Abstract

In recent years, online consumer credit in China has boomed. Many Chinese undergraduates are interested in utilizing online consumer credit to meet their increasing consumption needs. However, the explosion in online loans to students has created many problems. Based on a survey of 286 undergraduate students from four universities in Beijing, the capital of China, this study provides an empirical analysis of the economic and social determinants of undergraduates’ consumer credit. The estimation results indicate that online consumer credit demand is positively related to years of schooling, monthly living expenses, financial support from the student’s university, and consumption preferences. However, other factors, including major field of study, highest level of parental education, and advertisements in the media and on campus, have negative influences on undergraduates’ online consumer credit. The findings have significant practical and policy implications. Specifically, it is necessary and important for the government, universities, and families to coordinate to guide and educate college students to utilize online loans properly and wisely.

Introduction

With the country’s rapid economic development, fashionable consumption concepts have been widely adopted as Chinese people’s living standards have increased. For instance, credit card use has flourished because credit cards enable people to combine credit and consumption. As shown in Figure 1, the balance of credit consumption in China was 19 trillion RMB in 2015, which represented an increase of approximately 153% from 2010. Because university students have substantial consumption potential and quickly accept new things, commercial banks and various financial institutions have focused on college students as a key target for their consumer credit business. In 2004, China’s banking system began to issue credit cards to college students. However, in 2009, because of high rates of nonperforming loans caused in part by cutthroat competition among banks, the China Banking Regulatory Commission suspended the issuance of commercial bank credit cards to college students. In recent years, however, online credit platforms aimed at college students have filled this gap. It is very simple to utilize an online credit platform to make a purchase: Upon registration with the platform, students immediately receive credit, which they repay in installments. 1

Consumer credit balances (left scale) and corresponding growth rates (right scale), 2000-2015.

One of the most important advantages of online consumer credit is that it is easy to obtain. However, the convenience of applying and the lack of relevant regulations have caused both problems and abuse. In recent years, appalling incidents related to the granting of credit to undergraduates have occurred, triggering broad concerns and doubts about online consumer credit. 2 For instance, most college students do not have a stable income, which calls their repayment ability into question. Moreover, once they cannot repay a loan on time, college students are likely to engage in extreme behaviors, endangering both themselves and the public. In addition, college students tend to consume impulsively, which poses risks to both themselves and to the online credit platforms. In 2016, the Ministry of Education and the China Banking Regulatory Commission jointly issued a notice emphasizing the necessity of not only strengthening the supervision and reform of online credit platforms for college students but also educating and guiding students to help them establish rational and healthy consumption attitudes. 3 Undergraduates are relatively more likely to lose control of themselves with respect to credit because they have immature minds, little social experience, and limited purchasing power. Therefore, to further regulate online credit platforms and guide undergraduates to use credit rationally, it is necessary to analyze the factors that influence consumer credit demand among undergraduates.

Some studies have investigated the factors that influence college students’ consuming behavior (especially online shopping) and their attitudes toward consumer credit (e.g., Barboza, 2018; Jiang & Dunn, 2013; Oksanen, Aaltonen, Majamaa, & Rantala, 2017; Pinto et al., 2004; J. Wang & Xiao, 2009). Young people are aware of the two aspects of credit. Furthermore, personal factors such as education level, number of credit cards, and level of credit knowledge have significantly positive impacts on young people’s credit attitudes (Lachance, 2012). In addition, the frequency of use of credit cards can affect attitudes toward credit by influencing expectations of a personal financial crisis (Pinto, Mansfield, & Parente, 2004). Moreover, external factors such as family communication, a consumer society, and the media can affect credit attitudes (Pinto et al., 2004). Credit card holders tend to have positive attitudes toward credit because of their greater familiarity and lower anxiety about online shopping (Kiyici, 2012). Chinese college students are less knowledgeable about credit cards than U.S. students and are unable to distinguish between credit and debit cards. With the transformation of China into a market economy, it is unclear whether Chinese students will change their attitudes toward credit cards (Norvilitis & Mao, 2013). Younger consumers are found to tend to borrow more heavily and repay at lower rates than older generations. The accumulation of credit card debt is found to continue for the whole life cycle (Jiang & Dunn, 2013). The influence of parents on children’s consumption behavior and credit consumption attitude is also remarkable (Oksanen et al., 2017). Financial literacy may influence undergraduates’ money management behavior, as well as how undergraduates respond to economic, social, and psychological aspects relating to money management behavior (Bamforth, Jebarajakirthy, & Geursen, 2017). Using a sample of 380 college students, Barboza (2018) provided empirical support to the hypothesis that individuals with relatively high present-biased preferences tend to adopt a strategic procrastination repayment behavior that is not optimal to accomplish repayment in full amount. Numerous studies have shown that college students have relatively high credit risks because many college students are not yet prepared to use credit or pay in a timely manner (e.g., Singh, Rylander, & Mims, 2018). Age is an important influential factor of people’s consuming behavior and their attitudes toward consumer credit (Nai, Liu, Wang, & Dong, 2018). Besides, anxiety and power prestige have a significant effect on consumers’ compulsive buying behavior, which may be further strengthened by credit card usage (Ariffin, Richardson, Wahid, & Yusoff, 2018).

Some studies have investigated the relationship between online buying behavior and demand for credit card (e.g., Basnet & Donou-Adonsou, 2016; Liébana-Cabanillas, Marinkovic, de Luna, & Kalinic, 2018; Zhu, 2016). The majority of these studies have found evidence that online shopping promotes the demand for credit card. The application of Internet technology and the popularity of mobile payment methods have facilitated people to make online shopping and use the credit cards more frequently. (Liébana-Cabanillas et al., 2018). With the advancement and application of Internet technology, Internet consumer financial products have gradually emerged and maintained a good momentum of development. The popularity of online shopping has stimulated the rapid demand for online credit platforms such as Alibaba’s “Just buy” (Ma & Lu, 2018). The wide application of Internet technology and the booming of e-commerce platforms have made online shopping increasingly popular, and more online shopping has promoted the credit consumption needs of college students. Although Chinese college students are generally unable to obtain standard consumer credit based on credit, they can still obtain credit consumption services in the form of online shopping. (Zhu, 2016). Basnet and Donou-Adonsou (2016) found that the households with Internet access have more active attitudes toward maintaining larger credit card balances. Having access to the Internet increases the probability of carrying a positive credit card balance compared with those who do not. They also found that Internet access has a positive effect on credit card balances, which suggests that consumers with Internet access are prone to higher balances.

Some studies have explored the factors that influence university students’ credit card debt (e.g., Friedline, West, Rosell, Serido, & Shim, 2017; LaRose & Eastin, 2002; Limbu, 2017; Serido et al., 2015; J. Wang & Xiao, 2009). On one hand, buying behavior makes a significant contribution to credit card debt, especially among university students. Compulsive buying behavior has a significantly positive effect on credit card debt among university students, while impulsive buying behavior may also have a positive impact (J. Wang & Xiao, 2009). In addition, repeated buying behavior can lead to excessive consumption among university students (LaRose & Eastin, 2002). With respect to external impacts, parents’ financial behavior directly affects young adults’ financial behavior, and friends’ and lovers’ financial behavior can also have an effect (Serido et al., 2015). On the other hand, financial capacity can also affect credit card debt. A financial capacity index shows that people aged 18 to 24 possess lower financial capacity, which refers to objective financial knowledge, subjective financial knowledge, financially desirable behavior, and conscious financial capacity (Xiao, Chen, & Sun, 2015). Students with credit cards from on-campus solicitation had relatively higher debt-to-income ratios. Personality features may affect the attitudes toward money, but they are not closely related to debt levels. Many lenders require students to provide information about their credit and debt, which suggests that understanding financial issues may be an important factor that influences college students’ credit consumption (Norvilitis, Szablicki, & Wilson, 2003). In a follow-up study, Norvilitis et al. (2006) found that the lack of financial knowledge, age, delay of gratification, number of credit cards, and attitudes toward credit card use were related to debt. Individual characteristics (e.g., race and financial independence) and familial characteristics (e.g., their parents’ income and parents’ discussions of financial matters while growing up at home) were associated with a young adult college student’s acquisition and accumulation of credit card debt (Friedline et al., 2017). In a more recent study, Limbu (2017) found that knowledge about credit card and social motivation were inversely associated with credit card misuse mediated through credit card self-efficacy. Similarly, Brougham, Jacobs, Lawson, Hershey, and Trujillo (2011) found that college students are at high risk of becoming compulsive buyers because their relatively limited financial knowledge and current-oriented view of time often make them less responsible for repaying their debts.

The extant studies have conducted relatively comprehensive and in-depth analyses of the factors that influence attitudes toward consumer credit and the influence of buying behavior or financial capacity on credit card debt in Western countries. However, there have been few studies on Chinese undergraduates’ consumer credit demand. Therefore, this study makes the first attempt to systematically investigate the determinants of Chinese undergraduates’ consumer credit demand. This is the study’s primary contribution. A logit model is utilized as the benchmark estimation method for the binary dependent variable. The use of the proper empirical method ensures that the estimation results are both reasonable and reliable.

The remainder of this article is organized as follows. Section “Estimation Method” briefly explains our estimation method. Section “Data” introduces the data utilized in this study. Section “Empirical Analysis” describes the estimation results and provides a corresponding discussion. Section “Conclusions and Implications” concludes the study and offers policy implications.

Estimation Method

This article uses a logit model to analyze the influence of undergraduates’ individual characteristics, family characteristics, personal preferences, and other factors on their consumer credit demand.

A logit model is an extension of the ordinary multiple linear regression model that solves the problem that the Z value calculated using a linear discriminant model can only be used for judgment and cannot be intuitively explained. A logit model uses the maximum likelihood estimation method to estimate the parameters. It is suitable for the study of a dependent variable as a binary classification and does not require the sample data to be normally distributed, which is consistent with the distribution characteristics of the sample data in this article.

A logit model is used to examine the factors that influence undergraduates’ consumer credit. The basic form of the model is as follows:

In this formula,

Data

Sample

The data used in this article come from a May 2016 consumer credit survey conducted at four universities: Renmin University of China, Central University for Nationalities, Beijing Institute of Technology, and Beijing Foreign Studies University. The main reason for choosing these four universities is that they are of remarkably high quality and represent the most elite Chinese academic universities in the humanities and social sciences, the natural sciences and engineering, and ethnic and foreign language studies. All students who use online credit platforms are considered to have potential consumer credit demand.

To make the sample more representative, the researchers adopted random sampling to select 80 students as participants from each university. In this article, 286 valid questionnaires were obtained: 67 from Renmin University of China, 73 from Central University for Nationalities, 76 from Beijing Institute of Technology, and 70 from Beijing Foreign Studies University. 4 In this sample, 30 undergraduates have been using an online credit platform.

Questionnaire

The questionnaire is divided into two parts. The first part of the survey probes the use of online credit platforms, learning channels, and personal preferences, asking whether the informants have used online credit platforms, their consumption preferences, their repayment period preferences, and so on.

The second part primarily asks about the participants’ individual and family characteristics. The individual characteristics include gender, grade, major, and monthly living expenses and their sources. The family characteristics include family address and parents’ highest level of academic qualification. The questionnaire is included in the appendix.

Basic Situation of the Sample

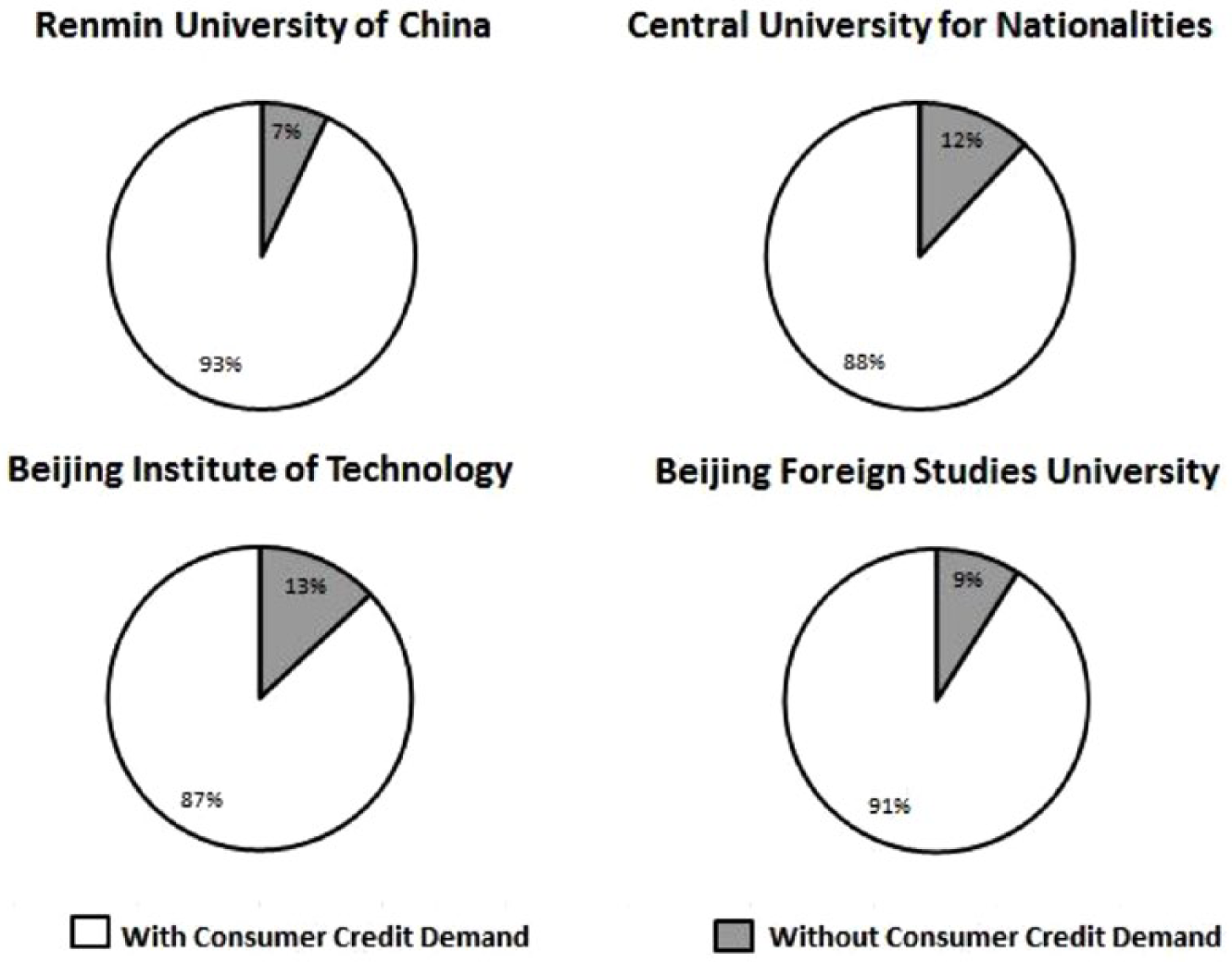

Of the 286 undergraduates surveyed, 30 undergraduates indicated that they had consumer credit, accounting for 10.49% of the overall sample. Among them, five students are from Renmin University of China, accounting for 7.46% of that school’s sample; nine students are from Central University for Nationalities, accounting for 12.33% of that school’s sample; 10 students are from Beijing Institute of Technology, accounting for 13.16% of that school’s sample; and six students are from Beijing Foreign Studies University, accounting for 8.57% of that school’s sample. This shows that only a small number of undergraduates have consumer credit.

Basic information about the sample is shown in Figure 2.

Consumer credit demand at four universities.

Of the 30 undergraduates with consumer credit, 12 students elected to repay the money using the “interest-free within 30 days” method, five students selected repayment in three installments, four students selected repayment in six installments, and nine students selected repayment in nine installments or above. The detailed information is shown in Figure 3.

Number of installments chosen by the students using online credit platforms.

Variable Definitions

The dependent variable

The dependent variable is whether undergraduates have consumer credit demand (yes = 1; no = 0). This article uses questionnaires to obtain information about undergraduates’ consumer credit demand and whether undergraduates have used online credit platforms to judge whether they have consumer credit demand. This article uses a logit model to analyze the factors that influence undergraduates’ consumer credit demand.

Independent variables

Based on the existing research, this article assumes that individual characteristics, family characteristics, personal preferences, and other factors may affect consumer credit demand.

According to the literature review, there are some important factors that influence undergraduates’ consumer credit demand, such as individual characteristics, family characteristics, individual preferences (e.g., present-biased preferences or otherwise), and the type of platforms. Therefore, following relative existent literature and considering the research focus of this study, the appropriate independent variables are selected. The names and definitions of the variables used in this study are reported in Table 1.

Definitions of Variables.

Note. * means that the respondents can choose more than one answer relating to that question.

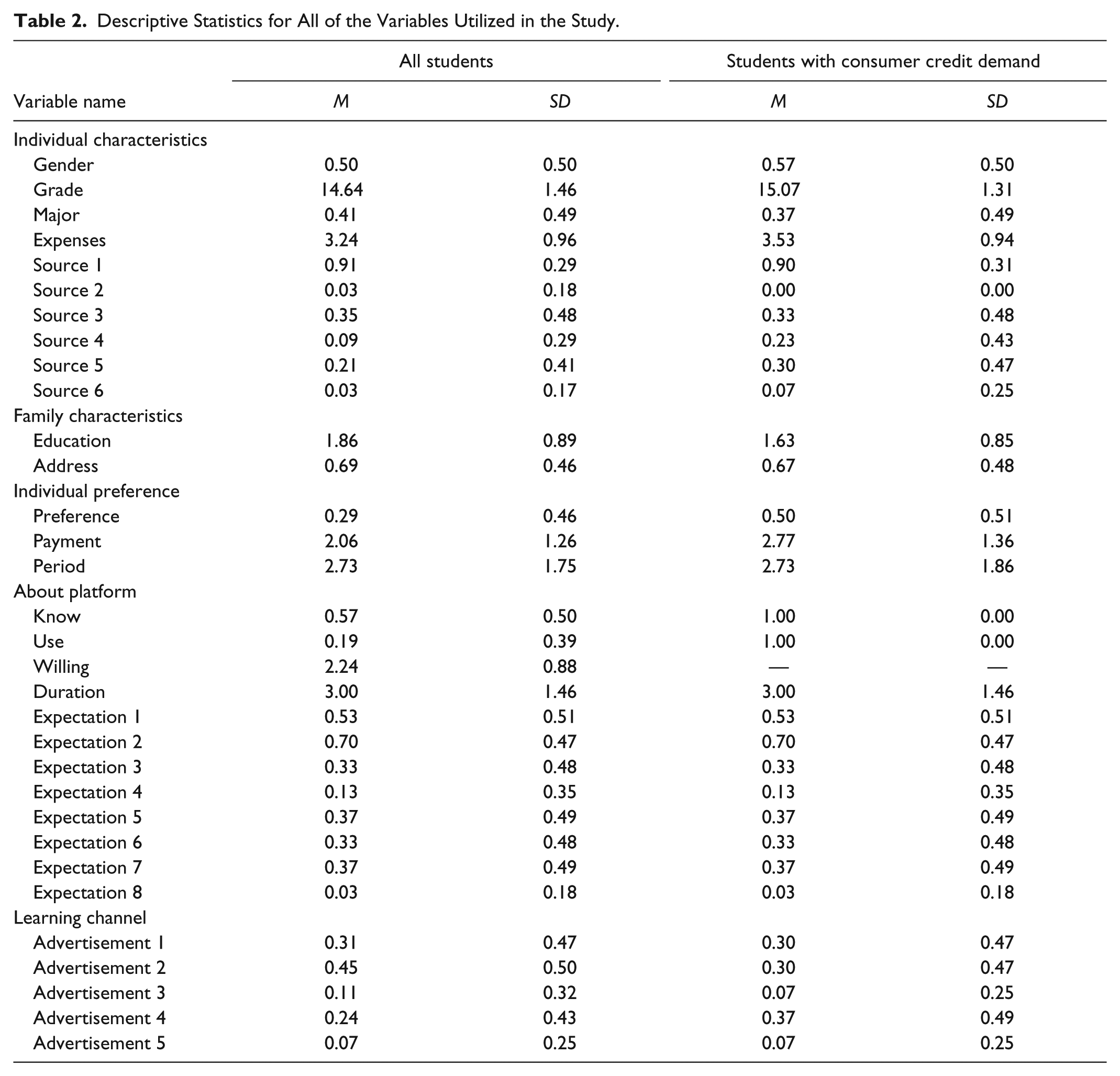

It is noteworthy that the respondents with consumer credit have relatively higher mean values on personal preferences (preferences regarding consumption patterns and preferred installment amount in each period), learning channels (Advertisement 4—peers), and individual characteristics (Expenses, Gender, Grade, and Source 5—part-time jobs), but especially on personal preferences. This may be caused by undergraduates who prefer a “one-time payment for low-price goods, installment payments for high-price goods,” and higher installment amounts for each period, as they may have higher consumption levels and a higher demand for capital, which are more likely to lead to consumer credit demand.

The descriptive statistics of the variables are shown in Table 2.

Descriptive Statistics for All of the Variables Utilized in the Study.

Empirical Analysis

Before the regression analysis was conducted, the sample was divided into two groups according to whether the informants reported consumer credit demand.

There are 162 respondents out of the 286 valid questionnaires who said they have heard or used at least one credit consumption platform. Because the purpose of this study is to investigate the possible determinants for the students who will use these credit consumption platforms on the condition that they know the existence of online credit platforms, these 162 students are the focus of the empirical analysis. The t-test results are presented in Table 3. Students with consumer credit demand have significantly higher mean values on the individual characteristic variables, including Grade, Expenses, and Source 4—difficulty subsidies. Similarly, there is a high degree of significance in the intergroup test of the consumption preferences (Preference) and the preferred installment amount in each period (Payment) among personal preferences. In the learning channel group, Learning Channel Variable 2—campus poster (Advertisement 2) and Learning Channel Variable 4—peers (Advertisement 4) are also significant.

Univariate Analysis of Subgroups for the Students Who Have Heard or Used Online Credit Platforms.

Note. The null hypothesis is there is no significant difference in the mean value between the two groups of data.

Significance at 10% levels. **Significance at 5% levels. ***Significance at 1% levels.

The results of the logit models are shown in Table 4. 5

Estimation Results for the Logit Model.

Note. The coefficients are based on logit model. Standard errors are in parentheses. AIC = Akaike information criterion.

Significance at 10% levels. **Significance at 5% levels. ***Significance at 1% levels.

Before analyzing the results of the model, it should be noted that there is no single statistics or indicator that could measure the goodness of fit of the logit model. It is also noteworthy that the conventional R2 for ordinary least squares (OLS) model is not available for the logit model. Therefore, following the suggestions of Wooldridge (2016), the percentage correctly predicted and a series of pseudo-R2 (e.g.,

Model 1 examines the impact of the individual characteristic variables on undergraduates’ consumer credit needs.

In the regression results, the coefficient of Grade is positive and significant (β = 0.288; p < .1), indicating that the higher a student’s grade, the more likely he or she is to have consumer credit demand. On one hand, this may be because upperclassmen pressured by the prospect of postgraduate entrance exams and employment spend more on the required learning materials, remedial classes, daily communication, and employment expenses. This result is consistent with B. Z. Wang, Zhang, and Zhang’s (2007) study of college students’ consumption psychology. On the other hand, upperclass students’ higher consumer credit demand may be caused by their participation in an established social network and need to spend money on social interaction. The study by Sotiropoulos and d’Astous (2012) shows that the higher a young person’s social intensity, the greater the probability of the student having credit card overdrafts.

The regression coefficient of monthly living expenses (Expenses) is positive and significant (β = 0.539; p < .05), indicating that the higher a student’s monthly living expenses, the more likely he or she is to have demand for consumer credit. In general, the higher a student’s monthly living expenses, the higher their level of consumption (e.g., they are more likely to purchase expensive 3C [computer, communication, consumer electronics] products). Online credit platforms for students currently provide expensive 3C products and consumer credit, thus satisfying undergraduates’ consumer credit demand. Therefore, the higher a student’s monthly cost of living, the more likely he or she is to have consumer credit demand. However, Kiyici (2012) found that the higher a college student’s income, the more likely he or she is to be familiar with online networks and the more he or she will recognize the convenience of online shopping; thus, such students are more willing to buy goods online, thereby increasing their consumer credit demand.

The regression coefficient of Source 4—difficulty subsidies—is positive and significant (β = 2.408; p < .01), indicating that students who receive difficulty subsidies are more likely to have consumer credit demand. This may be because students who receive difficulty subsidies cannot afford a one-time payment for a high-priced product and therefore have consumer credit demand. With respect to the results indicating “the higher the cost of living, the higher the consumer credit demand,” we conclude that undergraduates’ consumer credit demand shows a polarization trend, that is, undergraduates with higher or lower-than-average living costs are more likely to have consumer credit demand. The former group of students is focused on high-end products, whereas the latter concentrates on learning materials. This conclusion is supported by B. Z. Wang et al. (2007), who found that students with poor family conditions reduce not only their costs of learning materials but also their costs of communication.

Model 2 examines the impact of family characteristics and personal preference on undergraduates’ consumer credit demand.

Parents’ highest academic qualification has a negative and significant (β = −0.518; p<.1) influence on undergraduates’ consumption demand, possibly because parents with high academic qualifications tend to be conservative and risk averse when educating their children about finances. Nevertheless, because consumer credit has a certain degree of risk, these undergraduates’ consumer credit demand is relatively low. Sotiropoulos and d’Astous (2012) found that if parents emphasized the importance of financial responsibility, undergraduates are less likely to use credit cards. Thus, the higher the highest parental academic qualification, the more inclined parents are to teach their children about financial responsibility, resulting in reduced consumer credit needs. Cheng et al. (2011) found that of college students who have received reasonable financial education from their families, more than 90% engage in realistic consumer behavior, and 81% of the students in that group strictly implement a budget based on their cost of living. This conclusion contradicts the results of the model analysis, perhaps because installment platforms grew dramatically in 2014, stimulating undergraduates’ potential demand for consumer credit.

The regression coefficient of undergraduates’ consumption preferences (Preference) is positive and significant (β = 1.187; p < .01). This shows that undergraduates who prefer to make a “one-time payment for low-price goods, installment payments for high-priced goods” are more likely to have consumer credit demand. This may be because students who indicate that they “prefer a one-time payment regardless of price” are not accustomed to the consume-first-pay-last system and do not want to understand or try this consumption pattern. Overall, those who prefer to make a “one-time payment for low-price goods, installment payment for high-price goods” are unlikely to have consumer credit demand. In contrast, undergraduates who prefer to make a “one-time payment for low-price goods, installment payments for high-priced goods” may be able to understand and try online credit platforms. In other words, such students have higher consumer credit demand. Oosterbeek and van den Broek (2009) confirmed that loan aversion is a major factor in deciding whether a student is willing to obtain a loan.

Model 3 examines the impact of the learning channel variable on undergraduates’ consumer credit demand. The corresponding details about the main learning channels of the undergraduates are shown in Figure 4.

Main learning channels about online credit platforms.

The coefficient of the learning channel variable Advertisement 2—campus poster is negative and significant (β = −1.088; p < .05). This shows that undergraduates have negative attitudes toward campus posters. Perhaps because there are both reliable and unreliable posters on campus, undergraduates do not trust them. In addition, Zeng (2011) showed that compared with traditional marketing methods such as campus posters, college students are more receptive to Internet marketing. Therefore, to enhance the learning channel effect, enterprises should innovate in their propaganda methods.

Model 4 combines all of the variables in the three models above to determine the impact on consumer credit demand.

The results indicate that except for the differences in the degree of significance for the estimated coefficients of two variables in the two models, the other variables were significant. In other words, although the student’s Major and the learning channel variable Advertisement 3—media are not significant in Models 1 and 3, they are significant in Model 4. On one hand, adding more control variables leads to changes in the significance of some of the variables; on the other hand, this reflects that the models are stable.

Students’ Major has a negative effect on undergraduates’ demand for consumer credit, and the coefficient is significant (β = −1.004; p < .1), which indicates that science students are more likely to have consumer credit demand than literature students. This may be because students majoring in science not only pay higher tuition but must also spend more on learning materials. In addition, science students have a heavier academic burden and have little time for part-time employment. Therefore, science students are more likely to have consumer credit demand. This result may also be attributable to gender differences in willingness to consume on the Internet: More than 70% of the science students are males, who are more likely to consume online (Kiyici, 2012) because of their greater familiarity with online consumption, so they are more likely to have consumer credit needs.

The coefficient of the learning channel variable Advertisement 3—media is negative and significant (β = −2.971; p < .01). This result shows that students who learn about online credit platforms from the media are less likely to have consumer credit demand because there is abundant negative news and opinions about these platforms, leading to lower demand for consumer credit. Pinto et al. (2004) confirmed that the media significantly influences undergraduates’ attitudes toward using credit cards.

Model 5 only examines the impact of the significant variables in Model 4 on undergraduates’ consumer credit demand.

Although students’ Grade and Major are no longer significant in Model 5, Expense 4, Source 4—difficulty subsidies, Education, Preference, Advertisement 2—campus posters, and Advertisement 3—media remain important factors in establishing consumer credit demand.

Conclusions and Implications

This article conducts a quantitative analysis of the factors driving undergraduates’ consumer credit demand. The results show that (a) Grade, Expense, Source 4—difficulty subsidies, and Preference have positive impacts on undergraduates’ consumer credit demand, and (b) Major, Education, Advertisement 2—campus posters, and Advertisement 3—media have negative impacts on undergraduates’ consumer credit demand.

The following policy suggestions are based on the conclusions described above.

First, undergraduates do have demand for consumer credit, which is made accessible through online credit platforms. Therefore, the government should improve its regulations to guide the healthy development of this industry rather than ban it. China’s legal system and credit risk management system are not perfect and cannot provide a sufficient institutional guarantee for the development of undergraduates’ consumer credit. However, because undergraduates’ consumer credit is derivative of market demand and can play a positive role in innovation, prohibition of the industry would be unreasonable. In other words, it is the government’s duty to control the risk and recognize the positive effects of consumer credit for undergraduates through regulation of the legal system.

Second, universities, families, and society should be involved in improving the consumer education mechanism for undergraduates and helping students learn to control their consumer credit. Because of their limited purchasing ability, undergraduates possess weak credit consciousness and lack a conception of rational consumption. Therefore, financial education mechanisms should be improved to help them establish that conception. There are multiple dimensions of such financial education mechanisms, including schools, families, and society. Schools should cultivate students’ financial abilities by providing open financial classes and encouraging students to form mutual aid groups to increase their financial knowledge; families should provide consumer credit guidance, for example, by teaching children how to control their consumer credit and not comparing them with other children. Parents’ financial behavior has a direct impact on young people’s buying behavior, whereas parental financial education and motivation indirectly affect young people’s buying behavior by influencing their financial knowledge. Improving the financial participation of undergraduates and establishing a reasonable conception of consumer credit requires not only the dissemination of financial knowledge but also an increase in young people’s ability to cope with financial crises; thus, society should actively create a financial education atmosphere. Although financial education is a long process, it can help undergraduates establish appropriate attitudes toward consumption in their daily lives. This process requires governmental participation and support. At the same time, society should actively promote the rational dissemination of financial information.

Third, most undergraduates have negative attitudes toward campus posters, media reports, and other traditional learning channels. On the hand, enterprises should improve their existing methods of communication by, for example, improving the design of their websites, which can affect consumer sentiment and cognition, enhance consumer satisfaction, and increase consumer purchasing intentions. On the other hand, consumer credit platforms have developed rapidly in recent years. If enterprises want to survive in this highly competitive market, they must have a strong reputation. However, traditional advertising is becoming increasingly less attractive to undergraduates. Therefore, enterprises need to find new ways to communicate.

Although this study made primary research on the determinants of online consumer credit of Chinese university students, there are still some limitations remaining in this study. First, this study was conducted with the data collected from a relatively small sample of four universities in China’s capital city of Beijing and focused on undergraduates. Therefore, the findings may not be generalized to the whole population facilely. Future studies might benefit from including participants with various occupations and of different ages. Second, this study was conducted in China; therefore, some of the results are specific to China’s context. In this regard, the findings of the article cannot be generalized to all countries because China’s Political system, economic system, market organization, cultural practices, values, and family structure are still very different from the rest of the world. Least but not least, the econometric model in this article may be prone to endogeneity problem because there may be some potential variables ignored due to data unavailability or unobservable factors (e.g., a college student’s personality). These limitations could be addressed in future follow-up studies.

Footnotes

Appendix

Acknowledgements

The authors acknowledge the financial support from the National Natural Science Foundation of China (Award Number: 71761137001, 71403015, 71521002), the key research program of Beijing Social Science Foundation (Award Number: 17JDYJA009), and Joint Development Program of Beijing Municipal Commission of Education. The authors are also very grateful to two anonymous reviewers and Editor Prof. Dr. Suzanna ElMassah for their insightful comments that help us sufficiently improve the quality of this article. The usual disclaimer applies.

Authors’ Note

Y.H. and S.L. contributed equally to this study and share first authorship.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study was supported by the National Natural Science Foundation of China (Award Number: 71761137001, 71403015, 71521002), the key research program of Beijing Social Science Foundation (Award Number: 17JDYJA009), and the Special Fund for Joint Development Program of Beijing Municipal Commission of Education.