Abstract

At present, two big challenges have struck China’s economic development: economic containment “from the real to the virtual” and accomplishment in the goal of high-quality economic development. Taking China’s A-share public manufacturing enterprises from 2007 to 2020 as samples, this paper empirically analyzes the relationships among product market competition, non-financial enterprise financialization, and total factor productivity of enterprises. It is found that non-financial enterprise financialization significantly lowers down the total factor productivity of enterprises, that is, the total factor productivity of enterprises will drop by 1.7% as the non-financial enterprise financialization rises by 1 SD every time. After external regulation effects of product market competition are further taken into account, the furious product market competition, on the whole, mitigates the negative influences of non-financial enterprise financialization on total factor productivity of enterprises by strengthening the role of non-financial enterprise financialization as a “reservoir” and abating the “crowding-out” effect. Therefore, competition promotion policies combined with funds moving “from the virtual to the real” could more effectively elevate the enterprise productivity.

Keywords

Introduction

Recent years have witnessed the obvious tendency of China’s economy to move “from the real to the virtual.” From the macro perspective, the false prosperity in such markets as the real estate and the shadow banking is caused by the falling efficiency of financial services to the real economy, and the continuous cash flow to virtual departments for the circulation inside the financial system. According the data released by the National Bureau of Statistics (“NBS”), the total value added of China’s financial industry plus real estate industry in 2007 accounts for 10.7% of Gross Domestic Product (“GDP”) of that year, followed by an increase to 15.5% in 2020. On the contrary, the value created by China’s industrial sector fell to 30.9% of GDP in 2020 from 41.4% in 2007. In the micro sense, an increasing number of enterprises invest a large sum of funds in sectors like financial and real estate rather than focus on their main business. On top of this, the percentage of corporate financial returns is ascending year by year. The extra care must be taken to keep high alert on the large sum of funds that flow to virtual department, despite that the abovementioned situation incontrovertibly and partially arises from transformation and upgrading in enterprises by virtue of their diverse businesses. On the contrary to the exacerbating financialization, both the Chinese economy and its total factor productivity (“TFP”) have notably experienced the slack growth in recent years (Sleuwaegen & Ramboer, 2019), all of which have captured the attention of the whole society. At the National Conference on Finance in 2017, three priorities were concluded—service to real economy, prevention and control of financial risks, and deepening of financial reform, together with the significant principle (serving the real economy is the ultimate goal of financial tasks) that was stressed to carry out financing tasks. In the Report at the 19th National Congress of Communist Party of China, likewise, it is explicitly pointed out that “we shall deepen the reform in the financial system to strengthen capabilities of finance to serve the real economy. From the perspective of practice, China’s government has adopted a number of policies on financial risk prevention and guidance to funds “from the virtual to the real,” so as to crack down real estate speculation, supervise and well regulate banking services and financial derivative markets, and rectify enterprise’s purposes of fund raising.

Across the academic community, scholars have discussed impacts of the enterprise financialization in two dimensions of the “reservoir” role and the “crowding-out” effect of the non-financial enterprise financialization. Some studies show that due to the role of the enterprise financialization as a “reservoir,” increasing financial assets may effectively alleviate financial constraints on enterprises (Akbar et al., 2017), and thus, stimulate more corporate investments in real businesses like innovation (Mannasoo et al., 2018; Nasir et al., 2021). Some of other studies indicate that the “crowding-effect” that the enterprise financialization significantly imposes upon the real production and investment (Campling, 2020) will bring in negative influences to business performance and productivity of enterprises. Notwithstanding, these studies are not exempted from shortcomings as below in the holistic sense: first, the viewpoint on impacts of enterprise financialization has not yet been finalized in existing studies. In this paper, it is contended that the impacts of enterprise financialization upon real investment and total factor productivity contain the severe endogeneity problem posed by reciprocal causation. The inappropriate solutions to the endogeneity problem will interfere with empirical results, or even reverse the research conclusion. Second, though the enterprise financialization are theoretically endowed with both the “reservoir” effect and the “crowding-out” effect, no related study focuses on those factors that determine the relative extents of these two effects. Both internal and external environment of enterprises will affect investment decisions of enterprises. As a projection of external environment of corporate governance, the product market competition is bound to impose influences upon enterprises’ motives and conducts in connection with investment. According to this paper, it is argued that the product market competition is a significant factor that determines the relative extents of these two effects, on the basis of which this paper adopts the dimension of product market competition to observe whether or not the impacts of enterprise financialization upon total factor productivity will vary with the intensity of product market competition.

In this paper, the data about China’s A-share public manufacturing enterprises from 2007 to 2020 are used to empirically verify impacts of enterprise financialization and product market competition upon total factor productivity of enterprises. The verification results indicate that the increase in total factor productivity is significantly curbed by enterprise financialization which will lower down total factor productivity by 1.7% as it goes up by one standard deviation every time. On top of this, several groups of robustness testing are carried out by virtue of benchmark regression to ensure stability of results. Furthermore, the benchmark model is examined with the help of the instrumental variable method and the difference-in-differences model developed through exogenous policies promulgated by China Securities Regulatory Commission in 2012, in order to overcome potential impacts of exogeneity problems in the empirical model. After the external regulatory effect of product market competition is further taken into account, it is elicited that the intensified product market competition could remarkably impair negative influences of enterprise financialization upon corporate total factor productivity by enhancing the “reservoir” effect and abating the “crowding-out” effect.

Compared with existing literature documents, this paper is likely to make its marginal contributions including: one, adoption of both the instrumental variable method and the difference-in-differences model developed through exogenous policies promulgated by China Securities Regulatory Commission in 2012 to examine the benchmark model for overcoming potential impacts of exogeneity problems in the empirical model, so as to minimize biased estimates caused by endogeneity. Two, the interplay between enterprise financialization and product market competition is incorporated in this paper to discuss impacts of enterprise financialization upon total factor productivity, and prove the role of the intensified product market competition as a catalyze that enhances the “reservoir” effect of enterprise financialization and impairs its “crowding-out” effect. As a result, it serves as a market-oriented idea for governments to appropriately address the excessive enterprise financialization, and even provides experience in further deepening the supply-side structural reform, and creating the fair and open environment of market competition.

The rest parts of this paper consist of: literature review and research hypothesis (Part 2); research methods, including data description and indicator selection (Part 3); empirical analysis (Part 4); Discussion (Part 5), and Conclusion (Part 6).

Literature Review and Research Hypothesis

Literature Review

As far as the academic community’s concerned, most of studies on enterprise financialization center on two aspects from the perspective of literature search: causes of enterprise financialization, impacts of financialization. In the face of weak external demands, excess domestic product capacity, and diminishing bonuses of institution and human resources, enterprises experience soaring risks of fixed asset investment (Arellano et al., 2019) as enterprises’ earning expectation is consolidated, profit rates continue to fall down, and such uncertain factors as market competition pressure and economic policies play their roles (Deng & Yang, 2020). Consequently, enterprises are forced to pursue new channels for investment and earnings (Campling, 2020; Krippner, 2005; Orhangazi, 2008). Owning to the profit pursuit as a feature of capitals, the apparent return gap between high financial investment returns and low returns on real investment has further cajoled enterprises into financialization (Lashitew, 2017; Ma, 2003; Nguyen et al., 2017). Judging from the study made by Du et al. (2017), the discrimination on bank credit risks acts as the main cause why the returns on financial asset investment have overtaken those on fixed asset investment for a long time, while enterprises provide shadow banking services after their financialization. Furthermore, enterprise financialization may also be driven by participation in corporate governance and pursuit of immediate interests undertaken by institutional investors with shareholding (Davis, 2017), together with managerial staff’s overconfidence in their academic background on finance (Francis et al., 2015). Also, the corporate financial investment is stimulated by more resource supplies from financial sectors and abundant idle funds held by enterprises of good business performance.

Despite that a number of literature documents talk about impacts of enterprise financialization, there are big differences in conclusions of these literature documents, let alone positive or negative. From the positive perspective, Aktas et al. (2019) point out that financial assets featuring strong cashability and low adjustment costs could effectively satisfy enterprises’ demands for investment funds in the future. Likewise, Ehigiamusoe and Lean (2019) concludes in his study that financialization has acted as a “reservoir,” that is, the increasing percentage of financial assets held could alleviate financing constraints on enterprises. As far as financial assets are concerned, its profit effect could boost R&D and innovation of enterprises in the future (Carstens & Wesson, 2019), its high liquidity could mitigate risks of financial distress that enterprises may face (Aktas et al., 2019; Alexandridis et al., 2020), and its high return of investment (“ROI”) with rising asset prices could effectively ameliorate balance sheets of enterprises, which, in turn, will catalyze refinancing and drive enterprises to allocate more funds into real investments (Nasir et al., 2021). As for adverse viewpoints, enterprise financialization obviously imposes the “crowding-out” effect upon enterprises’ investment in main businesses and innovation (Stockhammer, 2004), while the decreasing funds for real investment and R&D greatly lowers down enterprises’ capabilities of innovation (Nguyen et al., 2020). Consequently, the development of enterprises in main businesses will be impaired (Aalbers, 2008), and the improvement in total factor productivity of enterprises will be held back (Bellocchi et al., 2020; Rico & Cabrer-Borras, 2020).

In studies concerning the relationship between product market competition and enterprise investment, contrary interpretations are given in different theories. Bonfatti and Pisano (2020) propose the escape competition effect of market competition. Enterprises experience diminishing profits as product market competition intensifies. For the purpose of more profits from market competition, enterprises are apt to avoid competition with other enterprises by improving business management and technical innovation. Also, similar conclusions are elicited from empirical studies made by Backus (2020) and Griffin et al. (2021) by virtue of enterprise samples from different countries. According to Schumpeter’s Hypotheses, however, the furious product market has dissipated innovation rents of enterprises, which, in turn, has demoralized enterprises in terms of incentives to invest in productivity. Some studies point out that impacts of product market competition upon enterprises’ investment in productivity are featured by heterogeneous enterprise’s productivity. In other words, product market competition holds back the productivity investment made by enterprises of high productivity, while those of low productivity will be motivated by product market competition to invest in productivity.

To sum up, scholars discuss impacts of financialization upon productivity in the dimension of the relationship between financialization and investment (especially investments in technical research and development). As for financialization, relative extents of its “reservoir” effect and “crowding-out” effect will be changed as product market competition will affect enterprises’ motives and behaviors in connection with investments. Therefore, this paper will deeply probe into the relationship between enterprise financialization and total factor productivity on the basis of enterprise financialization and interaction effect between enterprise financialization and product market competition, so as to shed light on solutions to excessive economic financialization, and on acceleration in the accomplishment of high-quality economic development.

Research Hypothesis

Enterprise financialization and total factor productivity

Total factor productivity is an important indicator used to measure overall output efficiency of enterprises. It could be greatly influenced by improvement of enterprises in fund allocation, technical innovation, and organizational management. Enterprise financialization is one of resource allocation ways that enterprises adopt largely for capital operation, and it could impose direct influences upon fund allocation efficiency and technical progresses of enterprises. To be specific, enterprise financialization will generate “reservoir” effect and “crowding-out” effect. The former one means that an enterprise decides to allocate financial assets for the purpose of transactions or precaution. In this case, total factor productivity suffers from three kinds of impacts: first, an enterprise invests surplus idle funds into financial assets for both great returns on financial asset investment and prompt chashability by selling financial assets to alleviate liquidity constraints. Consequently, the efficiency in fund use is improved on the whole to maintain or add value of funds (McMaster et al., 2020). Second, unlike assets in-kind, the high liquidity of financial assets is embodied as strong sense of financing mortgage. Due to balance sheets polished by financial assets, corporate capabilities of financial is further reinforced. Thus, the increasing share of financial assets could loosen more external financing constraints of enterprises (Nasir et al., 2021). Third, the corporate funds increased by great returns on financial assets and rising asset prices could stimulate more funds invested by enterprises into production equipment upgrading and real investment; furthermore, it could imbue enterprises with more power to carry out technical innovation and new product development (Thomas et al., 2015). Therefore, the “reservoir” effect could holistically elevate total factor productivity of enterprises.

As implicated in the “crowding-out” effect, in the case of limited disposable funds, the increasing share of corporate financial asset allocation will take up funds that should have been invested in such fields as talent cultivation, equipment upgrading, and technical development and innovation. In turn, both corporate technical innovation and business performance will be impaired. In addition, great returns of financial investment will catalyze more energy of business managers in financial investments. With less emphasis placed on the development of main businesses, investments in technical development and staff trainings will get reduced, and thus, improvement in total factor productivity of enterprises will be further held back.

Now therefore, the following hypotheses are proposed in this paper:

Hypothesis 1a: Enterprise financialization will accelerate the increase in total factor productivity, if such financialization has the predominant “reservoir” effect.

Hypothesis 1b: Enterprise financialization will curb the increase in total factor productivity, if such financialization has the predominant “crowding-out” effect.

“Moderating effect,” of product market competition on relationship between enterprise financialization and total factor productivity

On the basis of the relationship between product market competition and both “reservoir” effect and “crowding-out” effect of financialization, this paper discusses the “moderating effect” that product market competition imposes on the relationship between enterprise financialization and total factor productivity. With the diminishing excess corporate profits caused by the intensifying market competition, enterprises will face more risks of bankruptcy liquidation, or tend to be acquired or merged (Oh & Shin, 2020). As indicated in the “bankruptcy liquidation” theory, those enterprises under the pressure mechanism of bankruptcy liquidation risks will reduce inefficient investments like high-risk interest arbitrage, place more emphasis on the development of main businesses, and elevate their product positions in market competition by investing more in research and development of new products and new technologies, so as to avoid elimination from furious market competition. Therefore, the intensified product market competition will enhance the “reservoir” effect of enterprise financialization, and abate the “crowding-out” effect that is aimed at the cross-industry interest arbitrage. On the contrary, the “escape competition effect” hypothesis points out that in the case of weak market competition, corporate profits will decrease as market competition intensifies. Thus, enterprises will invest more in innovation to escape from current competition for the purpose of great innovation profits (Bonfatti & Pisano, 2020). More furious product market competition will more strongly drive enterprises to escape from competition with growing demands for productive investments. As a result, it is elicited that financialization will show “reservoir” effect more obviously. Accordingly, the following hypotheses are proposed in this paper:

Hypothesis 2a: in the case of weak product market competition, enterprise financialization holds back total factor productivity; as product market competition intensifies, enterprise financialization experiences decreasing suppression upon total factor productivity, but more strongly facilitates total factor productivity. Finally, the facilitation effect predominates.

Hypothesis 2b: in the case of weak product market competition, enterprise financialization has the predominant “crowding-out” effect; as product market competition intensifies, enterprise financialization experiences the stronger “reservoir” effect, while its “crowding-out” effect gets impaired. Finally, the “reservoir” effect predominates.

Research Methodology

In the face of changes in China’s related accounting standards in 2006, China’s A-share public manufacturing enterprises from 2007 to 2020 are taken are research samples in this paper to ensure the unity of financial data. The initial data are processed as follows: samples of financial enterprises and real estate enterprises are eliminated from this study for the sake of the subject matter in this study—enterprise financialization; on top of this, this paper is concerned with functions of corporate production functions, so only manufacturing enterprises remain as research samples to unify applicability of production functions; second, those enterprises who are listed on the market less than 2 year are eliminated according to usual practice; third, ST/*ST enterprises in the sample period are eliminated; fourth, those enterprises that severely suffer from data missing are eliminated. Eventually, altogether 1,763 sample enterprises and 18,976 valid observed values in 26 segmented manufacturing sectors are acquired. On the basis of abovementioned data, the unbalanced panel for 14 years are developed in this paper from the perspective of enterprises. The data about corporate financial standings are sourced from CSMAR database,and the data of regional financial development level are from the Financial Statistics Yearbook over the years.What’s more, all continuous variables in this paper are winsorized at extreme value 1% to mitigate impacts of abnormal values. The kernel variables used in the empirical study include:

(1) Level of enterprise financialization. With reference to studies made by Hattori (2020) and Lashitew (2017), the ratio of financial assets to total assets (far) is applied in this paper to measure the level of enterprise financialization, while the ratio of financial earnings to total earnings (fer) is adopted for robustness testing. Financial assets include: trading securities, financial derivatives, loans and net payment amounts on behalf, available-for-sale financial assets, held-to-maturity investments, dividends receivable, interests receivable, investment real estates, and other current assets. Demir (2009) brought monetary capital into the category of financial assets in their research.However, considering that monetary capital is mainly used to meet the needs of enterprise operation and enterprises will also generate monetary capital in the process of business activities, this paper does not include monetary capital into the category of financial assets.According to Demir (2009) and China’s accounting definition, financial income includes investment income, gain or loss from changes in fair values, and subtracted net investment income from joint ventures and affiliates.

(2) Total factor productivity.

in which, Y stands for business output. It is expressed with main business income, and deflated according to the producer price index for industrial products (“PPI”); K represents corporate capital input that is expressed with net value of corporate fixed assets, and deflated with reference to the investment price index of fixed assets; L refers to corporate labor input expressed with gross payroll and deflated on the basis of CPI; M is corporate intermediate input expressed with cashes used for goods purchase and labor cost, and deflated according to the producer purchase price index for industrial products. Furthermore, i is enterprises, j is the sector, and t is the time or year. For all nominal variables, the year 2007 is seen as the base period of the deflation index that are sourced from National Bureau of Statistics (“NBS”).

(3) Control variable. In this paper, the relevant influencing elements for the corporate total factor productivity are controlled with reference to existing literature documents. As for enterprises, they consist of: return of assets (roa), business scale (scale), ownership structure (top1), debt-to-asset ratio (debt), company age (age), Tobin value Q (Tb_Q), corporate fixed asset ratio (F_A); As far as industry’s concerned, concentration ratio (hhi) is controlled; and from the perspective of locality, the level of local financial development (fin) is controlled in this paper.

In the following Table 1 are listed the detailed definitions and descriptive statistical results.

Variables Definitions and Descriptive Statistics.

The related pearson tests are made for main explanatory variables in the paper to ascertain whether or not there is multicollinearity among variables. As indicated in Table 2, most of correlation coefficients among main explanatory variables are lower than 0.3, which discloses that no serious multicollinearity problem happen to explanatory variables. Therefore, these variables could be used as explanatory variables for regression analysis.

Matrix of Pearson Correlation Coefficient for Main Variables.

Empirical Analysis

Basic Regression

The following model is designed to verify impacts of enterprise financialization on total factor productivity:

in which, dependent variable lntfp is the corporate total factor productivity, kernel explanatory variable far stands for the level of enterprise financialization, X represents the group of foregoing enterprise control variables related to total factor productivity (including shareholding ratio held by the first majority shareholder (top1), return on assets (roa), business scale (scale), debt-to-asset ratio (debt), company age (age), Tobin value Q (Tb_Q), and corporate fixed asset ratio (F_A)), fin refers to the level of financial development in local cities where enterprises are located, hhi is the concentration ratio of the industry, µ

i

is the individual effect of enterprises,

First of all, this paper examines impacts of enterprise financialization on total factor productivity, with empirical results listed in Table 3. In Column (1), only the company-year two-way fixed effects is controlled during regression to check immediate impacts of enterprise financialization on total factor productivity, with no other control variable added. The result shows that due to enterprise financialization, total factor productivity declines and appears significant at the statistical level 1%. Even if the control variable is added into Column (2), the regression coefficient still significantly remains minus at the statistical level 1%. In the economic sense, enterprise financialization that goes up by one standard deviation every time could lower down total factor productivity by 1.7 (0.200 × 0.084). Meanwhile, in consideration of heterogeneity caused by the property of corporate ownership, this paper respectively examines samples of state-owned enterprises and non-state-owned ones. Judging from Columns (3) and (4) in Table 3, total factor productivity of both state-owned enterprises and non-state-owned ones are significantly reduced by enterprise financialization. On top of this, the dummy variable soe is set up for corporate ownership. If manufacturing enterprises are owned by the state, the soe value is 1; otherwise, soe = 0. As expressed in Column (5), the interaction term is incorporated for the level of enterprise financialization and the dummy variable soe for corporate ownership, but the interaction term coefficient doesn’t appear significant, which symbolizes no obvious difference in impacts of financialization on state-owned enterprises and non-state-owned ones.In column (6), this paper adds an interaction term between firm financialization and firm scale into the empirical model to further investigate the impact of firm scale on the relationship between firm financialization and total factor productivity.The result shows that the interaction coefficient is significantly negative, indicating that the financialization of large enterprises has a more significant negative impact on total factor productivity than that of small enterprises.The reason is that large-scale enterprises are generally less constrained by financing, and investment in financial assets is mainly for the purpose of arbitrage, thus crowding out productive investment of enterprises.

Impacts of Enterprise Financialization on Total Factor Productivity.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

Robustness Testing

As indicated in Table 4, several groups of robustness testing are further carried out to the benchmark model. In Column (1), the fixed effects model is used to estimate total factor productivity of enterprises. Column (2) shows that before testing, those enterprises that went public after 2007 are eliminated for the sake of impacts of newly-listed enterprises in the sample period. In Column (3), the financial earnings ratio is used to measure the level of enterprise financialization. Column (4) shows that those enterprises with no financial asset are eliminated, and that only financialized enterprises are taken as samples to observe whether or not the results are more significant than regression results of the full sample. Column (5) chooses current values for explanatory variables. It is elicited from results in Table 4 that the benchmark model in this paper generates robust results, that is, enterprise financialization has significantly held back the improvement in total factor productivity.

Robustness Testing.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

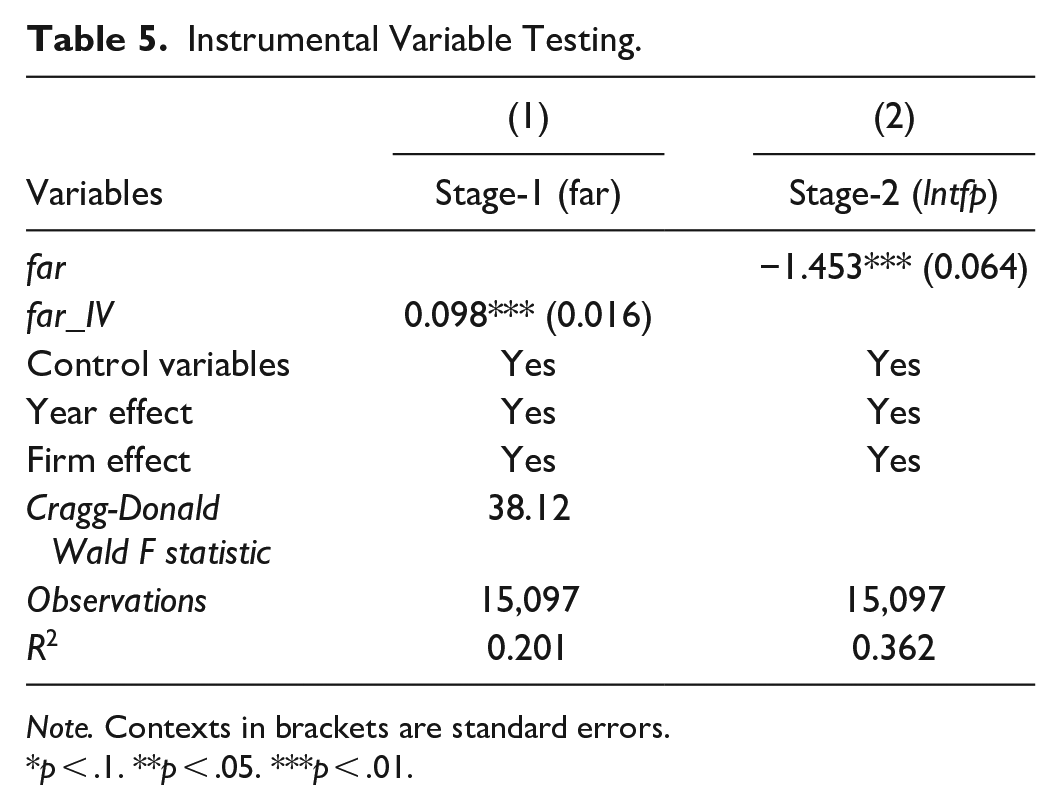

Regression of Instrumental Variables

The abovementioned results have testified the correlation between enterprise financialization and total factor productivity; notwithstanding, the endogeneity problem of reverse causality may be caused by financial asset investment that enterprises with low efficiency is likely to proactively made for the purpose of great returns. Therefore, the instrumental variables of financialization are introduced in this paper to minimize biased estimates. In this paper, the average financialization value of other enterprises in the same provinces and industries as sampled enterprises are used as instrumental variables (far_IV) to measure the financialization level of sampled enterprises. The average financialization value of other enterprises in the same provinces and industries as sampled enterprises is in connection with the financialization level of sampled enterprises, but has no immediate impact on total factor productivity. Instrumental variables are in line with prerequisites on correlation and exclusiveness. In Table 5 are listed testing results of instrumental variables.

Instrumental Variable Testing.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

Column (1) reports the stage-1 regression results of 2SLS: the far_IV coefficient is positive and significant at the statistical level 1%. Cragg-Donald Wald F equals to 38.12, greater than the critical value of weak instrumental variable testing. It tells that instrumental variables are highly correlated with endogenous variables, with no problem of weak instrumental variables. Column (2) reflects the stage-2 regression results of 2SLS. It says enterprise financialization has significantly lowered down total factor productivity of enterprises, which demonstrates robust conclusion from the benchmark regression in this paper.

Difference-In-Differences Retesting for Impacts of Exogenous Events

Both benchmark regression and instrumental variable testing prove the robust results in this paper. With reference to Guidelines of Supervision on Public Enterprises No. 2—Requirements of Supervision on Enterprise’s Management and Use of Raised Funds (“the Guidelines”) promulgated by China Securities Regulatory Commission (“CSRC”) in 2012, a difference-in-differences model is designed to verify the conclusion in this paper, in order to lessen more biased estimates caused by endogeneity. As stipulated in this policy, public enterprises are allowed to allocate idle raised funds for investment products of high safety and liquidity, including fixed income products like national bonds, bank financial products and other investment products. As this policy was promulgated, public enterprises witnessed a remarkably rising level of financial asset investment after the year 2012. Despite that this policy has greatly affected the financial asset investment of state-owned enterprises, centrally-administered state-owned enterprises haven’t suffered bitterly. As early as in 2006, the State-owned Assets Supervision and Administration Commission of the State Council (“the SASAC”) promulgated Interim Measures for Supervision and Administration of Investments by Centrally-administered Enterprises. In accordance to this policy, more efforts shall be made to supervise other business investments of enterprises contributed by the SASAC (including non-main investments like real estate, finance, securities, and insurance), and centrally-administered state-owned enterprises shall report to the SASAC about their non-main business investments with rigid constraints over proportions of investments. Therefore, the Guidelines impose limited impacts on financial asset investment by centrally-administered state-owned enterprises rather than by locally-administered ones. In this paper, furthermore, samples of non-state-owned enterprises are not introduced into the development of the difference-in-differences model, for the reason that the State Council promulgated a number of policies around the year 2012 to support both the non-public sector of the economy and the development of micro, small and medium companies. A great number of policies together have made it difficult to discern impact of the Guidelines on total factor productivity of non-state-owned enterprises (The following policies play a significant role in advancement of development of non-state-owned enterprises: Opinions on Encouragement and Guidance of Healthy Development of Private Investments promulgated by the State Council on May 17, 2010, and Opinions on Further Supporting Healthy Development of Micro and Small Enterprises promulgated by the State Council in 2012).

In this paper, the time tendency diagram is depicted on total factor productivity of both locally-administered and centrally-administered state-owned enterprises to vividly unveil differences in total factor productivity of these two kinds of enterprises. As indicated in Figure 1, the total factor productivity of both two kinds of enterprises shows the time tendency that largely remained parallel before the Guidelines was released, with no obvious fluctuation. As the Guidelines was released, however, locally-administered state-owned enterprises witnessed the lower growth of total factor productivity than that of centrally-administered state-owned ones. Judging from the time tendency diagram on financialization of locally-administered and centrally-administered state-owned enterprises, both two kinds of enterprises experienced the stable financialization that takes on unobvious fluctuation. After the year 2012, both of them saw the ascending level of their financialization, with the higher financialization rate of locally-administered state-owned enterprises than that of centrally-administered state-owned ones.

Time tendency on total factor productivity and financialization of locally-administered and centrally-administered state-owned enterprises.

It is argued in this paper that the Guidelines will raise the enterprise financialization, but total factor productivity will drop afterwards. The grouping variable treat is set up on the basis of difference-in-differences ideas. Locally-administered state-owned enterprises are categorized into the experimental group (treat = 1), while centrally-administered state-owned enterprises fall into the control group (treat = 0). Meanwhile, the grouping variable of time after is set up according to the promulgation date of the Guidelines; if the year is 2012 or later, after = 1, and otherwise, after = 0. On top of this, in Requirements on Supervision and Administration of Guidance and Regulation for Financing by Public Enterprises promulgated by CSRC in 2017, it is provided for that where any public company other than the company in the financial sector applies for refinancing, it shall not hold a large sum of trading financial assets with a long term at the end of the latest period, and shall also not have such financial investments in the same period as available-for-sale financial assets, loans to others, and consigned financing, in order to shield its financial asset investment from restrictions. Therefore, the difference-in-differences regression period is from 2007 to 2016 for this paper. The difference-in-differences model is designed as follows:

i stands for an enterprise, t represents year, and X is a group of control variables. With the corporate individual effect µ and time effect

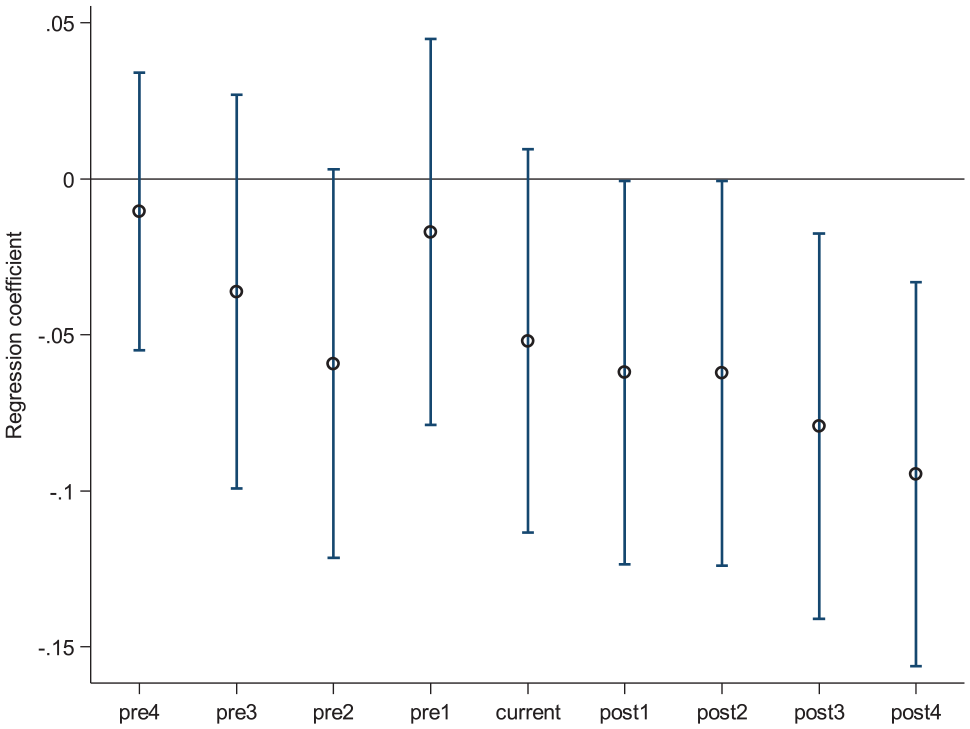

In Column (1) of Table 6, it shows that without any control variable added, the interaction term coefficient of treat and after appears minus and significant at the statistical level 1%. Column (2) demonstrates that even if such control variables as enterprise, industry, and locality features are added, the interaction term coefficient of treat and after still appears minus and significant at the statistical level 1%. According to results mentioned above, total factor productivity of locally-administered enterprises drops drastically after the Guidelines are promulgated. What’s more, it’s verified that impacts of the Guidelines have dynamic effects, treat × year2007 is the interaction term of treat and year2007, treat × year2008 is the interaction term of treat and year2008, and so on in a similar way. As disclosed in regression results in Columns (3) and (4), impacts of the Guidelines increasingly curbs total factor productivity of enterprises.Figure 2 completely shows the dynamic effect test of Guidelines on enterprise total factor productivity. It can be seen from the Figure 2 that treat × year2008, treat × year2009, treat × year2010, treat × year2011 and treat × year2012 are not significant.It indicates that there is no significant difference between the experimental group and the control group before the issuance of Guidelines, which meets the parallel trend hypothesis.

DID Testing Result.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

Dynamic effect test of CSRC guidelines on total factor productivity of enterprises.

In addition, the placebo test is adopted to identify real impacts of the Guidelines on total factor productivity of enterprises. In the model, the implementation year of this policy is respectively moved for 2 year forwards and backwards, that is to say, the year 2010 and 2014 respectively act as the virtual implementation year of the Guidelines. If the year is later than 2010 (2014), after = 1 and otherwise after = 0. As indicated in Columns (5) and (6) of Table 6, impacts of the Guidelines doesn’t greatly affect total factor productivity of enterprises if the year 2010 and 2014 act as the virtual implementation year of the Guidelines. Thus, the impacts of the Guidelines are proved to lower down total factor productivity of enterprises.

Following the demonstration that enterprise financialization significantly impedes total factor productivity, it is further to be testified that this consequence arises from the predominant “crowding-out” effect of enterprise financialization. These two kinds of effects are concerned with corporate productive investments that are expressed in this paper with corporate input into technical research and development (R&D) to further examine impacts of enterprise financialization on corporate input into technical research and development. The positive coefficient symbolizes the predominant “reservoir” effect of enterprise financialization, and otherwise, it signifies that the “crowding-out” effect overshadows the other.

As implied from regression results in Table 7, the rising level of enterprise financialization has significantly lessened corporate inputs into technical research and development. Judging from foregoing empirical results, Hypothesis 1b is current; in other words, enterprise financialization has the predominant “crowding-out” effect, and thus, he rising level of enterprise financialization has suppressed the increase in total factor productivity.

Impacts of Enterprise Financialization on Corporate Input into Technical Research and Development.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

Testing for Moderating Effect of Product Market Competition on Relationships Between Financialization and Total Factor Productivity

According to the research hypothesis in this paper, impacts of enterprise financialization on total factor productivity may vary with different extents of product market competition zones, as the external market competition environment may affect investment choices of enterprises. As a result, the enterprise’s motive in financialization may be adjusted to different extents of product market competition. To eliminate the possibility that the endogeneity problem strikes grouping variables of product market competition, this paper is not based on the analysis method that the benchmark regression is combined with such cross variables as product market competition and enterprise financialization; instead, the panel threshold model of fixed effects is adopted in this paper to examine impacts of enterprise financialization on total factor productivity in different regions of product market competition. Besides, Herfindahl-Hirschman Index (hhi) is used to measure intensity of product market competition. The higher index symbolizes product market competition at a lower level, and otherwise, it refers to more furious product market competition. A model is designed as below with fierceness of product market competition as its threshold variable:

in which, I (·) is the indicator function: when the expression in the bracket is grounded, the value of I (·) is 1, and otherwise, it is 0. hhi is the threshold variable, and

Before estimating the panel threshold, it is required to check whether or not there is a threshold value. In this paper, the statistical value F is obtained after the model estimation at 0 threshold, 1 threshold, and 2 thresholds. Furthermore, Bootstrap sampling is applied to calculate the threshold value for intensity of product market competition (see in Table 8). The single-threshold testing is carried out to ascertain the former hypothesis that the statistical value F rejects “0 threshold” at the statistic level 10%, while the dual-threshold testing is carried out to ascertain the former hypothesis that the statistical value F accepts “1 threshold.” It’s elicited that enterprise financialization only imposes on total factor productivity the threshold effect for intensity of single product market competition, with the threshold value 0.0327.

Testing for Threshold Effect in Product Market Competition of Enterprise Financialization on Total Factor Productivity.

Note. Both p-value and the critical value are obtained after Bootstrap-based simulation for 200 times.

Table 9 reports the regression results about the testing for threshold effects in product market competition of enterprise financialization on total factor productivity. If the intensity of product market competition is below the threshold value, enterprise financialization boosts total factor productivity, but appears insignificant statistically; when the intensity of product market competition goes beyond the threshold value, enterprise financialization significantly holds back total factor productivity. Consequently, the fierce product market competition could significantly impair negative effects of financialization on total factor productivity of enterprises, which supports Hypothesis 2a in this paper.

Threshold Effect in Product Market Competition of Enterprise Financialization on Total Factor Productivity.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

According to the theoretical analysis, threshold effects in product market competition of enterprise financialization on total factor productivity mainly stem from product market competition that moderates the “reservoir” effect and “crowding-out” effect of enterprise financialization. As proposed in the “escape competition effect” hypothesis and the “bankruptcy threat effect” hypothesis, the intensified product market competition will strengthen the “reservoir” effect but impair the “crowding-out” effect. In this paper, corporate inputs into technical research and development (R&D) are still used as the indicator of corporate productive investments for further examination about impacts of enterprise financialization on R&D inputs at different degrees of product market competition. Likewise, the positive coefficient symbolizes the predominant “reservoir” effect of enterprise financialization; otherwise, the “crowding-out” effect overshadows the other. The panel threshold model of fixed effects is still adopted:

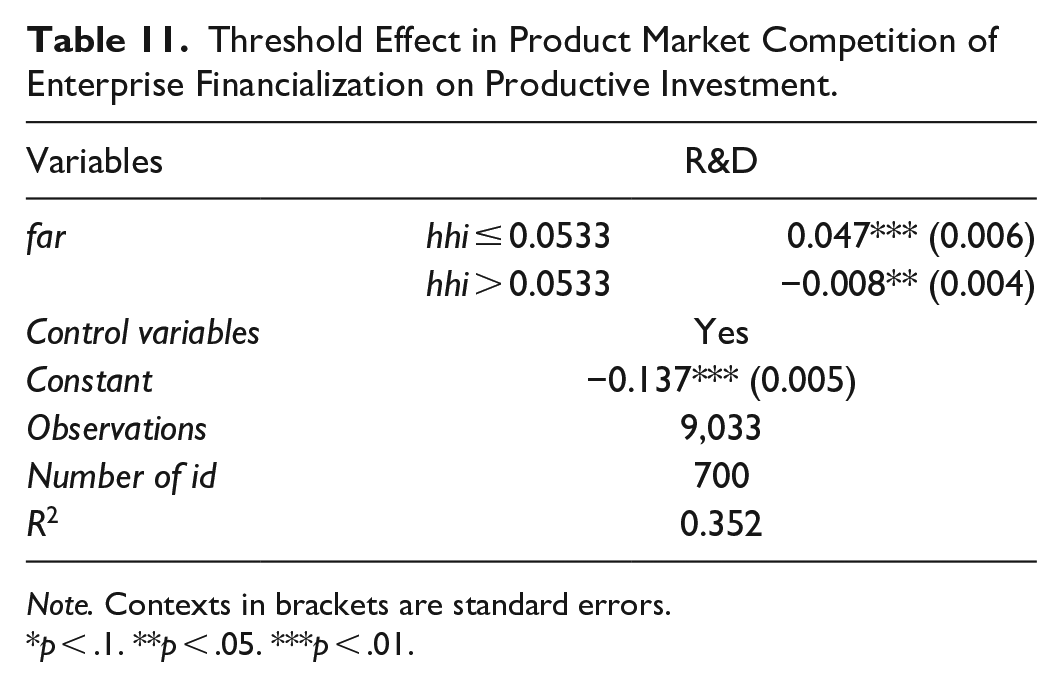

in which the variables other than R&D are the same as mentioned in previous paragraphs, while R&D represents the percentage of R&D inputs in main business revenues. Table 10 shows the same testing steps that are taken. After Bootstrap-based testing and threshold value estimation, it is found that financialization imposes on R&D inputs the single-threshold effect of product market competition.

Testing for Threshold Effect in Product Market Competition of Enterprise Financialization on Productive Investment.

Note. Both p-value and the critical value are obtained after Bootstrap-based simulation for 200 times.

According to parameter estimation results in Table 11, enterprise financialization could significantly stimulate more investments into technical research and development if financialization is in the region of high-level product market competition (hhi ≤ 0.0533), while enterprise financialization could drastically impede technical R&D inputs if financialization is in the region of low-level product market competition (hhi > 0.0533). When the level of financialization is very low, enterprises are constrained by financing, resulting in insufficient investment in productivity. In the context of fierce market competition, enterprises have a strong incentive to invest in productivity in order to obtain monopoly rents.Financialization of enterprises can not only satisfy the investment needs of enterprises by exerting the “reservoir effect,” but also obtain credit funds from banks by virtue of the high liquidity of financial assets to relieve the financing constraints of enterprises. At this point, financialization promotes productivity investment.With the gradual increase in the level of financialization, the increase in monopoly rents caused by the relaxation of financing constraints has greatly increased the investment of enterprises.The productivity gap between enterprises keeps widening and the degree of market competition starts to decrease. As a result, both the leading enterprises and the backward enterprises are not motivated to invest in productivity. At this time, the financialization of enterprises squeezes out the productivity investment.This result verifies the fact that on the part of enterprise financialization, the intensified product market competition strengthens its “reservoir” effect but impairs the “crowding-out” effect. To sum up, Hypothesis 2b in this paper is tenable.

Threshold Effect in Product Market Competition of Enterprise Financialization on Productive Investment.

Note. Contexts in brackets are standard errors.

p < .1. **p < .05. ***p < .01.

Discussion

This paper mainly focuses on impacts of non-financial enterprise financialization upon total factor productivity of enterprises, as it examines the impact mechanism of non-financial enterprise financialization upon total factor productivity. It is elicited that the rising level of non-financial enterprise financialization significantly lowers down total factor productivity of enterprises, and furthermore, the decrease in productivity mainly arises from technical innovation investments that are “crowded out” by non-financial enterprise financialization. This finding basically matches up with viewpoints proposed by Bellocchi et al. (2020), Stockhammer (2004), and Campling (2020), Aalbers (2008), Lashitew (2017), and Rico and Cabrer-Borras (2020). As for those conclusions in some studies contained in literature documents regarding micro enterprise financialization, they appear contradictory with the conclusion in this paper, for they indicate that the increase in corporate productivity could stem from corporate investments in R&D, innovation and real business that are stimulated by corporate allocation of financial assets for the purpose of great returns and alleviated financing constraints (Akbar et al., 2017; Mannasoo et al., 2018; Nasir et al., 2021; Thomas et al., 2015). According to the paper, endogeneity is the main reason why no consensus about impacts of enterprise financialization has yet been reached in the academic community. After the relationship between enterprise financialization and total factor productivity is examined in this paper with the help of the instrumental variable method and the difference-in-differences model developed through exogenous policies promulgated by China Securities Regulatory Commission in 2012, it is elicited from examination results that the benchmark regression results are robust. In addition, another explanation also works, that is, in the theoretical sense, the corporate allocation of financial assets is endowed with both the “reservoir” effect and the “crowding-out” effect, though these two kinds of effects show different extents in different circumstances. Eventually, this paper has got the conclusion that the enterprise financialization significantly imposes negative net impacts on total factor productivity; in other words, the “crowding-out” effect is predominant and overshadows the “reservoir” effect, which means the rising financialization level could hold back the increase in total factor productivity.

What’s more, those factors that affect two kinds of effects mentioned above are taken into account in this paper. Both internal and external environment in which enterprises are situated could affect corporate investments. On the basis of product market competition that projects the external governance environment, the paper examines changes in these two kinds of effects at different levels of product market competition. With the moderating variable—product market competition incorporated in this paper, the intensified product market competition is found to effectively weakens the function of enterprise financialization that suppresses total factor productivity by strengthening the “reservoir” effect. This conclusion supports the “bankruptcy liquidation threat” hypothesis and the “escape competition effect” hypothesis regarding market competition, that is to say, those enterprises that face with the intensified external competition will, more often not, seek for competitive strength via the development of new products and more inputs into technical innovation. (Bonfatti & Pisano, 2020).

This paper eclectically puts forth a model that comprises these two kinds of financialization effects, and is combined with the moderating variable—product market competition to empirically prove that the intensified product market competition could effectively enhance the “reservoir effect” of financialization to overturn the predominant “crowding-out” effect. As a result, it conveys a new theoretical viewpoint for researches in this field. It is elicited from the conclusion that the intensified product market competition could effectively mitigate negative impacts of financialization upon total factor productivity. In the practical sense, therefore, this paper has the argument that in the circumstance of economic financialization, tremendous efforts must be made to create the fair and open environment of product market competition, and continuously improve the favorable mechanism of market competition, so as to break barriers of market segmentation and monopoly for the purpose of a real critical role of markets in resource allocation. To drive funds to move backward entities, the solutions shall be made to settle financing problems that the real economy is facing; on the other hand, it’s imperative to solve the problem that profits of the virtual economy drop away from those of the real economy. To do so, we must work harder to make policies on cutting more taxes and fees, reduces corporate costs of production and business, and improve profitability of the real economy and its abilities of sustainable development, as we advance the reform in the financial system, and better align the financial structure, in order to push forward the establishment of the multi-tiered financial institution system for diverse financing demands from the real economy.

Despite that existing literature documents sufficiently probe in impacts of enterprise financialization, further efforts could be made in following aspects: first, this paper discusses impacts of enterprise financialization on its total factor productivity, but enterprise financialization, in fact, is one of resource allocation ways that enterprises adopt largely for capital operation. On the whole, it will result in resource reallocation on markets, and in turn, the resource allocation efficiency could be further used to get deeper insights about impacts of enterprise financialization on the overall productivity of the manufacturing sector. Second, we deeply recognize subjective motives of enterprises in financial asset investment, and take differentiated and applicable measures for investments from different motives, in order to drive capitals to move backward entities for the increase in efficiency of financial services to the real economy.

Conclusion

In recent years, the manufacturing sector has suffered from great impacts on its productivity, as manufacturing enterprises witness their financialization level raised by increasing investments of China’s enterprises in financial assets. In this paper, the data about China’s A-share public manufacturing enterprises are used to empirically examine impacts of enterprise financialization on total factor productivity. Also, the moderating variable—product market competition is introduced to observe impacts of product market competition environment upon the relationship between enterprise financialization and total factor productivity. As a result, it is found that enterprise financialization is largely based on the “crowding-out” effect, that is, the rising financialization level significantly curbs the growth of total factor productivity. As product market competition intensifies, enterprise financialization imposes weakened suppression on total factor productivity when the “reservoir” effect of enterprise financialization is enhanced.

As far as the policy’s concerned, the following connotations could be elicited from the conclusion in this paper: first, in the theoretical sense, enterprise financialization contains both positive and negative effects—”reservoir” effect and “crowding-out” effect, the latter of which is proved to overshadow the former one. According to this study, the rising intensity of product market competition could effectively enhance the positive effect of financialization to overturn the predominant “crowding-out” effect. Therefore, more efforts must be made to create the fair and open environment of product market competition, and establish a favorable mechanism of market competition, in order to break barriers of market segmentation and monopoly for the purpose of the critical role of market in resource allocation. Second, the excessive enterprise financialization largely stems from higher returns on financial assets than real investment. Therefore, before driving finance to move “from the virtual to the real,” it’s imperative to solve the problem that the profit rate of virtual economy drops away from that of real economy. To do so, applicable policies shall be made to cut more taxes and fees, lower down enterprises’ costs of production and business, and raise profitability and sustainable development ability of real economy.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The National Social Science Fund Project “Resource Allocation Effect of Financial Virtualization” and Financial Policy Optimization Research of “Escape from Virtual to Real” (No. 18BJL076).