Abstract

This paper aims to analyzes the English-language literature related to Systemically Important Banks (SIBs) by applying the bibliometric methodology to present the current state of SIBs’ intellectual structure and emerging trends from a large quantity of data for the period 2002 to first 2 months of 2022 from Scopus, which is which is considered the most widely used database. SIBs are large and powerful, their contribution to economic growth is significant but their failure is usually systematic and contagious. Regulators subsidize them with public money to avoid systematic financial crises. It is striking that smaller banks do not receive the same treatment, which places them under competitive disadvantage. The bibliometric methodology helps in focusing on this issue for being a rigorous way for exploring and evaluating large volumes of data, identifying gaps, deriving unique research ideas, and resulting in a significant research impact. Therefore, we apply the bibliometric analysis to describe the field’s evolution and structure, including co-authorship, bibliographical coupling, and co-citation. The findings reveal that, the USA is the most relevant country, the University of Southeast is the most relevant institution, and the Journal of Banking and Finance is the most relevant journal. We contribute to the literature mainly by: (1) identifying the benchmark authors, locations of SIBs, and journals; (2) specifying the research streams and summarizing the most cited papers; and (3) identifying the research gaps and future directions.

Introduction

Banking systems are usually faced with a number of challenges; an important one is related to the systematically important banks (SIBs). These organizations are so large, interconnected domestically with other banks and some of them are interconnected internationally and complex. Complexity is due to their large scale and scope of services and products, they are well diversified and are able to generate income from many sources and attract customers of different kinds. SIBs are usually criticized for receiving preferential treatment from central banks at times of financial distress because their failure can be systematic leading to a collapse in the financial sector at large. Varotto and Zhao (2018) claim that SIBs raise an overriding concern for “too-big-to-fail” (TBTF) institutions. Naturally, regulators are aware of this issue and in distress, they bail them out to avoid system-wide liquidation. While this may have some grounds, the fact that SIBs receive preferential treatment puts small and medium sized banks under competitive disadvantage. Regulators and academic scholars have recognized this challenge, Brewer III and Jagtiani (2013) argue that banks are usually in search for mergers to increase size that would place them in the (TBTF) category. SIBs could have an edge in terms of cost and profit by outperforming other banks without taking additional risk (Tabak et al., 2012).

The need to study SIBs stems from their significant economic contribution and to the fact that their failure can be detrimental leading to system failure. In distress, regulators usually rescue them using public money while smaller banks do not receive the same privileges (Alzoubi, 2021; Dam & Koetter, 2012; Violon et al., 2020). In addressing these issues, regulators can get some insights on the possible need to amend their guidelines to maintain stable financial system and academic scholars can get insights on the status-quo and future research directions.

Basel Committee on Banking Supervision (BCBS) recognized the need for dealing with SIBs and added special clauses in Basel III accord. Chiaramonte and Casu (2017) stress the need to increase the focus on SIBs and their results provided “support for Basel III’s initiatives on structural liquidity and for the increased regulatory focus on large and systemically important banks.” Fiordelisi and Ricci (2016) investigate the reaction of investors to bail out actions by central banks and monetary policy interventions and find out that investors do not agree to the bailout actions but agree to the monetary policy interventions (Alghusin, et al,. 2020).

Based on our reading of the literature, we identified the following research gaps:

First, there is a lack of research addressing the need for regulators to avoid unjust treatment to SIBs without jeopardizing the safety and soundness principle of the financial system, one such example is downsizing large banks or limiting their scope. Second, there is a lack of consensus on how to define and identify an SIB, while there is a general definition but no specific guidelines. In 2011, the BCBS proposed a definition for SIBs for member countries, which may not be appropriate to non-member countries or developing countries. Each country needs to apply its own specific guidelines that are consistent with the general guidelines and identify the number of SIBs accordingly.

This paper proposes the following guidelines that can be used as a working definition of an SIB:

- Large size such as holding more than 10% of market share.

- Highly diversified in terms of products and services that include non-conventional banking services such as investment banking, insurance services, and investment advising.

- Heavily interconnected with other domestic or international banks in terms of borrowing, lending, and other services.

Third, there is a limited evidence regarding the adequacy of the capital requirements proposed by Basel III especially those related to SIBs. While Basel III has introduced special clauses for SIBs, future research must address the appropriateness of those clauses especially after the accord becomes fully effective.

In this paper, we address the following primary research questions:

Q1. What are the most critical and influential features of systemically important banks literature?

Q2. Who are the most influential authors in systemically important bank?

Q3. What are the systemically important bank literature’s potential research directions?

This paper contributes to the literature by the following:

First, identifying the benchmark authors, the benchmark locations of SIBs and the benchmark journals.

Second, specifying the four research streams for academic researchers and policy makers and summarizing the most cited research studies.

Third, identifying the research gaps and future directions.

This paper reviewed the 222 articles available in the Scopus database only. This is due to lack of resources available in different databases, which limits the outcome of this bibliometric study.

Methodological Approach

Data Collection

Our analysis is based on Scopus database, which covers a wide range of peer-reviewed journals, provides accurate bibliographic information, and is limited to the English language. The number of documents that satisfy this criterion is 222 papers, which were analyzed for title, keywords, and abstract. The start date is 2002 as this year witnessed the beginning of research interests in this area. A vast number of search questions and related keywords were used to look for relevant terms in the title, abstract, and keywords of the publications in the database. The analysis is based on theoretical and empirical approaches.

Data Selection Strategy

Scopus database is used, which is the most widely used database for social sciences (Pérez-Gutiérrez et al., 2018). It is more popular and useful for researchers in compiling data. Also, due to the lack of access to other databases including SSCI (Web of Science Social Science Citation Index), this study uses Scopus database. Moreover, Google Scholar was ignored due to low-quality published articles.

Data Analysis

The research questions presented in this paper are answered through the overall literature patterns and by using a co-citation analysis to find the core publications that are the most co-cited by the reviewed studies.

A co-word analysis was also performed to aid in determining the conceptual framework and research topics of SIBs and answering the rest of the study questions (Donthu et al., 2021). The bibliometric research was conducted using VOSviewer software (version 1.6.17) and RStudio. Following Paltrinieri et al. (2019), our search strategy is summarized in the Figure 1.

Research design and search strategy.

Analysis and Interpretation

The general information of the data is presented in Table 1, which shows 131 sources (Journals, Books, etc.) publishing 222 documents, 56 of which only are single-authored documents suggesting a good level of collaboration.

Figure 2 also presents the annual distribution of the 222 research papers that were published between 2002and first 2 months of 2022 during 2011 to 2021, the number of publications accelerated reaching its peak in 2021 with 36 documents. Scholars showed more interest starting 2011. Basel III accord was finalized in 2009; research interest in that year and the following 4 years although improved but remained low because the standard was new. In 2013, research interest accelerated due to heightened awareness by scholars. In fact, 2013 marked the paper, which had the largest citations (128) (Table A1). Thereafter, until 2021, there was some volatility but with an upward trend. 2021 marked the highest in terms of the number of research papers published (36 papers) reflecting increased interests (Figure 2).

Annual distribution of systemically important bank papers.

Leading Countries, Institutions, Journals, and Authors

Figure 3 shows that M. Iwanicz-Drozdowska and J. Li to be the most frequent publishing authors with four articles each, followed by G. P. Clemente, K. Dally, R. Grassi, L. Wang, and W. Wang with three articles each. Finally, A. Akhigbe and H. P. Anderson have two articles each.

Most frequently published authors in systemically important bank.

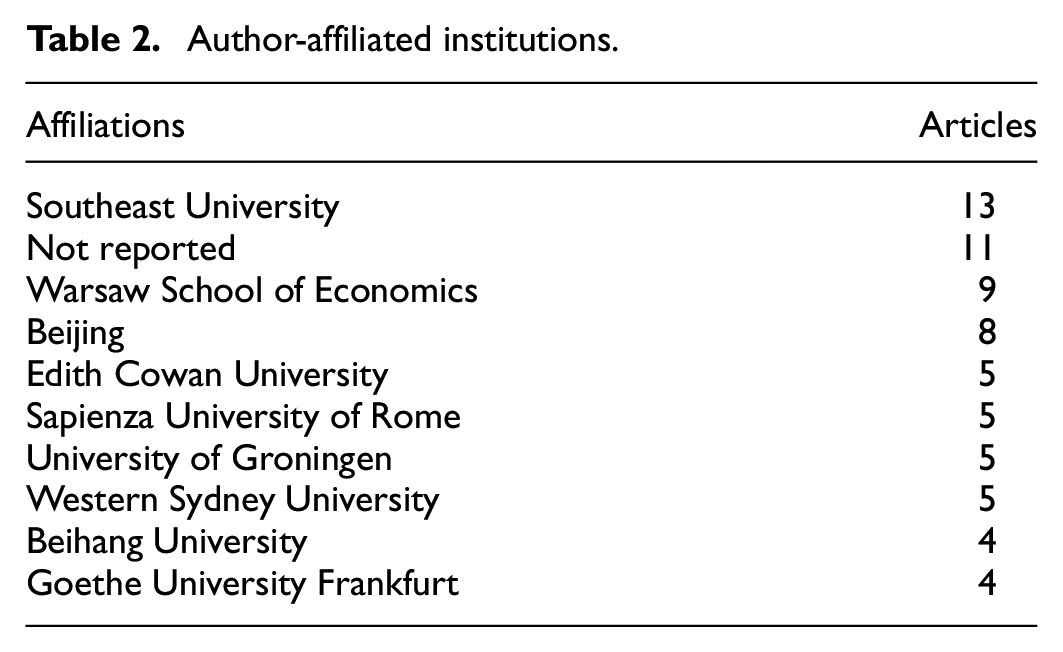

Table 2 shows that the most frequent affiliations of the authors are the Southeast University with 13 articles followed by the Not reported with 11 articles.

Author-affiliated institutions.

Figure 4 reports the countries covered in past SIBs studies. Advanced countries, like the US, China, Italy, Germany, and the UK, appear most frequently. The strong presence of these countries suggests that they support scientific research about SIBs.

Countries covered in systemically important banks.

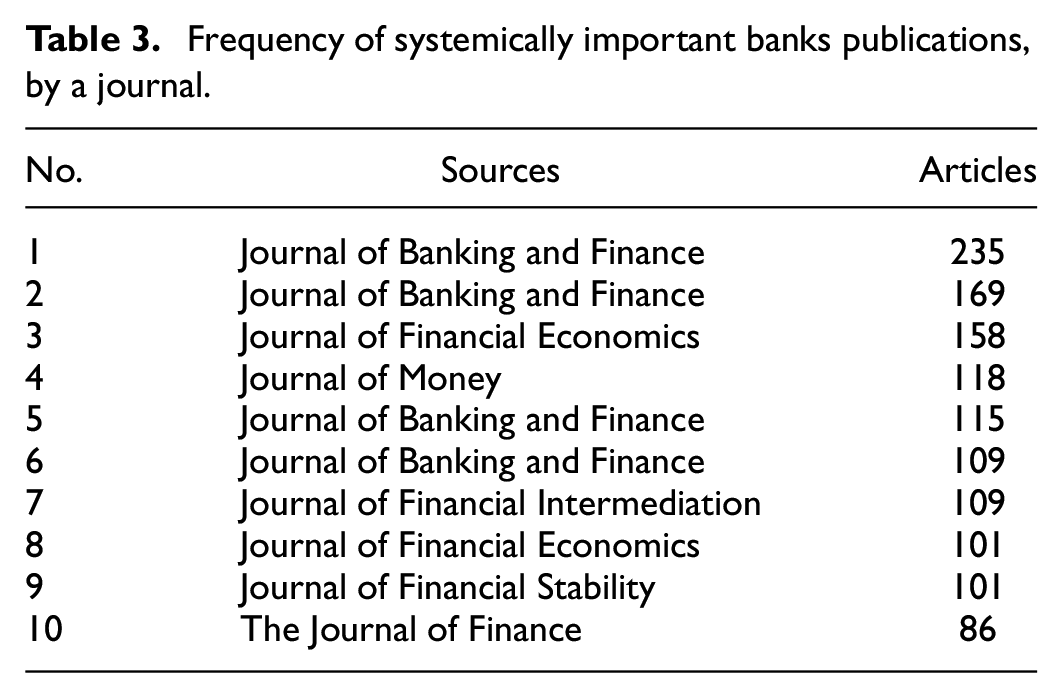

The Banking and Finance Journal, which appears twice, takes the first position then followed by the Journal of Financial Economics and the Journal of Money. Table 3 lists the SIBs publications in various journals.

Frequency of systemically important banks publications, by a journal.

Citation Analysis

Seglen (1989) proposed the analysis of citation as a way of bibliographic reference analysis to account for a connection between two documents. Some researchers are not in agreement with this approach claiming that it affects the quality of the paper, that is, the analysis of citation may include negative citations (incorrect results from citation), self-citations, and old research papers. Garfield (1979) argues that it is true that this kind of analysis has some weaknesses; it is yet a valid index of effectiveness.

This analysis emphasizes the impact of best authors defined in terms of publishing in high rank journals. Table A1 of the Appendix describes the most frequently cited research papers of SIBs. The most cited papers are related to the negative association between bank size and bank market to book value particularly in countries suffering from large budget deficits. Other papers focus on merger activities of banks that makes them large enough to fall in the category of too-big-to-fail and on the increased regulatory attention and the structural liquidity of large banks based on Basel III accord.

The impact of the author is reported in Table 4, which shows that P. Abedifar to be the most cited author followed by J. R. Barth.

Author Impact.

Mapping Tools to Analysis Network and Content

This part is concerned with the analysis of bibliography coupling, co-citation, co-authorship, thematic evolution, keywords, and hierarchical clustering to explore and identify the future directions and research streams.

Co-authorship

We identify 26 papers of co-authorships, which include two or more authors or organizations based on Ponomariov and Boardman (2016) methodology. Following van Eck and Waltman (2010), the total link strength is 47, the higher this indicator, the stronger is the link between the research papers. We use a link strength of 5 in this paper as identified in Figure 5 using VOSviewer.

Coauthorship.

The red cluster shows that W. Wang is the leader with three co-authors followed by I. Wang and Y. Ma with three clusters each in blue and green while W. Yang has two links in purple cluster and J. Zhang has one co-authorship link. This analysis shows the existence of cooperation among authors in different locations to address issues related to SIBs.

Bibliographic coupling

Based on Boyack and Klavans (2010) work, the analysis of the bibliographic coupling is applied using VOSviewer for big data. This method conducts automatic clustering to spot pairs of documents that site a third one in the bibliography. According to Figure 6, which plots the papers related to SIBs, there are five major clusters. The most co-cited research papers are those prepared by Demirguc-Kunta and Huizinga (2013) investigating the effect of size on bank stock prices. Next in order is a paper by Brewer III and Jagtiani (2013) which discusses the effect of bank large size through mergers to become too-big-to-fail on stock and bond prices.

Bibliographical coupling of documents.

The implication of those two papers is that security prices should react to increasing size, if large size is believed to be beneficial to investors, stock prices should react positively. In such cases, this will be an instrumental market-based finding confirming the need for further investigation by regulators. Many times banks merge, driven by moral hazard, to take advantage of the implicit subsidies offered by regulators (Andrieş et al., 2020).

Chiaramonte and Casu (2017) analyze the impact of structural liquidity and capital ratios as defined by Basel III on bank probability of failure. The emphasis on SIBs’ capital supports the increased interest by Basel on SIBs. This implies that SIBs’ failures are not only driven by inadequate capital, but also by liquidity levels. Basel III guideline on liquidity structure aims at minimizing “maturity mismatch” between short-term assets and liabilities leading to lower risk profiles. This paper questions the effectiveness of the new guidelines claiming that because they lower bank profitability, SIBs would be induced to take more risk. Clearly, these documents are in line with our subject and tackle important issues related to SIBs.

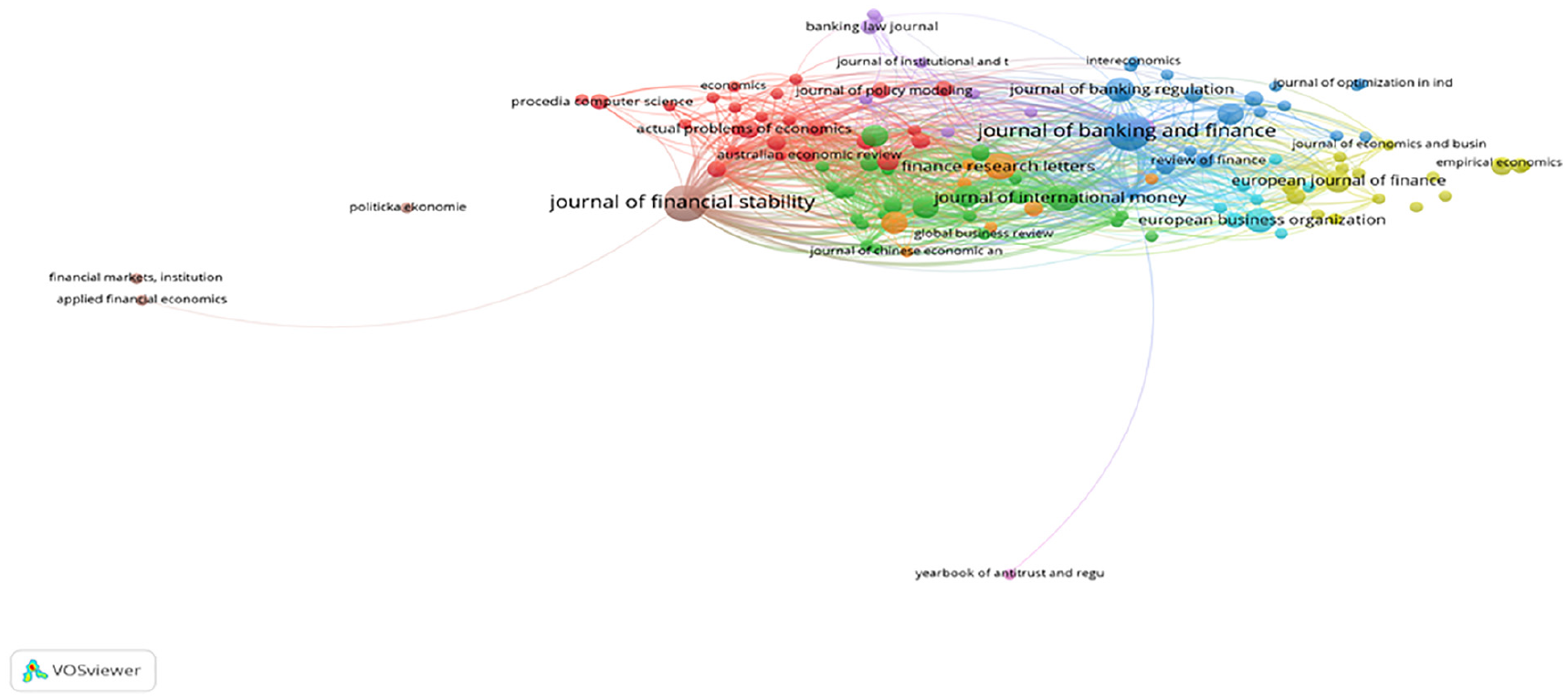

Figure 7 reports the clusters of the sources; our analysis limits the citations to five, each has a distinct color following Paltrinieri et al. (2019). The leader of the journals in terms of strongest link is the Journal of Financial Stability (JFS) in brown cluster. It is linked to the Australian Economic Review in red cluster (which has links with other journals such as the Finance Research Letters) and the Journal of Chinese Economic and Business Studies. JFS is followed by the Journal of Banking and Finance in blue cluster which has strong links with the Journal of International Money and Finance in green cluster and the Journal of Finance Research Letters, the lead journal in orange cluster which takes a center stage. The purple cluster includes the Journal of Policy Modelling. The most linked journal is the Journal of Financial Stability in brown cluster. It is notable that there is a diversity in terms of the levels of the journals implying a wide spread research publications and interests in SIBs issues from several levels of researchers.

Bibliographical coupling of sources.

Co-citation

According to Shiau et al. (2017), this analysis enables defining streams by the strength of relationship between documents, it spots pairs of documents cited in the same paper. Our threshold is set at a minimum of five citations and five clusters. The purple and green clusters have weak connection with blue, red, and light blue. On the other hand, the blue and red cluster exhibit the strong relations with each other (Figure 8).

Co-citation of references.

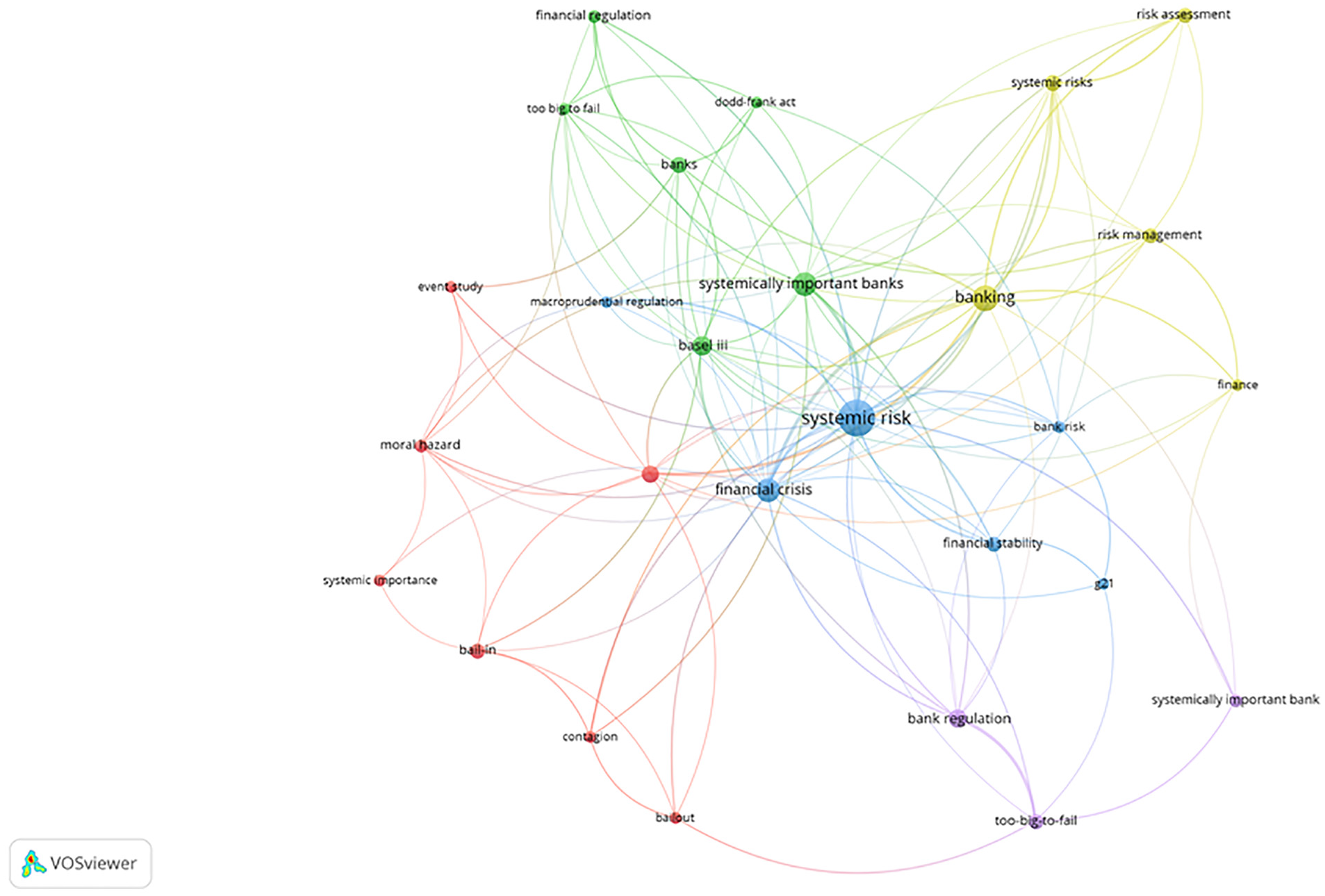

Keywords

The analysis of keywords sets the frequency to a minimum of five occurrences as shown in Figure 9, which reports five clusters. This analysis helps in determining our research streams. SIBs subject (which has five subcategories: Basel III, banks, too-big to-fail, financial regulation, and Dodd-Frank Act) falls into five categories:

- Systematic risk in green cluster

- Banking in blue cluster

- Financial crisis in red cluster

- Basel III in light green cluster

- Financial regulation in green cluster.

Co-occurrence of keywords.

Thematic evolution

Our analysis covers 20 years of SIBs literature (2002 to early 2022). While our time span is divided into four subperiods with 5 years each, we focus on the last subperiod (2017–2021) wherein this period witnessed the largest volume of research activities comprising 134 articles out of 222 publications (Figure 1). This subperiod was selected due to the fact that Basel III came out in 2009 but research activities accelerated during 2017 to 2021 and it was the first serious attempt to discipline SIBs. Before Basel III, large banks were known to be special institutions but they were not subjected to special guidelines.

- To identify the themes based on centrality and density and enhance the accuracy of the results, we apply the “thematic evolution map which is available in the R-software.”Figure 10 presents the quadrants according to Cobo et al. (2011) classification. The quadrants are as follows:

- The lower right is underlying theme; the subject is Basel III and systematic risk

- The lower left is emerging theme; the subject is general banking

- The upper right and left are specialized themes; the subjects are bailing out SIBs and financial crisis.

Thematic evolution.

Future Research Questions and Streams

Research Stream 1: Systematically Important Banks and bailout

Bailing out SIBs is one of the major issues facing regulators. Earlier studies argue that central banks believe that their subsides may stop bank deposit runs, minimize failure cost, and promote banking stability (Bi, 2012; Bianchi, 2012; Chari & Phelan, 2014; Cunliffe, 2014; Demirgüç-Kunt & Detragiache, 2002; Diamond & Dybvig, 1983; Farhi & Tirole, 2012; Gropp et al., 2011; Kelly et al., 2016).

Basel III recognized the overwhelming impact of the failure of SIBs and the subsidies they receive in the form of bailing out. Central banks and regulators around the world realize that SIBs are powerful in terms of asset size, connectedness, revenues, capital, complexity, and risk. If an SIB is financially distressed, regulators usually do not hesitate to bail it out. Many times regulators are doing so reluctantly because they know that insolvent banks should be liquidated according to their exit rules and guidelines. They also know that their failures trigger more failures especially due to their connections with other banks. Bailout induce more risk-taking due to moral hazard issues leading to system instability (Dam & Koetter, 2012; Saleh & Abu Afifa, 2020).

Research Stream 2: Systematically Important Banks, Financial Crises

SIBs are very influential; they contribute to economic development more than other banks and benefit from economies of scale and economies of scope. Their failure usually leads to crisis due to the contagious effect on other banks and to the rest of the economy. Regulators usually pay special attention to these organizations and many times SIBs are subjected to strict regulations. However, they benefit from the subsidies they receive from central banks whenever they are financially distressed. SIBs usually are connected to other small and large banks, the failure of any of these banks usually cause the failure of the other banks in the group leading to financial crisis. It is true that their existence is very beneficial to the economy and the society, but their failures result in severe consequences. Passmore and von Hafften (2019) suggest “Banks must self-insure against all losses to avoid all public bailouts, even catastrophic losses. Such self-insurance might result in restrictive credit conditions during times without financial crisis, but this policy would reassure taxpayers that public funds would not be used to assist G-SIBs.” In the US, the Dodd-Frank and Consumer Protection Act of 2010 targeted the elimination of too-big-to-fail moral hazard problem through a number of measures such as downsizing SIBs and limiting the types of activities of those organizations (Acharya et al., 2012; Bekaert & Hoerova, 2016; Campbell & Cochrane, 1999; Ohnsorge et al., 2014).

Research Stream 3: Systematically Important Banks, Basel III, and Systematic Risk

Basel III accord enacted special guidelines and limitations on SIBs to avoid financial distress due to their size. SIBs are too-big-to-fail meaning that regulators cannot afford to let them exit because their failure may disrupt the stability of the financial system due to their size and interconnectedness with other banks. The fact that too-big-to-fail banks anticipate that in crises they will be subsidized means that they will be induced to take more risk.

Before Basel III, they were treated just like all other banks without any restrictive measures. Financial crises had their impact on regulators who have been trying to limit such crises and maintain sound and safe banking systems. This was the case until Basel III became effective as this standard recognized that large banks should be subject to strict guideline to minimize the probability of failure (Benoit et al., 2017, 2019; Birn et al., 2017). Poledna et al. (2017) claim that “capital surcharges for Global-SIBs can reduce systematic risk, but must be larger than those specified in Basel III in order to have a measurable impact. This can cause a loss of efficiency. Basel III capital surcharges for G-SIBs can have pro-cyclical side effects.”

Research Stream 4: Systematically Important Banks and Banking

According to Yuksel (2014), “in 2010 the Financial Stability Board (FSB) defined systematically important financial institutions to be those institutions’ whose disorderly failure, because of their size, complexity and systemic interconnectedness, would cause significant disruption to the wider financial system and economic activity.”

The market share of SIBs in any country is usually high implying that their actions are more powerful. They are interconnected with other banks and more diversified yet their failure is very harming. It is true that diversification helps in reducing their risks but they have been criticized of being bureaucratic and less efficient. The literature addresses this issue but the evidence is not conclusive. On the one hand, SIBs are more capable of offering large scale products with enhanced scope, which makes them more profitable. However, being less efficient makes them less profitable and their failure can be severe especially due to their connections with other banks (Basel Committee on Banking Supervision, 2013; Bernanke, 2009; Drehmann et al., 2010; Li et al., 2012; Liang et al., 2013; Rajan, 2009).

Future Research Directions

Although bailing out SIBs seems to be necessary to prevent system-wide financial distress, if banks anticipate that they will be rescued, they will be induced for more risk-taking, which counters the safety and soundness objective. SIBs gained more attention after the 2008 financial crisis because regulators did not have a choice but to bail them out, which unfortunately induced more risk-taking. The moral hazard behavior was exacerbated by the degree of expectations of the subsidies, which distorted competition and increased the probability of failure (Dam & Koetter, 2012; Violon et al., 2020). These developments raised the question of whether SIBs should be subject to stricter capital requirements and improved supervision. We argue that more capital is necessary to enhance market discipline and the resilience of the banking system. That is, the safety and soundness objective takes precedent over the cost of capital. How can regulators avoid the unfair treatment and minimize financial crises is a question for future research. We expect future research to test the following issues:

First, the feasibility of raising the capital adequacy requirements significantly from the current 12.5% in Basel III to 20% or 25% and address the need to impose an even higher ratio to SIBs (Alzoubi, 2021; Passmore & von Hafften, 2017, 2019). Limited evidence is available on this subject. We argue that even though capital may be costly, the safety, and soundness of the banking system should take priority over the cost issues. Buch & Goldberg (2020), Buch (2020), and Giudici et al. (2020) argue that in order to increase the resilience of financial institutions and avoid systemic risk, there is a need to reform the regulations related to the financial sector. In addition, they suggest that more than 10 years after the crisis have passed, and the implementation of the agreed reforms is progressing, it has become possible to assess the effects of the implemented reforms. A large number of academic and policy-related studies have assessed the effects of financial sector reforms. “Some of these findings have been prepared using a framework for the post-implementation evaluation of the effects of financial regulatory reforms which the Financial Stability Board (FSB) introduced in 2017.”

Second, the possibility of downsizing SIBs and global SIBs (G-SIBs). Scholars have not tackled such issues adequately. More capital may be costly, but it raises owners’ control and enhances market discipline leading to lower risk (Schoenmaker, 2017). National authorities should identify the number of SIBs before they subject them to any additional restrictive measures (Buch & Goldberg, 2020). National authorities need to reform their regulations with specific guidelines for SIBs and academic scholar on the other hand may find this a subject of research and investigation.

Third, one of the important lessons that we have learned from crises is that the failure of large banks is systematic and may spillover to the rest of the economy, but limited evidence is available on the issue of too-big-to-fail (Andrieş et al., 2022; Avdjiev et al., 2019; Cohen, 2013; Park & Shin, 2020).

Fourth, identifying SIBs is another issue that has not been investigated enough in recent literature especially in developing countries and the new guidelines set by the BCBS is based on book values not market values (European Central Bank, 2021). In 2011, the BCBS introduced certain guidelines to define SIBs, these guidelines apply to member countries and may not be appropriate to developing countries. Each country needs to apply its own guidelines and identify the number of SIBs accordingly. This issue received more attention after the 2008 financial crisis. However, many countries “have not formally designated any financial institution as systemically important to date. Nor have they announced any formalized methodology of identifying systemic institutions” (Bengtsson et al., 2013; Foglia & Angelini, 2021).

Fifth, can national authorities refrain from subsidizing SIBs in crises? The evidence is very limited. Dam and Koetter (2012) claim that the bailing out financial institutions during the 2008 financial crisis proves two important lesson; first that governments were forced to bail out SIBs; second, whenever governments’ subsidies are expected, banks will be induced to take more risk due to moral hazard (Alzoubi, 2021). Bailing out undermines market discipline, distorts competition, and raise the probability of financial distress (Lambert et al., 2014; Ueda & Weder di Mauro, 2013).

Conclusions

Past studies on SIBs discussed many related issues. To provide a structured overview of the most important ones, we applied a bibliometric review and classified them into significant research groups (clusters) in addition to exploring future research needs. Scopus database is used to reach this goal by collecting 222 published papers on SIBs between 2002 and early 2022. In addition, VOSviewer and RStudio are used to analyze citation patterns, and various other relationships, keywords occurrence, and research performance. We find that the USA is the most relevant country to this topic, the University of Southeast is the most relevant institution, and the Journal of Banking and Finance is the most relevant journal. There are four main topics: (1) Bailout, (2) Financial Crisis, (3) Basel III, and the Role of Banking. SIBs are usually more diversified, which helps in reducing their risks but they have been criticized of being bureaucratic and less efficient. SIBs are more capable of offering large-scale products with enhanced scope, which makes them more profitable. However, being less efficient makes them less profitable and their failure can be severe especially due to their connections with other banks

Central banks believe that their subsides may stop bank deposit runs and minimize failure cost and promote banking stability. Large banks should be subject to strict guidelines to minimize the probability of failure, such as limiting the number and the types of activities of those organizations and be subject to higher capital surcharges. We provide several issues for future research including downsizing SIBs and G-SIBs, improving the capital adequacy requirements and defining SIBs with appropriate guidelines.

Footnotes

Appendix A

Declaration of Conflicting Interests

The author(s) declared the following potential conflicts of interest with respect to the research, authorship, and/or publication of this article: We hereby declare that we are not financially bound to or dependent on, any organization or any party having a direct financial contribution to the object of the study or materials tested in a given study (e.g., by employment, consultancy, holding of shares, fees), except for those mentioned in the attachment. We understand that every subsidy for studies or the project has to be listed in a footnote of the first page of the paper.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.