lee, 2012; Lietaer et al., 2010; Tilly, 2012). There is a scarcity of theoretical models that rigorously compare loans’ structural and actual processes (Bejelloun, 2010). Gilbest (2011) asserted that regulators dealing with crises have no template to follow to handle a financial crisis. Hence, there is a severe need to find some solution to insulate the economies from crises. A qualitative judgment is often adopted as to the concept of systemic banking crises (Chaudron & de Haan, 2014). Plenty of attempts have already been made to find out the systemic solution from within the system but looking for a solution to systemic problems within the box is a piece of poor advice (Greenwood, 2012). The solution to the systemic problem can easily be found from outside the current box of thinking. This study aims to conceptually break the complex whole of the banking system into parts to have a closer view of systemic problems to fix them inexactly. The study has essential conceptual inputs and theoretical contributions in the domain. It conceptualizes predictive interconnectivity causal links between actors and core processes of the banking system. A conceptual map of the Contemporary Banking Model (CBM), that is, Figure 2 and multiple linear graphs capturing systemic behavior of CBM (Figure 3) is a novel significant contribution of the study. The study also pointed out the pitfalls of a systemic ex-ante problematic levy. It also conceptualized four core systemic problems, that is, latency, turgescency, propagation, and concurrent cyclicality. It reemphasizes the need to investigate indistinct systemic concepts like jeopardous leverage, petulant investments, and requital for households. It divulges a more profound understanding by mapping banking processes that provide a solid basis for designing quantitative studies in the future. This qualitative exploratory research provides more supplementary information about the behavior of the systems that complement quantitative studies. It is ever first exo-box study on systemic issues that expose four vital systemic predicaments for further investigation. However, it is an initial step toward rethinking the core systemic problems of CBM. The remaining part of the study consists of six parts, that is, literature review, methodology, roots of banking in its paternal systems, engineering of banking model: fixing the problems, visualizing the behavior of banking model, and conclusion.

Literature Review

There are countless studies on the failure of the banking system and financial crises (Akinsola, 2018; Amri et al., 2017; Ba, 2021; Tailab, 2020). The scope of the study review of literature is limited to highly relevant studies concerning the economic/financial/banking systems, loans, defaults, crises, and attempts made to address the issue. Yuzbasioglu et al. (2011) asserted that frequent global financial crises harm all sectors of the economy and questions the validity of economic models (Kongsilp & Mateus, 2017). Streit and Borenstein (2012) revealed that various researchers had investigated issues related to the financial system, but most have concentrated only on quantitative factors in limited scope. The banking system leads to economic growth, but the recent banking scandals raised questions about structural flaws in the way banks to operate (Lee, 2012; Wehinger, 2013). Bhattacharya and Thakor (1993) asserted that there are many unresolved issues about banking system design. Jaffee and Levonian (2001) concluded that there should be a long-term approach to monitor the progress of the banking system, that is, how the system adjusts in the long run. Khan (1989) argued that a financial system is a collection of contracts and the nature and characteristics of these contracts define the system per se. The relations between variables should be studied independently of the physical components of the system (Heylighen & Joslyn, 2001). The academicians criticize the patterns of decision-making in the years leading up to the crisis instead of realizing the systemic fault of banking system design (Gilbest, 2011). Chortareas et al. (2011) argued that the relationship between bank performance and bank lending quality is the essence of promoting sound financial systems.

Gordon (2008) reported that American banking history revealed a financial panic roughly after every 20 years: 1819, 1836, 1857, 1873, 1893, 1907, 1929, 1987, and 2008. Schoenmaker and Taylor (2012) highlighted, altogether, a new dimension and argued that investment in capital or loans to troubled banks implies credit risk. Gordon (2008) invited attention to another point: an attempt to force the banks to make loans to people with limited creditworthiness. Contracts of interest-bearing bank loans signify ambiguity and uncertainty. Fixed return contracts do not necessarily generate a fixed return (Iqbal & Molyneux, 2005). Puri et al. (2011) emphasized that understanding the process of loan making is crucial. Plenty of literature can be found on the relationship of interest with financial crises, but interestingly more found minor literature on interest per se.

The contemporary banking system is based on payment receipt of interest and has achieved a high level of global integration. Therefore, the concept of bank and interest are intertwined, hence, considered inseparable (Cocheo, 2007; Simpson, 2010). The current banking system will have to be revamped (Kazmi, 2006). Interest and interest rates are considered identical terms. There is ambiguity in the definition of interest; therefore, it is controversial in the literature. Interest rate is a ratio of the fee we must pay to obtain the use of credit divided by the amount of credit obtained. Many confusing ways developed to measure the interest, for example, yield to maturity, bank discount rate, etc. (Rose, 2001). Tilly (2012) considered interest as a highly psychological phenomenon. Swartz (2013) urges that the rule of Islam about interest is simple, that is, in case of a loan, you are entitled to receive your principal back, and nothing more, and anything over and above the principal is an interest which is proscribed. According to Ahmad et al. (2011), interest is an additional amount paid and received on the principal amount according to an agreement due to the period attached thereof. Changes in the income of credit users or temporary loss to credit obligors incorporate changes in loan repayments by inserting postpone-able pay periods (Ramirez-Ceballos & Valencia-Delora, 2011).

The studies on the contagion of financial crises have become increasingly exciting, and empirical results of these studies enlighten upon many dimensions (Amri et al., 2017; Paas & Kuusk, 2012; Park & Shin, 2020; Sun, 2020). The financial crisis is not one dip, at any one point of time, but it lasts around 10 years, and the risk of contagion of crisis has increased over the period (Anari et al., 2005; Chan-Lau et al., 2012; Huynh et al., 2020). There is an enormous literature on the causes of banking crises. Origins of economic crises can be explained by long-term recurrent patterns of financial crises (Alvarez-Ramirez & Rodriguez, 2011). While studying the great depression of 1929 to 1931, Kopper (2011) provided new insights that banks’ credit contracts and write-off of big loans were the leading causes of aggravated depression in 1931. Simpson (2010) concluded that integration of banking at the global level implies inter-dependence, which contains the threat of crisis contagion. Fadare (2011 asserted that: (i) deterioration in balance sheets of financial/non-financial institutions, (ii) increasing interest rates, and (iii) uncertainty in the economy are determinants of financial crises. Jeffers and Baicu (2013) argued that interconnections between shadow banking and regular banking increase systemic risk. Gorton and Metrick (2010) concluded that shadow banking plays a harmful role in financial crises. Cornett et al. (2011) found that liquidity crisis in banks leads to a decline in credit supply. Wilson et al. (2010) asserted that a financial crisis is related to systemic instability. Excessive interest-based debt and bad loans are the main reasons for financial crises (Aikman et al., 2015; Logojan, 2009; Zarrouk & Ayachi, 2009). Karim et al. (2012) warned that contemporary interest-free banking is also vulnerable to a financial crisis. Acharya and Naqvi (2012) asserted that volume-based compensation and ex-post penalty system in banks ignite crises. Calvo (2012) revealed that financial crises stem from the financial system itself. The 2008 financial crisis truly affected all sectors of the economy and countries of the World (Clarke, 2010). The World’s economy is still dealing with the corollary of the global financial crises of 2008, and it was the worst financial crisis in global history (Contessi & El-Ghazaly, 2011; Iley & Lewis, 2011). World economies were one by one visited by this virulent shock of the international financial crisis of 2008 (Turkes, 2010). Lin and Wu (2011) asserted that different researchers advanced many early warning models of a financial crisis. A lot of research has been found on the role of the government in rescuing the banking system. As governments rescue banks during crises, there are studies for and against the involvement of governments (Lietaer et al., 2010). Amri et al. (2017) concluded that government supervision and regulation mitigate the effects of crises. Nagy and Benyovszki (2013) argued that as an aftermath of the banking system crisis and the present global financial environment, the governments would have to withdraw the official support from banking.

There is an influx of literature as a reaction to the recent 2008 financial crisis. The researchers opted for studying a wide variety of objects. It is not out of context to place few recent studies on record. Real GDP growth, share prices, the exchange rate, and the lending interest rate significantly affect NPL ratios (Beck et al., 2015; Kadanda & Raj, 2018). Lee and Lim (2019) revealed that larger service sectors also tend to increase the risk of the banking crisis. Peña (2017) facilitated that increasing interest rates will decrease future bank lending and accelerate the likelihood of a banking crisis. Vouldis and Louzis (2018) asserted that decline in industrial production is also a good predictor of financial crises. However, Radivojević et al. (2019) could not find evidence to support microeconomic variables have any significant impact on NPLs. Virtanen et al. (2018) emphasized that early warning signals precede financial crises in the form of financial bubbles and explosive credit growth. By which, as a first step, asset prices and debt-servicing costs are lifted. These early warnings indicate the nearness of banking crises. Pop et al. (2018) reported that NPLs of banks having high loans-to-deposit ratios are significantly more sensitive because low-liquid (risk-seeking) banks are a more significant threat to the banking system’s stability. Therefore, they should be rather closely monitored by watchdogs. Contemporary studies also highlighted a lot of variation coupled with transferability in the severity of banking crises. It has spillovers, and its vulnerabilities travel from one sector to another in the form of amplification (Lee et al., 2020; Peltonen et al., 2019; Pino & Sharma, 2019). Cesa-Bianchi et al. (2019) also affirmed the propagation of crises due to transmission through cross-border financial flows. Adams-Kane et al. (2017) posited that banks exposed to crises exhibit drastic changes in lending patterns. Keijsers et al. (2018) asserted that the financial crises have a feature of propagation and attribute of cyclicality. Since the banks are institutions of systemic importance, governments always rescue banks in financial crises (Amaglobeli et al., 2017). The system of effectuating recoveries at the strength of enforceability of contracts at law rather aggravates crises (Mora-Sanguinetti et al., 2017). Regulatory and supervision practices are not helpful in bankruptcy prevention (Pereira Pedro et al., 2018; Stef & Dimelis, 2020). Wilms et al. (2018) and Igharo et al. (2020) asserted that liquidity support, monetary policy, and financial freedom significantly affect the subsequent mitigation process of banking crises. Manz (2019) reported that loan and asset-specific events still lack a deeper understanding and deserve rigorous research.

Despite the importance of the systemic issues, one can rarely find a study that considers the banking system an object of research in a holistic manner (Huang et al., 2010). It is almost transparent that a bank’s contribution to systemic risk is linear to loan defaults (Huang et al., 2012). Loehel and Li (2011) urged that academicians and professionals are required to rethink the fundamental question of an appropriate banking business model in light of global financial turmoil. Contemporary research has been conducted within the box of banking, and it is curative rather than preventive. Coordinated actions by many central banks can be practical to resolve the banking system’s issues, and this line of investigation should be fine-tuned through finding theoretical models (Goel & Hasan, 2011). Comparing the ideas with practice, what can be learned from the literature on the cyclical financial crisis and the frequent failures of banking systems is significant. The review of scattered literature has implicitly underpinned the need to engineer the contemporary banking model to arrest die-hard issues.

Methodology

The study’s research design comprises mapping the banking model’s processes and contrast of the model’s behavior qua reality. The research design of the study uses an elementary concept of graph theory. The study of mathematical structures using graphs (objects made up of vertices, nodes, or points). Graphs are of two types undirected (linking two edges symmetrically) and directed (linking two edges asymmetrically). Graphs are one of the handy tools of discrete mathematics to analyze economic and financial phenomena (Rahman, 2017; Trudeau, 1993). An array of applications of graph theory in a wide variety of disciplines, including but not limited to economics, banking, and finance, can be found in contemporary literature. There are numerous reasons for applying graph theory in contemporary research. We applied elementary concepts of informally directed graphs and formal linear graphs because of easiness to apply, being better than that available rival solution, and high generalizability. There are thousands of studies using this type of graph currently available online at Jstor, Springer-link, Science Direct (Elsevier), Emerald, Wiley-Blackwell, and Taylor & Francis (Estrada, 2010). It is a simple, classical, traditional, and acceptable way of representing the systemic analysis since the graphs are an alternate representation of mathematical arguments having a high degree of generalizability (Bates et al., 2014; Chen, 2012; Gazda et al., 2015; Huang et al., 2013). Systemic issues have been formally identified, described, underpinned, and visualized by using informally directed graphs and formal linear graphs. Informally directed graphs follow the theory of informal drawing (i.e., informally using formulas to construct diagrams).

The graphs are constructed to visualize the arguments, make expressions easy to define and understand and present logically provable statements for reasoning. Directed lines adjoin vertices, and every line in the graph represents a specifically labeled process. Each drawing represents the precise definition of banking process(s) in mathematical vocabulary and may convert lines into corresponding formulas. Solid, bold, or dotted lines, arrowheads, ovals, squares, chamfered squares, etc., are duly defined and assume special meaning. Comparison of model’s behavior qua reality has critically been analyzed, and the systemic problems have been conceptually arrested on a Cartesian plane. Linear graphs follow general rules of plotting variables on the x-axis and y-axis. Arguments are built on graphs, and multiple compared linear graphs make visualization for understanding and communication. An attempt has been made to find behavioral patterns through piloting through hypotheses testing using a one-sample t-test (Singh, 2017).

Analyses of Contemporary Banking Model

Roots of banking in its paternal systems.

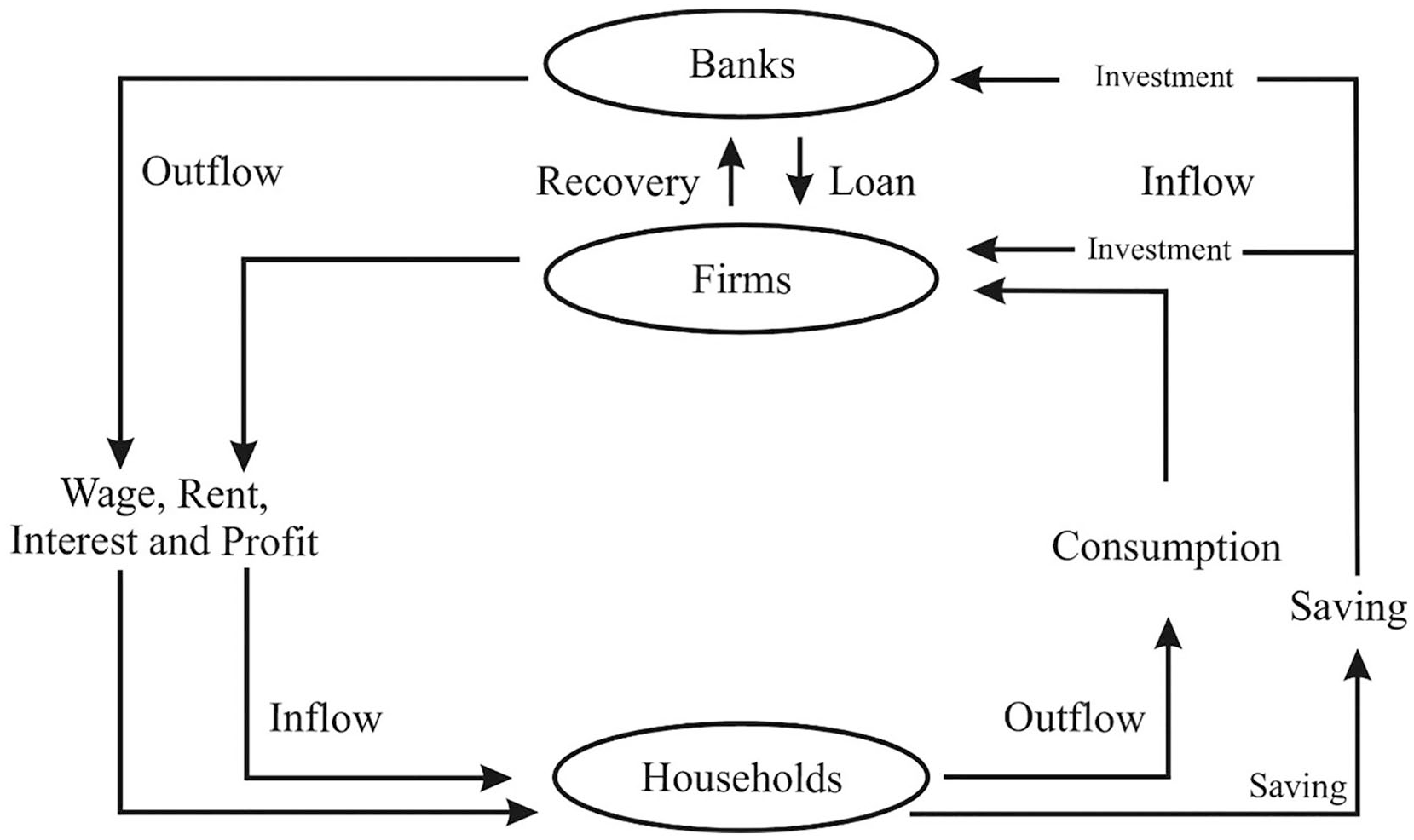

Banking has roots in economic systems; therefore, it is appropriate to trace it from within macro-economic theories. Relating the study with economic systems is vital because of the paternal authority of economics over banking. With this philosophy, the study started from classical macro-economic theory, that is, macroeconomic balance and visualized banking as its sub-system. Banking has been introduced as a part of a more extensive macroeconomic system. Many mainstream economists have defined the macroeconomic system, but the study follows an approach that has been represented by Ray (1998), Andreson (2002), and Jiang (2010). According to them, there is a continuous and systematic flow of capital from investors to real sectors as an investment for profit. Individual investors and actual sector firms interact with each other concurrently and simultaneously.

Their interaction patterns dictate economic and financial systems, and their interaction dynamics determine macro-economic variables that keep an economic balance at the macro level. Like an abstract, it can be said that households (individuals) and firms (organizations) are inter-related and inter-dependent actors of the economic system at the macro level. Careful examination of macroeconomic theory gives a closer view and reveals that households invest in firms, and firms pay wages, rents, interest, and profits to them. It provides their goods and services for their welfare (Andreson, 2002; Jiang, 2010; Ray, 1998). Households consume this money to buy goods and services from firms, making money available again through consumption expenditure. There is consensus in the literature that households do not spend the whole of their money through the consumption process, but they save some of the money for future uncertainties. The savings again go to the firms in the form of investment. This investment, production, consumption, and saving mechanism is termed “macro-economic balance” in literature. In this way, the outflow of one actor is an inflow of another actor and vice versa. The inflow of households in the income, whereas outflow, is their consumption or investment. The inflow of the firms is an investment, and outflow is their expense. It is a continuous process based on structural qualities. Many economists have endorsed the concept of macroeconomic balance. But an explanation of the system as given by economists leaves one question unanswered, that is, whether households invest all the savings in firms? The answer is: maybe not. This “not” again raises another question: What happens to the saving not consumed or invested in firms by households. The economists call that amount as leakage from the system (Ray, 1998). The savings that are not invested in firms directly by the households but are deposited in banks in the hope of risk-free return or making money available for unforeseen contingencies.

Direct investment by the households in firms is a classical form of investment; however, in the era of mass production, capital intensive industrialization, and globalization, the firms, while having reached the climax of requirements of capital, have ever-increasing demands for money, which cannot cater on the classical format of investment. There is a severe need for mediators to accumulate money and lend it in sizeable chunks to firms. The banks perform this mediation function. Therefore, it is imperative to identify the role of banks among the firms for uncovering the phenomenon under study. Banks, which generically are firms, have to be separated from the general form of firms to have a closer view of their functions. As described by Ray (1998), Actors of the system have been modified to this extent. We considered the banks as a separate actors in this scenario. Banks, within broad parameters of the macroeconomic system, work in a systemic way which is identifiable as a banking system. However, there is relatively limited literature directly addressing banking as a system, and therefore, for theoretical underpinning and conceptualization, the study has borrowed from relatively broader literature on economic systems. Figure 1 has therefore been adopted from the economics literature and modified to the extent of banks, which indicates the balance of production, consumption, saving, and investment at higher abstraction. A simplified representation of their relationships is given below in a directed graph (digraph) as Figure 1.

Banks in macroeconomic balance.

A conceptual engineering of banking model-Fixing the problems.

In this part of the study, the system has been mapped and closely analyzed by the authors. The connexions among composing elements of the model are identified and described for understanding and communication. The authors have prepared a map of the model, where the hot potatoes are sitting there-on, based on conceptual links buttressed in the literature using the template of input-process-output (general systems theory) and elementary concepts/logics used in geometry. By conjoining map of actors in banking, forward flow of financial resources, reverse flow of financial resources, visualizing interest, objectives of interest, map of the problem and effects of the problem, in the template of input-process-output (the generic map of a system) has been prepared as Figure 2.

Engineering of contemporary banking model.

The Rectangular outer boundary of Figure 2 indicates the natural environment. The angles of the giant triangle have been labeled as input-process-output to represent the system’s template in general. Three squares, labeled as financial resources, production, and welfare, indicate the banking system’s equivalence to input-process-output. Ovals within the squares bear labels of actors of the system. The outer bounds of squares denote the problem of each actor as pointed with the help of arrows, pointing from outside the outer triangle toward the outer bounds of squares. The arrows on triangular shapes show the direction of flow of the system and the direction of flow of funds within the system. Within the large triangle, there are lines arranged in triangular form; every line bears an arrow indicating the direction of the flow of funds. These triangles can be viewed as singles in the context of the preceding figures and can be identified as forward and reverse flow processes. They indicate forward and reverse flow of funds. The labels mentioned outside the triangle (i.e., jeopardous leverage, petulant investment, and requital) indicate the effect of the problem of interest. Ex-ante (interest) indicates toward illusory of interest levied on firms. The gap between squares and their outer bounds indicates financial crises. It also shows the origins of the crises. To simplify the situation, the outer bounds have been shown as static; in fact, they balloon up after they are born (Smithson & Hayt, 2000). They transform into balloons and burst when the matter goes beyond the control of firms and banks.

As the map of core banking processes has been constructed, and it is now possible to identify and uncover the effects of hot potatoes, therefore, this part of the study is devoted to underpinning the issue. The banking system is based on interest, that is, interest is demanded as an incentive by the depositors on their savings when deposited in banks and levied on loans when the banks give loans to firms for businesses. An interest-based banking system ignites financial crises (Logojan, 2009). In this section of the study, it has been recognized that interest is: (i) a levy, (ii) it is an ex-ante levy, and (iii) its ex-antes are problematic.

Following the definition of a system as “input-process-output” can uncover the hard part of the phenomenon under study. Considering the accumulated deposits (along with capital) as financial resources (input) by banks, application of loans in the production process by firms (process) and availability of goods and services for use as welfare (output) to households, and relating it to the underlying structure of forward and reverse flow processes conventionalized by “households and banks” and “banks and firms,” it can be recognized that interest is considered to the banks for providing the loan to firms in lieu thereof. The purpose of the interest is to arrange for the cost of survival of banks (with margin) and to incentivize their depositors to deposit money with them. It works just like any indirect tax which is levied against citizens to support the government. The only difference is that the purpose, that is, the purpose of interest, is to support banks and incentivize savers instead of supporting the government. Therefore, one can reach the reality that interest is a levy against households.

The banks are involved parties to conventionalize last and second last sub-processes of reverse flow, which legally bind firms (before production) for invariably initiating sub-processes after and dependent on production. Hence interest is levied by banks on firms before the process of production is carried out by them. The firms in this context are forced to agree pre-hand (i.e., under conventional structure) to collect interest (at a future point of time) without any leave to fail to obtain loans from banks. This format of inflicting any levy is termed an ex-ante levy, and hence, interest is an ex-ante levy.

Interest, part of the contracts of deposits and loans, is levied on firms through conventional structures before they produce goods and services. Firms incorporate the interest in the price of goods and services chargeable to consumers as a fraction thereof. The interest is an implicit levy against citizens. Firms collect the same from households and pass it on to banks, inclusive of loans’ repayments. The principal amount is the source of financing for businesses, whereas interest is just an obligation of firms for collection purposes. They perform this function to maximize banks’ returns in consideration of the provision of loans to them. But they might not necessarily and always be able to and willing to collect the levy sufficient enough to match the amount for which they are legally bound, particularly when they have a dual role (i.e., maximizing their returns and that of their financiers). There is a cynical duality of the role of obligors in the collection of the levy, which constitutes a problem of confliction of interest that arises due to the ex-antes of the levy.

The deposits are a source of expense, and loans are a source of revenue for banks, and the banks function in a narrow bracket of marginal difference of interest on deposits and loans. The contracts of deposits and loans (as conventionalized by actors), apart from interest, contain penal and compounding clauses invoke-able in case of no payments and delayed payments of loans or part thereof. Systemic problems arise when, somehow, the firms cannot collect the levy (interest) sufficiently, completely, or timely from households. If there is a difference between the contracted loan repayment and actual collection or payment by the firms, then the crisis starts. Firstly, the firms, being guilty of being unable to perform contracts, try not to disclose the difference to their financiers and cover it through their net worth (noted here as latency in the study). Secondly, the difference inflates due to compound interest and penal clauses (noted here as turgescency). Thirdly, since most of the time, it is impossible for firms to absorb the difference despite their best efforts, it propagates to banks and other institutions (noted here as propagation). Fourthly, since banks and firms continuously give and take loans, the problem is the concurrent and recurrent feature of the banking system (noted here as concurrent cyclicality). Crisis becomes severer and complex step by step, affecting households, banks, and firms.

Banks invest funds of depositors into firms’ businesses where there is always a risk of default. They take money from one side, lend it to the other side in consideration of a tiny margin, and assume credit risk in lieu thereof. They give depositors’ money to firms as loans; therefore, banking is a leveraged business. The risk of default (i.e., the difference between contracted and actual repayment by firms) makes this lever jeopardize banks. The firms avail themselves of the loans from banks and effortlessly invest into their businesses, and it is common for them to report losses with the countenance. This act of firms to obtain and invest effortlessly and report losses with countenance is noted as petulance in the study, and it embodies the risk of default in itself (Festić et al., 2009). Losses are, ultimately, faced by households, be them in the form of fewer wages, loss from firms, diminution in dividends, bad debts, provision for bad debts, diminution in value of the stock, opportunity loss, obsolescence in value of assets, and other losses (Minamihashi, 2011). The process of ultimate parking of the losses in account of households is noted as requital for households in the study.

Visualizing the behavior of the banking model.

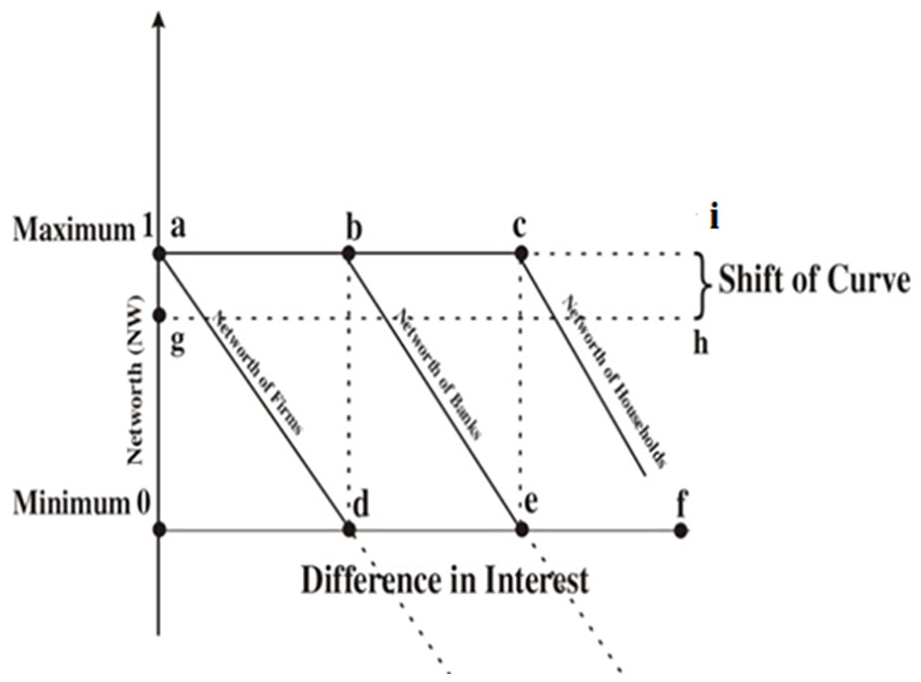

Financial crises, as indicated in Figure 2 (i.e., the gap between squares and their outer-bounds), are the function of shortfalls of ex-ante unfair contracts (Whittaker, 2011): (i) in incorporating interest in prices of goods, (ii) in a collection of interest on loans due to lesser buying of goods by households, and (iii) in recovering principal and the related interest on loans from households by the firms. These shortfalls (difference) are adjusted against the networth of the actors of the banking system, that is, firms, banks, and households (Darroch & McMillan, 2007). It has an inverse linear relationship with the network of actors. The authors have attempted to arrest the system’s behavior, as bolstered in literature, Figures 1 and 2, and demonstrated it in Figure 3. The variables: networth (noted as NW), networth of firms, a network of banks, and networth of households are duly plotted on the y-axis, whereas variable “difference of interest” in structure and operational behavior of collapsing CBM (Allen & Gale, 2000; Amri et al., 2017; Borio, 2014; Carlson & Rose, 2015; Chapra, 2007; Driga, 2004; Festić et al., 2009; Zarrouk & Ayachi, 2009) on the x-axis. The difference of principle in structure and operational behavior of CBM has been treated as an exogenous variable.

Graph of contemporary banking model: (a) H1 bold in this figure, (b) H2 bold in this figure, (c) H3 bold in this figure, (d) H4 bold in this figure, (e) H5 bold in this figure, (f) H6 bold in this figure, (g) H7 bold in this figure, (h) H8 bold in this figure, (i) H9 bold in this figure, and (j) H10 bold in this figure.

Networth has been shown on the y-axis as a minimum (i.e., equal to zero) and maximum (i.e., equal to one). Similarly, a difference of interest has been shown as minimum and maximum on the x-axis. The curve ad shows the relationship of difference of interest with networth of firms. It can be observed that if the difference of interest is zero, then the networth of firms is maximum (i.e., one at point a). On the other hand, if the difference of interest is maximum (i.e., at point d), then the networth of firms is zero.

The curve abe shows the trade-off of the difference of interest and networth of banks. It can be observed that the difference of interest is inflatable (Nidugala & Pant, 2017), which is first adjusted in networth of firms; therefore, from point a to b, the networth of banks remains constant but as soon as the networth of firms reaches to point d (where networth of firms is zero) the downward slope of curve abe starts. The slope starts from point b, which corresponds to point d (correspondence shown by dotted line) and approaches to pointe on the x-axis where banks’ networth is zero.

The curve acf shows a trade-off of difference of interest with networth of households. It can be observed that the difference of interest is first adjusted in networth of firms and banks; therefore, from the point a to c, the net worth of households remains constant, but as soon as the networth of banks reaches point e (where networth of banks is zero) the slope of curve acf starts (Merrett, 2006). It can also be observed that this slope starts from point c, which corresponds to point e on the x-axis (correspondence shown by dotted line). The curve ACF, in fact, never reaches point f because before reaching that point f, the system takes some appropriate correction due to exogenous factors (Amaglobeli et al., 2017).

The curve gh shows the trade-off of the difference of principal loans with the networth of firms, banks, and households. It can be observed that if a difference of principal occurs, the curve shifts from ai to gh (i.e., networth of firms, banks, and households directly shifts from point a to point g), which has been indicated by marking “shift of curve” as against point i and h. It also captures that due to the shift of the curve (i.e., the difference in principle), the speed of depletion (due to difference in interest) of the net worth of firms, banks, and households is increased.

The above argumentation is a theoretical base for the actual trade-offs, which may take more complex visualizations. However, the argument is sufficient enough to uncover the core issues and to arrest the systemic faults.

Piloting

Although multiple linear graphs conceptually well represent the argument. However, representing the argument in the form of mathematical equations and giving some statistical evidence adds value. Therefore, the authors opted to substantiate the conceptual representation in mathematical logic and through some statistical evidence.

Mathematical Representation

There is a linear relationship between the difference of interest and net worth. This relationship can be observed mathematically with the help of the equation

Where x = difference of interest

y = netwoth

For Firms

For Banks

For Households

It is important to note that in the third case, the value of net worth does not reach zero.

Statistical Evidence

There could be three options for statistical evidence, that is, by way of (i) simulation/hypothetical data in the form of a practical example, (ii) secondary data of real-life situation, and (iii) primary data in the form of perception of a community of practice. Simulation/hypothetical data in the form of practical examples might not surpass the mathematical logic, therefore, might not add value. Secondary data is ideal for validation of the behavior of the model, but since it is purely a conceptual study and actual secondary data will be huge in volume and scope. Practically it will involve a lot of effort, time, and money, and it will comparatively add lesser value, particularly toward conceptual development. Instead, it might confuse and drive the readers out of the scope of the study. Therefore, both of these options have been turned down by the authors. However, substantiating based on a perception of a community of practice is seemingly a better option. The pilot study has accordingly been conducted and briefly reported without compromising the clarity of the study. Thirty items Likert scale survey questionnaire was used to collect data from 35 respondents.

The survey was distributed to 35 persons from the community of banking practitioners. Respondents were selected on a convenience basis having a minimum of 10 years of experience with an educational background of at least a master’s in finance. Total 31 questionnaires could be completed in all respects; therefore, the pilot test was conducted based on 31 surveys. Critical behaviors shown on the Cartesian plane (Figure 3) were hypothesized as given in Table 1. Total 10 hypotheses were developed and tested through a one-sample t-test (Singh, 2017). The p-value for all the hypotheses was significant at a 95% confidence interval, which shows that the community of practice affirms behaviors conceptually expressed in Figure 3. The statistical results of each hypothesis (i.e., from hypotheses H1–H10) as contained in Table 1 can be related with curves on Figure 1 by observing the bold part of Figure 3a to j.

Results of Hypotheses Testing.

Source. Author’s own completion.

Note. n (number of respondents) = 31.

Accepted, if significance value two-tailed <.05.

According to the classical procedure of hypotheses testing, developed null and alternate hypotheses for 10 critical relationships depicted on the graph in Figure 3, and a two-tailed t-test was used. The test was performed on SPSS for calculating the mean with the 5% significance level, and the test value for the t-test was 3.5. Since all the hypotheses have a significant value of less than 5%, all are accepted in Table 1.

Conclusion

This theoretical study of the contemporary banking model pertains to hot potatoes (loan defaults) and resultant crises. Systemic issues have been formally identified, described, and underpinned through a discourse of literature review. The study used elementary concepts of graph theory (i.e., informally directed graphs and formal linear graphs). Findings of the study revealed that it is an inherent feature of the banking system to generate hot potatoes and allow them to sit there. It creates heat in the system by way of latency, turgescence, propagation, and concurrent cyclicality. Firstly, the firms, being guilty of not performing contracts, try not to disclose the difference (shortfalls) to their financiers and cover it through their networth (issue of latency). Secondly, due to compound interest and penal clauses, the difference inflates (issue of turgescency). Thirdly, since firms usually can’t absorb the difference despite their best efforts; therefore, it propagates to banks and other institutions (issue of propagation). Fourthly, since banks and firms continuously give and take loans, the problem is the concurrent and recurrent feature of the banking system (issue of concurrent cyclicality). These are four die problematic systemic issues that affect banks’ jeopardous leverage, petulance for firms, and requital for households (i.e., for system actors). In addition to the issues mentioned above, the hot potatoes deteriorate the networth of these actors (Figure 3). Mathematical representation also affirms and substantiates this argument. Hypothesizing the relations and testing the same using a one-sample t-test, based on primary data collected from the community of practice, further validates the concept in Figure 3.

The research study has significant theoretical and practical implications. The mapping diagrams will help to improve and understand the processes clearly. It has significant relevance for researchers, policymakers, and practitioners. It identifies the need for more theoretical development. It bolsters the interdependency of variables which indicates how closely they are related to each other and allows future researchers to consider these variables to develop and validate further options of alternate models. This seminal study strikes clarity in framing issues of banking crises which will be helpful to refine the plan of future research in the banking domain. Simple decomposition of banking processes and conceptual engineering of banking model is the novelty of the study. Uncovering predicaments of the system, its ex-ante levy, and capturing the behavior of the banking model on simple graphs is a contribution of the study. Since banking processes are series of receipt payments, future studies may fix the issues with the help of summation algebra, converting informal drawing into corresponding formulas.

Limitations of This Study and Future Research

The study also has certain limitations. Firstly, it is a conceptual study; therefore, the concepts and relations among them must be quantitatively validated using some statistical technique with larger data sets of primary and secondary data. Secondly, the methodologies used in this study are based on the elementary concept of geometry which only pinpoints the issues; therefore, rather rigorous and advanced methodologies will be helpful in the investigation. Thirdly, a vital issue to the CBM has been identified with the help of a literature review and simple logic; therefore, the literature review can be made rather extensive. Instead of simple logic, formal logic/statistical evidence will be helpful in future studies.

Footnotes

Author Note

Kashif Abbass is now affiliated to Riphah School of Business & Management, Riphah International University Lahore, Raiwind Campus, Pakistan.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical Approval

We confirmed that this manuscript has not been published elsewhere and is not under consideration by another journal. Ethical approval and Informed consent do not apply to this study.