Abstract

Many studies have examined the impact of economic fundamentals on the financial market, but few have explored how financial market information affects the real economy. In this paper, we examine the effects of stock price informativeness on firms’ total factor productivity (TFP) using panel data of Chinese listed manufacturing firms over the period 2007 to 2017. Specifically, we use stock price nonsynchronicity to measure stock price informativeness, and real economic activity efficiency is proxied by the listed firms’ total factor productivity estimated by the LP and ACF methods. We find that stock price informativeness is positively associated with firms’ productivity in China. More importantly, we propose two possible mechanisms to intensify the consequences of stock price informativeness and find that operating pressure and financial constraints can positively intensify the relationship between stock price informativeness and firms’ TFP. As financial information is crucial for sustainable and steady economic growth, our research not only helps to reveal how the financial market promotes economic growth but also helps to provide new ideas for managers and policy-makers to alleviate operating pressure and financing constraints.

Keywords

Introduction

It is extensively accepted that total factor productivity (TFP) is one of the most important core driving forces for firms’ development and economic growth. Since Solow (1957) proposed this concept, total factor productivity has always been a hot topic in academia and industry. How financial factors, such as financial development (Arizala et al., 2013), financial availability (Butler & Cornaggia, 2011), corporate governance (Ittner et al., 2003; Kim & Ouimet, 2014), and financial friction (Midrigan & Xu, 2014; Moll, 2014; Restuccia & Rogerson, 2008), may impact firms’ productivity has been widely studied. Although previous studies discuss the effects on TFP from many financial perspectives, few studies have focused on the effects of financial market information on firms’ productivity. The relationship between financial market information and firms’ TFP deserves more academic attention.

We believe that stock price informativeness may affect listed firms’ productivity in at least three ways. First, the managers of listed companies can learn and utilize the external private information contained in the stock price as a reference for decision-making (Chen et al., 2007; Luo, 2005; Zuo, 2016), such as investment or M&A plans, which would further influence the real business activities and promote the high-quality growth of those enterprises. This is called the feedback effect of the stock market on the real economy (Bond et al., 2012), or the managerial learning hypothesis (Ben-Nasr & Alshwer, 2016; Zuo, 2016). Second, stock price informativeness may enhance productivity by strengthening corporate governance. Higher stock price informativeness implies better internal and/or external monitoring (Ferreira et al., 2011), which leads to better corporate governance. Consequently, more informative stock prices may mitigate the agency problem or relieve the empire-building problem (Ben-Nasr & Alshwer, 2016), helping to improve the firm’s productivity. Third, more informative stock prices often mean higher transparency or lower information asymmetry of the company, which helps to reduce the financing cost (Hwang et al., 2013). Stock price informativeness is often positively correlated with better information disclosure and higher-quality financial reports (Jin & Myers, 2006; Zuo, 2016), which helps to alleviate information asymmetry (Diamond & Verrecchia, 1991) and thus mitigate financial market friction.

We believe it is of great significance to study whether China’s stock market information can have an impact on the real economy. First, an early study by Morck et al. (2000) believes that among the 40 largest economies in the world, stock market information efficiency in China is better than only that of Poland, ranking as the penultimate. As China’s stock market efficiency is seriously low, whether such low market efficiency can produce effective information is an important issue worthy of discussion. However, with the deepening of China’s financial market reform, such as the introduction of a short selling mechanism, increasing the proportion of foreign investors and the initialization of the Shanghai Shenzhen Stock Connect Program, the information efficiency of China’s stock market has greatly improved. Therefore, the conclusions of early studies may no longer be suitable. Second, the environment and motivation for managers in the Chinese stock market to learn stock price information are also quite distinct from mature markets. Compared with developed countries, such as the U.S. capital market, the trading mechanism, corporate governance environment, investor structure and legal system in China are still quite immature (Qin et al., 2021). For example, there are a large number of state-owned enterprises in China’s stock market. The “owner” of these enterprises lacks sufficient economic incentives to effectively supervise and evaluate managers. Furthermore, the managers’ shareholding ratio of Chinese listed companies is very low, and it is still difficult to form an effective incentive effect. Therefore, the question of whether the managers of Chinese listed companies learn financial market information and impact the real economy remains unanswered. Third, after more than 20 years of development, the Chinese stock market has become an indispensable part of the global financial market. A huge amount of money has flowed into China’s stock market from home and abroad. What factors of firms can help to enhance the managerial information learning process? Although a rich literature examines managerial information learning in the U.S. and other developed markets, little is known about emerging markets on these issues, especially China. Therefore, exploring the above issues is essential not only for the development of enterprises or the entire financial market in China but also for firms in other developing countries.

In this paper, we extend the previous strand of literature by investigating whether managers can ameliorate firms’ productivity by utilizing information incorporated in stock prices. Specifically, our paper examines whether higher stock price informativeness is associated with higher firm productivity. To test whether stock price informativeness can promote firms’ productivity, we use the Levinsohn-Petrin method (Levinsohn & Petrin, 2003) and Ackerberg-Caves-Frazer method (Ackerberg et al., 2015) to estimate TFP at the firm level, which proxies firms’ productivity. In terms of stock price informativeness, we follow Durnev et al. (2003, 2004), Ben-Nasr and Alshwer (2016), and Bennett et al. (2020) and use stock price nonsynchronicity as our main measurement, which represents firm-specific return variation that does not comove with market and industry returns. Using a sample of listed manufacturing firms in the Chinese A-share stock market over the period 2007 to 2017, we show that information incorporated in stock prices is positively related to productivity. Moreover, our paper finds that operating pressure and financial constraints positively intensify the relation between stock price informativeness and TFP. In particular, the sales growth and net profit margin on sales (the lower the two variables, the greater the operating pressure) downwardly moderate the impact of stock price informativeness on the overall TFP, indicating that operating pressure can intensify the positive relation between stock price informativeness and TFP. Similarly, financial constraints, which are represented by the KZ index and cash flow to capital ratio, upwardly intensify the feedback effects of stock price informativeness on TFP. Finally, based on the above findings, we further discuss whether stock price informativeness can improve financial performance through TFP. Our findings confirm that stock price informativeness will finally enhance ROA and ROE by promoting TFP.

Furthermore, we use three ways to alleviate potential endogeneity concerns caused by reversal causality or omitted variables. First, following the idea of Bennett et al. (2020), we use the average lagged stock price nonsynchronicity over the previous 1 to 6 years as our main independent variable. Second, we also use the addition to the Shanghai-Shenzhen 300 Index as the exogenous impact of the increase in stock price informativeness. Third, we also control for firm fixed effects and year fixed effects to minimize the possibility that time-invariant firm-specific omitted variables bias our results. Our results are also robust to TFP estimated by the perpetual inventory method and other alternative stock price informativeness estimation models.

Our paper contributes to at least two streams of literature. First, it adds to the literature that examines the managerial learning hypothesis. Luo (2005) and Chen et al. (2007) provide early evidence that managers can learn information on stock prices and use this information to ameliorate their decisions, helping to promote investment efficiency. Following their study, Bakke and White (2010), Foucault and Gehrig (2008), Foucault and Frésard (2012), Foucault and Fresard (2014), Ozoguz and Rebello (2013), and Ben-Nasr and Alshwer (2016) confirm that managers can improve investment efficiency by learning the information incorporated in stock prices. However, most of these studies only pay attention to firms’ investment behaviors and use developed countries as the research object. Little is known about whether stock price informativeness can affect firms’ productivity in emerging markets, especially in China. Our study provides direct evidence for the positive relation between stock price informativeness and TFP by using data from Chinese manufacturing listed companies. Second, we also extend the literature focusing on financial determinants of total factor productivity. How financial development (Arizala et al., 2013), financial availability (Butler & Cornaggia, 2011), corporate governance (Ittner et al., 2003; Kim & Ouimet, 2014), and financial friction (Midrigan & Xu, 2014; Moll, 2014; Restuccia & Rogerson, 2008) may impact firms’ productivity has been widely studied. However, there are still few studies investigating the mechanism of how financial information affects firms’ TFP. From a new perspective of financial information, our paper not only shows evidence that stock price informativeness is positively associated with firms’ TFP but also shows that operating pressure and financial constraints can intensify the positive relation between stock price informativeness and firms’ TFP.

The structure of this paper is as follows. Section 2 gives a literature review and hypothesis development. Section 3 introduces data, variable measurement, and empirical models. Selection 4 discuss empirical results. Section 5 gives the robustness test. Section 6 concludes this paper.

Literature Review and Hypothesis Development

Literature Review

In recent years, a growing strand of literature has focused on the feedback effect of stock market information on the real economy and believed that an important way to improve the investment efficiency of enterprises is to learn external information on stock prices. Luo (2005) finds that managers will utilize external information on stock prices when carrying out M&As and make the final decision by learning stock price performance after an M&A announcement. Chen et al. (2007) confirm that higher stock price informativeness (proxied by price nonsynchronicity and probability of informed trading) is associated with higher investment sensitivity to stock prices, which indicates that firm managers can learn private information in stock prices about their own firms’ fundamentals and use this information to guide their corporate investment. Bakke and White (2010) decompose the Tobin Q variance into two components; one component is considered to be related to firm investment, and the other component is irrelevant. The empirical evidence shows that firm managers can learn information incorporated in stock prices to guide their investment decisions since the variance of components related to investment in Tobin Q increases as a firm’s stock price informativeness increases. In addition to cross-market listing, managers will make further efforts to extract information from stock prices and increase investment-Q sensitivity, since international investors can bring more new information to stock prices, such as overseas business development prospects and foreign customers’ demand for products (Foucault & Frésard, 2012; Foucault & Gehrig, 2008). Foucault and Fresard (2014) further point out that to enhance investment efficiency, managers can also learn information from the stock prices of “peer” companies. Ozoguz and Rebello (2013) also find a positive relationship between corporate investment and peer valuation. When peers’ stock price is more informative, the relationship is stronger. Ben-Nasr and Alshwer (2016) conclude that labor investment efficiency will also be affected by stock price informativeness, which is very similar to fixed asset investment. They provide evidence that the probability of informed trading is positively related to the efficiency of labor investment. Edmans et al. (2017) carry out an international study in which they use the enforcement of insider trading laws as an exogenous shock to price informativeness and find that enforcement increases investment-Q sensitivity. Using the data in the U.S. market, Bennett et al. (2020) discover channels other than investment to affect firms’ productivity. In particular, they show that CEO turnover is more sensitive to firm value in firms with more informative stock prices. From the opposite perspective, Xiao (2020) suggests that noise in the stock price will inhibit the operating efficiency of firms via three channels: distorting the price signal, increasing the financing cost and reducing the effectiveness of incentive contracts.

Hypothesis Development

Hypothesis 1

Stock prices can provide forward-looking information on the future profitability of firms’ investment projects. Managers guide their actual decision-making behavior and optimize resource allocation by “learning” the information that is contained in the stock price. Fishman and Hagerty (1992) and Dow and Gorton (1997) proposed that different types of speculators (insiders and outsiders) trade stock according to their information. They establish a theoretical framework in which managers can learn information from stock prices. In the equilibrium point of the model, traders obtain and produce information about the company and use this information for stock trading, so stock prices include not only the internal information of insiders but also the private information of external investors (Balvers et al., 1990; Fama, 1991; Summers, 1986). As the stock price contains information that managers do not have (such as product demand, product competitors, industry trends, etc.), managers will guide their investment decisions by learning the future profitability information in the stock price. Finally, decision-making will be affected by forward-looking information on stock prices and impact the actual operating efficiency of firms.

In addition, stock price informativeness may also affect the company’s total factor productivity by strengthening the external or internal monitoring of managers. Through this monitoring mechanism, firms can improve efficiency if stock prices contain enough information (Ferreira et al., 2011). Bennett et al. (2019) demonstrate that private information in the stock price can reduce the information asymmetry between managers and shareholders, improve shareholders’ observability of the working results of managers, and thus better supervise managers.

Moreover, another benefit to firms with higher stock price informativeness is that they are always associated with a lower level of information asymmetry, which helps to reduce financing costs. Jin and Myers (2006), Hutton et al. (2009) and Zuo (2016) claim that when financial reports are opaque, specific information about the company released to the market will be rare, which will lead to higher information asymmetry (Diamond & Verrecchia, 1991). Therefore, the idiosyncratic volatility of stock prices will be reduced relative to market fluctuations and increase the synchronization of stock prices. Fernandes and Ferreira (2009) argue that insider trading will restrain the willingness of outside investors to collect information; thus, the stock price cannot reflect the true value of the listed company, and the market will undervalue the firm. Therefore, higher stock price informativeness is helpful to reduce the equity cost, making it easier for enterprises to finance and use external funds for technology upgrades. Hwang et al. (2013) provide evidence that there is a significant positive relation between the bias-free adjusted probability of informed trading and the implied cost of equity capital, and the relationship is more obvious in enterprises with poor information environments.

Stock price information implies the future market expectations of the company, and managers can adjust their behaviors accordingly to optimize its operating activities. In summary, stock price informativeness has an important impact on the business activities of listed companies through managerial information learning, strengthening corporate governance, and reducing financing costs. Thus, our first hypothesis is stated as follows.

Hypothesis 2

The relationship between stock price informativeness and TFP will be affected by operating pressure. First, operating pressure can influence managers’ willingness to learn stock market information through the sense of crisis. Eisfeldt and Kuhnen (2013) state that when the industry or business is in a downturn situation, the probability of changing CEOs is high. Due to this pressure of CEO turnover, CEO actions can be more consequential and prudent during periods of business decline compared to periods of strong growth (Wasserman et al., 2010). In crisis situations, the fear that business performance falls short of expectations will cause a huge sense of crisis and pressure for managers (Baucus, 1994; Han et al., 2016) and finally influence their behavior and decision-making. Therefore, when the conditions or performance of listed companies are in trouble, managers need to use more external resources to improve the operating status. As an important external resource, stock market information plays an important role in the process of policies and decision-making (Bond et al., 2012). Therefore, when the listed companies are in a good operating situation, the willingness of the manager to learn and utilize stock market information will be weakened. However, when the company is in a state of high pressure, managers will also increase their willingness to learn and employ external stock market information to eliminate difficulties.

Second, the operating status of listed companies also influences managers’ willingness to learn stock market information through agency costs. When the sales of listed companies grow rapidly, companies often accumulate a large amount of free cash flow. At this time, due to the increase in free cash flow, managers are likely to build a business empire (Stulz, 1988), increase their expenditures on perquisites and other personal consumption (Ang et al., 2000; Jensen, 1986), make ineffective overinvestments (Richardson, 2006) and ignore the information in the stock market. These behaviors or decisions will finally harm the efficiency of resource and capital allocation, reducing the promotion effect of stock market informativeness on total factor productivity. In contrast, when the listed company suffers great pressure from the stagnation of sales or other shocks, the threat of bankruptcy and liquidation will surge. In this circumstance, since this threat will bring losses to managers, such as wages, reputation, and privileges, managers’ interest will be tightly anchored to the company, and the agency problem will be alleviated (Harvey et al., 2004; Williams, 1987). Consequently, managers will increase their willingness to learn and utilize information on stock prices, which helps to eliminate the dilemma and strengthen the promotion effects of stock price informativeness on TFP.

Therefore, this paper proposes the second hypothesis.

Hypothesis 3

Compared to operating pressure, financing constraints have similar effects on the relation between stock price informativeness and TFP, since they curb some bad behavior of managers by generating external financial pressure. Moreover, companies with stronger financing constraints will be more inclined to make use of existing internal and external resources to enhance operational efficiency. Baker et al. (2003) establish an enterprise investment model proving that investment efficiency will be positively associated with financing constraints. They believe that under the pressure of financing constraints, enterprises will actively improve and monitor the efficiency of investment. Hovakimian (2011) finds that when the external financing cost is high, firms would increase the proportion of internal funds distributed to efficient departments, and this is more obvious for enterprises facing higher financial constraints. Although financial constraints cause the shrinkage of total funds, the quality of investment projects will be improved. Managers allocate more funds to valuable investment opportunities. Ben-Nasr and Alshwer (2016) also find that for enterprises with higher financing constraints, the promotion effect of stock price informativeness on the efficiency of labor investment is higher. Bennett et al. (2020) believe that companies with large financial constraints have a strong incentive to alleviate these restrictions by improving resource allocation and production efficiency. As long as information on stock prices can be used without additional funds, the productivity of financially constrained firms tends to be more affected by stock price informativeness.

The higher financial constraints are, the more difficult it is for enterprises to obtain external financing. In this case, managers will have stronger incentives to use external price information to allocate internal resources and funds efficiently and cease unwise investments. Therefore, costless information on stock prices is more favorable and valuable for firms with financial constraints. Based on the above analysis, this paper proposes the third hypothesis.

Variable Measurement, Empirical Models and Data

Variable Measurement

Total factor productivity

To ensure the robustness of our conclusions, this paper will use the Levinsohn-Petrin method (Levinsohn & Petrin, 2003) and Ackerberg-Caves-Frazer method (Ackerberg et al., 2015) to estimate the total factor productivity of the manufacturing listed companies. Since TFP in an index measures the efficiency of physical output, if firms in the service industry are added to the sample, the estimation of TFP will be biased. Therefore, our paper considers only manufacturing firms.

Assuming that the production function follows the Cobb Douglas function:

where

By taking logarithms on both sides of the formula, the above equation (1) can be transformed into the following form:

If we can obtain

Most enterprises in the manufacturing industry tend to produce more products than they sell in the current period. Therefore, the direct use of sales as total output is likely to underestimate it. To solve this problem, we need to use the inventory products to adjust the total output. The total output

Stock price informativeness

In this paper, we use stock price nonsynchronicity to measure stock price informativeness. This method was first proposed by Roll (1988), and it decomposes the change of stock return into the systematic part that can be explained by the market return and the idiosyncratic part that is related only to the specific firm. When there is relatively more firm-specific variation, the return will comove less with the market return and the industry return, so

Following Morck et al. (2000), Durnev et al. (2003, 2004), Ben-Nasr and Alshwer (2016), and Bennett et al. (2020), we perform the following regression:

where i is for firm i and j is for industry j (in this paper, we use the three-digit industry classification code set by the Securities Regulatory Commission in China), and t is for day t.

Since a large

Therefore, the stock price is more informative when a stock becomes less correlated with the market and industry returns, that is, when

Econometric Model

Baseline model

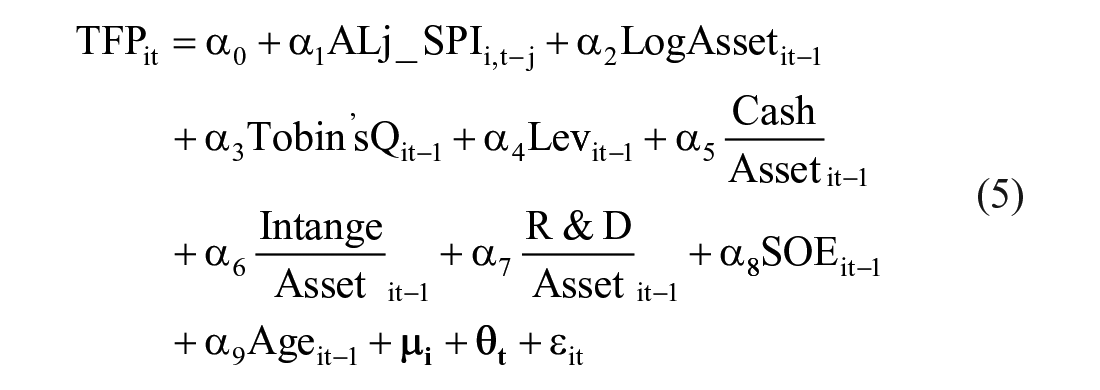

Following Kim and Ouimet (2014) and Bennett et al. (2020), we build our benchmark model as follows:

In equation (5),

The reason why we use the average lagged SPI as the core independent variable is that it can minimize the endogeneity caused by reversal causality. Another reason is that once the information is generated and “learned” by the manager, the impact of the information will be persistent, and even past information may have a strong impact in the current period. However, it is impossible to distinguish which period information is used by managers.

In addition,

Interactive model

To test the second and third hypotheses, we include operating pressure or financial constraints variables and their interactive terms with

In equation (6), the control variables

We use sales growth (

In terms of financial constraints, we use the KZ index and cash flow-to-capital ratio (

Data

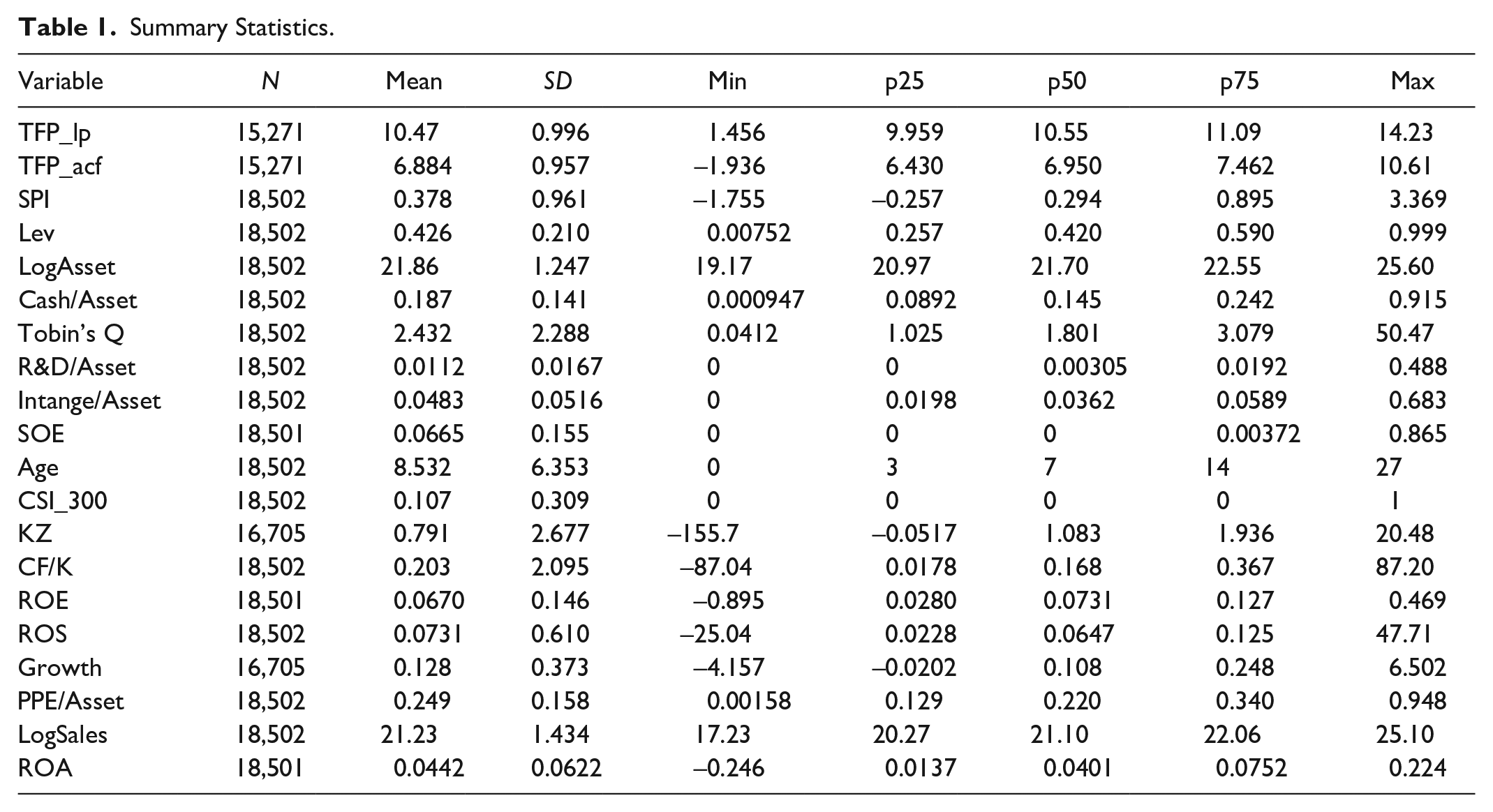

This paper uses the data of manufacturing listed companies in China’s Shanghai Stock Exchange and Shenzhen Stock Exchange from 2007 to 2017. We exclude companies in the financial and service industries and winsorize the continuous variables at the 1st and 99th percentiles to mitigate the impact of outliers. In addition, we also drop the observations in which leverage is negative or greater than 1. Our sample comprises a total of 18,502 observations. The variables in our sample are obtained from the CSMAR and WIND databases.

The summary statistics of the main variables are shown in Table 1.

Summary Statistics.

Empirical Results

Stock Price Informativeness and Total Factor Productivity

In the theoretical framework of the manager learning process (Bennett et al., 2020; Dow & Gorton, 1997; Fishman & Hagerty, 1992), we know that if the financial market can generate information about the future cash flow of company investment projects, managers can learn useful forward-looking information, use it to guide managers’ decision-making and finally increase firms’ TFP. Therefore, in our baseline regression model, the estimated coefficient of ALj_SPI should be significantly positive. This is because ALj_SPI represents the information content in the stock price. If this variable is higher, the manager will learn more information and play a greater role in its real activity.

The regression results for Model (5) are shown in Table 2. Panel A shows results for TFP_acf and

Stock Price Informativeness and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

The above results show that information on stock prices can promote firms’ TFP, that is, higher stock price informativeness is associated with the higher TFP of listed companies. In addition, after comparison of the coefficients in different periods, it is found that with the increase of duration, the estimated coefficients of

Endogeneity Test

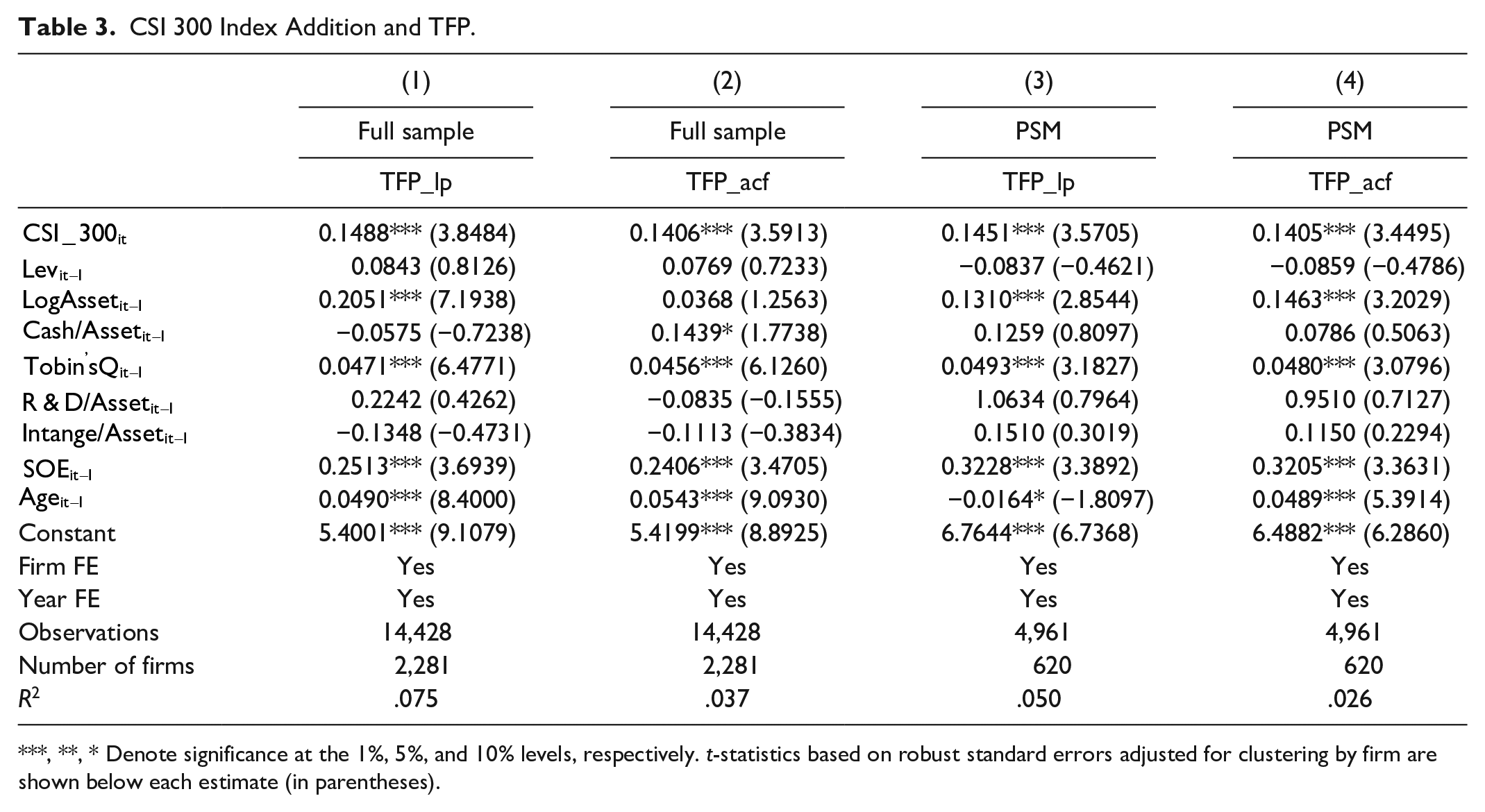

To further reduce endogenous concerns on the regression results, we will discuss the impact of stock price informativeness on TFP by considering whether the stock is a component of the Shanghai-Shenzhen 300 Index (CSI 300 Index). According to the CSI 300 Index instruction, the CSI 300 component stock selection process is mainly composed of three steps: first, calculate the average daily trading volume and the average total market value of each stock in the last year (the new-listed companies are calculated from the fourth trading day); second, rank the stocks by average daily trading volume from highest to lowest, and keep the first half stocks; and third, rank the first half stocks based on average daily market value and select the top 300 stocks. The China Securities Index Expert Committee usually meets in late May and November to verify the sample stocks of the CSI 300 Index, and if needed, the sample stock adjustment is implemented on the next trading day of the second Friday in June or December. According to the above process, we can intuitively conclude that the listed companies are basically not able to determine whether they can be selected as a component stock in the CSI 300 Index.

While studying the influence of stock analysts on the earnings management of listed companies, Denis et al. (2003) point out that if a stock is selected as a component of the S&P 500 index, it will draw more analysts’ attention in the market. Following this idea, when one stock becomes a component stock of the CSI 300 index, the relevant index or strategic funds will be subject to adjust their portfolio by buying this stock. To meet the needs of portfolio adjustment, investment band, or brokerage firms will allocate more analysts to track this stock (Chen et al., 2015), and finally, the number of analysts tracking this stock will rise. Since analysts can collect, sort out and analyze fundamental or industrial information and then disseminate to traders in the market, the more analysts tracking a stock, the higher the stock price informativeness of this stock (Bae et al., 2008; Bushman et al., 2005; Chen et al., 2015).

Based on the above analysis, we know that the addition to the CSI 300 index can be regarded as a quasi-exogenous shock that increases the stock price informativeness of listed companies. Therefore, we establish a multiphase DID regression model as follows:

In equation (7),

For Model (7), we will also use the PSM method (propensity score matching) year by year to select comparable companies for each CSI 300 component company according to total assets, leverage ratio, operating profit per share and earnings per share. In addition, because the composition of the CSI 300 index is dynamic, we perform PSM matching in the year when the stock is added to the CSI 300 index for the first time. In the new PSM sample, the treatment group is the CSI 300 component companies, while the control group is the matched companies that never were added into the CSI 300 index. In PSM matching, the logarithm of total assets, leverage ratio, operating profit per share, and earnings per share are used as matching variables.

Table 3 reports the regression results for equation (7). The estimates in Columns 1 and 2 of the full sample show that the coefficient of

CSI 300 Index Addition and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

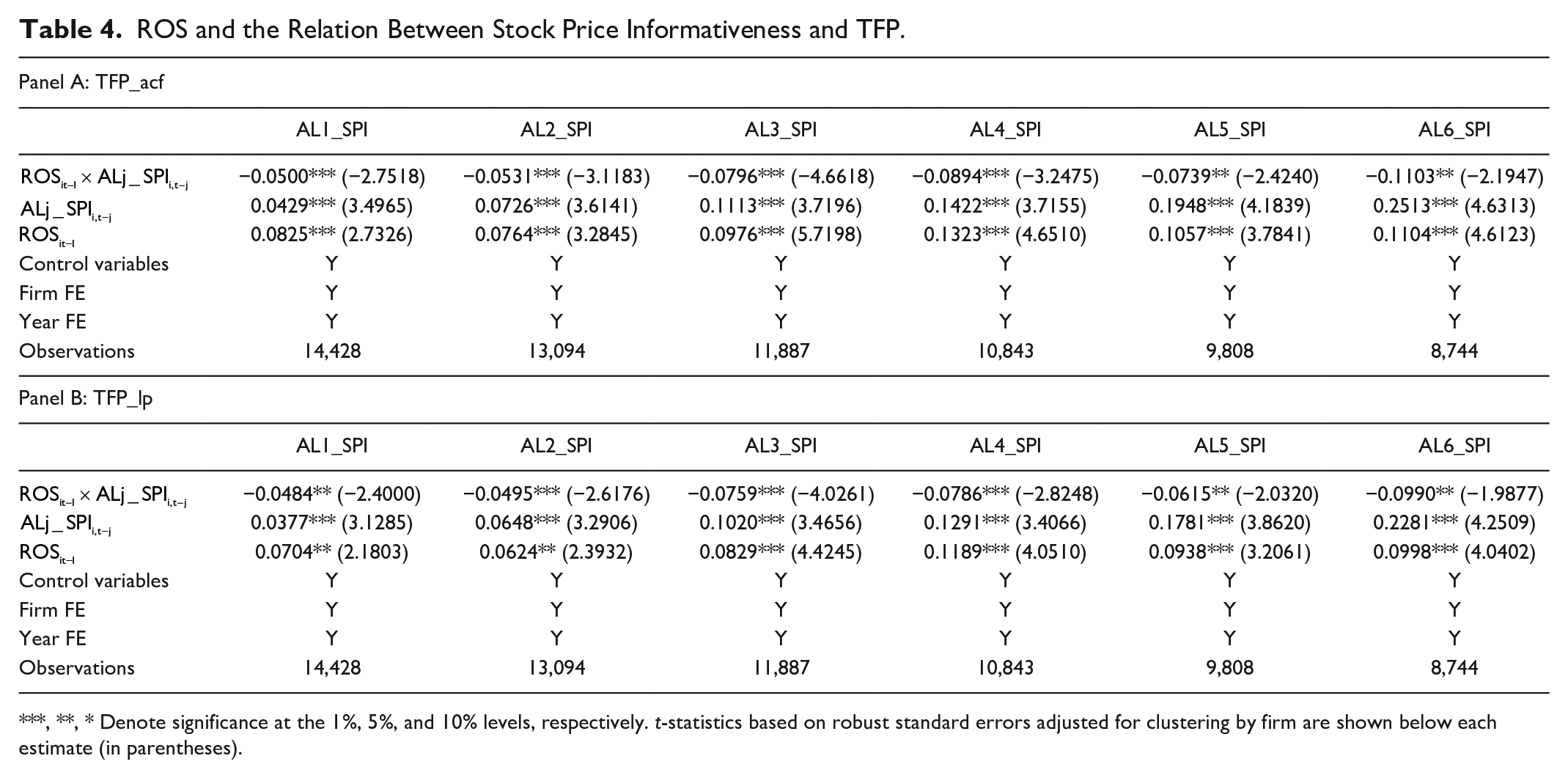

Operating Pressure

Theoretically speaking, operating pressure can affect the efficiency of the manager learning process via two aspects: sense of crisis and agency cost. The fear of CEO turnover will cause managers to use more external resources to improve their operating status (Baucus, 1994; Han et al., 2016), and the threat of bankruptcy and liquidation will alleviate the agency problem (Harvey et al., 2004; Williams, 1987). The above reasons will increase managers’ willingness to learn and utilize stock price information. Thus, in our interactive regression model, the estimated coefficient of the interactive term should be significantly positive.

Table 4 reports the impact of ROS on the relationship between stock price informativeness and TFP. Panel A shows that for TFP_acf, the estimated coefficients of

ROS and the Relation Between Stock Price Informativeness and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

Table 5 reports the impact of sales growth on the feedback effects between stock price informativeness and TFP. Regardless of TFP_acf or TFP_lp, the interactive terms

Sales Growth and the Relation Between Stock Price Informativeness and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

The above results provide evidence that poor operating performance could enhance the promotion effect of stock price informativeness on TFP. In contrast, if companies are in good performance, managers are less incentivized to learn stock price information. There may be two reasons explaining why good operating performance reduces the feedback effect of stock price informativeness. First, the better the performance of listed companies is, the weaker the manager’s sense of crisis (Baucus, 1994); thus, managers will pay less attention to stock market information. Second, when the firm grows rapidly, managers tend to be overconfident and conduct unwise investments, which will finally raise the agency cost (Jensen, 1986; Stulz, 1988). From a different point of view, we can obtain another enlightenment and implication. For regulators, increasing the information efficiency of the stock market will help poorly managed firms eliminate the dilemma and strengthen TFP as soon as possible.

Financial Constraints

The higher their financial constraints, the more difficult it is for firms to obtain external financing. In this case, managers will have stronger incentives to use external price information to allocate internal resources and funds efficiently and cease unwise investments. Therefore, costless information on stock prices is more favorable and valuable for firms with financial constraints.

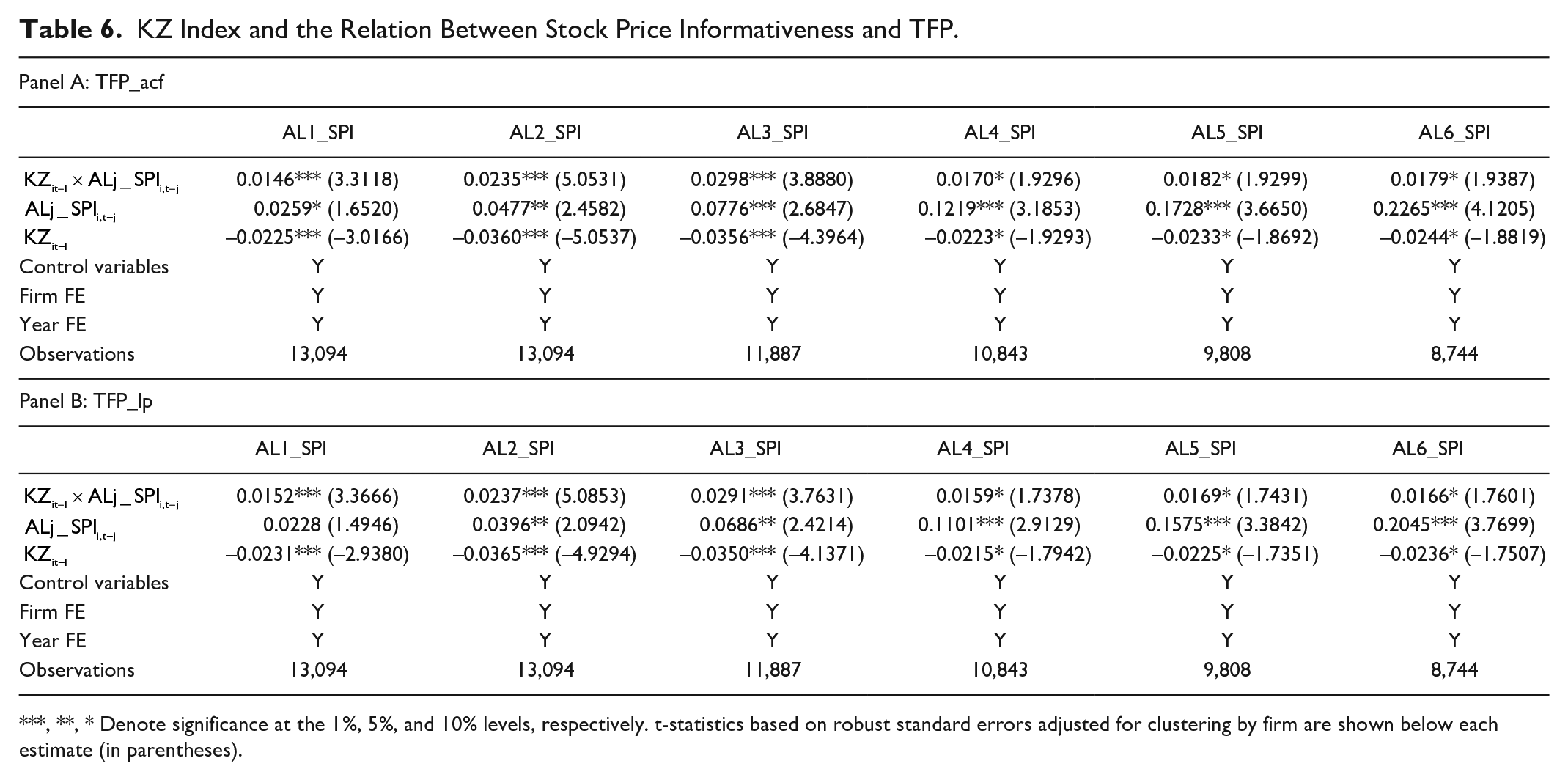

Table 6 reports the impact of the KZ index on productivity-information sensitivity. In Table 6, Panel A shows that for TFP_acf, all the estimated coefficients of

KZ Index and the Relation Between Stock Price Informativeness and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

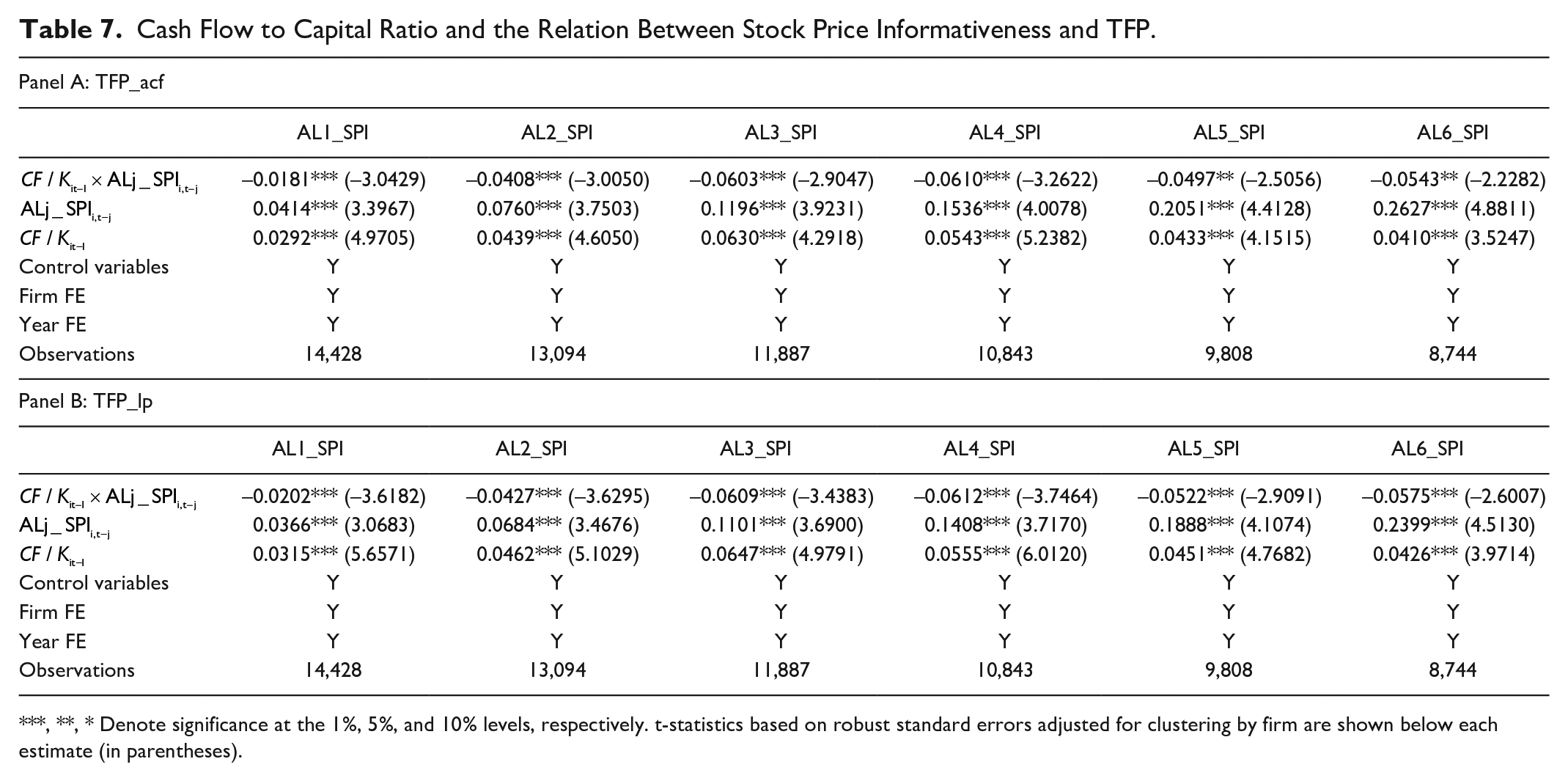

Cash Flow to Capital Ratio and the Relation Between Stock Price Informativeness and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

Our regression results provide evidence that the higher the financial constraints, the higher the productivity-information sensitivity. This result is consistent with the findings of Hovakimian (2011) and Ben-Nasr and Alshwer (2016). When managers are subject to severe external financial constraints, they often have a strong motivation and willingness to alleviate restrictions. They will allocate more resources to the efficient departments to improve the entire efficiency of the company. Since stock market information is a “free” external information resource, managers will be more inclined to learn and use stock market information to optimize business decisions when they encounter financial constraints. The above evidence implies that if policy-makers want to relieve the financial constraints of listed companies, an important and low-cost approach is to enhance the information efficiency of the stock market.

Further Discussion

Thus far, we have shown that stock price informativeness can affect productivity. We now ask whether stock price informativeness affects ROA and ROE. Since TFP is the core driving force of firms’ development, if information on stock prices can promote TFP, then financial performance should be improved as well. In other words, stock price informativeness can affect the financial performance outcomes of listed companies through TFP. ROA and ROE are generally regarded as important indicators of a firm’s financial performance outcome. We use the following model to further verify the impact of stock price informativeness on ROA and ROE:

Table 8 shows the regression results of ROA and ROE. In Panel A, the estimated coefficients of

ROA, ROE, and Stock Price Informativeness.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

Robustness Test

Stock Price Informativeness Estimated by Alternative Model

To test the robustness of our stock price informativeness measure, following Chan and Chan (2014), we add the lagged market and industry returns to the original return model to re-estimate.

For any company in a certain year, we use the following time series model to estimate

where

Table 9 shows the relationship between TFP and stock price informativeness estimated by the new model (Chan & Chan, 2014). Using TFP_acf and TFP_lp as dependent variables, the estimation coefficients of

Stock Price Informativeness (Chan & Chan, 2014) and TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

Total Factor Productivity Estimated by Perpetual Inventory Method

Because the net value of fixed assets is likely to be affected by financial manipulation, it may not well reflect the actual capital input of listed companies and bias the TFP estimation. Therefore, the perpetual inventory method can be used to adjust the net value of fixed assets and calculate the capital input in each period.

Following Brandt et al. (2012), the capital input based on the perpetual inventory method can be calculated from the following equation:

where

The calculation by the perpetual inventory method will incur a missing value problem in the first period. Since our data began in 1999, for firms that were listed before 2000, we take the price-adjusted fixed assets in 1999 as the first period actual capital input. For enterprises listed after 2000, we use price-adjusted fixed assets in the listing year as the actual capital input.

Table 10 shows the estimates adjusted by the perpetual inventory method. The results show that regardless of which kind of TFP is used, the coefficients of

Stock Price Informativeness and Perpetual Inventory TFP.

**, * Denote significance at the 1%, 5%, and 10% levels, respectively. t-statistics based on robust standard errors adjusted for clustering by firm are shown below each estimate (in parentheses).

Conclusion

Our paper concludes the following findings. First, this paper finds that the stock price informativeness of manufacturing listed companies in China’s A-share market can significantly promote their TFP. Although China’s stock market is relatively undeveloped and imperfect compared with those of developed countries, information on stock prices still has significant positive feedback on the production efficiency of listed companies. This affirms that China’s stock market plays an important role in the development of the real economy and confirms the feedback theory that managers can learn the information in China’s A-share stock market and use the information to improve their decision-making. Second, when the operating pressure and financial constraints of listed companies increase, the feedback effects of stock price informativeness on TFP will be strengthened. When facing excessive operating pressure or financial constraints, managers will be more inclined to analyze stock price information to improve the efficiency of internal resource allocation and eliminate the dilemma. Consequently, stock market information is more significant for companies that are facing operational difficulties or financial constraints.

Our study has some enlightening implications for policy-makers and corporate managers. First, the Chinese government should further strengthen the construction of the information disclosure system of listed companies, actively develop China’s institutional investors, and further improve the short selling mechanism of the stock market to improve the information efficiency of stock prices. In addition to equity financing, the stock market is also a place for information generation and transmission and can transmit information to listed companies via feedback effects, affecting the real business activities and production efficiency of listed companies. However, considering the short development history of China’s stock market, information efficiency is far lower than that of developed countries. To give full play to the financing function of the stock market, regulators should pay attention to the information function construction of the stock market and enhance the efficiency of the stock market. Second, for firms with high operational stress and financial constraints, managers will be more motivated to use the information in the stock market to improve their business status. Therefore, financial market information is an important external resource for corporate managers. The use of such resources does not require additional investment from the company; therefore, managers should learn and use financial market information more actively to improve the decision-making level of the company and alleviate its own business difficulties and financing pressure.

Our study has some limitations and can be further discussed in the following aspects. First, this paper examines only how stock market information impacts the total factor productivity of listed companies and does not study the information role of the bond market, futures market or other derivative markets. The trading scale of China’s bond market, futures market and options market is also quite large, and these trading activities will also integrate the external information of traders. Will these trading activities and hidden information also have an impact on the actual production efficiency of the real economy? In the next research step, we hope to explore further whether other relevant market information can affect the production efficiency of the real economy. Second, our paper studies only the impact of stock price information on the same firm’s total factor productivity and does not study the spillover effect of stock price information on the different peer listed companies in the same industry. Information on the stock market can be “learned” not only by managers of the same stock but also by other peer managers of listed companies in the same industry. Therefore, in future research, we can deeply explore the information spillover effect of a certain stock on different listed companies in the same industry.

Footnotes

Author Contributions

Fujun Lai proposed the methodology, gave the formal data analysis, and wrote the original formal draft. Sha Zhu performed the writing-review and editing. Qingxiang Feng performed the funding Acquisition and data collection. Yi Yao wrote the first English version draft.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was funded by the Scientific Research Foundation of Yunnan University of Finance and Economics (No. 2020B03), the Scientific Research Fund Project of Yunnan Education Department (No. 2021J0586), the National Natural Science Foundation of China (No. 71873118), the China Postdoctoral Science Foundation (No. 2019M663356), and the Fundamental Research Funds for the Central Universities. (No. 20wkpy85).

Availability of Data and Materials

The dataset supporting the conclusions of this article is included within the article and its submitted additional file—“submission_data.dta,” which is in Stata format.