Abstract

This study investigates the procyclicality of loan loss provision (LLP), with a focus on differentiating the procyclical inclinations of non-discretionary and discretionary components. Using a dataset of 377 IFRS-compliant banks from 75 countries around the world, we analyze how each component of LLP responds to economic cycles during the period from 2013 to 2022. Our findings indicate that non-discretionary LLP exhibits procyclicality, as they respond to observable credit losses that typically rise following economic downturns. Conversely, discretionary LLP, which reflects anticipatory adjustments made by banks in response to economic conditions, does not show procyclicality. These results underscore the role of LLP components in amplifying economic cycles. This research contributes to the broader understanding of procyclicality and financial stability, providing insights for standard setters and policymakers seeking to mitigate the procyclical effects of provisioning practices.

Keywords

Introduction

Over the past two decades, the financial sector has been both a driver of economic growth and a source of systemic vulnerability. Its expansion has contributed significantly to shaping macroeconomic outcomes across diverse economies (Geršl & Jakubík, 2009). However, the very mechanisms that fuel financial deepening have also amplified concerns over procyclicality—the tendency of financial system dynamics to move in sync with the business cycle, thereby magnifying economic fluctuations rather than smoothing them (Bikker & Metzemakers, 2005; Borio et al., 2001). Procyclicality operates through positive feedback loops between the financial and real sectors: in good times, credit expansion and rising asset prices reinforce each other, while in downturns, credit contractions and falling asset prices interact to exacerbate recessions.

The 2008 global financial crisis remains a stark illustration of the destructive potential of procyclicality. At its peak, global GDP contracted by 1.3% in 2009, the sharpest decline in decades. While global trade volumes fell by over 10% (World Bank, 2020). Banks that suffered extensive losses faced severe challenges in replenishing capital buffers, prompting them to curtail lending and liquidate assets at depressed prices, further accelerating the downturn (Financial Stability Forum, 2009). The crisis underscored the urgent need for regulatory frameworks that could break these destabilizing feedback mechanisms.

Loan loss provisioning (LLP) has been identified by the Financial Stability Forum (2009) as one of the priority areas for mitigating procyclicality. Given that loans account for more than 50% of total bank assets globally (Wendy, 2024), LLP plays a central role in both risk management and credit supply. LLP refers to reserves set aside by banks to absorb expected loan losses (Bikker & Metzemakers, 2005). Its inherently procyclical nature arises from banks’ tendency to under-provision during economic booms—when borrower credit quality appears strong—thereby encouraging excessive credit growth and inflating collateral values. Conversely, in recessions, defaults rise and provisions increase sharply, eroding capital and constraining credit supply precisely when it is most needed (Borio et al., 2001). This cyclical amplification not only heightens systemic risk but also complicates the pursuit of sustainable economic growth.

Recent evidence suggests that these dynamics remain a pressing concern. For example, during the COVID-19 shock in 2020, global GDP fell by 3.1% (International Monetary Fund [IMF], 2022), and many banks rapidly increased provisions. For instance, a sample of 70 large, internationally active banks reporting provisions totaled $161 billion in the first half of 2020, compared with $50 billion in the second half of 2019 (de Araujo et al., 2021). The increased provisions tightened credit conditions despite extensive policy interventions. Such patterns demonstrate that LLP’s procyclicality is not merely a historical artifact of the 2008 crisis but an ongoing structural feature of the banking sector.

Despite its importance, most existing research on LLP procyclicality (e.g., Huizinga & Laeven, 2019; Shala & Toçi, 2021) focuses on European banking systems, which, while diverse, share a unified regulatory framework under the EU. This geographical concentration limits our understanding of how LLP procyclicality manifests across different global regions with varying institutional, regulatory, and macroeconomic environments. Without broader cross-border evidence, it is difficult to generalize policy prescriptions or design globally effective regulatory interventions.

Moreover, the literature has largely treated LLP as a monolithic measure, overlooking its heterogeneous components. LLP consists of non-discretionary provisions, which are mechanically determined by incurred credit losses and regulatory requirements, and discretionary provisions, which allow bank managers to apply judgment and forward-looking estimates (Aristei & Gallo, 2019). These components may respond differently to economic cycles: non-discretionary provisions are more likely to reflect current credit conditions, whereas discretionary provisions can be influenced by managerial incentives such as earnings smoothing, capital management, or signaling. However, empirical research explicitly distinguishing these components in the context of procyclicality remains scarce. This gap is critical because regulators aiming to curb procyclicality need to know whether it originates primarily from mechanical credit risk dynamics or from managerial discretion.

This study addresses these gaps by providing the first large-scale cross-border analysis of the procyclicality of LLP subcomponents. Using a dataset of 377 commercial banks from multiple regions worldwide over the period 2013 to 2023, this study examines how discretionary and non-discretionary LLP behave across economic cycles, including both expansions and contractions. By disaggregating LLP and incorporating global evidence, this study offers a more granular and generalizable understanding of provisioning procyclicality, thereby generating insights relevant for standard setters, regulators, and policymakers seeking to enhance financial stability across diverse banking environments.

This study makes several contributions to the literature on loan loss provisioning (LLP) and financial stability. First, it overcomes the geographical limitations of much of the existing research by examining a diverse sample of 377 commercial banks across multiple countries and regions. Prior studies on LLP procyclicality have been heavily concentrated in Europe, where banks operate under a relatively unified regulatory framework. By adopting a global scope, this research captures the heterogeneity in provisioning practices across different institutional, regulatory, and macroeconomic environments. The resulting insights are not only more generalizable but also directly relevant to international policymakers, regulators, and financial institutions seeking to design effective cross-border stability measures.

Second, and most critically, this study advances the literature by explicitly disaggregating LLP into non-discretionary and discretionary components. Whereas previous studies have typically treated LLP as a single, homogeneous measure, our approach recognizes that these components are fundamentally different in their drivers and potential impacts on the business cycle. Non-discretionary LLPs are largely determined by observable credit risk and regulatory provisioning models, while discretionary LLPs are shaped by managerial judgment and can be strategically adjusted. This disaggregation yields two specific contributions. One is isolating the Sources of Procyclicality - While the literature widely acknowledges LLP procyclicality as a potential threat to financial stability, it rarely distinguishes whether such patterns originate from the mechanical effects of credit risk models or from managerial discretion. By separating LLP into its subcomponents, this study allows for the attribution of procyclical behavior specifically to non-discretionary provisions, while also testing whether discretionary provisions exacerbate or mitigate these effects. The other is clarifying Managerial Behavior and Earnings Management Incentives - Discretionary LLPs are known to serve strategic purposes such as earnings smoothing, capital management, and signaling (Ahmed et al., 1999; Kanagaretnam et al., 2004). By isolating them from their non-discretionary counterparts, this study provides a more precise lens through which to analyze managerial responses to economic and regulatory changes. This, in turn, enriches the literature on bank behavior, earnings management, and prudential policy by revealing whether discretion in provisioning serves as a stabilizing tool or a source of additional volatility. In doing so, this study not only extends the empirical understanding of LLP behavior across economic cycles but also provides actionable insights for regulators on designing provisioning frameworks that are sensitive to both the mechanical and discretionary drivers of procyclicality.

The remainder of this research is as follows. The second section is the literature review, which summarizes and criticizes the existing literature. The third section is hypothesis development. The fourth section is research methodology. The fifth section is empirical results. The sixth section is the robustness test. The last section is the conclusion.

Literature Review

The procyclicality of banks’ loan loss provisioning (LLP) has been a persistent concern in financial stability research, with substantial evidence showing that provisioning practices often amplify economic cycles rather than smooth them. The introduction of the Expected Credit Loss (ECL) model under IFRS 9 has intensified scholarly debate on whether forward-looking provisioning can effectively mitigate such procyclicality, or whether it introduces new forms of opportunistic behavior.

Recent empirical studies have begun to provide systematic evidence on the consequences of ECL adoption. Prisco et al. (2025), using a large EU dataset of 16,740 bank-year observations between 2012 and 2023, report that ECL adoption is associated with reduced provisioning procyclicality, but also with heightened capital management activities. Their difference-in-differences analysis reveals a nuanced effect: while forward-looking provisioning mitigates the “too little, too late” problem, it simultaneously expands managerial discretion, thereby enabling earnings and capital management. Notably, auditor specialization and strong regulatory quality temper these opportunistic tendencies, suggesting that institutional oversight remains a crucial moderating factor.

In the Chinese context, Li et al. (2025) extend the analysis by introducing the concept of Delayed Expected Loan Loss Recognition (DELR), a phenomenon whereby banks postpone the recognition of expected losses despite forward-looking requirements. Using quarterly data from 16 Chinese banks over 2011 to 2023, they find that DELR exacerbates LLP procyclicality, and that ECL reform-after controlling for discretionary management motives-significantly reduces both DELR and its amplification of procyclicality. This indicates that while ECL can address timing distortions in provisioning, its effectiveness depends on curbing both managerial discretion and institutional inertia.

Earlier research has largely approached LLP procyclicality through the lens of institutional factors, macroprudential policy tools, and bank-specific characteristics. Olszak, Chodnicka-Jaworska, et al. (2018) and M. A. Olszak and Kowalska (2023) show that macroprudential instruments such as borrower restrictions, dynamic provisioning, large exposure limits, and asset-specific taxes reduce procyclicality, with borrower restrictions proving most effective. Importantly, the efficacy of measures such as loan-to-value (LTV) and debt-to-income (DTI) caps varies by bank size, being more effective for large banks. Comparative evidence from Polish commercial and cooperative banks (Olszak et al., 2018) underscores structural heterogeneity: commercial banks exhibit stronger procyclicality, influenced primarily by capital adequacy ratios, whereas cooperative banks’ procyclicality is driven by income-smoothing incentives.

Theoretical contributions, notably Agénor and Zilberman (2015), reinforce the mitigating potential of dynamic provisioning systems, which recognize expected losses earlier and encourage countercyclical reserve accumulation. This aligns conceptually with the ECL model’s forward-looking mandate, though the latter’s actual impact is shown to be context-dependent in empirical studies. Bank-specific operational factors also matter: Huizinga and Laeven (2019) find that better-capitalized and larger banks exhibit stronger procyclicality, while Bhat et al. (2019) demonstrate that advanced credit risk models and transparent risk disclosures improve the timeliness of LLP and may restrain procyclicality. Meanwhile, market competition has emerged as a structural amplifier, with M. A. Olszak and Kowalska (2023) showing that intense competition-particularly in high-income markets-strengthens the cyclical sensitivity of provisioning, likely due to riskier lending strategies under pressure to maintain market share.

Taken together, these studies paint a complex picture of provisioning procyclicality. On one hand, forward-looking provisioning frameworks like ECL and dynamic provisioning can moderate the amplification of credit cycles by encouraging earlier recognition of expected losses. On the other, increased managerial discretion under these regimes may facilitate opportunistic behavior-such as earnings smoothing and capital management-that interacts with macroeconomic conditions in unpredictable ways.

The literature also remains predominantly regional, with much of the IFRS 9 evidence concentrated in the EU (Prisco et al., 2025) or single-country studies such as China (Li et al., 2025) and Poland (Olszak, Roszkowska, et al., 2018). This limits our understanding of how institutional diversity, regulatory quality, and bank heterogeneity interact with provisioning regimes on a global scale. Moreover, most empirical analyses treat LLPs as a single, aggregate measure, without distinguishing between non-discretionary (model-driven) and discretionary (managerially determined) components. This aggregation obscures the distinct channels through which different types of provisions influence procyclicality and financial stability.

Addressing this gap requires cross-country evidence that explicitly disaggregates LLPs, allowing for the isolation of mechanical, credit risk-driven provisioning from strategic managerial adjustments. Such an approach can clarify whether discretion serves primarily as a countercyclical buffer or as an amplifier of cyclical swings, thereby offering both theoretical and policy-relevant advances to the literature.

Hypothesis Development

Loan loss provisions (LLPs) are among the most important accruals in banking, serving as a forward-looking expense to cover potential credit losses in a bank’s loan portfolio (Aristei & Gallo, 2019). A growing body of literature has shown that LLPs often behave procyclically-falling in economic expansions when credit quality is strong, and rising in downturns as default risk materializes (Bikker & Metzemakers, 2005; Skała, 2020).

This procyclicality stems from the timing of loss recognition. When LLP increases concurrently with a downturn, it reduces earnings and bank capital precisely when lending is most needed, thereby tightening credit supply and amplifying the economic contraction (Buesa et al., 2023). The capital ratio constraint under Basel requirements exacerbates this mechanism: since LLPs reduce retained earnings (a core component of regulatory capital), banks may need to curtail loan growth to maintain minimum capital ratios (Engelmann & Pham, 2020). In essence, the synchronous increase in LLP during recessions reinforces the credit cycle.

Importantly, LLP is not a monolithic measure. It can be decomposed into non-discretionary LLP (NDLLP)-driven by observable credit losses and standardized models-and discretionary LLP (DLLP)-reflecting managerial judgment and strategic considerations (Jutasompakorn et al., 2021).

By disaggregating LLPs into NDLLPs and DLLPs, we can isolate the mechanical credit risk-driven element from the strategic, judgment-based element. The theoretical reasoning behind their expected behaviors is summarized in Table 1.

Expected Behavior of NDLLPs Versus DLLPs.

Source. Hand collected by the author.

The distinction matters because NDLLPs, being reactive, embed economic fluctuations into financial statements, amplifying cycles. DLLPs, by contrast, allow managers to shift provisions intertemporally, either to smooth income, manage regulatory capital, or signal prudent risk management.

The financial accelerator theory (Bernanke et al., 1999) posits that adverse economic shocks are amplified through the interaction of borrowers’ balance sheets and credit market frictions. In downturns, declining borrower net worth increases perceived credit risk, prompting lenders to tighten credit standards and raise the cost of borrowing. This contraction in credit supply depresses investment and spending, which in turn worsens borrower balance sheets-creating a self-reinforcing cycle.

Within the banking context, NDLLPs function as a mechanical link in this amplification process. NDLLPs are determined by observable credit losses and regulatory provisioning models, which are heavily influenced by macroeconomic indicators such as GDP growth (Aristei & Gallo, 2019). Because these provisions are backward-looking and tied directly to realized credit deterioration, they tend to rise sharply during downturns, precisely when borrowers’ balance sheets are already under stress.

The recognition of higher NDLLPs reduces bank earnings and depletes regulatory capital, which can push capital ratios closer to minimum thresholds (Engelmann & Pham, 2020). To preserve these ratios, banks may reduce loan supply-either by tightening lending standards or by rationing credit-at the very moment when firms and households most need liquidity. This capital-driven lending contraction reinforces the downturn, consistent with the financial accelerator mechanism.

Conversely, in periods of economic expansion, improvements in borrower performance and macroeconomic conditions reduce observed credit losses, leading to lower NDLLPs. This releases pressure on capital and enables banks to expand credit supply, fueling further growth. Thus, the NDLLP cycle tends to move in phase with the business cycle, mechanically amplifying economic fluctuations rather than smoothing them.

Based on the analysis above,

While NDLLPs are largely mechanical and reactive, DLLPs reflect the portion of provisioning subject to managerial judgment. This discretion allows bank managers to adjust provisions beyond what is dictated by observed credit losses, often in response to strategic, regulatory, or reputational considerations.

Several theoretical perspectives explain why DLLPs may behave differently and potentially less procyclical than NDLLPs. The first one is Earnings Management and Capital Management Theory. This theory suggests that managers often use DLLPs as a tool for income smoothing, reducing earnings volatility over time (Ahmed et al., 1999). During economic upturns, managers may intentionally increase provisions (despite low default rates) to build reserves for future downturns, thereby mitigating future earnings shocks. Conversely, in recessions, managers may reduce provisions to cushion reported profitability and maintain investor confidence. This smoothing behavior naturally dampens the synchrony between DLLPs and the macroeconomic cycle. In the same vein, because LLPs directly affect bank capital, managers may adjust DLLPs to manage regulatory capital ratios strategically. In downturns, they may reduce DLLPs to avoid breaching minimum requirements, thereby supporting lending capacity. This can counteract the capital-constraining effect observed with NDLLPs. The second one is Signaling Theory. Provisioning decisions can send information to the market about a bank’s private assessment of credit risk and long-term stability. Increasing DLLPs in good times may signal prudent risk management and forward-looking conservatism, while moderating provisions in bad times may signal confidence in asset quality and reassure investors. These signaling incentives can cause DLLP movements to diverge from the purely procyclical pattern of NDLLPs.

In sum, while NDLLPs mechanically amplify credit cycles, DLLPs allow for strategic intertemporal shifting of provisions. This discretion can be used to smooth earnings, manage capital buffers, and send favorable signals to stakeholders-mechanisms that can reduce their degree of procyclicality relative to NDLLPs.

Based on the analysis above,

Research Methodology

Data Collection

The data in this research involves a sample of 377 banks from various regions across the world. All the sample banks adhere to International Financial Reporting Standards (IFRS). This aims to overcome the impact of different accounting regimes. The primary financial data for these sample banks, including LLP, nonperforming loans, and other relevant variables, were collected from the Eikon (DataStream) database, which is a comprehensive source that widely used in financial and economic research. This ensures consistency and reliability in the reported financial information. Additionally, GDP growth rate data was obtained from the World Bank’s website, providing accurate and comparable economic indicators across the sampled countries.

Empirical Model

Firstly, we follow Beatty and Liao (2014) and estimate the discretionary loan loss provision using the following model:

Where:

LLP = current loan loss provision divided by the total loan of current period

ΔNPL = the change of nonperforming loan divided by the total loan at the beginning of the year

SIZE = logarithm of the total assets

LOANG = the change of the loan divided by the total loan at the beginning of the year

c = the country fixed effect

v = the bank fixed effect

t = the time fixed effect

ε = error term, which represents the discretionary loan loss provision.

This model estimates loan loss provisions (LLP) as a function of observable credit quality and bank characteristics that drive mechanical provisioning needs rather than managerial discretion. In this model (Model 1), the explained part of LLP represents the non-discretionary component (NDLLP), which driven by actual credit deterioration and required by regulatory rules, while the unexplained part (residuals, ε) is interpreted as the discretionary component (DLLP), reflecting managerial judgment or strategic motives (e.g., earnings smoothing, capital management, or signaling). The dependent variable is LLP (scaled by total loans), with key explanatory variables including ΔNPL (change in nonperforming loans, capturing credit losses), SIZE (bank size, controlling for scale effects), LOANG (loan growth, accounting for new lending). This separation is valid because the explanatory variables are chosen to capture required provisioning behavior, assuming discretion is orthogonal to these drivers. This approach well-established in LLP literature (Beatty & Liao, 2014; Bouvatier et al., 2014; Kanagaretnam et al., 2009 18). In sum, NDLLP is the part of LLP explained by mechanical drivers, while DLLP is the residual, assumed to arise from managerial discretion.

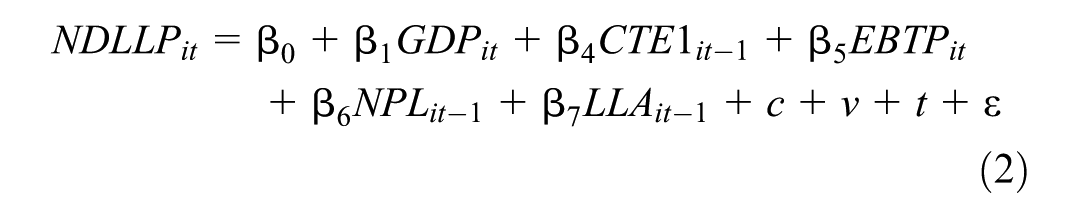

Second, we followed the model developed by Pastiranová and Witzany (2021) and test the procyclicality of NDLLP and DLLP. The procyclicality proxied by the relationship between NDLLP and GDP as well as the relationship between DLLP and GDP. If NDLLP and DLLP have a negative correlation GDP, it means NDLLP and DLLP fluctuate with GDP growth in an opposite direction and shows procyclicality. Since NDLLP and DLLP also be influenced by the banks’ earnings management and capital management activities, we control the earnings smoothing variable EBTP (Bouvatier et al., 2014) and capital management variable CTE1 (Bonin & Kosak, 2013). We also control variables NPL and LLA, which identified by prior research (Kanagaretnam et al., 2009; Ozili, 2017). The models are as follows:

Where:

NDLLP = non-discretionary loan loss provision derived from model 1

DLLP = discretionary loan loss provision derived from model 1

GDP = real gross domestic product growth rate

CTE1 = tier 1 capital adequacy rate

EBTP = earnings before tax and provision divided by total assets

NPL = nonperforming loan rate to total loan

LLA = loan loss allowance divided by total loan

c = the country fixed effect

v = the bank fixed effect

t = the time fixed effect

ε = the error term

This study adopts the empirical framework of Pastiranová and Witzany (2022), which is, to the best of our knowledge, the only model in the literature explicitly designed to measure the cyclical behavior of LLP. Unlike earlier studies (e.g., Beatty & Liao, 2014; Bikker & Metzemakers, 2005) that treat GDP growth merely as a control variable when modeling the determinants of LLP, Pastiranová and Witzany (2022) place real GDP growth at the center of the specification, allowing the estimated coefficient to serve as a direct measure of procyclicality. A significantly negative coefficient indicates that LLP increases during economic downturns, reflecting procyclical behavior. Their model further incorporates controls for earnings smoothing and capital management incentives, as well as credit risk indicators such as NPL ratios and loan loss allowances, ensuring that the observed GDP–LLP relationship captures genuine cyclical effects rather than managerial opportunism. This study extends their approach by applying it separately to non-discretionary and discretionary LLP components, enabling a more granular assessment of whether procyclicality originates from mechanical credit risk dynamics or from managerial discretion.

The procyclicality of loan loss provisioning (LLP) can be understood through the lens of three complementary theoretical perspectives: Financial Accelerator Theory, Earnings Management and Capital Management Theory, and Signaling Theory. Together, these provide the conceptual foundation for both the decomposition of LLP into discretionary (DLLP) and non-discretionary (NDLLP) components and for the empirical models used in this study. The financial accelerator framework (Bernanke et al., 1999) posits that financial frictions can amplify business cycle fluctuations through credit supply dynamics. During expansions, perceived borrower credit quality improves, reducing required provisions. This encourages further credit expansion, reinforcing the upswing. During contractions, deteriorating credit quality forces higher provisions, reducing bank capital and constraining lending, thereby deepening the downturn. Building on earnings management theory (Healy & Wahlen, 1999), discretionary provisions (DLLP) are subject to managerial judgment and can be strategically adjusted to smooth earnings or manage regulatory capital ratios. Managers may increase provisions in good times to create reserves for downturns (income smoothing). Conversely, they may reduce provisions in bad times to avoid reporting losses or breaching capital adequacy thresholds. These behaviors create deviations from purely risk-driven provisioning and explain why DLLP may display weaker or asymmetric procyclicality compared to NDLLP. The inclusion of EBTP (earnings before tax and provisions) and CTE1 (capital adequacy) in the models controls for these managerial incentives, following Bouvatier and Lepetit (2008) and M. Olszak et al. (2017). According to signaling theory (Spence, 1973), banks may adjust discretionary provisions to convey private information about future credit risk to investors and regulators. For example: Higher DLLP in expansions can signal prudent risk management. Lower DLLP in downturns can signal resilience despite adverse conditions. This theory supports the decomposition of LLP (via model 1) into discretionary and non-discretionary parts, since signaling effects are embedded primarily in the discretionary component.

Model (1) (Beatty & Liao, 2014) isolates DLLP by controlling for observable credit risk drivers (e.g., ΔNPL, loan growth, bank size), leaving the residuals as discretionary judgment. This separation is theoretically grounded in the distinction between mechanical risk-based provisioning (NDLLP) and managerial discretion (DLLP). Models (2) and (3) (Pastiranová & Witzany, 2022) directly operationalize the financial accelerator mechanism by linking provisioning components to GDP growth, while controlling for earnings and capital management motives. This ensures that the estimated cyclicality is not conflated with strategic reporting behavior.

Data and Inclusion Criteria

The initial dataset was drawn from the Eikon (DataStream) database and covers commercial banks reporting under International Financial Reporting Standards (IFRS) between 2013 and 2023. IFRS adopters were chosen to eliminate heterogeneity from differing accounting regimes, ensuring consistent recognition and measurement of loan loss provisions. The inclusion criteria are as follows:

Accounting basis - Banks must report under IFRS for the full sample period or for all available years within the period.

Data availability - Banks must have non-missing annual data for key variables: LLP, total loans, non-performing loans (NPL), loan growth, total assets, capital adequacy (CTE1), earnings before tax and provisions (EBTP), and loan loss allowance (LLA).

After applying these criteria, the final sample comprises 377 banks from 75 countries, representing diverse regions.

Data Cleaning and Outlier Treatment

To mitigate the influence of extreme values and reporting anomalies: All variables were winsorized at the 1st and 99th percentiles within each year to reduce the impact of outliers without losing valid information. Observations with negative total loans or capital adequacy ratios outside the 0% to 100% range were removed as implausible reporting errors. GDP growth rates below −20% or above 20% were cross-checked against World Bank data to confirm validity.

Empirical Results

Table 2 provides the statistical analysis for this study, showcasing variability across a range of financial and economic variables. This diversity reflects the different practices and conditions among the banks in the dataset. The subsequent paragraphs offer a detailed discussion of these descriptive statistics.

Descriptive Statistics.

Note. LLP = percentage of loan loss provision to the total loan; NDLLP = non-discretionary loan loss provision; DLLP = discretionary loan loss provision; GDP = the real GDP growth rate; NPL = the percentage of nonperforming loan to total asset; LLA = loan loss allowance rate to the total loan; EBTP = earnings before tax and provision; CTE1 = core tier 1 capital adequacy ratio. SIZE is the logarithm of bank assets. LOANG is the loan growth rate. ΔNPLt + 1 is the change of nonperforming loan for the next year. ΔNPL t is the change of nonperforming loan for the current year. ΔNPLt−1 is the change of nonperforming loan for the last year. ΔNPLt−2 is the change of nonperforming loan for the year before last year.

The average Loan Loss Provision (LLP) is 1.137 with high variability (standard deviation 1.343) from 0 to 9.755. Non-Discretionary Loan Loss Provision (NDLLP) averages 1.176 with less variation (standard deviation 0.460) from 0.034 to 2.541, due to regulatory guidance. Discretionary Loan Loss Provision (DLLP) shows a mean of 0.049 and high variability (standard deviation 0.559), ranging from 0 to 6.307. GDP growth averages 3.964, with a range of 0.194 to 10.636, while the Non-Performing Loan (NPL) ratio averages 0.051, reflecting variations in asset quality. Loan Loss Allowance (LLA) is modest at 0.038 (standard deviation 0.037), and Earnings Before Taxes and Provisions (EBTP) averages 2.018 with notable differences among banks. Core Tier 1 Capital (CTE1) has a mean of 15.103, Bank Size (SIZE) averages 23.977, and Loan Growth (LOANG) has a mean of 11.046, indicating varied lending practices. Changes in NPL metrics (ΔNPL t , ΔNPLt + 1, ΔNPLt−1, ΔNPLt−2) reflect significant fluctuations, likely influenced by economic cycles.

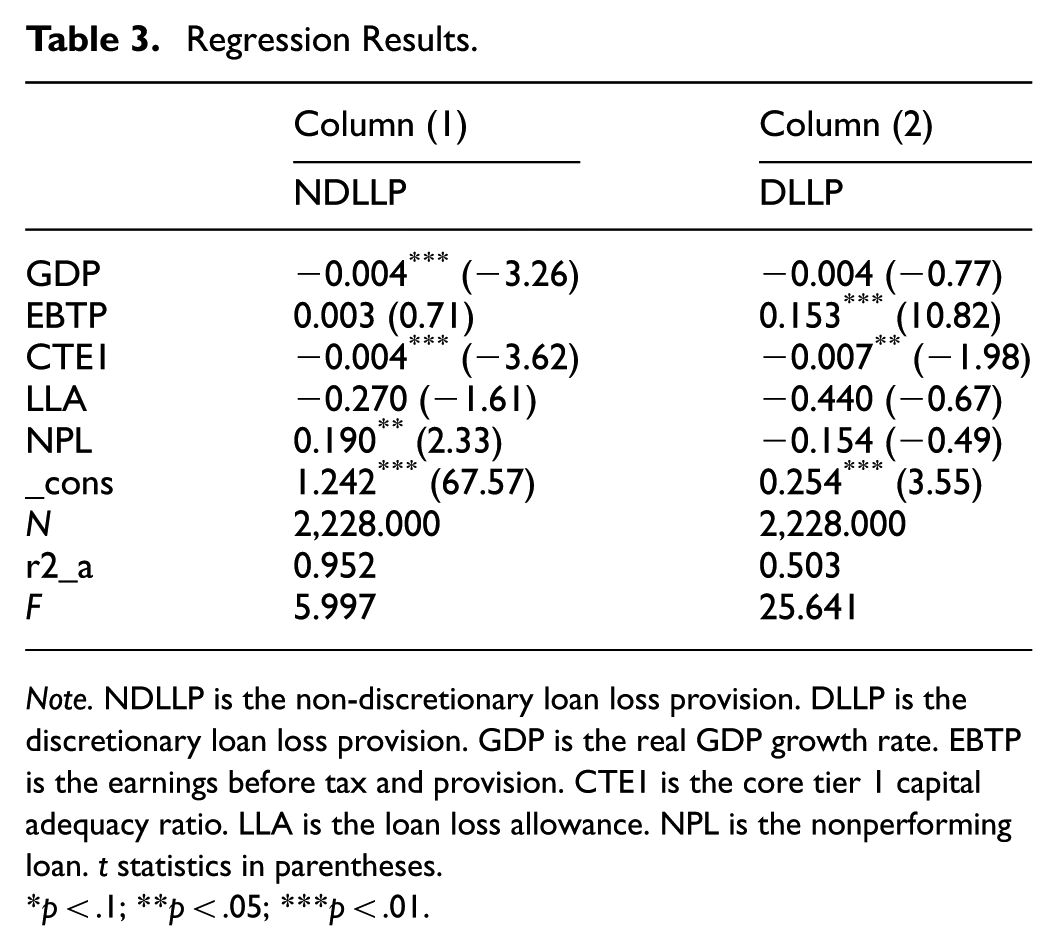

Table 3 presents the regression results.

Regression Results.

Note. NDLLP is the non-discretionary loan loss provision. DLLP is the discretionary loan loss provision. GDP is the real GDP growth rate. EBTP is the earnings before tax and provision. CTE1 is the core tier 1 capital adequacy ratio. LLA is the loan loss allowance. NPL is the nonperforming loan. t statistics in parentheses.

p < .1; **p < .05; ***p < .01.

The result in Column (1), Row 1 of Table 3 shows that the coefficient on GDP for NDLLP is −0.004 and statistically significant. This implies that a 1% point increase in GDP growth is associated with a 0.004% point decrease in NDLLP. Although the magnitude appears small in absolute terms, it is economically meaningful given that provisioning ratios for banks typically move within a narrow range; even small shifts can materially affect profitability and capital adequacy in aggregate. The negative sign indicates that in economic expansions, required provisions-driven largely by the mechanical outputs of credit risk models-decline, and in downturns they rise, demonstrating procyclicality. This is consistent with

The empirical finding that GDP growth is negatively and significantly associated with non-discretionary loan loss provisions (NDLLP) supports the financial accelerator theory (Bernanke et al., 1999). According to this theory, fluctuations in macroeconomic conditions amplify changes in credit risk and bank balance sheets. In periods of economic expansion, borrower creditworthiness improves, reducing model-driven credit losses and thus mechanically lowering NDLLP; in downturns, credit risk metrics deteriorate, prompting higher provisioning. This aligns with prior empirical studies (e.g., Bikker & Metzemakers, 2005; Laeven & Majnoni, 2003) that document a procyclical pattern in mandatory provisioning driven by credit risk models and accounting standards.

By contrast, Column (2), Row 2 of Table 3 shows that the coefficient between DLLP and GDP is also −0.004 but statistically insignificant. This suggests that discretionary adjustments to loan loss provisions are not systematically related to the economic cycle. The absence of significance may indicate that managerial discretion is influenced by factors other than contemporaneous macroeconomic conditions-such as earnings management, capital management objectives, or forward-looking expectations-which can vary idiosyncratically across banks and time. Furthermore, discretionary provisioning may be more subject to regulatory scrutiny or internal governance controls, reducing its cyclical sensitivity.

The statistically insignificant relationship between discretionary loan loss provisions (DLLP) and GDP suggests that managerial adjustments to provisions are less directly tied to contemporaneous macroeconomic conditions. This finding is consistent with earnings management theory (Healy & Wahlen, 1999) and capital management theory (Ahmed et al., 1999), which posit that bank managers use discretion in provisioning to smooth earnings, meet regulatory capital requirements, or achieve other strategic objectives that may not align perfectly with real-time economic cycles. Discretionary adjustments can be influenced by forward-looking assessments, strategic signaling, or idiosyncratic factors such as changes in loan portfolio composition, which weaken their cyclical sensitivity. The results also resonate with the signaling theory of financial reporting (Spence, 1973), under which discretionary provisions may be used to convey private information about future credit conditions or financial strength to stakeholders, rather than to respond mechanically to current macroeconomic fluctuations.

In sum, the results suggest that GDP movements exert a systematic and economically relevant influence on non-discretionary provisions, which are inherently linked to observed credit risk metrics; whereas discretionary provisions are more detached from the business cycle, reflecting managerial choices that do not necessarily track real-time macroeconomic changes.

To address potential endogeneity concerns, empirical design incorporates several strategies. First, lag structures are employed by using lagged GDP growth as an explanatory variable for LLP components, mitigating reverse causality. Second, bank- and time-fixed effects are included to capture unobserved bank-specific heterogeneity and global time-varying shocks. To account for autocorrelation, lagged LLP components are added as regressors to capture persistence, and residuals are tested for serial correlation. Heteroskedasticity concerns are addressed by using cluster-robust standard errors at the bank level, which simultaneously control within-bank serial correlation and heteroskedasticity. The results are presented in Tables 4 to 6. The results remain qualitatively unchanged after implementing these adjustments.

Using Lagged GDP.

Note. t statistics in parentheses.

p < .1; **p < .05; ***p < .01.

Add Lagged LLP.

Note. t statistics in parentheses.

p < .1, **p < .05, ***p < .01.

Using Cluster Standard Error Technique.

t statistics in parentheses.

p < .1; **p < .05; ***p < .01.

Robustness Test

Section 6 presents some findings on the robustness of our analyses. First, we dropped the data of the year 2020. This is because the pandemic of COVID 19 broke out at the beginning of 2020 and the GDP growth rate of many countries suddenly decreased. This is different from ordinary years. Second, we replaced LLP (the ratio of the LLP to the total loan) with LLPTA (which means the loan loss provision rate equals the rate of LLP to the total asset). Tables 7 and 8 presents the results of the robustness analyses. The analysis reveals that the results do not significantly change, indicating our findings’ robustness.

Remove the Data of 2020 Due to the Pandemic.

Note. t statistics in parentheses. NDLLP = non discretionary loan loss provision; DLLP = discretionary loan loss provision; GDP = real GDP growth rate; EBTP = earnings before tax and provision; CTE1 = core tier 1 capital adequacy ratio; LLA = loan loss allowance; NPL = nonperforming loan.

p < .1, **p < .05, ***p < .01.

Replace LLP with LLPTA.

Note. t statistics in parentheses. NDLLP = non-discretionary loan loss provision; DLLP = discretionary loan loss provision; GDP = real GDP growth rate; EBTP = earnings before tax and provision; CTE1 = core tier 1 capital adequacy ratio; LLA = loan loss allowance; NPL = nonperforming loan.

p < .1; **p < .05, ***p < .01.

Conclusions

This study examines the procyclicality of loan loss provisions (LLPs) by disaggregating them into their non-discretionary (NDLLP) and discretionary (DLLP) components, addressing key gaps in the literature-particularly the overreliance on aggregated LLP measures and region-specific evidence. Using a cross-border panel of 377 commercial banks from 75 countries over a 10-year period, we provide robust evidence that NDLLP exhibits significant procyclicality, while DLLP is largely non-procyclical. These results align with theoretical expectations from the financial accelerator framework, where provisions highly linked to incurred losses, tied closely to contemporaneous credit risk indicators, amplify the economic cycle. In contrast, the discretionary component appears less sensitive to real-time macroeconomic fluctuations, reflecting its reliance on managerial judgment, forward-looking expectations, and institutional governance.

From a policy perspective, these findings underscore the importance of differentiating between LLP components when designing regulatory frameworks. The strong procyclicality of NDLLP suggests that standard setters and regulators should consider countercyclical adjustments to model-based provisioning requirements, such as dynamic provisioning rules or through-the-cycle credit risk parameters, to mitigate amplification of economic fluctuations. Conversely, the non-procyclical nature of DLLP points to its potential as a stabilizing tool, enabling banks to build buffers in good times and support lending during downturns. Regulatory frameworks could thus preserve or even enhance the role of discretion-subject to strong oversight and transparency requirements to strengthen financial resilience. Furthermore, supervisory authorities may adopt heightened monitoring during economic booms to ensure that provisions remain adequate and do not fall to unsustainable levels, thereby reducing vulnerability in subsequent downturns.

The study’s limitations present opportunities for further research. First, our sample focuses solely on commercial banks, which may limit generalizability to other financial institutions such as investment banks or microfinance entities. Future research could expand the scope to assess whether similar cyclical patterns hold in different institutional contexts. Second, the annual frequency of our data restricts the ability to detect short-term dynamics; future studies employing quarterly or monthly data could capture more immediate provisioning responses to economic shifts, especially in periods of rapid macroeconomic change. Third, while we distinguish between NDLLP and DLLP, the drivers of discretionary decisions remain an open question. Investigating how managerial incentives, ownership structures, and risk cultures influence DLLP behavior would yield valuable insights into its stabilizing role. Fourth, this study focuses exclusively on countries that have adopted International Financial Reporting Standards (IFRS). While this scope ensures comparability in accounting practices and the treatment of loan loss provisions across jurisdictions, it also limits the generalizability of the findings to non-IFRS environments. The dynamics of procyclicality in loan loss provisioning may differ in countries that apply alternative accounting frameworks, such as U.S. GAAP or domestic standards, due to variations in recognition criteria, measurement approaches, and regulatory oversight. Future research could broaden the analysis by including both IFRS and non-IFRS countries to examine whether the observed relationships hold across diverse accounting environments.

By advancing the understanding of LLP procyclicality through both theoretical grounding and cross-border empirical evidence, this study provides actionable guidance for regulators, standard setters, and practitioners seeking to balance prudential soundness with macroeconomic stability. A regulatory approach that differentiates between LLP components, mitigates the procyclical tendencies of NDLLP, and leverages the stabilizing potential of DLLP could make the banking system more resilient to future economic cycles.

Footnotes

Acknowledgements

Thank for the editors and reviewers.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data of this study are available upon request.