Abstract

This study aims to (a) identify perception factors that affect current mobile banking (M-banking) consumers’ continuous use of the technology, (b) explain the self-service technology (STT) dimensions that affect customers’ behavioral intention, and (c) be able to offer recommendations to the banking industry or other organizations related to M-banking in terms of developing M-banking services in the future. Analyzed data were collected from 688 existing Thai M-banking users through online questionnaires. This study used the SPSS and AMOS statistical programs to analyze the data by applying structural equation modeling based on SSTs’ service qualities and the technology acceptance model (TAM). From the results, this analysis shows positive and significant relationships among SSTs’ service qualities, perception, and sustainable intention to use M-banking services. This study provides vital knowledge related to essential characteristics of M-banking as an STT that could assist banking institutions and application providers in enhancing their M-banking products. Moreover, this study adds to the knowledge area of SSTs’ service qualities in financial mobile application dimensions.

Keywords

Introduction

Banking institutions use advanced technologies to create various electronic channels that reduce the need for traditional banks. Mobile banking (M-banking) has become a new technology, new trend, and further interest (Cheng et al., 2006; Chin et al., 2003). Banks and other financial institutions allow their customers to manage business transactions by using mobile devices, such as smartphones and mobile tablets; this is known as M-banking. M-banking is different from internet banking because internet banking uses internet browsing software, while M-banking uses applications. Recently, smartphones have been playing an essential role in people’s daily lives. While smartphone technologies continuously develop, the demands for M-banking for financial services and mobile commerce have increased in Asian countries (Akhtar et al., 2019). M-banking can help financial institutions offer convenience to customers when they conduct banking transactions through mobile devices. For business persons, M-banking is a useful application and can create many benefits for entrepreneurs (Laukkanen et al., 2007).

The previous study considered the barrier to M-banking emphasized obstacles that negatively affect M-banking use intention and found a way to resolve these obstacles (Siyal et al., 2019). This research concerns specific factors influencing the adoption of M-banking to enhance the knowledge area of M-banking technologies. Customer relationship management is the required responsibility to provide customers with more satisfaction and interaction with M-banking (Hamidi & Safareeyeh, 2019). Previous scholars have studied factors affecting M-banking adoption. For example, Akturan and Tezcan (2012) studied the impact of perceived risk and the advantage for the customers to adopt M-banking. Selwyn (2007) integrated the involvement of gender with the adoption of new technologies. However, there is limited research in sustainable intention in using M-banking, concerning its characteristics as self-service technology (STT). Moreover, people still do not know the qualities of the technology that cause customers to use M-banking in the long term. Therefore, this research seeks to study the sustainable adoption intention of M-banking technology as an SST to understand which characteristics are generating sustainable adoption intention.

Based on the research gap, this study seeks to apply the technology acceptance model (TAM) in the research, as this is a suitable model for understanding the new technology adoption. Moreover, it can explain human behavior regarding the acceptance of modern technology. This research would like to answer the following research questions:

From the research questions, this study aims to investigate the role of STTs and to understand the perception of customers that becomes the critical factors influencing customers to select M-banking.

This research seeks to provide contributions from three perspectives. First, this research will fulfill characteristic knowledge of M-banking by assessing SSTs characters. Second, financial institutions can benefit from knowing the traits of M-banking that can sustain users’ adoption of M-banking. Finally, application developers can obtain a benefit along with financial institutions because they can develop the application to make M-banking more efficient, thereby offering a suitable M-banking application for the banking industry. This research has three objectives. First, this research seeks to identify factors that cause current consumers to continue using M-banking applications. Second, this research aims to understand how SSTs’ characteristics cooperate with customer behavioral intentions for using M-banking in the long run. Finally, this research seeks to provide a recommendation to the banking industry or to M-banking application developers to enable them to enhance their services in the future.

Literature Review

Mobile Banking

Shaikh and Karjaluoto (2015) defined M-banking as a type of electronic commerce (e-commerce) that is an essential frame of mobile application technologies or services. Moreover, in an era of new information and communications technologies (ICTs), M-banking can be an alternative for financial transactions such as shopping and donating, fund transferring, peer-to-peer payments, and other non-financial services such as PIN changes and balance enquiry checks. As the transactions mentioned above become essential services offered by banking institutions, customers can easily carry out banking transactions via mobile devices such as smartphones. One of the most commonly used transactions in M-banking services is mobile payment. Mobile payment is defined as a set of services, embedded in a mobile device, for payments for goods, services, and bills (Yang et al., 2012). The demand for M-banking services has increased due to the expansion of smartphone usage, resulting in each bank offering a new application through which to reach its customers. Banking service is proliferating throughout the world in terms of payments, mobile top-ups, credit applications, receipt alerts, bank account transactions, money transfers, and other banking transactions through mobile devices (Hanafizadeh et al., 2014). Previous studies concentrated mostly on internet banking or online banking, so there is room for the study of M-banking (Püschel et al., 2010). Laforet and Li (2005) studied M-banking in China and found that the attitude of customers affects M-banking adoption in that country. Moreover, they said that M-banking primary adopters are not necessarily young generations. Banking institutions are eager to find new methods to attract customers to use their services, and M-banking has become the primary tool for the banking industry because users tend to use M-banking more than e-banking (Shaikh & Karjaluoto, 2015).

J. Zhang et al. (2019) studied mobile payment, which is one of the M-banking services. Mobile payment has transformed conventional payment methods into digital payment methods. The researchers mentioned that there are vital factors such as the perception of interface design features. Liao et al. (1999) studied factors affecting M-banking usage using the theory of planned behavior (TPB) model and found that the TPB partially explains M-banking usage. Mortimer et al. (2015) studied the differences between M-banking adoption in Australia and Thailand and found the perceived usefulness (PU) and perceived ease of use (PEOU) effect on the intention to use M-banking in both countries. Finally, Sheng et al. (2011) found that PEOU has a more significant impact on intention to use M-banking in China. Thus, it can be assumed that M-banking and mobile payment become essential topics in different places, which relates to a cashless society.

The Concept of TAM

Many models have been used to explore the adoption of technologies. Moreover, many studies have concentrated on mobile service adoption. The original theory, the TAM, was created by Davis in 1986 (Davis et al., 1989). TAM was designed primarily to foresee the acceptance of new technology in the organizational context. The model focuses on attitude and intention, which have been applied in several technologies. Thus, many adjusted models have been used to understand technological acceptance and usage among users (Bertrand & Bouchard, 2008). TAM deals with awareness instead of real usage because users were asked about new technology. In this model, two key factors influence adoption intention: PU and PEOU. PU is described as the likelihood of potential users to use a particular technology to improve their job performance (Davis et al., 1989). PEOU is defined as the extent to which prospective users anticipate the system is effortless (Davis et al., 1989).

Koufaris (2002) tested TAM constructs to inspect how emotional and intellectual responses to visiting a web store can affect the intention of online customers to return and their probability of making unplanned purchases for the first time. Bertrand and Bouchard (2008) aimed to test how TAM utilizes virtual reality in clinical settings and revealed that only PU predicts the intention to use virtual reality (VR). Mathieson (1991) compared two models that predict an individual’s intention to apply an IS—TAM and the TPB—and found that it is easier to use TAM. Nevertheless, the model provides significant information about users’ beliefs regarding a system.

The Concept of SSTs

SSTs’ service quality has emerged as one of the broad service quality topics that have focused on how customers cooperate with firms to produce positive service outcomes. In addition, regarding the advancement of technologies, SSTs’ service quality is created to assist in the development of the customer experience, to reduce the expenses associated with employees, to keep customers, and to improve the technology to enhance business (Ryu et al., 2012). Meuter et al. (2000) referred to interface technology and mentioned that the type of SST could be classified based on telephone, internet, and interactive kiosks (i.e., ATM, video, and CD). Weijters et al. (2007) mentioned that SSTs have come to be famous in the retail industry because retailers attempted to find an approach to develop their products and services at a lower cost. SSTs can generate a higher level of customer behavioral intention if the quality is high (Spiros, 2010). Shahid Iqbal et al. (2018) studied how SSTs impact customer satisfaction, loyalty, and behavioral intentions and found a positive relationship between SSTs’ service quality, loyalty, and behavioral intention.

Moreover, the technology readiness (TR) model explains how users learn to integrate new technology (Parasuraman & Grewal, 2000). SST usage is influenced by TR to indicate the mental readiness of customers to accept new technologies (Liljander et al., 2006; Tsikriktsis, 2004). According to TAM, technology acceptance is shown through firm intention and attitude in the direction of the use of technology-enabled services that are principally affected by PU and PEOU (Davis et al., 1989). C. H. Lin et al. (2007) created the TRAM model by combining the constructs of TAM and TR into one model to explain better the intention to use electronic services among customers.

Parasuraman et al. (1988) used service quality to investigate the perception of customers toward services by using the multiple-item scale. In terms of the relationship between online service qualities, the quality measurement of online self-service increases as companies offer a variety of services through their websites, so-called E-SELFQUAL (Ding et al., 2011). SSTs’ service quality measurement constructs have been developed, including functionality, enjoyment, assurance, convenience, security, design, and customization, to understand the interaction of STT characteristics and customers (J.-S. C. Lin & Hsieh, 2011). First, functionality relates to reliability, ease of use, and responsiveness. Second, enjoyment is linked to customers’ satisfaction by investigating SST system usage. Third, assurance shows the confidence of consumers toward SST service providers. Fourth, convenience indicates whether customers can conveniently access and use the SSTs system. Fifth, security/privacy concerns focus on personal data, including protecting customers’ data from fraud. Sixth, the design pays attention to creating a plan for the SSTs’ service system. The last dimension is customization, which tests the customizability of the technology in meeting the demands of customers.

Moreover, Arcand et al. (2017) mentioned five dimensions. The first dimension is security and privacy. Security is no longer an addition in the software design and development process but is a primary dimension to initiate M-banking adoption. Second, functionality is defined as utilization and interactivity to improve self-efficiency. Next, the design is described as an aesthetic quality presented on a mobile device. The fourth dimension, sociality, is defined as the social benefits of interacting with others through a mobile device. The last aspect, enjoyment, is described as the perceived intrinsic motivation based on enjoyment while using electronic devices.

Several models have been developed to analyze and recognize the factors affecting computer technology acceptance in organizations (Guriting & Oly Ndubisi, 2006). There are theoretical models used by researchers to analyze the adoption, usage behavior, and acceptance of users, such as TAM (Davis et al., 1989), the model of PC utilization (Thompson et al., 1991), the theory of reasoned action (TRA) (Ajzen & Fishbein, 1980), and the TPB (Collins et al., 2011). According to TPB, a person’s actions can be described by behavioral intention, which is influenced by three factors: attitudes, subjective norms, and perceived behavioral control. Previous studies found that TAM tends to be superior to TPB in explaining behavioral intention to use an information system (Chau & Hu, 2001). The literature on consumer behavior uses TRA to understand the link between behavioral intention and actual behavior (Ajzen & Fishbein, 1980). TRA posits that the behavior shows the result of a desire of users to perform those behaviors (Ajzen & Fishbein, 1980). The main reason that TAM is the most suitable for M-banking is that it is widely accepted among IS researchers and can be applied to explain behavioral intention to use M-banking. Thus, this research uses perception from TAM, including PU and PEOU. PEOU and PU are essential perception components of TAM. The definition of PU is the degree to which users believe that using specific technology will improve their work performance. Meanwhile, PEOU is defined as the degree to which users can use technology free of effort (Davis et al., 1989).

Liébana-Cabanillas et al. (2017) found that m-commerce encouraged consumers to obtain new technology and to enhance their usefulness compared with existing alternatives. PU and PEOU helpfully and importantly influence people’s attitudes toward using M-banking (Mehrad & Mohammadi, 2017). The PU of e-learning was described as the magnitude of users who believe that e-learning can help them achieve goals (K. M. Lin et al., 2011). Moreover, PEOU was described as the magnitude of users who believe that adopting e-learning would be free of effort (K. M. Lin et al., 2011). The previous study suggested that PEOU affects attitude both directly and indirectly (Barkhi & Wallace, 2007). Moreover, PU directly impacts attitude (Bhattacherjee & Clive Sanford, 2016). In mobile business service circumstances, PU is the essential factor enhancing mobile service acceptance when consumers consider benefits (Luarn & Lin, 2005). Siyal et al. (2019) stated that the main factor influencing usage acceptance of the new technology is usefulness.

Behavioral intention can be described as a measure of the strength of personal intention to act in a particular way. Behavioral intention refers to a person’s likelihood to carry out an individual behavior (Hill et al., 1977). It is also defined as a consumer’s likelihood to use M-banking in the context of mobile commerce (Zarmpou et al., 2012). Wang et al. (2019) defined m-service user continuance intention as users’ long-term and regular use of a specific m-service. Thus, this study would like to set M-banking service users’ sustainable adoption intention as the long-term use of an M-banking service on a regular and consistent basis. Behavioral intention is the critical concept of TAM (L. Zhang et al., 2012), with the link to PEOU and PU. Researchers in information systems (Chang & Tung, 2008; Liébana-Cabanillas et al., 2017; Venkatesh & Davis, 2000; Yee-Loong Chong et al., 2015) have suggested that PU has a positive connection to behavioral intention in terms of using new systems. Generally, PU has a more significant impact on the acceptance of new technology compared with PEOU (Adams et al., 1992; Davis et al., 1989). In terms of sustainable adoption intention or sustainable usage intention, several scholars have studied how users tend to adopt certain technologies in the long run, such as mobile payment technology (X. Lin et al., 2019), mobile-based money acceptance (Gbongli et al., 2019), and perceived security (J. Zhang et al., 2019).

As reported by TAM, behavioral intention can be led by PU. Previous research revealed that PU directly and importantly influences behavioral intention to adopt online systems (Guriting & Oly Ndubisi, 2006; Khalifa & Ning Shen, 2008). Technology adoption can show the scope of human behavior that relates to the frequency of using a technology system (Webb & Sheeran, 2006). Previous studies also aimed to explore the customer intention to use STT (Venkatesh et al., 2012). For example, Shao and Liang (2019) studied the sustainable use intention and found that PU and PEOU have a significantly positive impact on the intention to continue using shared bicycles, to care and protect shared bicycles. Thus, PU and PEOU may be able to influence the sustainable use of specific technologies directly.

Conceptual Model and Hypothesis

This study adopts two main theories to gain more understanding about sustainable adoption intention regarding M-banking. The first theory is the SSTs. SSTs have been a theme of wide-ranging investigation for years and have emerged to understand the characteristics of service technologies that customers can apply by themselves. It affects how customers cooperate with businesses to reach positive service outcomes. SSTs combine several qualities that usually are studied separately. Thus, this research uses SSTs as a whole to verify that it can be implemented in the M-banking industry.

The second theory is TAM, as previous studies found that TAM tends to be more adept than TPB in clarifying information system adoption intention or the intention to use an information system (Chau & Hu, 2001). TAM is the most suitable for M-banking because it is extensively recognized among IS scholars and can be utilized to describe the sustainable adoption intention of M-banking. Thus, this research uses perception from the TAM model, including PU and PEOU. Previous studies also investigated customer intention to use STT (Venkatesh et al., 2012). Therefore, PU and PEOU are selected as critical perceptions that influence the sustainable use of M-banking. To that end, this research analyses the relationship between perception and sustainable intention to adopt M-banking.

Independent variables, dependent variables, and mediator variables are three types of variables used in this study. For independent variables, this research uses SSTs’ service quality because SSTs aim to understand the characteristics of STTs. The mediator variable is perception, which includes PU and PEOU—crucial factors from TAM. Finally, the dependent variable of this research is the sustainable intention to use M-banking services. In terms of sustainable adoption intention or sustainable usage intention, several scholars have studied how users tend to adopt technologies in the long run, such as mobile payment technology (X. Lin et al., 2019) and mobile-based money acceptance (Gbongli et al., 2019).

Therefore, as shown in Figure 1, the researcher offers the following hypotheses:

Hypothesized model of behavioral intention to use M-banking services.

Research Methodology

Questionnaire Design and Data Collection

This research collected data from 700 samples; 688 samples contain usable data from online questionnaires that the researchers distributed in Thailand. The online surveys were created through Google Forms because this channel is suited to the context of online adoption. The questionnaires were distributed for 2 months, from November to December 2019. This channel also helps researchers collect enough data within a restricted time frame. Thus, online data collection can help researchers avoid spending too much time on data collection and save money by using electronic devices instead of distributing paper questionnaires (Jansen et al., 2007). In this research, the target group is people who use M-banking for regular financial transactions such as money transfers or payment for goods and services. This research is exploratory. Independent variables, dependent variables, and mediator variables are three types of variables used in this study. For independent variables, this research uses SSTs’ service quality (functionality, enjoyment, security/privacy, assurance, design, convenience, and customization). The mediator variable is perception, which includes PU and PEOU. Finally, the dependent variable of this research is the sustainable intention to use M-banking services.

First, the researchers created the questionnaire items in English and translated them into Thai with an adjustment for Thai cultural context terms. After that, the questionnaire was checked by human–computer interaction and innovation experts to validate the content and characteristics of the questions, classify the questions, and examine the word use and language to ensure that it was proper. Next, this research completed the pilot test with 60 people who have experience in M-banking transactions. The SPSS program was used to calculate Cronbach’s alpha. From the pilot test, the Cronbach’s alpha of function was .901, of enjoyment was .886, of security was .911, of assurance was .929, of design was .869, of convenience was .943, and of customization was .907. The Cronbach’s alpha of PU was .899, the Cronbach’s alpha of PEOU was .899, and the Cronbach’s alpha of intention was .896. Nunnally & Bernstein (1994) explained that Cronbach’s alpha should be over .7. Therefore, the Cronbach’s alpha measurement scale of the pilot test was acceptable. After that, this research used the pilot test to adjust confusing words and fix wording mistakes. Finally, this research was ready for the distribution of the questionnaires.

Based on Table 1, the construct of the questionnaire was adapted from the previous studies. The constructs of SSTs’ service quality were adapted from Shahid Iqbal et al. (2018). The items of PU and PEOU were adjusted from C. Kim et al. (2010). Questions of intention were applied from Schierz et al. (2010). This research divided the questionnaire into three sections:

Questionnaire Items.

Note. FUN = functionality; ENJ = enjoyment; SEC = security/privacy; ASS = assurance; DES = design; CON = convenience; CUS = customization; PU = perceived usefulness; PEOU = perceived ease of use; INT = intention; M-banking = mobile banking.

Section 1: The questionnaire about demography, measured by using checklists;

Section 2: The questionnaire about the frequency of use of M-banking services;

Section 3: The questionnaire about proposed constructs, including SSTs’ service quality, perception, and intention.

For all questions, a 7-point Likert-type scale was used, ranging from strongly disagree (1) to strongly agree (7).

Data Analysis

This research used confirmatory factor analysis (CFA) to test the relationships among items in the first order and second order of the construct and used structural equation modeling (SEM) to evaluate the proposed model and test the hypotheses. SEM, as a second-generation technique, enables scholars to measure the nonobservable variables indirectly (Chin, 1998). The programs used in the statistical analysis and hypothesis measurement model are AMOS 26.0 and SPSS 26.0. SPSS is used to find descriptive information and the scale reliability test, which consists of mean, SD, and Cronbach’s alpha. This research used AMOS to analyze CFA and to analyze SEM of the proposed model.

Data Analysis and Results

Preliminary Analyses

Based on Table 2, the data of 688 respondents collected through an online questionnaire are distributed into the following characteristics. In terms of gender, females constitute 61.6%, while males constitute 38.4%. The age range between 21 and 25 years old was the most significant group, at 36.23%, while the age group of 56–60 years old was the smallest group, with 1%. In terms of education, the bachelor’s degree holds the most significant portion, at 71.5%. The main income level of M-banking users was under 10,000 baht per month. In terms of use of frequency, the percentage of customers who use M-banking more than 10 times per month was 66.9%, 7–9 times accounted for 16.2%, 3–6 times accounted for 13.9%, and fewer than 3 times accounted for 3%. The most successful financial transaction is a money transfer between accounts (94.8%). This research represents the proportion of gender in Thailand, as there were more female respondents than male respondents. Moreover, regarding the age of users with technological acceptance, respondents aged 25 and under (generation Z) were found to be the most technologically and digitally saturated generation who effortlessly mixes technology into their everyday lives. Hence, the respondent demographics reflect and represent society in Thailand.

Demographics.

Based on Table 3, the mean of constructs ranges between 5.38 and 5.78, and the standard deviation value ranges between 1.08 and 1.21. The highest mean was PU, which is equal to 5.78 with an SD of 1.21. The lowest mean score was security, equivalent to 5.38 and an SD of 1.09. All correlations were positive, and all significant pairs were positive.

Descriptive and Bivariate Correlations.

Note. FUN = functionality; ENJ = enjoyment; SEC = security/privacy; ASS = assurance; DES = design; CON = convenience; CUS = customization; PU = perceived usefulness; PEOU = perceived ease of use; INT = intention.

Later on, CFA was conducted to evaluate the measurement model and the fit index of the measurement model. From the measurement model of second-order CFA shown in Table 4, the value of all item standardized loading is higher than .50, which is similar to the suggestion of Hair et al. (2013). Moreover, the values of average variance extracted (AVE), Cronbach’s alpha, and composite reliability are all greater than .50, .7, and .80, respectively, which agrees with the statement of Fornell and Larcker (1981). Hence, the value of all items was acceptable. As shown in Table 5, the result of chi-square was 818.271, p < .001; normed χ2 or CMIN/df was 2.421; goodness of fit (GFI) was .915; adjusted GFI (AGFI) was .898; comparative fit index (CFI) was 0.969; and root mean square error of approximation (RMSEA) was 0.045.

Reliability and Validity Estimates of First-Order Constructs.

Note. AVE = average variance extracted; CR = composite reliability; SST = self-service technology; M-banking = mobile banking.

Significance at .001 level.

Values of Fit Indices.

Note. CFA = confirmatory factor analysis; SEM = structural equation modeling; GFI = goodness of fit; AGFI = adjusted goodness of fit index; CFI = comparative fit index; RMSEA = root mean square error of approximation.

Hypotheses Testing

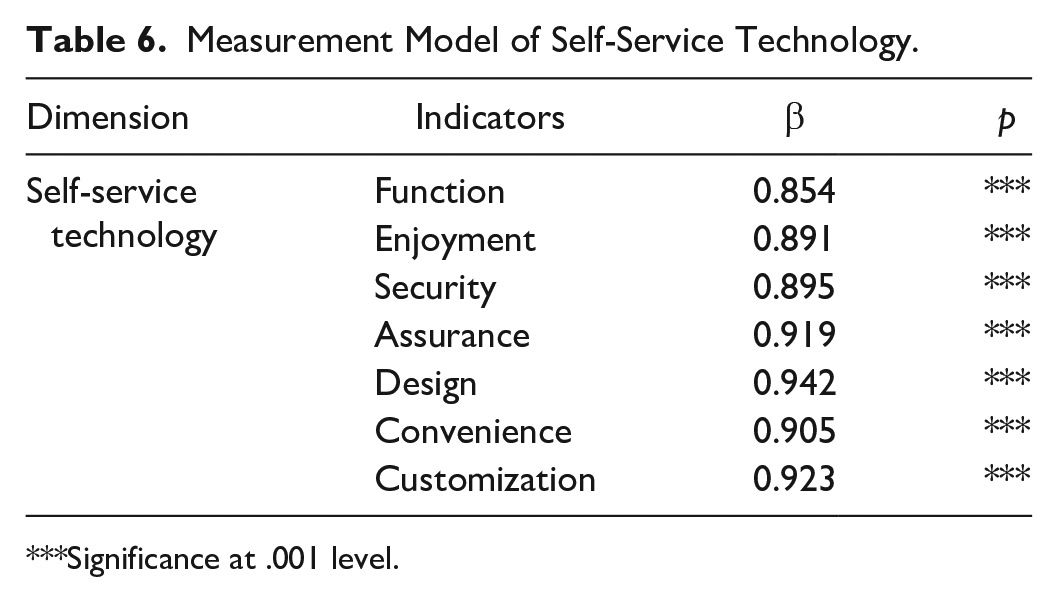

After investigating the measurement model, this research evaluated the first-order construct of STT. Based on Table 5, the measurement model results showed a significant chi-square (i.e., χ2 = 537.002, p < .001); the fit indices were CMIN/df = 2.951, GFI = .926, AGFI = .906, CFI = .970, and RMSEA = .053. In terms of the measurement model of STT, all seven constructs including function (i.e., β = 0.854, p < .001), enjoyment (i.e., β = 0.891, p < .001), security (i.e., β = 0.895, p < .001), assurance (i.e., β = 0.919, p < .001), convenience (i.e., β = 0.905, p < .001), and customization (i.e., β = 0.923, p < .001) are closely related. Table 6 illustrates the arrangement of significant value (p) and standardized estimate (β). The research of Hair et al. (2013) mentioned that the standardized estimation should be greater than 0.7 and that the critical ratio should be above 7.00. The result of this study was greater than the value proposed by Hair et al. (2013). Thus, this result supports H1, that SSTs’ service quality is a second-order construct reflected by the first-order dimensions of functionality, enjoyment, security, design, convenience, and customization, as shown in Table 6.

Measurement Model of Self-Service Technology.

Significance at .001 level.

After that, this research evaluated the first-order construct of perception. The results from Table 5 show that the value of CMIN/df was 0.102, while GFI = 1.000, AGFI = .999, CFI = 1.000, and RMSEA = .000. The measurement model of perception has two constructs consisting of PU (β = 0.884, p < .001), and PEOU (β = 0.994, p < .001). All the values were greater than the threshold of Hair et al. (2013). Hence, the results mentioned above support H2, which perception is a second-order construct reflected by the first-order dimensions of PU and PEOU, as shown in Table 7.

Measurement Model of Perception.

Significance at .001 level.

Moreover, Sharma et al. (2005) emphasized that the value of CFI must be higher than .90. RMSEA was lower than .08, and it was discussed that this value was an acceptable value for the fit index. Therefore, the value of first order, including STT and perception, was acceptable.

H3 stated that STT affects customer perception. The supportable outcome to H3 is shown in Table 8. For instance, path coefficients were .826, t-value was 18.801, and p < .001. Hence, PU and PEOU were affected by STT. For path coefficients, the result of H4 was 0.788, and the t-value was 18.137. Thus, H4 was supported, which means the behavior intention was affected by perception, consisting of PU and PEOU.

Path Coefficients and Significance.

Significance at .001 level.

Discussion and Conclusion

Discussion

Currently, banking institutions are seeking to provide heightened convenience to customers. Customers can conduct various transactions—such as payments and money transfers—via mobile phones. M-banking services have become imperative in the everyday lives of customers, have become widespread and trusted by many users. They can help customers perform various services without going to traditional banks. M-banking, as a STT, has been broadly accepted by people all over the world. Thus, this research seeks to study M-banking in the context of STT and sustainable adoption intention to understand how customers interact with and are satisfied by M-banking. The research does this by adopting the TAM perception dimension.

This research found that STT dimensions—security, enjoyment, functionality, customization, design, and convenience—are all linked to each other and can form M-banking characters with the potential to allow consumers to realize M-banking’s benefits and ease of use. This research found that the most valuable dimension of SSTs service quality in M-banking is functionality, followed by convenience, customization, enjoyment, design, assurance, and security, respectively. Moreover, SSTs service quality positively affects consumer perception, which includes PU and PEOU. Consumers use M-banking to transfer money in a second instead of wasting time finding an ATM or going to banks. Moreover, perception positively affects the sustainable intention of customers to use M-banking services.

SSTs service quality and perception, including PU and PEOU, were important variables affecting sustainable intention to use M-banking. This result is supported by the study of Gbongli et al. (2019). For instance, this study investigated the relationship between SSTs service quality and behavioral intention of customers, and the results were positively significant. Hence, if SSTs’ service quality was high, it could create a higher level of customers’ behavioral intention (Spiros, 2010). This study supports the work of Liao et al. (1999), which studied factors influencing M-banking usage in Taiwan. The results from this study also support the work of Mortimer et al. (2015), who studied the differences in culture between Australia and Thailand in terms of M-banking adoption. They found the effect of PU on the intention to use M-banking in both countries, while PEOU also has a direct impact on behavioral intention to use M-banking. Sheng et al. (2011) found that PEOU has a more substantial influence on the desires of Chinese users’ intention to use M-banking.

Recommendations

This study provides both theoretical and managerial implications as follows. First, the banking industry, software developers, and related organizations that provide M-banking services should pay attention to the functionality and convenience, as they are the highest dimensions that customer’s realize in terms of SSTs service quality. However, all of the SSTs’ service quality constructs are important enough to combine and create an attractive M-banking platform. Moreover, this research provides essential information about SST service quality that the banking industry, service providers, and software developers can use to improve applications in the future. In addition, the present technology plays an essential role in human life. The banking industry should enhance customer experiences to become familiar with advanced technology.

Furthermore, financial providers must support the improvement of features in M-banking applications so that the applications are easy to use. This research also adds to the knowledge area in terms of SSTs service quality in financial mobile application dimensions. As M-banking is well developed as a STT, the SSTs service quality can provide the necessary knowledge of application features to research in human–computer interaction, especially in the mobile application knowledge area.

Conclusion

This research makes contributions to the information system knowledge area by extending the factors affecting sustainable intention to use M-banking through the inclusion of SSTs and TAM. PU and PEOU have a crucial influence on the intention to use. Service qualities offered by banks also present an essential topic for M-banking. If M-banking maintains a high-quality standard, customers may realize this and prefer a convenient and easy-to-use application. Therefore, it is essential for banking institutions to provide the most reliable and consumer-friendly applications with a wide variety of services. Also, this will enable banks to keep existing users and attract new clients.

Although our research provides several benefits to both industry and academic sections, this research still has limitations, such as data collection and the selection of the sample size. First, this research distributed the online questionnaire in Thailand, which may not represent overall behavior in the whole picture. Hence, future research may choose a larger sample size to obtain more accurate information for analyzing this issue. Second, this study collected only quantitative data for quantitative analysis. It lacks hidden reasons why customers decide to use M-banking in the long run. Personal interviews with customers who use M-banking may provide more insight. Third, this research collects data in a whole country, regardless of the location. Thus, it may not reveal whether there are differences between people in urban areas and rural areas. In reality, customers who live in different locations may have different perspectives and attitudes toward the use of M-banking. Future research may seek to distinguish the behavior intention to use M-banking of people who live in urban and rural areas. Finally, this research focuses only on characteristics of SST service quality, regardless of the characteristics of the users. Hence, future research may study the characteristics of consumers in terms of M-banking usage intention.

Footnotes

Acknowledgements

The authors would like to thank the young researcher development project of Khon Kaen University for financial supports. Sincerely thank respondents for all their voluntary participation. We appreciate the anonymous reviewers for their productive comments.

Author Contributions

All authors collaborated equally. N.G. helped with the conceptualization and methodology, wrote the original draft, and was involved in revision and editing. N.G., N.H., P.T., T.U., and S.P. performed data collection, data analysis, and wrote the original draft. P.N. and C.K. helped with the supervision and was involved in revision and editing, adjustments, and other contributions that they considered appropriate.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research and/or authorship of this article: This research was funded by the Young Researcher Development Project of Khon Kaen University.

Ethics statement

This research was approved for a waiver of consideration in human ethics study with research code approval number HE623127.