Abstract

The technology acceptance model (TAM) has been regarded as a promising model for understanding technology adoption and can be extended to different situations. Currently, mobile payment services have been widely applied in people’s daily lives in China, and understanding their critical success factors is becoming important. Mobile payments are a complex system, and a large number of factors affect their success. Since mobile payments are directly related to financial issues, their wide adoption relies heavily on people’s trust. We developed a model based on the TAM to investigate the most influential factors in building trust within the mobile payment context. We conducted an empirical survey and 373 samples were collected using a valid questionnaire from the users of the popular payment platforms in China—Alipay and WeChat payment. We found that government monitoring is the most significant factor of customer trust, followed by reputation, and security. Government monitoring directly influenced behavioral intention, was negatively associated with perceived risk and positively affected behavioral intention. Moreover, mobility, subjective norms, usefulness, ease of use, and perceived enjoyment impacts customer behavioral intention.

Introduction

The advent of mobile payment (m-payment) has become popular in China and has enabled the customer to complete various transactions regardless of time and place, compared with the conventional way of payment (Liébana-Cabanillas et al., 2017; Qasim & Abu-Shanab, 2016). Mobile payment is a core driver for mobile commerce (Yang et al., 2012). It is also a tool used to effect payments for services, goods, bills, and helps with other communication (Dahlberg et al., 2008). Mobile payment is a technical innovation, which represents a traditional method of payment, and it is defined as “any payment where a mobile device is used to initiate, authorize, and confirm an exchange of financial value in return for goods and services” (Au & Kauffman, 2008; Kim, 2010). The ultimate goal of m-payment is to master the time and place of the traditional payment and cash-centric payment (Katawetawaraks & Wang, 2011). Specifically, Chinese mobile payment services benefit from third-party payment platforms, such as Alipay and WeChat pay (Huang, 2017; Katawetawaraks & Wang, 2011).

The advent of new innovation technology has increased the need for formulating a new regulation and policies framework. These policies include direct research and development funding, agency level research policy, and research and development tax credits (Wan & Ali, 2013). Without government law and policies, the abuse and discouragement toward adopting new technology innovation in organizations will be high, and many studies have confirmed that the government, through regulation, can encourage technological innovation adoption and use (Al Nahian Riyadh et al., 2009; Wan & Ali, 2013).

WeChat pay and Alipay have become the primary methods of payment in China, not only in big cities but also in rural areas. A survey found that 92% of the people preferred using mobile phones to make payments (UnionPay, 2017). The iResearch assessed that WeChat pay commands 40% of the market, compared to 54% for Alipay (UnionPay, 2017). The sustainable growth of the mobile payment market brings up an important question: what are the antecedents that encourage continued use of mobile payment by customers? Previous studies have found that trust is the most important antecedent that motivates customers to use mobile payments in different situations (Huang et al., 2014; Köster et al., 2016; Liébana-Cabanillas et al., 2014). Perceived risk hinders customers from using mobile payment platforms (IResearch, 2017; Liébana-Cabanillas et al., 2017; Oliveira et al., 2017). Many studies have found that customers’ trust in the service provider will enhance the continued use of mobile payments and decrease perceived risk (Qasim & Abu-Shanab, 2016).

The widespread use of mobiles (Yang et al., 2012) makes m-payment popular (Huang, 2017). The full use of smartphones, and extensive use of m-payment in China raises a critical question: what factors drive customers to trust mobile payment services in China? It has been proved by numerous studies that trust is the most critical factor that motivates customers to accept mobile payment in various situations. Perceived trust has been widely investigated with regard to other elements in the field of mobile payment as well as with other factors, such as perceived security, which represents customer reliability on the institution’s ability to protect their m-payment (Kow et al., 2017; Nijssen et al., 2016; Xin et al., 2015; Zhang, 2019). Perceived usefulness and perceived ease of use play a vital role in forming online trust (Chellappa, 2008; Nijssen et al., 2016; Qu et al., 2018). Moreover, mobility and reputation directly influence users’ trust in mobile payment usage intention (Alshare & Mousa, 2014; Gerhardt et al., 2010; Ittner et al., 2004; Kim, 2016; Luo et al., 2014). In the current study, the authors investigated the antecedents of China’s government monitoring in combination with trust.

Trust can be regarded from different perspectives, that is, trust in the government (McKnight et al., 2002; Turban & Lee, 2001), trust in involved companies (Huang et al., 2014), trust in social peers (Zhang et al., 2017), trust in technique, reputation, mobility (Zhou, 2014), enjoyment (Chong, 2013), perceived usefulness, and ease of use. Thus, trust is an essential issue in m-payment and building trust in the third-party platform has become critical in the continuity of m-payment services (Zhang, 2019).

Prior studies focused on mobile payment acceptance and mainly researched the motivation for customers to use m-payment. These studies were conducted by applying the technology acceptance model (TAM) (Gerhardt et al., 2010; Kalinic & Marinkovic, 2017; Kim et al., 2009; Qu et al., 2018). From the above argument, one question emerges: if trust is considered a significant factor in mobile payment, what should service providers do to enhance trust in the m-payment platform? What is the reason behind the success of mobile payment services in China?

This study is motivated by numerous factors. Our study addresses the gaps in prior studies by investigating the government monitor role within mobile payment sectors as an antecedent of trust that leads to behavioral intention. To the best of our knowledge, no previous study has been conducted to investigate the role of government within the mobile payment context. Second, it specifies the most influential factors in constructing trust within the mobile payment context based on the trust forming factors from previous studies with additional new factors such as reputation and mobility (Zhang, 2019). Third, the study aims to investigate the effect of government monitoring in building trust within the mobile payment context in China.

Furthermore, this research is expected to enrich and extend the literature review in the field of mobile payment because it discusses the most prevalent factors in the area of m-payment. The TAM was applied to achieve the aims of this research. Some additional factors were assumed, such as mobility, subjective norms, perceived risk, perceived enjoyment, and behavioral intention. Finally, the expected findings of this research can enhance the current literature and introduce new insights for the development of m-payment services.

This paper is organized as follows: Section 2 presents trust in mobile payment and the background of the TAM. Section 3 constructs the research model and proposes the relationship among the factors. Section 4 elaborates on the research methods and discusses the statistical analyses results. We conclude the research with findings, discussion, recommendations, and future research directions in Section 5.

Related Work

The Nature of Trust in Mobile Payment Service

Trust in the psychological context is considered a belief that the other party will act according to the particular behavior of generosity, honesty, and ability (Gefen, 2000; Zhou, 2014). Trust is considered to be faith in the predictability of a certain reaction (Luhmann, 1979). According to Mayer et al. (1995), trust arises between two groups who act consciously with altruism. McKnight et al. (2002). conducted a study to investigate the critical factors that influence people’s trust building and subsequent behavior. The investigation revealed that reputation, site quality, and structural assurance are essential in encouraging people’s trust and intention in e-commerce. Their framework has been applied to mobile and e-commerce by a number of authors (Corbitt et al., 2003; Huang et al., 2014; Qu et al., 2018; Teo & Liu, 2007). During the last 6 years, many researchers have focused on building trust mechanisms in mobile payment platforms by developing effective technical features and institutional mechanisms (Fan et al., 2018; Köster et al., 2016; Nguyen & Yao, 2018; Oliveira et al., 2017; Qasim & Abu-Shanab, 2016; Zhou, 2013). Technical features have been found to be important factors in building users’ trust in mobile payment platforms (Dahlberg et al., 2015). Customers depend on third-party reputation to settle the transaction and on the technical features of the platform, such as convenience and flexibility.

Technology Acceptance Model (TAM)

The TAM is the most influential model and is commonly used for measuring factors influencing the adaptation of information technology (Davis et al., 1989). It was developed from the theory of reasoned action (Ajzen & Fishbein, 1980) and investigates the factors that influence customer decision to use a specific technology (Wu & Wang, 2005). The TAM model suggests that the user’s determinant of using the information system is driven by two factors: perceived usefulness and perceived ease of use. Perceived usefulness is defined as “the degree to which an individual believes that using a particular system will enhance user’s job performance” and perceived ease of use is defined as the “degree to which an individual believes that using a particular system will be free of effort (Davis et al., 1989). These attitudes drive intention to use with respect to information technology systems.

The technology acceptance model (TAM) is a very successful model in examining factors influencing the usage of information technology systems; numerous studies have been conducted in the field of mobile payments by applying TAM such as (Amoroso & Magnier-Watanabe, 2012; Fan et al., 2018; Jeong & Yoon, 2013; Qu et al., 2018; Shaw, 2014). The TAM was gradually refined, and different factors were added to the original model, such as behavioral intention (Davis et al., 1989). Owing to the capability of TAM to predict and explain information technology system acceptance, this research believes that the TAM is suitable for analyzing customers’ trust in the use of m-payment.

Theoretical Model and Research Hypotheses

Alipay and Wechat Payment are the most influential mobile payment services in China 92% of the users choose mobile payment such as WeChat Pay as their primary offline payment tools (NFC World, 2017). Almost all public services, for example, transportation, retail services, and etc. accept mobile payment (Korella & Bundesbank, 2017). Nowadays it is not uncommon that some Chinese people have not used cash for more than 1 year or even longer. It is interesting to study how and why mobile payment service is becoming that popular in China.

To achieve the objectives of the current research, we extend the TAM by investigating the most reputable factors in the field. The TAM framework is used to test critical factors that affect the adoption of mobile payment by users. Moreover, the study investigates the role of government monitoring in the model, which, to the best of our knowledge, has not been previously examined to describe trust, and behavioral intention in mobile payment.

Studies on m-payment systems have analyzed different factors, drawing various conclusions. The current research attempts to build a trust model from the most common factors in the field of IT adoption, and notably, investigates the role of government as a new factor in the adoption of m-payment. Perceived usefulness and ease of use have been confirmed in many studies as determinants of m-payment service adoption (Lu et al., 2005). Security has been found to be a crucial factor in forming trust during online transactions (Chellappa, 2008). Li et al. (2008) confirmed that reputation is a critical factor affecting initial trust, as it may decrease the degree of uncertainty and risks related to online issues. Trust directly and indirectly affects users’ behavioral intentions (Ajzen, 1991). Mobility has been certified as one of the most important factors that influences perceived usefulness, ease of use, users’ attitude, and behavioral intention (Gerhardt et al., 2010). Rios and Riquelme (2010) found that subjective norms were a critical factor influencing customers’ acceptance of m-banking services. Perceived enjoyment, an intrinsic motivator, plays an important role in computer usage (Wang et al., 2012).

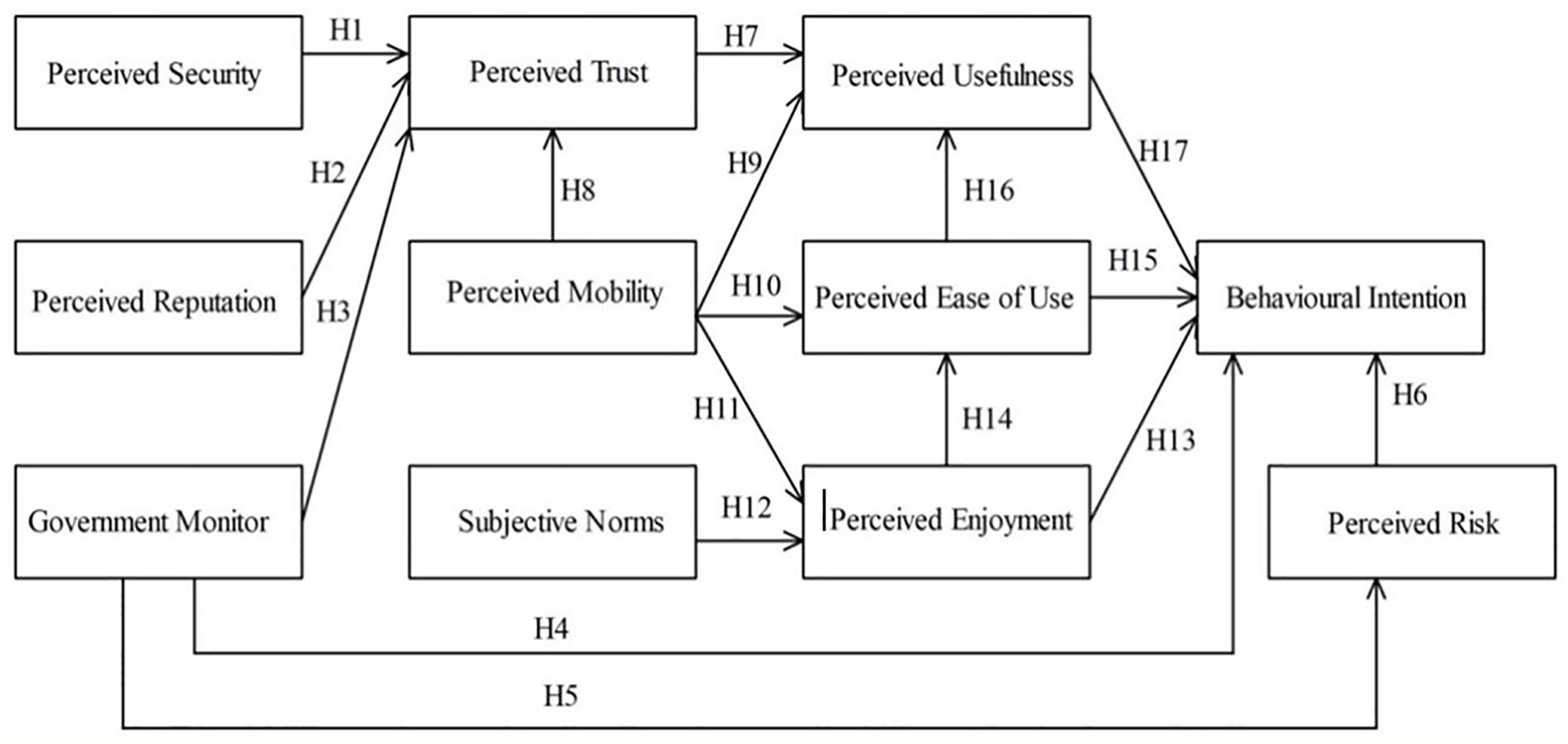

The proposed extended framework based on TAM was applied to investigate the possible influencing factors toward trust aware m-payment adoption in China, as shown in Figure 1, in which the factors are studied from the following perspectives: conventional TAM, perceived security, perceived reputation, government monitor role, perceived trust, perceived mobility, perceived subjective norms, perceived enjoyment, perceived ease of use, perceived usefulness, perceived risk, and behavioral intention.

The proposed model.

Perceived Security

Security is the capability of the website to protect user information from any suspicious sources during electronic transactions (Guo et al., 2012). Security, privacy, and confidentiality of information are recurring topics in a variety of projects. When sensitive information stored in wireless handheld devices or computers is lost or stolen this could create a breach of privacy (O’Donnell & Jackson, 2007). Security and privacy subjects emerge through the system’s ability to track people’s location through personally collected data (O’Donnell & Jackson, 2007). Security is found to be a crucial factor for online customers (Eid, 2011). Security plays a vital role in forming trust during online transactions (Chellappa, 2008). It is also found to be a critical success factor in online shopping in the Serbian market (Vasic et al., 2019). Security is an important factor for e-commerce sustainability and an influential factor for customers’ intention to use mobile payments (Friedman et al., 2000; Shaw, 2014). In the mobile payment context, it represents the user’s conception of safety and reliability of the institutional structures (Zhou, 2014). Therefore, ensuring high-quality security reduces uncertainty and transactional risk in a third-party platform (Xin et al., 2015) and can also promote mobile trust-building (Zhou, 2014). Based on that previous argument, we propose the following hypotheses:

Perceived Reputation

Initial trust is considered the most significant factor in building trust. When a customer makes the first purchase, the customer will make the first consumption only when initial trust is present (Kim, 2012; Luo et al., 2014; Zhou, 2014). Three factors are responsible for building initial trust: the first factor is related to website characteristics, website quality (Lin, 2011), information quality (Nicolaou & McKnight, 2006), and usability (Zhou, 2014). The second is associated with the service provider; reputation is a critical factor affecting initial trust, as it may decrease the degree of uncertainty and risks related to online issues (Li et al., 2008). The third factor is related to users.

Individual perception can be affected by the service provider’s reputation (Kim & Prabhakar, 2004). According to prior studies (Kim, 2012; Kim et al., 2009; Zhang, 2019), reputation is a critical success factor for firms. When the service provider has a reputation of being trustworthy, they benefit from their investment (Huang et al., 2014). In the studies conducted (Nicolaou & McKnight, 2006; Purohit & Srivastava, 2001), the result found that reputation was a strong predictor of perceived risk. Moreover, reputable service providers attract more transactions (Grazioli & Jarvenpaa, 2000; Teo & Liu, 2007), and providers with a bad reputation will lose transactions from capable customers (Ba, 2001). In the mobile payment context, the critical role of platform reputation in providing consumers’ trust was indicated. China’s m-payment systems are facilitated through two great platforms, WeChat payment and Alipay, which have an outstanding reputation among Chinese customers. Since reputation is a significant factor in building initial trust, we added to it our study factors. Drawing from the above argument, we defined the following hypotheses:

Perceived Trust

Trust is defined as a psychological expectation state of being a trusted partner that will not be opportunistic (Bunduchi, 2005). Trust is also described as a service provider’s obligation and the ability to meet customers’ expectations. This is a critical factor because it can reduce the uncertainty of fear and worry about using the service (Lu et al., 2011). Trust affects users’ behavioral intention, according to the theory of planned behavior (Ajzen, 1991). Trust has shown a direct relationship with willingness to buy online from Internet vendors (Kim, 2012; Kim et al., 2009). Moreover, trust has been combined with TAM to investigate m-payment users’ behavior (Zhou, 2014). The study (Shin, 2009) found that customer adoption of m-payment is influenced by perceived usefulness, perceived ease of use, perceived risk, and trust.

Perceived risk is defined as “the citizen’s subjective expectation of suffering a loss in pursuit of a desired outcome” (Warkentin et al., 2002). Perceived risk and trust are considered significant factors in e-commerce (McKnight et al., 2002; Teo & Liu, 2007) and m-commerce (Lu et al., 2011; Luo et al., 2014). It is also specified as a factor preventing the customer from continuous intentional usage within the mobile payment context (Yang et al., 2015). When risk exists, trust is compulsory (Corritore et al., 2003; Warkentin et al., 2002). When trust appears, risk disappears (Grazioli & Jarvenpaa, 2000; Salam et al., 2003; Warkentin et al., 2002). Customers’ intention toward sustained use of mobile payment services will increase when customers trust the system (McKnight et al., 2002). Additionally, trust is found to be a significant factor in perceived risk (Warkentin et al., 2002). Many studies, such as (Katawetawaraks & Wang, 2011; Luo et al., 2014; Teo & Liu, 2007; Warkentin et al., 2002) pointed out that perceived risk is a mediator that influences trust and intention.

Kim et al. (2010). suggested that individual differences and system characteristics affect users’ intentions through perceived ease of use and perceived usefulness. Zhou (2013) confirms that if vendors trust mobile payment services, this will lead to the intention of using the service.

Trust is essential within traditional web payment and m-payment services; it has been investigated in combination with other antecedents in several studies in the Western context (Köster et al., 2016; Liébana-Cabanillas et al., 2017; Nguyen & Yao, 2018; Oliveira et al., 2017; Qasim & Abu-Shanab, 2016). In them, trust arises from institutional structures that have been well developed in the Western market (Huang et al., 2014). While China is not well developed in terms of credit card usage compared with Western countries, trust plays a prominent role in encouraging customers’ transaction behavior (Huang et al., 2014). In this paper, we consider trust from the Chinese perspective. To discuss Chinese institutional trust, we need to mention government trust.

Government trust, in general, refers to “perceptions regarding the integrity and ability of the agency providing the service” (Mayer et al., 1995; McKnight et al., 2002; Turban & Lee, 2001). It can be considered as initial trust as people’s confidence in the capability of the service provider is essential for the wide use of e-government initiatives (Bélanger & Carter, 2008). Trust in a company as a service provider has a high influence on the adoption of technology (Gefen et al., 2005). The citizen must be sure that government agencies can process managerial and technical resources to implement a secure system before e-government initiatives are trusted (Bélanger & Carter, 2008; Gefen, 2000).

Reportedly, Chinese citizens have strong trust in the government (Nathan, 2017; Wu & Wang, 2005), both local and central (Nathan, 2017). According to Wu and Wang (2005), Chinese citizens have the highest level of confidence among the 27 countries in the World Values Survey. In another study (Kim, 2016), out of 26 countries, China ranked fifth in terms of highest public confidence in the government. The success of Alipay and WeChat pay comes from citizens’ trust in the government. China’s government has created a series of policies boosting and encouraging e-commerce and enterprises (Liu, 2015), and at the same time, focusing on monitoring and supervision in cyberspace. The government monitoring led to the success of e-commerce due to people’s trust in the government, that is, this trust created initial trust toward using a mobile payment system (Nishimura, 2020).

Additionally, Alipay and WeChat pay work positively and cooperatively with the government to improve and enhance the experience of public social services for Chinese citizens. This includes social contributions like ensuring security optimization and effectiveness of online payment systems, providing a variety of useful applications, and making investments in developing the economies of poor areas within China. All these activities enable Alipay and WeChat to gain a positive reputation and impression among Chinese citizens, who subsequently trust and commit to Alipay and WeChat pay. Furthermore, the third-party payments are expected to rapidly increase due to advances in innovation technology and government support (Liu, 2015).

Chinese people trust the government’s role and the advanced technology of Alipay and WeChat pay. This can be considered as initial trust and a positive reputation about the service provider will in turn affect the usage intention directly or indirectly (Liu, 2015; Zhong, 2014). Based on the above argument, we assume the following hypothesis:

Perceived Mobility

Mobility is defined as the relative advantage of the capability to use mobile payment regardless of place and time (Dahlberg et al., 2003). Obviously, mobility is the most remarkable characteristic of mobile commerce, which enables various m-payment services to be combined into one carry-on mobile terminal (Au & Kauffman, 2008; Dahlberg et al., 2008). Ittner et al. (2004). indicate that when m-payment users perceive a mobile platform that serves as a unique tool for payment services, they will trust it and use it continually. Mobility enhances consumers’ trust in mobile payment platforms (Zhou, 2014). Moreover, Yen and Wu (2016) verified that perceived mobility is one of the factors that influences continued usage intention in mobile financial services (MFS). Mobility has been certified as one of the most important factors that influence perceived usefulness, ease of use, users’ attitudes, and behavioral intention (Gerhardt et al., 2010). Early users of m-payment consider mobility as a necessary factor for the perceived ease of use, and it affects customers’ intention to use m-payment (Kim et al., 2010). Mobility enables mobile users to enjoy amusement through interaction with friends and financial services at any time and place (Hill & Roldan, 2005; Mallat et al., 2009). Based on the prior argument, we propose specific hypotheses.

Subjective Norms (SN)

Subjective norms are considered one of the influential factors that affect individual behavior. These refer to “individual perception of what most people who are important to one think of one’s behavior in question” (Hill et al., 1977). A subjective norm is an indicator of a person’s intentional behavior to use a certain service, and from a cultural viewpoint, trust and subjective norms were found to be strong predictors for users’ behavioral intentions (Atuahene-Gima & Li, 2002; Bagozzi et al., 2000; Gefen et al., 2003). Subjective norms were also found to be one of the critical factors influencing customers’ acceptance of m-banking services (Rios & Riquelme, 2010; Zhang et al., 2017). They were found to have a strong relationship with behavioral intention (Davis et al., 1989; Huang et al., 2020). Subjective norms were considered equivalent to social influence in perceived trust according to Lu et al. (2005). In a study conducted (Darmawan et al., 2010), peer influence, family, media, and television might affect people’s use of mobile commerce. Additionally, people’s behavior is affected by other factors such as peers; when users find that other people adopt instant messaging (IM), they will be more willing to use it (Lu et al., 2009). In the current study, perceived enjoyment mediated subjective norms and behavioral intention due to its influence on user intention. For example, when someone engages with their friends in social activities on the mobile payment application, the experience will affect his basic knowledge of the service, such as perceived enjoyment and perceived ease of use. The “new year red envelope promotion” is a typical practice in which friends use WeChat payments together. Moreover, “sharing coupons” is a similar activity where users can share coupons with their friends (Qu et al., 2018). Based on the above argument, we propose the following hypothesis:

Perceived Enjoyment

Perceived enjoyment is considered a new frontier in m-payment and a critical essential factor in social network services. Perceived enjoyment is defined as the extent to which an activity is perceived to be enjoyable without fear of untoward consequences (Davis et al., 1992). Perceived enjoyment, an intrinsic motivator, plays an important role in computer usage (Wang et al., 2012). Among the constructs discussed, perceived enjoyment is next to trust in terms of satisfaction and continued intention of e-commerce usage in the case of Chinese consumers (Chong, 2013). People tend to choose enjoyable services as a criterion among other services enjoyed (Qu et al., 2018). Moreover, perceived enjoyment positively influences people’s attitudes and intentions toward website adoption (Liébana-Cabanillas et al., 2017; van der Heijden, 2003). WeChat payment explored and introduced one of the most important features commonly known as “Red Packet” (hong bao). This feature allowed consumers to send money to an individual as a gift along with a message and served as a means of transferring large amounts of money (Qu et al., 2018). Perceived enjoyment is a strong predictor of intention to use mobile financial services (Chemingui & Ben Lallouna, 2013). In addition, it positively affects ease of use (Sedighimanesh et al., 2017; Wang et al., 2012). Based on the above, we propose the following:

Technology Acceptance Model

The TAM proposes that users’ intention to use information technology is a determinant of three influential factors, which are capable of explaining the actual use of information systems: perceived usefulness, perceived ease of use, and attitude toward using. Perceived usefulness is defined as “the degree to which an individual believes that using a particular system will enhance user’s job performance” (Davis et al., 1989). Tan et al. (2014) conducted a study in which the findings show that the intention to use m-payment is determined by perceived usefulness, perceived ease of use, social influence, and personal innovativeness in information technology. It has been argued by Kim et al. (2009) that people often estimate the outcome of their behavior and make a choice based on perceived usefulness. Thus, it influences customer intention to accept and adopt a system (Kim, 2010).

Perceived ease of use is defined as the degree to which a person believes that using m-payment would be free of effort (Davis et al., 1989). Prior studies show that perceived ease of use has a significant effect on usage intention, either directly or indirectly, through its impact on perceived usefulness (Davis et al., 1989; Jeong & Yoon, 2013; Venkatesh & Davis, 1996, 2000). Useable technology will attract more users (Venkatesh & Davis, 2000). Based on the above argument, the following hypotheses are proposed:

Behavioral Intention

Behavioral intention is defined as a state of sureness of the people’s intention to use specific technology. Behavioral intention is the most significant and critical factor influencing customers’ actual behavior (Ajzen, 1991). Our study model includes factors that have been tested or discussed by other scholars; thus, we hypothesize that behavioral intention directly influences users’ intention, which in turn will affect the actual behavior such as perceived ease of use, perceived usefulness and the TAM (Davis et al., 1989). Further, perceived reputation is critical for trust (Köster et al., 2016; McKnight et al., 2002; Zhou, 2014), perceived mobility (Gerhardt et al., 2010; Zhou, 2015), and perceived security (Friedman et al., 2000; Shaw, 2014; Shneiderman, 2000). In this study, we added the perceived role of the Chinese government as a new perception in investigating customers using mobile payment (Lu et al., 2005; Zhong, 2014; Zhou, 2014). Perceived risk was considered an influential factor on behavioral intention (Grazioli & Jarvenpaa, 2000; Salam et al., 2003; Warkentin et al., 2002) and subjective norms (Davis et al., 1989; Huang et al., 2020) and perceived enjoyment (Chong, 2013; Liébana-Cabanillas et al., 2017; van der Heijden, 2003) were also considered.

Research Methodology

In this section, we explain the data collection used in the empirical study to validate the suggested hypotheses. Exploratory and confirmatory analyses of the factors were used, and a discussion of the analyzed results was conducted. The limitations and future research of this study are also included in this section.

Data Collection

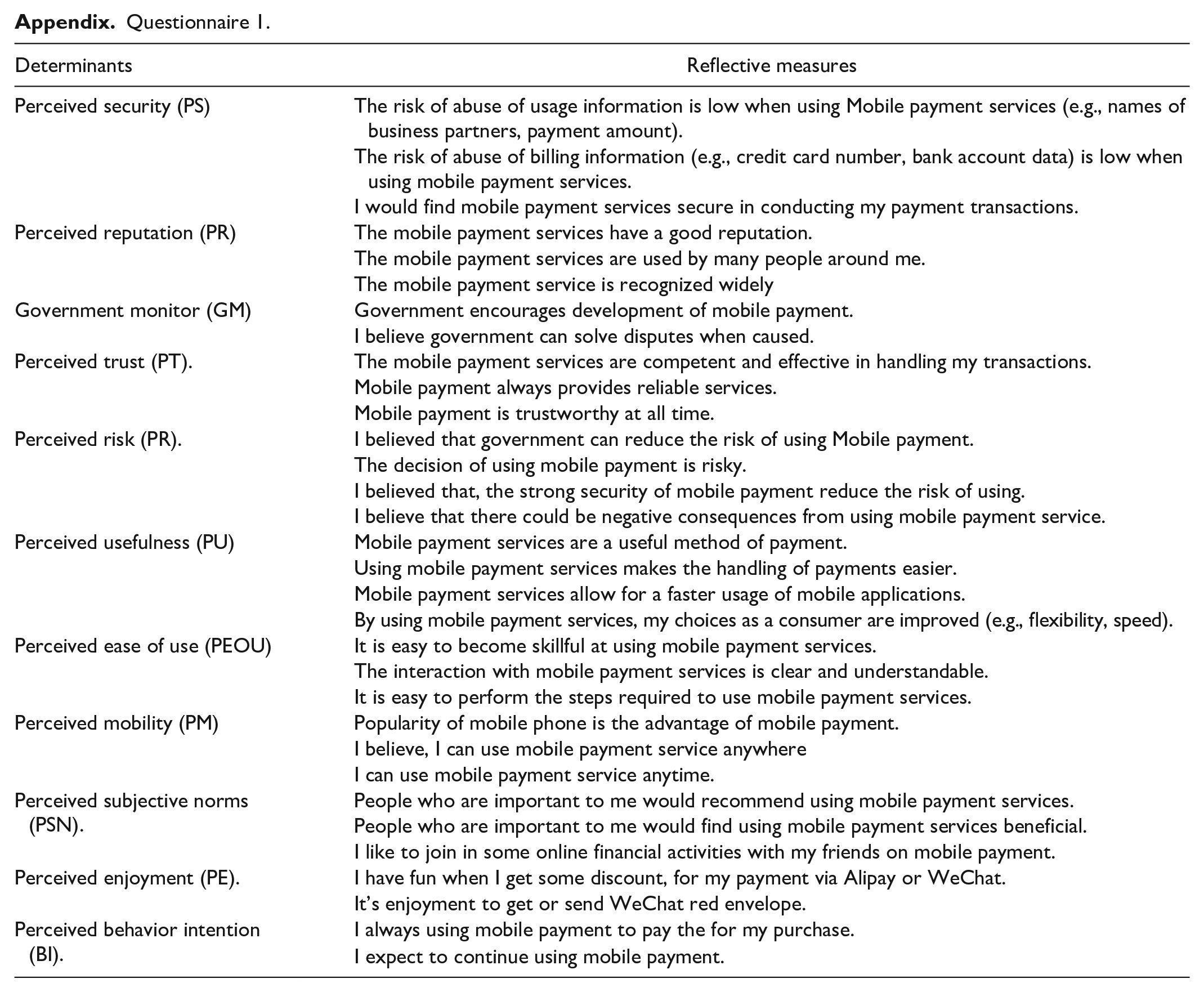

To validate our proposed research model, an online questionnaire was designed to collect data from Alipay and WeChat pay users in China. This study collected data from those who had experience using WeChat and Alipay. A total of 373 valid and effective data points were collected in Xian city and found suitable for statistical analysis; data collection took about 3 months. The measurement of this study was adopted from previous studies in the area (Bélanger & Carter, 2008; Davis et al., 1989; Gerhardt et al., 2010; Lu et al., 2009; Qu et al., 2018) and modified to fit the current research based on the two experts’ comments. The first application involved 50 users that were randomly selected to fill the questionnaire to test the validity and reliability of each item specifically. Four questions from the original questionnaire were removed, and some items were revised accordingly. Each question was measured on a 5-point Likert scale from strongly agree 5 to strongly disagree 1. The final questionnaire contained two parts: the first part included necessary personal information, such as gender, age, income range, and educational background. The second part included questions based on the hypotheses. The applied questionnaire is shown in Appendix 1. It had been mentioned in a report announced by WeChat in 2015 that most of the users were young people with income below 4,999 RMB and were undergraduate degree holders, as shown in Table 1.

Demographic Data.

The Exploratory and Confirmatory Analyses of the Factors

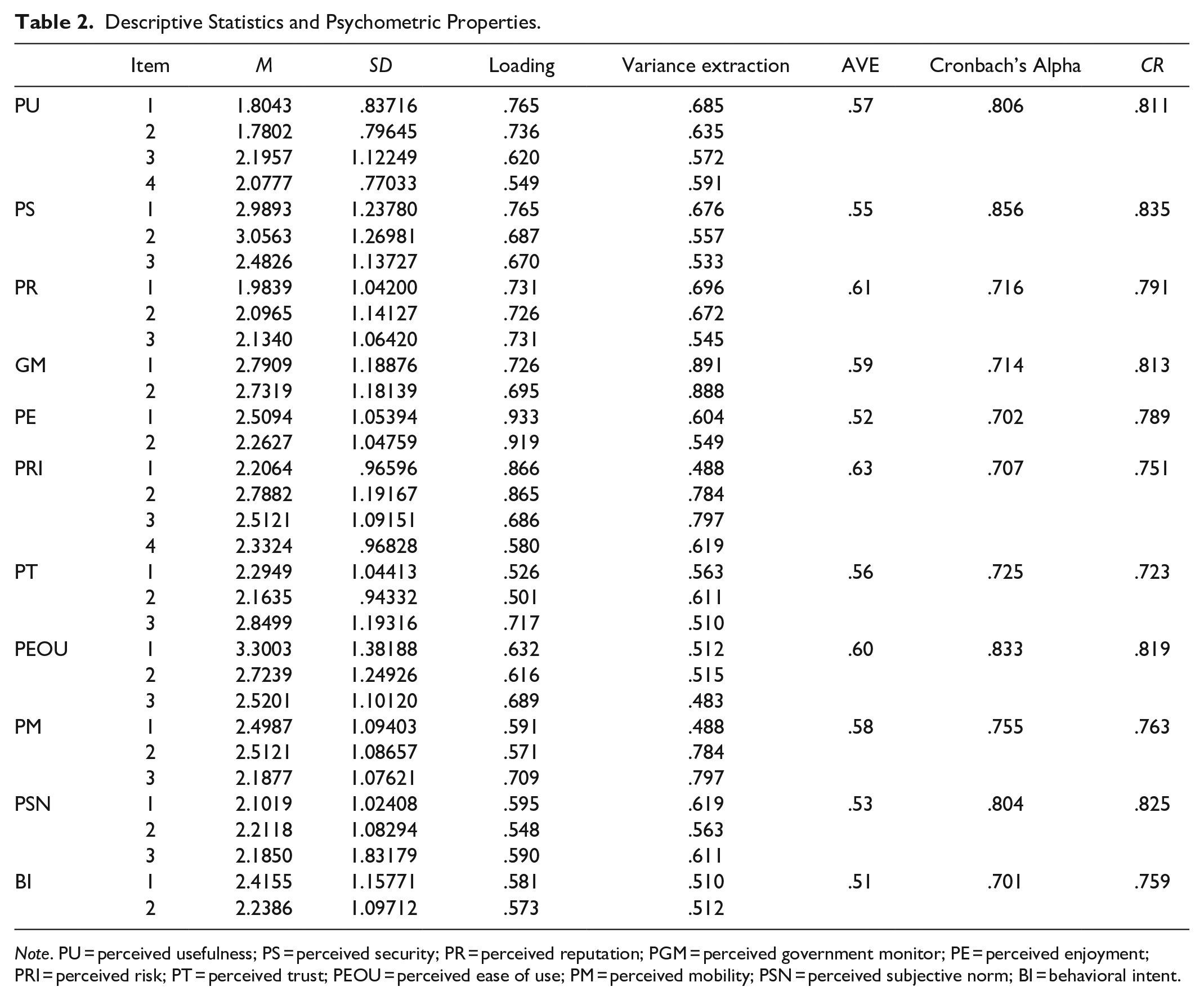

We conducted exploratory factor analysis to validate the samples of the study and determine the basic structures of the model framework. To ensure correlations between the factors and observed variables, a factor loading method was used (Yang et al., 2012). Analysis results are shown in Table 2. In this study, we used construct validity to evaluate the questionnaires, and KMO to measure the collected data, as the results appear .706 (Watkins, 2018).

Descriptive Statistics and Psychometric Properties.

Note. PU = perceived usefulness; PS = perceived security; PR = perceived reputation; PGM = perceived government monitor; PE = perceived enjoyment; PRI = perceived risk; PT = perceived trust; PEOU = perceived ease of use; PM = perceived mobility; PSN = perceived subjective norm; BI = behavioral intent.

Items were examined by confirmatory factor analysis and all results exceeded .50 in the loading of each item (Hair et al., 2011), which shows convergent validity. The CR is over .70, which refers to the satisfaction of each factor. The data met the requirements for further analyses. The AVE was examined for each factor, as illustrated in Table 2.

To test the internal consistency of the data, we used Cronbach’s alpha (Williams et al., 2010). The research calculated the Cronbach’s alpha coefficient of each hypothesis. The results shown in Table 2 reflect an overall Cronbach’s alpha of .802, and the coefficients of all factors were higher than .70, which means that the collected data meets the requirement that the Cronbach’s alpha coefficient should be higher than .80, and the coefficients should be greater than .70 (Williams et al., 2010). In addition, to determine the reasonability of the data validity, we calculated the square root of the AVE value for each factor, which is higher than the correlation between the different factors (Hair et al., 2011) as shown in Table 3.

The Correlation Between Factors.

Note. PU = perceived usefulness; PS = perceived security; PR = perceived reputation; PGM = perceived government monitor; PE = perceived enjoyment; PRI = perceived risk; PT = perceived trust; PEOU = perceived ease of use; PM = perceived mobility; PSN = perceived subjective norm; BI = behavioral intent.

p ˂ .05. **p ˂ .01.

Findings

In this section, we use exploratory factor analysis to analyze the data regardless of the theoretical support for the study factors. The main aim of confirmatory factor analysis is to ensure that the model suits the collected data and ensure the load of the factors. We conducted confirmatory factor analysis after exploratory factor analysis to test the proposed model relationship between the variables. It also analyzes the data and relationship to determine if the model is suitable and rational according to the fitting index (Bakhtiar, 2013). A path analysis was used in this study to evaluate the relationship between the factors in the hypothetical model and define which factors are regarded by the users. The statistical results are shown in the model Figure 2 and Table 4. Moreover, we estimated if the path is accepted through structural equation modeling (SEM) (Staphorst et al., 2013).

Path verification.

Correlational Statistics of the Study Hypotheses.

Note. PU = perceived usefulness; PS = perceived security; PR = perceived reputation; PGM = perceived government monitor; PE = perceived enjoyment; PRI = perceived risk; PT = perceived trust; PEOU = perceived ease of use; PM = perceived mobility; PSN = perceived subjective norm; BI = behavioral intent.

p ˂ .05. **p ˂ .01. ***p ˂ .001.

Furthermore, we used confirmatory factor analysis to determine if the model fit index is good. In SEM, many fit indices, like goodness-of-fit, exist to appraise the entire model, such as χ2, DF, CFI, GFI, AGFI, TLI, NFI, and RMSEA (Staphorst et al., 2013). χ2 is the most significant fit index because it is the foundation of many indexes and can also help in testing null hypotheses. In this research, we evaluate the fitness of the model using the indexes in Table 5, which show that fitness meets the requirement.

Model Fit Indices.

Note. χ2 = Chi-square; DF = degree of freedom; CFI = comparative fit index; GFI = general fit index; AGFI = adjusted goodness of fit index; TLI = Tucker-Lewis fit index; CFI = comparative fit index; RMSEA = root-mean square error of approximation.

Discussion

Our study offers a detailed conceptual understanding of the antecedents facilitating Chinese users’ trust or hindering Chinese users’ adoption of m-payment. Although TAM has been widely investigated in previous m-payment studies in China, to the best of our knowledge, no previous study has been conducted to investigate the government monitoring role to examine their impact on intention to adopt m-payment. Moreover, the study provides a further understanding of the trust formation process in the context of mobile payments in China. Finally, the study investigated several important factors that influence trust in mobile payment usage (Liébana-Cabanillas et al., 2014; Lin et al., 2014; Wang, 2014; Zhang, 2019).

Since security is one of the most important factors in financial services (Chellappa, 2008; Eid, 2011; Shaw, 2014), it is important to explore which factors influence the acceptance of mobile payment on third-party platforms. This study investigated the joint factors of the technical market and institutional factors of trust in mobile payment platforms. The findings of this research provide empirical support for the proposed model. The statistical results of the measurement of this research show that the hypothesized model can precisely define the intention of customers to use mobile payment services in China.

The most notable finding in this empirical study is that government monitoring should not be absent during mobile payment construction, as it is the most influential factor affecting trust in mobile payment platform usage in China. This strongly supports the proposed hypothesis 3. This finding is also supported by a previous study (Nathan, 2017; Nishimura, 2020; Wu & Wang, 2005). Chinese people prefer trusting the government (Kim, 2016; Nathan, 2017; Tolbert & Mossberger, 2006; Yen & Wu, 2016) because they believe that the government thoroughly investigate mobile payment platforms. Government roles toward using m-payment lead directly toward behavioral intention. While perceived risk negatively affects behavioral intention to use mobile payment, new users face the opportunity to use the new payment method. The impact of this influence has been widely affirmed in different fields (Liébana-Cabanillas et al., 2017). Moreover, it is important to increase users’ trust in decreasing perceived risk in mobile payments, which in turn will lead to the intention of use (Liébana-Cabanillas et al., 2014; Qasim & Abu-Shanab, 2016).

Regarding the role of the platform’s reputation, we found that it positively influences trust in mobile payment platforms (Zhang, 2019). In fact, WeChat and Alipay are among the most reputable companies in China. People are inclined to select services from more reputable providers (Corbitt et al., 2003; Huang et al., 2014; Qu et al., 2018; Teo & Liu, 2007), including in the mobile payment field. This finding suggests that m-payment operators need to realize the importance of reputation in building trust within m-payment and work toward strengthening it, for example, through positive word-of-mouth and a positive public image (Zhang, 2019).

Further, we found that security has a positive relationship with trust in the m-payment context. In mobile payment applications, people can now use many security mechanisms to verify the transaction, for example, text messages, face verification, and fingerprints. Thus, expectedly, it is essential for the service provider to ensure consistent m-payment transaction security and provide more personal options to keep users secure (Wang, 2014; Zhang, 2019).

Trust is considered essential for financial transactions. In our study, trust was found to have a significant relationship with perceived usefulness, which influenced behavioral intention toward actual usage. Trust in the current research is influenced by government monitoring of m-payment in China; it seems to be the most critical factor motivating customers to accept mobile payments in various situations. According to Lu et al. (2011), the decrease in the perception of risk within third-party services increases the continued utilization of m-payment. People prefer to interact with their friends whom they know and trust, especially when it comes to financial transactions. M-payment online transactions are not limited to friends. Regardless, we can conclude that trust has a direct effect on perceived usefulness in the m-payment context.

Mobility has been found to have a positive effect on trust. Mobility enhances users’ ability to perceive usefulness and ease of use related to m-payment. Therefore, mobility indirectly affects behavioral intention through perceived usefulness and ease of use, consistent with other studies (Kim, 2010; Kim et al., 2010; Yen & Wu, 2016). Moreover, mobility has a positive effect on perceived enjoyment. Mobile payment platforms normally provide different games to prompt financial services. Via mobility, users can enjoy interacting with friends and using financial services at the same time regardless of time and place; this advantage indirectly impacts users’ intention to use mobile payments (Hill & Roldan, 2005; Mallat et al., 2009). Furthermore, mobility positively impacts perceived subjective norms, which indirectly leads to behavioral intention via perceived enjoyment. Notably, perceived enjoyment is a significant antecedent for users’ intention to use mobile payment. The entertainment feature in the new payment methods strengthens the relationships among friends, which enhances and increases the use of m-payment. For example, in WeChat, if people get coupons from friends, they will consider WeChat pay in some situation, despite being customers of other online payment services. Our study results are consistent with other studies (Chen et al., 2017; Kalinic & Marinkovic, 2017; Soares & Pinho, 2014). Moreover, perceived enjoyment has a strong and significant effect on perceived ease of use, which has a strong, direct positive effect on behavioral intention for using m-payment.

The results also show that perceived ease of use and perceived usefulness have a significant direct effect on behavioral intention in m-payment adoption, which has been proven in the community (Belanche et al., 2012). Perceived ease of use could enhance customer intention to use m-payment and could also increase trust among the users, which in turn will affect the behavioral intention to use m-payment (Wu & Wang, 2005). Higher perceived ease of use might create a more satisfactory atmosphere when using m-payment services (Casaló et al., 2007).

Our proposed model extended the TAM, and it has some practical and theoretical implications for the researchers in the field of mobile payment adoption. First, the study provides better theoretical insight into the perceived trust from different perspectives and perceived risks that impact the adoption of m-payment by identifying their impact on users. Second, the study successfully investigated government monitoring roles, thus providing a clear picture of m-payment adoption.

The government should place an emphasis on mobile payment services to promote trust, usefulness, and strengthen the security system. User characteristics should be taken into consideration when developing mobile payments. Moreover, the government should pay attention to different mobile payment users at various stages.

For companies, our study has notable implications in designing their m-payment strategies that lead to higher acceptance and distribution of this new financial transaction tool.

Furthermore, service providers need to work toward strengthening mobile payment services. First, by exploring the most influential factor that enhances people’s use of mobile payment—. Second, they should bear in mind perceived trust and risk issues. Additionally, service providers could use various promotions and strategies to attract more users.

The study provides an in-depth analysis of the factors influencing customers’ trust and mobile payment services popularity in China, which can be applied to the development of m-payment services and e-commerce trade. Moreover, the paper analyzes the driving factor behind mobile payment popularity in China in combination with other mobile payment features. We argue that the Chinese government monitoring of m-payment brings more opportunities for the service provider and users to trust the m-payment system. Further, perceived enjoyment should considered, and service providers should offer more excitement and fun to keep customers online.

Conclusion and Directions for Future Research

Applications like WeChat pay and Alipay have received attention both users and firms through enabling e-commerce. Based on the proposed model and TAM, the study examined the most significant factors that encouraged customers to use mobile payment platforms. The results showed that government monitoring was the most considerable antecedent that led to mobile payment usage in mainland China. Thus, the government should place more emphasis on monitoring mobile payments to strengthen trust among users.

Moreover, the government should help service providers promote the usefulness of m-payment and the security system considering user characteristics. The government should pay attention to different user interests at different levels. Future research should examine the effect of other factors such as culture, social interaction, customization, and perceived value in enhancing users’ trust—and thus behavioral intention—and the actual usage of mobile payment.

Footnotes

Appendix

Questionnaire 1.

| Determinants | Reflective measures |

|---|---|

| Perceived security (PS) | The risk of abuse of usage information is low when using Mobile payment services (e.g., names of business partners, payment amount). |

| The risk of abuse of billing information (e.g., credit card number, bank account data) is low when using mobile payment services. | |

| I would find mobile payment services secure in conducting my payment transactions. | |

| Perceived reputation (PR) | The mobile payment services have a good reputation. |

| The mobile payment services are used by many people around me. | |

| The mobile payment service is recognized widely | |

| Government monitor (GM) | Government encourages development of mobile payment. |

| I believe government can solve disputes when caused. | |

| Perceived trust (PT). | The mobile payment services are competent and effective in handling my transactions. |

| Mobile payment always provides reliable services. | |

| Mobile payment is trustworthy at all time. | |

| Perceived risk (PR). | I believed that government can reduce the risk of using Mobile payment. |

| The decision of using mobile payment is risky. | |

| I believed that, the strong security of mobile payment reduce the risk of using. | |

| I believe that there could be negative consequences from using mobile payment service. | |

| Perceived usefulness (PU) | Mobile payment services are a useful method of payment. |

| Using mobile payment services makes the handling of payments easier. | |

| Mobile payment services allow for a faster usage of mobile applications. | |

| By using mobile payment services, my choices as a consumer are improved (e.g., flexibility, speed). | |

| Perceived ease of use (PEOU) | It is easy to become skillful at using mobile payment services. |

| The interaction with mobile payment services is clear and understandable. | |

| It is easy to perform the steps required to use mobile payment services. | |

| Perceived mobility (PM) | Popularity of mobile phone is the advantage of mobile payment. |

| I believe, I can use mobile payment service anywhere | |

| I can use mobile payment service anytime. | |

| Perceived subjective norms (PSN). | People who are important to me would recommend using mobile payment services. |

| People who are important to me would find using mobile payment services beneficial. | |

| I like to join in some online financial activities with my friends on mobile payment. | |

| Perceived enjoyment (PE). | I have fun when I get some discount, for my payment via Alipay or WeChat. |

| It’s enjoyment to get or send WeChat red envelope. | |

| Perceived behavior intention (BI). | I always using mobile payment to pay the for my purchase. |

| I expect to continue using mobile payment. |

Acknowledgements

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was supported by the Soft Science Research Program of Shaanxi Province (No. 2019KRZ008), the National Key Research and Development Program of China (No. 2018YFB2101502) and the National Natural Science Foundation of China (No. 61977002), Shaanxi Provincial Philosophy and Social Science Foundation Project in 2021: Research on “Embedded Climbing” of Agricultural Industrial Cluster in the context of Rural Revitalization Strategy (No. 2021D033).