Abstract

We provide an empirical analysis of herding behavior in cryptocurrency markets during COVID-19 and periods of cyber-attacks, differentiating between fundamental and nonfundamental herding. The results show that herding behavior is driven by fundamental information during the full sample period and the cyber-attack days. However, herding is not prevalent during the COVID-19 outbreak, either when reacting to fundamental or nonfundamental information. This finding suggests heterogeneity in the behaviors of participants in the cryptocurrency markets during the COVID-19 period.

Keywords

Introduction

It is often argued that herding behavior among investors challenges the efficient market hypothesis and can explain some of behavioral anomalies in the financial markets. Herding can be classified into two categories (Bikhchandani & Sharma, 2000). First, “spurious herding” is the tendency of investors to behave similarly to the same set of fundamental information. When fundamental information is easily available and processable, investors herd by buying or selling specific assets until the market price becomes equal to its fundamental value (Alhaj-Yaseen & Rao, 2019). This type of herding stabilizes the asset market, because it is fundamental information based. Second, “intentional herding” is the inclination of investors to suppress their own private information (or fundamental information) and intentionally copy others. This type of herding increases volatility, drives prices away from the fundamental value (Dang & Lin, 2016), and leads to instability in financial markets. Therefore, spurious (intentional) herding leads to market efficiency (inefficiency).

Although herding is well documented in conventional assets such as stocks (Chang et al., 2000; Christie & Huang, 1995), bonds (Galariotis et al., 2016), and commodities (Kumar et al., 2021), it is relatively understudied in the cryptocurrency markets that have emerged over the past years as a new digital asset, attracting a great deal of attention from researchers, investors, and policymakers. The emergence and attractiveness of the cryptocurrency markets are mostly supported by (a) the speculative nature of cryptocurrencies and their detachment from the global financial system, (b) the decline in public trust toward the central banking system after the global financial crisis (Weber, 2016), (c) the fourth industrial revolution and use of smart technologies, and (d) the acceptance of Bitcoin and many other cryptocurrencies as digital means of payment (https://www.businessinsider.com/top-cryptocurrencies). Cryptocurrency markets are immature, highly subject to psychological and sociological factors, and often criticized as risky and inefficient (Bouri et al., 2019). Their market participants are mostly young individuals, with a low level of education, an “animal” spirit, large cultural differences, and their information is irregular. Furthermore, the cryptocurrency markets have weak regulatory frameworks and weak information disclosure, and there is a lack of fundamental models to evaluate the price of a cryptocurrency (Gerritsen et al., 2020). These malfunctions can push crypto-traders to ignore their own opinions and herd toward the market consensus, leading to abnormal volatility. Previous studies examine herding in the cryptocurrency markets during bullish and bearish days (Ballis & Drakos, 2019; Bouri et al., 2019; da Gama Silva et al., 2019; Stavroyiannis & Babalos, 2019; Vidal-Tomás et al., 2019) and high and low trading volume days (Haryanto et al., 2020; Kallinterakis & Wang, 2019). Notably, the scarce evidence on herding points to the tendency of herding in cryptocurrencies when uncertainty is high (Bouri et al., 2019). However, no study has so far examined whether specific informational events related to the unprecedented COVID-19 outbreak and cyber-attacks induce herding behavior and whether herding in the cryptocurrency markets is driven by fundamental or nonfundamental information. This study addresses this literature gap.

The COVID-19 outbreak has adversely affected stock market indices and raised economic policy uncertainty and implied volatility indices to extremely high levels. It has shaped global economic activity and the financial markets (The China Manufacturing Purchasing Manager’s Index [PMI] declined by 33% in February 2020. U.S. equity indices declined by more than 30% during the period February 19, 2020 to March 23, 2020. Crude oil prices declined by more than 60% during the period January 1, 2020 to March 23, 2020. During the same period, Bitcoin price declined by 19%, including the cryptocurrency markets (e.g., Shahzad et al., 2021). Given the assumption that investors are fully informed, behave rationally, and make investment decisions after considering public information, crisis events such as COVID-19 have the power to induce uncertainty and noise in markets that disturb the decision processes of investors leading to irrational behavior. Herding intensity increases during market stress (Christie & Huang, 1995). Several studies have detected herding in various stock markets during crisis periods (Chiang & Zheng, 2010; Yousaf et al., 2018) as well as in commodity markets (Babalos & Stavroyiannis, 2015; Kumar et al., 2021). However, the existing literature remains salient regarding the herding behavior in the cryptocurrency markets around the COVID-19 outbreak.

As for cyber-attacks, they represent a major challenge in the cryptocurrency markets that rely on the internet and blockchain technology. Previous evidence exists for the frequent occurrence of cyber-attacks and their ability to destabilize the cryptocurrency markets (Caporale et al., 2020; Ciaian et al., 2016; Moore & Christin, 2013). Negative events related to cyber-attacks on Bitcoin/cryptocurrency exchanges reduce Bitcoin/cryptocurrency attractiveness for investors (Ciaian et al., 2016). The occurrence of cyber-attacks in the cryptocurrency markets generally drive crypto-traders to engage in sell-offs as a way to conform to the market consensus. Corbet et al. (2020) find that cyber-attacks not only increase the volatility of the cryptocurrency involved but also increase the correlation with other currencies. However, it is not clear whether cyber-attacks can shape herding in the cryptocurrency markets.

Cryptocurrencies do not have an underlying physical/monetary form as conventional assets such as equities. Various methods have been employed for valuation, such as the cost of production model for determining the fair value of Bitcoin (e.g., Hayes, 2017), aggregate blockchain characteristics (e.g., Bhambhwani et al., 2019), and the concept of utility (García-Monleón et al., 2020). This suggests the need for examining whether herding is driven by fundamental or nonfundamental information, which remains understudied.

This article contributes to the academic literature on four fronts. First, it contributes to the growing body of literature on the effects of the COVID-19 pandemic on financial markets (Bouri et al., 2021; Chowdhury et al., 2021) and cryptocurrency markets (Corbet et al., 2020; Shahzad et al., 2021; Yousaf & Ali, 2020) by extending the studies on herding in cryptocurrencies to the effect of the COVID-19 outbreak which represents an unprecedented crisis period. Second, it contributes to the literature on the effects of cyber-attacks on the cryptocurrency markets that are continuously facing the challenge of cybersecurity (e.g., Corbet et al., 2020). Caporale et al. (2020) point to the necessity to extend our limited understanding of the impact of cyber-crime to avoid potential disruption to cryptocurrency markets. Third, it nicely extends the growing literature on herding behaviors in cryptocurrencies by exploring whether herding is driven by fundamental or nonfundamental information (e.g., Bouri et al., 2019; Vidal-Tomás et al., 2019), especially given recent on the use of valuation models to evaluate the price of cryptocurrencies (Bhambhwani et al., 2019; García-Monleón et al., 2020; Hayes, 2017). Fourth, it accounts for the three-factors (market, size, and reversal factor) of the cryptocurrency model of Shen et al. (2019), which adequately capture important fundamental information that may affect cryptocurrency investor decisions at a market level.

Data and Methodology

Data

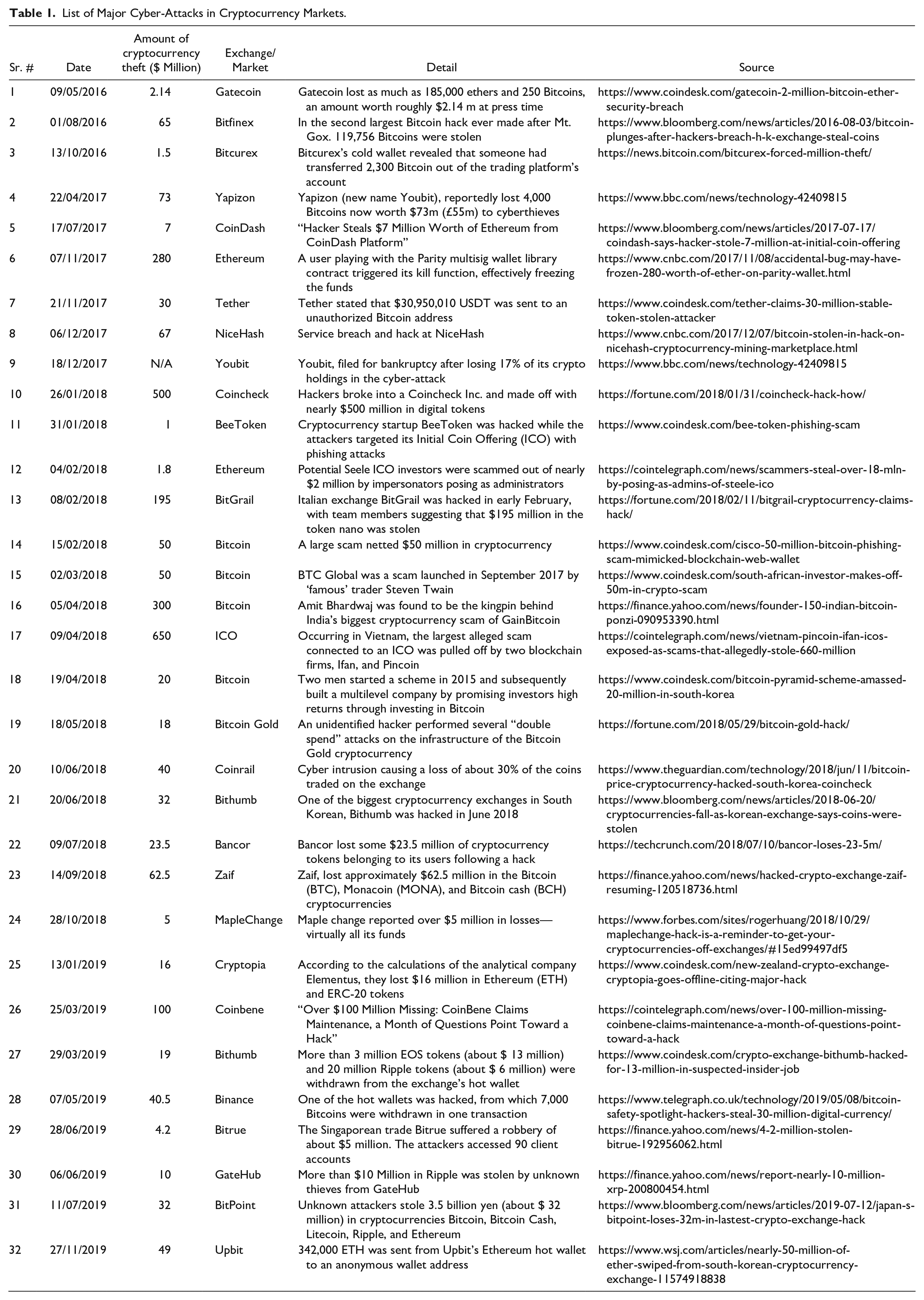

This study employs daily data on 75 cryptocurrencies that represent more than 82% (as of January 1, 2020) of the market capitalization of all cryptocurrencies (www.coinmarketcap.com). The full sample period is from 01/03/2015 to 19/03/2020, yielding 1,845 daily observations and covering the recent COVID-19 outbreak period that spans 01/01/2020 to 19/03/2020. Many recent studies (e.g., Shahzad et al., 2021; Yousaf & Ali, 2020) use approximately similar data segments to define the COVID-19 period while studying the financial markets and cryptocurrency markets. In Table 1, we have provided a list of the 32 largest cryptocurrency hacking events between 01/03/2015 and 19/03/2020. This list consists of different types of cyber-attack events that affected either the wallets of cryptocurrency investors, the cryptocurrency exchange, or the blockchain supporting a specific cryptocurrency. We have used the mainstream news sources of cryptocurrency market to identify these cyber-attack events, like Bloomberg, BBC, Forbes, Fortune, Yahoo Finance, Wall street Journal, and Coin desk. We have also used those cyber-attack events which are used by the Corbet et al. (2020). The risk-free rate is defined as the U.S. 3-month T-bill rate, for which the data are taken from the U.S. Department of the Treasury (https://www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/default.aspx). The empirical analysis is performed with daily log return of cryptocurrency series. Unreported results show that all cryptocurrency returns exhibit a high standard deviation value and a departure from the normal distribution, which points to tail events. Furthermore, all return series are stationary.

List of Major Cyber-Attacks in Cryptocurrency Markets.

Spurious vs. Intentional Herding During COVID-19 and Hacking Days

Our base model follows Chang et al. (2000) who argue that the nonlinear relationship between the dispersion of individual asset returns and market returns is interpreted as evidence of herding behavior. Dispersion is measured through the cross-sectional absolute deviations (CSAD) as follows:

In the framework of our study, i denotes the cryptocurrency, t denotes the time period, and N represents the number of cryptocurrencies. Rit indicates the returns of each cryptocurrency i at time t, Rmt denotes the market returns (i.e., cross-sectional average returns of N cryptocurrencies) at time t. Lower values of CSADs suggest that investors discard their private information and copy their peers. Chang et al. (2000) propose the following model to estimate herding:

The rational asset pricing model suggests that

Following Galariotis et al. (2015), we split the total CSAD into two parts, (a) CSAD due to common fundamental factors and (b) CSAD due to nonfundamental information. To estimate CSAD fundamental and CSAD nonfundamental, we first calculate the three-factors (excess market returns, small minus big, and reversal factor) of the cryptocurrency model, suggested by the Shen et al. (2019), to adequately capture the important fundamental information that may affect cryptocurrency investor decisions on a market level. We then estimate a regression of the total CSAD as follows:

where

However, the CSAD based on fundamental information can be written as:

Then, the fundamental and nonfundamental information-based herding is estimated through the following equations:

In Equation 6, if

To estimate whether herding is spurious or intentional in the cryptocurrency markets during the COVID-19 outbreak, the following regressions are used:

For COVID-19,

To examine whether herding is spurious or intentional during cyber-attack days in cryptocurrency markets, the following regressions are used:

For hacking events,

Empirical Findings

The results for fundamental and nonfundamental herding are reported in Tables 2 to 4. Table 2 reveals that the

Results of Fundamental and Nonfundamental Herding—Full Sample Period.

Note. If

Results of Fundamental and Nonfundamental Herding During COVID-19.

Note.

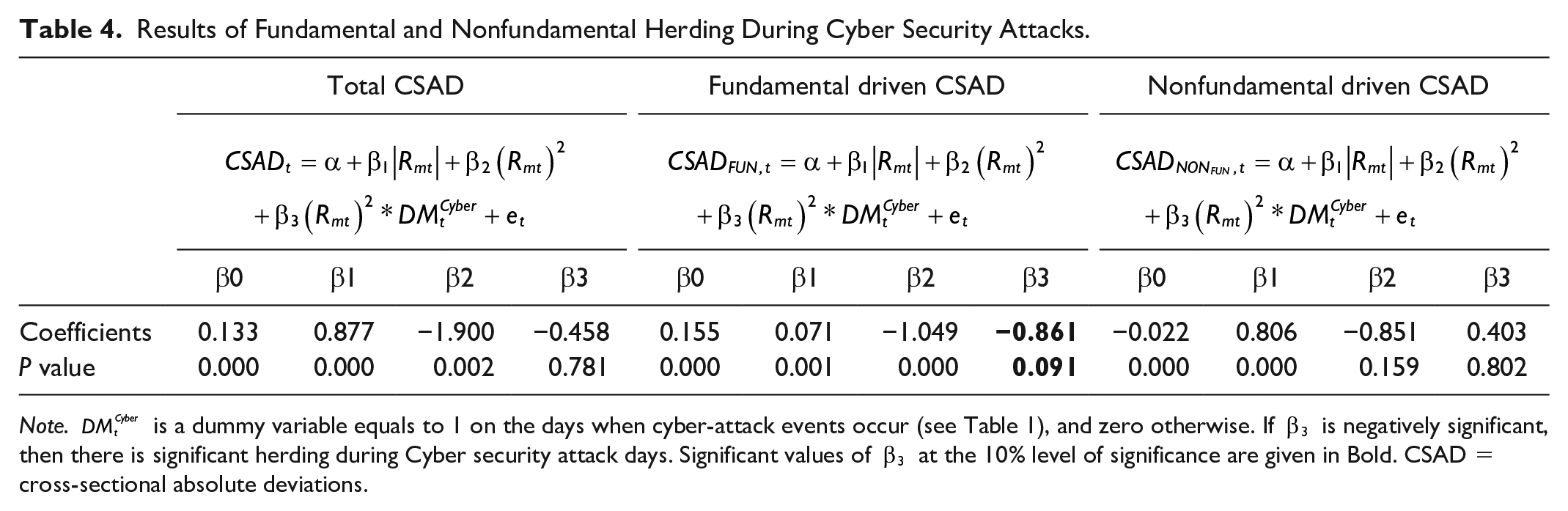

Results of Fundamental and Nonfundamental Herding During Cyber Security Attacks.

Note.

Our results emphasize the importance of the sample periods used in this analysis. The cryptocurrency markets exhibit significant (fundamental) herding during cyber-attacks but do not show any evidence of herding behaviors due to the COVID-19 pandemic. This concords with previous studies showing that herding increases with the level of uncertainty, which in our case is related to cyber-attacks, but not to COVID-19. The latter seems to represent an exogenous factor to the behavior of crypto-traders, suggesting the irrelevance of informative signals derived from COVID-19 on herding whereas informative signals derived from technological factors such as cyber-attacks matter to herding. This finding can also be explained in light of the literature showing the detachment of cryptocurrencies from the global financial system and their hedging ability. Accordingly, our results indicate that participants in the cryptocurrency markets during COVID-19 do not feel the panic of uncertainty seen during cyber-attacks, probably because COVID-19 does not induce enough uncertainty to make investors mimic the actions of others, implying a lack of consensus on how crypto-traders interpret this unprecedented pandemic event in the era of cryptocurrencies. In contrast, crypto-traders have the learning from previous cyber-attacks, which makes them use their cognitive learning and long memories to herd toward the consensus.

Conclusion

The related literature is unclear about whether herding behavior in cryptocurrencies is significant during specific informational events related to COVID-19 and to cyber-attacks. In this article, we provide an empirical analysis of herding behavior in the cryptocurrency markets while decomposing deviations into deviations due to fundamental and deviations due to nonfundamental information. Results show significant fundamental herding during the full sample period and the cyber-attack days, which leads to efficiency (Bikhchandani & Sharma, 2000) in the cryptocurrency markets. Therefore, investors behave similarly in response to fundamental information during cyber-attack days, suggesting that cyber-attack events matter to investors and contain information that affects investor behavior and their future preferences. This evidence is not surprising given that the cryptocurrency markets are shaped by security issues and technological development related to blockchain technology. However, further analysis shows no evidence of significant fundamental or nonfundamental herding behavior during the COVID-19 outbreak, suggesting that investors behave heterogeneously in cryptocurrency markets during this unprecedented pandemic period. It seems that crypto-traders believe that the cryptocurrency markets, which are detached from the global financial system, will be relatively unaffected by the COVID-19 uncertainty. Accordingly, crypto-traders exhibit heterogenous behavior regarding whether they should cash out or remain invested, which has led to insignificant herding.

Our results matter to portfolio managers and have implications that involve both theory and empirical study. Theoretical herding models could benefit from our new evidence that crypto-traders spuriously copy each other’s actions during cyber-attacks, whereas the COVID-19 outbreak does not provide significant information to induce herding. These findings deserve further investigation in the spirit of Philippas et al. (2020). As argued by Bikhchandani and Sharma (2000), the lack of nonfundamental herding does not jeopardize the fragility of markets. Therefore, crypto-traders can herd for various reasons, independent of global uncertainty. This seems to be a feature of cryptocurrency markets, which requires future studies on equity markets. Further studies can consider how COVID-19 and cyber-attacks have shaped the dynamics of return and volatility across cryptocurrencies. This can be done using high-frequency data.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Availability of Data and Materials

Data will be available from the authors upon request.