Abstract

We compare the hedging, safe-haven, and diversification potential of gold and Bitcoin for different investment styles and industry portfolios in the United States. We find that gold is at least a weak hedge for the style and industry portfolios except for utilities, energy, and telecom. The hedging potential of gold is comparatively higher for large-cap portfolios, whereas Bitcoin offers minimal hedging effectiveness. However, Bitcoin shows hedging potential for the noncyclical industries. Although investors need a higher amount of investment to hedge the downside risk using gold, it still is a superior hedging instrument compared with Bitcoin. Finally, the analysis using the conditional diversification approach shows that gold is a superior and stable diversifier for style and industry portfolios. Overall, our findings provide evidence of superior safe-haven and hedging potential of gold over Bitcoin.

Introduction

In this study, we compare the hedging, safe-haven, and diversification potential of gold and Bitcoin for various investment styles and industry portfolios. The hedging effectiveness of gold against economic downturns, in general, and other financial assets, in particular, is both historically and empirically well-recognized. Much of the empirical evidence also confirms the hedging ability of gold for stock markets (Baur & Lucey, 2010; Baur & McDermott, 2010). In recent years, however, particularly in the aftermath of the global financial crisis (GFC), the hedging and safe-haven properties of gold have diminished (Baur & Glover, 2012; and Baur & McDermott, 2016). Luckily, over the same time, Bitcoin emerged as an alternative safe-haven asset with a consistent display of this character during the European debt crisis of 2010–2013. Consequently, Bitcoin has attracted a great deal of scholarly attention recently (see Corbet et al., 2019; Demir et al., 2018 for a comprehensive review). Often found as weakly linked with most other financial assets, Bitcoin exhibits an extremely low correlation with the stock market, and positive co-movement with gold Naeem et al. (2020), thereby offering a wide range of opportunities for hedging and diversification (Baur, Hong, & Lee, 2018 and Guesmi et al., 2019). It is due to those attractive benefits of Bitcoin that even the financial press has started comparing the merits of Bitcoin and gold for financial markets, especially the stock market (Forbes, February 13, 2018).

As we will emphasize in section “Extant Literature on Gold, Bitcoin, and Stock Markets” shortly, gold and Bitcoin have several features in common, which make them comparable hedge assets. Motivated by this comparability, some recent studies have begun to compare gold with Bitcoin with regard to their hedging potential for stock markets (Kajtazi & Moro, 2019; Klein et al., 2018; Shahzad et al., 2019, 2020). Although the studies provide evidence of differences between the two assets, most of this incipient evidence exists on an aggregate (market-wide) level of the stock market only, which, despite being relevant, offers little knowledge about the two sublevels of the stock market. First, the broad-market-based studies have hardly paid any attention to the fact that market aggregation tends to mask the characteristics of various industries. The aggregate stock market index—being an orthodox proxy of the benchmark portfolio—serves only those investors who are concerned with the overall riskiness of the stock market and offers little help to those wanting to hedge or diversify the riskiness of their industry portfolio holdings. As industries are exposed to varying degrees of risks, their relationship with hedge and safe-haven assets, like gold and Bitcoin, may not be the same across all industries (Mohamed, 2012, among others). Any potential differences may be more evident for specific industries, such as technology and energy, which have unique connections with Bitcoin (Symitsi & Chalvatzis, 2018). Also, it is well-known that some industries are cyclical, while others are counter-cyclical. Some industries sell essential items, and others produce luxuries. Likewise, certain industries are more sensitive to inflation and other macro-financial factors than others (Naeem, Balli, et al., 2020). In other words, there is a great deal of heterogeneity across industries that could well be reflected in their relationship with Bitcoin and gold. One may, therefore, expect the hedge/safe-haven potential of gold and Bitcoin to be different across industries.

Second, and maybe even more important, is the fact that the previous studies seem to neglect the natural propensity of the equity investors to classify stocks into different categories. Literature suggests that investors do not necessarily mimic aggregate market portfolios, but rather tend to categorize stocks into broad classes like small/large stocks, value/growth stocks, and momentum stocks (Fama & French, 1995). Portfolios strategies thus formed are often known as investment styles, and the allocation of funds across investment styles is often called as style investing. Style investing has gained massive popularity recently as stock categorization does not just reduce the information complexity around equity investment decisions but also helps investors evaluate the performance of money managers more efficiently. Nevertheless, given this increased popularity, the empirical evidence also points to the risks associated with different investment styles due to their heterogeneous responses under different economic conditions, that is, in good and bad times (Arshanapalli et al., 2006).

The evidence suggests that some styles are more penalized (rewarded) than others by the market under certain economic conditions, which in turn leads institutional investors to seek risk diversification by creating style-diversified portfolios (Addoum et al., 2019) as well as hedging opportunities. This might happen because different types of investors follow different investment styles, even though hedging remains one of the main objectives of style investors (Cronqvist et al., 2015). Hence, given the prevalence of heterogeneity in both investment types and investors in style, it is crucial, as well as possible, that gold and Bitcoin demonstrate different hedging potential for different style portfolios. Furthermore, a portfolio level analysis that encompasses optimal portfolio weights, hedge ratios, and hedge effectiveness offers significant implications for devising risk management and diversification strategies. The economic benefits of hedging can be assessed by checking the hedging effectiveness through risk mitigation efficiency of the hedged versus the unhedged portfolios.

In this study, we examine the hedging, safe-haven, and diversification potential of gold and Bitcoin for equity styles and industry portfolios in the U.S. stock market. The fact that the U.S. market plays a dominant role among global equity markets and therefore draws a considerable amount of attention and capital flows from across the globe motivates us to analyze the market for this study. Our main objective is to draw a distinction between gold and Bitcoin from the portfolio management viewpoint by explicitly considering the style and industry portfolios as contrasted to the prior research in which aggregate stock market indices (market portfolios) are predominantly examined. Covering a period from May 1, 2013, to June 28, 2019, the data on a wide range of benchmark style portfolios and industry portfolios are obtained from Kenneth R. French - data library. The style portfolios have been constructed using size (small and big) and other attributes (book-to-market, investment, short- and long-term prior return, operating profit, and momentum) of the stocks. In our methodological approach, we follow three steps to examine the hedging, safe-haven, and diversification role of gold and Bitcoin for the investment styles and industry portfolios. First, we employ the Baur and McDermott (2010) model to assess the safe-haven and hedging potential of gold and Bitcoin. Second, we compare the hedging effectiveness of gold and Bitcoin by computing their hedge ratios. Finally, we follow the method proposed by Christoffersen et al. (2018) to analyze the conditional diversification benefits offered by each of these assets.

Our findings suggest that gold is at least a weak hedge for the style and industry portfolios, except utilities, energy, and telecom. In addition, the hedging potential of gold is more pronounced for large-cap style portfolios, whereas Bitcoin offers minimal hedging potential. However, Bitcoin’s hedging potential is more pronounced for noncyclical industries. Furthermore, the results of hedge effectiveness indicate that even though investors require a higher amount of investment to hedge the downside risk using gold, it still is a superior hedging instrument compared with Bitcoin. Finally, the analysis of conditional diversification benefit provides further evidence for gold being a superior and stable diversifier for style and industry portfolios.

The balance of the study unfolds as follows. section “Extant Literature on Gold, Bitcoin, and Stock Markets” summarizes related literature. Section “Method” elaborates methodology. Section “Data and Empirical Findings” details data and empirical findings. Section “Conclusion” offers concluding remarks.

Extant Literature on Gold, Bitcoin, and Stock Markets

In this section, we provide a brief overview of the related literature. As we aim to draw a comparison between gold and Bitcoin, a brief discussion on their comparable features is essential. Gold and Bitcoin share several features, including classification as a commodity, production process called mining, independence from central authority authorities, limited supply, hedging potential against inflation and equity market risk, positive return-volatility relationship, and, last but not least, inability to generate regular cash-flows. Although all these features are well-known for gold, they are not that well-documented for Bitcoin. The most critical of these features is the ability of Bitcoin and gold against stock market risk, inflation, and economic policy uncertainty (Baur & McDermott, 2016; and Demir et al., 2018). This ability is due to both assets being deflationary and having generally negative (or even zero) association with stocks. Also, Bitcoin is related only slightly to gold, and only for specific periods (Kristoufek, 2015). It may, therefore, be reasonable to examine Bitcoin and gold together and compare their hedging, safe-haven, and diversification features simultaneously.

From a comparative perspective, only a few attempts have been made in the extant literature. Bouoiyour et al. (2019), for instance, aim to draw a general comparison between Bitcoin and gold by asking whether the former could ever equal or even overtake the latter as a safe-haven asset, concluding that Bitcoin and gold are more likely to compliment than compete each other. Through looking at stock markets, Klein et al. (2018) find that gold and Bitcoin present fundamentally distinct features as assets as well as in terms of their stock market linkages. With particular attention to the stock market, Shahzad et al. (2019) examine the safe-haven properties of gold, general commodity index, and Bitcoin under extreme conditions. Their results suggest that while Bitcoin, gold, and the commodity index can be seen as poor safe-haven assets in some instances, their safe-haven potential is time-varying and market-specific. In more related work, Shahzad et al. (2020) investigate the hedging and safe-haven properties of Bitcoin and gold for G7 stock markets, pointing to the dominance of gold over Bitcoin as a safe-haven, hedge, and diversifier for G7 markets.

Most of the above-mentioned empirical studies look at the hedging and diversification possibilities of either Bitcoin or gold or both for stock markets but only consider aggregate (market-wide) stock indices. The studies pay little attention to the fact that market aggregation could well mask the characteristics of different industries in the stock market. As we pointed out earlier, the possibility of industry portfolios exhibiting their unique relationship with safe-haven assets is reasonably plausible. As this could also be the possibility for gold and Bitcoin, investigating the hedging (and safe-haven) potential of these two assets for industry portfolios can, therefore, improve our understanding of the cross-hedging and diversification possibilities available for investors interested in industry portfolios. Much like the limited evidence for industry portfolios, there is also scanter evidence about the hedging ability of gold and Bitcoin for style portfolios. To the best of our knowledge, the present research is the first to add to the ongoing debate on hedging opportunities around well-diversified portfolios, sector portfolios, and investment styles (Addoum et al., 2019; Bouri et al., 2020; Kajtazi & Moro, 2019). Overall, we move the existing literature on the gold-Bitcoin-stock nexus from the overall stock market level to the portfolio level, which, in our study, are formed based on industry and investment style.

Method

Our method consists of three steps. First, we examine the hedging and safe-haven potential of gold and Bitcoin for investment styles and industry portfolios in the United States by employing the model introduced by Baur and McDermott (2010). Second, we evaluate the hedging effectiveness of gold and Bitcoin for a given investment style (industry portfolio) via the out-of-sample setting. As the third and final step, we use the measure devised by Christoffersen et al. (2018) to compute the conditional diversification benefits (CDBs) of gold and Bitcoin for equity investors. What follows is a brief discussion of the methods adopted in the three-step approach.

Testing Hedge and Safe-Haven Properties

To uncover the hedging and safe-haven properties of gold and Bitcoin, we follow the Baur and McDermott (2010) approach, which allows for simultaneous estimation of the following three principle regression models:

Equation 1 relates the returns of Bitcoin (gold) to the returns of a given style (industry) portfolio.

Hedge Effectiveness

Next, we perform the out-of-sample hedging effectiveness of Bitcoin and gold for style (industry) portfolios, which enables us to compare the hedging ability of both assets. We do this by computing the hedge effectiveness of the hedged positions between Bitcoin (gold) and a given style (industry) portfolio and infer how much risk is reduced by the addition of Bitcoin (gold) in a combined portfolio. Such tools of portfolio risk assessment are commonly used by the research community.

Suppose

where

The computation of the hedge ratios come from the covariance and conditional-volatility estimation achieved through the AGDCC-GARCH model, which is the asymmetric generalized dynamic conditional correlation form of the generalized autoregressive conditional heteroscedasticity model. This model provides a robust analysis by investigating the second moments of correlations and covariance. This helps us to assess how well gold or Bitcoin can hedge the style (industry) portfolios. Thus, a long position in a style (industry) portfolios can be hedged with a short position in Bitcoin (gold) under the following specification:

where

In absolute terms, a higher

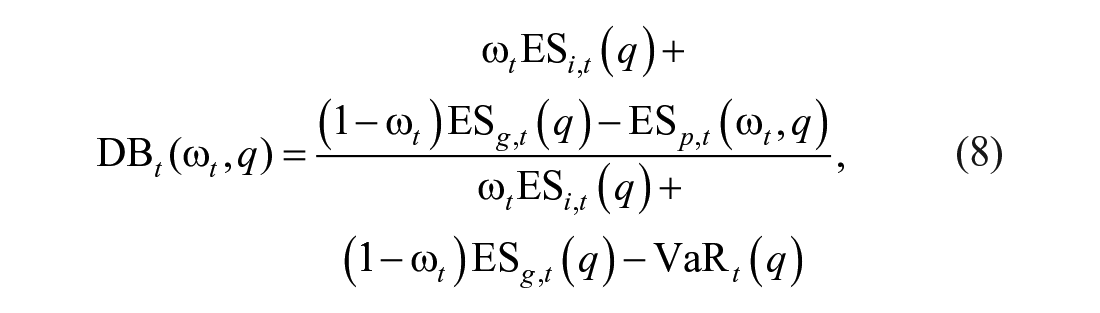

Diversification Benefit

Finally, we apply the CDB measure proposed by Christoffersen et al. (2018) to compute the diversification benefits arising from combining gold (Bitcoin) with each of the style (industry) portfolios. Measured as the potential shortfall for a probability q, CDB is given by:

where

where

As the value of diversification benefit depends on the composition of the combined portfolios as well as on the probability q, we calculate CDBs for various portfolio weights, which are based on two probability values, 5% and 50%, that correspond to the distribution values at the lower-extreme and at the median location, respectively. The ES can be written as:

where the cumulative distribution function is given by D and d utilizing the Student’s t density function with

Data and Empirical Findings

Data and Descriptive Statistics

The data set for this study comprises gold, Bitcoin, style portfolios, and industry portfolios’ prices. The price data for Bitcoin are taken from coinmarketcap.com, whereas gold prices are from Thomson Reuters Datastream International. We use style and industry portfolios’ data from Kenneth R. French - data library. The style portfolios are a composition of similar stocks combined to represent different investment styles. These style portfolios are constructed using market capitalization (small or big) and other stock attributes such as book-to-market (BM) ratio, investment, short- and long-term prior returns, operating profit, and momentum. Each style construction has six subportfolios divided into combinations of market capitalization and other attributes. For example, size and BM combination has six subportfolios as small-low BM, median-median BM, small- High BM, big-low BM, median-median BM, and big- Hi BM. Our choice of the study period spanning between May 1, 2013, and June 28, 2019, hinges on the fact that Bitcoin price remained consistently stable before the start of our sample period. From then on, however, Bitcoin’s price underwent substantial price fluctuations, thus making the price behavior more interesting to study over this period.

Table 1 presents descriptive statistics for data variables. In style portfolios, generally large-cap style (BIG) portfolios have higher returns as compared with small-cap (SMALL). Combinations of large-cap and higher investment (high long-term return reversal) portfolios exhibit the highest profits. These portfolios represent investors that are looking for stable returns in less risky investments. Conversely, small stock portfolios of long-term high return reversal and momentum have the lowest average return among all style portfolios. The small-cap portfolio combinations represent riskier investors interested in high growth investments.

Descriptive Statistics and Unit Root Test.

Note. JB = Jarque–Bera test of normality. ADF = augmented Dickey–Fuller test of stationarity. *** represents significance at 1%.

The volatility estimates of style portfolio returns show that small-cap portfolios are predominantly riskier than large-cap portfolios. Notably, small-cap style portfolios of growth, short-term return reversal, and momentum have the highest standard deviation. Conversely, large-cap portfolios of median investment and long-term return reversal have the lowest standard deviation. This observation corroborates the well-known evidence of Fama and French (1993), that small-cap stocks are riskier than large-cap investments.

Furthermore, Table 1 presents the summary statistics for industry portfolios. Hi-Tech (energy) industry portfolio has the highest (lowest) average return. In addition, the energy portfolio has the highest standard deviation, followed by durable goods, whereas a nondurable industry portfolio has the most moderate return variability. The return variability results indicate that the portfolios constructed using cyclical industry stocks are more volatile as compared with noncyclical industry portfolios. Finally, Table 1 presents the descriptive statistics for gold and Bitcoin. Expectedly, Bitcoin has the highest average return and standard deviation as compared with gold, industry and style portfolios. Conversely, gold returns are the lowest among all considered investments.

Although not reported to conserve space, the correlation results of gold, Bitcoin, style and industry portfolios. While gold has a negative correlation with all the style portfolio combinations, it is more pronounced with large-cap investments and otherwise, for small-cap portfolios. Similarly, all the industrial indices show a negative correlation with gold, excluding the energy industry. However, the positive relationship is present for Bitcoin with most of the style and industry portfolios, excluding manufacturing, telecom, energy, durable, and nondurable industries.

Safe-Havens and Hedging

The correlation results show, on average, gold (Bitcoin) is negatively (positively) correlated with style and industry portfolios. The existing evidence suggests that the correlation between total market and gold (Bitcoin) is asymmetric. Resultantly, it offers safe-haven and hedging opportunities (Baur, Dimpfl, & Kuck, 2018). We employ Baur and McDermott’s (2010) approach to estimate the association between gold (Bitcoin) and style (industry) portfolios when the later experience extreme negative returns. Consequently, we are interested in exploring the safe-haven and hedging potential of gold (Bitcoin) for style and industry portfolios.

Table 2 presents the results of the safe-haven and hedging potential of gold (Bitcoin) for investment styles and industry portfolios in Panels A and B, respectively. Primarily, the results show gold is at least a weak safe-haven and hedge for all investment styles and particularly for large-cap investments. The safe-haven and hedging potential of gold is strongest when large-cap investment style ties with stocks having higher growth characteristics such as higher investment, higher operating profits, and long-term return reversals. For example, large-cap investment portfolios with higher investment and operating profits receive greater protection from gold as compared with a small-cap investment portfolio with similar characteristics. Conversely, gold offers the weakest safe-haven and hedging potential when a stock characteristic such as lower investment, lower growth, short- and long-term return reversal combines with small-cap investment style.

The Estimation Results for the Role of Gold/Bitcoin as a Hedge and Safe-Haven Asset.

Note. *, **, and *** represent significance at 10%, 5%, and 1%, respectively.

However, Bitcoin does not show safe-haven and hedging potential for most of the style portfolios, excluding some large-cap investments. Like gold but to a lower magnitude, Bitcoin exhibits safe-haven potential for large-cap style investments having characteristics such as higher momentum, operating profit, and long- and short-term return reversal. In addition, Bitcoin is a weak hedge for portfolios with a higher long-term reversal and large-cap style.

Our findings of safe-haven and hedging potential of gold for large-cap style further corroborates the evidence reported by He et al. (2018). We draw this inference from the fact that the renowned market indices such as S&P500 are primarily considered the benchmark for large-cap investments. However, our findings for small-cap stocks add a new dimension to existing literature and question the substantial evidence on the safe-haven and hedging potential reported for overall market indices (Shahzad et al., 2020).

From the investors’ standpoint, our findings on safe-haven and hedging potential of gold (bitcoin) have two important implications for risk-seeking and risk-averse investors. First, gold offers higher protection to risk-averse investors in normal and volatile market conditions. This finding concords with Lean and Wong (2015) as they find risk-averse investors to benefit more by including gold in their portfolios compared with risk-seeking investors. Second, similar to gold, but to a lower degree, Bitcoin exhibits safe-haven and hedging potential for risk-averse investors. Thus, we offer new insights into the role of (Gold) Bitcoin as a hedging and safe investment for different investment styles.

Table 3 presents the results of safe-haven and hedging attributes of gold and Bitcoin for 10 industry portfolios in Panels A and B, respectively. Gold is a strong (weak) hedge for all industrial portfolios (energy and telecom), excluding the utilities. In addition, gold offers weak (strong) safe-haven potential for all industry portfolios (Shops), excluding energy and utilities. Similarly, Chen and Wang (2019) also report the non-safe-haven nature of gold for the utilities industry using the Dow Jones industry indices. It is worth mentioning that safe-haven and hedging potential of gold is more pronounced for cyclical industry portfolios such as shops, consumer durables, and manufacturing and less noticeable for noncyclical industry portfolios such as nondurables.

The Estimation Results for the Role of Gold/Bitcoin as a Hedge and Safe-Haven Asset for 10 Industry Portfolios.

Note. *, **, and *** represent significance at 10%, 5%, and 1%, respectively.

However, Bitcoin is a strong safe-haven and hedge only for the health industry. In addition, Bitcoin exhibits weak safe-haven potential for nondurable and utilities industry portfolio. Interestingly, Bitcoin only shows safe-haven and hedging potential for noncyclical industry portfolios, which is otherwise in case of gold. For example, in the case of utilities industry portfolios, Bitcoin shows the negative correlation in normal conditions, whereas gold does not possess such property.

Our findings concerning the ability of gold and bitcoin to protect cyclical and noncyclical industry portfolios differently provide novel evidence that can substantially improve portfolio managers’ hedging options. In addition, different industry portfolio investors can benefit from these findings by choosing the right hedging and safe-haven instrument for their industry portfolios.

Overall, gold presents both safe-haven and hedging potential for all style portfolios, and it turns out to be more pronounced for large-cap investments possessing higher growth characteristics. This hedging and safe- haven potential evidence is in line with Hou et al. (2019) and provides more extensive evidence for a large number of investment styles. Similarly, our results on the safe-haven and hedging potential of gold for industry portfolios complement the existing evidence (Beckmann et al., 2019). However, the Bitcoin results largely contradict existing evidence reported by Bouri et al. (2019) and support the views of Shahzad et al. (2020).

Hedging Effectiveness

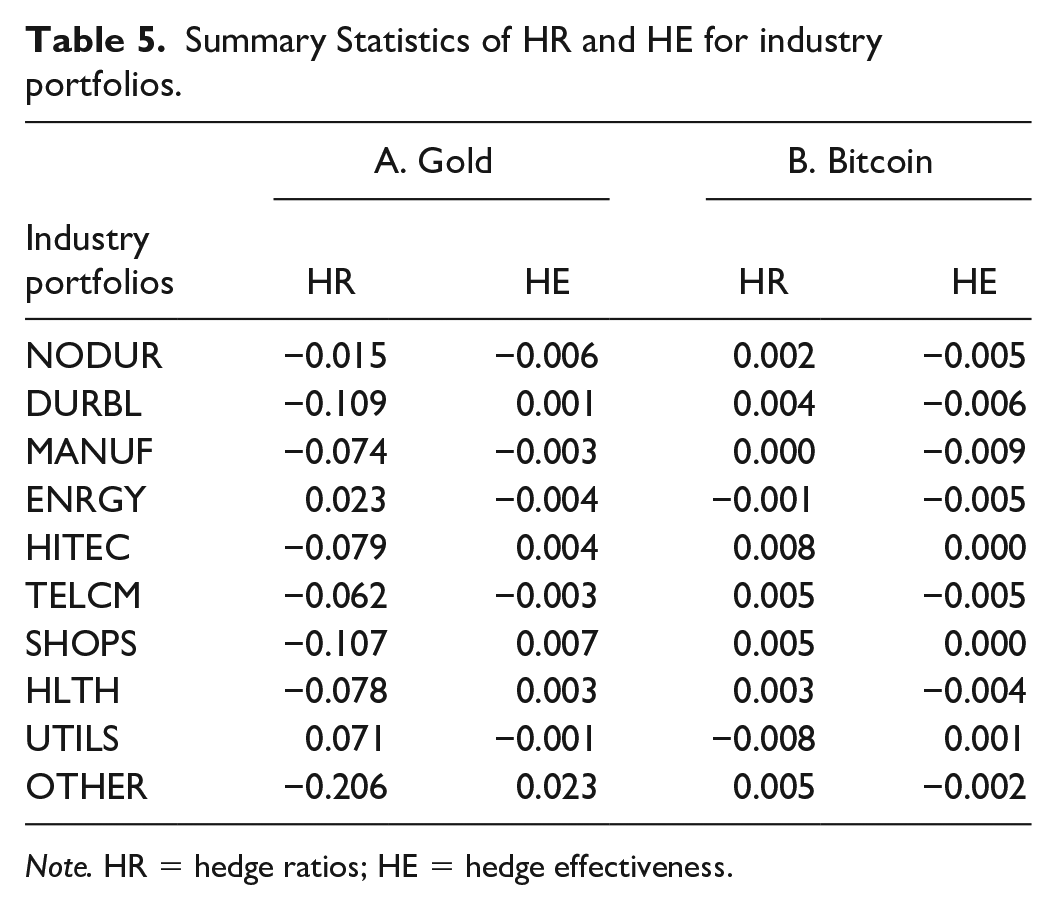

We further explore the hedging characteristic of gold (Bitcoin) by estimating hedge ratios (HR) and hedging effectiveness (HE) index. HE index measures the hedging effectiveness of an asset where higher values indicate higher efficiency and otherwise. Tables 4 and 5, Panel A and B, present HR and HE index results of gold and Bitcoin, respectively.

Summary Statistics of HR and HE.

Note. HR = hedge ratios; HE = hedge effectiveness.

Summary Statistics of HR and HE for industry portfolios.

Note. HR = hedge ratios; HE = hedge effectiveness.

We observe mostly negative hedging ratios of gold for style and industry portfolios that indicate hedge is formed by taking a long position in either assets (i.e., gold and portfolios). For example, a long position of US$1,000 in a small-cap growth portfolio is hedged by taking another long position of US$114 in gold. Conversely, positive and smaller mean hedge ratios for Bitcoin suggest investors can hedge style and industry portfolios by taking a smaller short position in Bitcoin as compared with gold. For instance, a US$1,000 long position in the nondurable industry is hedged by a US$4 short position in Bitcoin.

While, higher HE index scores for gold shows higher effectiveness of gold in most of the cases compared with Bitcoin, which confirms the evidence reported by (Shahzad et al., 2020). We also observe higher hedging effectiveness of Bitcoin for some style portfolios such as large-cap value and small-cap momentum styles. This finding again confirms the notation that style investing is different from index investments. Thus, portfolio managers should pay careful attention while using hedging instruments such as gold (Bitcoin).

Conditional Diversification Benefit

As the HE index estimates presented above are estimated under certain assumptions, we employ (Christoffersen et al., 2018) approach to check their robustness. The results do not change by varying the number of model refits and forecast span. Accordingly, to determine the diversification benefit in varying market conditions (turmoil and average), we calculate conditional diversification benefit (CDB) estimates for gold and Bitcoin that show diversification benefit at the extreme lower tails of style portfolios’ return distribution.

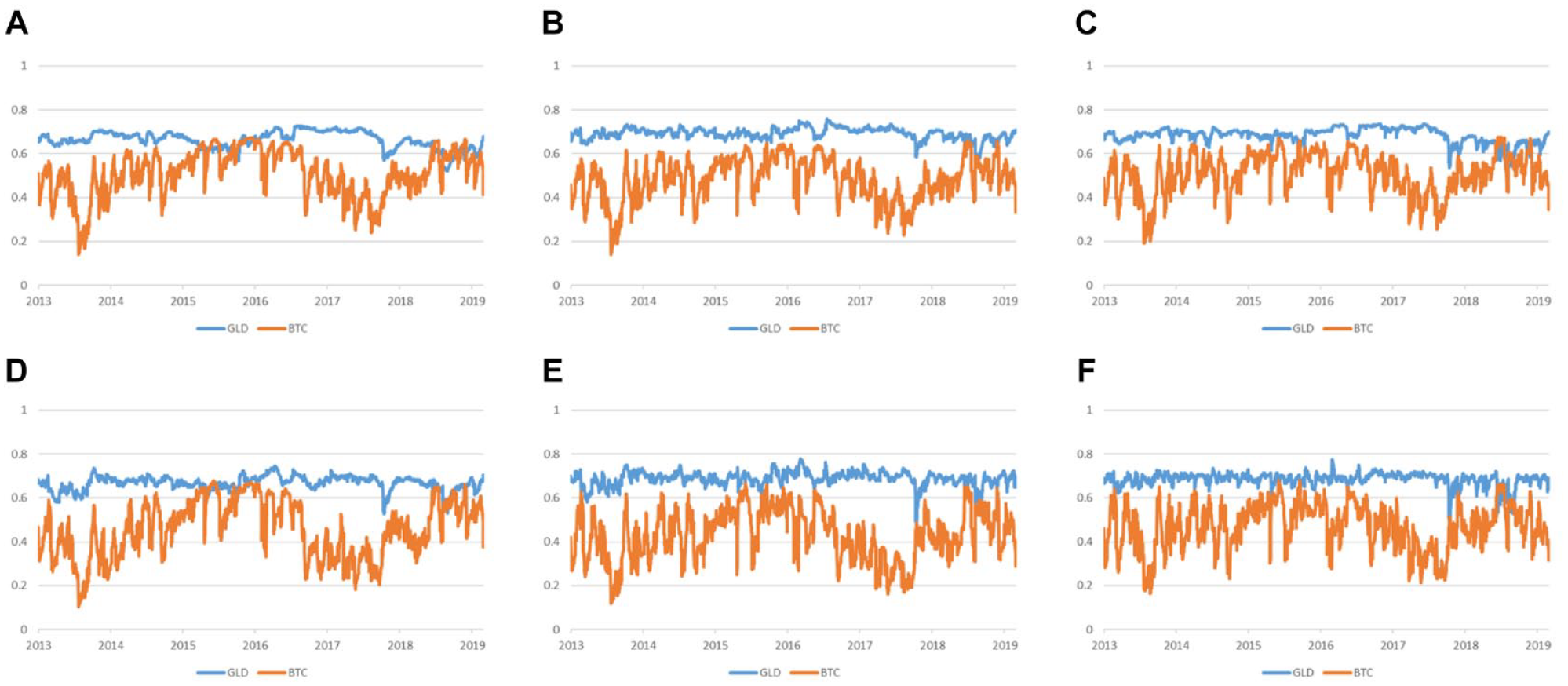

Figures 1 to 6 present the graphical representation of CDBs for style portfolios. Generally, we observe higher CDBs for gold as compared with Bitcoin for most of the style portfolios during the sample period. In addition, variability in CDB of Bitcoin is more distinct in the second quarters of 2014 and 2018. Similarly, significant dips can be seen in CDB of Bitcoin during the first, second, third, and fourth quarters of 2014, 2016, 2015, and 2017, respectively.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and book-to-market portfolios—equally weighted portfolios, 5% quantile: (A) Small LoBM, (B) ME1 BM2, (C) Small HiBM, (D) Big LoBM, (E) ME2 BM2, and (F) Big HiBM.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and investment portfolios—equally weighted portfolios, 5% quantile: (A) Small LoINV, (B) ME1 INV2, (C) Small HiINV, (D) Big LoINV, (E) ME2 INV2, and (F) Big HiINV.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and long-term reversal portfolios—equally weighted portfolios, 5% quantile: (A) SMALL LoPRIOR, (B) ME1 PRIOR2, (C) SMALL HiPRIOR, (D) BIG LoPRIOR, (E) ME2 PRIOR2, and (F) BIG HiPRIOR.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and short-term reversal portfolios—equally weighted portfolios, 5% quantile: (A) SMALL LoPRIOR, (B) ME1 PRIOR2, (C) SMALL HiPRIOR, (D) BIG LoPRIOR, (E) ME2 PRIOR2, and (F) BIG HiPRIOR.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and momentum portfolios—equally weighted portfolios, 5% quantile: (A) SMALL LoPRIOR, (B) ME1 PRIOR2, (C) SMALL HiPRIOR, (D) BIG LoPRIOR, (E) ME2 PRIOR2, and (F) BIG HiPRIOR.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and operating profit portfolios—equally weighted portfolios, 5% quantile: (A) Small LoOP, (B) ME1 OP2, (C) Small HiOP, (D) Big LoOP, (E) ME2 OP2, and (F) Big HiOP.

While CDBs of gold are higher and more stable than Bitcoin, there exist episodes of overlap that show Bitcoin can provide better diversification benefits for some investment styles and during certain market conditions. For example, there is evidence of overlap in most of the style portfolio CDBs toward the mid of 2018, where diversification benefit of Bitcoin either outperforms or equals gold.

In terms of industry portfolios, we observe similar patterns of CDBs for gold (Bitcoin), as presented in Figure 7. While all industry portfolios show the superior CDB of gold over Bitcoin, there are several periods where Bitcoin outperforms or equals the CDB of gold. This pattern is more pronounced for the energy and utility industry portfolios.

Time series plot of the conditional diversification benefits (CDB) of gold and Bitcoin for size and industry portfolios—equally weighted portfolios, 5% quantile: (A) Nondurable, (B) Durable, (C) Manufacturing, (D) Energy, (E) HiTech, (F) Telecomm, (G) Shops, (H) Health Care, (I) Utilities, and (J) Others.

Overall, gold is a better diversifier than Bitcoin as it provides higher CDBs for style and industry portfolios in extreme adverse market conditions when the investors need the diversification benefits most. The high volatility in Bitcoin prices is a primary reason for lower CDBs as compared with stable rates of gold during the sample period.

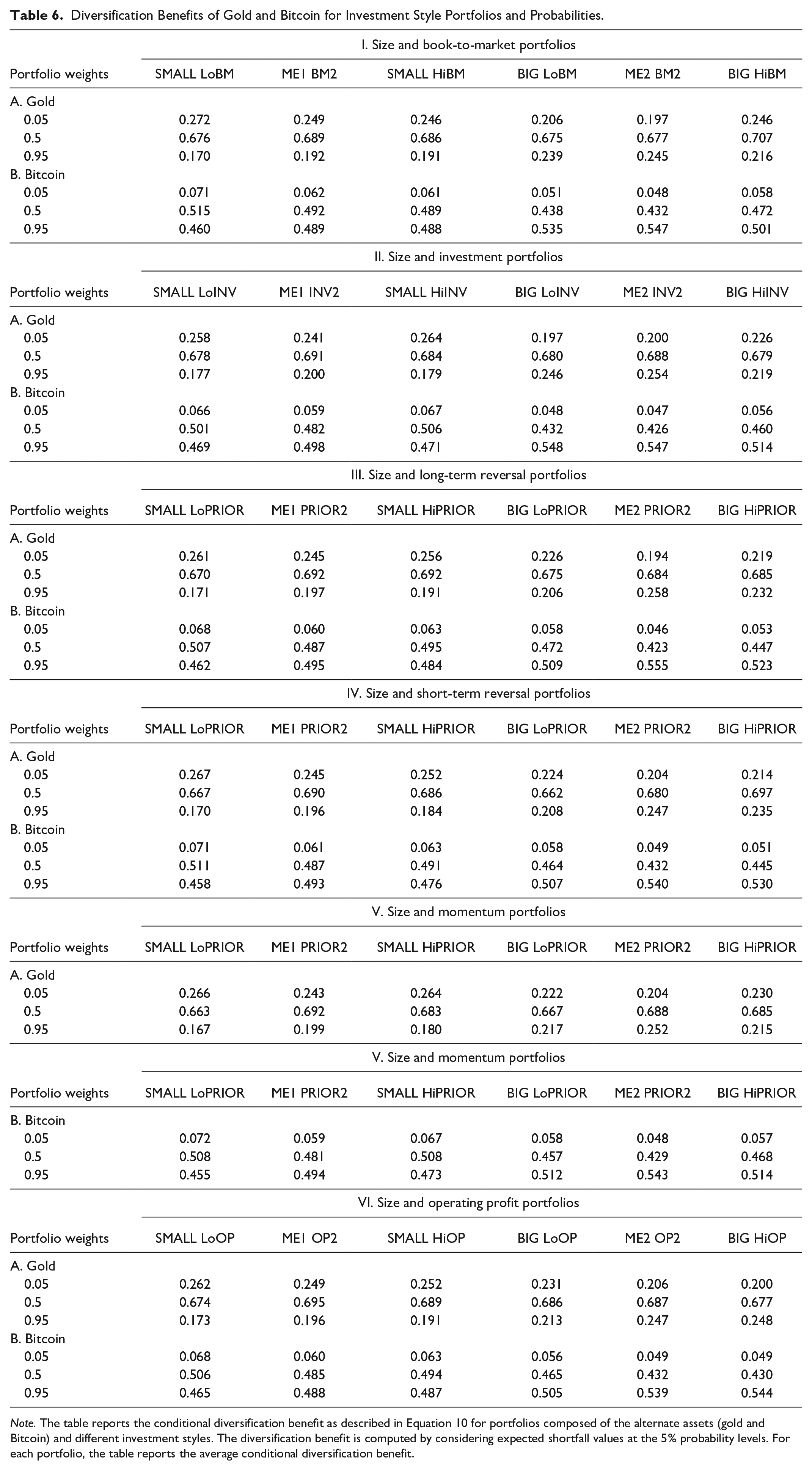

To illustrate further about diversification benefits, we estimate the mean CDBs of gold (Bitcoin) for style portfolios at 5% probability level. Table 6 presents the mean CDBs for different compositions of gold (Bitcoin) and style portfolios. Generally, gold outperforms Bitcoin for almost all the style portfolios when gold (Bitcoin) contributes 50% or less to portfolio weights. Whereas Bitcoin exhibits higher CDBs when gold (Bitcoin) adds a minimal portion of the portfolio (i.e., 5%). Across equally weighted style portfolios, gold offers the highest relative diversification benefits for small-cap style portfolios as compared with large-cap investments. However, Bitcoin offers the highest CDBs for large-cap portfolios in comparison to small-cap investments when it contributes a nominal portion of portfolio weight.

Diversification Benefits of Gold and Bitcoin for Investment Style Portfolios and Probabilities.

Note. The table reports the conditional diversification benefit as described in Equation 10 for portfolios composed of the alternate assets (gold and Bitcoin) and different investment styles. The diversification benefit is computed by considering expected shortfall values at the 5% probability levels. For each portfolio, the table reports the average conditional diversification benefit.

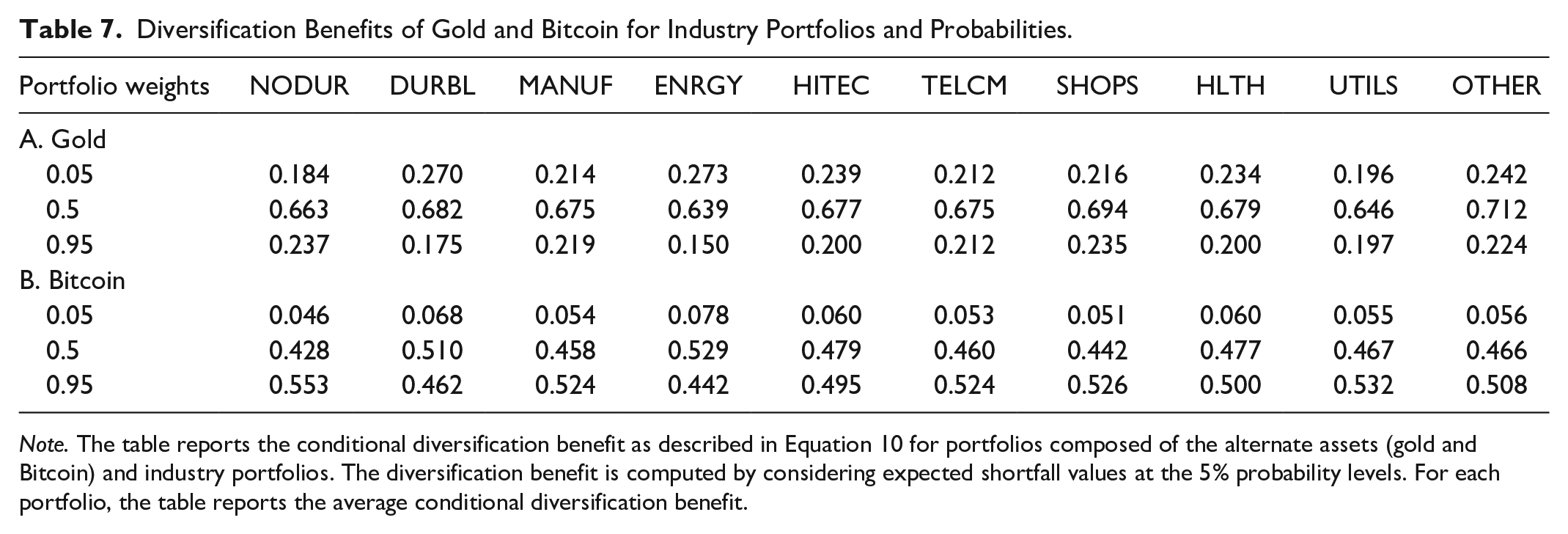

Furthermore, Table 7 presents the CDBs of gold and Bitcoin for differently weighted industry portfolios. Like style portfolios, mainly gold offers higher CDBs for industry portfolios as compared with Bitcoin. The highest CDBs are present for gold in equally weighted portfolios, and for Bitcoin, the highest CDBs exist in portfolios where it has a token presence. However, we observe different behavior of gold (Bitcoin) for cyclical and noncyclical industries. Gold exhibits relatively higher CDBs for cyclical industries such as consumer durable and shops as compared with noncyclical industries (i.e., nondurable and utilities). Instead, Bitcoin comparatively shows higher CDBs for noncyclical industries such as nondurables and utilities.

Diversification Benefits of Gold and Bitcoin for Industry Portfolios and Probabilities.

Note. The table reports the conditional diversification benefit as described in Equation 10 for portfolios composed of the alternate assets (gold and Bitcoin) and industry portfolios. The diversification benefit is computed by considering expected shortfall values at the 5% probability levels. For each portfolio, the table reports the average conditional diversification benefit.

Overall, the inclusion of gold in a style (industry) portfolios improves portfolio performance and offers protection against downside risk. Similarly, Bitcoin provides hedging and diversification opportunities to selected large-cap style portfolios and noncyclical industries. However, investors have to be mindful about the share of gold and Bitcoin in their portfolios, as only having an optimal weight of gold (Bitcoin) as indicated by the efficient frontier would provide the above-stated diversification benefits. For example, given the underlying nature of Bitcoin prices, having a higher weight of Bitcoin could lead to higher volatility of portfolio returns.

Conclusion

Economic agents, that is, traders, investors, and policymakers, consistently apply different risk management strategies to either mitigate or diversify the risk of their investments. With the growing concerns that financialization might hinder the potential safe-haven properties of commodities, such as gold, the growing popularity of cryptocurrencies as safe-haven assets warranted a comparison between the two. We employ Baur and McDermott’s (2010) approach to explore the safe-haven and hedging properties of gold and Bitcoin for a very diverse universe of style and industry portfolios. In addition, we estimate and evaluate the hedging effectiveness and conditional diversification benefits that gold and Bitcoin offer for equity investors.

Our findings show gold offers at least weak safe-haven potential for all style portfolios and most of the industry portfolios. These results are more pronounced in large-cap style portfolios and cyclical industries. Alternatively, Bitcoin is a weak safe-haven for some of the large-cap style and cyclical industry portfolios, excluding the health industry where it serves as a strong safe-haven. In the case of hedging potential, gold is, at minimum, a weak hedge for most of the style and several industry portfolios except utilities, energy, and telecom. Again, the hedging potential of gold is more pronounced for large-cap style and cyclical industry portfolios.

However, Bitcoin offers minimal hedging potential for large-cap style portfolios. However, Bitcoin’s hedging potential is more pronounced for noncyclical industries. This finding might be due to the comparatively stable and noncyclical features of Bitcoin, which makes it distinct from gold. For instance, the central bank’s decisions, which affect even noncyclical firms and financial markets, including gold, do not seem to influence Bitcoin’s liquidity and volatility (Baur, Dimpfl, & Kuck, 2018). Similarly, Bitcoin has a weak association with noncyclical macroeconomic factors relative to gold (Baek & Elbeck, 2015; Ciaian et al., 2016). Furthermore, Bitcoin exhibits a distinct price behavior (Chaim & Laurini, 2019; Ciaian et al., 2016) that makes it less reliant on the macro-financial factors which potentially affect noncyclical stocks and gold market simultaneously, turning it into a detached asset class. It may, therefore, be possible for Bitcoin to show more pronounced hedging potential for noncyclical industry stocks compared with the cyclical stocks.

Furthermore, we explore the hedging effectiveness and conditional diversification benefits of gold (Bitcoin) for style and industry portfolios. Our findings show that investor requires a smaller amount to hedge downside risk using Bitcoin as compared with gold. However, superior hedging effectiveness of gold makes it a better hedge than Bitcoin. Furthermore, diversification benefit results show higher benefits of including gold in a portfolio during market turmoil are emanates in equally weighted portfolios. Alternatively, a minimal presence of Bitcoin in style (industry) portfolio produces the highest diversification benefit. In totality, our findings provide evidence of superior hedging and safe potential of gold over Bitcoin in the U.S. equity market. However, we also find some style and industry portfolios, where Bitcoin shows relatively higher performance.

Our finding offers several implications for equity investors. First, from a style portfolio investor’s standpoint, our findings suggest that both gold and Bitcoin offer higher protection to risk-averse portfolio investors as compared with risk-seekers. Second, gold and Bitcoin offer relatively higher hedging and safe-haven potential for cyclical and noncyclical industry portfolios investors, respectively. Finally, our conditional diversification benefit analysis shows that investors have to carefully choose the weight of gold (Bitcoin) in their portfolio to optimize their portfolio performance.

Our findings are of interest to the above-mentioned economic agents, who now have empirical evidence that gold is still glittering, and even though Bitcoin has grown tremendously over the last decade, it still needs time to grow up to the ranks of gold. Finally, future studies may expand these findings by investigating different developed and developing countries’ equity markets and comparing other commodities and cryptocurrencies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.