Abstract

This research investigates the corporate social responsibility (CSR) reporting for banking industry in Nordic countries and China, and compares the convergence and disparity of disclosed CSR information across these two regimes. The study encompasses a sample of eight largest commercial banks by total assets in Nordic countries and China over a 5-year period of 2013–2017. We employ a disclosure index approach to assess the contents of CSR reporting based on eight categories and a total of 60 CSR indicators. The results indicate that Nordic banks have a higher overall disclosure level of CSR information than Chinese banks, and significantly ahead of their counterparts with respect to the international commitment, and a wider coverage of addressing stakeholders’ needs. In contrast, CSR reporting in Chinese banks put greater emphasis on national public policy and philanthropic activities. Nevertheless, all sample countries share a convergence on underlining the importance of complying with applicable laws and regulations. The study findings assert that the convergence and disparity of CSR reporting across countries is relevant to pre-existing socio-political institutions the firms can rely on. This research probes into an unexplored research territory by comparing the CSR reporting between banks from a so-called Nordic business-society model and a Confucian-tradition model. Hence, it entails some important policy prescriptions for the concerned administrators and corporate practitioners in the sample countries.

Introduction

Corporate social responsibility (CSR) has picked up momentum as a critical issue for many companies given the increasing public awareness of the influence of corporate activities on the environment and society (Amran et al., 2017). CSR related investments have significant implications for the financial performance of firms (Akbar et al., 2021; Qureshi et al., 2021). Companies are expected to act in a socially responsible manner and be financially accountable (Hackston & Milne, 1996). To obtain this “social license,” CSR reports are disseminated to communicate an enterprise’s achievement in striking a balance between financial goals and non-financial sustainability undertakings (Gunningham et al., 2004). Considering the widespread importance of CSR disclosures, 78% of the 250 largest companies in the Fortune Global 500 included CSR information in their annual financial reports in 2017. However, in 2004, only 44% reported this information (KPMG, 2017). This trend highlights the growing relevance of CSR information for company’s stakeholders. The trend for large companies to issue separate CSR reports also continued to grow globally as 75% for the 100 largest companies in 43 counties published CSR reports in 2017, while only 41% of them had issued such reports in 2005 (KPMG, 2017).

Most of the previous studies on CSR reporting commonly exclude banks from the sample (Aerts et al., 2006; Cormier & Gordon, 2001; Deegan et al., 2002; Siregar & Bachtiar, 2010). The reason for the difference in CSR reporting between banks and other industries is that the banking industry is exposed to lower environmental pollution and product safety standards (Khan et al., 2011). Most banks tend to disclose information regarding the efforts in energy conservation, waste management policies (Branco & Rodrigues, 2006), poverty reduction, and unemployment (Khan et al., 2011). The content of CSR reporting in banks is also found to be closely related with their core operation like financial literacy (Lock & Seele, 2015). Nonetheless, targeting the banking industry is crucial as the banks have come under greater scrutiny by the stakeholders regarding their credibility and CSR conduct since the U.S. financial crisis of 2007–2008 (Carnevale et al., 2012).

CSR reporting studies in developed countries are mostly related to companies operating in North America and Northwestern Europe (Ali et al., 2017). Companies in these countries always treat CSR reporting as a common business practice (Amran et al., 2017). Nevertheless, CSR research in terms of disclosure in developing countries is still limited (Ali et al., 2017). The discrepancies in CSR reporting between developed and developing countries are associated with the differences in social, political and economic environment (Jenkins, 2005; Visser et al., 2008). The field of CSR reporting research is still restricted due to little focus on comparative studies (Aguilera et al., 2007).

Notwithstanding, CSR reporting is a reflection of corporate efforts in terms of sustainable solutions to social and environmental challenges. Although, such endeavors may be regulatory affected since governments also need to be accountable in CSR promotion so as to be perceived as legitimate and modern (Clapp & Utting, 2008). Therefore, nowadays, CSR is not only a business-driven phenomenon but also a concept legitimated by a variety of institutional participants (Zhu et al., 2016). Owing to norms and values practiced in various regions are presented in different ways, CSR may be translated and transformed in various ways when governments intend to operationalize it in their national context (Gjølberg, 2010).

In the present research, we focus on two regimes: Nordic countries (Sweden, Denmark, Norway, and Finland) and People’s Republic of China. In line with the prior studies, Iceland has not been included in the sample of Nordic countries owing to a small country with less representative sample size (Gjølberg, 2010, 2011; Midttun et al., 2015). According to the Nordic Council of Ministers (2010), Nordic is an innovative and competitive region that has close collaboration with China, particularly with respect to climate change and energy. These two regimes share certain convergences about how the government affects economy and business practices. Nordic business system is typically regarded as coordinated market economies (Hall & Soskice, 2003) or social democratic business system (Amable, 2006). One of the unique characteristics of the Nordic model is that the government plays a central role in the economy (Gjølberg, 2010). This is similar to the Chinese business environment, where a strong government continues to exert major influence on the corporate economy (Su et al., 2003). Such normative pattern of economy in these two regimes also extends to CSR interpretation that CSR may be defined as a moral obligation toward the public, and therefore businesses need to give something back to the society. It is also a duty of the government to actively develop course of actions and public policy to promote CSR in the national or the international arena.

In this pretext, disparities in CSR’s understanding and interpretation may also exist between Nordic countries and China. CSR receives a strong national focus in China where CSR is potently reflected in governmental policy. In the last decade, the Communist Party of China began to incorporate the concept of CSR into its national-building project, namely “Harmonious Society” (Lin, 2010). Chinese business system also has a tradition of emphasizing economic aspects of CSR (Tang et al., 2015). Conversely, in Nordic countries, CSR is always extended to a wider perspective, in both definitional scope and the geographic context, referring to global human rights, peace, and sustainable development. Due to Nordic governments’ strong tradition of internationalism, some Scandinavian countries like Sweden and Denmark may recognize the role of CSR as “global corporate citizenship,” and perceive it as a way of regulating corporate resources in their government’s internationalist projects (Gjølberg, 2010).

Given that not only convergence but also disparity of CSR perception and practices emerge between Nordic countries and China, it is of particular interest to compare how CSR information to be reported across these two regimes. Prior studies have frequently examined CSR reporting in China (Ane, 2012; Liu & Anbumozhi, 2009; Zeng et al., 2010), but there are little studies focusing on Nordic context (Branco et al., 2014; Hąbek & Wolniak, 2013; Vormedal & Ruud, 2009). To the best of the authors’ knowledge, no prior studies shed light on CSR reporting in Nordic countries and China, making this study contribute to fill the research gap with a cross-country comparative analysis between the so-called Nordic business-society model and the Confucian-tradition model. By evaluating CSR reporting for each eight largest banks over the period of 2013–2017, we aim to investigate the convergence and disparity of disclosed CSR information across China and Nordic countries including Sweden, Denmark, Norway, and Finland. Iceland is not included in the research sample because of the relatively smaller size of banks and limited access to their CSR reporting information. Besides, we examine whether or not the similarities and differences in reporting standards are caused by the prevailing institutional environment under which the firms operate.

The rest of this article is organized as follows: Section “Literature Review” presents the literature review. Section “Method” entails the methodology. Section “Findings” presents the findings. Section “Discussion and Conclusion” provides the discussion and conclusion of the article.

Literature Review

CSR Reporting in the Banking Industry

As noted by Gray et al. (2001), CSR reporting entails information regarding an enterprise’s activities, desirability, and public image in terms of environment, community, employees, and customers. Extant literature commonly used legitimacy theory to explain CSR reporting for companies. This theory argues that a social contract exists between companies and the society (Deegan & Gordon, 1996; Milne & Patten, 2002; Patten, 1991). The viability of an organization depends on society’s perception of the organization’s value system and whether or not it is consistent with society’s own value system (Gray et al., 1996). As such, a company should operate in line with social values and expectations (Branco & Rodrigues, 2008). When the social contract is met, a company is legitimatized (Cormier & Gordon, 2001). When social expectations are not satisfied by the company, a legitimacy gap may appear (Branco & Rodrigues, 2006). CSR reporting helps companies to reduce the legitimacy gap by repairing lost or threatened legitimacy, retaining the current level of legitimacy, or even increasing legitimacy (Branco & Rodrigues, 2008). Besides social and environmental reporting can serve as an early response to alleviate legislative pressures (Parker, 1986).

The concept of organizational legitimacy enables CSR studies to advance into cross-country or cross-region analyses (Brammer et al., 2012; Joutsenvirta & Vaara, 2015). For instance, prior scholars investigated the mechanism where institutional arrangements within countries guide CSR motivations and practices (Matten & Moon, 2008). It is evident that CSR practices vary across different social, political, and economic contexts (Gjølberg, 2009; Matten & Moon, 2004). Also, CSR reporting performs differently across countries (Freundlieb & Teuteberg, 2013) because each country has a unique socio-political system (Visser et al., 2008) and political-economic system (Gjølberg, 2009). A cross-country study of CSR disclosure on websites between Spain and Sweden by Branco et al. (2014) compared the CSR communications in these two countries and revealed that Spanish companies are likely to disclose more CSR information, whereas Swedish firms tend to report more code of conduct and CSR-related press clips. Likewise, in a comparative study of Malaysia and Indonesia, CSR reports of Islamic banks in these two countries were examined by Amran et al. (2017). They used content analysis to assess CSR reporting and revealed that workplace and community dimensions are of most concern to banking companies in both Malaysia and Indonesia. Similarly, Tang et al. (2015) compared CSR information disclosures of Chinese companies with that of United States firms. The study found that the U.S. companies provided a higher level of CSR disclosure than their Chinese counterparts.

Although banking ethics are globally scrutinized by various stakeholders (Bhattacharya & Sen, 2004), there are still few studies on CSR reporting in the banking industry. As certain aspects of irresponsibility, environmental pollution, occupational health, and product safety are largely unrelated to the banking industry (Khan et al., 2011; Kiliç et al., 2015). As a matter of fact, banking companies are playing an increasingly important role in promoting CSR by providing financial support to such firms so as to mitigate the negative influence on the environment or society (Simpson & Kohers, 2002). Prior studies have also claimed that these indirect effects on CSR should be taken into consideration (Jain et al., 2015), along with the direct influences on resource consumption such as wastage of paper and energy (Branco & Rodrigues, 2006).

Achua (1998) also pointed out that the banking industry significantly affects socio-economic development of countries. Thus, today, most banks are concerned with CSR issues and disclose particular information about their efforts in energy conservation and waste policies (Branco & Rodrigues, 2006). Khan (2010) stated that banks often report activities concerning the reduction in poverty and local unemployment conditions. The 2017 KPMG survey revealed that CSR reporting among financial firms increased globally from 49% to 71% between 2008 and 2017 (KPMG, 2017). Recently, scholars have begun to investigate the nature and the extent of CSR reporting in the banking industry (Amran et al., 2017; Barako & Brown, 2008; Branco & Rodrigues, 2008; Khan et al., 2011). Khan et al. (2009) analyzed 20 banks in the Dhaka Stock Exchange. Their findings conjecture that the number of CSR reports in the selected banks is limited and the quality of disclosure is low. Likewise, Jain et al. (2015) examined voluntary CSR disclosure in six large banks each from Japan, China, Australia, and India. They report that Australian banks have the best reporting level of CSR information while Indian banks illustrate a significant improvement. In Turkey, the annual reports of the banks were examined by Kiliç et al. (2015). The result show that CSR reporting of Turkish banks improved between 2008 and 2012. Besides, the firm size, ownership diffusion, board composition, and diversity also positively affect CSR disclosure of sample banks.

CSR and Reporting in Nordic Countries

Generally, the Nordic countries geographically consist of Sweden, Denmark, Norway, Finland, and Iceland, while Iceland is often excluded from prior CSR studies focusing on Nordic regime (Gjølberg, 2010, 2011; Midttun et al., 2015). The Nordic governments and business systems have some similarities in terms of political system, economic institutions and social norms, therefore they are collectively referred as the “Nordic Model.” With the massive size of economy and population in Nordic countries, Sweden established a national CSR initiative, namely “Swedish Partnership for Global Responsibility” in 2002, for actively facilitating Swedish companies to engage into human rights, environmental conservation and anti-corruption based on the UN Global Compact and OECD policy (Swedish Ministry of Foreign Affairs, 2004). Sweden is also the first country that enforced CSR disclosure guideline, requiring all state-owned companies to publish an annual CSR report based on the Global Reporting Initiatives (GRI) Framework since 1 January 2008 (Hąbek & Wolniak, 2013).

Concerning CSR in Denmark, Danish government was the first Nordic country to launch CSR policy in 1993. Initially some incentive schemes were introduced by the Ministry of Social Affairs to encourage companies to employ migrants, disabled, and long-term unemployed people (Gjølberg, 2010). CSR is perceived as a strategic tool for Danish companies to earn competitive advantage in global markets. The government also required the 1,100 largest Danish firms to release CSR report or socially responsible investment policies since 2009 (Danish Ministry of Economic Affairs, 2008).

With respect to CSR in Norway, a consultative body of Norwegian government, termed as “KOMpakt,” was established to assist Norwegian companies to work closely to the basic norms of international society. In particular, helping firms operating in countries with poor human rights protection (Vormedal & Ruud, 2009). Normally, CSR in Norway is characterized as “humanitarianism,” and is strongly associated with global peace promotion and human right advocacy. Norwegian firms were also legally mandated to report CSR information under Section 3-3a of Norwegian Accounting Act since 1998 (Vormedal & Ruud, 2009).

In Finland, CSR firmly adheres to EU Lisbon Agenda (Gjølberg, 2010). Due to the fact that Finnish society more often agrees the importance of “action speaks louder than words,” CSR may be not always perceived as a critical factor in achieving competitive advantage in the market (Halme & Huse, 1997). Besides, Finnish firms do not traditionally consider CSR reporting as a necessity because Finnish business networking is relatively centered in southern regions, and people may be familiar with each other’s business practices (Fifka & Drabble, 2012).

CSR and Reporting in China

CSR reporting has gained considerable traction in China owing to increased pressure from various stakeholders (Yang et al., 2019). CSR in China is in the early stage of development in comparison with Western countries (Patten et al., 2015). As the second largest economy on earth, China is experiencing fast-paced economic growth, with increasingly negative impacts on environment and society (Yu & Rowe, 2017). For example, the high-level consumption of carbon-intensive fossil fuels generate serious environmental problems like contaminated air, water, and land resources (Guo, 2011). Heightened pollutant emissions are found to be associated with increased health problems in the society and higher public health expenditures of the government (A. Akbar et al., 2020; M. Akbar et al., 2021) In addition, social problems such as inequality at the workplace and the violation of human rights are also noticeable (Diener & Rowe, 2005). To cope with this emerging challenge, Chinese enterprises have now escalated environmental protection investments (Jiang & Akbar, 2018).

Prior scholars identified that CSR reporting in China is still at an early phase (Noronha et al., 2015; Zhao & Patten, 2016). Since 2006, the Chinese government has rolled out policies to shift the focus from economic development to a more equitable growth and sustainability of environmental and social dimensions (Yin & Zhang, 2012). Several legislative terms of CSR reporting have been enforced by the state administration and stock exchange regulators. For instance, in 2008 the State-owned Assets Supervision and Administration Commission of the State Council (SASAC) launched the “Guidelines for the State-owned Enterprises Directly under the Central Government on Accomplishing Corporate Social Responsibility,” emphasizing the importance of CSR reporting for State-owned companies (SASAC, 2008). In December 2008, the Shanghai Stock Exchange (SSE) issued specific guidelines, requiring that companies in the SSE Corporate Governance Index or listed abroad or financial companies need to publish stand-alone CSR reports (SSE, 2009).

Given the intensified efforts by regulatory authorities, the number of CSR reports in China has grown dramatically since 2009 (Patten et al., 2015). Nevertheless, the number of CSR reports of Chinese companies still lags behind the global average. The 2013 KPMG survey on CSR reporting for G250 companies indicated that the CSR reporting score of companies in China was only 39%, which was 20% below the global average (KPMG, 2013). The 2015 KPMG survey further demonstrates that Chinese companies have a significantly low score in terms of the quality of carbon disclosure in their CSR reports (KPMG, 2015).

Convergence and Disparity of CSR: Nordic Countries vs. China

Despite the fact that CSR was originally a business-driven concept, it has gained a widespread political interest so that governments may perceive CSR as a legitimate factor for achieving a modern civil society (Sahlin-Andersson, 2006). CSR reporting does not only reflect corporate efforts in providing solution of social and environmental challenges, but also explicate that how firms comply with regulatory approaches to better promote CSR (Clapp & Utting, 2008). Nevertheless, there are continuous disparities in CSR practices and their reporting across countries in the context of different social, political, and economic arenas.

The disparity in CSR practices could be explained by the institutional theory, mainly from the perspective of comparative political economy (CPE) approach. It focuses on how organizations constantly embedded in the national institutions of a country are essential to build its political-economic system (Manow, 2001). In a national context, governments may offer organizations with a set of defined norms and rules, hence continuously influencing their existing and potential practices. Due to the slow change of national institutions worldwide, CPE approach tends to agree the significance of continuous disparities in organizational forms across countries. Therefore, when firms develop their CSR perception and bring it into practice, they may be affected by the national pre-existing socio-political system (Gjølberg, 2010).

As a matter of fact, the increasing globalization may lead to more standardization of organizational forms and managerial applications, and also result in greater level of convergence in CSR and its reporting. This convergence could be interpreted by the new-institutional theory, which emphasizes the spread of organizational ideas toward the global context, and focuses on how organizations exercise their managerial discretion to apply new ideas to be considered as legitimate and modern (March & Olsen, 2004; Meyer & Rowan, 1977). In hindsight, the new-institutional theory is managed to explain the convergence of organizational practices due to global homogenization in terms of social, economic and political settings. CSR and its reporting are also converging over time because CSR ideas perceived by multinational enterprises may travel globally, and some CSR perceptions and practices are progressively diffused in a variety of global institutions.

CSR is prevalent both convergently and diversely across Nordic countries and China. According to Gjølberg (2010), both Nordics and China are the countries with a normative justification of CSR, where the governments are likely to emphasize the moral obligation of a company toward the wider society. This interpretation of CSR is different with that of America, which is regarded as self-interest and business-driven society. CSR in Nordic countries and China is always described as “corporate citizenship” that governments will play important role in promoting CSR. Accordingly, these two regimes more often agree the importance of CSR regulation, and frequently incorporate CSR into their public policies.

However, CSR will be interpreted with different focuses across Nordic countries and China. Chinese government only formulates, develops and embeds CSR in the national context, and has less incentive to extend CSR to the international arena. CSR is always linked to domestic political interest, for instance, in last decade it was inherently embedded in the Chinese national-building project, named “Harmonious Society” advocated by the Communist Party of China (Lin, 2010). Moreover, triple bottom line in China is not equally valued, and CSR traditionally emphasizes the greater importance of economic responsibility (Tang et al., 2015). Nevertheless, enforcement of corporate and public environmental spending in China is also attributed to a significant backlash from the society due to a conistent depletion in environmental quality (Shah et al., 2020; Jiang & Akbar, 2018). However, Nordic governments more often describe CSR as “global corporate citizenship,” and have wider focus with international implications. Because of Nordic governments’ strong tradition of internationalism, CSR is commonly incorporated into global business projects aiming to brand the country as a “hub of humanitarianism or environmentalism.” Nordic countries also have strong international profiles on a variety of CSR issues including human rights, poverty reduction, resource conservation and sustainable development (Gjølberg, 2010).

Although CSR practices and reporting may vary across countries with diverse socio-political and economic contexts, there might be some similarities in CSR reporting between sample Nordic countries and China given both governments have strong emphasis on promoting CSR endeavors. As such, the research question of current study lies in assessing the convergence and disparity of CSR reporting across these two regimes, and investigating whether such convergence resonates to the pre-existing institutional environment that the firms are embedded in.

Method

The study sample encompasses eight largest commercial banks by total assets in Nordic countries and China. The sample constitute three banks from Sweden, two banks from Denmark, two banks from Norway, and one bank from Finland to represent Nordic countries. The imbalance in number of banks selected from Sweden and Finland is because Nordea, the largest bank of Sweden is trans-regionally operating in the Nordic market, is also the biggest bank in Finland. The information of the sample banks is shown in Table 1.

Information of Sample Banks.

The stand-alone CSR reports and integrated annual reports (CSR disclosure included) were analyzed. The time period of 2013–2017 was used to assess whether CSR reporting of banks in Nordic countries and China changed over the years. Since banks in Nordic countries more actively integrate into European and international markets, their English version of CSR reporting were analyzed. Moreover, not all sample banks from China disclosed CSR information in English during the study period; therefore, only reports in Chinese language were analyzed.

The evaluation of CSR reporting consists of two parts. The first part presents the characteristics of reporting, including the written language and average length of CSR reports. The second part measures the content of reporting by using the disclosure index approach. The construct of content assessment is based on eight categories of indicators commonly used in banking industry, and on the criteria of relevance and credibility of disclosed information.

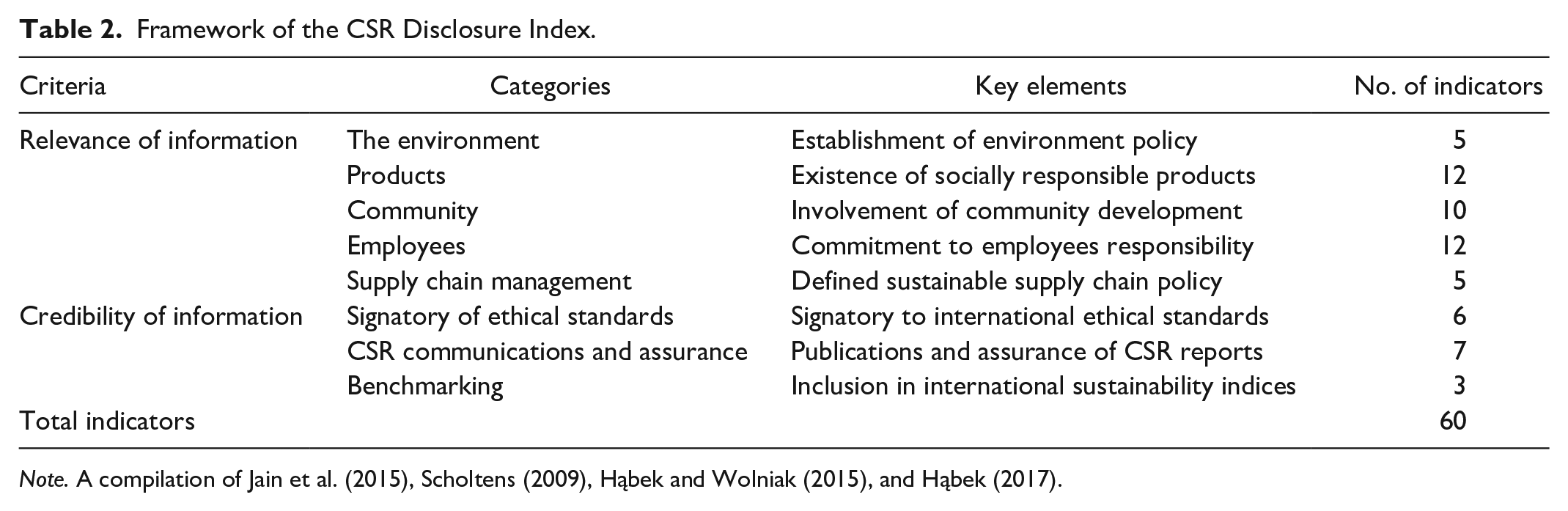

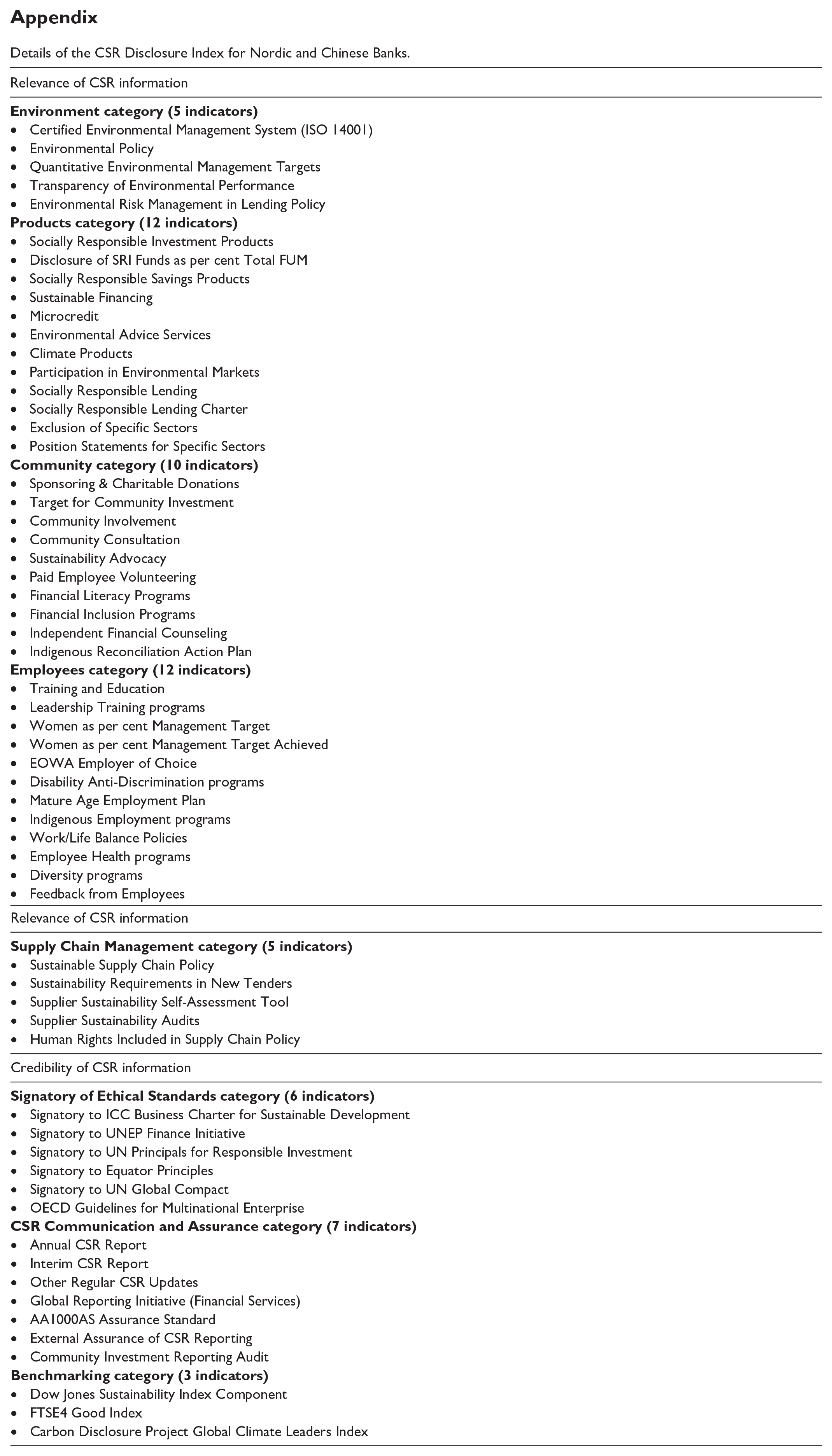

The layout of indicators conforms to the work of Guthrie and Jain et al. (2015) and Scholtens (2009) both carried out in the banking sector. The eight categories comprise of environment, products, community, employees, supply chain management, signatory of ethical standards, CSR communications and assurance, and benchmarking. We modified this layout by further defining the two-dimensional reporting criteria of relevance and credibility of information from Hąbek and Wolniak (2015) and Hąbek (2017), and sorted abovementioned eight categories as per the corresponding criteria. The framework of the CSR disclosure index for this study is presented in Table 2. More details on the disclosure index including a total of 60 indicators is included in the appendix table.

Framework of the CSR Disclosure Index.

Note. A compilation of Jain et al. (2015), Scholtens (2009), Hąbek and Wolniak (2015), and Hąbek (2017).

To value the content of CSR reporting, a score of either 0 or 1 for each of the 60 indicators was assigned to the banks. If a bank discloses a corresponding item of CSR information, it is assigned a score of 1, and 0 otherwise. In addition, the relative value of each category was calculated. For example, if a bank receives 4 out of 10 in the environment, it has a score of 40% relative to environment disclosure.

To ensure reliability, a trial analysis was first developed by the coder who is able to bilingually read CSR disclosures in both Chinese and English. A total of six CSR reports in three banks each from Nordic countries and China were preliminarily reviewed. The trial scoring process was then assessed and checked by a co-author with bilingual background. Upon validation of the scoring technique, the same coder scored CSR reporting for all sample banks.

Findings

Characteristics of CSR Reporting in Sample Countries

The characteristics of CSR reporting across Nordic countries and China are shown in Table 3. The type of format for CSR reporting was first compared. All Chinese sample banks have published separate PDF-format CSR reports on their website, while 22% of Nordic sample banks integrated their CSR reporting into annual reports. A Norwegian bank, named Storebrand, only published integrated reports during the whole study period. With respect to language used in CSR reporting, all Nordic sample banks have English-written version of CSR reporting, indicating that they are not only dedicated to native readers, but also make efforts to publicize their CSR information to readers around the world. Taking into account that there might be some differences in report prepared in native language and in English version, we choose a native report from each of the four Nordic countries, and compared with English-written version in terms of report layout, structure and length. We found that there is no significant difference of language interpretation, suggesting that Nordic sample banks did not use English language to publish a more concise or summary report. In Chinese sample banks, however, 53% of CSR reports have been prepared in two languages (Chinese/English). The top four leading commercial banks in China (ICBC, China Construction Bank, Agricultural Bank of China, and Bank of China) have published English-written version CSR reports during the study period, whereas two banks (Industrial bank and SPD bank) only disclosed CSR information in native language. The average length of an individual CSR report is 54 pages for reports from Nordic banks and 72 pages for reports from Chinese banks. It is striking to note that a Chinese bank, namely China Merchants Bank, has consecutively published CSR report with more than 100 pages between 2013 and 2017.

Characteristics of CSR Reporting.

Content of CSR Reporting in Studies Countries

The content of CSR reporting was assessed by the CSR disclosure index, in light of the two-criteria with eight categories of a total of 60 indicators. The descriptive statistics for the CSR disclosure index is shown in Table 4. There is a growth in the average number of CSR indicators reported during the sample period, suggesting that banks from Nordic countries and China are dedicated to improve their CSR reporting level over the years. There is also a continued increase in the minimum and maximum number of CSR indicators per region, inferring that CSR and its reporting has garnered growing importance by sample banks. Although compared with banks in Nordic countries, Chinese banks have a lower reporting level. For instance, a Chinese commercial bank, namely SPD bank, reported only 14 CSR indicators out of 60 in 2013 and 2014. Conversely, a leading Swedish commercial bank in the Nordic, termed SEB, reports the maximum number of indicators with 51 out of 60 reported in 2017.

Descriptive Statistics of the CSR Disclosure Index.

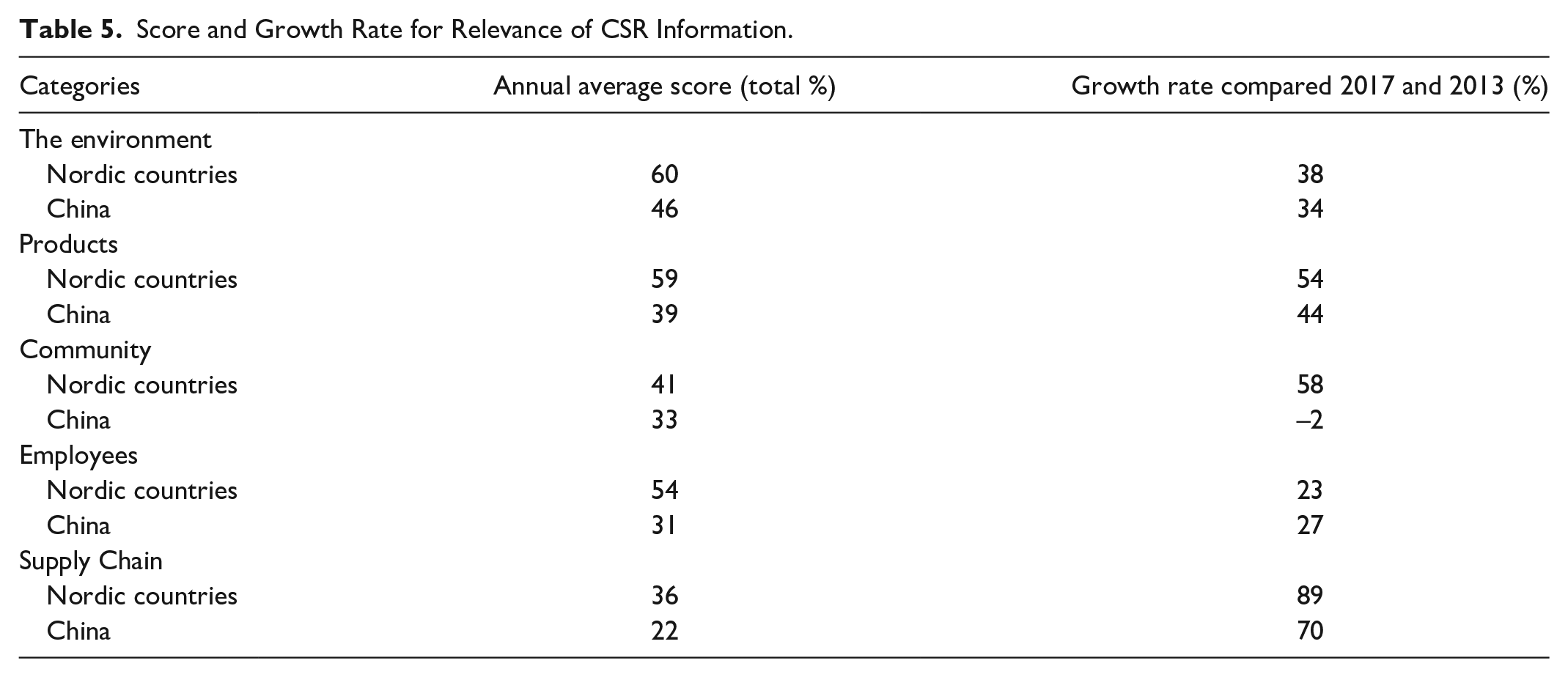

Relevance of CSR information

The relevance of CSR information is used to examine whether or not the disclosed information is understandable and useful that relates to the decision-making of internal and external stakeholders. Five categories of stakeholders are involved in this section including the environment, product, community, employees, and supply chain management. The score and growth rate for relevance of CSR information across Nordic and Chinese banks is shown in Table 5. The relative values were calculated by using actual disclosed indicators divided by the total number of indicators.

Score and Growth Rate for Relevance of CSR Information.

First, the category of the environment assesses whether sample banks comply with the following five indicators: compliance with the principle of a certified environmental management system such as ISO 14001, the establishment of environmental policy, the formation of a quantitative environmental management target, the transparency of environmental performance, and the existence of environmental risk management in the lending policies. When comparing banks’ CSR reporting toward environmental issues across countries, Nordic banks have more comprehensive reporting, revealing a higher disclosure level of 60% relative to 46% for banks from China. Moreover, Nordic banks more often adopt international environmental standards. For instance, in 2017 some Nordic banks including SEB in Sweden, Danske Bank in Denmark and DNB in Norway all disclosed firms’ compliance with the ISO 14001 standard. The quantitative targets of environmental management, such as greenhouse reduction and carbon footprint measurement, are also commonly disclosed in Nordic banks’ CSR reports. In contrast, Chinese banks are more likely to emphasize firms’ commitment toward national environmental policies. For example, over the analyzed period, most of Chinese banks have reported how corporate practices conform to public environmental provisions mandated by the Chinese Securities Regulatory Commission (CSRC).

Second, the category of products has 12 indicators to measure whether banks commit to socially responsible investment and saving and lending policies. This category also evaluates whether climate products, micro-credit, and participation in the environmental market are included in the reporting. Nordic banks exhibit a higher level of disclosure of 59% than Chinese banks with 39% disclosure level. Nordic banks also emphasize the importance of climate products, socially responsible lending, green bonds and sustainable financing. For example, one of the biggest banks in Finland, namely OP-Pohjola, elaborated how bank evaluate environmental risk during the creditworthiness analysis, and disclosed related ethical principles and guidelines for sustainable financing in its 2014 CSR report. On the contrary, Chinese banks more often simply describe their commitments toward responsible products and services, but seldom materialize how firms evaluate potential risks during the selection of specific products.

Third, the category of community composes of 10 indicators that measures banks’ social citizenship in community involvement, charitable donations, paid volunteering, and financial literacy. Banks from Nordic countries have a disclosure level of 41%, suggesting 8% higher than banks from China. Compared with Chinese banks, Nordic banks present more disclosure in terms of local financial literacy. For instance, Handelsbaken from Sweden disclosed that it had constantly supported economic research in local higher education and developed various projects for improving young people’s knowledge of personal finance. However, Chinese banks actively report charitable practices and poverty aids, taking in account the local and country’s best interests. It is interesting to note that all Chinese banks’ CSR report of 2017 has disclosed some elements related to “targeted poverty alleviation,” which a national strategic agenda was proposed by the 2016 National Congress of the Communist Party of China.

Fourth, category of employees has 12 indicators that measure whether banks disclose policies or commitments to training and education, leadership programs, disability programs, work life balance policies, employee health programs, equality and diversity programs, employment of women, and feedback from employees. Banks from Nordic countries have a disclosure level of 54%, significant ahead of Chinese banks which have only 31%. All sample banks across different regions have disclosed information regarding employees training and education programs, health and safety at work, equal pay, and diversity and equality.

One of the features of employees’ disclosure in Nordic banks is a focus of gender balance. For example, DNB, one of the biggest commercial banks in Norway, concretely disclosed the target and performance to improve female candidates when recruiting to and filling vacated management positions, as well as the measures to ensure sufficient access to female management talents. Conversely, over the analyzed period, very few Chinese banks reported information about gender targets and performance or the inclusive measures of female management.

Fifth, the category of supply chain examines the impact of banks’ sustainable practices on their supplier networks. There are five indicators including sustainable supply chain policy of new tender, the assessment process, human rights examination, and the supplier’s sustainability audits. Banks from Nordic countries have a disclosure level of 36%, 14% higher than banks from China. When disclosing sustainable supply chain, Nordic banks are likely to emphasize the assessment of sustainability risk among suppliers. For instance, in 2015 SEB’s CSR report, it elaborated how the bank formulated a systematic tool to comprehensively evaluate sustainability risk for each supplier.

Credibility of CSR information

The credibility of CSR information refers to examine whether the reporting can communicate CSR information fairly and objectively to relevant stakeholders. Three categories are formulated including whether the CSR reporting is signatory to international ethical standards, the extent of CSR communications and assurance, and the comparability of benchmarking. The score and growth rate for credibility of CSR information across Nordic and Chinese banks is shown in Table 6.

Score and Growth Rate for Credibility of CSR Information.

The first category is the signatory of ethical standards. It has six indicators, aiming to examine the extent to which banks are signatories to internationally industry-wide codes of conduct and ethical principles in terms of the financial services industry. The overwhelming number of banks from Nordic countries has signed with globally accepted ethical standards, with 81% of disclosure level during the analyzed period. Conversely, few CSR reports of Chinese banks were subjected to international signatory, with only 6% of disclosure level. Besides, most of Nordic banks’ CSR reports have committed to the signatory of United Nations Environmental Programme Finance Initiative (UNEP FI) and ICC Business Charter on Sustainable Development, whereas none of reports of Chinese banks have similar signatories from financial sector.

The second category is the CSR communications and assurance. There are seven indicators to examine the extent of CSR information communications to stakeholders, and whether or not the reporting is verified by external auditors. The disclosure level among analyzed countries is similar, revealing 46% in Nordic countries and 49% in China, respectively.

The third category is the benchmarking where three indicators are included to examine whether banks are listed on the Dow Jones Sustainability Index Component, the FTSE4 Good Index, and the Carbon Disclosure Project Global Climate Leaders Index. Nordic banks have a highly advanced disclosure level of 55%, whereas none of Chinese banks has any score in the benchmarking category during the study period. The results noticeably suggest that Chinese banks tend not to list on the global sustainable indices, and have fewer concerns with international affiliations than Nordic banks.

Overall disclosure level of CSR information

The overall disclosure level of CSR information in banks from Nordic countries and China is shown in Figure 1. It is evident that Nordic banks have higher overall disclosure level over the years, ranging from 51.04% in 2013 to 66.46% in 2017. As compared with Nordic banks, Chinese banks are still in the early stage of CSR reporting, with a lower disclosure level between 29.79% and 39.38% over the 5-year period. Although, all banks in each country have demonstrated a growing commitment to CSR reporting during this period. Banks from China have a slightly higher rate of growth with respect to the overall disclosure level, with 32.19% between 2013 with 2017, while the rate of growth in banks from Nordic countries is 30.21%.

Overall disclosure level of CSR information in Nordic countries and China.

Discussion and Conclusion

Despite the fact that the disclosure level of CSR reporting in banks from Nordic countries is ahead of banks from China, their CSR reporting may share some convergences. Both banks from Nordic countries and China have emphasized the importance of complying with prevailing laws and regulations. For instance, in 2017, SEB’s CSR report disclosed that the bank had taken various initiatives to strengthen the compliance with Swedish laws and internationally recognized guidelines. As a matter of fact, Nordic business system has some similarities with Chinese business system as both governments extensively engage in economic affairs through public policy (Gjølberg, 2010; Su et al., 2003). Unlike the Anglo-Saxon countries like the United States and Canada where the interests of shareholders and investors are often emphasized, stakeholder-oriented countries like Nordic and China may perceive CSR in a more normative manner and interpret CSR as a concept of political interest. Therefore, the moral obligation of businesses always contributes to a wider society, rather than firm’s own self-interests (Matten & Crane, 2005). Detailed set of provisions, rules and regulations is also a crucial factor when executives of firms exercise their management discretion to conduct CSR practices.

Another convergent feature of CSR reporting across Nordic countries and China is that over the investigation period, banks have increasingly recognized the importance of supporting international commitments. There are a growing number of Chinese banks who adopted ISO 14001 environmental certification and GRI guidelines. Likewise, an increasing number of Nordic banks adopted international financial-sector specific standards in their CSR reporting over the 5-year period. Such global standardization of CSR can be explained by the new-institutional theory which emphasizes how firm decide to adopt new ideas to become more legitimate and modern in the context of globalization in social, economic and political settings (March & Olsen, 2004).

Nevertheless, some disparities of CSR reporting between Nordic countries with China also emerged. First, Nordic banks are significantly ahead of Chinese banks when compared in terms of the credibility of disclosed CSR information. In particular, they are signatory of international, industry-wide, and sector-specific standards. Besides, the inclusion of international sustainable indices has been a key focus for Nordic banks. These findings are in line with Gjølberg (2010) as CSR in Nordic countries always attach high importance to a global perspective and contributes to the global governance in general. Moreover, the international tendency of CSR is due to Nordic governments’ traditions of internationalist ambitions and their continuous support of the United Nations (UN) and multilateral policy solutions.

On the contrary, national political agenda and public programs are key considerations for Chinese banks when disclosing CSR information. For instance, in 2017 an overwhelming numbers of Chinese banks demonstrated strong commitment toward the “Belt and Road Initiative,” a key program by the central government of China since 2014. Correspondingly, CSR in China has a national focus, and is always perceived as a moral obligation toward the nation (Gjølberg, 2010). The dominant power of the state also reflects the view that the CSR concept has been framed by the Chinese government and tightly links to a national-building project, termed as “Harmonious Society,” outlined by the Communist Party of China at the 2006 National People’s Congress (Lin, 2010).

The second disparity in CSR reporting across regimes is the different level of disclosed CSR information relevant to a variety of stakeholders. Nordic countries have advanced disclosure level, as their banks have overwhelming number of CSR indicators reported with respect to the category of the environment, product and employees. It is evident that Nordic business system, commonly with reference to “Nordic capitalism,” is more democratic and collaborative with a combination of economic competitiveness and social welfare (Fellman & Sjögren, 2008). Similarly, all Nordic countries share some similarities in public domain and equality, dialogue and participation are always emphasized. Some Nordic countries like Norway also lead the world in terms of humanitarianism and environmentalism, and have superior international profiles on CSR issues including poverty reduction, human right advocacy, resources conservation, and sustainable development (Gjølberg, 2010). In hindsight, Nordic banks follow suit to realize the importance of “global corporate citizenship” and address key issues in their CSR reporting including environmental protection, sustainable product development and the diversity and equality of employees.

Unlike Nordic banks which have more elaborate disclosure for all relevant stakeholders, philanthropic perspective has been a focal point in Chinese banks’ CSR reporting. During the analyzed period, most of Chinese banks reported substantial amounts allocated for philanthropy and poverty alleviation for undeveloped regions in China. For instance, in 2017 four leading commercial banks from China namely ICBC, China Construction Bank, Agricultural Bank of China, and Bank of China, disclosed charitable donation information on the section of “CSR at a glance,” with a total amount of 10.44, 10.43, 5.68 and 9.13 million, respectively. Notwithstanding, Chinese banks also have more economic indicators disclosed in philanthropy, whereas in other respects like green product and sustainable supplier network, the disclosed information tend to be more subjective and descriptive. The extensive disclosure of philanthropy is probably due to the fact that Confucian-tradition countries like China more often advocates collectivism where individuals need to cooperate and benefit each other in the society. Philanthropy, benevolence and humanity are the core values embedded in Chinese socio-political institution (Wang et al., 2015). Accordingly, CSR in China is always perceived as a synonymous to philanthropy (Yin & Zhang, 2012).

When explaining the disparities of CSR reporting between Nordic countries with China, the CPE approach of institutional theory can illustrate the inherent differences in CSR perception, practices and reporting across countries. To make CSR policies more compatible with pre-existing political and economic status, it is essential for the governments to transform the concept and content of CSR to a certain degree. Countries as diverse as Nordics and China have divergent level of political-economic institutions and different concerns of social and environmental issues, therefore result in a diverse disclosure level in CSR reporting.

Besides the structural institutional environment, different legal requirements across regimes also exert influence on banks’ CSR reporting level. In fact, Nordic countries are geographically part of Europe and under wide-range regulation by a variety of European Union (EU) rules in terms of non-financial reporting. Commencing on 1 January 2017, the European Directive 2014/95/EU requires that banks across EU to disclose the information in relation to environmental, social, treatment of employees, respect of human rights, anti-corruption and bribery, and diversity on company boards. Complementally, in June 2017, the European Commission released a voluntary guideline to help companies better disclose environmental and social information (European Commission, 2016). These particular EU’s non-financial reporting directives may explain why Nordic countries present a significant growth in the overall disclosure level of CSR information in 2017. In China, stock exchange regulators began mandating CSR reporting for a subset of firms including banks since 2008. However, such regulation only specifies which set of firms are subjected to the disclosure, and there is still no mandatory announcement in terms of what items or indicators to be disclosed in the reporting (Chen et al., 2017).

Our findings provide several implications to regulators, business management professional and related stakeholders. First, Chinese policy makers can set out some guidelines or rules to regulate the quality of CSR reporting. Moreover, to achieve greater transparency of CSR reporting at par with the Nordic countries and EU, regulatory body like CSRC can formulate a set of reporting standards including layout, contents, indicators and benchmarks that firms can rely on. Moreover, our findings also provide practical value for business, particularly international companies, as their operations extend beyond home country. Recently, there has been flourishing economic ties between Nordic countries and China, with a growing number of multinational corporations like Volvo, Maersk, and Huawei transnationally operating their business across Scandinavian and East Asia. Hence, as diverse social, political, and economic contexts prevalent in different countries, international companies need to gain requisite understanding of the existing institutional environment before conducting CSR reporting in a new country.

This study also entails some limitations. First, the analyzed regime is composed of only relatively large countries, but excludes small countries or regions like Iceland, Hong Kong, and Macau. Future research can be extended to the inclusion of more Confucian-tradition countries such as Japan, Korea, and Vietnam. Second, there is a relatively small sample that can hardly represent the whole banking industry. Thus, future studies can include more sample firms, and cover other industry sectors. Third, the legal contexts of CSR reporting among Nordic countries, EU and China have not received an elaborate attention. Future extension can compare diverse legal requirements in CSR reporting across countries and investigate how these differences cause the disparities in CSR reporting. Given some similarities of CSR reporting between countries, future research can also explore the standardization and harmonization of CSR reporting. Even though some globally recognized standards like GRI have been widely used, the pressure of converging CSR reporting to a universal standard is not as strong as that of financial accounting standards convergence due to less regulatory pressure and more stakeholder involvement (Tschopp & Nastanski, 2014). Future studies in this domain can therefore examine the factors that can contribute to a more harmonized CSR reporting framework.

Footnotes

Appendix

Details of the CSR Disclosure Index for Nordic and Chinese Banks.

| Relevance of CSR information |

|---|

|

|

| • Certified Environmental Management System (ISO 14001) |

| • Environmental Policy |

| • Quantitative Environmental Management Targets |

| • Transparency of Environmental Performance |

| • Environmental Risk Management in Lending Policy |

|

|

| • Socially Responsible Investment Products |

| • Disclosure of SRI Funds as per cent Total FUM |

| • Socially Responsible Savings Products |

| • Sustainable Financing |

| • Microcredit |

| • Environmental Advice Services |

| • Climate Products |

| • Participation in Environmental Markets |

| • Socially Responsible Lending |

| • Socially Responsible Lending Charter |

| • Exclusion of Specific Sectors |

| • Position Statements for Specific Sectors |

|

|

| • Sponsoring & Charitable Donations |

| • Target for Community Investment |

| • Community Involvement |

| • Community Consultation |

| • Sustainability Advocacy |

| • Paid Employee Volunteering |

| • Financial Literacy Programs |

| • Financial Inclusion Programs |

| • Independent Financial Counseling |

| • Indigenous Reconciliation Action Plan |

|

|

| • Training and Education |

| • Leadership Training programs |

| • Women as per cent Management Target |

| • Women as per cent Management Target Achieved |

| • EOWA Employer of Choice |

| • Disability Anti-Discrimination programs |

| • Mature Age Employment Plan |

| • Indigenous Employment programs |

| • Work/Life Balance Policies |

| • Employee Health programs |

| • Diversity programs |

| • Feedback from Employees |

| Relevance of CSR information |

|

|

| • Sustainable Supply Chain Policy |

| • Sustainability Requirements in New Tenders |

| • Supplier Sustainability Self-Assessment Tool |

| • Supplier Sustainability Audits |

| • Human Rights Included in Supply Chain Policy |

| Credibility of CSR information |

|

|

| • Signatory to ICC Business Charter for Sustainable Development |

| • Signatory to UNEP Finance Initiative |

| • Signatory to UN Principals for Responsible Investment |

| • Signatory to Equator Principles |

| • Signatory to UN Global Compact |

| • OECD Guidelines for Multinational Enterprise |

|

|

| • Annual CSR Report |

| • Interim CSR Report |

| • Other Regular CSR Updates |

| • Global Reporting Initiative (Financial Services) |

| • AA1000AS Assurance Standard |

| • External Assurance of CSR Reporting |

| • Community Investment Reporting Audit |

|

|

| • Dow Jones Sustainability Index Component |

| • FTSE4 Good Index |

| • Carbon Disclosure Project Global Climate Leaders Index |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research project is funded by the excellent PhD project of GCU-SCUT wide grant number 2019035. This research is also supported by the Key Project of the National Social Science Fund of China “Research on mechanism innovation and practice path of deepening mixed ownership reform” under grant number 21ZDA039. Authors also acknowledge scientific support by Postdoc Research Mobility at University of Hradec Kralove, and Research Centre of Accounting and Economic Development for Guangdong-Hong Kong-Macau Bay Area at Guangdong University of Foreign Studies.